Correlated Binomial Models and Correlation Structures

Abstract

We discuss a general method to construct correlated binomial distributions by imposing several consistent relations on the joint probability function. We obtain self-consistency relations for the conditional correlations and conditional probabilities. The beta-binomial distribution is derived by a strong symmetric assumption on the conditional correlations. Our derivation clarifies the ’correlation’ structure of the beta-binomial distribution. It is also possible to study the correlation structures of other probability distributions of exchangeable (homogeneous) correlated Bernoulli random variables. We study some distribution functions and discuss their behaviors in terms of their correlation structures.

pacs:

02.50.CwI Introduction

Incorporation of correlation into Bernoulli random variables taking the value 1 with probability and taking the value 0 with probability has long history and have been widely discussed in a variety of areas of science, mathematics and engineering. Writing the expectation value of a random variable as , the correlation between and is defined as

| (1) |

If there are no correlation between the random variables, the number of the variables taking the value 1 obeys the binomial probability distribution b. The necessity of the correlation comes from the facts that there are many phenomena where dependency structures in the random events are crucial or are necessary for the explanation of experimental data.

For example, in biometrics, the teratogenic or toxicological effect of certain compounds was studied Griffiths ; Williams ; Kupper . The interest resides in the number of affected fetuses or implantation in a litter. One parameter models, such as the Poisson distribution and binomial distributions provided poor fits to the experimental data. A two-parameter alternative to the above distributions, beta-binomial distribution (BBD), has been proposed Griffiths ; Williams . In the model, the probability of the binomial distribution b is also a random variable and obeys the beta distribution Be.

| (2) |

The resulting distribution has probability function

| (3) |

The mean and variance of the BBD are

| (4) |

where

| (5) |

is a measure of the variation in and is called as “correlation level” Bakkaloglu . The case of pure binomial distribution corresponds to . However, true “correlation” of the BBD is given as

| (6) |

The derivation of the relation is straightforward. If we denote the sum of as , we can write as and . From eq.(1) and the results for BBD, we obtain eq.(6). We rewrite the variance as

| (7) |

In the area of computer engineering, in the context of the design of survivable storage system, the modeling of the correlated failures among storage nodes is a hot topic Bakkaloglu . In addition to BBD, a correlated binomial model based on conditional failure probabilities has been proposed. The same kind of correlated binomial distribution based on conditional probabilities has also been introduced in financial engineering. There, credit portfolio modeling has been extensively studied Schonbucher ; Frey . In particular, the modeling default correlation plays central role in the pricing of portfolio credit derivatives, which are developed in order to manage the risk of joint default or the clustering of default. As a default distribution model for homogeneous (exchangeable) credit portfolio where the assets’ default probabilities and default correlations are uniform and denoted as and , Witt has introduced a correlated binomial model based on the conditional default probabilities Witt . Describing the defaulted (non-defaulted) state of i-th asset by and the joint default probability function by , are defined as

| (8) |

Here means the expectation value of a random variable under the condition that is satisfied. The expectation value of signifies the default probability and the condition corresponds to the situation where the first assets among are defaulted. and from the homogeneity (exchangeability ) assumption, any assets among can be chosen in the default condition . in eq.(8) is also substituted by anyone which is not used in the default condition.

In order to fix the joint default probability function completely, it is necessary to impose conditions on them from the homogeneity assumption. Witt and the authors have imposed the following condition on the conditional correlations Witt ; Mori .

Here Corr means the correlation between the random variable and under the condition is satisfied. From them, recursive relations for are obtained and are calculated as

The joint default probability function and the default distribution function has been expressed with these explicitly. However, the expression has many contributions and it is not an easy task to evaluate them for . In addition, the range of parameters and are also restricted and one cannot study the large correlation regime. Furthermore, for case, the distribution does not have the symmetry as . The distribution has irregular shape and for some choice of parameters, it shows singular rippling.

In this paper, we propose a general method to construct correlated binomial models (CBM) based on the consistent conditions on the conditional probabilities and the conditional correlations. With the method, it is possible to study the correlation structure for any probability distribution function for exchangeable correlated Bernoulli random variables. The organization of the paper is as follows. In section II, we introduce conditional probabilities and conditional correlations and show how to construct CBMs. We prove that the construction is self-consistent. In addition, in order to assure the probability conservation or the normalization, the conditional correlations and the probabilities should satisfy self-consistent relations. We also calculate the moments of the model. In the course, we introduce a linear operator which gives the joint probabilities in the “binomial” expansion of . Section III is devoted to some solutions of the self-consistent relations. We obtain the beta-binomial distribution (BBD) with strong symmetric assumptions on the conditional correlations. For other probability distribution functions which include the Witt’s model and the distributions constructed by the superposition of the binomial distributions (Bernoulli mixture model), we calculate and . We study the probability distribution functions for these solutions from the viewpoint of their correlation structures . We conclude with some remarks and future problems in section IV.

