MARKET MILL DEPENDENCE PATTERN IN THE STOCK MARKET: DISTRIBUTION GEOMETRY, MOMENTS AND GAUSSIZATION

Andrei Leonidov(a,b,c)111Corresponding author. E-mail leonidov@lpi.ru, Vladimir Trainin(b),

Alexander

Zaitsev(b), Sergey Zaitsev(b)

(a) Theoretical Physics Department, P.N. Lebedev Physics Institute,

Moscow, Russia

(b) Letra Group, LLC, Boston, Massachusetts, USA

(c) Institute of Theoretical and Experimental Physics, Moscow, Russia

Abstract

This paper continues a series of studies devoted to analysis of the bivariate probability distribution of two consecutive price increments (push) and (response) at intraday timescales for a group of stocks. Besides the asymmetry properties of such as Market Mill dependence patterns described in preceding paper [1], there are quite a few other interesting geometrical properties of this distribution discussed in the present paper, e.g. transformation of the shape of equiprobability lines upon growing distance from the origin of plane and approximate invariance of with respect to rotations at the multiples of around the origin of plane. The conditional probability distribution of response is found to be markedly non-gaussian at small magnitude of pushes and tending to more gauss-like behavior upon growing push magnitude. The volatility of measured by the absolute value of the response shows linear dependence on the absolute value of the push, and the skewness of is shown to inherit a sign of the push. The conditional dynamics approach applied in this study is compared to regression models of AR-ARCH class.

1 Introduction

Intensive investigations over recent decades have revealed statistically significant deviations from an assumption of independent identically distributed (IID) increments that underlies the random walk model of stock price dynamics. A direct statistical evidence showing significant deviations from IID using a BDS test [2] was presented in [3]. The rejection of the IID hypothesis also follows from the volatility - based test described in [4]. There is a number of dependence patterns showing themselves in such stylized facts as statistically significant autocorrelations at intraday timescales, volatility clustering, leverage effect, etc. [4, 5, 6, 7], as well as correlations between simultaneous increments of different stocks. Each of these effects corresponds to some sort of probabilistic dependence between the lagged and/or simultaneous price increments and their moments.

In a series of papers [1, 8, 9] including the present one we study further evidence of the presence of dependence patterns in financial time series. An approach we apply is based on the direct analysis of the multivariate probability distributions of simultaneous and lagged price increments for both single stocks and a basket of stocks. A simplest case we concentrate upon is that of the bivariate distribution describing the interdependence of two price increments in two coinciding or non-overlapping time intervals. We also consider a natural and transparent interpretation of the bivariate probability distribution provided by its sections corresponding to the fixed value of one of the variables, i.e. conditional distributions.

Despite their fundamental importance, multidimensional probability distributions of stock price returns (increments) are, to the best of our knowledge, not widely used. The bivariate distribution of returns in two consecutive intervals was analyzed, in the particular case of Levy-type marginals, in [10], where some interesting geometric features of this distribution both for the case of independent and dependent returns were described. As discussed in [11], the bivariate distribution in question can be considered as a ”fingerprint” reflecting the nature of the pattern embracing the two consecutive returns. Let us also mention the ”compass rose” phenomenon [12, 13, 14] and the discussion of return predictability in [12] and [14]. Another line of research is an explicit analytical reconstruction of the bivariate distribution in question using copulas, see e.g. [15, 16, 17, 18]. There is a few studies devoted to a direct analysis of the conditional distributions. Recently an analysis of volatility dynamics exploiting such conditional distributions was described in [19]. The first moment of the corresponding conditional distribution for daily time intervals was studied in [20].

At the same time the main focus of the efforts to quantify the conditional dynamics of financial instruments was on constructing and studying the regression models, see e.g. [6, 21, 22, 23, 24, 25, 26, 27, 28, 29, 30]. Each of these models realizes a particular version of the conditional dynamics, in which parameters of the conditional distribution describing the forthcoming increment depend on lagged increments and moments. In the simplest version of ARCH model [6, 22] this conditional distribution is gaussian with a standard deviation depending on the magnitude(s) of one or more lagged increments. In GARCH models [6, 23] the conditional standard deviation depends on lagged standard deviation as well. As such conditionally gaussian approach did not allow to describe an observed degree of fat-tailedness of the increments, further development included considering fat-tailed conditional distributions [25] and, in modern versions [27, 28, 29, 30], the fat-tailed and skewed conditional distributions in which fat-tailedness and skewness are conditional as well. A case of nonlinear dependence of the conditional mean of forthcoming increment on lagged increments could most naturally be treated within a class of threshold autoregressive models [21].

