The Growth of Business Firms:

Theoretical Framework and Empirical Evidence

Dongfeng Fu∗, Fabio Pammolli∗‡§,

S. V. Buldyrev¶, Massimo Riccaboni‡§, Kaushik Matia∗, Kazuko Yamasaki∥, H. E. Stanley∗∗Center for Polymer Studies and Department of Physics,

Boston University, Boston, MA 02215 USA

‡Faculty of Economics,

University of Florence, Milan, Italy

§IMT Institute for Advanced

Studies, Via S. Micheletto 3, Lucca, 55100 Italy

¶Department of

Physics, Yeshiva University, 500 West 185th Street, New York, NY 10033 USA

∥Tokyo University of Information Sciences, Chiba City 265-8501

Japan

Abstract

We introduce a model of proportional growth to explain the distribution

of business firm growth rates. The model predicts that is

exponential in the central part and depicts an asymptotic power-law behavior

in the tails with an exponent . Because of data limitations,

previous studies in this field have been focusing exclusively on the Laplace

shape of the body of the distribution. In this article, we test the model at

different levels of aggregation in the economy, from products to firms to

countries, and we find that the model’s predictions agree with empirical

growth distributions and size-variance relationships.

I Introduction

Gibrat Gibrat30 ; Gibrat31 , building upon the work of the astronomers

Kapteyn Kapteyn16 , assumed the expected value of the growth rate of a

business firm’s size to be proportional to the current size of the firm,

which is called “Law of Proportionate Effect” Zipf49 ; Gabaix99 . Several

models of proportional growth have been subsequently introduced in economics

in order to explain the growth of business firms Steindl65 ; Sutton97 ; Kalecki45 . Simon and co-authors Simon55 ; Simon58 ; Simon75 ; Simon77

extended Gibrat’s model by introducing an entry process according to which

the number of firms rise over time. In Simon’s framework, the market consists of a

sequence of many independent “opportunities” which arise over time, each of

size unity. Models in this tradition have been challenged by many

researchers Stanley96 ; Lee98 ; Stanley99 ; Bottazzi01 ; Matia04 who found

that the firm growth distribution is not Gaussian but displays a tent shape.

Here we introduce a general framework that provides an unifying explanation

for the growth of business firms based on the number and size distribution of

their elementary constituent

components Amaral97 ; Sergey_II ; Sutton02 ; DeFabritiis03 ; Amaral98 ; Takayasu98 ; Canning98 ; Buldyrev03 . Specifically we present a model of proportional growth in both

the number of units and their size and we draw some general implications on

the mechanisms which sustain business firm growth Simon75 ; Sutton97 ; Kalecki ; Mansfield ; Hall ; DeFabritiis03 . According to the model, the

probability density function (PDF) of growth rates is Laplace in the

center Stanley96 with power law tails Reed01 ; Reed02 decaying as

where .

Because of data limitations, previous studies in this field focus on the

Laplace shape of the body of the distribution Kotz01 . Using a database

on the size and growth of firms and products, we characterize the shape of

the whole growth rate distribution.

We test our model by analyzing different levels of aggregation of economic

systems, from the “micro” level of products to the “macro” level of

industrial sectors and national economies. We find that the model accurately

predicts the shape of the PDF of growth rate at all levels of aggregation

studied.

II The Theoretical Framework

We model business firms as classes consisting of a random number of units.

According to this view, a firm is represented as the aggregation of its

constituent units such as divisions Amaral98 ,

businesses Sutton02 , or products DeFabritiis03 . Accordingly, on

a different level of coarse-graining, a class can represent a national

economy composed by economic units such as firms. In this article we study the

logarithm of the one-year growth rate of classes

where and are the sizes of classes in the year and

measured in monetary values (GDP for countries, sales for firms and

products). Our model is illustrated in Fig. 1. Two key sets of

assumptions in the model are (A) the number of units in a class grows in

proportion to the existing number of units and (B) the size of each unit

fluctuates in proportion to its size.

The first set of assumptions is:

(A1)

Each class consists of number of

units. At time , time step measured by year generally, there are

classes consisting of total number of units. The initial

average number of units in a class is thus .