II Correlated Binomial Models and Their Constructions

In this section, we construct the joint probabilities and the distribution functions of CBMs. We introduce the following definitions. The first one is the products of and and they include all observables of the model.

| (9) |

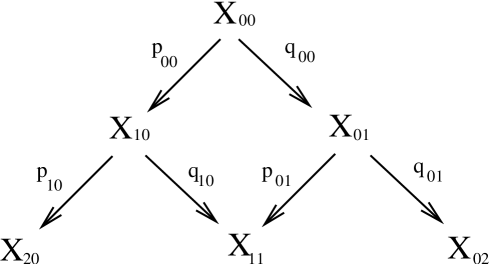

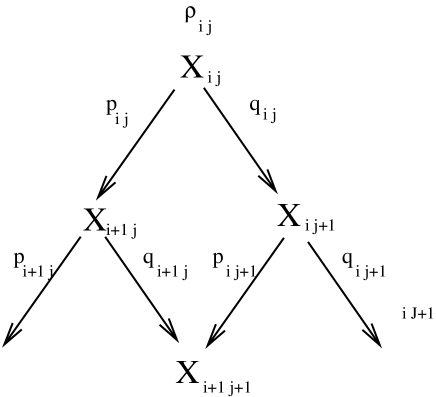

The following definitions are their unconditional and conditional expectation values (see Figure 1.).

| (10) | |||||

| (11) | |||||

| (12) |

, and . Furthermore, the relation should hold for any , because of the identity . All informations are contained in . The joint probability with is given by and the distribution function is also calculated as

| (13) |

In order to estimate , we need to calculate the products of and from to . As the path, we can choose anyone and the product must not depend on the choice. This property is guaranteed by the next condition on and as

| (14) |

In order for and to satisfy these conditions, we introduce the following conditional correlations

| (15) |

We set . and are also correlated with the same strength and the following relations hold.

| (16) |

From these relation, we obtain the recursive relations for and as

| (17) |

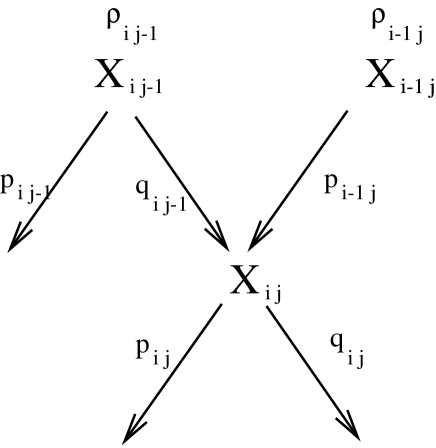

If we assume the identity , we obtain , and . Then holds and we see that the above consistency relation (14) does hold.

The remaining consistency relations or the probability conservation identity is . We prove the identity by the inductive method. For , the identity holds trivially as . For or , and are calculated as and and the identity also holds trivially. Then we assume and prove the identity . From the recursive equations (17) on and , we have the following relations.

| (18) |

For the identity to be satisfied, the conditional correlation and must satisfy the following relations.

| (19) |

If the conditional correlations are fixed so as to satisfy the relations, the model becomes self-consistent. In other words, it guarantees the normalization of the resulting probability distribution.

We estimate the moments of CBM. For the purpose, we introduce following operators and . The former one is a linear operator which maps polynomial in to joint probabilities . By its linearity, we only need to fix its action on monomial as

| (20) |

The joint probability is expressed as . Here we choose the far left path from to on the Pascal’s triangle (See Figure 1). The action of on the binomial expansion can be interpreted as the probability distribution and its normalization condition.

| (21) |

In order to calculate the moments of CBM, it is necessary to put in the above summation. Instead, we will put and introduce the following differential operators .

| (22) |

The action of on for is

| (23) |

On the other hand, the same expression can be obtained as

| (24) |

This relation defines the action of on the operator with any polynomial as

| (25) |

The calculation of the expectation value of is performed by the action of operator on the binomial expansion of .

| (26) |

The right hand side is nothing but the expectation value . The left hand side is calculated by using eq.(25) as

| (27) | |||||

We obtain the relation,

| (28) |

From the relation, we can estimate the moments of CBM.

