Long-range dependence in Interest Rates and Monetary Policy

Abstract

This paper studies the dynamics of Brazilian interest rates for short-term maturities. The paper employs developed techniques in the econophysics literature and tests for long-range dependence in the term structure of these interest rates for the last decade. Empirical results suggest that the degree of long-range dependence has changed over time due to changes in monetary policy, specially in the short-end of the term structure of interest rates. Therefore, we show that it is possible to identify monetary arrangements using these techniques from econophysics.

I Introduction

The analysis of persistence in interest rates is a fundamental question in macroeconomics and finance. In macroeconomics, since monetary policy is implemented through the setting of short-term interest, the term structure of interest rates carries information regarding expectations of future movements in short-term interest rates. However, very little research has been conducted to study changes in the dynamics of persistence in interest rates.

This paper presents a contribution to the literature by studying whether changes in monetary policy stance, namely the implementation of an inflation targeting regime and adoption of a floating exchange rate regime, produce a change in the persistence of interest rates. We measure persistence in this paper employing two developed techniques in econophysics, which are the detrended fluctuation analysis (DFA) [Moreira et al, 2004; Peng et al, 2004] and Generalized Hurst exponents (GHE) [Barabási and Vicsek (1991)]. We show that changes in monetary policy produce a a substantial change in persistence of interest rates, specially for short-term interest rates.

This paper proceed as follows. In section 2 a brief review of literature is presented. In section 3 the approaches used to evaluate the Hurst’s exponent are presented. In section 4, the data used in this work is described. In section 5, empirical results are presented. Finally, section 6 concludes the paper.

II Brief Literature Review

Recent research has studied whether long-range dependence in asset returns and volatility changes over time, and has provided evidence of time-varying long-range dependence (Cajueiro and Tabak, 2004,2005). Nonetheless, while the presence of long-range dependence in asset returns and returns volatility seems to be an stylized fact111For details, see Mandelbrot (1971) and Willinger et al. (1999)., only few papers have provided empirical evidence of long-range dependence in interest rates [Backus and Zin (1993), Tsay (2000), Barkoulas and Baum (1998), McCarthy et al. (2004), Sun and Phillips (2004), Duan and Jacobs (1996, 2001), Cajueiro and Tabak (2006a, 2006b)].

This paper contributes to the literature by studying changes in long-range dependence parameters in interest rates time series. We focus on the Brazilian economy due to recent changes that occurred in monetary policy, with the adoption of an inflation targeting regime and a floating exchange rate regime.

III Measures of Long-Range Dependence

There are several methods that may be used to take into account the long range dependence phenomena222A survey of these methods may be found in Taqqu et al. (1995) and Montanary et al. (1999). See also Hurst (1951), Lo (1991) and Willinger et al. (1999).. However, in spite of the existence of several methods, the task of calculation the Hurst exponent is not straightforward and the methods sometimes present incompatible estimations of the long range dependence parameter.

In this paper we follow two different approaches. The method introduced by Barabási and Vicsek (1991) and used recently by Di Matteo et al. (2005b) to measure the degree of market development of several financial markets. According to Di Matteo et al. (2005b), it combines sensitivity to any type of dependence in the data and simplicity. Moreover, since it does not deal with and functions, it is less sensitive to outliers than the popular R/S statistics. And, also, the detrended fluctuation analysis (DFA) which was developed independently in (Moreira et al, 2004) and (Peng et al, 2004) and provides an alternative for the determination of the Hurst exponent.

III.1 Generalized Hurst exponent

Let be the integrated time series of logarithm returns, i.e., . The generalized Hurst exponent is a generalization of the approach proposed by Hurst. Barabási and Vicsek (1991) suggest analyzing the q-order moments of the distribution of increments, which seems to be a good characterization of the statistical evolution of a stochastic variable ,

| (1) |

where the time-interval can vary333For , the is proportional to the autocorrelation function .. The generalized Hurst exponent can be defined from the scaling behavior of , which can be assumed to follow the relation

| (2) |

III.2 Detrended fluctuation analysis

Let be the integrated time series of logarithm returns, i.e., . So, one considers the -neighborhood around each point Y(t) of the time series. The local trend in each -size box is approximated by a polynomial444This polinomial of order is usually a first order polinomial, i.e., a straight line where the parameters are determined by a least square fitting. of order , namely .

Then, one evaluates the local roughness, namely

| (3) |

Moreira et al. (1994) showed that

| (4) |

IV Data

The data considered here are interest rate swaps maturing on 1, 3, 6 and 12 months’ time, which are the maturities available for a “long time” span (more than 10 years of data). In these contracts, a party pays a fixed rate over an agreed principal and receives a floating rate over the same principal, the reverse occurring with his or her counterpart. There are no intermediate cash-flows, with the contracts being settled on maturity. The floating rate is the overnight CDI rate (interbank deposits), which tracks very closely the average rate in the market for overnight reserves at the central bank. The fixed rate, negotiated by the parties, is the one used on this paper.