(A2)

At each time step a new unit is created. Thus the number

of units at time is .

(A3)

With birth probability , this new unit is assigned to a new

class, so that the average number of classes at time is .

(A4)

With probability , a new unit is assigned to an existing

class with probability , so

.

For simplicity, we do not consider the decrease of the number of units in a

class. In reality, elementary units enter and exit. Because we are considering

the case of a growing economy, it is legitimate to assume the entry rate

being higher than the exit rate. On the average, the net entry rate of units

can be simplified as a positive constant. In the model, the net entry rate of

units is fixed at . Thus, at large , it gives results equivalent to the ones

that would have been obtained considering a value for the exit rate of units.

Our goal is to find , the probability distribution of the number of

units in the classes at large . This model in two limiting cases (i)

, and (ii) ,

, has exact analytical solutions

Johnson ; Kotz2000 and

Reed04 respectively.

In the general case, the exact analytical solution is not known and we obtain

a numerical solution by computer simulations and compare it with the

approximate mean field solution. (see, e.g., Chapter 6 of book and

Appendix A)

Our results are consistent with the exactly solvable limiting cases as well

as with the empirical data on the number of products in the pharmaceutical

firms and can summarized as follows. In the limit of large , the

distribution of in the old classes that existed at converges to an

exponential distribution Cox

(1)

where and is the average number of units in the old

classes at time , . The

distribution of units in the new classes created at converges to a

power law with an exponential cutoff

(2)

where for small , and decays for

faster than . The distribution of units in all classes

is given by

(3)

The mean field approximation for is given by

(4)

where .

The second set of assumptions is:

(B1)

At time , each class has units of

size , where and are independent random variables taken from the distributions

and respectively. is defined

by Eq. (3) and is a given distribution

with finite mean and standard deviation and has finite mean

and variance

. The size of a class is

defined as .

(B2)

At time , the size of each unit is decreased or

increased by a random factor so that

(5)

where , the growth rate of unit , is independent random

variable taken from a distribution , which has a finite mean.

We also assume that has finite mean

and variance

.

The growth rate of each class is defined as

(6)

Here we neglect the influx of the new units, so

. The resulting distribution of the

growth rates of all classes is determined by

(7)

where is the distribution of the number of units in the classes,

computed in the previous stage of the model and is the conditional

distribution of growth rates of classes with given number of units determined

by the distribution and .

The analytical solution of this model can be obtained only for certain

limiting cases but a numerical solution can be easily computed for any set of

assumptions. We investigate the model numerically and analytically (see

Appendix B) and find:

(1)

The conditional distribution of the logarithmic growth

rates for the firms consisting of a fixed number of units

converges to a Gaussian distribution for :

(8)

where is a function of parameters of the distribution

and , and is mean logarithmic growth rate of a unit,

.

Thus the width of this distribution decreases as . This result is

consistent with the observation that large firms with many production units

fluctuate less than small firms Sutton97 ; Amaral97 ; Amaral98 ; Hymer .

(2)

For , the distribution

coincides with the distribution of the logarithms of the growth

rates of the units:

(9)

In the case of power law distribution which dramatically

increases for , the distribution is dominated by the growth

rates of classes consisting of a single unit , thus the distribution

practically coincides with for all . Indeed,

our empirical observations confirm this result.

(3)

If the distribution , for

, as happens in the presence of the influx of new units , , for which in the limiting case

, gives the cusp ( and

are positive constants), similar to the behavior of the Laplace

distribution for .

(4)

If the distribution weakly depends on for ,

the distribution of can be approximated by a power law of :

in wide range , where

is the average number of units in a class. This case is realized for

, when the distribution of is dominated by the

exponential distribution and as defined by

Eq. (1). In this particular case, for can be approximated by

(10)

(5)

In the case in which the distribution is not dominated by

one-unit classes but for behaves as a power law, which is the

result of the mean field solution for our model when , the

resulting distribution has three regimes, for small , for intermediate ,

and for . The approximate solution of

is obtained by using Eq. (8) for for finite

, mean field solution Eq. (4) in the limit

for and replacing summation by integration in Eq. (7):

(11)

For the integral above can be expressed in elementary

functions. In the case, Eq. (11) yields the main

result

(12)

which combines the Laplace cusp for and the power law decay

for . Note that due to replacement of summation by

integration in Eq. (7), the approximation Eq. (12)

holds only for .

