Modeling long-range memory trading activity by stochastic differential equations

Abstract

We propose a model of fractal point process driven by the nonlinear stochastic differential equation. The model is adjusted to the empirical data of trading activity in financial markets. This reproduces the probability distribution function and power spectral density of trading activity observed in the stock markets. We present a simple stochastic relation between the trading activity and return, which enables us to reproduce long-range memory statistical properties of volatility by numerical calculations based on the proposed fractal point process.

pacs:

89.65.Gh; 02.50.Ey; 05.10.GgI Introduction

There are empirical evidences that the trading activity, the trading volume and the volatility of the financial markets are stochastic variables with the power-law probability distribution function (PDF) Mandelbrot ; Lux and the long-range correlations Engle ; Plerou ; Gabaix . Most of proposed models apply generic multiplicative noise responsible for the power-law probability distribution function (PDF), whereas the long-range memory aspect is not accounted in the widespread models BookDacorogna .The additive-multiplicative stochastic models of the financial mean-reverting processes provide rich spectrum of shapes for PDF, depending on the model parameters Anteneodo , however, do not describe the long-memory features. Empirical analysis confirms that the long-range correlations in volatility arise due to those of trading activity Plerou . On the other hand, trading activity is a financial variable dependant on the one stochastic process, i.e.interevent time between successive market trades. Therefore, it can be modeled as event flow of the stochastic point process.

Recently, we investigated analytically and numerically the properties of the stochastic multiplicative point processes, derived formula for the power spectrum GontisPhA ; KaulakysPRE and related the model with the multiplicative stochastic differential equations KaulakysPhA . Preliminary comparison of the model with the empirical data of the power spectrum and probability distribution of stock market trading activity Gontis2 stimulated us to work on the more detailed definition of the model. Here we present the stochastic model of the trading activity with the long-range correlations and investigate its connection to the stochastic modeling of the volatility. The proposed stochastic nonlinear differential equations reproduce the power spectrum and PDF of the trading activity in the financial markets, describe the stochastic interevent time as the fractal-based point process and can be applicable for modeling of the volatility with the long-range autocorrelation.

II Modeling fractal point process by the nonlinear stochastic differential equation

Trades in financial markets occur at discrete times and can be considered as identical point events. Such point process is stochastic and totaly defined by the stochastic interevent time . A fractal stochastic point process results, when at least two statistics exhibit the power-law scaling, indicating that represented phenomena contains clusters of events over all scales of time Lowen . The dimension of the fractal point process is a measure of the clustering of the events within the process and by the definition coincides with the exponent of the power spectral density of the flow of events.

We can model the trading activity in financial markets by the fractal point process as its empirical PDF and the power spectral density exhibit the power-law scaling Plerou ; Plerou2 . In this paper we consider the flow of trades in financial markets as Poisson process driven by the multiplicative stochastic equation. First of all we define the stochastic rate of event flow by continuous stochastic differential equation

| (1) |

where is a standard random Wiener process, denotes the standard deviation of the white noise, is a coefficient of the nonlinear damping and defines the power of noise multiplicativity. The diffusion of should be restricted at least from the side of high values. Therefore we introduce an additional term into the Eq. (1), which produces the exponential diffusion reversion in equation

| (2) |

where and are the power and value of the diffusion reversion, respectively. The associated Fokker-Plank equation with the zero flow gives the simple stationary PDF

| (3) |

with and . Eq. (2) describes continuous stochastic variable , defines the rate and, after the Ito transform of variable, results in stochastic differential equation

| (4) |

where and . Eq. (4) describes stochastic process with PDF

| (5) |

and power spectrum KaulakysPRE ; KaulakysPhA ; GontisPhA

| (6) |

Noteworthy, that in the proposed model only two parameters, and (or ), define exponents and of two power-law statistics, i.e., of PDF and of the power spectrum. Time scaling parameter in Eq. (4) can be omitted adjusting the time scale. Here we define the fractal point process driven by the stochastic differential equation (4) or equivalently by Eq. (2), i.e., we assume as slowly diffusing mean interevent time of Poisson process with the stochastic rate . This should produce the fractal point process with the statistical properties defined by Eqs. (5) and (6). Within this assumption the conditional probability of interevent time in the modulated Poisson point process with the stochastic rate is

| (7) |

Then the long time distribution of interevent time has the integral form

| (8) |

with defined from the normalization, . In the case of pure exponential diffusion reversion, , PDF (8) has a simple form

| (9) |

where denotes the modified Bessel function of the second kind. For more complicated structures of distribution expressed in terms of hypergeometric functions arise.