These contracts have been traded over-the-counter in Brazil since the early 90’s, and have to be registered either on Bolsa de Mercadorias e de Futuros - BMF (a futures exchange) or on Central de Títulos Privados - CETIP (a custodian).

We use data on interest rates swaps due to the lack of good quality data on government bond indices for different maturities. Nonetheless, these interest rates are used as benchmarks in the Brazilian financial market.

The data is sampled daily, beginning on January 2, 1995 and ending on May 30, 2006. The full sample has 2828 observations, collected from the Bloomberg system.

V Long-Range Dependence in the Term Structure of Brazilian Interest Rates

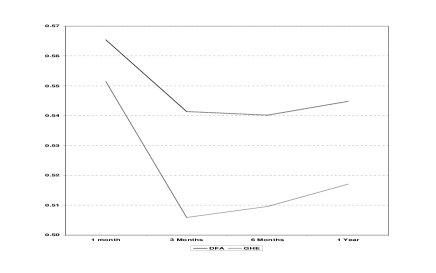

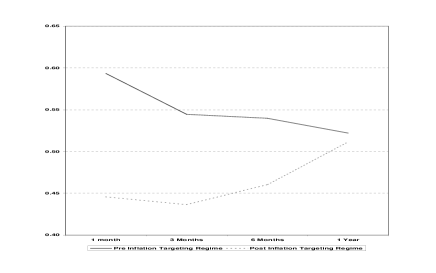

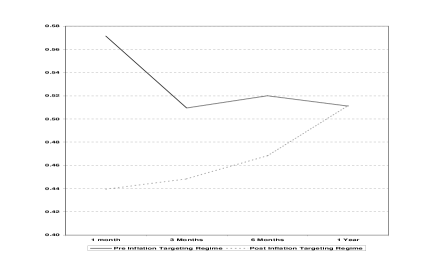

This section presents results for testing for long-range dependence in interest rates for different maturities. Table 1 shows Hurst exponents estimated using both DFA and GHE methods. We estimate these Hurst exponents using the entire sample and also constructing two sub-samples. The differences between monetary policy regimes are striking, with Hurst exponents above 0.5 for all maturities in the period before the implementation of the inflation targeting regime and below 0.5 for maturities up to 6 months after the implementation of this regime. Panel D presents the differences in Hurst exponents, which decrease monotonically with maturity, suggesting that very little changed in the dynamics of the 1 year maturity interest rate. However, changes in 1-month interest rates were substantial, and robust to the methodology employed to estimate Hurst exponents.

Figure 1 presents Hurst exponents for the entire sample, using both the DFA and GHE methodology. These Hurst exponents are decreasing but the difference in Hurst exponents is small. However when we compare Hurst exponents across monetary regimes the pattern changes dramatically. Figures 2 and 3 present Hurst exponents for two different monetary regimes, using the DFA and GHE methods.

Two main conclusions emerge from these empirical results. Hurst exponents show a substantial break in the dynamics of persistence in Brazilian interest rates, specially for short-term maturities. Second, the period before the implementation of the Inflation Targeting Regime is characterized by a downward slope in the Term Structure of Hurst exponents, while the period after the implementation with an upward slope. 1 year maturity interest rates do not present any evidence of a structural break, which suggests that studying the term structure of interest rates is worthwhile.

VI Conclusions

In this paper we have shown empirical evidence of long-range dependence in the Brazilian term structure of interest rates. We show that Hurst exponents change substantially with the implementation of the Inflation Targeting Regime in 1999, reducing substantially interest rates persistence afterwards.

The economic intuition for the empirical results is that the previous monetary policy cycles that occurred within the period before the implementation of the Inflation Targeting regime have had a substantial change. This is true because within an Inflation Targeting regime the exchange rate is floating and therefore, the exchange rate may absorb, at least partially, external shocks. When exchange rates are fixed external shocks must be absorbed by changes in domestic interest rates, and therefore, one should expect interest rates to show more persistence.

This phenomenon is particularly true in our study, because structural changes in interest rates were more pronounced in short-term interest rates, with very little changes in 1 year maturity interest rates (considered long-term interest rates in Brazil).

Our results show that methods derived from econophysics may be able to help explain dynamics of important macroeconomic and financial variables such as interest rates. Further research could focus on a variety of countries that have adopted different monetary regimes and studying changes in persistence across regimes.