An approach based on constructing regression type models is, by definition, a parametric one. Assuming some specific form of increment dynamics one runs statistical tests to determine optimal values of the parameters in question. Our approach [1, 8, 9] is, on contrary, inherently non-parametric. We do not use any assumptions on the particular form of probabilistic links between price increments. The analysis of price dynamics is made in terms of direct examination of the observed multivariate probability distributions.

In our study of dependence patterns in stock price dynamics [8] a direct examination of the moments of the bivariate distributions linking consecutive returns of a stock and simultaneous returns of a pair of stocks was performed. It was shown that some empirical features of the bivariate distribution in question, e.g. conditional volatility smile, result from non-gaussian nature of the distirbution.

In the preceding paper [1] we analyze the asymmetry properties of the bivariate probability distribution of two consecutive stock price increments (push) and (response) resulting in remarkable market mill dependence patterns. In the present paper we continue the analysis of [1, 8] by a more close inspection of the properties of the full bivariate distribution of increments and the conditional distribution of the response . Therefore, despite the fact that we do not discuss specifically the market mill properties in the present paper, this paper still belongs to the series of studies [1, 8, 9] under the umbrella title - ”Market mill dependence pattern …”.

The paper is organized as follows. In paragraph 2.1 we describe the dataset and the probabilistic methodology used in our analysis.

A detailed description of the results is given in paragraph 2.2. In 2.2.1 we study geometrical properties of the full bivariate probability distribution . First we show that the shape of the equiprobability lines of the distribution changes upon growing distance from the origin of plane. Another property of is its approximate invariance with respect to rotations at the multiple of around the origin of plane. In 2.2.2 we switch to studying properties of the conditional probability distribution and find that the volatility of measured by the absolute value of the response shows linear dependence on the absolute value of the push, and the skewness of inherits a sign of the push.

In the discussion section of the paper we first concentrate on non-gaussian properties of both the full bivariate distribution and conditional one (see paragraph 3.1). We discuss that the conditional distribution tends to more gauss-like behavior upon growing magnitude of the push.

Our studies of the bivariate distribution are, by default, also studies of a special version of the conditional dynamics in which information on the value of a price increment is fully accounted for in describing the probabilistic pattern characterizing the next increment. It is therefore of direct interest to compare our results with the ones obtained within the regression model approach. This is done in section 3.2 of the paper.

The paragraph 4 finalizes the paper by describing main conclusions and outlook of the future studies.

2 Properties of push - return distribution

An analysis of the properties of the push - return distribution described in the present paragraph continues the study initiated in [1]. It goes into further details in describing the unique properties of the geometry of the bivariate probability distribution under consideration and analyzes moments of the corresponding conditional distribution 222Although an analysis of the properties of the bivariate probability distribution and the corresponding conditional distribution presented in the present paper is self-contained, we strongly refer to [1] for a more comprehensive picture..

2.1 Data and methodology

Our study of high frequency dynamics of stock prices is based on data on the prices of 100 stocks traded in NYSE and NASDAQ in 2003-2004 sampled at 1 minute frequency333The list of stocks is given in the Appendix.

Let us consider two non-overlapping time intervals of length and , where the interval immediately follows after . We shall denote the price increment in the first interval (push) by and that in the second one (response) by . In this study we consider 1 min., 3 min., 6 min. The full probabilistic description in plane is given by the bivariate probability density . An analysis of the full bivariate distribution is often facilitated by considering its cross-sections corresponding to conditional distributions such as, e.g., the conditional distribution of response at given push .

Let us stress that our data set combines pairs of price increments for all stocks belonging to the specified group (see Appendix), so that a set of events (pairs of increments) unifies all subsets of events characterizing individual stocks. A further detailed study of general features of the probability distributions and constitutes the main topic of the present paper and comprehends the analysis of [1] .

Let us note that analogously to [1] in our analysis we use price increments. The results obtained using returns are in qualitative agreement to the ones discussed in the present paper.

2.2 Structure of the bivariate distribution

Let us discuss properties of the bivariate distribution .