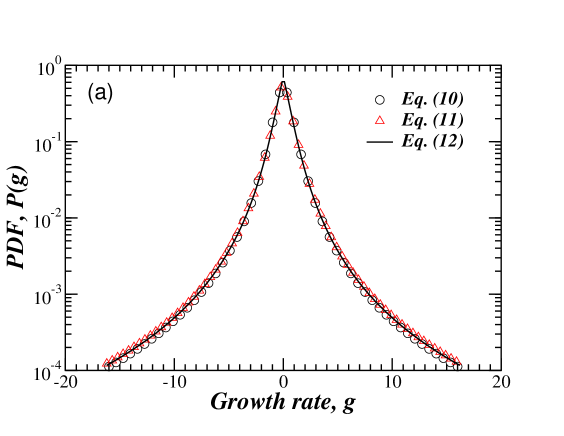

In Fig. 2a we compare the distributions given by

Eq. (10), the mean field approximation

Eq. (11) for and Eq. (12) for

. We find that all three distributions have very similar tent shape

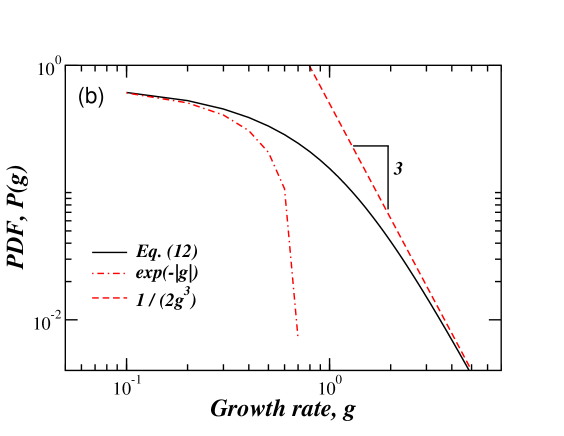

behavior in the central part. In Fig. 2b we also compare the

distribution Eq. (12) with its asymptotic behaviors for

(Laplace cusp) and (power law), and find the

crossover region between these two regimes.

III The Empirical Evidence

To test our model, we analyze different levels of aggregation of economic

systems, from the micro level of products to the macro level of industrial

sectors and national economies.

First, we analyze a new and unique database, the pharmaceutical industry

database (PHID), which records sales figures of the 189,303 products

commercialized by 7,184 pharmaceutical firms in 21 countries from 1994 to

2004, covering the whole size distribution for products and firms and

monitoring the flows of entry and exit at both levels kindly provided by the

EPRIS program. Then, we study the growth rates of all U.S. publicly-traded

firms from 1973 to 2004 in all industries, based on Security Exchange

Commission filings (Compustat). Finally, at the macro level, we study the

growth rates of the gross domestic product (GDP) of 195 countries from 1960

to 2004 (World Bank).