VII Acknowledgements

The authors thank participants of the AFPA5 2006 for helpful suggestions. Benjamin M. Tabak gratefully acknowledges financial support from CNPQ foundation. The opinions expressed in this paper are those of the authors and do not necessarily reflect those of the Banco Central do Brasil.

References

- (1) Backus,D, Zin, S. Long memory inflation uncertainty: evidence of term structure of interest rate. Journal of Money, Credit and Banking, 25, p. 687-700, 1993.

- (2) Barabási, A. L. and Vicsek, T. Multifractality of self-affine fractals. Physical Review A, 44, p. 2730, (1991).

- (3) Barkoulas, J. T. and Baum, C. F. Fractional dynamics in Japanese financial time series. Pacific-Basin Finance Journal, 6, p. 115 124, 1998.

- (4) Cajueiro, D. O. and Tabak, B. M. The Hurst’s exponent over time: testing the assertion that emerging markets are becoming more efficient. Physica A, 336, 521 (2004).

- (5) Cajueiro, D. O. and Tabak, B. M. Testing for time-varying long-range dependence in volatility for emerging markets. Physica A, 346, 577-588 (2005).

- (6) Cajueiro, D. O. and Tabak, B. M. Time-varying long-range dependence in US interest rates. Forthcoming in Chaos, Solitons and Fractals, (2006a).

- (7) Cajueiro, D. O. and Tabak, B. M. Long-range dependence and multifractality in the term structure of LIBOR interest rates. Forthcoming in Physica A, (2006b).

- (8) Di Matteo, T., Aste, T. and Dacorogna, M. M. Long-term memories of developed and emerging markets: Using the scaling analysis to characterize their stage of development. Journal of Banking and Finance, 29, 827–851, (2005b).

- (9) Duan. J.-C., Jacobs, K.A simple long-memory equilibrium interest rate model. Economics Letters, 53, 317-321, (1996).

- (10) Duan. J.-C., Jacobs, K. Short and long memory in equilibrium interest rate dynamics. CIRANO, s-22, (2001).

- (11) Hurst, E. Long term storage capacity of reservoirs. Transactions on American Society of Civil Engineering, 116, 770 (1951).

- (12) Lo, A. W. Long term memory in stock market prices. Econometrica, 59, 1279 (1991).

- (13) Mandelbrot, B. When can price be arbitraged effciently? A limit to the validity of the random walk and Martingale models. Review of Economics and Statistics, 53, 225 (1971).

- (14) McCarthy, J., DiSario, R., Saraoglu, H., Li, H. Tests of long-range dependence in interest rates using wavelets. The Quarterly Review of Economics and Finance, 44, 180-189 (2004).

- (15) Montanari, A., Taqqu, M. S. and Teverovsky, V. Estimating long-range dependence in the presence of periodicity. Mathematical and Computer Modelling, 29, 217-228, (1999).

- (16) Moreira J. G., Silva, J. K. L. and Kamphorst, S. O. On the fractal dimension of self-affine profiles. Journal of Physics A, 27, 8079 (1994).

- (17) Peng, C. K., Buldyrev, S. V., Havlin, S., Simons, M. Stanley, H. E. and Goldberger, A. L. Mosaic organization of dna nucleotides. Physics Review E, 49, 1685 (1994).

- (18) Sun, Y. and Phillips, P. C. B. Understanding the Fisher equation. Journal of Applied Econometrics, 19, p. 869-886, 2004.

- (19) Taqqu, M. S., Teverovsky, V. and Willinger, W. Estimators for long-range dependence. Fractals, 3, 785-798, (1995).

- (20) Tsay, W. J. Long memory story of the real interest rate. Economics Letters, 67 , p. 325 330, (2000).

- (21) Willinger, W., Taqqu, M. S. and Teverovsky, V. Stock market prices and long-range dependence. Finance and Stochastics, 3, 1 (1999).

| 1 month | 3 Months | 6 Months | 1 Year | |

|---|---|---|---|---|

| Panel A: Full Sample | ||||

| DFA | 0.565 | 0.541 | 0.540 | 0.545 |

| GHE | 0.551 | 0.506 | 0.510 | 0.517 |

| Panel B: Pre Inflation Targeting Regime | ||||

| DFA | 0.593 | 0.544 | 0.540 | 0.522 |

| GHE | 0.571 | 0.509 | 0.520 | 0.511 |

| Panel C: Post Inflation Targeting Regime | ||||

| DFA | 0.446 | 0.436 | 0.460 | 0.511 |

| GHE | 0.440 | 0.448 | 0.468 | 0.511 |

| Panel D: Difference in Hurst Exponents () | ||||

| DFA | 0.148 | 0.108 | 0.079 | 0.011 |

| GHE | 0.132 | 0.061 | 0.052 | 0.000 |