Cross-country hierarchical structure and currency crisis

Abstract

Using data from a sample of 28 representatives countries, we propose a classification of currency crises consequences based on the ultrametric analysis of the real exchange rate movements time series, without any further assumption. By using the matrix of synchronous linear correlation coefficients and the appropriate metric distance between pairs of countries, we were able to construct a hierarchical tree of countries. This economic taxonomy provides relevant information regarding liaisons between countries and a meaningful insight about the contagion phenomenon.

pacs:

PACS Nos.: 02.50.Sk, 89.90.+nI Introduction

Prediction and contagion of financial crises have received much attention in recent years. The financial instability during the nineties has caused intense exchange and banking crises, in developed and, especially, in developing countries. Most of the empirical literature has focused their interest in identification, prediction and contagion of currency crises, and the macroeconomic variable which seems to better account for both effects is the real exchange rate (RER) KL98 ; Ab03 ; Pe05 ; PA03 . However, conclusive results from the empirical literature are hard to achieve. One of the reason for unconvincing answers in this debate is the enormous differences in periods and countries used in the empirical works, without taking account for regional or country specific differences in the underlying dynamics of the variables time series used Zh01 PA03 .

From a methodological point of view, techniques and tools formerly used in the physical and biological fields, have become to be applied in the analysis of economic data MS00 ; BP00 , in particular, to the case of stock portfolios. In this case, correlation based clustering of synchronous financial data has been performed to obtain a taxonomy of a set stocks from the US equity market. The last objective in this kind of works is to improve economic forecasting and modeling the complex dynamic underlying the raw data and their basic hypothesis is that financial time series are carrying valuable economic information that can be detected.

Following the above ideas, we shall extract information present in the correlation matrix of the RER in a sample of 28 representative countries, in the period of 1990-2002. By using the subdominant ultrametric associate with a metric distance in the correlation space, we first construct the Minimum Spanning Tree (MST) which provides a topological picture of the countries links. Then, we shall proceed to construct a hierarchical tree associated with the distance matrix in order to obtain a country taxonomic description provided by the real exchange data. So, the main aim of this work is to detect hierarchical structure of our country sample that arises from the relations links in their exchange rate dynamics. Clustering countries in such a way could be of importance in several economic aspects related to the empirical currency crises and contagion literature. Probably the most important is the identification of homogenous countries in their exchange rate dynamics in order to construct better regional Early Warning Systems (EWS), more accurate forms of dating the events of crises especially design for homogeneous regions (or isolated countries) and, finally, for understanding the possibilities of forecasting of contagion.

II Methodology

II.1 Data

Returns from in each of the 28 time series has been calculated in the usual way,

| (1) |

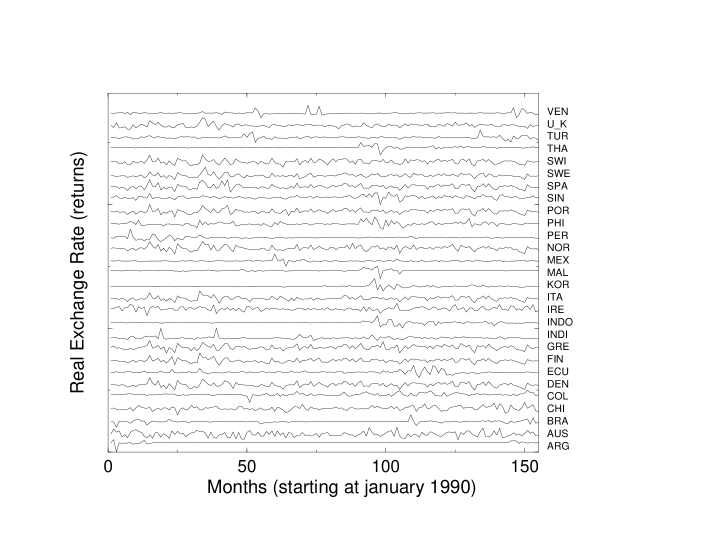

where is the monthly real exchange rate from country , at month , and the corresponding return. The period 1990-2002 has been used, yielding a total of 156 data points for each country. Figure (1) shows the actual time series used for further calculations. is computed as the ratio of foreign price proxied by U.S. consumer price to domestic consumer price, and the result is multiplied by the nominal exchange rate of the domestic currency with U.S. dollar. Data has been drawn from International Financial Statistics in the IMF database available on-line .

