The uniqueness of the profits distribution function

in the middle scale region

Abstract

We report the proof that the expression of extended Gibrat’s law is unique and the probability distribution function (pdf) is also uniquely derived from the law of detailed balance and the extended Gibrat’s law. In the proof, two approximations are employed that the pdf of growth rate is described as tent-shaped exponential functions and that the value of the origin of growth rate is constant. These approximations are confirmed in profits data of Japanese companies 2003 and 2004. The resultant profits pdf fits with the empirical data with high accuracy. This guarantees the validity of the approximations.

PACS code : 04.60.Nc

Keywords : Econophysics; Pareto law; Gibrat law; Detailed balance

1 Introduction

In the large scale region of income, profits, assets, sales and etc (), the cumulative probability distribution function (pdf) obeys a power-law for which is larger than a certain threshold :

| (1) |

This power-law and the exponent are called Pareto’s law and Pareto index, respectively [1]. The power-law distribution is well investigated by using various models in econophysics [2].

Recently, Fujiwara et al. [3] find that Pareto’s law can be derived kinematically from the law of detailed balance and Gibrat’s law [4] which are also observed in the large scale region . In the proof, they assume no model and only use these two laws in empirical data.

The detailed balance is time-reversal symmetry ():

| (2) |

Here and are two successive incomes, profits, assets, sales, etc. and is the joint pdf. Gibrat’s law states that the conditional pdf of growth rate is independent of the initial value :

| (3) |

Here growth rate is defined as the ratio and is defined by using the pdf and the joint pdf as .

In Ref. [5], the kinematics is extended to dynamics by analyzing data on the assessed value of land in Japan. In the non-equilibrium system we propose an extension of the detailed balance (detailed quasi-balance) as follows

| (4) |

From Gibrat’s law (3) and the detailed quasi-balance (4), we derive Pareto’s law with annually varying Pareto index. The parameters , are related to the change of Pareto index and the relation is confirmed in the empirical data nicely.

These findings are important for the progress of econophysics. Above derivations are, however, valid only in the large scale region where Gibrat’s law (3) holds. It is well known that Pareto’s law is not observed below the threshold [4, 6]. The reason is thought to be the breakdown of Gibrat’s law [3]. The breakdown of Gibrat’s law in empirical data is reported by Stanley’s group [7]. Takayasu et al. [8] and Aoyama et al. [9] also report that Gibrat’s law does not hold in the middle scale region by using data of Japanese companies.

In Ref. [10], Gibrat’s law is extended in the middle scale region by employing profits data of Japanese companies in 2002 and 2003. We approximate the conditional pdf of profits growth rate as so-called tent-shaped exponential functions

| (5) | |||||

| (6) |

By measuring we have assumed the dependence to be

| (7) |

and have estimated the parameters as [11]

| (8) | |||||

| (9) | |||||

| (10) |

From the detailed balance (2) and extended Gibrat’s law (7) – (10), we have derived the pdf in the large and middle scale region uniformly as follows

| (11) |

where . This is confirmed in the empirical data.

In this study, we prove that the dependence of (7) with is unique if the pdf of growth rate is approximated by tent-shaped exponential functions (5), (6). This means, consequently, that the pdf in the large and middle scale region (11) is also unique if the dependence of is negligible. We confirm these approximations in profits data of Japanese companies 2003 and 2004 [12] and show that the pdf (11) fits with empirical data nicely by the refined data analysis.

