Crossover between Lvy and Gaussian regimes in first passage processes

Abstract

We propose a new approach to the problem of the first passage time. Our method is applicable not only to the Wiener process but also to the non-Gaussian Lvy flights or to more complicated stochastic processes whose distributions are stable. To show the usefulness of the method, we particularly focus on the first passage time problems in the truncated Lvy flights (the so-called KoBoL processes), in which the arbitrarily large tail of the Lvy distribution is cut off. We find that the asymptotic scaling law of the first passage time distribution changes from -law (non-Gaussian Lvy regime) to -law (Gaussian regime) at the crossover point. This result means that an ultra-slow convergence from the non-Gaussian Lvy regime to the Gaussian regime is observed not only in the distribution of the real time step for the truncated Lvy flight but also in the first passage time distribution of the flight. The nature of the crossover in the scaling laws and the scaling relation on the crossover point with respect to the effective cut-off length of the Lvy distribution are discussed.

pacs:

02.50.Ga, 02.50.Ey, 89.65.GhI Introduction

The first passage process or the first passage time (FPT) problem deals with the event where a diffusing particle or a random-walker firstly reaches a specific site at a specific time Redner . These FPT problems have been studied in various research fields, such as statistical physics, chemistry Kappen and biological neuroscience Tuckwell ; Tuckwell2 . In finance, several authors Simonsen ; Raberto ; Scalas ; Kurihara ; Sazuka ; Sazuka2 have analysed tick-by-tick data of the US dollar/Japanese yen (USD/JPY) exchange rate and studied the FPT distribution for which the FPT is defined by the time that the rate firstly moves out from a given range.

Among these studies, the USD/JPY exchange rates of the Sony Bank SonyBank are reproduced from the market rates by using some rate windows with a width of yen Sazuka ; Sazuka2 . That is, if the USD/JPY market rate changes by more than yen, the Sony Bank rate for USD/JPY is updated to the market rate otherwise it remains constant. In this sense, it is possible for us to say that the procedure for determining the USD/JPY exchange rate of the Sony Bank is essentially the first passage process. Despite many demands from various research fields and business in financial markets, one could obtain explicit analytical expressions or solutions of the FPT distribution only in very few cases. In addition, except for a few cases Rangarajan , most of the analytical expressions are of the ordinary Wiener process (ordinary Brownian motion).

Based on this fact, here we propose a new approach to the problem of the FPT or first passage processes. Our method is applicable not only to the Wiener process but also to the anomalous diffusion of the non-Gaussian Lvy flights or more complicated stochastic processes. To show the usefulness of our approach, we particularly focus on the FPT problems in the truncated Lvy flights Mantegna94 ; Mantegna94_2 ; Koponen , in which the arbitrarily large tail of the Lvy distribution is cut off. Using the method, we find that the asymptotic scaling law of the FPT distribution changes from a -law (non-Gaussian Lvy regime) to a -law (Gaussian regime) at some crossover point. This fact means that the crossover between non-Gaussian Lvy and Gaussian regimes is observed not only in the distribution of the real-time step of the truncated Lvy flight, which was reported by Mantegna and Stanley Mantegna94 , but also in the FPT distribution of the flight. Moreover, we give a scaling relation on the crossover point with respect to the effective cut-off length of the Lvy distribution. The scaling relation enables us to predict the crossover point of the FPT distribution for a given truncated Lvy flight.

This paper is organised as follows. In the next section, we explain general formalism of our method and apply it to the FPT problem for the Wiener process, for which the solution of the FPT distribution is well-known, in order to check the validity of our method. In Sec. III, we show that our method is widely useful for a class of stable stochastic processes. We derive the FPT distribution for Lvy flight which includes Gaussian and Lorentzian stochastic processes as its special cases. For each stable stochastic process, we discuss the scaling law of the FPT distribution in the asymptotic regime. The analytical results are confirmed by computer simulations. In Sec. IV, we apply our method to the FPT problem of the truncated Lvy flight and discuss the crossover in the scaling laws of the FPT distribution between non-Gaussian Lvy and Gaussian regimes. The last section is a summary.