2.2.1 Global two-dimensional geometry. Invariance with respect to rotations.

The two-dimensional projection of in case of two adjacent 1-minute intervals is shown

in Fig. 1. To facilitate a discussion of some qualitative features seen in Fig. 1, let us sketch profiles of the equiprobability levels of in Fig. 2,

where the plane is divided into sectors numbered counterclockwise from I to VIII. The shape of equiprobability lines shown in Figs. 1,2 can be described as a superposition of a basic regular pattern, rhomboid in the vicinity of the origin and circular away from it, perturbed in such a way that each of the even sectors (II,IV,VI,VIII) contains more probability density than each of the odd ones (sectors I,III,V,VII). The geometry of unperturbed basic regular pattern (shown in brown in Fig. 2) can be described as

| (1) |

where in the vicinity of the origin and far away from it.

An interesting property of the bivariate distribution is its approximate invariance with respect to rotations at the multiples of . The distribution geometry is quite nontrivial: as already mentioned, all even sectors contain more probability density than the odd ones 444The nontrivial asymmetric properties of the distribution leading to the market mill structure and z-shaped structure of the conditional mean response was analyzed in full details in [1]. . In terms of sample paths (pairs of increments) composed by increments and the exact symmetry with respect to rotations at multiples of leads to the following chain of equalities:

| (2) |

An approximate character of the symmetry with respect to rotations at multiples of shows itself in varying degree of proximity of the corresponding distributions. To give a quantitative estimate of this proximity we consider three bivariate probability distributions , and obtained by rotating the original distribution at an angle , where . To compute a distance between two matrices corresponding to distributions and obtained by rotations of at and respectively we flatten each of them into a vector, normalize it and compute a distance between these vectors using the (”Manhattan”) metric555In this estimate we restrict our consideration to the domain .. We find

| (3) | |||||

| (4) |

and

| (5) |

Therefore we see that the rotation at is a ”better” symmetry of the full distribution than the rotation at implying, in turn, that equality holds to a better accuracy than .

2.2.2 Geometry of response profile

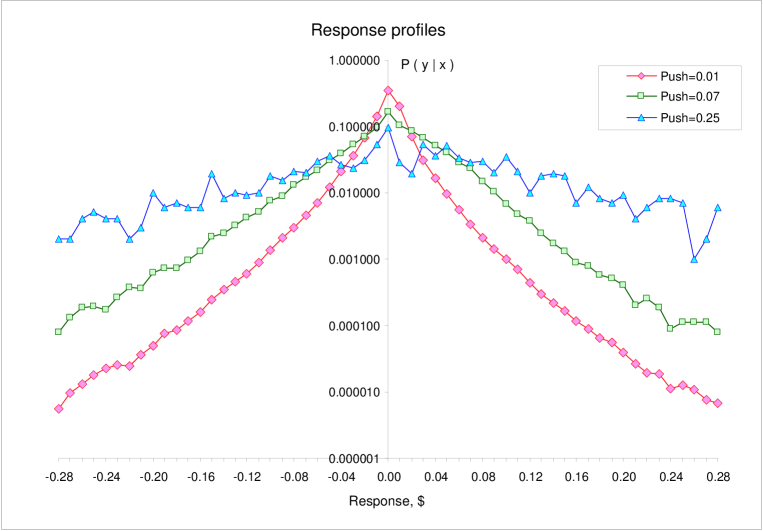

A detailed view on the distribution is provided by examining the corresponding conditional distributions such as, e.g., describing the probabilistic shape of response at given push . In Fig. 3 we plot three cross-sections of the surface corresponding to and .

We observe a clear change in the structure of the response with growing push. Qualitatively this change can be described by evolution of the parameter in the stretched exponential distribution from at small to at large , so that the distributions looks evolving from the squeezed tent-like at small pushes to almost gaussian at large ones. Note that this interpretation is consistent with the suggested description of the geometry of equiprobablity lines in Eq. (1).