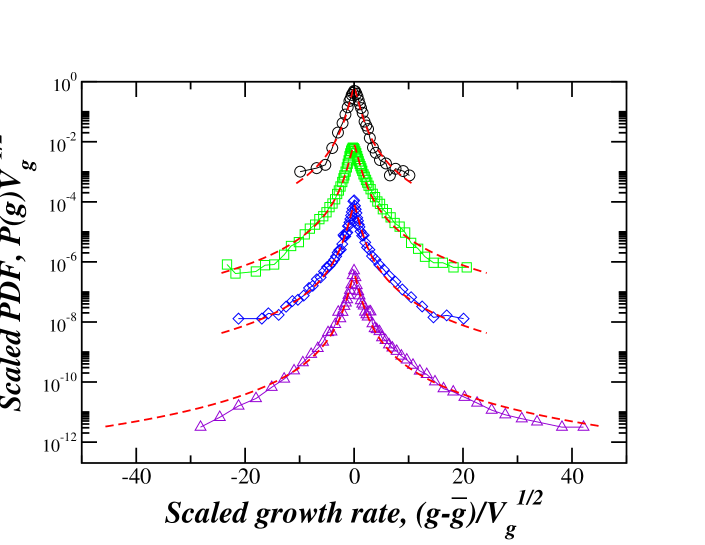

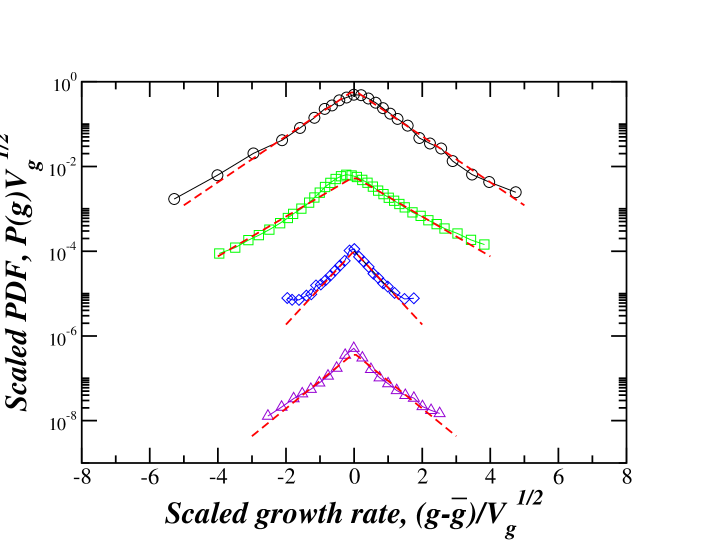

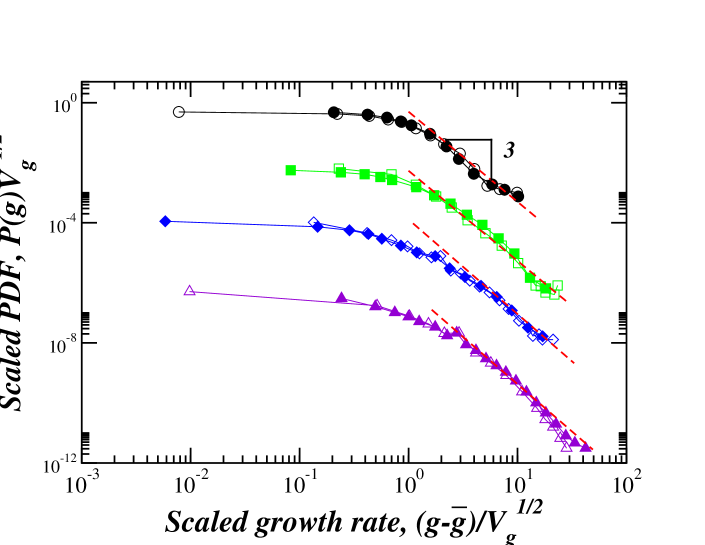

Fig. 3 shows that the growth distributions of countries,

firms, and products are well fitted by the distribution in

Eq. (12) with different values of . Indeed, growth

distributions at any level of aggregation depict marked departures from a

Gaussian shape. Moreover, even if the of GDP can be approximated by a

Laplace distribution, the of firms and products are clearly more

leptokurtic than Laplace. Based on our model, the growth distribution is

Laplace in the body, with power-law tails. In fact, Fig. 4 show that

the central body part of the growth rate distributions at any level of

aggregation is well approximated by a double exponential

fit. Fig. 5 reveals that the asymptotic behaviors of at any

level of aggregation can be well fitted by power-law with an exponent

.

Our analysis in Sec. II predicts that the power law regime of may

vary depending on the behavior of for , and the distribution

of the growth rates of units. In case of PHID, for which the growth rate distribution of firms must be almost the same as

the growth rate distribution of products, as we stated in Sec. II. Hence the

power law wings of for firms originate on the level of

products. Because PHID does not contain information on the subunits of products

we can not test our prediction directly, but we can hypothesize that the

distribution of the product subunits (number of customers or shipping ways)

is less dominated by small , but has a sufficiently wide power law regime

due to the influx of new products. These rather plausible assumptions are

sufficient to explain the shape of the distribution of the product growth

rates, which is well described by Eq. (12).