II General formalism

The problem we deal with in this paper is defined as follows. Let us consider the stochastic process : . For this time series, the FPT is defined by . Then, our problem is to obtain the distribution of , namely, the first passage time distribution . In other words, we evaluate the distribution of , that is , which is defined as the survival probability that the time series , starting from keeps staying within the range up to the time step . The problem we are dealing with is motivated by the real mechanism of the Sony Bank foreign exchange rate Sazuka ; Sazuka2 . The Sony Bank rate is the foreign exchange rate that the Sony Bank offers with reference to the market rate. Basically, trades can be made on the web SonyBank while the market is open. The Sony Bank rate depends on the market rate but is independent of the customers’ orders. If the USD/JPY market rate changes by yen or more, the Sony Bank rate for USD/JPY is updated to the market rate. For instance, for the stochastic process of the real market (what we call tick-by-tick data): with and , the Sony Bank rate stays flat from the time to , as the market rate is in the range of yen based on the market rate at . When the market rate exceeds the range of yen at , the Sony Bank rate is updated to the market rate. Obviously, the time interval here corresponds to the FPT we explained above and it is worth while for us to evaluate its distribution to investigate statistical property of the Sony Bank USD/JPY rates.

To calculate the FPT distribution for the time series , we define the probability , which means the probability of the FPT is as

| (1) |

where means the Heviside step function, namely, for and for . We usually solve a kind of (fractal) Fokker-Plank equations under some appropriate boundary conditions Kappen ; Tuckwell ; Tuckwell2 ; Rangarajan ; Rangarajan2 ; Rangarajan3 or use the so-called image method Redner ; Durrett to discuss the FPT problem. However, as we saw in equation (1), our approach is completely different from such standard treatments. To evaluate the FPT (probability) distribution, say , we directly count the number of , namely, appearing within quite a long time interval . We might choose as a time interval during which the market is open. Then, the ratio should be expected to converge to as tends to infinity. This is the meaning of equation (1) and is our basic idea for evaluating the FPT distribution. From our method, to evaluate the FPT distribution by counting (), the probability is also given by , that is to say,

| (2) | |||||

In the same way as the probability , the probability is obtained as

| (3) | |||||

We should notice that the probability was cancelled in this expression (3). Thus, we easily generalise this kind of calculations to evaluate the distribution by repeating the above procedure as follows.

| (4) |

where were all cancelled in this final formula (4). This equation (4) is the starting point of our evaluation. At a glance, this equation seems to be just a definition of the FPT distribution; however, for some classes of stochastic processes, we can derive the explicit form of the FPT distribution from this simple equation. In the next subsection, we derive the FPT distribution for the Wiener process as a simple test of our method. We stress that our approach helps as an intuitive account for the first passage process and derivation of its distribution.

II.1 A simple test of the method for Wiener stochastic processes

To show the validity and usefulness of our method, we derive the FPT distribution from the above expression (4) for Wiener stochastic processes (Brownian motion). The ordinary Wiener process is described by , where the noise term obeys the white Gaussian with zero-mean and variance . Then, we should notice that the difference is rewritten in terms of the sum of the noise terms as . As is well-known, as the Gaussian process is stable, obeys the Gaussian with zero-mean and variance. Using the same argument as , also obeys the Gaussian with zero-mean and variance. Therefore, the FPT distribution derived by equation (4) leads to

| (5) | |||||

| (6) |

when we assume that the underlying stochastic process is ergodic, namely, that time average and ensemble average coincide. For the ordinary Wiener process, the probability distributions for and are Gaussians with zero mean and variances , respectively. Thus, we easily evaluate the integral appearing in (6) after substituting and obtain as