2 Growth rate distributions of profits in the database

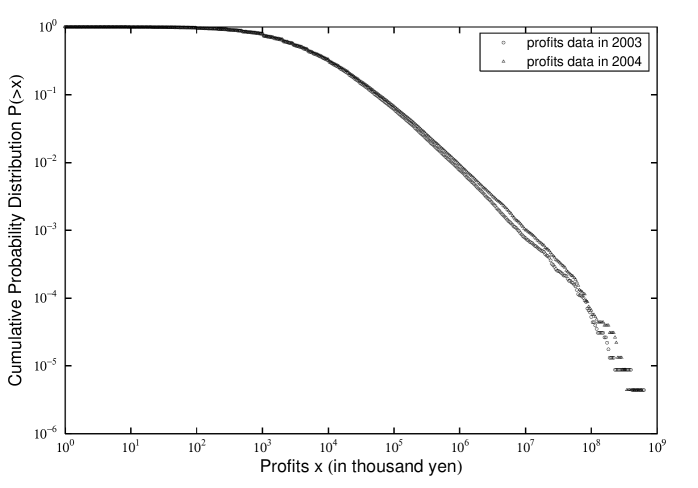

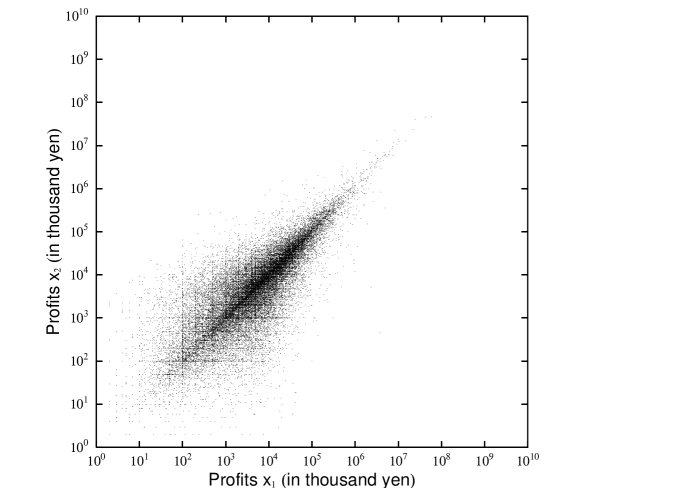

In the database, Pareto’s law (1) is observed in the large scale region whereas it fails in the middle one (Fig. 1). At the same time, it is confirmed that the detailed balance (2) holds not only in the large scale region and but also in all regions and (Fig. 2). 222 The scatter plot in Fig. 2 is different from one in Ref [10]. The reason is that the identification of profits in 2002 and 2003 in Ref. [10] was partly failed. As a result, the pdfs of profits growth rate are slightly different from those in this paper. The conclusion in Ref. [10] is, however, not changed.

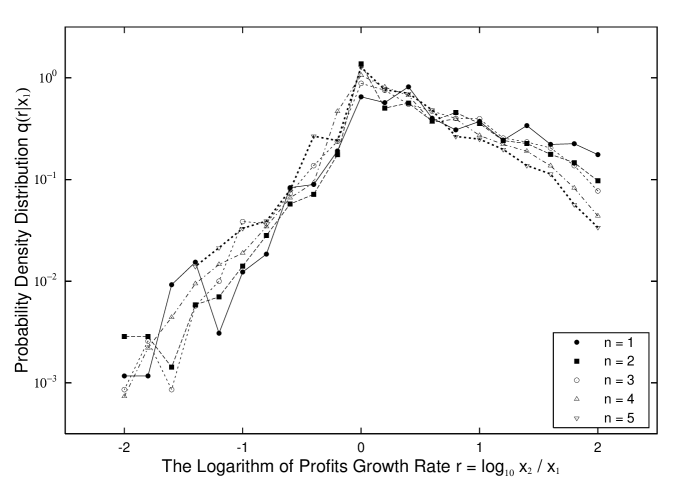

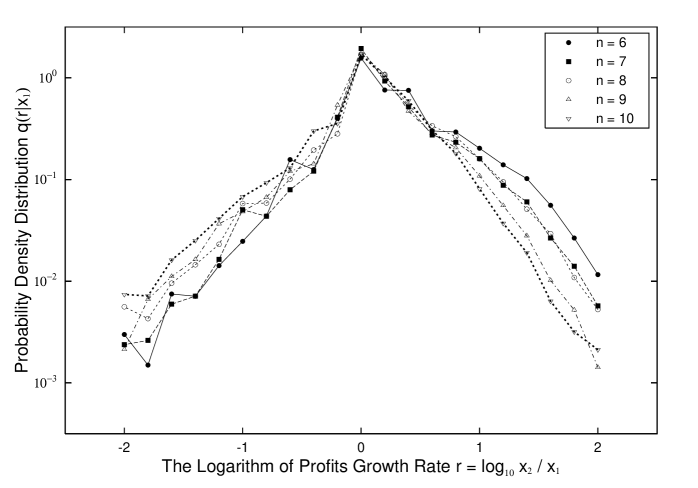

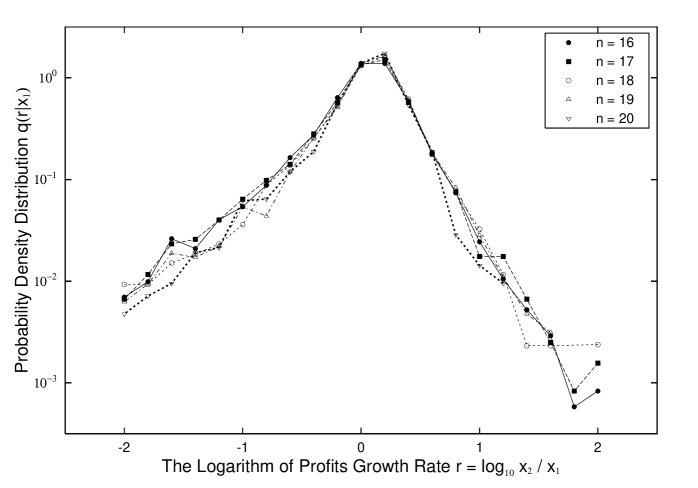

The breakdown of Pareto’s law is thought to be caused by the breakdown of Gibrat’s law in the middle scale region. We examine, therefore, the pdf of profits growth rate in the database. In the analysis, we divide the range of into logarithmically equal bins as thousand yen with . In Fig. 3 – 6, the probability densities for are expressed in the case of , , and , respectively. The number of the companies in Fig. 3 – 6 is “”, “”, “” and “”, respectively. Here we use the log profits growth rate . The probability density for defined by is related to that for by

| (12) |

3 The uniqueness of extended Gibrat’s law

In this section, we show that the dependence of (7) is unique under approximations (5), (6) ((13), (14)).

