Evaluation of Tranche in Securitization and

Long-range Ising Model

K Kitsukawa †111kj198276@sfc.keio.ac.jp

, S Mori ‡222mori@sci.kitasato-u.ac.jp and

M Hisakado ¶333masato_hisakado@standardpoors.com† Graduate School of Media and Governance, Keio University,

Endo 5322, Fujisawa, Kanagawa 252-8520, Japan

‡ Department of Physics, School of Science,

Kitasato University, Kitasato 1-15-1 , Sagamihara, Kanagawa 228-8555, Japan

¶ Standard & Poor’s, Marunouchi 1-6-5, Chiyoda-ku, Tokyo 100-0005, Japan

Abstract

This econophysics work studies the long-range Ising model

of a finite system with spins and

the exchange interaction and

the external field as a model

for homogeneous credit portfolio of assets with

default probability and

default correlation .

Based on the discussion on the phase diagram,

we develop a perturbative calculation method for the model and

obtain explicit expressions for and the normalization

factor in terms of the

model parameters and .

The effect of the default correlation

on the probabilities for defaults and on the

cumulative distribution function are discussed.

The latter means the average loss rate of the“tranche”

(layered structure ) of the

securities (e.g. CDO), which are synthesized from a pool of many

assets. We show that the expected loss rate of the

subordinated tranche decreases with and that of the senior

tranche increases linearly, which are important in their

pricing and ratings.

pacs:

05.50.+q,02.50.-r

††: Physica A

1 Introduction

The statistical properties of the models for credit risks

have been widely discussed in the past ten years from the standpoint of

financial

engineering [1, 2] and econophysics

[3, 4].

In the context of econophysics, the mechanism of systemic failure in

banking has been studied [5, 6]. Power law behavior of the

distributions of

avalanches and several scaling laws in the context of percolation theory

were found.

On the other hand, in

financial engineering, the

evaluation of the effect of the

correlation between the rates of return of assets or

between the default of assets is a

hot topic and is widely discussed from theoretical

and empirical

viewpoints. Empirically, historically realized values of correlations

and their implied values, which are estimated based on the

market value

of credit derivatives,

are compared and their discrepancies, called correlation risk premium,

attract investors’ interests from the viewpoint of portfolio

management [7].

Theoretically, many statistical models are proposed for modeling

credit risk of the pool of many assets

[2, 8, 9, 10, 11, 12, 13, 14, 15, 16].

There are two categories in the models. The models in the

first category use two state discrete variables which describe whether the

asset is defaulted or not [9, 10, 5, 11].

In the financial literature a

two-valued variable

takes values and depending on whether

the -th asset described by is not defaulted or defaulted.

The default probability is defined by the average number of

defaulted assets per an asset as .

Here means the expectation value.

Ising Spin variable

is also used and it is related to as .

Moody’s Binomial (Expansion) approach [9], Moody’s correlated

Binomial model [10], Long-range Ising model [11]

are in this category.

The default correlation is defined by the

simultaneous default probability. If we denote the probability

distribution of two asset as , the

default correlation is defined by

(1)

Here, and are the probability

distributions of and and they are calculated from

the joint probability distribution .

In the second category, the models adopt a continuous variable for

the earning rate of an asset and correlation between the earning rates

is introduced

[8, 12, 13, 14].

On the assumption that the

earing rates obey multivariate normal distribution with correlation

, the probability for the simultaneous default of

the -th and -th assets is given by

(2)

Here and are the default probabilities of the

-th and -th assets and is the inverse function of the

normal distribution function. The variables mean the earing rates

of the two assets. If the random variable (or ) becomes lower than

(resp. ),

the -th (-th) asset is judged to be defaulted.

The correlation parameter is named as “asset correlation”

and and are related via the equation (1).

The conditionally independent model [12],

such as the Merton based model, the credit metrix model [13]

and the copula model [14] are in

the second category.

The reason why default or asset correlations are widely discussed

recently is that the pricing of Asset backed Security (ABS),

like CDO, needs detailed information about

the probabilities for defaults.

Here CDO is an abbreviation for Collateralised debt obligation,

which is a financial innovation to securitise portfolios of

defaultable assets. The portfolio of the underlying debts (assets)

collateralizes the securitites (obligations), CDO is a kind of ABS.

Securitization by CDO, we mean to synthesize securities

based on a pool of many assets, like loans (CLO), commercial bonds

(CBO) etc.

In the process, layered structure is introduced and securities with

high priority (reliability), which is called senior tranche, and

those with low priority (called subordinated tranche or equity) are

synthesized.

Between the senior tranche and the equity, the mezzanine tranche with middle

priority is also synthesized.

The difference between them is that if some of the assets

in the pool are defaulted, the security with lower priority

loses its value at first. If the rate of defaulted assets

exceeds some threshold value , e.g. for the mezzanie

tranche and for the senior tranche,

those with higher priority begin to lose their values.

The equity play the role of “shock absorber”.

By the “tranche” structure, the risk of the senior tranche is reduced

and investors feel safe about the investment.