The PHID database allows us to test the empirical conditional distribution

and the dependence of its variance on , where

is the number of products. We find that , which is

significantly smaller than behavior. This result does not imply

correlations among product growth rates on the firm

level DeFabritiis03 , but can be explained by the fact that for skewed

distributions of product sizes characterized by large

, the convergence of to its Gaussian limit

Eq. (8) is slow and the growth rates of the firms are determined

by the growth of the few large products. Using the empirical values for the

PHID , , ,

and assuming lognormality of the distributions and

we find that the behavior of can be well

approximated by a power law for . For this

set of parameters, the convergence of to a Gaussian distribution

takes place only for . This result is consistent with the

observations of the power law relationship between firm size and growth rate

variance reported earlier Stanley96 ; Amaral97 ; Sergey_II ; Matia05 .

IV Discussion

Business firms grow by increasing their scale and scope. The scope of a firm

is given by the number of its products. The scale of a firm is given by the

size of its products. A firm like Microsoft gets few big products while Amazon

sells a huge variety of goods, each of small size in terms of sales. In this

article we argue that both mechanisms of growth are proportional. The number of

products a firm can successfully launch is proportional to the number of

products it has already commercialized. Once a product has been launched its

success depends on the number of customers who buy it and the price they are

willing to pay. To a large extent, if products are different enough, the

success of a product is independent from other products commercialized by the

same company. Hence, the sales of products can be modeled as independent

stochastic processes. Moreover, sometimes, new products are commercialized by

new companies. As a result, small companies with few products can experience

sudden jerks of growth due to the successful launch of a new product.

In this article, we find that the empirical distribution of firm growth rates

exhibits a central part which is distributed according to a Laplace

distribution and power-law wings where

. If the distribution of number of units is dominated by single

unit classes, the tails of firm growth rate are primarily due to smaller

firms composed of one or few products. The Laplace center of the distribution

is shaped by big multiproduct firms. We find that the shape of the

distribution of firm growth is almost the same in presence of a small entry

rate and with zero entry. We also find that the model’s predictions are

accurate also in the case of product growth rates, which implies that

products can be considered as composed by elementary sale units, which evolve

according to a random multiplicative process Steindl65 . Although there

are several plausible explanations for the Laplace body of the distribution

Amaral97 ; Kotz01 , the power law decay of the tails has not previously

been observed. We introduce a simple and general model that accounts for both

the central part and the tails of the distribution. The shape of the business

growth rate distribution is due to the proportional growth of both the number

and the size of the constituent units in the class. This result holds in the

case of an open economy (with entry of new firms) as well as in the

case of a closed economy (with no entry of new firms).

Acknowledgment

We thank S. Havlin, J. Nagler and F. Wang for helpful discussions and

suggestions. We thank NSF and Merck Foundation (EPRIS Program) for financial

support.

References

(1) Gibrat, R. (1930) Bulletin de Statistique

Général, France, 19, 469.

(2) Gibrat, R. (1931) Les Inégalités

Économiques (Librairie du Recueil Sirey, Paris).

(3) Kapteyn, J. & Uven M. J. (1916) Skew Frequency

Curves in Biology and Statistics (Hoitsema Brothers, Groningen).

(4) Zipf, G. (1949) Human Behavior and the Principle of

Least Effort (Addison-Wesley, Cambridge, MA).

(5) Gabaix, X. (1999) Quar. J. Econ.114,

739–767.

(6) Steindl, J. (1965) Random Processes and the Growth of

Firms: A study of the Pareto law (London, Griffin).

(7) Sutton, J. (1997) J. Econ. Lit.35, 40-59.

(8) Kalecki, M. (1945) Econometrica13,

161-170.

(9) Simon, H. A. (1955) Biometrika, 42, 425-440.

(10) Simon, H. A. & Bonini, C. P. (1958) Am. Econ. Rev.48, 607-617.