2.2.3 Moments of conditional distribution

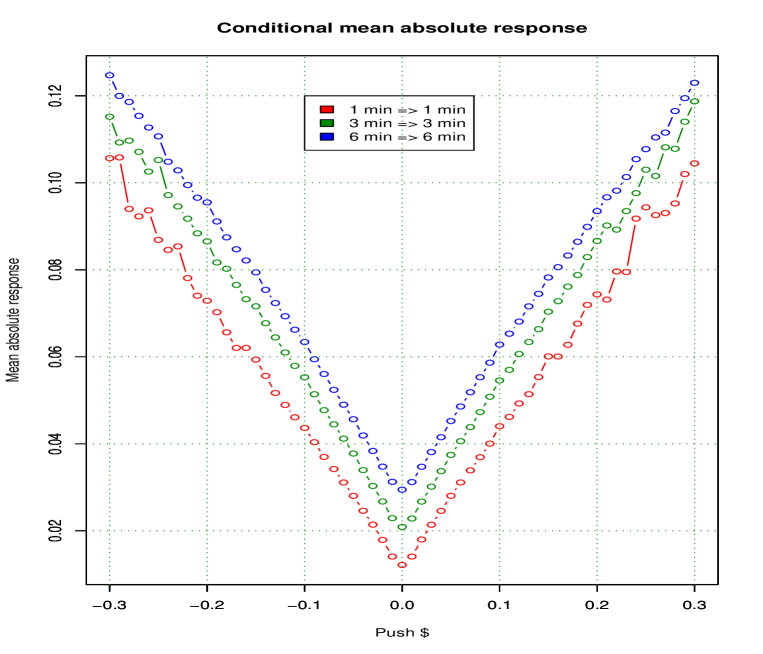

Let us first consider a useful quantitative characteristics of a shape of the distribution , the conditional mean absolute response

| (6) |

The dependence of on the push is plotted in Fig. 4.

We see that to a good accuracy the mean absolute response is linear in the absolute value of the push, . Let us recall that the mean response is a nonlinear function of the push [1]. As the absolute response is a robust measure of volatility, in Fig. 4 we have an example of conditional volatility smile or dependence volatility smile that was studied, in terms of a standard deviation of normalized returns, in [8]. The dependence of on describes how much of response volatility is created for a given push.