On the other hand, the interest rates of the securities of the equity and

the mezzanine tranche

are set to be higher than those of the senior tranche and

the subordinated tranches are high-risk-high-return products.

The default correlation becomes important when one try to estimate

the expected loss in each tranche, which is essential in the evaluation

of its price (premium).

For example, we assume a pool of homogeneous assets

with default probability

. If there is no

correlation between the defaults, is the binomial

distribution and has a peak at .

The standard deviation is

for small . If the threshold value

is large enough, the upper tranche does not suffer from the defaults

in the pool. On the other hand, in the extreme case where

the default correlation is , all assets behave

in the same way and there are only two cases.

One case is that all assets are not defaulted and the probability

for the case is . The other case is that all assets are

defaulted simultaneously and the probability is .

In the strong correlation limit (),

when there occur defaults, all assets become defaulted simultaneously.

Both senior and subordinated tranches lose their values completely.

If there occurs no default, both tranche does not suffer from any

damage.

The essential problem is to know the dependence of

the probabilities . It is important to estimate

the expected loss rate of each tranche based on .

In addition, we should also study

which probabilistic model is good or useful in order to describe

the behaviors of the assets.

This paper deals with these problems.

The organization of the paper is as

follows. In section 2, we study the phase diagram of

finite size long-range Ising model and

show

that the

assets begin to be correlated in the “Two Peak” Phase

in the plane.

The realistic magnitude of the default correlation ranges from

1 % to several % [2],

only the Two Peak Phase

is interesting from the financial engineering viewpoint.

Section 3 is devoted to the calculation of the

important parameter and in terms of and .

Here, we develop a perturbation method which is based on the discussions

in section 2. Up to zero-th order in the perturbation theory,

is expressed as the superposition

of two binomial distributions, corresponding to the two peaks of .

The developed method and obtained relations

are useful when one apply the

long-range Ising model to the evaluation and hedging of the securities

with tranches.

In section 4, we study the

dependence

of

and of the expected loss rates of the tranches.

For the latter purpose,

we introduce the cumulative distribution

and discuss that they are directly related

with the average loss rates of tranches.

As the correlation becomes strong (with fixed default probability

), the left peak becomes taller and moves towards to the

origin ().

The right peak also becomes taller and shifts to .

Its area approaches to as comes close to 1.

These behaviors are different from those of the binomial expansion

approach, where has only one peak and its shape

becomes broader as increases. We then discuss

the dependence of .

for large

increases linearly with and the senior tranche

cannot avoid the default damage of the assets pool, even when we set

to be large. This crucial behavior of the long-range Ising model

has been pointed out previously [11], we have clarified

the importance in the evaluation of the tranches.

Section 5 is dedicated to concluding remarks and

future problems. We discuss the usefulness of the long-range Ising model

from the viewpoint of financial engineering.

2 Model and Phase Diagram in plane

We use Ising Spin variables which

represent states of assets in the reference pool.

Here indicates

default of -th asset and means that the -th

asset is not defaulted.

We denote the number of spins by , so the number of

defaulted assets is .

The probability distribution for the states of the assets

is assumed to be described by the following canonical distribution with the long-range

Ising model of a finite system with spins and

the exchange interaction and

the external filed , which are measured in units of Boltzmann

constant times temperature.

(3)

We do not omit the terms in the Hamiltonian for later convenience.

As is well-known, the exchange interaction

controls the strength of the

correlation between and and the external field favors

one of the two spin states. In the actual case where

the spin variable represents

the states of the assets, the

default probability is at most a few percent and

almost all assets are not defaulted (). The sign of the external

field is set to be .

The reason to choose the long-range Ising

model is that it gives the default distribution directly.

In [11], another motivation for the long-range Ising model has

been discussed and their conclusion is that

the model is the most natural choice from the viewpoint of

the Maximum

Statistical Entropy principle.

The two parameters and are introduced as Lagrange multipliers

which ensure that the default probability and the default correlation

of the model are and .

From the economical viewpoint, we can interpret the model as a kind

of factor model. Here, the term ’factor’ means the systematic risk

factor

or the state of the business cycle [2].

In a boom, we have fewer defaults than in a recession.

We denote the state of the business cycle as

and assume that

the defaults of the assets are independent from each other,

conditional on the realization of the systematic factor .

The joint probabilities for the assets

and the business cycle variable is assumed to be written as

(4)

Here, the random variable obeys the probability density function

and the denominator is the normalization term.

Condition on the realization , the each asset state becomes independent

from each other and the default probability is given as

(5)

The default probability is a decreasing function of

and for a boom (recession) is large (small).

In order to derive the long-range Ising model starting from the

above factor mode, we assume that obeys the standard normal

distribution with mean and variance .

(6)

By averaging over the possible realization of weighted with

the above , we obtain the expression for the long-range Ising

model.

(7)

The validity of the Maximum

Statistical Entropy principle or the factor model with the normally

distributed business factor should be checked by the

comparison with other more reliable models.