II.2 Numerical Methods

In order to quantify the degree of similarity between pairs of time series belonging to different countries, we have calculated the Pearson correlation coefficient PT92

| (2) |

where is the mean value of in the period considered. Because is a measure of similarity, and a measure of ”distance” is actually needed in order to construct the ultrametirc space RT86 , following Gower Go66 , we define the distance between the time evolution of and as,

| (3) |

The last equality came from the symetry property of the correlation matrix, and the normalization . In this way, fulfils the three axioms of a distance:

-

•

if and only if

-

•

-

•

The third axiom, the triangular inequality, characterize a metric

space. An ultrametric space, on the other hand, is endowed with

a distance that obeys a stronger inequality, the

ultrametric distance :

| (4) |

Thus, it follows that the distance matrix given by Equation (3) satisfies ultrametricity and a hierarchical tree can be uniquely constructed RT86 .

One method to obtain directly from the distance matrix is through the MST method RT86 . Given the metric space , that is, countries and the distance defined by Equation (3), there is associated with this space a nondirected graph with the same elements of as vertices, and links between the elements , the distances . The MST is a tree with the same vertices as in but of minimal total lenght. Although more than one MST can be constructed on , is unique. With the information provided by the MST, the distance between two elements and in is given by

| (5) |

where denotes the unique path in the MST between and (). We shall show in the next section how to construct in our particular case.

III Results

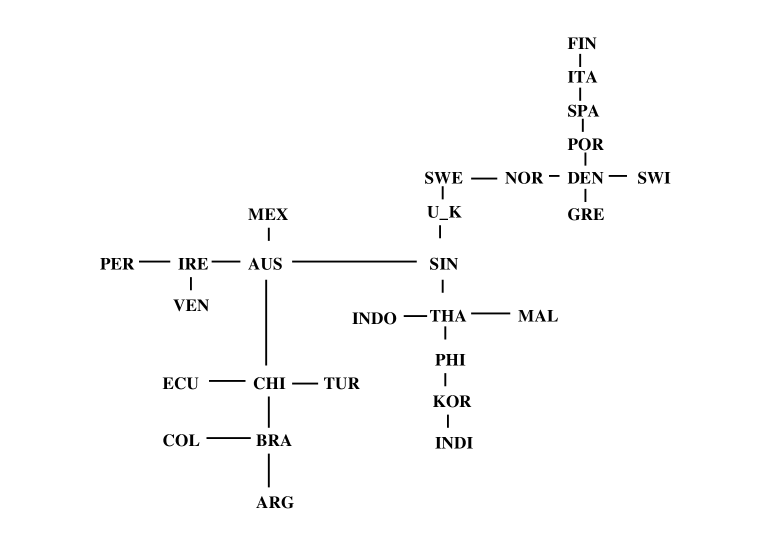

We first construct the MST directly from the distance matrix . One begins by connecting the closest countries given by , in this case POR-SPA with a distance equal to 0.41. Table 1 shows some representative distances. One then proceeds by linking the remaining countries accordingly with their closeness to the previously connected countries. For instance, in the distance matrix, the shortest distance following POR-SPA is DEN-SWI with a distance of 0.411, and in this way, we have another link between both countries. The next one is DEN-GRE with a distance of 0.464. We then proceed to connect GRE to the former pair DEN-SWI, giving GRE-DEN-SWI. At this moment, we have two ”clusters”, POR-SPA and GRE-DEN-SWI. Proceeding in the above explained way, we finally construct a tree with the 28 countries and 27 links among them. Figure (2) shows the complete MST given by the distance matrix .

