Dynamic instability in a phenomenological model of correlated assets

Abstract

We show that financial correlations exhibit a non-trivial dynamic behavior. We introduce a simple phenomenological model of a multi-asset financial market, which takes into account the impact of portfolio investment on price dynamics. This captures the fact that correlations determine the optimal portfolio but are affected by investment based on it. We show that such a feedback on correlations gives rise to an instability when the volume of investment exceeds a critical value. Close to the critical point the model exhibits dynamical correlations very similar to those observed in real markets. Maximum likelihood estimates of the model’s parameter for empirical data indeed confirm this conclusion, thus suggesting that real markets operate close to a dynamically unstable point.

Financial markets – as prototypical examples of the collective effects of human interaction – have recently attracted the attention of many physicists. This is because, in spite of their internal complications, their aggregate behavior exhibits surprising regularities which can be cast in the form of simple, yet non-trivial, statistical lawsJPB-book ; MantegnaStanley ; Daco , reminiscent of the scaling laws obeyed by anomalous fluctuations in critical phenomena. Such a suggestive indication has been put on even firmer basis by recent research on the statistical physics approach to interacting agent modelsmercatino ; Lux ; contbouchaud ; levy ; MG . This has shown that quite realistic market behavior can indeed be generated by the internal dynamics generated by traders’ interaction.

The theoretical approach has, thus far, mostly concentrated on single asset models, whereas empirical analysis has shown that ensembles of assets exhibit rich and non-trivial statistical properties, whose relations with random matrix theory jpb-rmt ; gopicorr , complex networks kertesz ; gcalda and multi-scaling Eisler have attracted the interest of physicists. The central object of study is the covariance matrix of asset returns (at the daily scale in most cases). The bulk of its eigenvalue distribution is dominated by noise and described very well by random matrix theory jpb-rmt . The few large eigenvalues which leak out of the noise background contain significant information about market’s structure. The taxonomy built with different methods mantegna ; gopicorr ; states from financial correlations alone bear remarkable similarity with a classification in economic sectors. This agrees with the expectation that companies engaged in similar economic activities are subject to the same “factors”, e.g. fluctuations in prices or demands of common inputs or outputs. Besides their structure, market correlations also exhibit a highly non-trivial dynamics: Correlations “build up” as the sampling time horizon on which returns are measured increases (Epps effect) and saturate for returns on the scale of some days Drozdztau . Furthermore, these correlations are persistent over time kertesz and they follow recurrent patterns states .

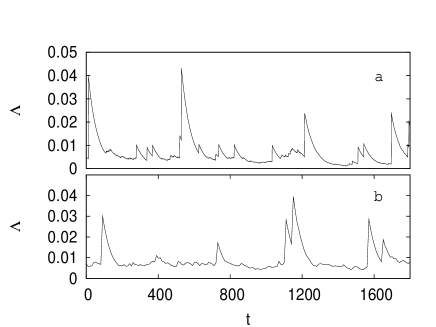

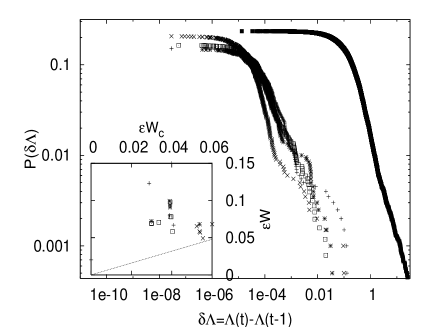

In what follows we shall mostly concentrate on the dynamics of the largest eigenvalue of the correlation matrix. The corresponding market mode jpb-rmt describes the co-movement of stocks and it accounts for a significant fraction of the correlationsnota_ec . Fig. 1a shows the time dependence of the largest eigenvalue of the (exponentially averaged) correlation matrix of daily returns for Toronto Stock Exchange data . Similar behavior has been reported earlier Drozdz for different markets. Fig. 2 shows that fluctuations in the largest eigenvalue are broadly distributed, suggesting that Fig. 1a can hardly be explained entirely as the effect of few external shocks.

