Bidding process in online auctions and winning strategy: rate equation approach

Abstract

Online auctions have expanded rapidly over the last decade and have become a fascinating new type of business or commercial transaction in this digital era. Here we introduce a master equation for the bidding process that takes place in online auctions. We find that the number of distinct bidders who bid times, called the -frequent bidder, up to the -th bidding progresses as . The successfully transmitted bidding rate by the -frequent bidder is obtained as , independent of for large . This theoretical prediction is in agreement with empirical data. These results imply that bidding at the last moment is a rational and effective strategy to win in an eBay auction.

pacs:

89.75.-k, 89.75.Da, 89.65.-s, 89.65.GhElectronic commerce (e-commerce) refers to any type of business or commercial transaction that involves information transfer across the Internet. As a formation of e-commerce, the online auction, i.e., the auction via the Internet heck , has expanded rapidly over the last decade and has become a fascinating new type of business or commercial transaction in this digital era. Online auction technology has several benefits compared with traditional auctions. Traditional auctions require the simultaneous participation of all bidders or agents at the same location; these limitations do not exist in online auction systems. Owing to this convenience, “eBay.com,” the largest online auction site, boasts over 40 million registered consumers and has experienced rapid revenue growth in recent years.

Interestingly, the activities arising in online auctions generated by individual agents proceed in a self-organized manner mantegna ; bouchard ; stanley ; challet ; pennock ; hulst . For example, the total number of bids placed in a single item or category and the bid frequency submitted by each agent follow power-law distributions yang . These power-law behaviors simon ; zhang ; albert are rooted in the fact that an agent who makes frequent bids up to a certain time is more likely to bid in the next time interval. This pattern is theoretically analogous to the process that is often referred to as preferential attachment, which is responsible for the emergence of scaling in complex networks ba . This is reminiscent of the mechanism of generating the Zipf law zhang ; pareto . The accumulated data of a detailed bidding process enable us to quantitatively characterize the dynamic process. In this paper, we describe a master equation for the bidding process. The master-equation approach is useful to capture the dynamics of the online bidding process because it takes into account of the effect of openness and the non-equilibrium nature of the auction. This model is in contrast to the existing equilibrium approach lb ; kauf in which there is a fixed number of bidders. The equilibrium approach is relevant to traditional auctions; however, it is unrealistic to apply this approach to Internet auctions. The power-law behavior of the bidding frequency submitted by individual agents can be reproduced from the master equation. Moreover, we consider the probability of an agent who has bidden times, called the -frequent bidder, becoming the final winner. We conclude that the winner is likely to be the one who bids at the last moment but who placed infrequent bids in the past.

Our study is based on empirical data collected from two different sources yang . The first dataset was downloaded from the web, http://www.eBay.com, and is composed of all the auctions that closed in a single day. The data include 264,073 auctioned items, grouped into 194 subcategories. The dataset allows us to identify 384,058 distinct agents via their unique user IDs. To verify the validity of our findings in different markets and time spans, the second dataset was accumulated over a period of one year from eBay’s Korean partner, auction.co.kr. The dataset comprised 215,852 agents that bid on 287,018 articles in 355 lowest categories.

An auction is a public sale in which property or items of merchandise are sold to the bidder who proposes the highest price. Typically, most online auction companies adopt the approach of English auction, in which an article or item is initially offered at a low price that is progressively raised until a transaction is made. Both “eBay.com” and “auction.co.kr” adopt this rule and many bidders submit multiple bids in the course of the auction. An agent is not allowed to place two or more bids in direct succession. It is important to notice that the eBay auction has a fixed end time: It typically ends a week after the auction begins, at the same time of day to the second. The winner is the latest agent to bid within this period. In such an auction that has a fixed deadline, bidding that takes place very close to the deadline does not give other bidders sufficient time to respond. In this case, a sniper–the last moment bidder–might win the auction, while the bid that follows has a substantial probability of not being transmitted successfully. While such a bidding pattern is well known empirically, no quantitative analysis has been performed on it as yet. In this study we analyze this issue through the rate equation approach.

To characterize the dynamic process, we first introduce several quantities for each item or article as follows:

-

(i)

When a bid is successfully transmitted, time increases by one.

-

(ii)

Terminal time is the time at which an auction ends. Thus, the index of bids runs from to .

-

(iii)

is the number of distinct bidders who successfully bid at least once up to time . Thus, the index of bidders (or agent) runs from to .