| (7) |

where we defined . The function is defined by . We should keep in mind that the above result is valid for discrete time , however; it is easy for us to obtain its continuous time version by replacing , and evaluating (7) in the limit of . Then, we have

| (8) |

Thus, the FPT distribution for the ordinary Wiener process in the continuous time limit is given by

| (9) |

This well-known form is expected the inverse Gaussian distribution Chikara for the FPT distribution of the ordinary Wiener process and is often observed in the so-called inter-spike interval (ISI) of the integrate-and-fire model for neural networks Tuckwell ; Tuckwell2 ; Gerstner . Therefore, in the asymptotic regime , the FPT distribution for the Wiener process obeys -scaling law. From the above discussion, we found that our new approach based on direct counting of the FPT to obtain the FPT distribution is effective and gives a well-known solution for the ordinary Wiener process.

Before we move to the main section, we should comment on the much shorter derivation of the above formulation (9). Let us define our stochastic process by and the probability density function finding the process in at time provided that it was in at time by . Here, we assume that is symmetric with respect to . We also define the FPT with absorbing barriers by . Then, the complementary cumulative distribution of is given by

| (10) |

and the cumulative distribution function leads to

| (11) |

Thus, the FPT distribution is obtained by

| (12) |

This equation coincides with equation (9). We should also mentioned that the similar derivations are found in the references Risken ; Gardiner .

III Stable processes and their FPT distributions

We stress that our method is widely applicable to stochastic processes whose distributions are stable. Stable processes are specified as follows. If stochastic variables () are identically independently distributed from , the Fourier transform of the sum of the , namely, is given by

| (13) |

where is the Fourier transform of the stochastic variable , namely, the characteristic function and defined by

| (14) |

Then, the stochastic process is referred to as a stable process. Strictly speaking, equation (13) is a possible definition of infinitely divisible random variables and not of stable random variables. A stable random variable is infinitely divisible and stability refers to the invariance of the distribution with respect to convolutions.

It is obvious that for this class of stable processes, the FPT distribution is easily obtained by our method because the probability distributions and to evaluate in (5) are defined explicitly. In the next subsections, we show several results from our new approach.

III.1 Lorentzian stochastic processes

As a first simple example of the stable distributions, let us think about Lorentzian stochastic processes: , where the noise term obeys the following white Lorentzian :

| (15) |

Then, the characteristic function of the stochastic variable is given by

| (16) |

By using the convolution of the Fourier transform for the variable , we have . Therefore, the inverse Fourier transform of leads to the probability distribution of the sum of noise term as follows.

| (17) |

By substituting this probability into equations (5) and (6), we obtain the FPT distribution for the Lorentzian stochastic processes as follows:

| (18) | |||||

where we defined . This is a result for discrete time steps; however, its continuous version is easily obtained by using as follows.

| (19) |

From this result (19), we find that the FPT distribution for the Lorentzian stochastic processes obeys Lorentzian. In the asymptotic regime , the FPT distribution for the Lorentzian stochastic processes obeys the -scaling law.

III.2 Anomalous diffusion of Lvy flight

We next consider the case of Lvy stochastic processes whose noise term of the stochastic process obeys the following Lvy distribution :

| (20) |

We should keep in mind that the above distribution (20) is reduced to the Wiener stochastic process () and the Lorentzian stochastic process () as its special cases. As this process () is also stable, the sum of the noise term has the following probability distribution

| (21) |

Now, we can derive the FPT distribution by substituting into equations (5) and (6) as

| (22) | |||||

Expression of a continuous time version (22) is obtained from the derivative of the above discrete time distribution with respect to as

| (23) |

In the asymptotic regime , by replacing the variable as and after some simple algebra, we obtain

| (24) | |||||

| (25) |

where the means Gamma function and is a constant of order . Then, we should notice that the above scaling law is consistent with both the Wiener stochastic process ( for ) and with the Lorentzian stochastic process ( for ) we discussed in the previous subsections.

