How Do Output Growth Rate Distributions Look Like?

Some Time-Series Evidence on OECD Countries

Abstract

This paper investigates the statistical properties of within-country GDP and industrial production (IP) growth rate distributions. Many empirical contributions have recently pointed out that cross-section growth rates of firms, industries and countries all follow Laplace distributions. In this work, we test whether also within-country, time-series GDP and IP growth rates can be approximated by tent-shaped distributions. We fit output growth rates with the exponential-power (Subbotin) family of densities, which includes as particular cases both the Gaussian and the Laplace distributions. We find that, for a large number of OECD countries including the U.S., both GDP and IP growth rates are Laplace distributed. Moreover, we show that fat-tailed distributions robustly emerge even after controlling for outliers, autocorrelation and heteroscedasticity.

pacs:

89.65.Gh; 89.90.+n; 02.60.EdI Introduction

In recent years, empirical cross-section growth rate distributions of diverse economic entities (i.e., firms, industries and countries) have been extensively explored by both economists and physicists Stanley et al. (1996); Canning et al. (1998); Lee et al. (1998); Amaral et al. (1997); Bottazzi and Secchi (2003a, b); Castaldi and Dosi (2004); Fu et al. (2005); Bottazzi et al. (2005); Sapio and Thoma (2006).

The main result of this stream of literature was that, no matter the level of aggregation, growth rates tend to cross-sectionally distribute according to densities that display tails fatter than those of a Gaussian distribution. From an economic point of view, this implies that growth patterns tend to be quite lumpy: large growth events, no matter if positive or negative, seem to be more frequent than what a Gaussian model would predict.

For example, at the microeconomic level, growth rates of U.S. manufacturing firms (pooled across years) appear to distribute according to a LaplaceStanley et al. (1996); Amaral et al. (1997). This result robustly holds even if one disaggregates across industrial sectors and/or considers cross-section distributions in each given year Bottazzi and Secchi (2003a, b). Moreover, in some countries (e.g., France) firm growth rates display tails even fatter than those of a Laplace density Bottazzi et al. (2005). Interestingly, similar findings are replicated at higher aggregation levels: both growth rates of industrial sectors Castaldi and Dosi (2004); Sapio and Thoma (2006) and countries Canning et al. (1998); Lee et al. (1998); Castaldi and Dosi (2004) display tent-shaped patterns.

Existing studies have been focusing only on cross-section distributions. In this paper, on the contrary, we ask whether fat-tailed distributions also emerge across time within a single country. More precisely, for any given country, we consider GDP and industrial production (IP) time series and we test whether their growth rate distributions can be well approximated by densities with tails fatter than the Gaussian ones.

Our analysis shows that in the U.S. both GDP and IP growth rates distribute according to a Laplace. Similar results hold for a large sample of OECD countries. Interestingly enough, this evidence resists to the removal of outliers, heteroscedasticity and autocorrelation from the original time series. Therefore, fat-tails emerges as a inherent property of output growth residuals, i.e. a fresh stylized fact of output dynamics.

Our work differs from previous, similar ones Canning et al. (1998); Lee et al. (1998); Castaldi and Dosi (2004) in a few other respects. First, we depart from the common practice of using annual data to build output growth rate distributions. We instead employ monthly and quarterly data. This allows us to get longer series and better appreciate their business cycle features. Second, we fit output growth rates with the exponential-power (Subbotin) distribution Subbotin (1923), which encompasses Laplace and Gaussian distributions as special cases. This choice allows us to measure how far empirical growth rate distributions are from the Normal benchmark 111A thorough comparative study on the goodness-of-fit of the Subbotin distribution vis-à-vis alternative fat-tails distributions (e.g., Student’s-t, Cauchy, Levy-Stable) is the next point in our agenda.. Finally, we check the robustness of our results to the presence of outliers, heteroscedasticity and autocorrelation in output growth rate dynamics.