(11) Ijiri, Y. & Simon, H. A. (1975) Proc. Nat. Acad. Sci.72, 1654-1657.

(12) Ijiri, Y. & Simon, H. A., (1977) Skew distributions

and the sizes of business firms (North-Holland Pub. Co., Amsterdam).

(13) Stanley, M. H. R., Amaral, L. A. N., Buldyrev, S. V.,

Havlin, S., Leschhorn, H., Maass, P., Salinger, M. A. &

Stanley, H. E. (1996) Nature379, 804-806.

(14) Lee, Y., Amaral, L. A. N., Canning, D., Meyer, M. &

Stanley, H. E. (1998) Phys. Rev. Lett.81, 3275-3278.

(15) Plerou, V., Amaral, L. A. N., Gopikrishnan, P.,

Meyer, M. & Stanley, H. E. (1999) Nature433, 433-437.

(16) Bottazzi, G., Dosi, G., Lippi, M., Pammolli, F. &

Riccaboni, M. (2001) Int. J. Ind. Org.19, 1161-1187.

(17) Matia, K., Fu, D., Buldyrev, S. V., Pammolli, F.,

Riccaboni, M. & Stanley, H. E. (2004) Europhys. Lett.67,

498-503.

(18) Amaral, L. A. N., Buldyrev, S. V., Havlin, S.,

Leschhorn, H, Maass, P., Salinger, M. A., Stanley, H. E. &

Stanley, M. H. R. (1997) J. Phys. I France7, 621–633.

(19) Buldyrev, S. V., Amaral, L. A. N., Havlin, S.,

Leschhorn, H, Maass, P., Salinger, M. A. , Stanley, H. E. &

Stanley, M. H. R. (1997) J. Phys. I France7, 635-650.

(20) Sutton, J. (2002) Physica A312, 577–590.

(21) Fabritiis, G. D., Pammolli, F. &

Riccaboni, M. (2003) Physica A324, 38–44.

(22) Amaral, L. A. N., Buldyrev, S. V., Havlin, S.,

Salinger, M. A. & Stanley, H. E. (1998) Phys. Rev. Lett80,

1385-1388.

(23) Takayasu, H. & Okuyama, K. (1998) Fractals6, 67–79.

(24) Canning, D., Amaral, L. A. N., Lee, Y., Meyer, M. &

Stanley, H. E. (1998) Econ. Lett.60, 335-341.

(25) Buldyrev, S. V., Dokholyan, N. V., Erramilli, S.,

Hong, M., Kim, J. Y., Malescio, G. & Stanley, H. E. (2003) Physica A330, 653-659.

(26)

Kalecki, M. R. Econometrica (1945) 13, 161-170.

(27)Mansfield, D. E. (1962) Am. Econ. Rev.52,

1024-1051.

(28)Hall, B. H. (1987) J. Ind. Econ.35, 583-606.

(29) Reed, W. J. (2001) Econ. Lett.74, 15-19.

(30) Reed, W. J. & Hughes, B. D. (2002) Phys. Rev. E66, 067103.

(31) Kotz, S., Kozubowski, T. J. & Podgórski, K. (2001) The Laplace Distribution and Generalizations: A Revisit with Applications to

Communications, Economics, Engineering, and Finance (Birkhauser, Boston).

(32) Johnson, N. L. & Kotz, S. (1977) Urn Models and Their

Applications (Wiley, New York).

(33) Kotz, S., Mahmoud, H. &

Robert, P. (2000) Statist. Probab. Lett.49, 163-173.

(34) Reed, W. J. & Hughes, B. D. (2004) Math. Biosci.189, No. 1, 97-102.

(35) Stanley, H. E. (1971) Introduction to Phase Transitions and

Critical Phenomena (Oxford University Press, Oxford).

(36) Cox, D. R. & Miller, H. D. (1968) The Theory of

Stochastic Processes (Chapman and Hall, London).

(37) Hymer, S. & Pashigian, P. (1962) J. Polit. Econ.70, 556-569.