III Adjustment of the model to the empirical data

We will investigate how the proposed modulated Poisson stochastic point process can be adjusted to the empirical trading activity, defined as number of transactions in the selected time window . Stochastic variable denotes the number of events per unit time interval. One has to integrate the stochastic signal Eq. (4) in the time interval to get the number of events in the selected time window. In this paper we denote the integrated number of events as

| (10) |

and call it the trading activity in the case of the financial market.

Detrended fluctuation analysis Plerou2 is one of the methods to analyze the second order statistics related to the autocorrelation of trading activity. The exponents of the detrended fluctuation analysis obtained by fits for each of the 1000 US stocks show a relatively narrow spread of around the mean value Plerou2 . We use relation between the exponents of detrended fluctuation analysis and the exponents of the power spectrum Beran and in this way define the empirical value of the exponent for the power spectral density .

Our analysis of the Lithuanian stock exchange data confirmed that the power spectrum of trading activity is the same for various liquid stocks even for the emerging markets Gontis2 . The histogram of exponents obtained by fits to the cumulative distributions of trading activites of 1000 US stocks Plerou2 gives the value of exponent describing the power-law behavior of the trading activity. Empirical values of and confirm that the time series of the trading activity in real markets are fractal with the power law statistics. Time series generated by stochastic process (4) are fractal in the same sense.

Nevertheless, we face serious complications trying to adjust model parameters to the empirical data of the financial markets. For the pure multiplicative model, when or , we have to take to get and to get , i.e. it is impossible to reproduce the empirical PDF and power spectrum with the same relaxation parameter and exponent of multiplicativity . We have proposed possible solution of this problem in our previous publications GontisPhA ; Gontis2 deriving PDF for the trading activity

| (11) |

When this yields exactly the required value of and for .

Nevertheless, we cannot accept this as the sufficiently accurate model of the trading activity since the empirical power law distribution is achieved only for very high values of the trading activity. Probably this reveals the mechanism how the power law distribution converges to normal distribution through the growing values of the exponent, but empirically observed power law distribution in wide area of values cannot be reproduced. Let us notice here that the desirable power law distribution of the trading activity with the exponent may be generated by the model (4) with and . Moreover, only the smallest values of or high values of contribute to the power spectral density of trading activity KaulakysPhA . This suggests us to combine the stochastic process with two values of : (i) for the main area of and diffusion and (ii) for the lowest values of or highest values of . Therefore, we introduce a new stochastic differential equation for combining two powers of the multiplicative noise,

| (12) |

where a new parameter defines crossover between two areas of diffusion. The corresponding iterative equation for in such a case is

| (13) |

where denotes uncorrelated normally distributed random variable with the zero expectation and unit variance.

Eqs. (12) and (13) define related

stochastic variables and , respectively, and they should

reproduce the long-range statistical properties of the trading

activity and of waiting time in the financial markets. We verify

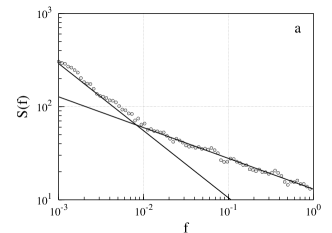

this by the numerical calculations. In figure 1 we

present the power spectral density calculated for the equivalent

processes (12) and (13) (see

GontisPhA for details of calculations). This approach

reveals the structure of the power spectral density in wide range

of frequencies and shows that the model exhibits not one but

rather two separate power laws with the exponents

and . From many numerical calculations performed

with the multiplicative point processes we can conclude that

combination of two power laws of spectral density arise only when

the multiplicative noise is a crossover of two power laws as in

Eqs. (12) and (13). We will show in

the next section that this may serve as an explanation of two

exponents of the power spectrum in the empirical data of

volatility for S&P 500 companies Liu .

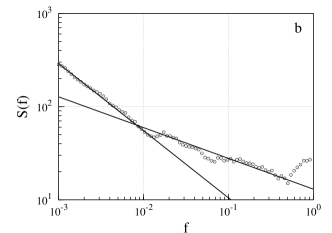

Empirical data of the trading activity statistics should be modeled by the integrated flow of events defined in the time interval . In figure 2 we demonstrate the probability distribution functions and its cumulative form calculated from the histogram of generated by Eq. (13) with the selected time interval . This illustrates that the model distribution of the integrated signal has the power-law form with the same exponent as observed in empirical data Plerou ; Gabaix .