-

(iv)

is the number of successful bids transmitted by an agent up to time .

-

(v)

is the number of bidders with frequency up to time .

From the above, we obtain the relations

| (1) |

and

| (2) |

for any time including the terminal time .

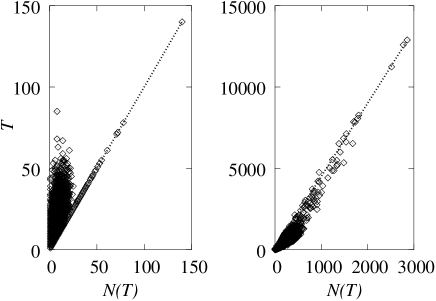

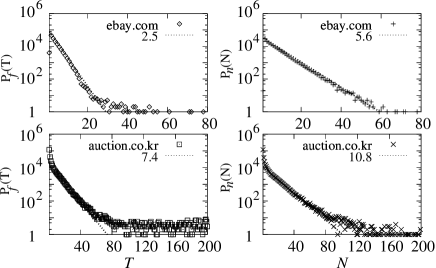

It is numerically found that is linearly proportional to , that is, . The average value of the proportional coefficient for different items or articles listed in eBay is estimated to be when the total number of bidders exceeds . However, when the number of bidders is lower, the proportional coefficient is very large, as shown in Fig. 1. For the Korean auction, , regardless of the number of bidders. On the other hand, the bidding frequencies and the number of bidders for each article are not uniform. Their distributions, denoted as and , respectively, follow the exponential functions and , respectively, where and 10.8 for the eBay and Korean auctions, respectively, and and 5.6 for the eBay and Korean auction, respectively (Fig.2).

We introduce the master equation for the bidding process as

| (3) |

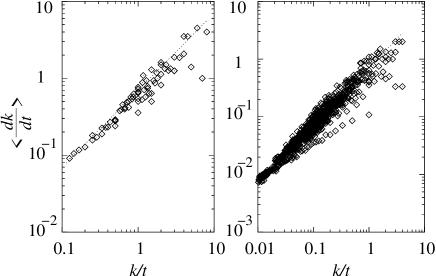

where is the transition probability that a bidder, who has bid times up to time , bids at time . In this case, the total bid frequency of that agent up to time becomes . Note that a bidder is not allowed to bid successively. In the master equation, we presume that the bidding pattern is similar over different items when is sufficiently large. Then, may be written as on average over different items. Empirically, we find that

| (4) |

where is estimated to be for both the eBay and Korean auctions (Fig. 3). The fact that is reminiscent of the preferential attachment rule in the growing model of the complex network ba . is the probability that a new bidder makes a bid at time . Using the property that , we obtain

| (5) |

Next we then change the discrete equation, Eq. (3), to a continuous equation as follows:

| (6) |

which can be rewritten as

| (7) |

When , we use the method of separation of variables, , thus obtaining

| (8) |

where is a constant of separation, and

| (9) |

Thus, we obtain

| (10) |

When ,

| (11) |

Next from the fact that , we obtain

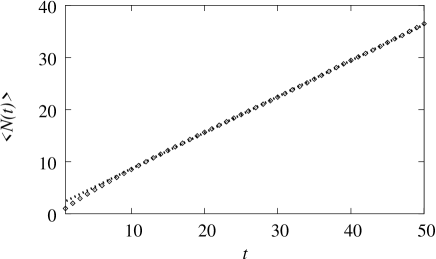

Therefore, we obtain and by using Eq. (11). Note that , and the linear relationship holds asymptotically. The linear relationship breaks down for small . From the empirical data, Fig. 4, we find that . Since in Fig. 3, we obtain . Therefore,

| (12) |

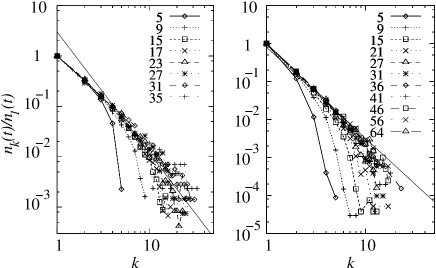

for large , which fits reasonably with the numerical data shown in Fig.5.