II Data and Methodology

Our study employs two sources of (seasonally adjusted) data. As far as the U.S. are concerned, we employ data drawn from the FRED database. More specifically, we consider quarterly real GDP ranging from to (235 observations) and monthly IP from to (1018 observations). Analyses for the OECD sample of countries are performed by relying on monthly IP data from the “OECD Historical Indicators for Industry and Services” database (, 287 observations).

The main object of our analysis is output growth rate , defined as:

| (1) |

where is the output level (GDP or IP) at time in a given country, and is the first-difference operator.

Let the time interval over which we observe growth rates. The distribution of growth rates is therefore defined as . We study the shape of in each given country following a parametric approach. More precisely, we fit growth rates with the exponential-power (Subbotin) family of densities 222More on fitting Subbotin distributions to economic data is in Bottazzi and Secchi (2003a, b)., whose functional form reads:

| (2) |

where , and is the Gamma function. The Subbotin distribution is thus characterized by three parameters: a location parameter , a scale parameter and a shape parameter . The location parameter controls for the mean of the distribution. Therefore it is equal to zero up to a normalization that removes the average growth rate. The scale parameter is proportional to the standard deviation.

The shape parameter is the crucial one for our aims, as it directly gives information about the fatness of the tails: the larger , the thinner are the tails. Note that if the distribution reduces to a Laplace, whereas for we recover a Gaussian. Values of smaller than one indicate super-Laplace tails (see Figure 1 for an illustration).

III Empirical Results

In this section we present our main empirical results. We begin with an analysis of U.S. growth rate distributions. Next, we extend our results to other OECD countries. Finally, we turn to a robustness analysis of growth residuals, where we take into account the effects of outliers, heteroscedasticity and autocorrelation.

III.1 Exploring U.S. Output Growth Rate Distributions

Let us start by some descriptive statistics on U.S. output growth rates. Table 1 reports the first four moments of U.S. time series. Standard deviations reveal that after World War II growth rates of industrial production and GDP have been characterized by similar volatility levels.

| Series | Mean | Std. Dev. | Skewness | Kurtosis | Jarque-Bera | Lilliefors |

|---|---|---|---|---|---|---|

| test | test | |||||

| GDP | 0.0084 | 0.0099 | -0.0891 | 4.2816 | 15.4204* | 0.0623* |

| IP (1921) | 0.0031 | 0.0193 | 0.3495 | 14.3074 | 5411.7023* | 0.1284* |

| IP (1947) | 0.0028 | 0.0098 | 0.3295 | 8.1588 | 784.0958* | 0.0822* |

The standard deviation of IP growth rates becomes higher if the series is extended back to 1921. Skewness is close to zero: -0.09 for GDP and for IP. Notice that both the Jarque-Bera and Lilliefors normality tests reject the hypothesis that our series are normally distributed. Furthermore, the relatively high reported kurtosis values suggest that output growth rate distributions display tails fatter than the Gaussian distribution. In order to better explore this evidence, we fit U.S. output growth rates distribution with the Subbotin density (see eq. 2).