The power spectrum of the trading activity has the same exponent as power spectrum of in the low frequency area for all values of .

The same numerical results can be reproduced by continuous stochastic differential equation (12) or iteration equation (13). One can consider the discrete iterative equation for the interevent time (13) as a method to solve numerically continuous equation

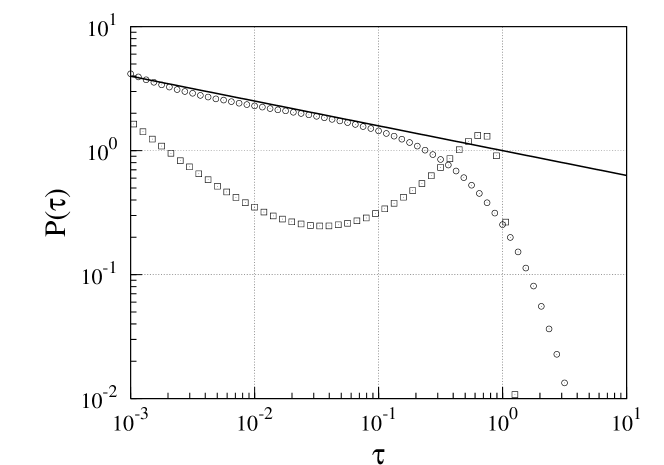

We can conclude that the long-range memory properties of the trading activity in the financial markets as well as the PDF can be modeled by the continuous stochastic differential equation (12). In this model the exponents of the power spectral density, , and of PDF, , are defined by one parameter . We consider the continuous equation of the mean interevent time as a model of slowly varying stochastic rate in the modulated Poisson process (7). In figure 3 we demonstrate the probability distribution functions calculated from the histogram of generated by Eq. (7) with the diffusing mean interevent time calculated from Eq. (14).

Numerical results show good qualitative agreement with the empirical data of interevent time probability distribution measured from few years series of U.S. stock data Ivanov . This enables us to conclude that the proposed stochastic model captures the main statistical properties including PDF and the long-range correlation of the trading activity in the financial markets. Furthermore, in the next section we will show that this may serve as a background statistical model responsible for the statistics of return volatility in widely accepted geometric Brownian motion (GBM) of the financial asset prices.

IV Modeling long-range memory volatility

The basic quantities studied for the individual stocks are price and return

| (15) |

Let us express return over a time interval through the subsequent changes due to the trades in the time interval ,

| (16) |

We denote the variance of calculated over the time interval as . If are mutually independent one can apply the central limit theorem to sum (16). This implies that for the fixed variance return is a normally distributed random variable with the variance

| (17) |

where is the normally distributed random variable with the zero expectation and unit variance.

Empirical test of conditional probability Plerou confirms its Gaussian form, and the unconditional distribution is a power-law with the cumulative exponent . This implies that the power-law tails of returns are largely due to those of . Here we refer to the theory of price diffusion as a mechanistic random process Farmer ; Farmer2 . For this idealized model the short term price diffusion depends on the limit order removal and this way is related to the market order flow. Furthermore, the empirical analysis confirms that the volatility calculated for the fixed number of transactions has the long memory properties as well and it is correlated with real time volatility Farmer3 . We accumulate all these results into the assumption that standard deviation may be proportional to the square root of the trading activity, i.e., . This enables us to propose a simple model of return

| (18) |

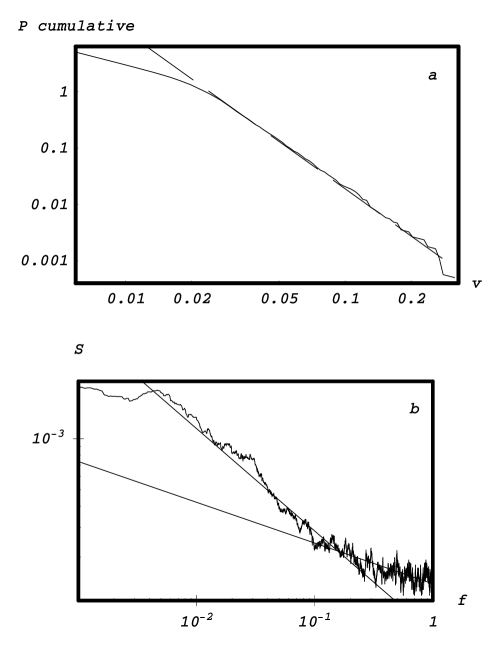

and related model of volatility based on the proposed model of trading activity (12). We generate series of trade flow numerically solving Eq. (12) with variable steps of time and calculate the trading activity in subsequent time intervals as . This enables us to generate series of return , of volatility and of the averaged volatility .