III Beta-binomial Distribution and Other Solutions

In the previous section, we have derived self-consistent equations for and . They are summarized as

| (29) | |||||

| (30) | |||||

| (31) |

In this section, we show several solutions to these equation. We note, if one knows joint probabilities , from the definitions for and , we can estimate . Then are estimated from the recursive equation (29). In addition, we interpret the behaviors of the solutions from the viewpoint of correlation structures.

III.1 Beta-binomial Distribution

In order to solve the above relations on and , we use the symmetry viewpoint. For case, the model should have particle-hole duality between and or symmetry. Then should hold. We put stronger assumption that for any , the system has the symmetry and depends on only through the combination . With a suitable choice of indexes and , eq.(31) reduces to

| (32) |

From this relation, we see that with the same consist a arithmetic sequence with the common difference .

| (33) |

satisfy the following equation

| (34) |

can be solved with as

| (35) |

From the relation (29) for , we obtain the following recursive relation for as,

| (36) |

The explicit form for and are

| (37) |

Then and can be obtained explicitly and the results are

| (38) | |||||

| (39) |

are then obtained by taking the products of producing these conditional probabilities from to

| (40) |

Putting the above results for and into them, we obtain

| (41) |

Here . By multiplying the binomial coefficients , we obtain the distribution function as

| (42) |

This distribution is nothing but the beta-binomial distribution function (see eq.(3)) with suitable replacements .

III.2 Moody’s Correlated Binomial Model

In the original work by Witt, he assumed for all Witt . We call this model as Moody’s Correlated Binomial (MCB) model. The above consistent equations are difficult to solve and the available analytic expressions are those for as . With the result, we only have a formal expression for as

| (43) | |||||

With this expression, it is possible to estimate , and from their definitions. However, equation (43) contains and as becomes large, it becomes difficult to estimate them. With the above choice for , it is possible to set . If damps as with some positive , we can set at most for small values of and .

III.3 Mixed Binomial Models: Bernoulli Mixture Models

Bernoulli mixture model with some mixing probability distribution function , the expression for the joint probability function is calculated with

| (44) |

If we use the beta distribution for , we obtain eq.(41). However, this does not mean that it is trivial to solve the consistent equations with the assumption and obtain the BBD. The consistent equations completely determine any correlated binomial distribution for exchangeable Bernoulli random variables. Every correlated binomial distributions obey the relations. With the assumption , we are automatically lead to the BBD. That is, the probability distribution with the symmetry , we prove that it is the BBD. No other probability distribution has the symmetry.

Here we consider the relation between CBM and Bernoulli Mixture model. According to De Finetti’s theorem, the probability distribution of any infinite exchangeable Bernoulli random variables can be expressed by a mixture of the binomial distribution DeFinetti . CBM in the limit should be expressed by such a mixture. From eq.(44), we have the relation . is expressed as , we have a correspondence between the moments of and a CBM. That is, if one knows for any , we know the mixing function and vice versa. This correspondence shows the equivalence of CBM and the Bernoulli mixture model in the large limit. But CBMs with finite can describe probability distribution more widely. In the Bernoulli mixture model, the variance of is positive and the correlation cannot be taken negative. In CBM, we can set negative for small system size . In addition, CBM is useful to construct the probability distribution and discuss about the correlation structure. Particularly we can understand the symmetry of the solution. For example, we want to have symmetry distributions. In the Bernoulli mixture model, we need to impose on as

| (45) |

where . On the other hand, in CBM, we only need to seek a solution with . This simple constraint is useful in the construction and in the parameter calibration of CBMs.

As other mixing functions , we consider the cases which correspond to the long-range Ising model with some strength of magnitude of correlation . It has some correlation only in the regime where the probability distribution for the magnetization has two peaks at for Kitsukawa . If the system size is large enough, the distribution can be approximated with the superposition of two binomial distributions. If we take for , the system loses its ergodicity and the phase space breaks up into two space with and Goldenfeld and the correlation disappears. Even if there appears two peaks in , only one of them represents the real equilibrium state.

The precise values of and depend on the model parameters, we consider the cases which correspond to ( symmetric case) and . For the symmetric case, there is no external field and holds. Between the Bernoulli random variable and the Ising Spin variable , there exists a mapping . has two peaks at and with the same height. On the other hand, for and infinitely weak positive external field case , has one tall peak at and another short peak at . In the language of the Bernoulli random variable case, has a tall peak at and a short peak at . We consider the following mixing functions and call them Two-Binomial models.

-

•

with .

This mixing function corresponds to the long-range Ising model with symmetry and . are given as

(46) and are calculated easily as

(47) (48) This solution has the symmetry .