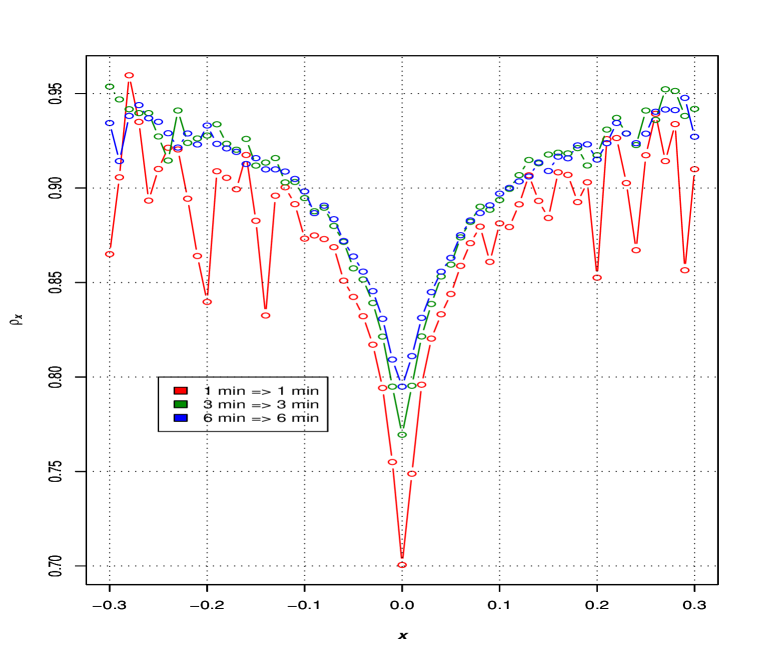

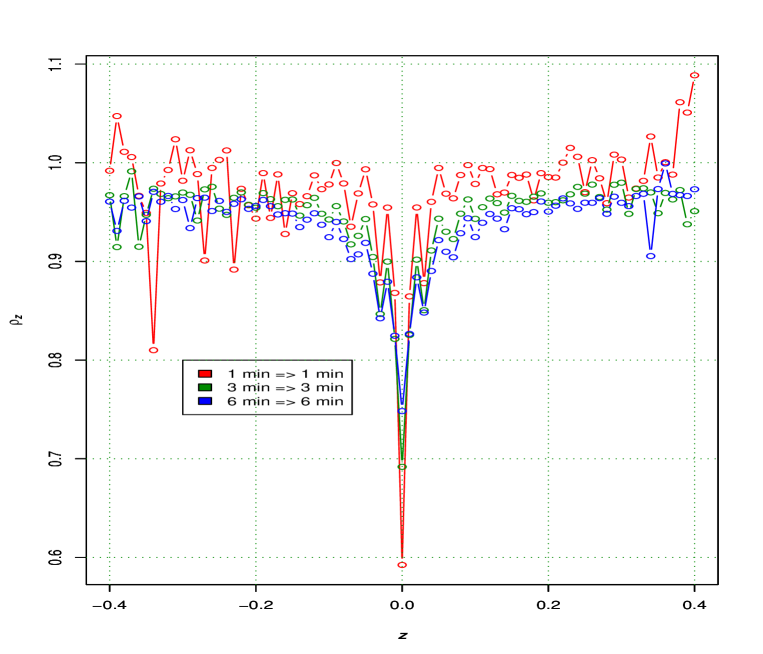

Because of the sensitivity of the mean conditional absolute response to the higher moments of the conditional distribution one can, by comparing it to the value obtained for the Gaussian distribution with the same standard deviation, gauge the deviation of the distribution in question from the Gaussian [7]. Let us thus consider the following ratio:

| (7) |

where and is an observed standard deviation of the corresponding conditional response. The ratio is plotted, in three cases of consecutive 1 - minute, 3 - minute and 6 - minute intervals in Fig. 5

The pattern seen in Fig. 5 unambiguously shows the progressive ”gaussization” of the response profile with growing push. This is a highly nontrivial property of the distribution . The same question can be addressed by computing the anomalous kurtosis of the conditional distribution. The results obtained for anomalous kurtosis support the conclusion on ”gaussization” but are rather noisy, especially for the case of 1 minute intervals.

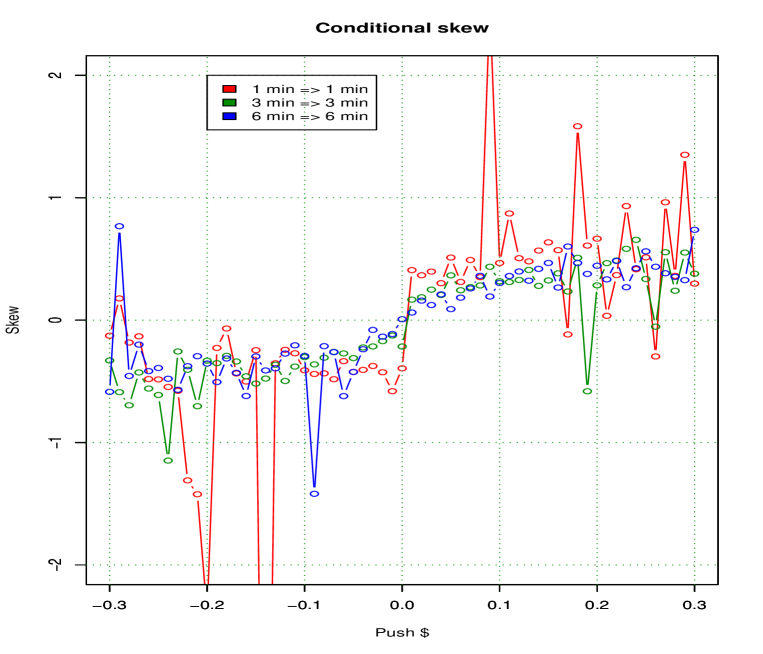

The mean absolute response by default characterizes the symmetric component of the conditional probability distribution with respect to the axis . Asymmetry of with respect to this axis is characterized by its odd moments. The first moment, the mean conditional response, was studied in detail in [1]. It was shown that the mean conditional response has a nontrivial zizgag-shaped dependence on the push. To probe the asymmetric contributions of higher order, let us consider the skewness of the conditional response666Here we assume that the third moment of the conditional distribution exists.

| (8) |

where is the conditional standard deviation of response at given push. In Fig. 6 we plot the skewness of the response for the same set of consecutive time intervals.

The pattern seen in Fig. 6 corresponds to an interesting phenomenon. The asymmetry of the distribution of conditional response characterized by skewness has the sign of the initial push, so that for negative pushes the response distribution is always negatively skewed, etc. Let us note that the same conclusion can be reached by considering a robust characteristics of distribution asymmetry, a difference between the median of the distribution and its mean.