This leads us to formulate the hypothesis that such non-trivial behavior arises as a consequence of the internal market dynamics. One of the key functions of financial markets is indeed that of allowing companies to “trade” their risk for return, by spreading it across financial investors. Investors on their side, diversify (i.e. spread) their strategies across stocks so as to minimize risk, as postulated by portfolio optimization theory elton . The efficiency of portfolio optimization depends on the cross correlations among the stocks the financial market is composed of. The optimal portfolio is computed under the price taking assumption that investment does not affect the market. While this is reasonable for the single investor, the effect of many investors following this same strategy can be sizeable. If financial trading activity resulting from portfolio optimization strategies have an impact on prices’ dynamics, it will also affect the correlations which these strategies exploit. Hence financial correlations enter into a feedback loop because they determine in part those trading strategies which contribute to the price dynamics, i.e. to the financial correlations themselves. This feedback is somewhat implicit in the Capital Asset Pricing Model (CAPM), which concludes that since all traders invest according to the optimal portfolio, the market is well approximated by a one factor model elton (see however gcalda ). While this explains why the largest eigenvalue of the correlation matrix is so well separated from the other ones, CAPM relies on rational expectation equilibrium arguments, and it does not address dynamical effects such as those of Fig. 1a.

This Letter discusses a general phenomenological approach, in the spirit of Landau’s theory of critical phenomena Landau , which shows that a non-trivial dynamics of correlations can indeed result from the internal dynamics due to trading on optimal portfolio strategies. The model predicts a dynamical instability if the investment volume exceeds a critical value. Not only we find very realistic dynamics of correlations close to the critical point (see Fig. 1b) but maximum likelihood parameter estimation from real data suggest that markets are indeed close to the instability. Phenomenological models are particularly suited for modeling complex systems, such as a financial market, were a bottom-up (microscopic) approach inevitably implies dealing with many complications and introducing ad hoc assumptions note . For the ease of exposition, we shall first introduce a minimal model which captures the interaction among assets induced by portfolio investment. Later we will show that this model contains the lowerst order terms in a general expansion of the dynamics and that all the terms beyond these are irrelevant as far as the main conclusions are concerned. A further reason for focusing on the simplest model is that it will make the comparison with empirical data easier.

Let us consider a set of assets. We denote by the vector of log-prices and use bra-ket notation bra-ket . We focus on daily time-scale and assume that undergoes the dynamics

| (1) |

where is the vector of bare returns, which describes all external “forces” which drive the prices, including economic processes. This is assumed to be a Gaussian random vector with

| (2) |

and will be considered as parameters in what follows.

The last term of Eq. (1) describes the impact of portfolio investment on the price dynamics: is an independent Gaussian variable with mean and variance and the vector is the optimal portfolio with fixed return and total wealth . In other words, is the solution of

| (3) |

where is the correlation matrix at time . Both the expected returns and the correlation matrix , which enter Eq. (3), are computed from historical data over a characteristic time :

| (4) | |||||

| (5) |

where noteavg . This makes the set of equations above a self-contained dynamical stochastic system. In a nutshell, it describes how the economic bare correlated fluctuations are dressed by the trading activity due to investment in optimal portfolio strategies. and are phenomenological parameters reflecting the portfolio composition which dominates trading activity, not necessarily those of a representative investor. In particular, note that is a quantity, not a percentage as in portfolio theory elton . Indeed, the impact of investment on prices depends on the volume of transactions. The parameter , which can be taken as a proxy for the volume of trading on portfolio strategies, will play a crucial role in what follows.

These parameters are assumed to be constant, meaning that portfolio policies change over time-scales much longer than . Portfolio theory is, in principle, based on expected returns and covariances. We implicitely assume that historical data can be used as a proxy for expected correlations and returns. Eqs. (1–5) also assume that portfolio investment is dominated by a single time scale . Later we shall argue that a generic distribution of time scales would not change the main results. Finally, Eq. (1) assumes a linear price impact and gaussian bare returns. Both assumptions may be questionable, specially at high frequency high_freq_impact ; impact . We shall see, however, that non-trivial dynamics and statistics (including a fat tailed distribution of returns) arises even in such a simplified setting, thus suggesting that the specific market mechanism and the statistics of bare returns are unessential ingredients.

Numerical simulations of the model show a very interesting behavior. In Fig 1b we plot the temporal evolution of the maximum eigenvalue of the correlation matrix for a particular choice of parameters (see later). The dynamics is highly non-trivial, with the appearance of instabilities resembling those observed for real markets (Fig. 1a). To be more precise, we also analyze the statistics of the day-to-day differences in . In Fig. 2 we can see a clear power-law behavior emerging, again very similar to the one we get for real markets.

In order to shed light on these findings, let us consider the behavior of the model in the limit . We assume that, in this limit, the correlations and hence reach a time independent limit, which by Eqs. (1, 3) is given by

| (6) |

where and are fixed by the constraints and . Notice that needs to be determined self-consistently. We find which, combined with Eq. (6), yields an equation for . In order to make the analysis simpler, we assume structure-less bare correlations . In this case has eigenvalues equal to , and one eigenvalue with eigenvector parallel to , whose value is 2solutions

| (7) |

where and , are the average and the variance of bare returns, respectively. If and are both proportional to , then the contribution to due to portfolio investment is also proportional to . This is indeed the order of in empirical data. Most remarkably, Eq. (7) makes sense only for , i.e. for

| (8) |

As the solution develops a singularity with infinite slope . This is reminiscent of the divergence of susceptibility close to a phase transition, signalling that the response to a small perturbation diverges as . The origin of the singularity at is directly related to the impact of portfolio investment. Indeed, notice that the two constraints are hyper-planes in the space of portfolios when and always have a non-empty intersection. When , the constraint on return becomes an hyper-sphere, centered in and of radius . Hence intersections exist only for .