-

•

with .

This is the modified version of the above solution with a parameter . If we set , it is nothing but the above solution. are given as

(49) and are

(50) (51) If we denote , , then the mixing function becomes . This solution may look trivial. One obtain this solution using the parallel shift of the above solution (46). We replace with in eq.(46) and obtain the solution. Such a parallel shift may give birth to another solution, we would like to note it here.

-

•

.

This mixing function corresponds to the long-range Ising model without symmetry, and . We call the model as Binomial plus (B+) model, because it is a binomial distribution plus one small peak at . Between and , we have the relations

(52) and

(53) are given as

(54) and are calculated easily as

(55) and

(56)

III.4 Correlation Structures of the Solutions

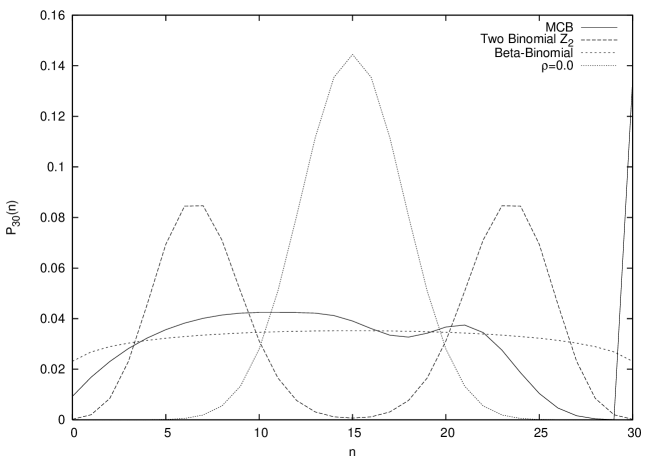

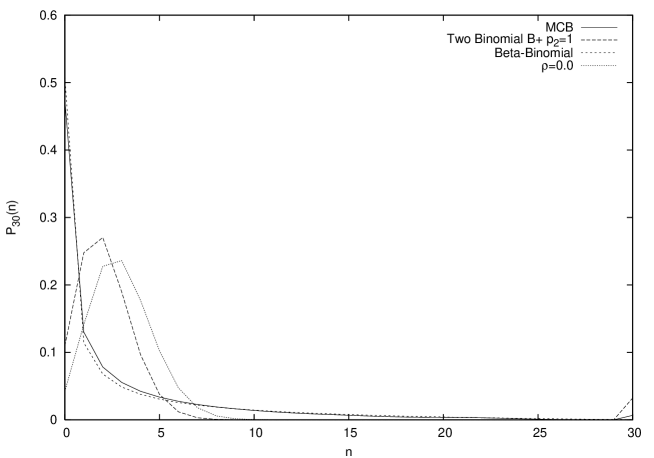

In this subsection, we study the relations between probability distributions and correlation structure. Figure 4 shows the probability distribution profiles for three correlated models, MCB, BBD and Two-Binomial models. We set , and . We also shows the pure binomial distribution for comparison. The former three curves have the same and , however their profiles are drastically different. Two binomial model with symmetry has two peaks and their overlaps decreases as increases. At the thermodynamic limit , the overlap disappears and the system loses its ergodicity. The long-range Ising models shows spontaneous symmetry (SSB) breaking of the symmetry . On the other hand, the BBD’s profile is broad and even if we set , we obtain the beta distribution and the shape is almost unchanged. That is, the BBD system does not show SSB and it maintain its (particle-hole) symmetry at .

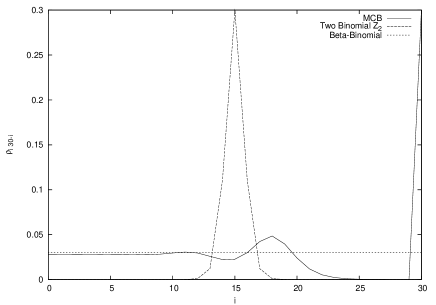

The profile of MCB model is peculiar. It is not symmetric and shows singular rippling. The origin for the ripping can be understood from the inspection of its correlation structure. Figure 5 shows the correlation structures for the above three models. The parameters are equal and we show . In contrast to the BBD’s correlation, which is constant with fixed, the correlations for MCB has sharp peak at and show strong rippling structure. The curve is not symmetric and the distortion is reflected in the shape of its probability distribution. On the other hand, the correlation curve for Two-binomial distribution has a strong peak at and is it much different from the BBD’s correlation curve. This strong peak and rapid decay may be reflected in the decomposition of the probability distribution. However, we have not yet understood the relation well.

