Relation between Bid-Ask Spread, Impact and Volatility in Order-Driven Markets

Abstract

We show that the cost of market orders and the profit of infinitesimal market-making or -taking strategies can be expressed in terms of directly observable quantities, namely the spread and the lag-dependent impact function. Imposing that any market taking or liquidity providing strategies is at best marginally profitable, we obtain a linear relation between the bid-ask spread and the instantaneous impact of market orders, in good agreement with our empirical observations on electronic markets. We then use this relation to justify a strong, and hitherto unnoticed, empirical correlation between the spread and the volatility per trade, with s exceeding . This correlation suggests both that the main determinant of the bid-ask spread is adverse selection, and that most of the volatility comes from trade impact. We argue that the role of the time-horizon appearing in the definition of costs is crucial and that long-range correlations in the order flow, overlooked in previous studies, must be carefully factored in. We find that the spread is significantly larger on the nyse, a liquid market with specialists, where monopoly rents appear to be present.

Science & Finance, Capital Fund Management, 6 Bvd Haussmann,

75009 Paris, France

now at: Division of Engineering and Applied Sciences, Harvard University,

Pierce Hall, 29 Oxford Street, Cambridge, Massachusetts 02138, USA

1 Introduction and review of the literature

One of the most important attribute of financial markets is to provide immediate liquidity to investors [1], who are able to convert cash into stocks and vice-versa nearly instantaneously whenever they choose to do so. Of course, some markets are more liquid than others and the liquidity of a given market varies in time and can in fact dramatically dry up in crisis situations. How should markets be organized, at the micro-structural level, to optimize liquidity, to favor steady and orderly trading and avoid these liquidity crises? In the past, the burden of providing liquidity was given to “market makers” (or specialists). In order to ensure steady trading, the specialists alternatively sell to buyers and buy to sellers, and get compensated by the so-called bid-ask spread – i.e. the price at which they sell to the crowd is always slightly larger than the price at which they buy. The determinants of the value of the spread in specialists markets have been the subject of many studies in the economics literature [2, 3, 4, 5, 6, 7, 8, 9, 10], and [11] for a recent review.

However, most financial markets have nowadays become fully electronic (with the notable exception of the New-York Stock Exchange, nyse – although this will soon change). In these markets, liquidity is self-organized, in the sense that any agent can choose, at any instant of time, to either provide liquidity or consume liquidity. More precisely, any agent can provide liquidity by posting limit orders: these are propositions to sell (or buy) a certain volume of shares or lots at a fixed minimum (maximum) price. Limit orders are stored in the order-book. At a given instant in time, the best offer on the sell side (the ‘ask’) is higher than the best price on the buy side (the ‘bid’) so no transaction takes place. For a transaction to occur, an agent must consume liquidity by issuing a market order to buy (or to sell) a certain number of shares; the transaction occurs at the best available price, provided the volume in the order book at that price is enough to absorb the incoming market order. Otherwise, the price ‘walks up’ (or down) the ladder of offers in the order book, until the order is fully satisfied. The liquidity of the market is partially characterized by the bid-ask spread , which sets the cost of an instantaneous round-trip of one share (a buy instantaneously followed by a sell, or vice versa).111Other determinants of liquidity discussed in the literature are the depth of the order book and market resiliency, see [12, 13]. A liquid market is such that this cost is small. A question of both theoretical and practical crucial importance is to know what fixes the magnitude of the spread in the self-organized set-up of electronic markets, and the relative merit of limit vs. market orders. In the present work, we argue that on electronic markets, profitable high frequency strategies using either limit or market orders should not exist, imposing a linear relation between the bid-ask spread and the average impact of market orders. This, in turn justifies a simple, but hitherto unnoticed, proportionality relation between the spread and the volatility per trade.

In a large fraction of the economics literature [2, 3, 4, 5], liquidity providers are described as market makers who earn their profit from the spread. The value of the spread is non zero because this market making strategy has costs. Three types of cost are discussed in the literature [11]:

-

•

(i) order processing costs (which includes sheer profit for the market maker);

-

•

(ii) adverse selection costs: liquidity takers may have superior information on the future price of the stock, in which case the market maker loses money;222This is also discussed as the free option trading problem in the literature, see e.g. [14] and refs. therein.

-

•

(iii) inventory risk: market makers may temporarily accumulate large long or short positions which are risky. If agents are risk-sensitive and have to limit their exposure, this adds extra-costs.

Theoretical models that account for these costs typically introduce a rather large amount of free parameters (such as risk-aversion, fraction of informed trades, fraction of patient/ impatient traders, etc.) most of which cannot be measured directly. In order to extract the different determinants of the spread from empirical data, some drastic assumptions must be made. For example, assuming the order flow to be short-ranged correlated, Huang and Stoll [8] find (using data from 1992) that of the spread is associated to order processing costs, and not to adverse selection333Adverse selection is even found to have, within this framework, a negative contribution to the spread!. This is would mean rather comfortable profits for market making444Direct processing costs can be estimated to be at least ten times smaller than the spread, in particular on electronic markets., and is a somewhat surprising conclusion since the spread on purely electronic markets is found comparable to the spread in markets with specialists. A related approach is that of [9], where the ratio of adverse selection to processing costs was estimated to be in the range on the nyse in 1990 (see also [11] for similar numbers). We will review this theoretical framework below and detail the similarities and differences with our own analysis; one particularly crucial difference is the assumption that the order imbalance has short-ranged correlations [8, 9], and therefore that market impact of a single trade is permanent, in striking disagreement with empirical data, where the order flow is instead found to be a long-memory process [15, 16], and single trade impact transient, but decaying very slowly [15, 17]. The long-range correlation between trades, and the corresponding temporal dependence of market impact will turn out to play an important role in the following discussion.

On general grounds, both adverse selection and inventory risk imply a positive correlation between the spread and the volatility of the traded asset. This makes perfect intuitive sense, and the aim of the present paper is to clarify in detail the origin of this relation. Positive correlation between spread and volatility is indeed documented empirically (see e.g. [18, 4, 19, 11, 20, 21, 22, 23]), but is not particularly spectacular and stands as one among other reported correlations, e.g., with traded volume, flow of limit orders, market capitalization, etc.[11]. Here, we want to argue theoretically, and demonstrate empirically on different markets, that there is in fact a very strong correlation between the spread and the volatility per trade, rather than with the volatility per unit time. Such a strong relation was first noted on the case of France-Telecom [15], and independently on the stocks of the ftse-100 [24], but no theoretical argument was given in favor of this relation.

From a theoretical point of view, several statistical models of limit and market order flows have been analyzed to understand the distribution of the bid-ask spread, and relate its average value to flow and cancellation rates [3, 25, 26, 27, 29, 28, 30, 31]. Some models include strategic considerations in order placement and look for a trade-off between the cost of delayed execution and that of immediacy, but suppose that the price dynamics is bounded in a finite interval [26], therefore neglecting the long term volatility of the price (see also [30, 31]). As such, these finite band models have nothing to say about the spread-volatility relationship. Another line of models discards all strategic components (“Zero intelligence models”) and assume Poisson rates for limit orders, market orders and cancellation [27, 29, 28].555More elaborated ‘weak intelligence’ models have been studied recently, see [33]. One can then compute both the average bid-ask spread and the long-term volatility as a function of these Poisson rates, and compare these predictions with empirical data [32]. The problem with such models is that although the order flow itself is completely random, the persistence of the order book leads to strong non-diffusive short term predictability of the price, which would be very easily picked off by high frequency automated execution machines. These programs search to optimize execution costs (see e.g. [10, 36]) by adequately conditioning the order flow (proportion of limit and market orders, timing, aggressivity) and use any short-term predictability to do so. As a result there are in fact very strong high frequency correlations in the order flow, coming from the ‘hide and seek’ game played by buyers and sellers within the order book [15, 16, 34]. A key observation is that for small tick stocks, the total available volume in the order book at any instant in time is in fact extremely small, on the order of of the market capitalization, or of the daily volume (see Table 2 in Appendix 2). Clearly, the reason for such a small outstanding liquidity is that liquidity providers want to avoid giving a free trading option to informed traders. As a consequence, liquidity takers must cut their total order in small chunks; this creates the long term correlation in order flow [35]. But since on electronic markets sophisticated buyers and sellers can trade using at their best convenience either limit or market orders, the average cost of limit and market orders should be very similar. If – say – market orders were on average significantly more expensive than limit orders, more limit orders would be issued, thereby reducing the spread and the cost of market orders, until an equilibrium is reached.666Data from brokers VWAP machines indeed show that the fraction of issued market orders is close to . That a competitive ecology between limit and market orders should exist on order-driven markets was emphasized in [38, 15, 17]. However, as our analysis reveals, this ecology turns out to be considerably more intricate than anticipated by Handa & Schwartz [38].

In the following, we introduce the idea of infinitesimal strategies, participating to a vanishing fraction of market or limit orders. Imposing that such strategies lead at best to marginal profits motivates a linear relation between the instantaneous price impact of a market order and the bid-ask spread, which we check empirically. Interestingly, we find that the profitability of these strategies depend in a non trivial way on the time horizon over which they are implemented. We show in particular that fast market making strategies can be profitable even though the long-term average cost of limit orders is positive, a rather paradoxical situation brought about by the presence of long-range correlations in the order flow and the temporal structure of the impact function.

The linear relation between spread and impact in turn allows us to establish a proportionality relation between the spread and volatility per trade, which holds both across different stocks and for a given stock across time, on electronic markets and on the nyse. This result shows that in a competitive electronic market the bid-ask spread in fact mostly comes from “adverse selection”, provided one extends this notion to account for the fact that trades can be uninformed but still impact the price. What is relevant here is that any unexpected component of the market order flow, whether it is truly informed or just random, impacts the price and creates a cost for limit orders, which must be compensated by the spread, as we now explain in detail.

2 Limit orders vs market orders and market impact

2.1 A simple theoretical framework

We start by reviewing the theoretical framework proposed by Madhavan, Richardson and Roomans (mrr) in [9], which helps define various quantities and hone in on relevant questions. We will call the volume of the th market order, and the sign of that market order ( for a buy and for a sell). The assumptions of the model are (i) that all trades have the same volume and (ii) the ’s are generated by a Markov process with correlation , which means that the average value of conditioned on the past only depends on and is given by:

| (1) |

where denotes averaging. The case corresponds to independent trade signs, whereas describes positive autocorrelations of trades. Note that in this model, correlations decay exponentially:

| (2) |

The mrr model assumes that the ‘true’ price evolves both because of random external shocks (or news) and because of trade impact. It is natural to postulate that both external news and surprise in order flow should move the price. Since the surprise at the th trade is given by , mrr write the following evolution equation for the price:

| (3) |

where is the shock component, with variance , and measures trade impact, assumed to be constant (all trades are assumed to have the same volume). Since market makers cannot guess the surprise of the next trade, they post a bid price and an ask price given by:

| (4) |

where is the extra compensation claimed the market maker, covering processing costs and the shock component risk. The above rule ensures no ex-post regrets for the market maker. The spread is therefore , whereas the midpoint immediately before the th trade is given by:

| (5) |

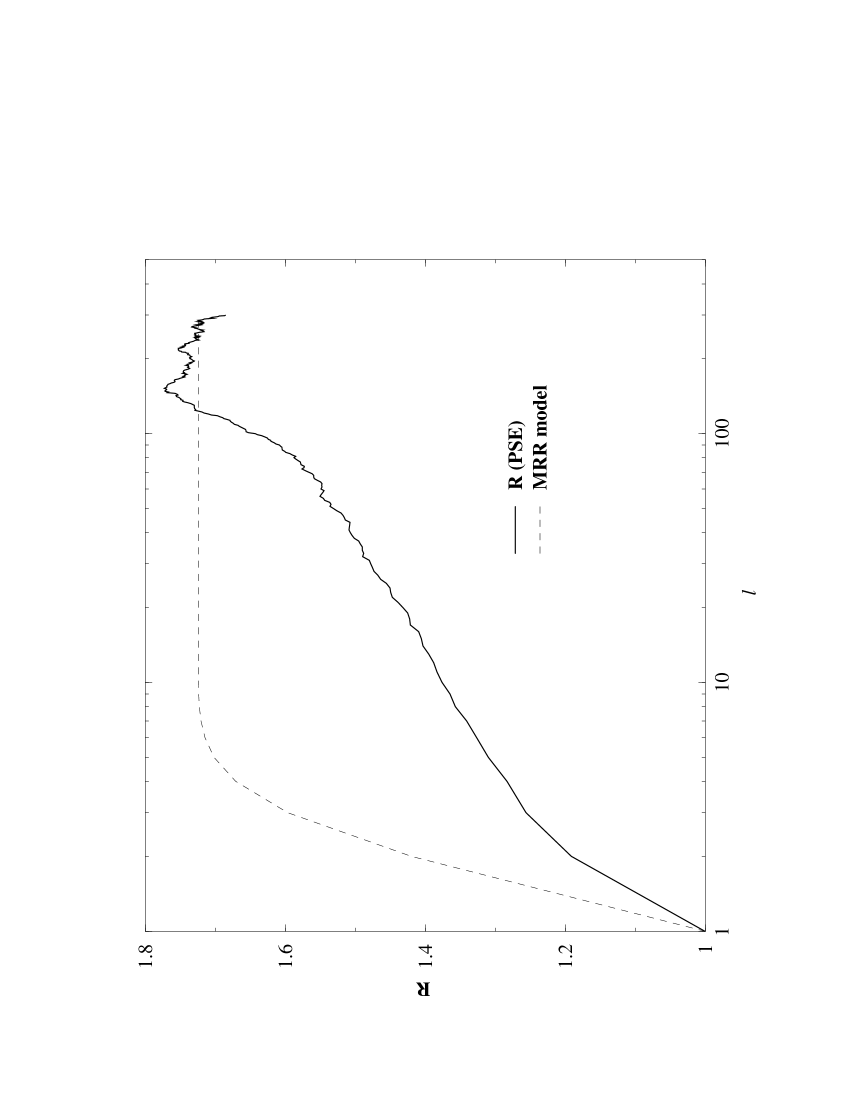

These equations allow to compute several important quantities for the following discussion, although not explicitely considered by mrr. The first one is the lagged impact function introduced in [15, 17]:

| (6) |

which is found, within the mrr model, to increase from to (See Appendix 1 and Fig. 1). Due to correlations between trades, the long time impact is therefore enhanced compared to the short term impact by a factor:

| (7) |

where in the mrr model, but the above relation is more general (see Appendix I).

The second quantity is the mid-point volatility, defined as:

| (8) |

which is easily computed to be:777The is an extra contribution to coming from any high-frequency noise component that we neglect here, coming from decimalisation, small volumes at bid/ask, etc. See [9, 15] and footnote 18 below.

| (9) |

Within the above interpretation, the mrr model leads to the following simple relations between spread, impact and volatility per trade:

| (10) |

relations which we generalize and test empirically in the following. From the data presented in mrr, one observes that was rather large on the nyse in 1990: .

Note that in the simplest case of independent trade signs (), the impact function is time independent. In the absence of extra compensation for the market makers, and the above equation reduces to . In economical terms, this last equality has a very simple meaning: it indicates that on average, the new mid-price after the transaction is equal to the last transaction price , and therefore that is precisely the condition where both market orders and limit orders have zero ex-post cost. This is more generally the meaning of the mrr relation, Eq. (10): the transaction price is exactly equal to the expected long term value of the mid-point.

It is interesting to discuss the cost of limit orders slightly differently. Suppose one wants to trade at a random instant in time. Compared to the initial mid-point value, the average execution cost of an infinitesimal buy limit order is given by:

| (11) |

with probability , the order is executed right away, below the mid-point; otherwise, the mid-point moves on average by a quantity , to which must be added the cost of a limit order conditioned to the last trade being a buy, , for which a similar equation can be obtained:

| (12) |

with obvious notations. Since the mrr model is Markovian, one has and , so that:

| (13) |

Plugging this last relation in Eq. (11), we finally find:

| (14) |

Imposing that , one recovers the mrr relation between the spread and the asymptotic impact (Eq. (10) with ). Note, however, the cost of a market order compared to the initial mid-point value is within the mrr model – but of course the order is still executed at the ‘right’ long term value of the stock.

2.2 Real markets are more complicated

The above model, although suggestive and capturing the essence of the correlation between spread, impact and volatility, is however not fully satisfactory since it completely neglects the very broad distribution of traded volumes (often found to be log-normal, or power-law tailed) and, more importantly, the non-Markovian, long ranged correlation of the trade signs, which is found to decay as [15, 16]:888These long ranged correlations were also noted in e.g. [21, 37], but the detailed shape of the tail of was not investigated, and its long-memory nature not discussed.

| (15) |

instead of the fast, exponential decay assumed in the mrr model. Because the exponent is found to be less than unity, the correlation function is not integrable, which technically makes the series of trade signs a long-memory process. As emphasized in [15, 17], this imposes a number of non-trivial constraints on price impact for the returns to remain uncorrelated while the order flow is strongly auto-correlated. In particular, simple models (such as Huang and Stoll’s [8, 11]) where price changes include a term proportional to would lead to strong super-diffusion (trends) of prices on the long run [15], in disagreement with empirical data.

The volume-dependent lagged impact is now defined as:999In the definition of , care has been taken to remove any long term trend of the mid-point. In any case, since is close to zero, this trend contribution would very nearly vanish.

| (16) |

In the mrr model, takes a single value and reduces to the previously defined quantity. The function was studied in detail in [15]. To a good level of approximation, the following factorization property is found to hold: , where is a strongly concave function, and an increasing function of that varies by a factor of when increases from to several thousands (corresponding to a few days of trading).101010The true asymptotic behaviour of for longer horizons is difficult to determine empirically due to statistical noise, and might in fact be stock dependent, see [17] for a discussion of this point. The shape of , averaged over a collection of different stocks of the pse, is shown in Fig. 1, and compared with the simple form assumed in the mrr model (see caption for more details). Perhaps more importantly, the enhancement factor is found empirically to be substantially larger than predicted by Eq. (7). For example, on the pool of 68 pse stocks studied below, we find, averaged over all stocks, whereas (see Table 2 of Appendix 2). The difference between the two will turn out to play a crucial role in the following.

2.3 Market order strategies

In this section and below, we want to show how the simple relations derived in the mrr model can be extended and tested in the general case of fluctuating volumes and long-ranged correlation of trade signs. A first idea is to measure empirically the average execution cost of market-orders. One can define the ex-post cost the difference between the transaction price at (trade-)time and the mid-point price at time later, with but still much smaller than the typical horizon of the trading strategy itself (a few days or more), in order not to mix in the quality of the decision to trade. The above definition of execution cost marks the trade to market after and is referred to the realized spread in the literature [41, 11]. The volume weighted averaged cost (over trades) of a single market order over horizon is therefore:111111Note that this definition neglects the fact that one single large market order may trigger transactions at several different prices, up the order book ladder, and pay more than the nominal spread. Nevertheless this situation is empirically quite rare on the markets we are concerned with, and corresponds to only a few percents of all cases [42].

| (17) |

The choice allows us to use the asymptotic value of , , where we have introduced a factor in conformity with the notation of the previous section. Using the factorization property of , we finally obtain for the average cost of a single market order:

| (18) |

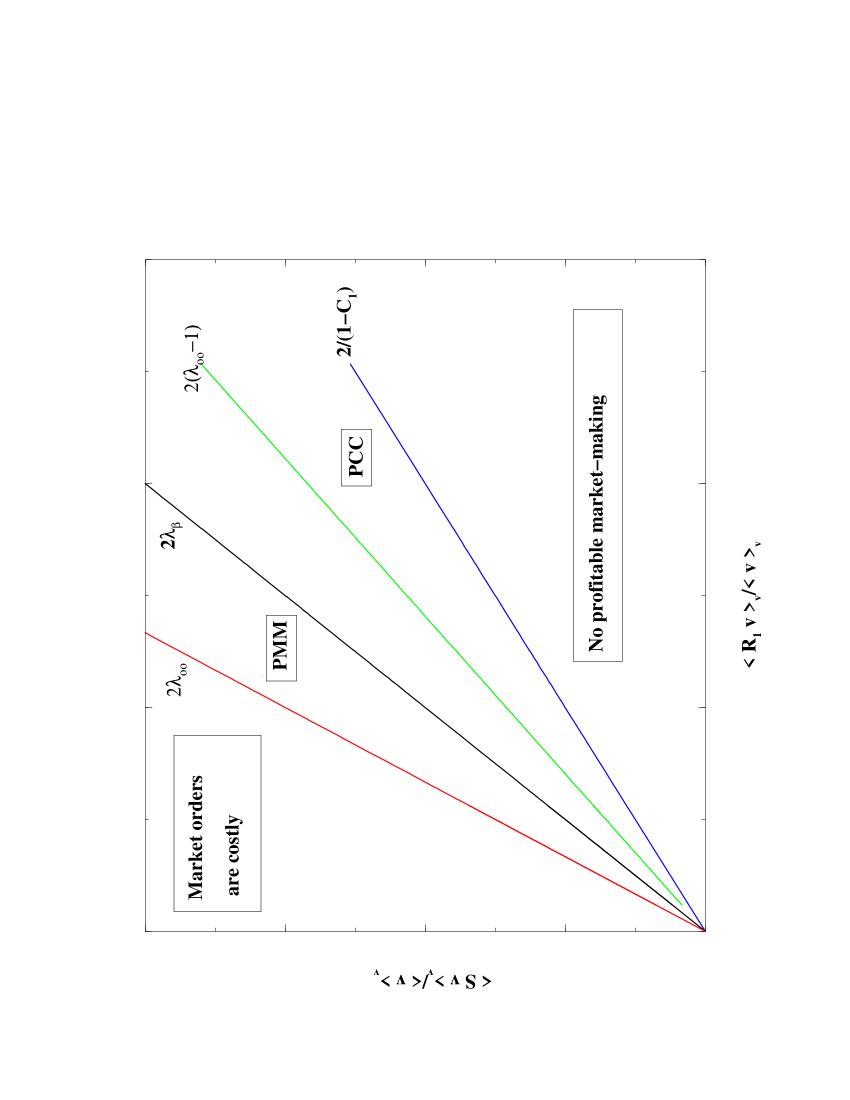

meaning, as intuitively clear, that this cost is positive when spreads are large, but may become negative if the total price impact is large. In the plane , (which will repeatedly be used below to represent empirical data) the condition defines a straight line of slope separating an upper region where market orders are on average costly, from a region where single market orders are favored: see Fig. 2.

The above computation suggests an upper bound on the spread, which we establish more rigorously in the next section. For larger spreads, the positive average cost of market order would deter their use; limit orders would then pile up and reduce the spread. What would happen if the spread was below the red line of slope in Fig. 2? Naively, market orders have a negative cost in that region, and one might be able to devise profitable strategies based solely on market orders. The idea would be to try to benefit from the impact term in the above balance equation. The growth of ultimately comes from the correlation between trades, i.e. the succession of buy (sell) trades that typically follow a given buy (sell) market order. The simplest ‘copy-cat’ strategy which one can rigorously test on empirical data is to place a market order with vanishing volume fraction (not to affect the subsequent history of quotes and trades), immediately following another market order. This strategy suffers on average from the impact of the initial trade, used as a guide to guess the direction of the market. Therefore, the profit of such a copy-cat strategy, marked to market after a long time and neglecting further unwinding costs, is reduced to:121212A more rigorous estimate of the gain of a copy-cat strategy participating to all the trades can be obtained following the method outlined in the next section.

| (19) |

Imposing that this gain is non-positive, one obtains a lower line in the plane , of slope . Only below this green line can the above infinitesimal copy-cat strategy be profitable. We therefore expect markets to operate above this line and below the red line of slope . Note however that market orders below the line are not necessarily favorable in practice, since the cost for executing a series of market orders (which is the typical situation faced by large investors, since the outstanding liquidity is, as noted above, always quite small) must include the impact of past trades and this increases their average cost. Hence, the slope of the effective zero-cost line for a series of market orders is indeed smaller than . Similarly, the long-time impact of an isolated market order, uncorrelated with the order flow, is in fact very small [15]. These isolated market orders thus also have a positive cost, equal to half the spread. The only way to benefit from the average impact is to free-ride on a wave of orders launched by others, as in the above copy-cat strategy. Let us now take the complementary point of view of limit orders and determine the region of profitable market making strategies.