As we saw in the above stochastic processes, our new approach based on direct counting of the FPT is widely useful for the class of stable stochastic processes and the final expressions (5)(6), containing at most just two integrals. Moreover, our approach can be applied to the FPT problems with a surprisingly wide variety of absorbing boundary conditions. This is one of the advantages of our method over other approaches based on analysis of Fokker-Plank equations. To show the advantage, in the next section, we apply our method to much more complicated stochastic stable process.

III.3 Computer simulations

To check the theoretical prediction of the power-law exponent for the FPT distribution, we perform computer simulations. Then, to generate the additive noise for each time step, the Lvy stable distribution is needed. As shown by Umeno Umeno , the Lvy stable distribution is obtained by a superposition of a chaotic map such as

| (26) |

namely, for independently selected initial conditions , the quantity obeys a Lvy stable law with , that is,

| (27) |

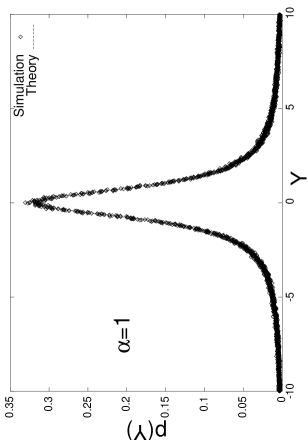

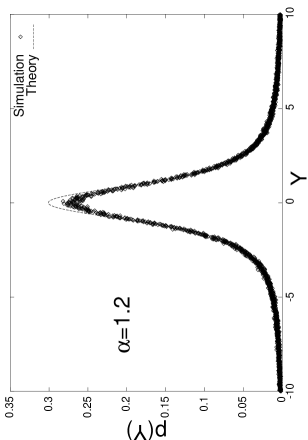

In FIG. 1, we plot the Lvy distribution with (Lorentzian) and obtained by the superposition of the chaotic map (26). We set the number of the superposition of the chaotic map .

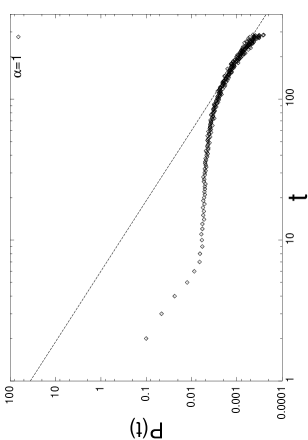

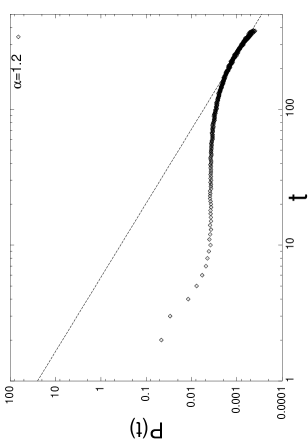

From this figure, we find that the distributions obtained by the simulations are in good agreement with the corresponding analytical expressions (27). Keeping these results in mind, we use the sampling point from the superposition of the chaotic map (26) as the additive noise in the stochastic process for each time step. Then, we should notice that one should choose a large value for the width of the rate window , say, to investigate the tail of the FPT distribution. This is because it is a rare event for the random walker to stay in the range and it takes quite long computational time for us to obtain the tail exponent (relatively long FPT) if is small. Here, we choose and evaluate the power-law exponent of the FPT distribution for the Lvy processes with and . The results are shown in FIG. 2.

From this figure, we find that the power-law tails have almost the same exponents as those predicted by our theory. Of course, the tail region is too noisy to conclude that the simulations are completely consistent with the theory. However, at least, we may say that they are not in disagreement. Thus, the computer simulations provided us with a justification of our theoretical formulation.