| Estimated Parameters | ||||||

|---|---|---|---|---|---|---|

| Series | Par. | Std. Err. | Par. | Std. Err. | Par. | Std. Err. |

| GDP | 1.1771 | 0.1484 | 0.0078 | 0.0006 | 0.0082 | 0.0006 |

| IP (1921) | 0.6215 | 0.0331 | 0.0091 | 0.0004 | 0.0031 | 0.0002 |

| IP (1947) | 0.9940 | 0.0700 | 0.0068 | 0.0003 | 0.0030 | 0.0003 |

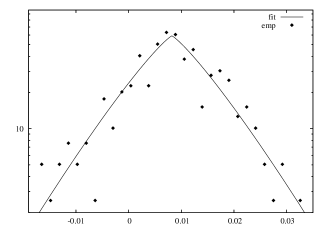

Consider GDP first. In the first row of Table 2, we show the maximum-likelihood estimates of Subbotin parameters and their standard errors 333The period of strong growth experienced by the U.S. economy after World War II is probably responsible for the positive location parameter (0.0082), which implies a positive sample average growth rate.. Estimates indicate that GDP growth rates seem to distribute according to a Laplace: the shape parameter is equal to 1.18, very close to the theoretical Laplace value of one. Therefore, U.S. output growth rates display tails fatter than a normal distribution. This can be also seen from Figure 3, where we plot the binned empirical density vis-à-vis the fitted one 444As one can visually appreciate, the goodness-of-fit is quite good. Preliminary results from extensive bootstrap goodness-of-fit testing exercises seems to statistically support this visual evidence..

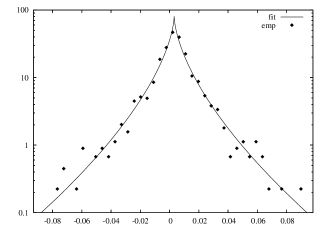

Next, we employ monthly industrial production (IP) as a proxy of U.S. output 555IP tracks very closely GDP in almost all countries. More precisely, the GDP-IP cross-correlation profile mimics from time to time the GDP auto-correlation profile.. Notice that, by focusing on IP growth, we can study a longer time span and thus improve our estimates by employing a larger number of observations. During the period , the IP growth rate distribution displays tails much fatter than the Laplace distribution (see Fig. 3 and the row of Table 2), an outcome probably due to the turmoils of the Great Depression.

Moreover, in order to better compare IP growth rate distribution with the GDP one, we also carry out an investigation on the post war period only (). Notwithstanding this breakdown, our results remain unaltered. In the post-war period the IP growth rate distribution exhibits the typical “tent-shape” of the Laplace density (cf. Fig. 4). This outcome is confirmed by a very close to one (see the third row of Table 2). As pointed out by the lower standard error, the estimate of is much more robust when we employ IP series instead of the GDP one.

To perform a more precise check, one might also compute the Cramer-Rao interval , where is the standard error of (Table 2, third column). A back-of-the-envelope computation shows that, for all three growth rate series, normality is always rejected. Moreover, one cannot reject the Laplace hypothesis for both GDP and IP-1947 series, whereas tails appear to be super-Laplace for IP-1921 666Cramer-Rao bounds are also graphically reported in Figure 5 at lag ..

Finally, in line with Bottazzi and Secchi (2006) we inspect the distribution of output growth rates computed over longer lags. More precisely, we consider growth rates now defined as:

| (3) |

where when GDP series is employed, and when IP series is under study. In line with Bottazzi and Secchi (2006), we find that the shape parameter estimated on GDP data becomes higher as increases (cf. the top panel of Fig. 5). When we consider IP series, the first falls and then starts rising (see the bottom panel of Fig. 5). Therefore, as the “growth lag” increases, tails become thinner (see Silva et al. (2004) for similar evidence in the contest of stock returns).

III.2 Cross-Country Analyses

In the previous section we have provided evidence in favor of fat-tailed (Laplace) U.S. output growth rate distributions. We now perform a cross-country analysis in order to assess whether this regularity pertains to the U.S. output only, or it might also be observed in other developed countries. Our analysis focuses on the following OECD countries: Canada, Japan, Austria, Belgium, Denmark, France, Germany, Italy, Netherlands, Spain, Sweden, and the U.K. .