The generic symmetry properties of the distribution are best revealed by considering its symmetry with respect to the axes and (patterns I – IV) [1]. The patterns are of two types: pattern I is equivalent to pattern III and pattern II is equivalent to pattern IV. Pattern I was analyzed above, so let us consider pattern II. To analyze the symmetry properties of the distribution with respect to the axis it is convenient to introduce the new variables

| (9) |

so that in this case one deals with the conditional distribution .

The dependence of the shape of on the ”push” can again be explored by considering the ratio

| (10) |

The ratio is plotted in Fig. 7.

The generic pattern is the same as in Fig. 5: the distribution is progressively more and more gaussian with growing . The shape is somewhat different though, so that the gaussization process is different in this case.

3 Discussion

In the previous section we discussed a number of properties characterizing the probabilistic dependence patterns relating stock price increments in consecutive time intervals. Our approach is based on the direct analysis of the bivariate probability distribution dependent on the two price increments in question and of the corresponding conditional distribution . We have concentrated on high frequency data with increments in time intervals of length 1 min., 3 min. and 6 min777The results of [1] show that it is reasonable to expect that all the features discussed in the present paper will hold at larger intraday time scales as well..

3.1 Gaussization of conditional distribution at large magnitudes of price increments

Let us first discuss in some more details a remarkable property of gaussization of multivariate distributions of price increments far away from the origin in the plane. A first hint comes from the analysis of the geometry of equiprobability levels of the push - response bivariate probability distribution . As seen in Fig. 1 and sketched in Fig. 2, the geometry of equibrobability lines changes from rhomboid in the vicinity of the origin to circular far away from it, which is consistent with distribution changing the shape from bivariate Laplace to bivariate gaussian one. This is, however, not a proof of gaussization: a Laplace distribution with standard deviation of growing with leads to the same visual pattern.

Quantitative proof of gaussization comes from considering the ratio defined in eq. (7) characterizing the shape of the conditional response distribution. In this ratio the effect of variable conditional standard deviation is factored out. We have checked the gaussization of the bivariate distribution along the two axes, and (see Figs. 5 and 7). The speed of gaussization turns out different, but the phenomenon itself is undoubtedly present in both cases.

3.2 Conditional dynamics: direct analysis of multivariate distribution vs regression models

Knowledge of full bivariate distribution fully specifies corresponding conditional distributions and, therefore, a particular variant of conditional dynamics. As already mentioned in the introduction, the main body of research on conditional dynamics in financial markets was done within a paradigm of regression models [6, 21, 22, 23, 24, 25, 26, 27, 28, 29, 30], in which conditional distribution for the forthcoming price increment depends on lagged increments and lagged conditional moments. In the simplest version of the AR(1)-ARCH(1) model [6, 22] the conditional distribution of the return is gaussian, , where conditional mean and conditional standard deviation depend on return in the previous interval, and . This setting is methodologically equivalent to the one considered in the present paper in the sense that the only information required for computing the conditional distribution for is the value of , so that the conditional dynamics of AR(1)-ARCH(1) is fully described by conditional distribution . To match the features described in the preceding [1] and present papers one would have to consider a nonlinear dependence of on and construct a fairly complicated fat-tailed skewed conditional probability distribution. Even forgetting for a moment about the z-shaped dependence of mean conditional response on the push, meaningful comparison could be with a version of ARCH(1) with a fat-tailed skewed conditional distribution. As to the zigzag-shaped dependence of the mean conditional response on the push, the most natural treatment could be given within a class of threshold autoregressive (TAR) models [21].

To compare our results with the properties of autoregressive models considered in the literature let us consider the AR(1)-GARCH(1,1) model [6, 23], particularly its versions with fat-tailed [25] and conditionally fat-tailed and skewed conditional distributions for residuals [26, 27, 28, 29, 30]. In these models conditional volatility is a function of both lagged returns and volatility, so a comparison with the results obtained using the bivariate distribution is not direct. With this remark in mind, let us make some comparison at the ”moment by moment” basis.

-

•

The conditional mean in the AR(1) model is by default a linear function of the push, . This is equivalent to an assumption of the ellipticity of the underlying bivariate distribution . As shown in [1], the intraday conditional dynamics is characterized by a fairy complex nonlinear z-shaped pattern of mean conditional response. To take this into account one should generalize AR(1) to TAR(1).