2.4 An infinitesimal market making strategy

Our aim is to discuss the profitability of providing liquidity to the market formalizing the idea of infinitesimal strategies used in the previous section. To do so we compute the gain of a simple market making strategy which consists in participating to a vanishing fraction of all trades through limit orders. The simplest strategy is to consider a market maker with a certain time horizon who provides an infinitesimal fraction of the total available liquidity. As illustrated by Eq. (17), the cost incurred by the market maker comes from market impact: the price move between and is anti-correlated with the accumulated position. When the crowd buys, the price goes up while the market making strategy accumulates a short position which would be costly to buy back at time , and vice-versa. More precisely, we consider a steady-state market making strategy (which avoids explicit unwinding costs). The strategy is such that volume offered dynamically depends on the accumulated position, which insures that the inventory is always bounded. We choose the tendered fraction to be given by: , where is the (signed) position accumulated up to time , and for orders placed at the ask and for orders placed at the bid. This mean-reverting strategy insures that the typical position is always bounded. One can now use this strategy for an arbitrary long time ; its profit & loss is simply given by:

| (20) |

For large , one can replace this expression by:

| (21) |

with corrections due to the residual position at . Discarding the constraint and neglecting volume-volume correlations, which are much smaller than sign-sign correlations [15, 16], we finally find:

| (22) |

where fixes the typical time scale of the market making strategy. The above expression is exact in the limit , and only approximate otherwise. When (fast market making), Eq.(22) reduces to:

| (23) |

whereas , corresponding to slow market making, yields:

| (24) |

Setting to zero leads to a linear relation between spread and impact:

| (25) |

Using the empirical shape of and , the slope is found to increase between and when increases. Contrarily to market orders which benefit from the growth of the impact with time, slow market making is suboptimal. When , and the lower limit of profitability of very slow market making is precisely the red line of Fig. 2 where market orders become profitable. Faster strategies correspond to smaller values of , closer to , leading to an extended region of profitability for market making. From the assumption that the above market making strategy for any value of should be at best marginally profitable (since one might find more sophisticated strategies, which take full advantage of the correlations between signs and volumes), we finally obtain the following bound between spread and impact:

| (26) |

defining the blue line of slope in the plane of Fig. 2. Consistently with the mrr model, when , the blue and red line of Fig. 2 exactly coincide. Using that fact that , a simple generalisation of the argument presented at the end of Sect. 2.1 allows one to show that the cost of limit orders is indeed negative above the blue line.

2.5 Theoretical analysis: conclusions

Eqs. (18,19,26) and the resulting microstructural “phase diagram” of Fig. 2 are our central results. These equations show that the cost or profitability of infinitesimal market and limit order strategies can be estimated from empirical data alone, without having to make any further assumption on the fraction of informed trades, the correlation between trades, etc. In order to proceed, we made two approximations. Firstly, we assumed that these strategies could be made infinitesimal, which allows us to neglect their impact on the price dynamics. In practice, trades occur in discrete volume, and strictly speaking the assumption of infinitely small volumes does not hold. However, the volume of typical trades is much larger than the minimum size, which suggests that this approximation is accurate. Secondly, we neglected all direct transaction costs, which obviously affect profitability. These costs are in general very small compared to the spread, and can therefore also reasonably be neglected.

Our main result is that profitability, perhaps surprisingly, depends on the frequency of these strategies, a result closely related to the anomalous time dependence of the impact function. Market orders are favored at low frequencies, when impact has fully developed, whereas limit orders are favored at high frequencies, where impact is still limited and the execution probability significant.

Our analysis delineates, in the impact-spread plane, a central wedge bounded from above by a slope and from below by a slope , within which both market orders and limit orders are viable. In the upper wedge, market orders would always be costly and would be substituted by limit orders. In the lower wedge, market making strategies, even at high frequencies, would never eke out any profit. Such a market would not be sustainable in the absence of any incentive to provide liquidity. But if the spread happened to fall in this region, the enhanced flow of market orders would soon reopen the gap between bid and ask.

Our next assumption is that simple statistical strategies must have negative or marginal profit. These is quite reasonable since high-frequency strategies carry relatively small risks. Applying this idea to market making strategies, we conclude that competition between liquidity providers will push the spreads close to the lower limit, corresponding to the blue line of slope in Fig. 2. Now, since market taking (copy-cat) strategies should not be profitable either, the green line of slope should necessarily lie below the blue line, leading to the following inequality on the asymptotic impact enhancement factor :

| (27) |

where the lower bound comes from the existence of correlation between trades (see Eq. (7)). In other words, the impact function cannot grow more than roughly twice its initial value, otherwise statistical arbitrage would set in. Interestingly, our data is compatible with the above bound; in practice the blue and green lines turn out to be not very far from each other.

Finally, we note that market microstructure studies insist on large inventory risks being an important determinant of the bid-ask spread. However, large inventories correspond to long horizons and slow market making. Our analysis above shows that accumulating inventories on a long horizon is not only risky, but may also be extremely costly on average. When , market making on large horizons is significantly more costly than on short horizons, by an amount proportional to the spread itself. This is a very strong effect, which makes the existence of low-frequency market makers very unlikely. Therefore, inventory risk by itself should not be important in determining the value of the spread, at least on electronic markets.

In conclusion, we expect that electronic markets should operate in the vicinity of the blue line of Fig. 2, imposing a linear relation between spread and market impact of slope close to . This is what we test on empirical data in the following section.

3 Comparison with empirical data

3.1 Small tick electronic markets

We first consider small tick electronic markets, such as the Paris Stock Exchange (pse) or Index Futures. The case of large tick stocks is different since in this case the spread is (nearly) always one tick, with huge volumes at both the bid and the ask. The case of such markets will be considered below.

We studied extensively the set of the 68 most liquid stocks of the pse during the year 2002. The summary statistics describing these stocks is given in Appendix 2. From the Trades and Quotes data, one has access the the bid-ask just before each trade, from which one can obtain the sign and the volume of each trade (depending on whether the trade happened at the ask or at the bid) and the mid-point just before the trade. From this information, one computes the quantities of interest, such as the instantaneous impact function , the one-lag correlation , the spread and . Note that we have removed ‘block trades’, which appear as transactions with volumes larger than what is available at the best price that are not followed by a change of quotes. Clearly, these block trades are outside the scope of the above arguments; in any case they represent typically a fraction of the total number of trades and do not significantly affect the following results.

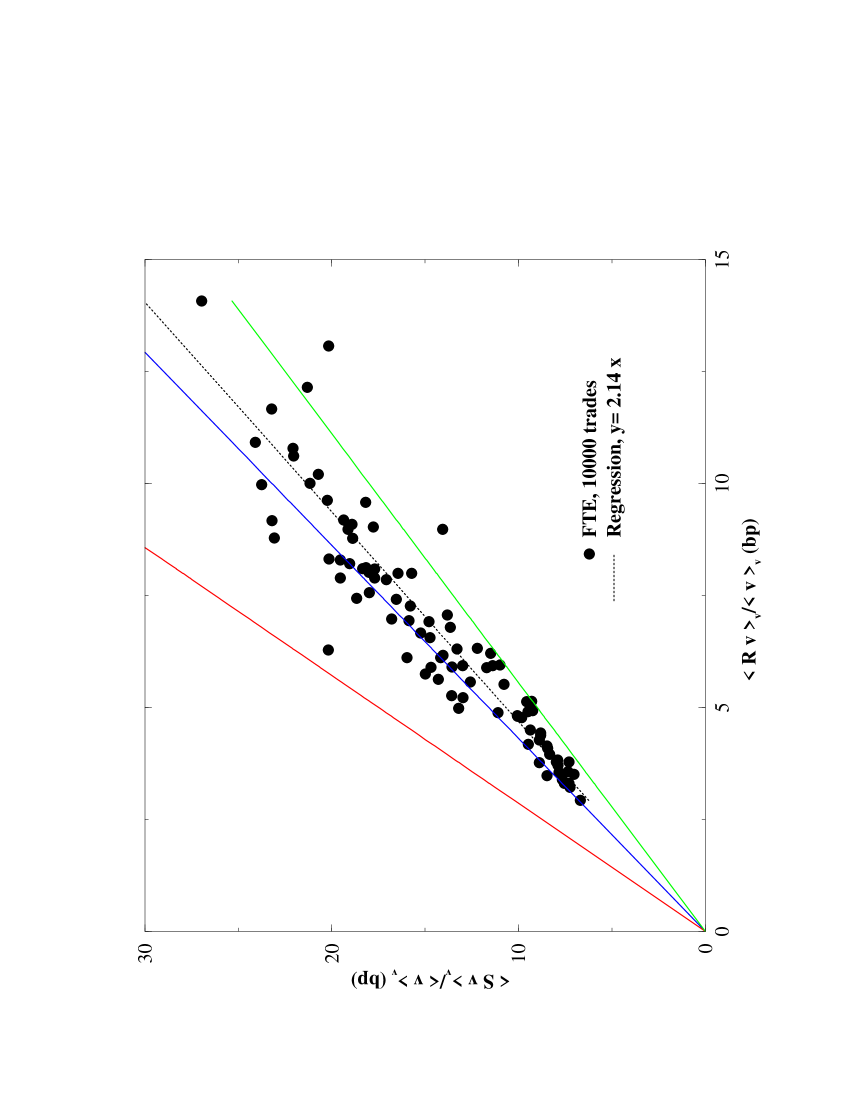

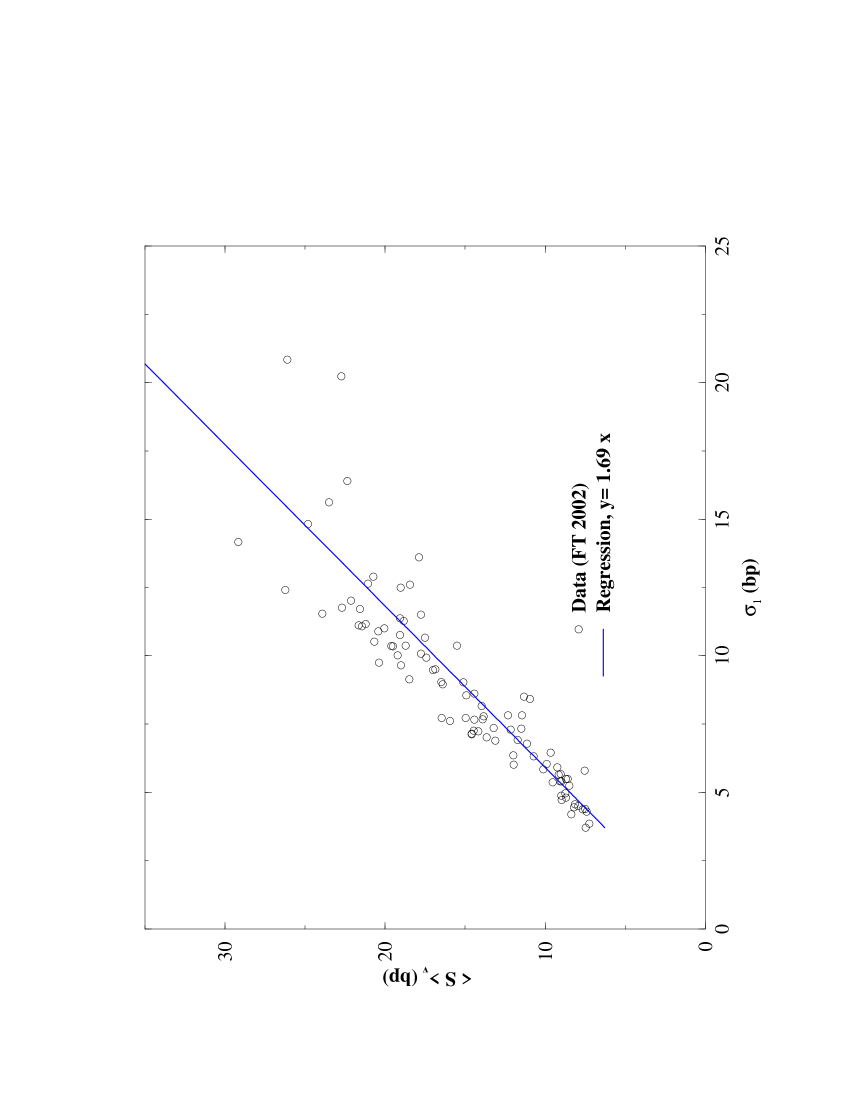

We test the above ideas in two different ways – for a given stock across time, and across all different stocks. Since both the spread and impact vary with time, one can measure ‘instantaneous’ quantities by averaging for a given stock and over a number of successive trades. In the example of Fig. 3, each point corresponds to an average over 10000 non overlapping trades, corresponding to 2 days of trading in the case of France Telecom in 2002. Doing so we obtain quantities that vary by a factor 5 that allows us to test the linear dependence predicted by Eqs.(19,26). For France Telecom, we find that is close to the average value shown in Fig. 1. Therefore in this case, meaning that copy-cat market making strategies are impossible, as expected for highly liquid stocks. We also find that (see Appendix 2). Our results shown in Fig.3 are in good agreement with the above theoretical bounds, even for averages over rather short time scales. A linear fit with zero intercept gives a slope equal to , to be compared with , meaning that providing liquidity is hardly rewarded at all for this very liquid, small tick stock. In fact, if the intercept of the linear fit is left free, its value (which should equal the ‘processing costs’ in the mrr model) is found to be slightly negative.