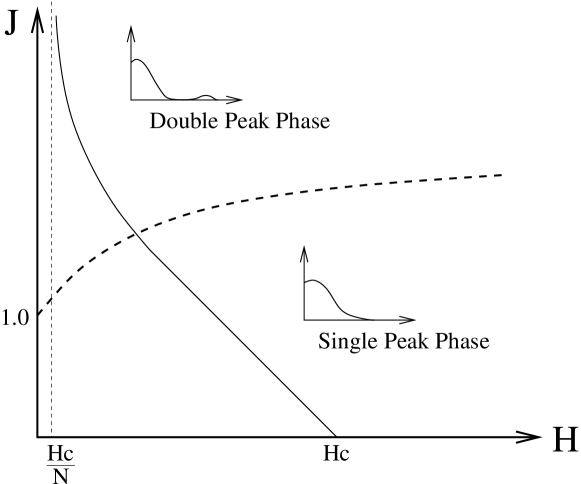

Figure 1: Phase diagram in plane. For large and small ,

has a single peak at .

We call the

region as “Single Peak” Phase.

For small and large , there are

two

peaks in and we call the region “Two Peak” Phase.

The phase boundary is depicted with the broken line (– – –).

The solid

line (——) corresponds to a constant line.

It starts at , where . In the limit, the line

approaches asymptotically and

.

The Hamiltonian of the long-range Ising model depends on the spin

variables only through the combination of the magnetization

. There is a simple relation between

and as ,

the default number distribution function is

(8)

The default probability is defined by the expectation value of

as

(9)

Here is the expectation value with the probability

distribution (8).

For , the probability distribution (8) becomes

that of the binomial distribution and there is a

relation between and as

(10)

We denote this value of as .

On the other hand, for limit, there are only 2

configurations with all spins up or all spins down that have nonzero

probabilities. The probabilities are

(11)

From the relation , one obtains

the following relation between and for as

For general and , it is difficult to obtain .

However, for large enough , by changing variable from

to in eq.(8), we can estimate

by the saddle point approximation.

The saddle point equation is

(12)

Of course, by changing variable from to

the magnetization per spin ,

the saddle point equation is transformed into the

famous self-consistent equation of the magnetization

[17].

Depending on the values of the parameters ,

there are two cases. For large and small , the equation

(12) has only one solution .

We call this region in

the plain as “One Peak” Phase, because the probability

distribution has a single peak at .

is almost the same with in the One Peak Phase.

For small and large , the equation (12) has

three solutions, two are

at maxima and one is at minimum.

We call the

region in the plane as “Two Peak” Phase,

as the reader may easily anticipate the reason.

In the case, there is no simple relation between and the

solutions . If is large, the solution

is almost the same with . However, when the

correlation is large, the strength of is of the order of

and we cannot neglect the second peak .

In the case, and the average value of

and with and

corresponds to the value of .

For example, when and , the

average value of and

with probabilities eq.(11) is equal to .

In figure 1, we summarize the situation.

The solid curve (——) in the

plane corresponds to the constant line. The dotted line (– – –)

is the “phase transition” line between the One-Peak Phase and the Two

Peak Phase. In the remainder of the

section, we study the correlation in the phase

diagram. We will see that is almost zero in the One Peak Phase.

Only in the Two Peak Phase can take nonzero value.

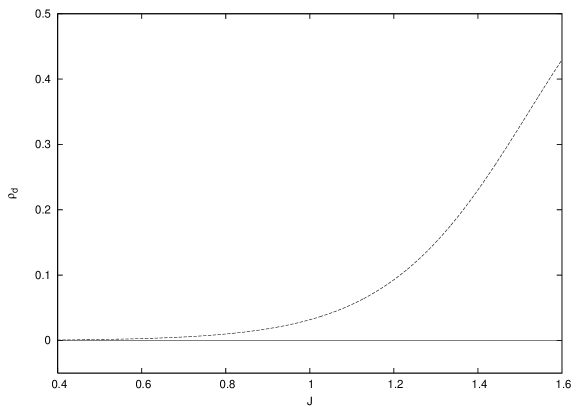

Figure 2: Second peak contribution in .

Along the line with eq.(17), we plot the approximated

estimation for . The lower solid line (——) shows the data

from eq.(15) and the data from eq.(16) are depicted

with upper dotted curve ().

We discuss the default correlation and

recall the definition . In order to obtain

, in equation (3), we

take the trace over .

(13)

The trace over is replaced by the summation

over of Spins. We obtain

(14)

If the system size is large,

the summation over is replaced by the estimation at the

saddle points.

In the One-Peak region, the saddle point

is at and is given by

(15)

In the Two Peak region, two saddle points contribute to the

summation and is estimated as

(16)

Here and are the probabilities

for the two peaks and .

In the One Peak phase, the constant line in the

plane

is almost given by the following relation between and

(17)

We calculate the default correlation with equations

(15) and (16)

on the above approximate constant line.

About the two saddle points and their probabilities

, we take them the values

at and . We set and

.

We set and we plot vs in figure 2.

We see that the correlation with equation (15),

which is plotted with solid line (——),

does not become large

even in the Two Peak Region. On the other hand,

with equation

(16), which is depicted with dotted line ()

becomes large in the Two Peak Region.