IV Crossover in scaling laws of FPT distributions

In the previous section, we showed our new formulation is effective and much more simpler than the approach of the (fractal) Fokker-Plank equations Rangarajan to obtain the FPT distribution for stable stochastic processes. We actually found that the FPT distribution of the general non-Gaussian Lvy stochastic process specified by parameter is obtained and its scaling behaviour in the asymptotic regime is -law. In this section, we show that our formalism is also useful in obtaining the FPT distribution for the so-called truncated Lvy flight (the so-called KoBoL processes from Koponen, Boyarchenko and Levendorskii Koponen ; KoBoL ; Boyarchenko ), for which it is well-known that the crossover between the a Lvy and a Gaussian regime in the distribution of the real time step takes place Mantegna94 ; Mantegna94_2 ; Koponen ; Mantegna2000 . In this section, we show, by using our method based on direct counting of the FPT, this kind of crossover in scaling laws is also observed in the FPT .

The characteristic function for the truncated Lvy flight is defined by

| (28) |

where as Voit . Therefore, in this limit , the above equation (28) is reduced to . Obviously, this is identical to the characteristic function of the conventional Lvy flight as we already saw in the previous section. For this reason, a non-zero value of controls the cut-off width of the truncated Lvy flight. We should notice that one could also use a hard cut-off version of the truncation scheme Mantegna94 , namely,

| (29) |

However, for its mathematical simplicity, we use the soft cut-off version of the truncation scheme which will be explained below.

By the convolution of the Fourier transform, we can show

| (30) |

and then the sum of the noise term of the truncated Lvy flight obeys the following probability distribution:

| (31) | |||||

Substituting these probability distributions into equations (6) and (5), and taking the derivative of with respect to , we obtain the FPT distribution of the truncated Lvy flight for continuous time case as

| (32) | |||||

Thus far, it has been difficult to perform the above two integrals with respect to and analytically to obtain a compact form of the FPT distribution. However, numerical integrations of equation (32) enable us to proceed to it.

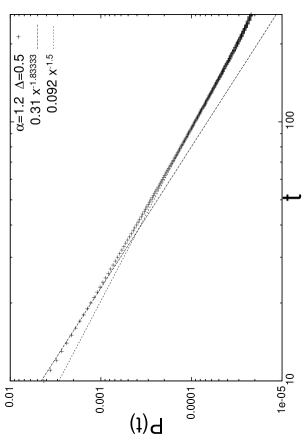

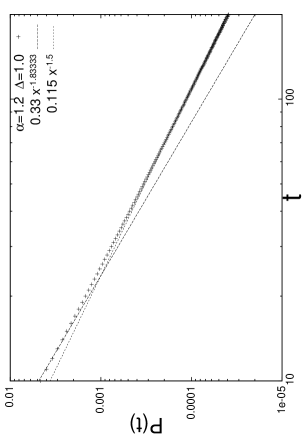

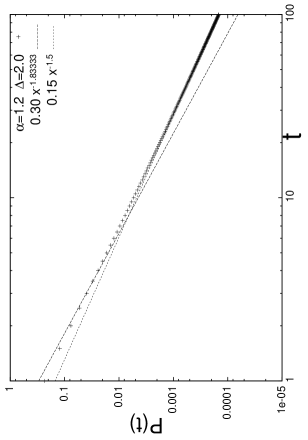

In FIG. 3, we show the scaling plot of the FPT distribution for the truncated Lvy flight with for several values of . From these three panels in FIG. 3, we find that the scaling law of the FPT distribution changes from to at some crossover points (), 19 () and (). To obtain useful information about the crossover point , we evaluate the asymptotic form of the FPT distribution (32) for both (Gaussian regime) and (non-Gaussian Lvy regime).

For Gaussian regime , by replacing the variable with as , that is,

| (33) |

we obtain

| (34) | |||||

| (35) |

It should be noted that this -law is valid for . From the equation (33), this condition reads

| (36) |

On the other hand, for , that is to say, for , the FPT distribution (32) is evaluated as

| (37) | |||||

This result is identical to the FPT distribution for the conventional Lvy flight, which is defined by equations (24) and (25), and was already obtained in the previous section.