| Series | Mean | Std. Dev. | Skewness | Kurtosis | Jarque-Bera | Lilliefors |

|---|---|---|---|---|---|---|

| test | test | |||||

| Canada | 0.0021 | 0.0113 | -0.2317 | 3.5631 | 5.9848 | 0.0391 |

| USA | 0.0026 | 0.0073 | -0.1505 | 4.6337 | 31.6281* | 0.0705* |

| Japan | 0.0027 | 0.0404 | -0.2250 | 4.6895 | 35.0981* | 0.0944* |

| Austria | 0.0024 | 0.0253 | 0.1707 | 5.7806 | 90.8554* | 0.0565* |

| Belgium | 0.0013 | 0.0401 | -0.5689 | 5.9446 | 115.6987* | 0.0884* |

| Denmark | 0.0025 | 0.0340 | 0.1214 | 7.2748 | 213.3210 | 0.0958* |

| France | 0.0013 | 0.0130 | 0.1525 | 3.7251 | 6.9217* | 0.0740* |

| Germany | 0.0015 | 0.0212 | 0.0098 | 9.2312 | 453.1891* | 0.0875* |

| Italy | 0.0017 | 0.0321 | 0.0453 | 5.8380 | 93.3429* | 0.0692* |

| Netherlands | 0.0015 | 0.0285 | -0.0350 | 6.5731 | 148.3145* | 0.0741* |

| Spain | 0.0017 | 0.0401 | 0.2559 | 4.0067 | 14.5026* | 0.0469 |

| Sweden | 0.0016 | 0.0302 | -0.2955 | 37.0700 | 13627.2129* | 0.1153* |

| UK | 0.0012 | 0.0140 | -0.1631 | 8.4090 | 342.3813* | 0.0712* |

We start by analyzing the basic statistical properties of the output growth rate time series (cf. Table 3). In order to keep a sufficient time-series length, we restrict our study to the industrial production series only. The standard deviations of the IP series range from 0.0073 (U.S.) to 0.0404 (Japan). In half of the countries that we have analyzed, the distributions of IP growth rates seem to be slightly right-skewed, whereas in the other half they appear to be slightly left-skewed. The analysis of the kurtosis reveals that in every country of the sample the IP growth rate distribution is more leptokurtic than the Normal distribution. Indeed, apart from Spain and Canada, standard normality tests reject the hypothesis that IP growth series are normally distributed.

Given this descriptive background, we turn to a country-by-country estimation of the Subbotin distributions. Estimated coefficients are reported in Table 4.

| Estimated Parameters | ||||||

|---|---|---|---|---|---|---|

| Country | Par. | Std. Err. | Par. | Std. Err. | Par. | Std. Err. |

| Canada | 1.6452 | 0.2047 | 0.0104 | 0.0007 | 0.0020 | 0.0010 |

| USA | 1.2980 | 0.1516 | 0.0060 | 0.0004 | 0.0031 | 0.0004 |

| Japan | 0.8491 | 0.0901 | 0.0259 | 0.0020 | 0.0021 | 0.0014 |

| Austria | 1.2499 | 0.1446 | 0.0204 | 0.0014 | 0.0010 | 0.0014 |

| Belgium | 1.0202 | 0.1125 | 0.0284 | 0.0021 | 0.0011 | 0.0017 |

| Denmark | 0.8063 | 0.0847 | 0.0215 | 0.0017 | 0.0000 | 0.0012 |

| France | 1.2623 | 0.1464 | 0.0106 | 0.0008 | 0.0010 | 0.0007 |

| Germany | 0.9768 | 0.1067 | 0.0144 | 0.0011 | 0.0024 | 0.0008 |

| Italy | 1.0778 | 0.1204 | 0.0237 | 0.0017 | 0.0010 | 0.0015 |

| Netherlands | 1.2133 | 0.1393 | 0.0223 | 0.0016 | 0.0019 | 0.0015 |

| Spain | 1.4583 | 0.1755 | 0.0352 | 0.0024 | 0.0021 | 0.0029 |

| Sweden | 0.8826 | 0.0944 | 0.0168 | 0.0013 | 0.0010 | 0.0009 |

| U.K. | 1.0972 | 0.1230 | 0.0103 | 0.0008 | 0.0019 | 0.0006 |

The results of the cross-country analysis confirm that output growth rates distribute according to a Laplace almost everywhere. Excluding Canada, estimated “shape” coefficients are always close to 1. If one considers the Cramer-Rao interval , the only country where output growth rate distribution does not appear to be Laplace is Canada, whose -interval lies above one 777Another exception is Denmark, where the upper bound of its -interval is slightly below one..