In figure 4 we demonstrate cumulative distribution of and the power spectral density of calculated from FFT. We see that proposed model enables us to catch up the main features of the volatility: the power law distribution with exponent and power spectral density with two exponents and . This is in a good agreement with the empirical data Liu ; Farmer3 .

V Conclusions

Starting from the concept of the fractal point processes Lowen we proposed process driven by the nonlinear stochastic differential equation and based on the earlier introduced stochastic point process model KaulakysPRE ; GontisPhA ; KaulakysPhA ; Gontis2 . This may serve as a possible model of the flow of points or events in the physical, biological and social systems when their statistics exhibit power-law scaling indicating that the represented phenomena contains clusters of events over all scales. First of all, we analyze the statistical properties of trading activity and waiting time in financial markets by the proposed Poisson process with the stochastic rate defined as a stand-alone stochastic variable. We consider the stochastic rate as continuous one and model it by the stochastic differential equation, exhibiting long-range memory properties KaulakysPhA . Further we propose a new form of the stochastic differential equation combining two powers of multiplicative noise: one responsible for the probability distribution function and another responsible for the power spectral density. The proposed new form of the continuous stochastic differential equation enabled us to reproduce the main statistical properties of the trading activity and waiting time, observable in the financial markets. In the new model the power spectral density with two different scaling exponents arise. This is in agreement with the empirical power spectrum of volatility and implies that the market behavior may be dependant on the level of activity. One can observe at least two stages in market behavior: calm and excited. Finally, we propose a very simple stochastic relation between trading activity and return to reproduce the statistical properties of volatility. This enabled us to model empirical distribution and long-range memory of volatility.

Acknowledgment

This work was supported by the Lithuanian State and Studies Foundation. The authors thank Dr. M. Alaburda for kind assistance preparing illustrations.

References

- (1) Mandelbrot B B, J.Business 36, 394 (1963).

- (2) Lux T, Appl.Fin. Econ. 6, 463 (1996).

- (3) Engle R. F. and Patton A. J., Quant. Finance 1, 237 (2001).

- (4) Plerou V, Gopikrishnan P, Gabaix X, Amaral L A N and Stanley H E, 2001 Quant. Finance 1 262

- (5) Gabaix X, Gopikrishnan P, Plerou V, Stanley H E, 2003 Nature 423 267

- (6) Dacorogna M M, Gencay R, Muller U A, Olsen R B and Pictet O V, 2001 An Introduction to High-Frequency Finance (Academic Press, San Diego)

- (7) Anteneodo C and Riera R, 2005 Phys. Rev. E 72 026106

- (8) Kaulakys B, Gontis V and Alaburda M, 2005 Phys. Rev. E 71 051105

- (9) Gontis V and Kaulakys B, 2004 Physica A 343 505

- (10) Kaulakys B, Ruseckas J, Gontis V and Alaburda M, 2006 Physica A 365 217

- (11) Gontis V and Kaulakys B, 2004 Physica A 344 128

- (12) Lowen S B, Teich M C, 2005 Fractal-Based Point Processes (Wiley, ISBN: 0-471-38376-7)

- (13) Plerou V E, Gopikrishnan P, Amaral L, Gabaix X and Stanley E, 2000 Phy. Rev. E 62 R3023

- (14) Beran J, 1994 Statistics for Long-Memory Processes (Chapman and Hall, NY)

- (15) Liu Y, Gopikrishnan P, Cizeau P, Meyer M, Peng Ch and Stanley H E, 1999 Phys. Rev. E 60 1390

- (16) Ivanov P, Yuen A, Podobnik B, Lee Y, 2004 Phys. Rev. E 69 056107

- (17) Daniels M, Farmer D, Gillemot L, Iori G and Smith E, 2003 Phys. Rev. Lett. 90 108102

- (18) Farmer D, Gillemot L, Lillo F, Szabolcs M and Sen A, 2004 Quantative Finance 4 383

- (19) Gillemot L, Farmer J D, Lillo F, Santa Fe Institute Working Paper 05-12-041