Let us summarise the result for the scaling laws of the FPT distribution for the truncated Lvy flight.

| (40) |

We should bear in mind that the crossover point obtained by (36) contains integral variable . Therefore, it is hard to say that is well-defined. To delete the -dependence of , we consider the ratio of and . From equation (36), we obtain , namely, . Let us check this scaling relation for the result we obtained in FIG. 3. For , the relation reads . This relation predicts the crossover point , which is very close to the results obtained in FIG. 3, namely, and . The small difference is probably because of impreciseness of numerical integrations appearing in equation (32).

The relation for successive values of and is easily extended for the relation between and () as follows.

| (41) |

This scaling relation for the crossover point in the scaling laws of the FPT distribution of the truncated Lvy flight is one of the main results in this paper. From this result (41), we find that the crossover point increases rapidly as the effective cut-off length also increases as

| (42) |

where we set . Therefore, we conclude that the crossover between non-Gaussian Lvy and Gaussian regimes is observed not only in the distribution of the real-time flight, which was reported by Mantegna and Stanley Mantegna94 , but also in the FPT distribution of the truncated Lvy flight.

In the study by Mantegna and Stanley Mantegna94 , they investigated the stochastic variable , where obeys the truncated Lvy flight. They evaluated the probability of return and found that the obeys the Gaussian -law in the large real time step regime. In this section, it was shown that this ultra-slow convergence from Lvy regime to the Gaussian regime is conserved even if we consider the first passage process of the truncated Lvy flight. The relation between their results and ours is clearly understood as follows.

For a given time interval of the first passage process of the truncated Lvy flight, the time series of the variable behaves as , where is an origin for the measurement of the interval . Then, from the observation by Mantegna and Stanley, the sum obeys a Gaussian with zero-mean and variance if the time interval is large enough, that is, . Then, the probability of return is given by . In other words, for , it takes quite long time for a random-walker to escape from the region , and the time for escaping guarantees that the central limit theorem works to make the variable a Gaussian. As a result, the FPT distribution should follow the corresponding Gaussian -law from our argument for the case of the Wiener process (9). On the other hand, if the interval is smaller than the crossover point , the central limit theorem for does not work and is no longer a Gaussian. Then, as we checked, the FPT distribution obeys -law of the Lvy flight.

V Summary

In this paper, we proposed a new approach to evaluate the FPT distribution. Our method is based on direct counting of the FPT. We show that our approach gives an explicit form of the FPT distribution for stable stochastic processes. Actually, for Wiener (Brownian motion), Lorentzian and Lvy stochastic processes, our method was demonstrated. Thanks to the mathematical simplicity of our method, it becomes easy to grasp the intuitive meaning of the FPT distribution and to tackle more complicated stochastic processes. As an example, we discussed the FPT distribution of the truncated Lvy flight (the KoBoL process). We found a clear crossover between non-Gaussian Lvy and Gaussian regimes in the scaling laws of the FPT distribution. We found the scaling relation on the crossover point with respect to the effective length of the cut-off as with .

Very recently, Koren et.al. Koren investigated not only the FPT distribution but also the first passage leapover (FPL) distribution under a single absorbing boundary condition. A relatively new concept, the FPL is defined as the flight length for a random walker to move beyond the single boundary (a target). Our system in this paper possesses two boundaries (in this sense, our process might be referred to as a first exit process); however, it might be possible to apply our analysis to the problem in order to discuss the FPL distribution. This will be addressed in future work.

We hope that beyond the present analysis for the Sony Bank rate, our approach might be widely used in many scientific research fields, especially in the field of econophysics including financial data analysis.

Acknowledgements.