We see that the existence of the second peak in

plays a crucial role in the emergence of correlation

in the long-range Ising model.

3 Perturbative Calculation and Second Peak Contribution

In this section, we try to calculate several quantities

of interest of the long-range Ising model. In particular,

we obtain the expressions for and in terms of the

model parameter and .

In addition, we also obtain the

expression for the

probability (or weight) of the second peak ,

which means that almost all assets are defaulted [11].

The probability plays a crucial

role when one discuss the evaluation

of the tranche.

When one calculate , one way is to calculate

and . Here, we calculate the moment of

with the probability distribution eq.(8). The default probability

is then given by . About the default

correlation , we start from the following relation.

(18)

The magnetization and is related as and

, we obtain the following expression

(19)

In order to calculate the moment with eq.(8), the

quadratic term

prevents us from

taking summation over . As we have noted previously, the

distribution with is binomial distribution and taking summation

over is easy.

In addition, the is at most a few percent

and the distribution have a peak very close to

(and the second peak at in the Two Peak Phase).

We expand the quadratic term as

(20)

and perform the calculation of the moment

perturbatively. The expansion is about , which

is evaluated as

. In the actual risk

portfolio problem, is at most and the system size

is several hundred, the

perturbative approximation is considered to be applicable.

We also note that, in the Two Peak Phase, the above expansion

should be carried out also at .

In order to perform the calculation in more concrete manner,

we use variables and start from the

following expression for the Hamiltonian.

(21)

(22)

In the vicinity of , we denote as

and we can expand the quadratic term in

eq.(21). Likewise, in the vicinity of ,

we call as and it can also be expanded in .

(23)

(24)

is the normalization constant to ensure that

. To the zero-th order perturbation

approximation and are binomial

distributions and

is given by the superposition of these distributions.

We summarize the

situation as

(25)

Here is set to be at the middle of the interval .

The moment is calculated with the following equation.

(26)

The summation over is from to , however

damps rapidly in , it is not so bad to change the

range from to . About the range of

is . We change variable from to and

denote the probability distribution

also as .

(27)

also damps

rapidly in , we will change the summation

range from to .

is then calculated perturbatively as

(28)

The normalization constant is calculated as

(29)

In equation (29), we denote the two terms as , which come

from the summation over and .

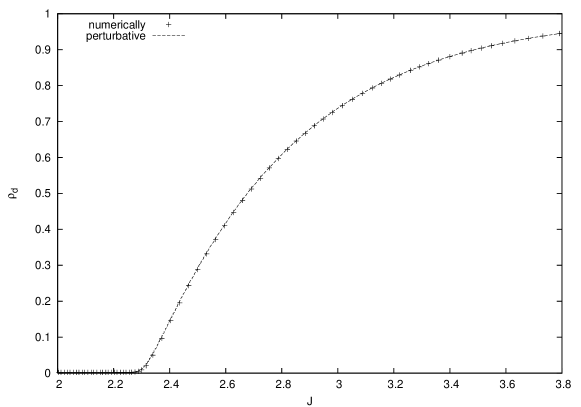

Figure 3: The default correlation on a constant line.

and we plot versus . is set to be the

value which realize for .

The solid line (——) shows

the result from the perturbative calculation up to second order in

and the line with symbols

shows numerically calculated exact data.

In the above calculation, moments of the binomial distribution

appears frequently. We introduce the following unnormalized

binomial moments .

(30)

The parameters are defined as .

Calculations of is straightforward.

The zero-th moment is given by

(31)

The -th moment is then obtained by

differentiating with respect to repeatedly.

(32)

We show the results for the first 6 moments, which are necessary for

the second order perturbative calculation.

(33)

(34)

(35)

(36)

(37)

(38)

where and .

In general, the -th binomial moment is

calculated as

(39)

where the coefficients for

is calculated with the following recursive relations.

(40)

and with the conditions for and .

With these preparations, we are ready to write down the results.

The perturbative calculation of the normalization

constant is given as

(41)

The moment is given by

(42)

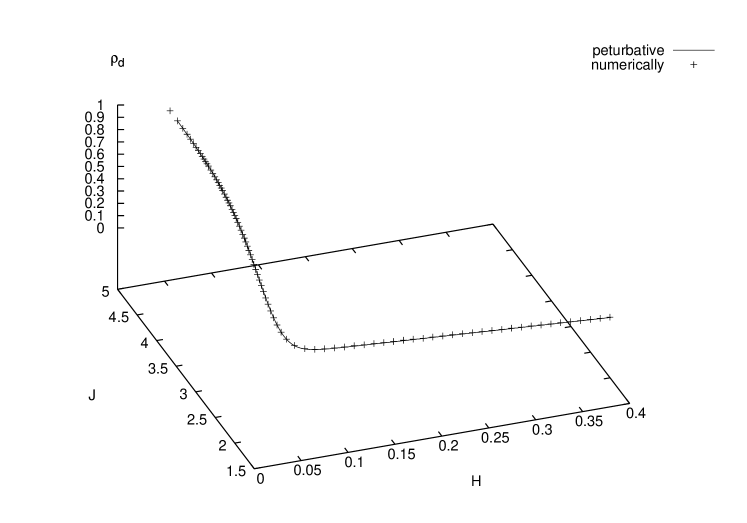

Figure 4: 3-dimensional plot of in

space.