III.3 Robustness Checks: Outliers, Heteroscedasticity, and Autocorrelation

The foregoing discussion has pointed out that within-country output growth rate distributions are markedly non-Gaussian. The evidence in favor of Laplace (or super-Laplace) densities robustly arises in the majority of OECD countries, it does not depend on the way we measure output (GDP or IP), and it emerges also at frequencies more amenable for the study of business cycles dynamics (i.e. quarterly and monthly). Notice also that our analysis does not show any clear evidence in favor of asymmetric Laplace (or Subbotin) growth rate distributions. Hence, almost all OECD countries seem to exhibit (with a probability higher than we would expect) large, positive growth events with the same likelihood of large, negative ones.

This “fresh” stylized fact on output dynamics must be however scrutinized vis-à-vis a number of robustness checks. More precisely, the above results can be biased by two classes of problems. First, the very presence of fat-tails in the distribution of country-level growth rates might simply be due to the presence of outliers. Thus, one should remove such outliers from the series and check whether fat tails are still there. Second, our within-country analysis relies on pooling together growth rate observations over time. Strictly speaking, the observations contained in should come from i.i.d. random variables. In other words, we should verify that fat tails do not characterize growth rates only, but they are a robust feature of growth residuals (also known as “innovations”). To do so, one might remove the possible presence of any structure in growth rate time series due to autocorrelation and heteroscedasticity, and then fit a Subbotin density to the residuals.

Our robustness analyses seem to strongly support the conclusion that fat-tails still characterize our series also after having controlled for outliers, autocorrelation and heteroscedasticity. More precisely, in the first row of Table 5 we have reported the estimates of the Subbotin parameters in the case of U.S. GDP, after having removed the most common types of outliers Darné and Diebolt (2004). The estimate for the shape parameter () still remains close to one, thus reinforcing evidence in favor of Laplace fat-tails.

| Estimated Parameters | ||||||

| After removing | Par. | Std. Err. | Par. | Std. Err. | Par. | Std. Err. |

| Outliers only | 1.2308 | 0.1568 | 0.0073 | 0.0006 | 0.0000 | 0.0006 |

| Outliers and autocorrelation | 1.2696 | 0.1628 | 0.0071 | 0.0006 | 0.0000 | 0.0006 |

Moreover, in order to remove any structure from the growth rate process, we have fitted a battery of ARMA specifications to the growth rate time series obtained after cleanup of outliers and we have selected the best model trough the standard Box and Jenkins’s procedure. In Table 5, second row, we report – for the case of U.S. GDP – our Subbotin estimates for the distribution of residuals of the best ARMA model, which turns out to be an AR(1) without drift (thus implying the presence of some autocorrelation in the original growth rate series). However, the best fit for the distribution of the AR(1) residuals is a Subbotin distribution very close to a Laplace (). Similar results hold also for the IP growth rate series and are reasonably robust across our sample of OECD countries.

Finally, we ran standard Ljung-Box and Engle’s ARCH heteroscedasticity tests on our growth series without detecting any clear-cut evidence in favor of non-stationary variance over time.

As Figure 6 shows for U.S. GDP, fat-tailed Laplace densities seem therefore to robustly emerge even after one washes away from the growth process both outliers and autocorrelation (and moving-average) structure (i.e., when one considers growth residuals as the object of analysis).

IV Concluding Remarks

In this paper we have investigated the statistical properties of GDP and IP growth rate time series distributions by employing quarterly and monthly data from a sample of OECD countries.

We find that in the U.S., as well as in almost all other developed countries of our sample, output growth rate time series distribute according to a symmetric Laplace density. This implies that the growth dynamics of aggregate output is lumpy, being considerably driven by “big events”, either positive or negative. We have checked this result against a number of possible sources of bias. We find that lumpiness appears to be a very property of the data generation process governing aggregate output growth, as it appears to be robust to the removal of both outliers and auto-correlation.