(38) Matia, K., Amaral, L. A. N., Luwel, M., Moed, H. F. &

Stanley, H. E. (2005) J. Am. Soc. Inf. Sci. Technol. 56, 893-902.

Appendix A: The distribution of units in old and

new classes

Assume that at the beginning there are classes with

units. Because at every time step one unit is added to the system and a new

class is added with probability , at moment there are

units and classes, among which there are new classes with

units and old classes with units, such that

.

Because of the preferential attachment assumption, we have

(A1)

(A2)

Solving the second differential equation and taking into account initial

condition , we obtain

(A3)

Analogously, the number of units at time in the classes existing at time

is

where the subscript ‘e’ means “existing”. The average number of units in

old classes is

(A4)

It is known that Cox for the preferential attachment

model converges to the exponential distribution:

(A5)

Thus, we obtain

(A6)

and the part of of old classes is

(A7)

The number of units in the classes that appear at is and the

number of these classes is . Because the probability that a class

captures a new unit is proportional to the number of units it has already

gotten at time , the number of units in the classes that appear at time

is

The average number of units in these classes is

. Assuming

that the distribution of units in these classes is given by a continuous

approximation in Eq. (A5):

(A8)

Thus, their contribution to the total distribution is

The contribution of all new classes to the distribution is

(A9)

If we let , then

(A10)

Note that Eq. (A7) and Eq. (A10) are not exact

solutions but continuous approximations which assume is a real

number. Now we investigate the distribution in Eq. (A10).

1. At fixed when , the low limit of integration in

Eq. (A10) goes to zero and we have

(A11)

As ,

(A12)

As ,

(A13)

2. At fixed when , we use the partial integration to

evaluate the incomplete function:

Appendix B: Calculation of the growth distribution

of classes

Let us assume both the size and growth of units ( and

respectively) are distributed lognormally

(A15)

(A16)

If units grow according to a multiplicative process, the size of units is distributed lognormally with and .

The moment of the variable

distributed lognormally is given by

(A17)

Thus, its mean is and its variance is

.

Let us now find the distribution of growth rate of classes. It is defined

as

(A18)

Here we neglect the influx of new units. According to the central limit

theorem, the sum of independent random variables with mean

and finite variance is

(A19)

where is the random variable with the distribution converging to

Gaussian

(A20)

Because and we have

(A21)

For large the last term in Eq. (A21) is the difference of two

Gaussian variables and that is a Gaussian variable itself.

(A22)

where is the average growth rate. To find the distribution

of we must find its mean and variance. In order to do this, we rewrite

and

Thus

(A23)

Because , the average of each term

in the sum is . The variance of each

term in the sum is where

, and are all lognormal independent

random variables. Particularly, is lognormal with and ; is lognormal with and ; is lognormal with and . Using Eq. (A17) and

Eq. (A23)

(A24a)

(A24b)

(A24c)

Collecting all terms in Eqs. (A24a-A24c) together and

using Eq. (A23) we can find the variance of :

(A25)

Therefore, for large , has a Gaussian distribution

(A26)

where ,

and .

The distribution of the growth rate of the old classes can be found by

Eq. (7) in the text. In order to find a close form approximation,

we replace the summation in Eq. (7) by integration and replace

the distributions by Eq. (A6) and by the

Eq. (A26) assuming :

(A27)

where is the average number of units in the old classes (see

Eq. (A4)). This distribution decays as and thus does

not have finite variance. In fact, we approximate the distribution of number

of units in the old classes by a continuous function ,

while in reality it is a discrete distribution

(A28)

where . The corrected distribution of growth rates is

then given by the sum

(A29)

The slowest decaying term is

(A30)

which describes the behavior of the distribution when .

Thus there is a crossover from Eq. (A27) to Eq. (A30) when

.

For the new classes, when the distribution of number of units

is approximated by

(A31)

Again replacing summation in Eq. (7) in the text by integration

and by Eq. (A26) and after the switching the order

of integration we have:

(A32)

As , we can evaluate the second integral in Eq. (A32) by

partial integration:

(A33)

We compute the first derivative of the distribution (A32) by

differentiating the integrand in the second integral with respect to .