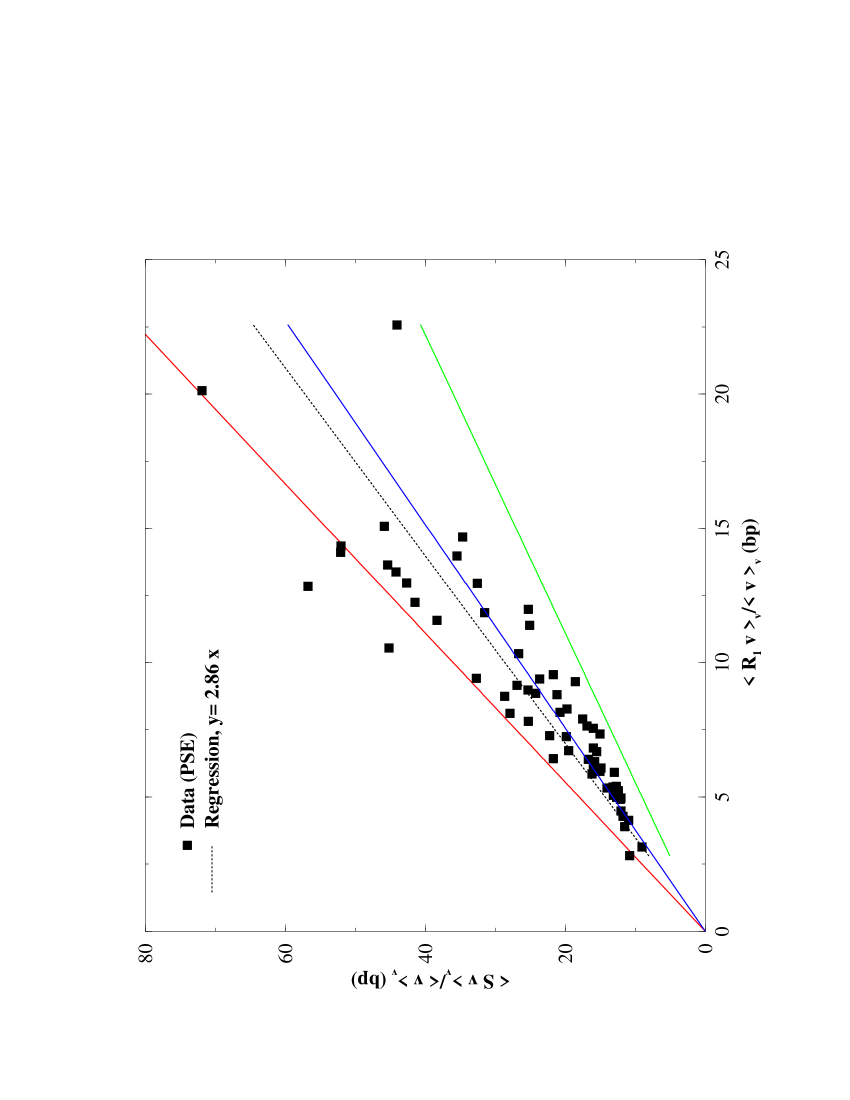

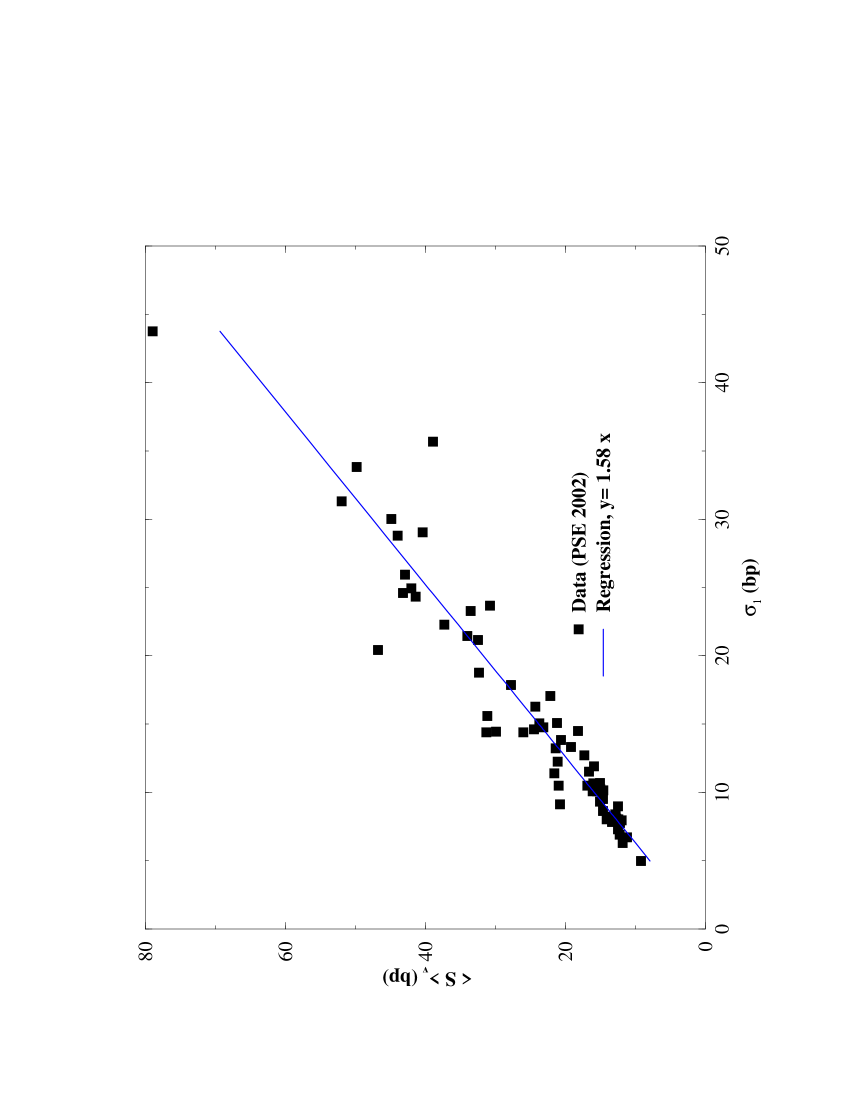

We also test Eq.(26) cross-sectionally in Fig. 4, using the above 68 different stocks of the pse. The relative values of the spread and the average impact also varies by a factor 5 between the different stocks, which enables to test the linear relations (19,26). Once again we find a good agreement with the predicted bound, and the linear fit with zero intercept gives a slope of , while . Hence, fast market making strategies are on average weakly profitable on the pse. However, the intercept of a two-parameter regression is very slightly negative, showing that no order processing costs component can be detected on these fully electronic markets.