In eBay auctions, the winner is the last bidder in the bidding sequence. Now, we trace the bidding activity of the winner in the bidding sequence in order to find the winning strategy. To proceed, let me define as the probability that a bidder, who has bid times up to time , bids at time successfully. Note that a bidder is not allowed to bid successively. In this case, is nothing but the probability that a -frequent bidder becomes the final winner. The probability satisfies the relation,

| (13) | |||||

with the boundary conditions and . The first term on the right hand side of Eq. (13) is composed of three factors: (i) is the probability that one of the existing bidders bids successfully at time , (ii) means that bidding at time is carried out by the -frequent bidder, and (iii) the last factor is derived from the bidding rate, Eq. (4), where the contribution by the bidder at time is excluded because he/she is not allowed to bid at time . The second term represents the addition of a new bidder at time .

The rate equation, Eq. (13), can be solved recursively. To proceed, we simplify Eq. (13) by assuming that is significantly larger than , which is relevant when the number of bidders is large. Then,

Since , is obtained to be

| (15) |

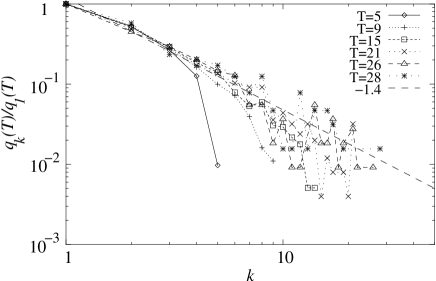

within the leading order. Considering that in Eq. (12) and is constant, we obtain for large and , with a weak dependence on . Thus, the winning probability by the -frequent bidder is simply given as

| (16) |

in the limit . This result is confirmed by the empirical data in Fig. 6.

Our analysis explicitly shows that the winning strategy is to bid at the last moment as the first attempt rather than incremental bidding from the start. This result is consistent with the empirical finding by Roth and Ockenfels roth in eBay. According to them, the bidders who have won the most items tend to wait till the last minute to submit bids, albeit there is some probability of bids not being successfully transmitted. As evidence, they studied 240 eBay auctions and found that 89 bids were submitted in the last minute and 29 in the last ten seconds. Our result supports these empirical results.

In conclusion, we have analyzed the statistical properties of

emerging patterns created by a large number of agents based on the

empirical data collected from eBay.com and auction.co.kr.

The number of bidders and the winning probability

decay in power laws as and , respectively, with bid frequency , which

has been confirmed by empirical data.

This work is supported by the KRF Grant No. R14-2002-059-01000-0 in the ABRL program funded by the Korean government MOEHRD and the CNS research fellowship in SNU (BK).

References

- (1) E. van Heck and P. Vervest, Communication of the ACM 41, 99 (1998).

- (2) R.N. Mantegna and H.E. Stanley, An introduction to econophysics: Correlations and complexity in finance (Cambridge University Press, Cambridge, 2000).

- (3) J.P. Bouchard and M. Potters, Theory of financial risks: From statistical physics to risk management (Cambridge University Press, Cambridge, 2000).

- (4) M.H.R. Stanley, L.A.N. Amaral, S.V. Buldyrev, S. Havlin, H. Leschhorn, P. Maass, M.A. Salinger and H.E. Stanley, Nature 379, 804 (1996).

- (5) D. Challet and Y.-C. Zhang, Physica A 246, 407 (1997).

- (6) D.M. Pennock, S. Lawrence, C.L. Giles and F.A. Nielsen, Science 291, 987 (2001).

- (7) R. D’Hulst and G.J. Rodgers, Physica A 294, 447 (2001).

- (8) I. Yang, H. Jeong, B. Kahng, and A.-L. Barabási, Phys. Rev. E 68, 016102 (2003).

- (9) H.A. Simon, Biometrika 42, 425 (1955).

- (10) M. Marsili and Y.-C. Zhang, Phys. Rev. Lett. 80, 2741 (1998).

- (11) R. Albert and A.-L. Barabasi, Rev. Mod. Phys. 74, 47 (2002).

- (12) A.-L. Barabasi and R. Albert, Science 286, 509 (1999).

- (13) V. Pareto, Cours d’economie politique (Rouge, Lausanne et Paris, 1897).

- (14) Y. Shoham and M. Tennenholtz, Games and Economic Behavior, 35, 197 (2001).

- (15) R.J. Kauffman and C.A. Wood, Proc. of ICIS (2000).

- (16) A.E. Roth and A. Ockenfels, American Economic Review, 92, 1093 (2002).