The solid line (——) shows

the result from the perturbative calculation up to second order in

and the line with symbols

depicts numerically calculated exact data.

The conditions are the same with those

in figure 3.

Putting these results into and

eq.(19),

the expressions for and in

terms of model parameters are obtained. In addition, the weight

of the second peak , that is the probability of almost

all assets are defaulted, is estimated as

(43)

As we have noted previously, the zero-th order

approximation means that we express as a

superposition of two binomial distributions. In the case, the

results for and can be written down

in the following simple expressions.

(44)

(45)

(46)

(47)

The subscript indicates the zero-th order

perturbation results.

In figure 3, we

shows the result for along the constant line.

is set to be and with solid line (——)

we show the data from the above

perturbative calculation up to second order in .

The line with symbols

depicts the numerical data.

The two lines coincide well and the match is very good as long as

is set to be small. Figure 4 is the 3-dimensional plot

of the data in space. begins to be large

in the Two Peak region and its rapid growth is well captured by the

above perturbative calculation.

4 Effect of on and on average loss rates

of tranches

We would like to discuss the effect of default correlation

on the probabilities and

on the tranche synthesized from the pool of the

homogeneous assets. In order to discuss the latter case,

we introduce the cumulative

distribution function , which is directly related with

the average loss rate of the tranche.

The default rate and the system size is fixed.

When we show numerical data, we set and .

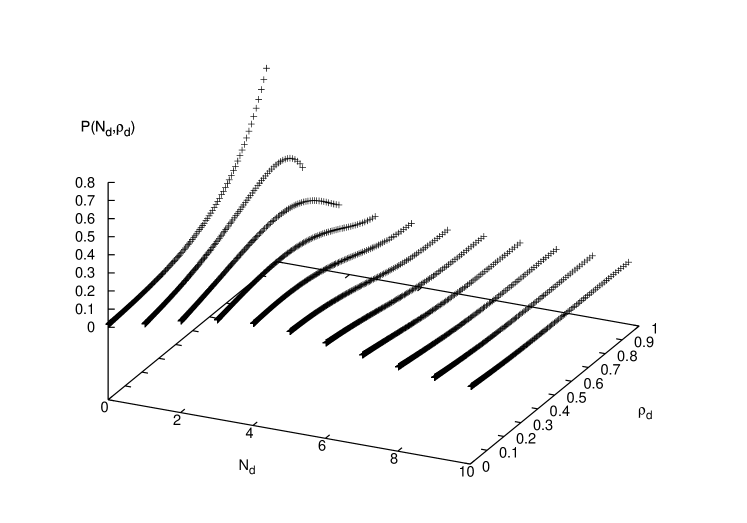

Figure 5:

Plot of vs .

and .

At first, we discuss the former case, the

effect on the probabilities . Here we

write down their dependence explicitly.

The case is easy and is only the

binomial distribution . It has a single peak at

and the width is roughly .

For ,

and as

becomes large, approaches .

In figure 5, we plot versus for

. The system size and .

grows monotonically as grows.

For ,

at first increases and then decreases

as a function of .

On the other hand, for ,

decreases

with .

is small and damps rapidly in

for ,

is almost zero

for any , which holds for .

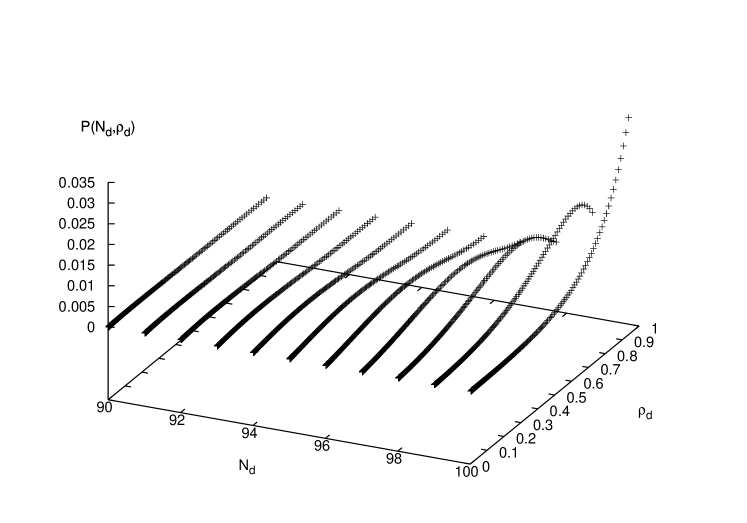

Figure 6 depicts the plots of

for .

and ,

grows monotonically from to . For ,

is upward convex with respect to .

The area of the second peak

becomes greater with the increase of and

increases for . As becomes large, the width of the

second peak becomes narrow and for

decreases. On the other hand, increases

monotonically to .

Figure 6:

Plot of vs .

and .

To sum up, for , is and

it has a single peak. The width of the peak is order

and it

is small for small . As grows, the system

is in the Two Peak Phase.