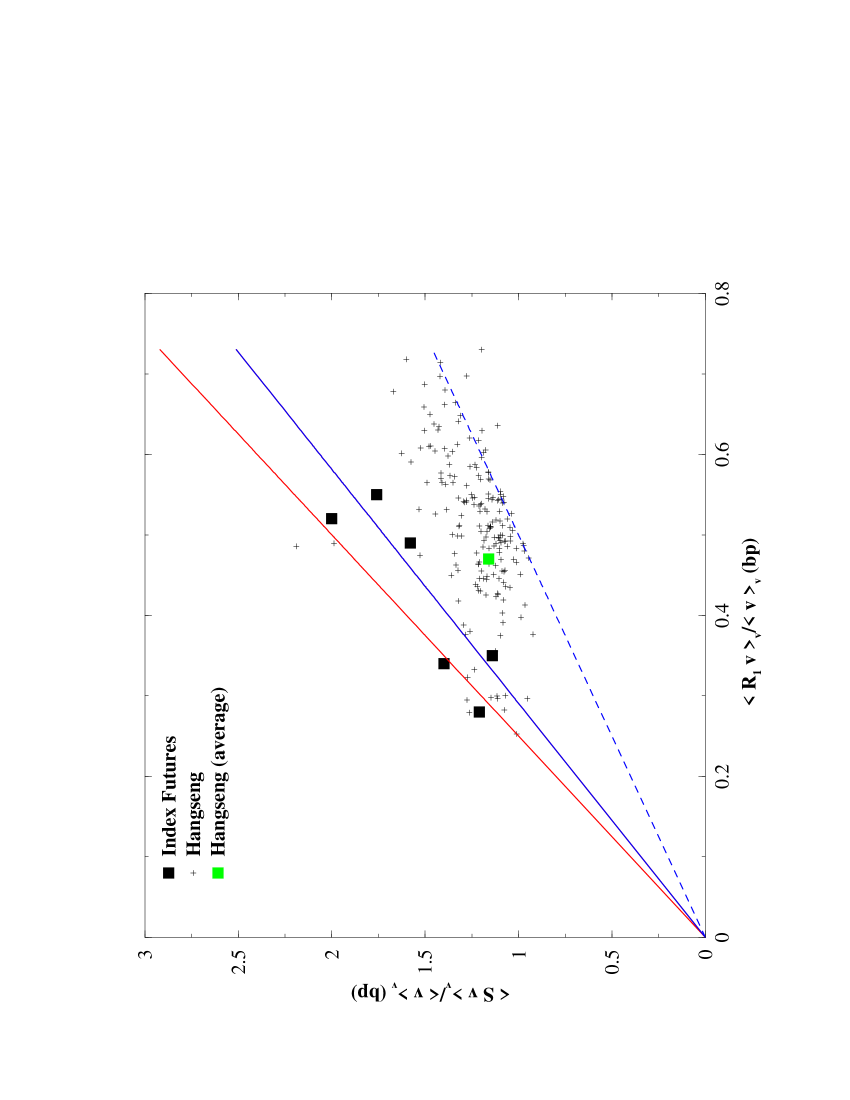

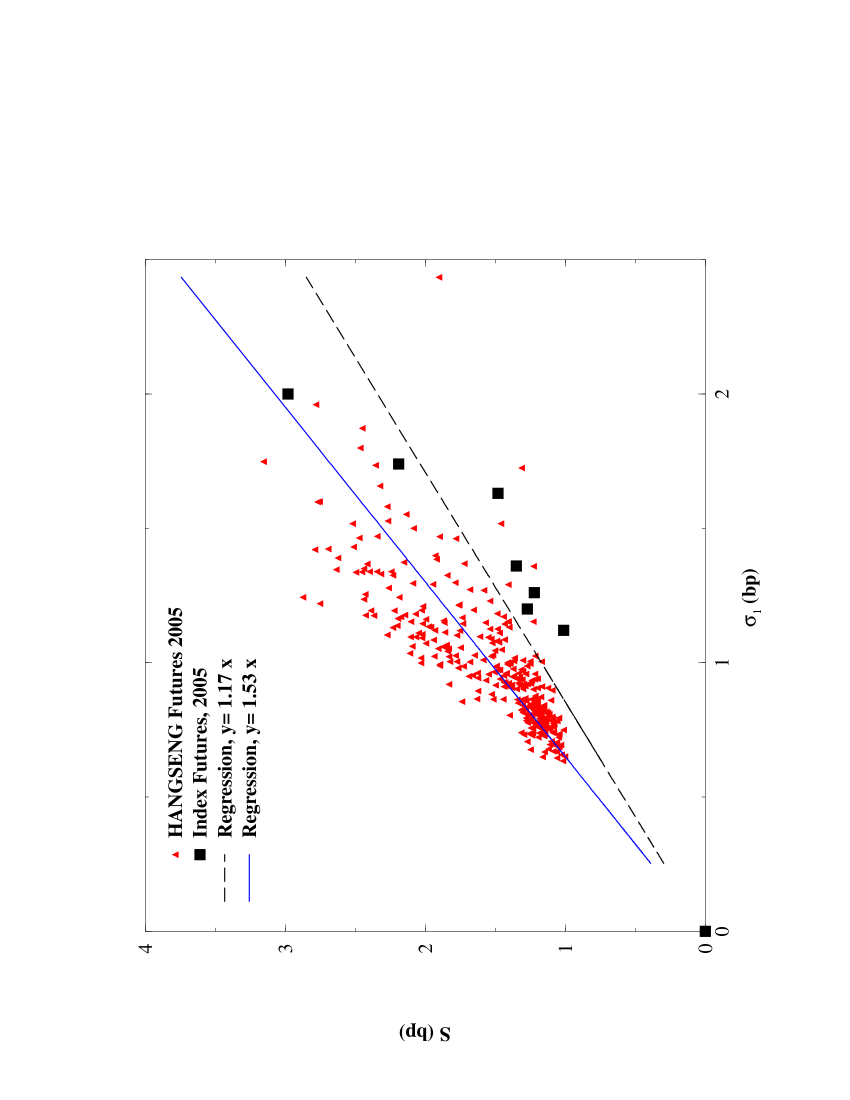

It is also interesting to analyze small tick Futures markets, for which the typical spread is ten times smaller than on stock markets. We have studied a series of small tick Index Futures in 2005 (except the mib for which the data is 2004), again both as a function of time and across the 7 indexes of our set. For most contracts, the value of is quite large () except for the hangseng where . Results are shown in Fig. 5; the bounds are again quite well obeyed both across contracts and across time, even when the time averaging is restricted to only 1000 consecutive trades. This shows that on these highly liquid contracts, where the transaction rate as high as a few per second, the equilibrium between spread and impact is reached very quickly.

3.2 NYSE stocks

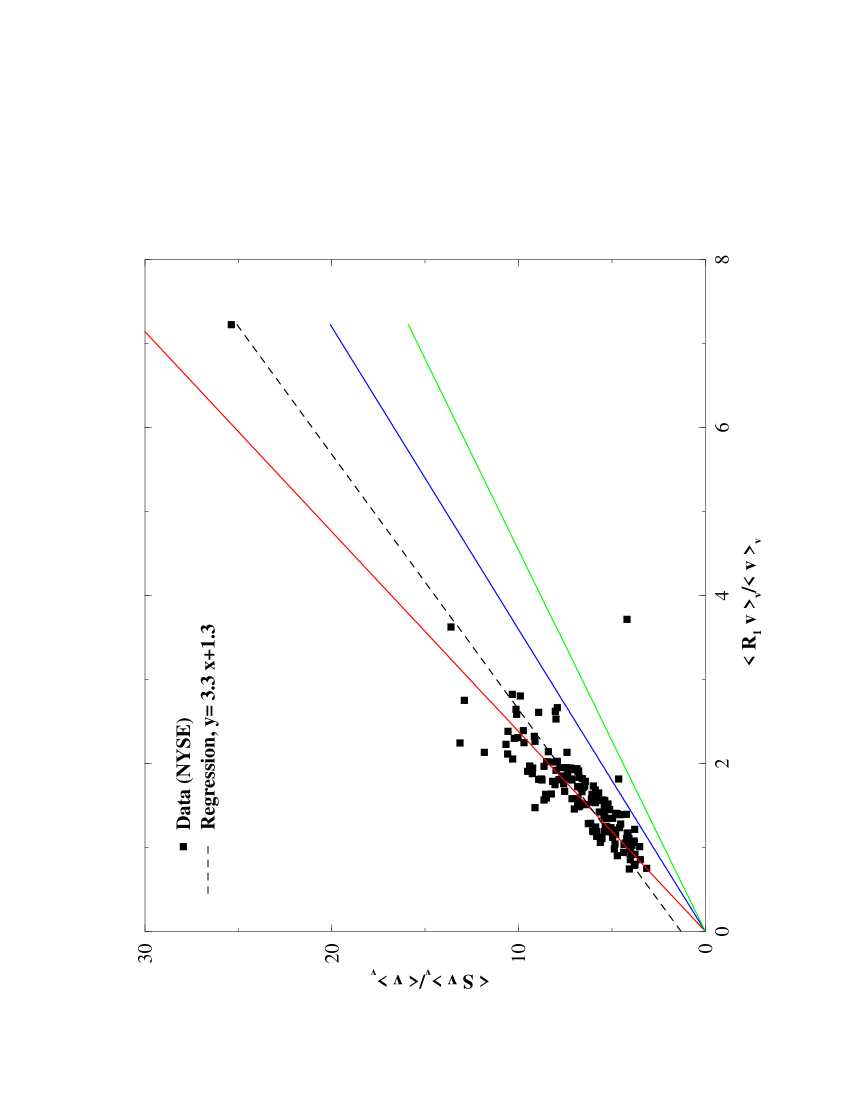

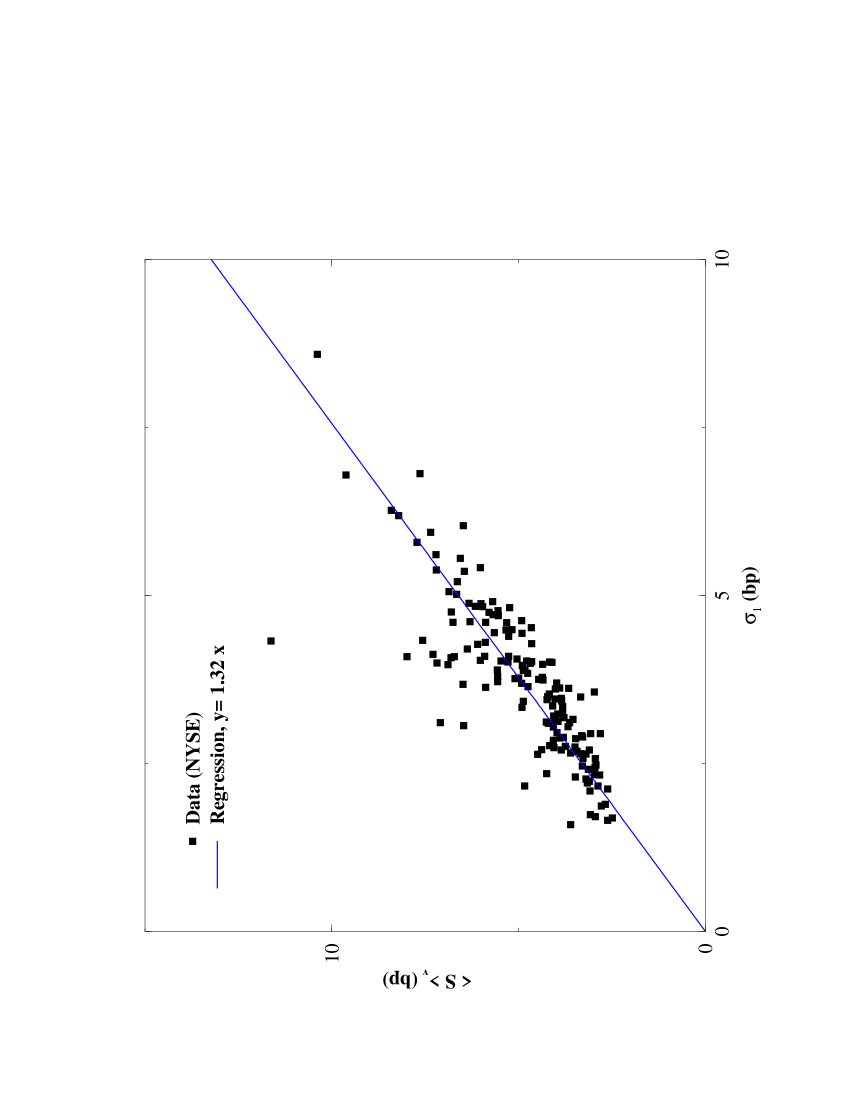

The case of the nyse is quite interesting since the market is still ruled by specialists, who however compete to provide liquidity with other market participants placing limit orders. We again test Eqs.(18,26) cross sectionally, using the set of the 155 most actively traded stocks on the nyse in 2005.131313The list of the 155 names is available on request. We use the quoted bid-ask posted by the specialist. We have first determined the average impact function , which has a shape roughly similar to Fig. 1, although the asymptotic plateau value is slightly larger, leading to . On the other hand, is also slightly larger, equal to .

Plotting the data in the spread-impact plane, we now find that the empirical results cluster around to the upper red line limit where market orders become costly. The regression has a significantly larger slope of and now a positive intercept basis points.141414This is five times smaller than the average spread, leading to , much smaller than the result found within mrr model in 1990, or a similar value reported in [11]. This suggests that, perhaps not surprisingly, the existence of monopoly rents on nyse: market makers post spreads that are systematically over-estimated compared to the situation in electronic markets, with a non-zero extrapolated spread for zero market impact. This result is in agreement with the study of Harris and Hasbrouck performed in the early 90’s on the nyse [39], which showed that limit orders were more favorable than market orders, and also with Handa and Schwartz [40], who showed that pure limit order strategies were indeed profitable. On the other hand, the value of the regression slope on the purely electronic pse show that pure limit order strategies can only be marginally profitable. We have checked that using the traded spread instead of the quoted spread does not change appreciably the above conclusions.

3.3 The case of large tick electronic markets

A priori, the string of arguments leading to Eq. (26) does not directly apply in the case where the tick size is large. In that case the spread is most of the time stuck to its minimum value, i.e. one tick, while the size of the queue at the bid and at the ask tends to be extremely large (see e.g. Appendix 2, Table 3). Because of the large value of the spread, limit orders appear to be favorable, but huge limit order volumes accumulate as liquidity providers attempt to take advantage of the spread. The size of the queue at the bid or at the ask is thus much larger than the typical value of the traded volume at each transaction : (see Table 3), to be compared with (see Appendix 2, Table 2) for smaller tick stocks. Therefore, the simple market making strategy considered above, which assumes that one can participate to a small fraction of all transactions, cannot be implemented. We thus expect that the spread on these markets will be substantially larger than predicted by the bound Eq. (26), because the competition between liquidity providers, that acts to reduce the spread, cannot fully operate. We indeed find that the ratio between and is large for large tick stocks. For example, in the case of Ericsson, during the period March-November 2004, for which the tick size is bp, we find . However, we also find on the same data that , meaning that market orders are in fact not systematically unfavored in these large tick electronic markets. In fact, all data points are found to lie between our bounds, Eqs. (18,26), but indeed significantly higher than the blue line of Fig. 2 in this case.

3.4 Comparison with empirical data: conclusion

Our empirical analysis shows that on liquid markets, an approximate symmetry between limit and market orders indeed holds, in the sense that neither market orders nor limit orders are systematically unfavorable. Markets operate in the ‘neutral wedge’ of Fig. 2.

For fully electronic markets, competition for providing liquidity is efficient in keeping the spread close to its lowest value, marginally compensating impact cost. There is therefore hardly any room for market making strategies. Although the cost of isolated market orders is found to be negative, the empirically established proximity of the blue and green line in Fig. 2 means that there is no room for simple market taking strategies either. In this discussion, time horizon and long range correlations in the order flow play an important role, overlooked in previous studies [8, 9, 11]: somewhat paradoxically, liquidity providers as a whole offer average negative costs to market orders but high frequency market making strategies still manage to get (marginally) compensated. Our analysis shows that the ecology between liquidity takers and liquidity providers turns out to be considerably more complex than anticipated by Handa & Schwartz [38]: when costs are computed on large time scale, limit orders are in average costly. This implies that a significant fraction of limit orders cannot be due to market makers, since limit orders as a whole are in arrears. The common assumption that limit orders can be attributed to liquidity providers compensated by the spread cannot be correct in electronic markets. This argument can only concern a small fraction of high-frequency market makers, whose existence is nevertheless crucial to prevent liquidity crises.