| Distance | country | country |

|---|---|---|

| 0.410 | POR | SPA |

| 0.411 | DEN | SWI |

| 0.464 | DEN | GRE |

| 0.465 | DEN | NOR |

| 0.490 | DEN | POR |

| … | … | … |

| 0.666 | MAL | THA |

| 0.669 | ITA | NOR |

| 0.669 | FIN | SWI |

| … | … | … |

| 0.797 | SIN | THA |

| 0.834 | INDO | THA |

| 0.847 | MAL | SIN |

| 0.905 | PHI | THA |

| 0.926 | INDO | SIN |

| 0.937 | INDO | MAL |

| 0.952 | SWE | U_K |

| 0.972 | ITA | U_K |

| … | … | … |

| 1.020 | AUS | IRE |

| … | … | … |

| 1.137 | ARG | BRA |

| 1.156 | PHI | SIN |

| 1.171 | BRA | CHI |

| 1.184 | KOR | PHI |

| … | … | … |

| 1.241 | BRA | COL |

| … | … | … |

| 1.272 | CHI | TUR |

| … | … | … |

| 1.281 | AUS | MEX |

| … | … | … |

| 1.329 | INDI | KOR |

| … | … | … |

| 1.330 | SPA | TUR |

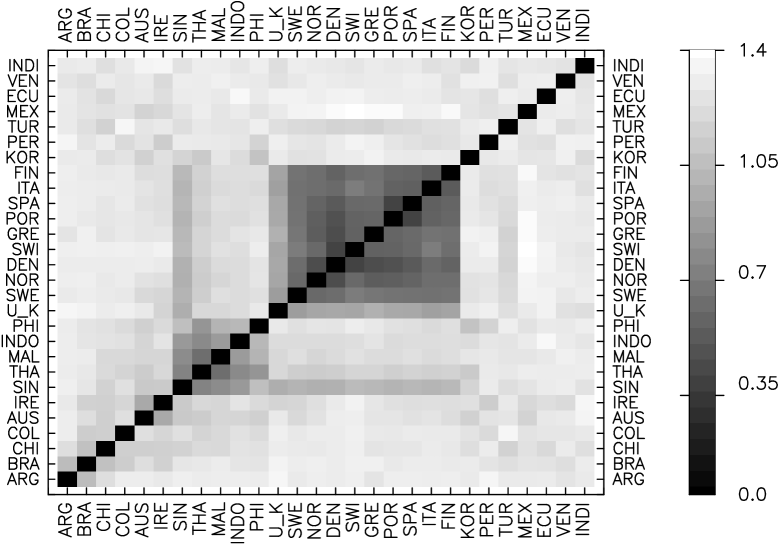

Armed with the information provided by the distance matrix and the MST, we proceed to construct the subdominant ultrametric, accordingly with Equation (5). Firstly, we define the subdominant ultrametric distance matrix . This ultrametric matrix is obtained by defining the subdominant ultrametric distance between countries and , as the maximum value of the distance detected by moving, in single steps, from country to country through the shortest path connecting and in the MST (Equation 5). For instance, the ultrametric distance = 0.410 because both countries are placed side by side in the MST, and in this way, the ultrametric distance coincide with the metric distance, however, = 0.490, which is the maximum metric distance between adjacent countries in the path from SWI to SPA (see Figure 2 and Table 1). Proceeding in this way, we then order countries accordingly with their ultrametric distances to the others, placing the more tightly connected countries in the center, and outward the less connected. In order to obtain a clear picture of the distances between countries, we have plotted in Figure (3) the distance matrix given by Equation (3), but countries ordered accordingly with their ultrametric distances.

In the MST three groups of countries are clearly seen. It is interesting to note that these groups are built by geographical neighbor countries. EU countries group appears in first place with the smallest distances among them; Asian countries followed and in third place Latin American countries have shown higher distances between their countries than the other two first groups. As expected, EU countries have shown the shortest distances in our sample (distances between 0.41 and 0.76) due to common relative real exchange movementsAI00 inside the European Monetary System111In January 1, 1999, Spain, Portugal, Ireland, Finland, Italy and Norway, and other european countries not in our sample, gave up their own currencies and adopted the Euro currency, with fixed nominal exchange among them, and in January 2001 Greece joined the Euro too (United Kingdom, Denmark and Swedden refused to join the Euro). After Januay 1999, the Greek and Danish currencies joined to the new Exchange Rate Mechanism, where currencies are allowed to float within a range of against the Euro. But as Greece joined the Euro in 2001, Denmark is the only participant in the mechanism in our country sample., although two different sub-groups of countries shows up; one in the north, with DEN as the most linked country and the other one in the south of Europe with short distances and intense links among SPA, POR and ITA. Finally, FIN is the least connected country in this group and U_K and IRE seem not to belong to it. Correlations coefficients in Figure (3) clearly support the closeness among EU countries exchange rate dynamics based, of course, in the common policy they have followed.

Asian countries form the next group order by distance. By far, THA and MAL are the most connected into the group (distances between 0,66 and 1) and are also quite connected with the EU countries and AUS and U_K (). On the other side, KOR and especially INDI form a relatively isolated pair and have shown little and less intense connections with any of the groups.

Our third group is the Latin American one. Distances show high values (above 1,1) and very diffuse connections so, in fact, it is not a homogeneous group. Interesting enough is the important role played by BRA in South America as a centre of connections in this region. In this sense, BRA is the first link for ARG, CHI and COL showing the central role of their exchange rate economic policy in the South American continent. (In Figure (3) the correlation coefficients show the same central role of BRA). On the other hand, ARG, PER, ECU and VEN have shown relative isolated exchange rate dynamics in the analyzed period, with no apparent relevant links in the region. The same occurs to MEX but in this case the reason probably was their intense trade and financial relations with the United States. In Figure (3) we can see no apparent group formation in the region, except light correlations in BRA.