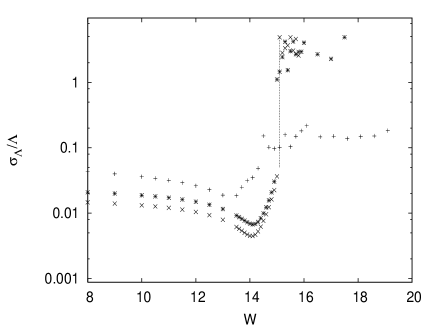

As anticipated, Eq. (1) can be thought of as the lowest order of a phenomenological expansion Landau . Higher orders, e.g. , as well as terms proportional to and its time derivatives, can be included. Likewise, one can consider a generic matrix , or add several components of portfolio investment in Eq. (1), each with different parameters , and or acting over different time horizons . In all these case, we confirmed elsewhere the existence of a dynamical instability when the volume of trading exceeds a critical value, as long as the time-scales () over which averages are taken in Eqs. (4,5) are very large. The analytic approach can be extended to finite by a systematic expansion in the phase elsewhere . This expansion describes how fluctuations in slow quantities, such as or vanish as . We find that the coefficients of the expansion diverge as , signalling that fluctuations do not vanish for . For example, we find that fluctuations in diverge as , when . This is why higher order terms such as in Eq. (1) are irrelevant, in the sense of critical phenomena, i.e. their presence does not affect the occurrence of the phase transition.

Numerical simulations fully confirm these results. Fig. 3 reports the relative fluctuations of as a function of , for simulations carried out at different time scales . For , fluctuations vanish as increases and converges to the value of Eq. (7). For , instead, the dynamics is characterized by persistent instabilities with fluctuations of the same order of , and it does not attain a smooth limit as . For values of smaller but close to the model exhibits strong fluctuations, precursors of the instabilities for . It is precisely in this critical region that we recover realistic results, such as those of Fig 1b. Moreover, the distribution of returns develops a power law behavior as approaches (with a cutoff which diverges as ).

The presence of a phase transition from a stable to an unstable state and the strong resemblance of the dynamics of the model close to criticality with real data (see Fig. 1) suggests that real markets might be close to the phase transition. In order to investigate this issue systematically, we estimate the parameters of our model from real data. In doing this we implicitly assume that parameters , , etc. vary slowly on time scales of order . We compute the likelihood that the particular set of time series of a given market are produced as output of Eq. (1) for a particular choice of parameters. Next we find the parameters which maximize the likelihood elsewhere . As a check, the procedure was run on synthetic data set generated by Eq. (1) and it allowed us to recover the parameters with which the data set was created. In the inset of Fig. 2 we plot the result of such a fit for (the assets of) four different indices in the time period 1997-2005 data . We used and fits were taken on a time window of days. Notice, in this respect, that while in our model enters both in the dynamics and in the way we take averages, in the empirical analysis it only enters in the way we take averages, whereas we don’t have access to the time scale used by investors. We checked that the main results do not depend significantly on the choice of . We see that fitted parameters for real markets tend to cluster close, but below, the transition line . This is also consistent with the similarity of the distribution of for real and synthetic data of Fig. 2.

Our model is very stylized and it misses many important aspects. For example, it is undeniable that external factors and global events have an effect on financial markets. For example, the introduction of the Euro has a visible effect on the scatter of points for the DAX in the inset of Fig. 2. On the other hand, the points relative to non-European markets in different time windows cluster in the same region, showing that parameters can indeed be considered as roughly constant on the time-scales discussed here. At any rate, rather than insisting on the validity of the model on theoretical grounds, we have shown that it reproduces key empirical features of real financial markets. This makes us conjecture that a sizeable contribution to the collective behavior of markets arises from its internal dynamics and that this is a potential cause of instability. If, following Ref. crashes , crashes were activated events triggered by large fluctuations, the proximity to the instability would make the occurrence of such correlated fluctuations more likely, thus enhancing the likelihood of crashes.