On the nyse, spreads appears to be significantly larger: isolated market orders are now marginally costly. A linear relation between spread and impact still applies, albeit with a larger slope and a residual intercept, corresponding to market maker monopoly rents, which are absent in electronic markets.

4 Liquidity vs. volatility

4.1 Theoretical considerations

Consider again the mrr model discussed above, which predicts a simple relation between volatility and impact, Eq. (9). Using the relation between spread and impact established above, this suggests a direct link between volatility per trade and spread, which we motivate and test in this section.

By definition of the volatility per trade and of the instantaneous impact , one has as an identity:

| (28) |

The instantaneous impact is expected to fluctuate over time for several reasons. First, the volume of the trade, the volume in the book and the spread strongly fluctuate with time. For example, on the pse, the spread has a distribution close to an exponential, hence one has (see Table 2, Appendix 2).151515The distribution appears to be a power-law on other markets [33], but this is irrelevant for the following discussion. Large impact fluctuations may also arise from quote revisions due to addition or cancellation of some limit orders. Second, there might also be important news affecting the ‘fundamental price’ of the stock. These result in large, instantaneous jumps of the mid-point, unrelated to the trading activity itself. In order to account for both effects, we write, generalizing the above mrr relation:

| (29) |

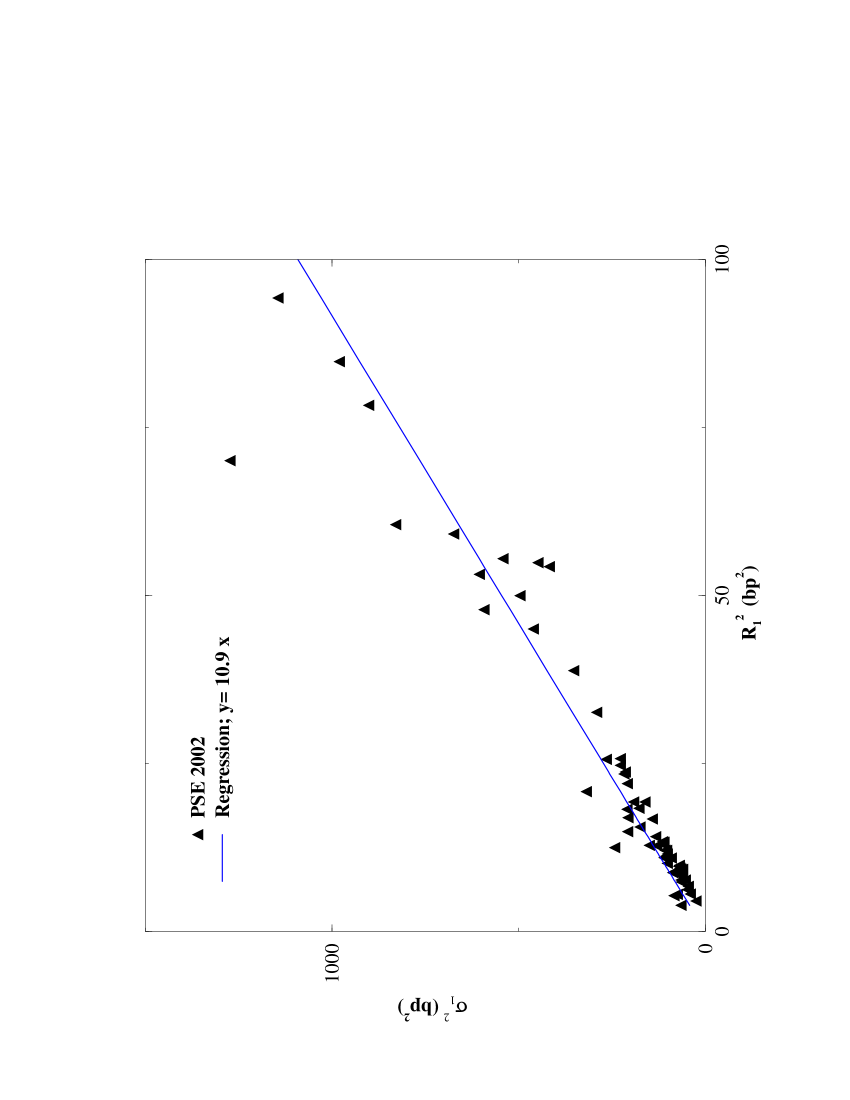

where is the average impact after one trade, is a coefficient measuring the variance of impact fluctuations and is the news component of the volatility (see Section 2.1). A specific model for Eq. (29) was worked out in [15], and tested on France-Telecom (see also [44]). Here, we establish that this relation holds quite precisely across different stocks of the pse, with a correlation of (see Fig. (7)). Perhaps surprisingly, the exogenous ‘news volatility’ contribution is found to be small. (The intercept of the best affine regression is even found to be slightly negative). This could be related to the observation made in Farmer et al. [42] that for most price jumps, some limit orders are canceled to slowly and get ‘grabbed’ by fast market orders, which means that most of these events are already included in , in line with our general statements on the approximate symmetry between limit and market orders.161616One could argue that our results simply show that the news volatility itself is proportional to and thus to the spread . However, there is no reason why this should a priori be the case. For example, a model where jumps of typical amplitude have a small probability per trade leads to , whereas the cost of such jumps, contributing to , is . In the following, we will therefore neglect , as suggested by Fig. (7): in this sense the volatility of the stocks can be mostly attributed to market activity and trade impact. This is in agreement with the conclusions of Lyons and Evans on currency markets [43]; see also the discussion in [15, 37].

Our final assumption is that of universality, i.e. when the tick size is small enough and the typical number of shares traded is large enough, all stocks within the same market should behave identically up to a rescaling of the average spread and the average volume. In particular we assume that the statistics of (i) the volume of market orders (ii) the spread S and (iii) the impact , and the correlations between these quantities are independent on the stock when these quantities are normalized by their average value.171717The universality of the shape of the order book was indeed checked to hold rather well in [29]. This universality implies that:

| (30) |

where is stock independent. Similarly,

| (31) |

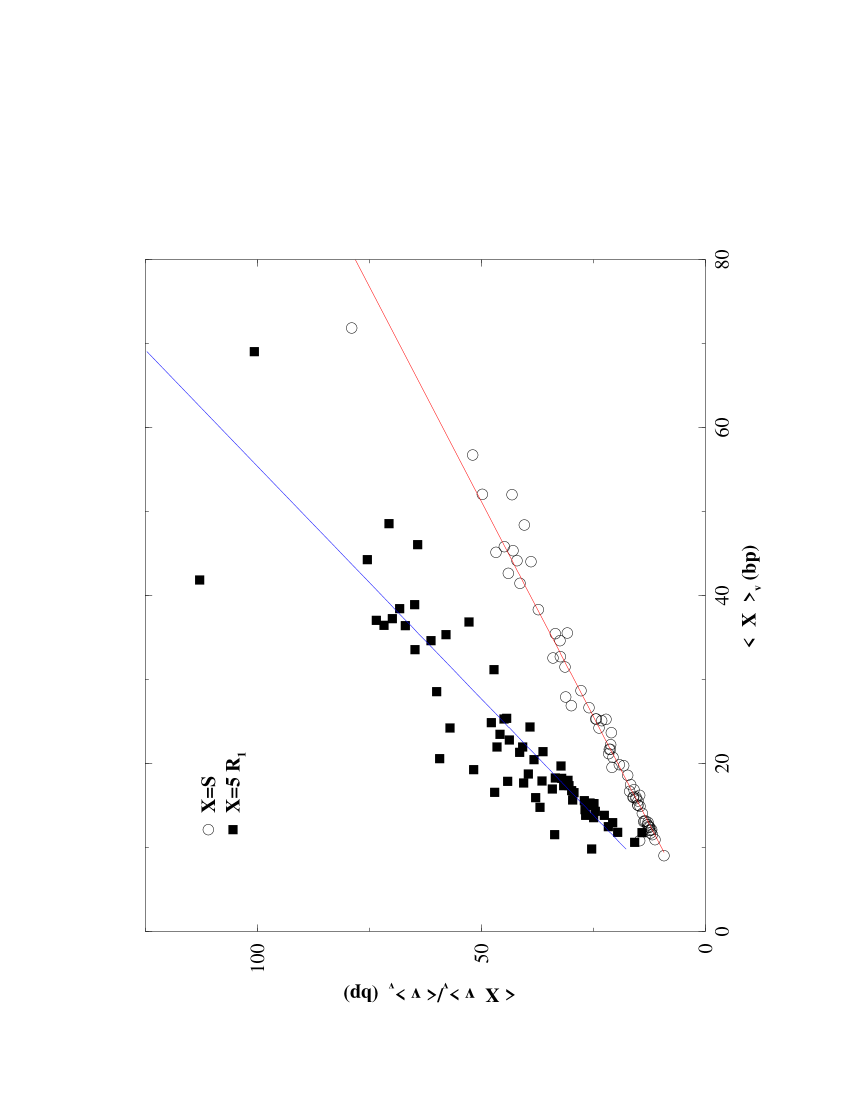

where is also stock independent. Note that this assumption is consistent with the empirical observation of [45], where the impact function for different US stocks can indeed be rescaled onto a unique Master curve by a proper scaling of both the and axis. We test Eqs. (30,31) in Fig. 8 in the case of the Paris Stock Exchange, from which we extract and . Interestingly, we find that the volume and the spread are nearly uncorrelated (), whereas the volume traded and the impact are correlated (), as expected.

Therefore, using Eq. (26) as an equality (as suggested by the empirical results of Section 3), and Eqs. (29,30,31), we obtain the main result of this section:

| (32) |

where is a stock independent numerical constant, which can be expressed using the constants introduced above as . This very simple relation between volatility per trade and average spread was noted in [15, 24], and we present further data in the next section to support this conjecture. Therefore, the constraints that (i) optimized high frequency execution strategies impose that the price is diffusive (see [15, 17]), and (ii) the cost of limit and market orders are nearly equal [Eqs.(18,26)], lead to a simple relation between liquidity and volatility. As an important remark, note that the above relation is not expected to hold for the volatility per unit time , since it involves an extra stock-dependent and time-dependent quantity, namely the the trading frequency , through:

| (33) |

We will discuss this issue further in Section 5.

4.2 Comparison with empirical data

Using the same data sets as in Sections 3.1 and 3.2, we now test empirically the predicted linear relation between spread and volatility per trade, Eq. (32). The average spread is defined as the average distance between bid and ask immediately before each trade (and not as the average over all posted quotes). The volatility per trade is defined as the root mean square of the trade by trade return.181818Since prices are very close to random walks, defining the volatility from returns defined on a longer time scale gives very similar results. On our set of pse stocks, we find that , indicating a small anti-correlation of returns () of short time scales. Our results for the Paris Stock Exchange are shown in Figs 9 and 10. We see that Eq. (32) describes the data very well, with s over 0.9. Interestingly, using the results obtained above across the pse stocks, we have , , , , leading to , in close correspondence with the direct regression result . Similar results are obtained for Index futures (Figs. 11-a & b) or for the nyse (Fig. 12), with values of which are all very similar . We have also checked that there is an average intra-day pattern which is followed in close correspondence both by and : spreads are larger at the opening of the market and decline throughout the day. Note that the trading frequency increases as time elapses, which, using Eq. (33), explains the familiar U-shaped pattern of the volatility per unit time.

5 Discussion and conclusion

The main theoretical result of this paper is the possibility to express the cost of market orders and the profit of infinitesimal market-making/taking strategies in terms of directly observable quantities, namely the spread and the lag-dependent impact function. Imposing that any market taking or liquidity providing strategies is at best marginally profitable allows one to define viable regions of the microstructural “phase-diagram” (Fig. 2) where electronic markets should operate, and suggest a linear relation between spread and instantaneous impact. This relation is in good agreement with empirical data on small tick contracts, with a slope compatible with marginal profitability of both fast market making and copy-cat market taking strategies. Somewhat paradoxically, we find that liquidity providers as a whole offer average negative costs to market orders although high frequency market making strategies still manage to get (marginally) compensated. Our analysis allows us to compare in an objective way the spreads in different markets and suggests that spreads are distinctly larger on the nyse. Note that our analysis does not require any model specific assumptions such as the nature of order flow correlations or the fraction of informed trades. In fact our results hold even if trades were all uninformed but still mechanically impact the price.