At the zero-th order perturbative approximation,

is a superposition of two binomial distributions.

has a peak at and is

approximately obeys . On the other hand,

is and has a peak at .

The increase in accompanies the increase in , however

the change of is not so large and it decreases slightly

(See Figure 1).

The first peak position of , which is governed by

, moves towards to as increases.

The first peak

becomes narrower and higher with the left slide and only

grows monotonically. For ,

is upward convex with respect to .

for damps with

monotonically.

On the other hand, the second peak position,

which is governed by , shifts towards to .

The area of the

second peak, which is calculated as in eq.(43), approaches

and the width becomes narrow.

increases monotonically to with and

near is upward convex.

We would like to discuss the above effect on the tranche

of securities synthesized from the homogeneous assets pool with

parameters .

For the purpose, it is useful to

introduce the cumulative distribution function , which is

defined as

(48)

From the definition and

is the probability of the occurrence

of default.

We explain the

relation between

and the evaluation of the tranche briefly.

The tranche for the interval implies that if the number of

default is below ,

the tranche does not suffer from any

damage. However, if exceeds or becomes equal to , it begins to lose its value.

The value of the tranche is in

units of the number of assets (we assume that the

values of all assets in the pool are equal.)

and if defaults with

occurs, it loses units. When exceeds , the tranche lose its value completely.

The expected loss rate of the tranche is calculated as

(49)

The first terms comes from the partial damage in the tranche

and the second term implies the contribution from

its complete loss of the tranche .

are directly related with the price of the tranche (premium),

which can be observed in the market.

For , we denote as and call it as the expected loss

rate at the -th tranche.

It is related with the cumulative distribution as

(50)

is useful, because we can reconstruct as a

sum of as

(51)

The proof of the relation is straightforward.

(52)

We note that, if we set and in equation (51), we obtain

(53)

Here we use the relation , which is

intuitively clear and can be proved as in the equation (52).

From the second equality in eq.(53)

that the average of the expected loss rate at each tranche is ,

tranches look like to “share between them”

or “toss to other tranches”.