The second integral converges as , and we find the behavior of the

derivative for by the substitution . As , the derivative behaves as , which means that the function itself behaves as , where and are positive constants. For

small this behavior is similar to the behavior of a Laplace distribution

with variance :

.

which behaves for as and for as

. Thus the distribution is well approximated by a Laplace

distribution in the body with power-law tails.

Because of the discrete nature of the distribution of the number of units,

when the behavior for is dominated by

.

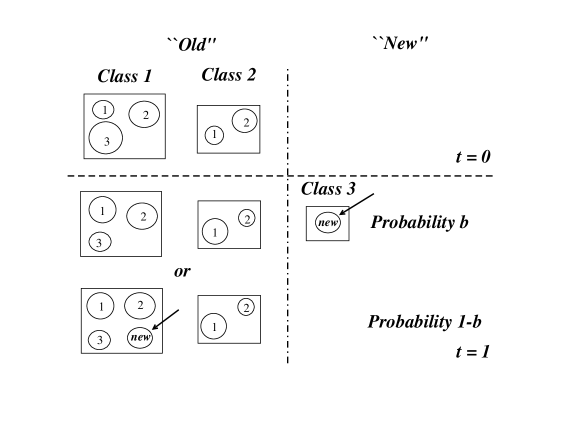

Figure 1: Schematic representation of the model of proportional growth. At

time , there are classes () and units

() (Assumption A1). The area of each circle is proportional to the

size of the unit, and the size of each class is the sum of the areas of

its constituent units (see Assumption B1). At the next time step, , a new unit is

created (Assumption A2). With probability the new unit is assigned to a

new class (class 3 in this example) (Assumption A3). With probability

the new unit is assigned to an existing class with probability proportional

to the number of units in the class (Assumption A4). In this example, a new

unit is assigned to class with probability or to class with

probability . Finally, at each time step, each circle grows or

shrinks by a random factor (Assumption B2).

Figure 2: (a) Comparison of three different approximations for the growth

rate PDF, , given by Eq. (10), mean field

approximation Eq. (11) for and

Eq. (12). Each shows similar tent shape behavior

in the central part. We see there is little difference between the three

cases, (no entry), (with entry) and the mean field

approximation. This means that entry of new classes () does not

perceptibly change the shape of . Note that we use

for Eq. (10) and for

Eq. (12). (b) The crossover of given by

Eq. (12) between the Laplace distribution in the center

and power law in the tails. For small , follows a Laplace

distribution , and for large ,

asymptotically follows an inverse cubic power law .Figure 3: Empirical tests of Eq. (12) for the probability

density function (PDF) of growth rates rescaled by

. Shown are country GDP (), pharmaceutical firms

(), manufacturing firms (), and pharmaceutical products

(). The shapes of for all four levels of aggregation

are well approximated by the PDF predicted by the model (dashed

lines). Dashed lines are obtained based on Eq. (12) with

for GDP, for pharmaceutical

firms, for manufacturing firms, and for

products. After rescaling, the four PDFs can be fit by the same function. For

clarity, the pharmaceutical firms are offset by a factor of ,

manufacturing firms by a factor of and the pharmaceutical products by

a factor of . Note that the data for pharmaceutical products extend

from to and the mismatch in the tail parts

is because for large is mainly determined by the logarithmic

growth rates of units .Figure 4: Empirical tests of Eq. (12) for the central part in the PDF of growth rates rescaled by

. Shown are 4 symbols: country GDP (),

pharmaceutical firms (), manufacturing firms (), and

pharmaceutical products (). The shape of central parts for

all four levels of aggregation can be well fit by a Laplace distribution

(dashed lines). Note that Laplace distribution can fit only over a

restricted range, from to . Figure 5: Empirical tests of Eq. (12) for the tail

parts of the PDF of growth rates rescaled by . The asymptotic

behavior of at any level of aggregation can be well approximated by power

laws with exponents (dashed lines). The symbols are

as follows: Country GDP (left tail: , right tail: ),

pharmaceutical firms (left tail: , right tail: ),

manufacturing firms (left tail: , right tail: ),

pharmaceutical products (left tail: , right tail:

).