Making reasonable further assumptions, we have then shown that spread and volatility per trade are also proportional, a result that we confirm empirically with correlations above . This very simple relation means that most of the volatility comes from trading alone, and suggests that the bid-ask spread is dominated by adverse selection, provided one considers the volatility per trade as a measure of the amount of ‘information’ included in prices at each transaction. There are indeed two complementary economic interpretations of the relation in small tick markets:

-

•

(i) since the typical available liquidity in the order book is quite small, market orders tend to grab a significant fraction of the volume at the best price; furthermore, the size of the ‘gap’ above the ask or below the bid is observed to be on the same order of magnitude as the bid-ask spread itself which therefore sets a natural scale for price variations. Hence both the impact and the volatility per trade are expected to be of the order of , as observed;

-

•

(ii) the relation can also be read backward as : when the volatility per trade is large, the risk of placing limit orders is large and therefore the spread widens until limit orders become favorable.

Therefore, there is a clear two-way feedback that imposes the relation , valid on average; any significant deviation tends to be corrected by the resulting relative flow of limit and market orders. Our result therefore appears as a fundamental property of the markets organization, which should be satisfied within any theoretical description of the micro-structure. Zero intelligence models [32], or bounded-range models [26, 30, 31] fail to predict any universal relation between and .

Our relation involves the volatility per trade whereas most of the econometric work has instead focused on the volatility per unit time . The relation between the two involves the trading frequency , which is itself both time- and stock-dependent. As a function of time, we find, in agreement with [48], that volatility per trade and trading frequency are positively correlated; the volatility therefore increases because both and increase.191919The long-memory property of is argued in [47] to be related to long range correlation in the trading frequency rather than in the volatility per trade, but see [23]. Across stocks, on the other hand, the volatility per unit time exhibit only weak systematic variations with capitalization : with , whereas the trading frequency increases with capitalization as . For stocks belonging to the ftse-100, Zumbach finds [24], while for US stocks the scaling for is less clear [49]. Interestingly, our result then leads to a result between average spread and capitalization of the form , in good agreement with Zumbach’s data [24], with the impact data of Lillo et al. [45] and with our own data on the pse.

The fundamental question at this stage is to know what fixes the volatility and the trading frequency . Clearly, the trading frequency has to do with the available liquidity and the way large volumes have to be cut in small pieces. But is the volatility per unit time the primary object, driven by a fundamental process such as the arrival of news, to which the volatility per trade and therefore the spread is slaved? Or is the market micro-structure and trading activity imposing, in a bottom-up way, the value of the volatility? Understanding these coupled dynamical problems appears to be a major challenge for the theory of financial markets, and an unavoidable step to understand the interrelation between order flow and price changes, and liquidity and market efficiency [9, 43, 20, 21, 37, 15, 16, 50].

We want to warmly thank S. Bogner, J. D. Farmer, Th. Foucault and G. Zumbach for important and useful discussions. We also thank the referees for very constructive remarks, which helped improving the manuscript.

Appendix 1: Impact and volatility in the mrr model

From the basic equation determining the dynamics of the mid-point,

| (34) |

one gets:

| (35) |

Therefore, taking into account the correlation between s, and the assumption that external shocks are uncorrelated with the order flow, the impact function is:

| (36) |

Note that in this model, the ‘bare’ impact function defined in [15, 17] through:

| (37) |

is here found to be constant, equal to . Finally, one finds:

| (38) |

and

| (39) |

More generally, assuming that only the sign surprise matters, one can write, for arbitrary correlations between signs:

| (40) |

where the last term is the conditional expectation of the next sign. The impact function now generalizes to:

| (41) |

and therefore .

Appendix 2: Summary statistics

| Code | Name | Code | Name |

|---|---|---|---|

| ACA | Credit Agricole | IFG | Infogrames Entertainment |

| AC | Accor | LG | Lafarge |

| AF | Air France-KLM | LI | Klepierre |

| AGF | Assurances Generales de France | LY | Suez |

| AI | Air Liquide | MC | LVMH |

| ALS | Alstom RGPT | ML | Michelin |

| ALT | Altran | MMB | Lagardere |

| AVE | Aventis | MMT | M6-Metropole Television |

| BB | Societe BIC | NAD | Wanadoo |

| BN | Groupe Danone | NK | Imerys |

| CAP | Cap Gemini | OGE | Orange |

| CA | Carrefour | OR | L Oreal |

| CDI | Christian Dior | PEC | Pechiney |

| CGE | Alcatel | PP | PPR |

| CK | Casino Guichard (pref.) | PUB | Publicis Groupe |

| CL | Credit Lyonnais | RF | Eurazeo |

| CNP | CNP Assurances | RHA | Rhodia |

| CO | Casino Guichard | RI | Pernod-Ricard |

| CS | AXA | RNO | Renault |

| CU | Club Mediterranee | RXL | Rexel |

| CY | Castorama Dubois | SAG | Safran |

| DEC | JC Decaux | SAN | Sanofi-Aventis |

| DG | Vinci | SAX | Atos Origin |

| DSY | Dassault Systemes | SCO | SCOR |

| EF | Essilor International | SC | Simco |

| EN | Bouygues | SU | Schneider Electric |

| FP | Total | SW | Sodexho Alliance |

| FR | Valeo | TEC | Technip |

| FTE | France Telecom | TFI | Television Francaise 1 |

| GFC | Gecina | TMM | Thomson |

| GLE | Societe Generale | UG | Peugeot |

| GL | Galeries Lafayette | UL | Unibail |

| HAV | Havas | VIE | Veolia Environnement |

| HO | Thales | ZC | Zodiac |

| Code | Tnv | # | Tick | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| ACA | 15.4 | 78 | 11.1 | 347 | 9.12 | 20.76 | 18.28 | 2.30 | 0.28 | 1.70 | 5.13 |

| AC | 22.1 | 87 | 26.3 | 211 | 8.97 | 12.45 | 13.00 | 2.99 | 0.26 | 2.16 | 2.68 |

| AF | 4.0 | 40 | 7.2 | 139 | 14.40 | 25.96 | 25.57 | 3.85 | 0.23 | 2.30 | 7.01 |

| AGF | 9.6 | 80 | 16.9 | 142 | 13.32 | 19.17 | 18.88 | 4.28 | 0.28 | 2.28 | 5.46 |

| AI | 34.0 | 154 | 26.9 | 316 | 8.21 | 13.72 | 11.07 | 3.06 | 0.26 | 1.42 | 6.87 |

| ALS | 14.2 | 57 | 13.0 | 274 | 14.75 | 23.11 | 20.80 | 4.84 | 0.14 | 1.84 | 12.02 |

| ALT | 12.7 | 53 | 14.6 | 217 | 23.66 | 30.75 | 27.88 | 7.15 | 0.17 | 2.71 | 11.04 |

| AVE | 134.1 | 362 | 62.6 | 536 | 6.70 | 11.18 | 7.31 | 2.59 | 0.21 | 1.72 | 7.54 |

| BB | 0.8 | 30 | 11.9 | 16 | 28.80 | 43.94 | 47.51 | 7.78 | 0.33 | 1.66 | 2.55 |

| BN | 59.5 | 310 | 45.9 | 324 | 6.30 | 11.80 | 7.79 | 2.37 | 0.28 | 1.03 | 7.62 |

| CAP | 34.7 | 94 | 28.9 | 300 | 12.71 | 17.27 | 17.03 | 4.39 | 0.20 | 2.55 | 5.17 |

| CA | 79.8 | 229 | 40.1 | 497 | 6.92 | 12.20 | 9.16 | 2.48 | 0.22 | 1.85 | 5.35 |

| CDI | 5.1 | 59 | 14.9 | 86 | 18.76 | 32.32 | 29.08 | 6.23 | 0.29 | 1.74 | 2.79 |

| CGE | 79.8 | 152 | 21.3 | 936 | 10.49 | 20.94 | 14.85 | 3.31 | 0.13 | 1.70 | 15.37 |

| CK | 0.3 | 37 | 11.4 | 6 | 20.43 | 46.72 | 32.24 | 7.37 | 0.22 | 0.93 | 8.06 |

| CL | 30.1 | 163 | 23.0 | 328 | 8.05 | 13.60 | 13.04 | 1.96 | 0.36 | 1.77 | 3.43 |

| CNP | 1.7 | 41 | 9.3 | 45 | 15.58 | 31.12 | 33.74 | 3.53 | 0.31 | 1.43 | 2.67 |

| CO | 13.8 | 98 | 22.9 | 151 | 10.38 | 15.43 | 14.42 | 3.47 | 0.27 | 1.50 | 6.58 |

| CS | 96.1 | 144 | 36.6 | 657 | 8.32 | 12.78 | 10.17 | 3.13 | 0.17 | 1.97 | 6.39 |

| CU | 1.0 | 22 | 7.7 | 32 | 30.02 | 44.83 | 47.65 | 8.85 | 0.23 | 1.84 | 3.97 |

| CY | 15.4 | 2148 | 77.1 | 50 | 8.64 | 14.61 | 14.49 | 2.35 | 0.26 | 1.67 | 8.03 |

| DEC | 0.7 | 27 | 12.7 | 13 | 43.75 | 78.92 | 77.84 | 13.81 | 0.33 | 1.53 | 8.15 |

| DG | 16.8 | 134 | 25.4 | 165 | 8.02 | 14.05 | 10.90 | 2.76 | 0.22 | 1.24 | 7.76 |

| DSY | 10.4 | 65 | 19.6 | 133 | 17.06 | 22.11 | 23.83 | 5.71 | 0.27 | 2.30 | 5.28 |

| EF | 5.6 | 59 | 20.4 | 69 | 13.21 | 21.38 | 23.01 | 3.94 | 0.25 | 1.90 | 2.52 |

| EN | 17.8 | 66 | 21.3 | 210 | 10.15 | 14.55 | 14.35 | 3.47 | 0.25 | 1.85 | 3.46 |

| FP | 322.4 | 662 | 114.4 | 705 | 4.96 | 9.17 | 4.86 | 2.12 | 0.20 | 1.49 | 6.71 |

| FR | 8.3 | 80 | 24.1 | 86 | 13.84 | 20.60 | 22.46 | 4.39 | 0.25 | 1.99 | 3.50 |

| FTE | 112.7 | 137 | 29.5 | 956 | 9.12 | 15.04 | 12.57 | 2.93 | 0.14 | 1.85 | 6.39 |

| GFC | 0.3 | 35 | 9.9 | 7 | 17.85 | 27.74 | 31.55 | 4.56 | 0.27 | 0.98 | 5.62 |

| GLE | 82.7 | 239 | 46.0 | 449 | 8.07 | 12.70 | 9.27 | 3.04 | 0.23 | 2.26 | 7.07 |

| GL | 0.9 | 43 | 13.6 | 17 | 24.34 | 41.34 | 39.96 | 6.92 | 0.29 | 1.38 | 7.24 |

| HAV | 8.1 | 57 | 14.6 | 139 | 21.15 | 32.44 | 26.53 | 7.41 | 0.18 | 1.91 | 17.15 |

| HO | 11.3 | 61 | 19.7 | 143 | 10.68 | 15.02 | 15.86 | 3.65 | 0.29 | 1.94 | 2.85 |

| IFG | 3.2 | 24 | 4.9 | 163 | 29.05 | 40.35 | 32.95 | 8.51 | 0.15 | 2.31 | 21.79 |

| LG | 38.2 | 193 | 36.6 | 261 | 7.82 | 13.31 | 9.99 | 2.90 | 0.24 | 1.67 | 7.33 |

| LI | 0.2 | 50 | 15.8 | 3 | 14.43 | 29.90 | 23.18 | 4.69 | 0.20 | 0.70 | 8.54 |

| Code | Tnv | # | Tick | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| LY | 58.4 | 111 | 28.8 | 507 | 8.40 | 12.84 | 11.94 | 3.11 | 0.20 | 1.97 | 4.31 |