Due to the relation of under the change of variables from to , these two joint pdfs are related to each other . By the use of this relation, the detailed balance (2) is rewritten in terms of as follows:

| (15) |

Substituting the joint pdf for the conditional probability , the detailed balance is expressed as

| (16) |

Under approximations (5) and (6), the detailed balance is reduced to

| (17) |

for . By using the notation , the detailed balance becomes

| (18) |

By expanding Eq. (18) around , the following differential equation is obtained

| (19) |

where denotes . The same differential equation is obtained for . The solution is given by

| (20) |

where and .

In order to make the solution (20) around satisfies Eq. (18), the following equation must be valid for all :

| (21) |

The derivative of Eq. (21) with respect to is

| (22) |

By expanding Eq. (22) around , following differential equations are obtained

| (23) | |||

| (24) |

The solutions are given by

| (25) | |||||

| (26) |

To make these solutions satisfy Eq. (21), the coefficients must be and . Finally we conclude that is uniquely expressed as Eq. (7) with .

4 The profits distribution and the data fitting

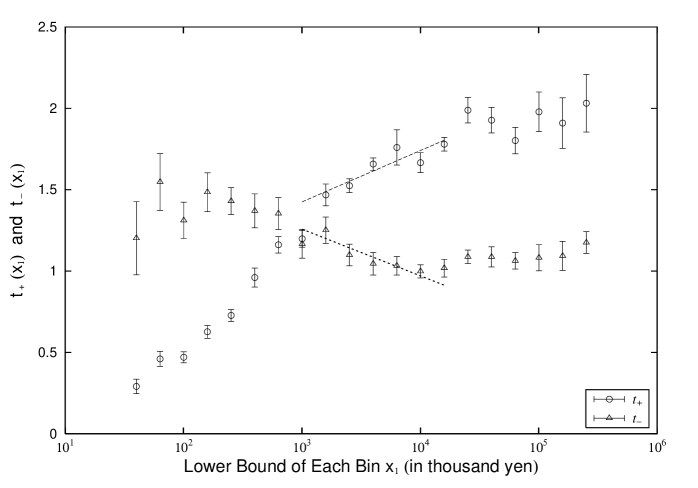

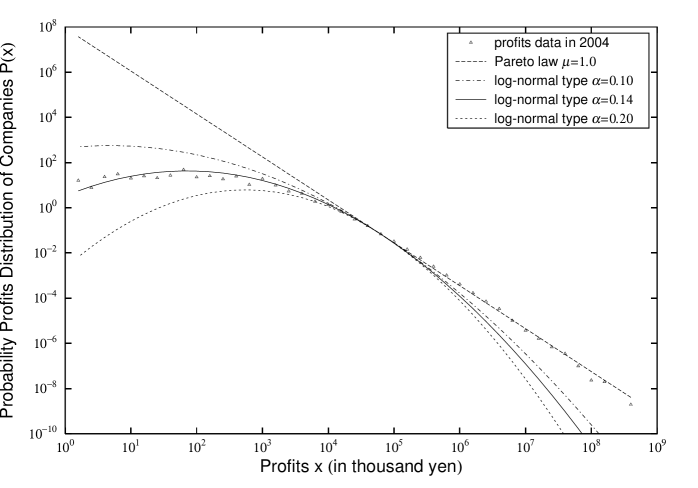

In Fig. 7, hardly responds to for . This means that Gibrat’s law holds in the large profits region. On the other hand, linearly increases and linearly decreases symmetrically with for . The parameters are estimated as Eq. (8) and (9) with ( and thousand yen. Because the dependence of () is negligible in this region, the profits pdf is reduced to Eq. (11). We observe that this pdf fits with the empirical data nicely in Fig. 8.

5 Conclusion

In this paper, we have shown the proof that the expression of extended Gibrat’s law is unique and the pdf in the large and middle scale region is also uniquely derived from the law of detailed balance and the extended Gibrat’s law. In the proof, we have employed two approximations that the pdf of growth rate is described as tent-shaped exponential functions and that the value of the origin of growth rate is constant. These approximations have been confirmed in profits data of Japanese companies 2003 and 2004. The resultant pdf of profits has fitted with the empirical data with high accuracy. This guarantees the validity of the approximations.