-

•

The conditional standard deviation in GARCH(1,1) models is a growing function of , . This is consistent with the dependence smile discussed in [8] and shown in Fig. 3.

-

•

The results obtained in the framework of generalized GARCH models for the conditional skewness [26, 27, 28, 29, 30] (only the daily timescale was considered) are somewhat contradictory. In [18, 27, 28, 29] a conclusion was that negative return is followed by negative conditional skew - in agreement with the results of the previous section, while no conclusion on the sign of conditional skew following the positive return was reached. At the same time, the conclusion of [30] was that the sign of conditional skew is always opposite to the sign of initial return.

-

•

The main result on conditional kurtosis obtained within the generalized GARCH approach was [28] that it is time dependent and not always existent. A comparison with our result on the progressive gaussization of the response distribution with growing magnitude of the push does not seem possible.

Our method of directly analyzing the conditional distribution allows to describe its properties in a model-independent framework. If analyzed from the point of view of regressive conditional dynamics the results described in the present paper and in the preceding paper [1] can be formulated as follows. The conditional dynamics is

-

•

nonlinear

-

•

heteroskedastic as seen in the volatility dependence smile

-

•

not conditionally gaussian

-

•

characterized by conditional skew depending on the lagged increment

-

•

characterized by conditional fat-tailedness that diminishes with growing magnitude of lagged increment

4 Conclusions and outlook

Let us formulate once again the main conclusions of the paper. Studying the geometry of the full bivariate probability distribution and the corresponding conditional distribution we have found that

-

•

The shape of equiprobability lines of the bivariate probability distribution changes from roughly rhomboid in the vicinity of the origin to roughly circular far away from it.

-

•

The conditional distribution is shown to become progressively more gaussian at increasing push magnitudes. Analogous gaussization takes place for conditional distribution considered with respect to the axis .

-

•

The bivariate distribution is approximately invariant with respect to rotations at multiples of

-

•

The conditional mean absolute response is linear in the absolute value of push

-

•

The skewness of the response distribution inherits a sign of the push

As was emphasized above in [1] and the present paper we study a combined ensemble of all pairs of consecutive price increments from all stocks. How is this overall geometry related to the geometric properties of individual stocks? Only after answering this question can one come close to describing the microscopic mechanism underlying the uncovered probabilistic dependence patterns. This issue is analyzed in the companion paper [9].

The work of A.L. was partially supported by the Scientific school support grant 1936.2003.02

5 Appendix

Below we list stocks studied in the paper:

A, AA, ABS, ABT, ADI, ADM, AIG, ALTR, AMGN, AMD, AOC, APA, APOL, AV, AVP, AXP, BA, BBBY, BBY, BHI, BIIB, BJS, BK, BLS, BR, BSX, CA, CAH, CAT, CC, CCL, CCU, CIT, CL, COP, CTXS, CVS, CZN, DG, DE, EDS, EK, EOP, EXC, FCX, FD, FDX, FE, FISV, FITB, FRE, GENZ, GIS, HDI, HIG, HMA, HOT, HUM, JBL, JWN, INTU, KG, KMB, KMG, LH, LPX, LXK, MAT, MAS, MEL, MHS, MMM, MO, MVT, MX, MYG, NI, NKE, NTRS, PBG, PCAR, PFG, PGN, PNC, PX, RHI, ROK, SOV, SPG, STI, SUN, T, TE, TMO, TRB, TSG, UNP, UST, WHR, WY

References

- [1] A. Leonidov, V. Trainin, S. Zaitsev, A. Zaitsev, ”Market Mill Dependence Pattern in the Stock Market: Asymmetry Structure, Nonlinear Correlations and Predictability”, arXiv:physics/0601098.

- [2] W. Brock, W. Dechert, J. Scheinkman, ”A test of independence based on the correlation dimension”, Working paper, University of Wisconsin at Madison, University of Houston and University of Chicago (1987).