One of the authors (J.I.) was financially supported by Grant-in-Aid for Young Scientists (B) of The Ministry of Education, Culture, Sports, Science and Technology (MEXT) No. 15740229 and Grant-in-Aid Scientific Research on Priority Areas “Deepening and Expansion of Statistical Mechanical Informatics (DEX-SMI)” of The Ministry of Education, Culture, Sports, Science and Technology (MEXT) No. 18079001. N.S. would like to thank Shigeru Ishi, President of the Sony Bank, for useful discussions. The authors thank the anonymous referee for many instructive comments on the manuscript. We also thank Enrico Scalas for fruitful discussion and useful comments.References

- (1) S. Redner, A Guide to First-Passage Processes, Cambridge University Press (2001).

- (2) N.G. van Kappen, Stochastic Processes in Physics and Chemistry, North Holland, Amsterdam (1992).

- (3) H.C. Tuckwell, Introduction to Theoretical Neurobiology, Vol. 2, Cambridge University Press (1988).

- (4) H.C. Tuckwell, Stochastic Processes in the Neurosciences, Society for Industrial and Applied Mathematics, Philadelphia, Pennsylvania (1989).

- (5) I. Simonsen, M.H. Jensen and A. Johansen, Eur. Phys. J. B 27, 583 (2002).

- (6) M. Raberto, E. Scalas and F. Mainardi, Physica A 314, 749 (2002).

- (7) E. Scalas, R. Gorenflo, H. Luckock, F. Mainardi, M. Mantelli and M. Raberto, Quantitative Finance 4, 695 (2004).

- (8) S. Kurihara, T. Mizuno, H. Takayasu and M. Takayasu, The Application of Econophysics, H. Takayasu (Ed.), pp. 169-173, Springer (2003).

- (9) T. Kaizoji and M. Kaizoji, Physica A 336, 563 (2004).

- (10) E. Scalas, Physica A 362, 225 (2006).

- (11) N. Sazuka, Eur. Phys. J. B 50, 129 (2006).

- (12) N. Sazuka, Physica A 376, 500 (2007).

- (13) http://moneykit.net/

- (14) G. Rangarajan and M. Ding, Phys. Rev. E 62, 120 (2000).

- (15) G. Rangarajan and M. Ding, Phys. Lett A. 273, 322 (2000).

- (16) G. Rangarajan and M. Ding, Fractals 8, 139 (2000).

- (17) R. Durrett, Essentials of Stochastic Processes, Springer-Verlag New York (1999).

- (18) R. Chikara and L. Folks, The Inverse Gaussian Density, Dekker, New York (1989).

- (19) W. Gerstner and W. Kistler, Spiking Neuron Models, Cambridge University Press (2002).

- (20) R.N. Mantegna and H.E. Stanley, Phys. Rev. Lett. 73, 2946 (1994).

- (21) R.N. Mantegna, Phys. Rev. E 49, 4677 (1994).

- (22) I. Koponen, Phys. Rev. E 52, 1197 (1995).

- (23) R.N. Mantegna and H.E. Stanley, An Introduction to Econophysics : Correlations and Complexity in Finance, Cambridge University Press (2000).

- (24) H. Risken, The Fokker-Plank Equation: Methods of Solution and Applications, Springer-Verlag, Berlin; New York (1989).

- (25) C.W. Gardiner, Handbook of Stochastic Methods, Springer-Verlag, Berlin; New York (1983).

- (26) K. Umeno, Phys. Rev. E 58, 2644 (1998).

- (27) W. Schoutens, Lvy Processes in Finance: Pricing Financial Derivatives, Wiley, New York (2003).

- (28) S.I. Boyarchenko and S.Z. Levendorskii, Generalizations of the Black-Scholes equation for truncated Lvy processes, Working paper (1999).

- (29) J. Voit, The Statistical Mechanics of Financial Markets, Springer (2001).

- (30) T. Koren, A.V. Chechkin and J. Klafter, Physica A 379, 10 (2007).