At a very general and rather broad level, the robust emergence of fat-tailed distributions for within-country time series of growth rates and residuals can be interpreted as a fresh, new stylized fact on output dynamics, to be added to the long list of its other known statistical properties 888Two rather undisputed stylized facts of output dynamics – at least for the U.S. – are: (i) GNP growth is positively autocorrelated over short horizons and has a weak and possibly insignificant negative autocorrelation over longer horizons; (ii) GNP appears to have an important trend-reverting component Nelson and Plosser (1982); Cochrane (1988, 1994); Blanchard and Quah (1989); Rudebusch (1993); Murray and Nelson (2000)..

¿From a more empirical perspective, our results (together with the already mentioned cross-section ones Stanley et al. (1996); Canning et al. (1998); Lee et al. (1998); Amaral et al. (1997); Bottazzi and Secchi (2003a, b); Castaldi and Dosi (2004); Fu et al. (2005); Bottazzi et al. (2005); Sapio and Thoma (2006)) ought to be be interpreted together with recent findings against log-normality for the cross-section distributions of firm and country size Cabral and Mata (2003); Dosi (2005); Axtell (2006); Quah (1996, 1997), and on power-law scaling in cross-country per-capita GDP distributions Di Guilmi et al. (2003). This joint empirical evidence seems to suggest that in economics the room for normally-distributed shocks and growth processes obeying the “Law of large numbers” and the “Central limit theorem” is much more limited than economists were used to believe. In other words, the general hint coming from this stream of literature is in favor of an increasingly “non-Gaussian” economics and econometrics. A consequence of this suggestion is that we should be very careful in using econometric testing procedures that are heavily sensible to normality of residuals 999Such as Gibrat-like regressions for the dependence of firm growth on size Sutton (1997) and cross-section country growth rates analyses Barro and Sala-i Martin (1992).. On the contrary, testing procedures that are robust to non-Gaussian errors and/or tests based on Subbotin- or Laplace-distributed errors should be employed when necessary.

Finally, country-level, non-Gaussian growth rates distributions (both within-country and cross-section) might have an important implication on the underlying generating processes. Suppose to interpret the country-level growth rate in a certain time period as the result of the aggregation of microeconomic (firm-level) growth shocks across all firms and industries in the same time period. The emergence of within-country non-Gaussian growth distributions strongly militates against the idea that country growth shocks are simply the result of aggregation of independent microeconomic shocks over time. Therefore, some strong correlating mechanism linking in a similar way at every level of aggregation the units to be aggregated seems to be in place. This interpretation is in line with the one proposed by Amaral et al. (1997); Canning et al. (1998); Castaldi and Dosi (2004) who envisage the widespread presence of fat tails as an indicator of the overall “complexity” of any growth process, mainly due to the strong inner inter-relatedness of the economic organizations under study.

Acknowledgements.

Thanks to Giulio Bottazzi, Carolina Castaldi, Giovanni Dosi, Marco Lippi, Sandro Sapio, Angelo Secchi and Victor M. Yakovenko, for their stimulating and helpful comments. All usual disclaimers apply.References

- Stanley et al. (1996) M. H. Stanley, L. A. N. Amaral, S. V. Buldyrev, S. Havlin, H. Leschhorn, P. Maass, M. A. Salinger, and H. E. Stanley, Nature 379, 804 (1996).

- Canning et al. (1998) D. Canning, L. A. N. Amaral, Y. Lee, M. Meyer, and H. E. Stanley, Economic Letters 60, 335 (1998).

- Lee et al. (1998) Y. Lee, L. A. N. Amaral, D. Canning, M. Meyer, and H. E. Stanley, Physical Review Letters 81, 3275 (1998).