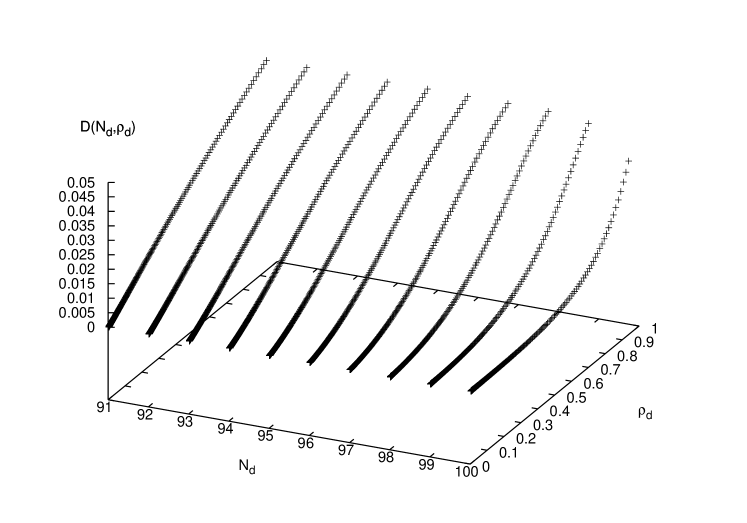

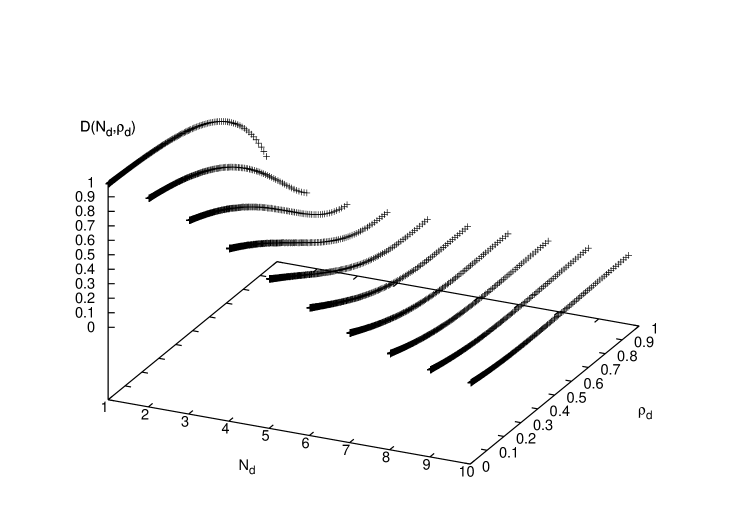

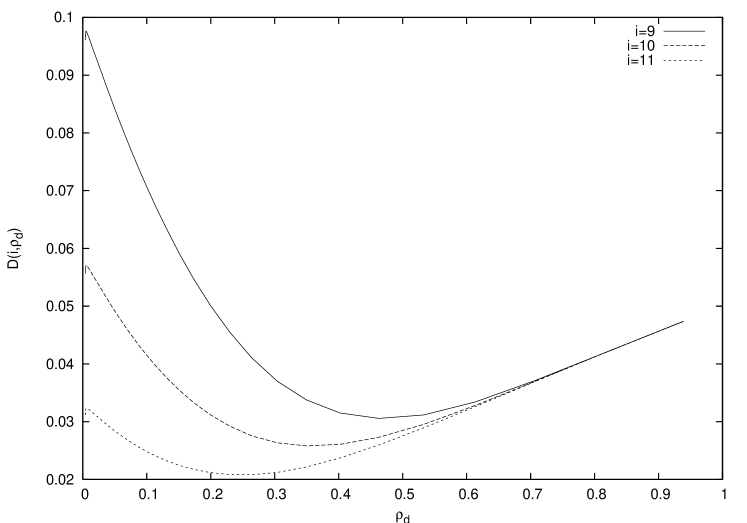

Figure 7: Plot of vs . .Figure 8: Plot of vs . and .

Now we discuss the effect of the default correlation on

. From the definition

,

we can understand the

dependence easily from the previous discussions on

. In figure 7, we show

for .

The area of the second peak

increases monotonically to as we increase ,

the cumulative distributions also grow up to .

is almost zero for ,

for

behaves in the same way with these for .

If becomes

small, we see the contribution from the first peak in

. For small , the damps of

for

with respect to dominates the contribution from the second

peak. increases monotonically and

decreases with .

for also decreases as in

figure 8, which shows for .

These behaviors reflect the left shift and the width tinning

of the first peak. For the intermediate value of ,

the dependence of

is not monotonous. In figure 9, we

depict for .

Along with the shape change of the first peak

with ,

at first decrease. Then, the contribution from the second peak dominates

the decrease of the first peak contribution and

begins to increase.

is downward convex

with respect to for the interval of .

We note that the

ranges where is downward convex,

decreases monotonically,

or increases monotonically depends on the

parameters . The above discussions

may not hold for other values of and .

In particular the range of the downward convex region,

if we set , we observe that it shift to the left.

The positions of the boundaries between the

regions are important from the

viewpoints of risk management and rating of the securities,

we should note this point.

Figure 9: Plot of vs . .

Solid line , broken line and dotted line .

From these observations, we summarize the dependence of .

•

Senior tranche, the range

with are set to be large,

suffers from the default

correlation seriously. for the range increase linearly

with . It is approximately given by

(54)

If change from to , change from to

and the evaluations of the securities decrease almost linearly.

•

Equity or subordinate tranche, the range

is and is small. In the range

, damps monotonically with

and also damps. The increase in causes the increase

of the evaluation of the tranche.

•

Mezzanine tranche, whose range is between the equity and the senior

tranche.

In the range, the behaviors of depends on and

the system size . In the above mentioned case,

has downward convex shape for some intermediate values

of .

5 Concluding Remarks and Future Problems

In this paper, we have studied the long-range Ising model as

a model for a pool of homogeneous assets with default probability

and default correlation . We have studied in the

plane, the behavior of and . There are two phases in

the plane. In the One Peak Phase, the probabilities

have a single peak at . The correlation

is almost zero in the phase. In the Two Peak Phase, there are two peaks

in and can take large value. The first peak

is closer to origin than and its area is larger than

. The second peak is at about and its area is less than .

The parameters

should be chosen in the Two peak phase, if the model intends to describe

the portfolio with some default correlation between the

assets. We have developed the perturbative

method and expressed as a superposition of

two binomial distributions with the above two peaks at zero-th order.

We have obtained the closed form expression for and the

weights for the second peak , which means the probability

that almost all assets are defaulted. These expressions are in good

agreement with numerically calculated values and give an efficient method

for the actual application of the long-range Ising model. Otherwise,

for and , it is difficult to know the parameters

and and the long range

Ising model is hard-to-use as a model for homogeneous credit risk

portfolio.

Furthermore, we have studied the dependence of

and

the cumulative distribution . is binomial

distribution and it has a peak at .

As we increase from

0 to 1, the profile of changes from One peak shape

to Two Peak shape. The first peak

shifts to the left and its shape

becomes higher and narrower. The second peak’s area increases and it

shifts to the right with the decrease of its width.

At ,

has two thin peaks at and and the probabilities

are and . Other probabilities

are zero. The cumulative distribution functions

correspond to the average loss rates of the -th tranche.

About the senior tranche, the range of the tranche

is large.

As increases,

increase almost linearly with

like .

The average loss rate of the senior tranche is given as a sum of

in the range , the expectation

value of the loss rate of the senior tranche also increases as

. The price of the tranche is based on the

average loss rate, the value of the senior tranche

decreases with .

The range of the equity, the subordinated

tranche, is near the origin and the s decrease

monotonically.

The average loss rate of the equity decreases with and

the price of the equity increase with .

The mezzanine tranche is between the equity and the senior tranche.

The profile of in the range depends on the model parameters

and . In the text example, has a

downward convex shape in some region. If the mezzanine range

is chosen to lie in the region, the average loss rate also behaves similarly.