In this regional hierarchy there are countries with connections more ”diffuse”. For instance, the U_K shows small distances with the EU group (0,95) in first term but also with Asian countries and IRE and AUS. In the same direction, CHI shows short distance with BRA (1,17) in first time but immediately are AUS, COL, IRE, ECU and MAL. More isolated is INDI with very diffuse connections and high distances (1,33), to KOR, U_K, CHI, ITA and SIN.

IV Conclusions

We have introduced a new criterion to characterize the effects of currency crises based solely on the correlations of real exchange rate returns time series. By using the information provided by the correlations between synchronous movements in the real exchange rates in different countries, we were able to construct a geometrical picture of the countries connections by means the MST. Moreover, taxonomic information is also extracted from the time series, by ordering countries accordingly with its ultrametric distance (Figure 3).

The hierarchical structure has shown three groups of countries which are clearly divided in a regional dimension. EU and Asian countries are relatively homogenous groups, meanwhile Latin American countries form a heterogeneous region where Brazil exchange rate dynamics is central. On the other side, we have shown a group of countries which do not belong to a specific group, such us Chile, India or United Kingdom. From an economic point of view, information of our hierarchical tree could be useful in three relevant aspects. First of all, we would expect that countries or group of countries with short distances among them were affected commonly by the same, or almost the same, economic and non economic factors, such as the EU group and in the central Asian group. When distances are larger among countries, exchange rate dynamics are affected by country specific factors.

In second place, information of our tree could be of interest for defining different methods of dating a currency crises depending of the range of countries to be used in the empirical analysis. So, this approach could improve results in dating a currency crises and also in defining the event of crises. In the same direction, this taxonomy can be used to define different regional or individual Early Warning Systems.

In third place, the taxonomy associated with the obtained hierarchical structure might be useful in the theoretical description of contagion and in the search of specific economic and no economic factors affecting different groups of countries. In addition, this hierarchy may be a useful tool in the analysis of exchange rate crises contagion.

Acknowledgments

We would like to thank, without implicating, International Economics Research Group in Oviedo University. G.O. thanks financial support from the Consejo Nacional de Investigaciones Cientificas y Técnicas, Argentina. D. M. thanks financial support from the University of Oviedo.

Appendix A Countries

The 28 countries included in this work are as follows: Argentine (ARG), Malaysia (MAL), Thailand (THA), Mexico (MEX), Korea (KOR), Indonesia (INDO), Brazil (BRA), Venezuela (VEN), Peru (PER), India (INDI), Ecuador (ECU), Turkey (TUR), Colombia (COL), Singapore (SIN), Philippines (PHI), United Kingdom (U_K), Sweden (SWE), Italy (ITA), Ireland (IRE), Finland (FIN), Chile (CHI), Greece (GRE), Portugal (POR), Switzerland (SWI), Denmark (DEN), Spain (SPA), Norway (NOR), Australia (AUS)

References

- (1) G. Kaminsky, S. Lizondo, and C. M. Reinhart, IMF Staff Papers, 45, 1-56 (1998).

- (2) A. Abiad, IMF Working Paper,32, 1-60 (2003)

- (3) Pérez, J. Applied Financial Economics Letters, 1 (1), 41-46 (2005)

- (4) S. Pozo, C. Amuedo-Dorantes, Journal of International Money and Finance, 22, 591-609 (2003).

- (5) Z. Zhang (2001) IMF Working Paper, International Monetary Fund (November) (2001).

- (6) R. N. Mantegna, H. E. Stanley, An introduction to Econophysics: Correlations and Complexity in Finance (Cambridge University Press, UK, 2000)

- (7) J.-P. Bouchaud, M. Potters, Theory of Financial Risk: from Statistical Physics to Risk Management (Cambridge University Press, Cambridge, UK, 2000).

- (8) R. N. Mantegna, European Physical Journal B,11, 193-197 (1999).

- (9) J. C. Gower, Biometrika,53, 325 (1996).

- (10) W.H. Press, S.A. Teukolsky, W.T. Vetterling and B.P. Flannery, Numerical Recipes (Cambridge University Press, Cambridge, 1992), 2nd. ed.

- (11) R. Ramal, G. Toulouse and M. A. Virasoro, Review of Modern Physics, 58(3), 765-788 (1986).

- (12) M. Ausloos, K. Ivanova, Physica A, 286, 353-366 (2000).

- (13) G. Kaminsky, M. Reinhart and C. A. Vegh, Journal of Economic Perspectives, American Economic Association, 17(4), 51-74 (2003).