Our results indicate the existence of an additional component of risk due to the enhanced susceptibility of the market. Such “market impact” risk arises because investing in risk minimization strategies affects the structure of correlations with which those strategies were computed. This component of risk diverges as the market approaches the critical point , thus discouraging further investment. This provides a simple rationale of why markets “self-organize” close to the critical point. Such a scenario is reminiscent of the picture which Minority Games MG provide of single asset markets as systems driven to a critical state, by speculative trading GCMG . In both cases, the action of traders (either to exploit predictable patterns or to minimize risk) produces a shift in the position of the equilibrium that counteracts the effect of this action (by either making the market less predictable or more risky), as if a sort of generalized Le Chatelier’s principle were at play.

References

- (1) J.-P. Bouchaud and M. Potters Theory of financial risk and derivative pricing: from statistical physics to risk management (Cambridge University Press, Cambridge, 2003).

- (2) R. Mantegna and E. Stanley, Introduction to Econophysics (Cambridge University Press, 1999)

- (3) M. M. Dacorogna, et al. An Introduction to High-Frequency Finance, Chap. V, Academic Press, London (2001)

- (4) Caldarelli G., Marsili M. and Zhang Y-C., Europhys. Lett. 40, 479 (1997)

- (5) Lux T. and Marchesi M., Nature 397 (6719) 498-500 (1999)

- (6) R. Cont and J.-P. Bouchaud, Macroecon. Dyn. 4, 170 (2000).

- (7) H. Levy, M. Levy, S. Solomon, From Investor Behaviour to Market Phenomena, Academic Press, London (2000).

- (8) Challet D., Marsili M. and Zhang Y-C. Minority Games. Interacting agents in financial markets Oxford University Press (Oxford, 2004)

- (9) Laloux L, et al., Phys. Rev. Lett. 83 1467 (1999); Plerou V, et al., Phys. Rev. Lett. 83 1471 (1999)

- (10) Plerou V, et al. Phys. Rev. E 65 066126 (2002).

- (11) Onnela JP, et al., Phys. Rev. E 68 056110 (2003)

- (12) Bonanno G., et al., Phys. Rev. E 68 046130 (2003).

- (13) Z. Eisler, et al. Europhys. Lett. 69, 664 (2005).

- (14) Mantegna RN, Eur. Phys. J. B, 11, 193 (1999).

- (15) Marsili M. Quant. Fin. 2 297 (2002)

- (16) Kwapien J, Drozdz S. and Speth J, Phys. A 330 605 (2003); G. Bonanno, F. Lillo and R. N. Mantegna, Quant. Fin. 1 96 (2001)

- (17) The persistence of the structure of correlations mantegna ; kertesz and their overlap with economic sectors gopicorr ; states suggests that it can be related to economic factors which evolve on long time scales. Financial activity is instead relevant over time scales of few days and it is responsible for the emergence of the market mode.

- (18) Data was taken form finance.yahoo.com in the time period June 1997 to May 2005 for all assets except for the Dow Jones, for which we used May 1995 to May 2005. Correlations were measured on the set of assets composing the index at the final date.

- (19) Drodz S, em et al.,Physica A 294, 226 (2001).

- (20) Elton E.J. and Gruber M.J., Modern Portfolio theory and investment analysis (J. Wiley & sons, New York, 1995).

- (21) Landau, L. D., in Collected Papers of L. D. Landau (ed. ter Haar, D.) 193-216 (Pergamon, Oxford, 1965).

- (22) should be considered as a column vector, whereas is a row vector. Hence is the scalar product and is the direct product, i.e. the matrix with entries .

- (23) A simple generalization of single asset market models Lux ; MG might also produce a complex dynamics. The emergence of a market mode is a natural consequence of ad hoc behavioral assumptions (herding). Such an approch, however, focuses on speculative trading where the dynamicsis driven by expected returns, and misses the peculiar role which risk and correlations play.

- (24) Exponential moving averages such as that used in Eqs. (4,5) are widely used in finance (see elton p. 59). Our main results are related to the behavior of the model for and clearly remain unchanged if one assumes uniform averages over a finite window (as e.g. Refs. mantegna ; kertesz ; gcalda ; states ), and then lets .

- (25) Gabaix X., et al., Nature 423 267-270 (2003) and Lillo F., Farmer J. D., Mantegna R. N., Nature 421 129-130 (2003).

- (26) Farmer, J.D. Ind. & Corp. Change 11, 895 (2002)

- (27) There are indeed two solutions for . We choose the one for which as .

- (28) Raffaelli G., Ponsot B. and Marsili M., in preparation.

- (29) R. Cont and J.-P. Bouchaud, Eur. Phys. J. B 6, 543 (1998).

- (30) Challet D. and Marsili M. Phys. Rev. E 68 (3) 036132 (2003)