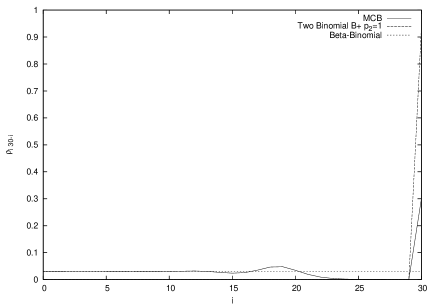

Figure 6 shows the probability distribution for MCB, BBD and B+ models. We set , and . We also shows the pure binomial distribution for comparison. MCB and BBD have almost the same bulk shape, however MCB has a small peak at . B+ has more strong peak at and its bulk shape can be obtained by a small left shift of the pure binomial distribution . These profile differences are reflected in their correlation structures. See Figure 7. It shows the correlation structures for the above three models. The parameters are equal as in the previous figure. Contrary to the constant BBD structure, MCB and B+ models have a peak at . MCB has a small and B+ has a tall peak and the difference is reflected int the size of their tail peak of the probability distributions.

IV Concluding Remarks and Future Problems

In this paper, we show a general method to construct correlated binomial models. We also estimate their moments. Our method includes Witt’s model and the BBD. In addition, with the consistent equations on and , it is possible to prepare correlated binomial distributions with any choice for or . Of course, the resulting distribution function should be non-negative , ’any’ should be taken with some care. In addition, from the joint probabilities , it is possible to estimate and . We can see the detailed structure of the system with any distribution function. In the work Bakkaloglu , the conditional strange failure probabilities were studied. Some recursive relations on were proposed and the resulting conditional probabilities were compared with real data on server networks. We note that can be freely changed and it may be possible to make a good fitting with data. However, if the correlation structure becomes too complex and it shows oscillation, such a modeling may be over-fitting.

At last, we make comments about future problems. The first one is to seek another interesting solution to eq.(29), eq.(30) and eq.(31) about and . In this paper, we have assumed strong symmetry in in the derivation of the BBD. For any value of , we have assumed symmetry . Furthermore, we have assumed stronger constraint that depends on only through the combination . The consistent relation is then solved easily and we get the BBD. However, we think that the correlated binomial distribution space is rich and there may exist other interesting solutions. We discuss some simple solutions which are superpositions of two binomial distribution. They try to mimic the long-range Ising model in the large limit and Kitsukawa . A simple seamless solution for the consistent relations which correspond to the long-range Ising model may exist. Taking the continuous limit of the consistent relations and studying their solution is also an interesting problem. The solution space may become narrow, however differential equations are more tractable than the recursion relations. There should exist the beta distribution and the superposition of delta-functions, which are the continuous limits of the simple solutions presented here.

The second problem is the generalization of the present method. In this paper, we have assumed that the Bernoulli random variables are all exchangeable. If one consider to apply the correlated binomial model to the real world, such an idealization should be relaxed. One possibility is the inhomogeneity in and the other is the inhomogeneity in . The first step is to add one other Bernoulli random variable to exchangeable variable system. This system case has been treated in Mori , it seems much difficult to introduce the self-consistent equations in the present context. However, such a generalization may lead us to find new probability distribution functions, we believe that it deserves for extensive studies.

References

- (1) D.A.Griffiths, Biometrics 29 637 (1973).

- (2) D.A.Williams, Biometrics 31 949 (1975).

- (3) L.L.Kupper and J.K.Haseman, Biometrics 34 69 (1978).

- (4) M.Bakkaloglu et al, Technical Report CMU-CS-02-129, Carnegie Mellon University (2002).

- (5) P.J.Schönbucher Credit Derivatives Pricing Models : Model, Pricing and Implementation, U.S. John Wiley & Sons (2003).

- (6) R. Frey and A. J. McNeil, Journal of Risk, 6 59 (2003).

- (7) G.Witt, Moody’s Correlated Binomial Default Distribution (Moody’s Investors Service)August 10 (2004).

- (8) S.Mori, K.Kitsukawa and M.Hisakado, Moody’s Correlated Binomial Default Distributions for Inhomogeneous Portfolios, submitted to Quantitative Finance, arXiv:physics/0603036.

- (9) K.Kitsukawa, S.Mori and M.Hisakado, Evaluation of Tranche in Securitization and Long-range Ising Model, to be published in Physica A (2006), arXiv:physics/0603040.

- (10) De Finetti, Theory of Probability, Wiley (1974-5).

- (11) N. Goldenfeld, Lectures on Phase Transitions and the Renormalization Group, Addison-Wesley Publishing Company (1992).