However, other probabilistic model for a pool of assets, e.g. the copula

model [14],

suggest

upward convex shape for the average loss of the mezzanine tranche.

The discrepancy comes from the difference of the shapes of

. The more complete comparison between the

probabilistic models for a pool of correlated assets should be

done.

As concluding remarks, we comment on the usage of the long-range Ising

model and related future problems. As a statistical

model for an ensemble of many assets, the long-range Ising model is

an attractive one from the viewpoint of physicists. Its phase diagram

and phase transitions are throughly studied and its analytic calculation

method, like Hubbard-Stratanovich transformation, guides us how to

make theoretically tractable models. On the other hand, from the

viewpoint of financial engineers, the long-range Ising model is not

so convenient. One reason is that the model parameters are not

directly related with the observed data and (or

). Other statistical models incorporate these parameters

as a model parameters. For example, the Moody’s correlated binomial

model gives as a function of and

explicitly.

When one uses Ising model, it is necessary

to know the parameters which correspond to .

The definition of and

include the moments or

and , it is necessary to take the trace .

The long-range

Ising model has the advantage that the trace is reduced to the summation

over the total magnetization and the calculation

is not so heavy task. Even so, this one step spoils the usefulness of

the model. We have obtained a closed form expressions for and

and try to circumvent the step. The computational time

to obtain for given is reduced much and

the failing of the model are partially overcome.

In order to apply the long-range Ising model to

the evaluation of the tranche in more realistic situation,

the assumption of homogeneity of the assets pool

should be weakened. One step toward the direction is to introduce

multi sectors and assume the homogeneity only in each sector.

We label each sector by and -th sector contains

assets. In the -th sector, the default rate is

and the default correlation is .

Between different sectors, say between -th and -th sector,

the default correlation is .

We use Ising Spin variables to represent the states

of the -th asset in the -th sector, the generalized long-range

Ising model Hamiltonian for the probabilities is

(55)

As in the homogeneous model, the Hamiltonian depends on

only through the magnetization of the -th sector . When we set

and , the model reduces to the homogeneous model with

. The problem is to get the relation between

and .

In order to accomplish the task, the phase diagram in

and the profile

should be cleared and it is left for future analysis.

Furthermore, for more complex situation where -th asset has

default probability and the default correlation between

-th and -th asset is , the model Hamiltonian

becomes that of the random Ising spin systems. The exchange interaction

and the external field should be connected to

and , which is also left for future problem.

Other step is to discard the Ising model and adopt other

probabilistic models. One possibility is the Moody’s

correlated binomial model, which uses two state variables

for the state of an asset

and incorporates

and directly in the model parameters. Its

generalization to the multi-sector case and more complex situations

is an interesting problem.

Other possibility is to introduce simplified version of

the long-range Ising model.

We use two state variable for the state of the -th asset.

The number of defaults is expressed as .

The probabilities is given as

(56)

Instead of the superposition of two binomial distributions,

we use for the second peak. The first peak

is and the parameters are related with the default

probability as .

This probabilities

is more tractable than the original probability distribution (3)

and the

generalizations to more complex situations may be carried out easily.

This work has received financial support from Kitasato University,

project SCI:2005-1706.

References

References

[1] Fabozzi F J and Goodman L S 2001 Investing in

Collateralized Debt Obligations (U.S. John Wiley & Sons).

[2] Schonbucher P J 2003 Credit Derivatives

Pricing Models : Model, Pricing and Implementation (U.S. John Wiley & Sons)

.

[3] Bouchaud J-P and Potters M 2000 Theory

of Financial Risks(Cambridge University Press).

[4] Mantegna R N and Stanley H E 2000 An Introduction to

Econophysics (Cambridge University Press).

[5] Aleksiejuk A and Holyst A 2001 Physica A299 198.

[6] Iori G 2001 Physica A299 205.

[7] Calamaro J P, Nassar T and Thakkar K 2004 Correlation: Trading Implications for Synthetic CDO Tranches

(Deutsche Bank: Global Market Research, 27 September).

[8] Merton R 1974 The Journal of Finance29 449.

[9] Cifuettes A and O’Connor G 1996

The Binomial Expansion Method Applied

to CBO/CLO Analysis

(Moody’s Investors Service).

[10] Witt G 2004 Moody’s Correlated Binomial Default

Distribution

(Moody’s Investors Service)August 10.

[11] Molins J and Vives E 2004 Long range Ising Model for

credit risk modeling in homogeneous portfolios

Preprint

cond-mat/0401378.

[12] Martin R, Thompson K and Browne C 2001

RiskJuly 86.

[13] Finger C C 2000 A Comparison of stochastic default

rate models: Working Paper (The RiskMetrics Group).

[14] Li D X 2000 The Journal of Fixed Income9(4)43.

[15] Duffie D and Gârleau 2001

Financial Analyst Journal57(1)41-59.

[16] Duffie D and Singleton K J 2003

Credit Risk-Pricing, Measurement and Management (Princeton:Princeton

University Press).

[17] Stanley H E 1983 Introduction to Phase Transitions and

Critical Phenomena, vol 8 of International Series of Monographs on

Physics (New York : Oxford University Press) .