For profits data we have used, the distribution is power in the large scale region and log-normal type in the middle one. This does not claim that all the distributions in the middle scale region are log-normal types. For instance, the pdf of personal income growth rate or sales of company is different from tent-shaped exponential functions [3]. In this case, the extended Gibrat’s law takes a different form. In addition, we describe no pdf in the small scale region [13]. Because the dependence of in this region is not negligible (Fig. 3).

Against these restrictions, the proof and the method in this paper is significant for the investigation of distributions in the middle and small scale region. We will report the study about these issues in the near future.

Acknowledgments

The author is grateful to the Yukawa Institute for Theoretical Physics at Kyoto University, where this work was initiated during the YITP-W-05-07 on “Econophysics II – Physics-based approach to Economic and Social phenomena –”, and especially to Professor H. Aoyama for the critical question about the author’s presentation. Thanks are also due to Dr. Y. Fujiwara for a lot of useful discussions and comments.

References

- [1] V. Pareto, Cours d’Economique Politique, Macmillan, London, 1897.

- [2] R.N. Mategna, H.E. Stanley, An Introduction to Econophysics, Cambridge University Press, UK, 2000.

-

[3]

Y. Fujiwara, W. Souma, H. Aoyama, T. Kaizoji, M. Aoki,

cond-mat/0208398, Physica A321 (2003) 598;

H. Aoyama, W. Souma, Y. Fujiwara, Physica A324 (2003) 352;

Y. Fujiwara, C.D. Guilmi, H. Aoyama, M. Gallegati, W. Souma, cond-mat/0310061, Physica A335 (2004) 197;

Y. Fujiwara, H. Aoyama, C.D. Guilmi, W. Souma, M. Gallegati, Physica A344 (2004) 112;

H. Aoyama, Y. Fujiwara, W. Souma, Physica A344 (2004) 117. - [4] R. Gibrat, Les inegalites economiques, Paris, Sirey, 1932.

-

[5]

A. Ishikawa,

Annual change of Pareto index dynamically deduced from the law of

detailed quasi-balance, physics/0511220, to appear in Physica A;

A. Ishikawa, Dynamical change of Pareto index in Japanese land prices, physics/0607131. -

[6]

W.W. Badger, in: B.J. West (Ed.), Mathematical Models as a Tool for the Social Science,

Gordon and Breach, New York, 1980, p. 87;

E.W. Montrll, M.F. Shlesinger, J. Stat. Phys. 32 (1983) 209. -

[7]

M.H.R. Stanley, L.A.N. Amaral, S.V. Buldyrev, S. Havlin, H. Leschhorn,

P. Maass, M.A. Salinger, H.E. Stanley,

Nature 379 (1996) 804;

L.A.N. Amaral, S.V. Buldyrev, S. Havlin, H. Leschhorn, P. Maass, M.A. Salinger, H.E. Stanley, M.H.R. Stanley, J. Phys. (France) I7 (1997) 621;

S.V. Buldyrev, L.A.N. Amaral, S. Havlin, H. Leschhorn, P. Maass, M.A. Salinger, H.E. Stanley, M.H.R. Stanley, J. Phys. (France) I7 (1997) 635;

L.A.N. Amaral, S.V. Buldyrev, S. Havlin, M.A. Salinger, H.E. Stanley, Phys. Rev. Lett. 80 (1998) 1385;

Y. Lee, L.A.N. Amaral, D. Canning, M. Meyer, H.E. Stanley, Phys. Rev. Lett. 81 (1998) 3275;

D. Canning, L.A.N. Amaral, Y. Lee, M. Meyer, H.E. Stanley, Economics Lett. 60 (1998) 335. - [8] H. Takayasu, M. Takayasu, M.P. Okazaki, K. Marumo, T. Shimizu, cond-mat/0008057, in: M.M. Novak (Ed.), Paradigms of Complexity, World Scientific, 2000, p. 243.

-

[9]

H. Aoyama,

Ninth Annual Workshop on Economic Heterogeneous Interacting Agents (WEHIA 2004);

H. Aoyama, Y. Fujiwara, W. Souma, The Physical Society of Japan 2004 Autumn Meeting. - [10] A. Ishikawa, physics/0508178, Physica A367 (2006) 425.

- [11] A. Ishikawa, physics/0506066, Physica A363 (2006) 367.

- [12] TOKYO SHOKO RESEARCH, LTD., http://www.tsr-net.co.jp/.

-

[13]

A. Drgulescu, V.M. Yakovenko, cond-mat/0103544,

Physica A299 (2001) 213;

A.C. Silva, V.M. Yakovenko, Europhys. Lett. 69 (2005) 304.