| MC | 52.9 | 143 | 34.7 | 381 | 8.01 | 12.41 | 10.75 | 3.01 | 0.26 | 2.20 | 4.18 |

| ML | 13.2 | 71 | 21.2 | 156 | 10.23 | 14.98 | 15.36 | 3.35 | 0.30 | 1.93 | 2.71 |

| MMB | 13.3 | 76 | 18.9 | 177 | 10.67 | 15.96 | 15.84 | 3.60 | 0.25 | 1.94 | 3.50 |

| MMT | 0.7 | 33 | 10.1 | 17 | 33.82 | 49.77 | 48.42 | 9.71 | 0.32 | 1.66 | 3.57 |

| NAD | 4.6 | 47 | 6.0 | 188 | 14.39 | 31.27 | 20.91 | 4.11 | 0.17 | 1.89 | 20.36 |

| NK | 1.1 | 43 | 13.4 | 21 | 25.95 | 42.89 | 39.34 | 7.69 | 0.29 | 1.40 | 8.07 |

| OGE | 36.4 | 182 | 21.2 | 429 | 11.40 | 21.53 | 13.35 | 3.57 | 0.16 | 1.82 | 16.03 |

| OR | 68.0 | 211 | 41.9 | 406 | 7.30 | 12.45 | 9.45 | 2.76 | 0.25 | 1.39 | 6.59 |

| PEC | 9.5 | 110 | 31.9 | 75 | 15.06 | 23.71 | 24.89 | 5.07 | 0.24 | 2.41 | 5.45 |

| PP | 36.8 | 154 | 31.5 | 292 | 10.08 | 15.44 | 13.25 | 3.39 | 0.25 | 2.23 | 7.23 |

| PUB | 11.9 | 78 | 27.3 | 109 | 15.08 | 21.19 | 22.92 | 4.97 | 0.23 | 2.46 | 3.85 |

| RF | 0.1 | 25 | 7.0 | 3 | 22.27 | 37.26 | 32.69 | 7.07 | 0.23 | 0.72 | 8.25 |

| RHA | 2.1 | 32 | 9.7 | 55 | 21.45 | 33.99 | 32.97 | 6.71 | 0.22 | 1.87 | 10.83 |

| RI | 12.6 | 138 | 39.1 | 80 | 10.49 | 16.82 | 16.01 | 3.64 | 0.22 | 1.49 | 6.42 |

| RNO | 35.8 | 158 | 34.4 | 260 | 8.01 | 12.80 | 11.13 | 2.71 | 0.25 | 2.27 | 4.38 |

| RXL | 0.7 | 34 | 13.0 | 14 | 31.30 | 51.91 | 50.49 | 9.21 | 0.26 | 1.50 | 6.77 |

| SAG | 1.5 | 36 | 10.3 | 35 | 24.59 | 43.15 | 42.89 | 7.29 | 0.22 | 1.73 | 7.48 |

| SAN | 94.2 | 301 | 56.4 | 417 | 7.76 | 12.18 | 8.60 | 3.04 | 0.25 | 1.49 | 7.92 |

| SAX | 6.0 | 57 | 20.4 | 73 | 23.28 | 33.48 | 33.79 | 7.45 | 0.27 | 2.58 | 5.23 |

| SCO | 2.0 | 25 | 9.3 | 55 | 35.67 | 38.88 | 40.00 | 8.37 | 0.23 | 2.16 | 7.40 |

| SC | 0.5 | 55 | 13.9 | 10 | 12.24 | 21.08 | 19.01 | 3.58 | 0.22 | 1.28 | 6.10 |

| SU | 26.2 | 129 | 33.0 | 198 | 9.52 | 14.60 | 13.43 | 3.30 | 0.26 | 2.15 | 5.63 |

| SW | 11.2 | 67 | 19.5 | 144 | 14.48 | 18.19 | 20.40 | 4.26 | 0.32 | 1.92 | 3.22 |

| TEC | 9.4 | 123 | 31.6 | 74 | 16.27 | 24.27 | 25.77 | 5.06 | 0.24 | 2.18 | 7.31 |

| TFI | 17.4 | 63 | 21.0 | 207 | 11.91 | 15.87 | 16.19 | 4.09 | 0.25 | 2.07 | 3.71 |

| TMM | 28.0 | 78 | 20.8 | 338 | 10.08 | 16.08 | 15.59 | 3.18 | 0.19 | 2.34 | 4.29 |

| UG | 33.2 | 141 | 36.2 | 229 | 7.95 | 11.91 | 10.80 | 2.86 | 0.26 | 2.11 | 4.43 |

| UL | 3.0 | 64 | 22.9 | 33 | 14.61 | 24.45 | 23.47 | 4.87 | 0.27 | 1.41 | 8.07 |

| VIE | 19.8 | 77 | 24.8 | 199 | 11.52 | 16.60 | 17.81 | 3.75 | 0.23 | 2.23 | 3.57 |

| ZC | 0.9 | 33 | 8.7 | 26 | 24.95 | 41.99 | 42.40 | 7.28 | 0.24 | 1.64 | 4.21 |

| Code | Turnover | # trade | Tick | ||||||

|---|---|---|---|---|---|---|---|---|---|

| LMEB | 262 | 21 | 199 | 211 | 8.4 | 46.7 | 4.4 | 11.5 | 46.6 |

References

- [1] A. Orléan, Le pouvoir de la finance, Odile Jacob, Paris (1999); A quoi servent les marchés financiers ?, in Qu’est-ce que la Culture ?, Odile Jacob, Paris (2001).

- [2] M. O’Hara, Market microstructure theory, Cambridge, Blackwell, (1995).

- [3] B. Biais, Th. Foucault, P. Hillion, Microstructure des marchés financiers, PUF (1997)

- [4] A. Madhavan, Market microstructure: A survey, Journal Financial Markets, 3, 205 (2000)

- [5] L. R. Glosten, P. Milgrom, Bid, Ask and Transaction Prices in a Specialist Market with Heterogeneously Informed Traders, Journal of Financial Economics 14 71 (1985)

- [6] L. R. Glosten, Components of the Bid-Ask Spread and the Statistical Properties of Transaction Prices, Journal of Finance, 42 293 (1987).

- [7] J. Hasbrouck, Measuring the information content of stock trades, Journal of Finance, XLVI, 179 (1991).

- [8] R. D. Huang, H. R. Stoll, The components of the Bid-Ask spread: A general approach, Review of Financial Studies, 4 995 (1997).

- [9] A. Madhavan, M. Richardson, M. Roomans, Why do security prices fluctuate? a transaction-level analysis of NYSE stocks, Review of Financial Studies, 10, 1035 (1997).

- [10] B. Hollifield, A. Miller, P. Sandas, Empirical Analysis of Limit Order Markets, forthcoming Review of Economic Studies.

- [11] H. Stoll, Friction, Journal of Finance , 55 1479 (2000)

- [12] F. Black, Towards a fully automated exchange, Review Financial Analysts, 27, 29 (1971).

- [13] A. S. Kyle, Continuous auctions and insider trading, Econometrica 53, 1315 (1985).

- [14] W.-M. Liu, Monitoring and Limit Order Submission Risks, University of New South Wales Working Paper, 2005.

- [15] J. P. Bouchaud, Y. Gefen, M. Potters, M. Wyart, Fluctuations and response in financial markets: The subtle nature of ‘random’ price changes, Quantitative Finance 4, 176 (2004).

- [16] F. Lillo, J. D. Farmer, The long memory of efficient markets, Studies in Nonlinear Dynamics and Econometrics, 8, 1 (2004).

- [17] J. P. Bouchaud, J. Kockelkoren, M. Potters, Random walks, liquidity molasses and critical response in financial markets, Quantitative Finance, 6, 115 (2006).

- [18] H. Bessembinder, Bid-Ask Spread in the Interbank Foreign Exchange Markets, Journal of Financial Economics, 35, 317 (1994)

- [19] M. Coppejans, I. Domowitz, A. Madhavan, Liquidity in Automated Auction, Working paper, 2001.

- [20] T. Chordia, R. Roll, A. Subrahmanyam, Order Imbalance, Liquidity and Market Returns, Journal of Financial Economics, 65, 111 (2001).

- [21] T. Chordia, A. Subrahmanyam, Order imbalance and individual stock returns, Journal of Financial Economics, 72 485 (2004)

- [22] T. Chordia, L. Shivakumar, A. Subrahmanyam, Liquidity dynamics across small and large firms, Economic Notes, 33 111 (2004)

- [23] L. Gillemot, J. D. Farmer, F. Lillo, There’s more to volatility than volume, physics/0510007

- [24] G. Zumbach, How the trading activity scales with the company sizes in the ftse 100, Quantitative Finance, 4, 441 (2004)

- [25] Th. Foucault, Order flow composition and trading costs in a dynamic limit order market, Journal of Financial Market, 2, 99 (1999)

- [26] Th. Foucault, O. Kadan, E. Kandel, Limit order book as a market for liquidity, Review of Financial Studies, 18, 1171 (2003).

- [27] M. G. Daniels, J. D. Farmer, G. Iori, E. Smith, Quantitative model of price diffusion and market friction based on trading as a mechanistic random process, Phys. Rev. Lett. 90, 108102 (2003).

- [28] E. Smith, J. D. Farmer, L. Gillemot, S. Krishnamurthy, Statistical theory of the continuous double auction, Quantitative Finance 3, 481 (2003).

- [29] J.P. Bouchaud, M. Mézard, M. Potters, Statistical properties of stock order books: empirical results and models, Quantitative Finance 2, 251 (2002).

- [30] H. Luckock, A steady-state model of the continuous double auction, Quantitative Finance, 3, 385 (2003)

- [31] I. Rosu, A dynamic model of the limit order book, Working paper, 2005.

- [32] J. D. Farmer, P. Patelli and I. Zokvo, The predictive power of zero intelligence in financial markets, PNAS 102, 2254-2259 (2005)

- [33] S. Mike, J. Doyne Farmer, An empirical behavioral model of price formation, physics/0509194.

- [34] P. Weber, B. Rosenow, Order book approach to price impact, Quantitative Finance, 5, 357 (2005)

- [35] F. Lillo, S. Mike, and J. D. Farmer, Theory for long memory in supply and demand, Physical Review E, 7106, 287 (2005).

- [36] R. Almgren, C. Thum, E. Hauptmann, H. Li, Direct estimation of equity market impact, working paper (May 2005).

- [37] C. Hopman, Are supply and demand driving stock prices?, MIT working paper, Dec. 2002, to appear in Quantitative Finance.

- [38] P. Handa, R. A. Schwartz, A. Tiwari, The ecology of an order-driven market, Journal of Portfolio Management, Winter (1998), 47-56.

- [39] L. Harris, J. Hasbrouck, Market vs. limit orders: the SuperDOT evidence on order submission strategy, Journal of Financial and Quantitative Analysis 31, 213-31 (1996).

- [40] P. Handa, R. A. Schwartz, Limit order trading, J. Finance, 51, 1835 (1996).

- [41] see e.g. H. Bessembinder, Issues in assessing trade execution costs, Journal of Financial Markets 6, 233 (2003), and refs. therein.

- [42] J. D. Farmer, L. Gillemot, F. Lillo, S. Mike, A. Sen, What really causes large price changes?, Quantitative Finance, 4, 383 (2004).

- [43] M. D. Evans, R. K. Lyons, Order Flow and Exchange Rate Dynamics, Journal of Political Economy, 110 170 (2002)

- [44] B. Rosenow, Fluctuations and market friction in financial trading, Int. J. Mod. Phys. C, 13, 419 (2002).

- [45] F. Lillo, J. D. Farmer, R. Mantegna, Master curve for price-impact function, Nature, 421, 129 (2003).

- [46] V. Plerou, P. Gopikrishnan, X. Gabaix, H. E. Stanley, Quantifying Stock Price Response to Demand Fluctuations, Phys. Rev. E 66, 027104 (2002).

- [47] V. Plerou, P. Gopikrishnan, L. A. N. Amaral, X. Gabaix, and H. E. Stanley, Diffusion and Economic Fluctuations, Phys. Rev. E 62, 3023 (2000).

- [48] R. F. Engle, The econometrics of ultra-high frequency data, Discussion paper 96-15, University of California, San Diego, 1996.

- [49] Z. Eisler, J. Kertecz, Size matters, some stylized facts of the market revisited, xxx.lanl.gov/ physics/0508156.

- [50] T. Chordia, R. Roll, A. Subrahmanyam, Liquidity and Market Efficiency, Working paper 2005.