- Amaral et al. (1997) L. A. N. Amaral, S. V. Buldyrev, S. Havlin, M. A. Salinger, H. E. Stanley, and M. H. Stanley, Physica A 244, 1 (1997).

- Bottazzi and Secchi (2003a) G. Bottazzi and A. Secchi, Review of Industrial Organization 23, 217 (2003a).

- Bottazzi and Secchi (2003b) G. Bottazzi and A. Secchi, Economic Letters 80, 415 (2003b).

- Castaldi and Dosi (2004) C. Castaldi and G. Dosi, Working Paper 2004/18, Laboratory of Economics and Management (LEM), Sant’Anna School of Advanced Studies, Pisa, Italy (2004).

- Fu et al. (2005) D. Fu, F. Pammolli, S. Buldyrev, M. Riccaboni, K. Matia, K. Yamasaki, and H. Stanley, Proceedings of the Nationaly Academy of Science 102, 18801 (2005).

- Bottazzi et al. (2005) G. Bottazzi, A. Coad, N. Jacoby, and A. Secchi, Working Paper 2005/21, Laboratory of Economics and Management (LEM), Sant’Anna School of Advanced Studies, Pisa, Italy (2005).

- Sapio and Thoma (2006) S. Sapio and G. Thoma, Working Paper 2006/09, Laboratory of Economics and Management (LEM), Sant’Anna School of Advanced Studies, Pisa, Italy (2006).

- Subbotin (1923) M. Subbotin, Matematicheskii Sbornik 31, 296 (1923).

- Bottazzi (2004) G. Bottazzi, Working Paper 2004/14, Laboratory of Economics and Management (LEM), Sant’Anna School of Advanced Studies, Pisa, Italy (2004).

- Bottazzi and Secchi (2006) G. Bottazzi and A. Secchi, RAND Journal of Economics Forthcoming (2006).

- Silva et al. (2004) A. Silva, R. Prange, and V. Yakovenko, Physica A 344, 227 (2004).

- Darné and Diebolt (2004) C. Darné and O. Diebolt, Journal of Monetary Economics 51, 1449 (2004).

- Goḿez and Maravall (2001) V. Goḿez and A. Maravall, in A Course in Time Series Analysis, edited by D. Peña, G. Tiao, and R. Tsay (Wiley, NewYork, 2001).

- Cabral and Mata (2003) L. Cabral and J. Mata, American Economic Review 93, 1075 (2003).

- Dosi (2005) G. Dosi, Working Paper 2005/17, Laboratory of Economics and Management (LEM), Sant’Anna School of Advanced Studies, Pisa, Italy (2005).

- Axtell (2006) R. Axtell, CSED Working Paper 44, The Brookings Institution, Washington, DC (2006).

- Quah (1996) D. Quah, Economic Journal 106, 1045 (1996).

- Quah (1997) D. Quah, Journal of Economic Growth 2, 27 (1997).

- Di Guilmi et al. (2003) C. Di Guilmi, E. Gaffeo, and M. Gallegati, Economics Bulletin 15, 1 (2003).

- Nelson and Plosser (1982) C. R. Nelson and C. O. Plosser, Journal of Monetary Economics 10 (1982).

- Cochrane (1988) J. Cochrane, Journal of Political Economy 96, 893 (1988).

- Cochrane (1994) J. Cochrane, Quarterly Journal of Economics 109, 241 (1994).

- Blanchard and Quah (1989) O. Blanchard and D. Quah, American Economic Review 79, 655 (1989).

- Rudebusch (1993) R. G. Rudebusch, American Economic Review 83 (1993).

- Murray and Nelson (2000) C. J. Murray and C. R. Nelson, Journal of Monetary Economics 46 (2000).

- Sutton (1997) J. Sutton, Journal of Economic Literature 35, 40 (1997).

- Barro and Sala-i Martin (1992) R. Barro and X. Sala-i Martin, Journal of Political Economy 100, 223 (1992).