- [3] D.H. Hsieh, ”Chaos and Nonlinear Dynamics: Application to Financial Marekts”, Journal of Finance 46 (1991), 1839-1878

-

[4]

A.C. MacKinlay, A.W. Lo, J.Y. Kampbell, The Econometrics of Financial Markets, Princeton, 1997;

A.W. Lo, A.C. MacKinlay, A Non-Random Walk Down Wall Sreet, Princeton, 1999 - [5] B. Mandelbrot, ”Fractal and Multifractal Finance. Crashes and Long-dependence”, www.math.yale.edu/mandelbrot/webbooks/wb_fin.html

- [6] A. Shiryaev, ”Essentials of Stochastic Finance: Facts, Models, Theory”, World Scientific, 2003

- [7] J.-P. Bouchaud, M. Potters, Theory of Financial Risk and Derivative Pricing, Cambridge, 2000, 2003.

- [8] A. Leonidov, V. Trainin, A. Zaitsev, ”On collective non-gaussian dependence patterns in high frequency financial data”, ArXiv:physics/0506072, submitted to Quantitative Finance

- [9] A. Leonidov, V. Trainin, A. Zaitsev, S. Zaitsev, ”Market Mill Dependence Pattern in the Stock Market: Individual Portraits”, in preparation

- [10] B. Mandelbrot, ”The Variation of Certain Speculative Prices”, Journal of Business 36 (1963), 394-419

- [11] B. Mandelbrot, R.L. Hudson, ”The (Mis)behavior of Prices: A Fractal View of Risk, Ruin, and Reward”. New York: Basic Books; London: Profile Books, 2004

- [12] T.F. Crack, O. Ledoit, ”Robust Structure Without Predictability: The ”Compass Rose” Pattern of the Stock Market”, The Journal of Finance 51 (1996), 751-762

- [13] A. Antoniou, C.E. Vorlow, ”Price Clustering and Discreteness: Is there Chaos behind the Noise?”, arXiv:cond-mat/0407471

- [14] C.E. Vorlow, ”Stock Price Clustering and Discreteness: The ”Compass Rose” and Predictability”, arXiv:cond-mat/0408013

- [15] P. Embrechts, A. McNeil, D. Straumann, ”Correlation and depenendence in risk management: properties and pitfalls”, Risk Lab working paper (1999)

- [16] P. Embrechts, P. Lindskog, A. McNeil, ”Modelling Dependence with Copulas and Applications to Risk Management”, Risk Lab working paper (2001)

- [17] Y. Malevergne, D. Sornette, ”Testing the Gaussian Copula Hypothesis for Financial Asset Dependencies”, ArXix:cond-mat/0111310

- [18] E. Jondeau, M. Rockinger, ”Conditional Dependency of Financial Series: an Application of Copulas”, Banque de France working paper NER 82 (2001)

- [19] K. Chen, C. Jayprakash, B. Yuan, ”Conditional Probability as a Measure of Volatility Clustering in Financial Time Series”, arXiv:physics/0503157

- [20] M. Boguna, J. Masoliver, ”Conditional dynamics driving financial markets”, ArXiv:cond-mat/0310217

- [21] H. Tong, K. Lim, ”Threshold autoregression, limit cycles and cyclical data”, Journal of the Royal Statistical Society B42 (1980), 245-292

- [22] R.F. Engle, ”Autoregressive Conditional Heteroskedasticity with Estimates of the Variance of United Kingdom Inflation”, Econometrica 50 (1982), 987-1007

- [23] R.F. Engle, T. Bollerslev, ”Nodelling the persistence of conditional variances”, Economics Reviews 5 (1986), 1-50

- [24] T. Bollerslev, ”Generalized autoregressive conditional heteroskedasticity”, Journal of Econometrics 31 (1986), 307-327

- [25] T. Bollerslev, ”A Conditionally Heteroscedastic Time Series Model For Speculative Prices Rates Of Return”, Review of Economics and Statistics 69 (1987), 542-547

- [26] B.E. Hansen, ”Autoregressive Conditional Density Estimation”, International Economic Review 35 (1994), 705-730

- [27] C.R. Harvey, A. Siddique, ”Autoregressive Conditional Skewness”, Journal of Finanical and Quantitative Analysis 34 (1999), 465-487

- [28] E. Jondeau, M. Rockinger, ”Conditional volatility, skewness, and kurtosis: existence and persistence”, Banque de France working paper NER 77 (2000)

- [29] P. Lambert, S. Laval, ”Modelling skewness dynamics in series of financial data using skewed location-scale distributions”, University of Louvain working paper (2002)

- [30] A. Charoenrook, H. Daouk, ”Conditional Skewness of Aggregate Market Returns”, NBER working paper (2004)