Underlying Dynamics of Typical Fluctuations of an Emerging Market Price Index: The Heston Model from Minutes to Months

Abstract

We investigate the Heston model with stochastic volatility and exponential tails as a model for the typical price fluctuations of the Brazilian São Paulo Stock Exchange Index (IBOVESPA). Raw prices are first corrected for inflation and a period spanning 15 years characterized by memoryless returns is chosen for the analysis. Model parameters are estimated by observing volatility scaling and correlation properties. We show that the Heston model with at least two time scales for the volatility mean reverting dynamics satisfactorily describes price fluctuations ranging from time scales larger than 20 minutes to 160 days. At time scales shorter than 20 minutes we observe autocorrelated returns and power law tails incompatible with the Heston model. Despite major regulatory changes, hyperinflation and currency crises experienced by the Brazilian market in the period studied, the general success of the description provided may be regarded as an evidence for a general underlying dynamics of price fluctuations at intermediate mesoeconomic time scales well approximated by the Heston model. We also notice that the connection between the Heston model and Ehrenfest urn models could be exploited for bringing new insights into the microeconomic market mechanics.

keywords:

Econophysics , Stochastic volatility , Heston model , High-frequency financePACS:

02.50.-r , 89.65.-s1 Introduction

In the last decades the quantitative finance community has devoted much attention to the modeling of asset returns having as a major drive the improvement of pricing techniques [1] by employing stochastic volatility models ameanable to analytical treatment such as Hull-White [2], Stein-Stein [3] and Heston [4] models.

Despite differences in methods and emphasis, the cross fecundation between Economics and Physics, which dates back to the early nineteenth century (see [5] and [6]), has intensified recently [7]. Following the statistical physics approach, substantial effort has been made to find microeconomic models capable of reproducing a number of recurrent features of financial time series such as: returns aggregation (probability distributions at any time scale) [8, 9], volatility clustering [11], leverage effect (correlation between returns and volatilities) [12, 13], conditional correlations [14, 15] and fat tails at very short time scales [7]. A central feature of economical phenomena is the prevalence of intertwined dynamics at several time scales. In very general terms, one could divide the market dynamics onto three broad classes: the microeconomic dynamics at the time scales of books of orders and price formation, the mesoeconomic dynamics at the scales of oscillations in formed prices due to local supply and demand and the macroeconomic dynamics at the scales of aggregated economy trends.

The literature on empirical finance have emphasized the multifractal scaling [16] and the power law tails of price fluctuations. However it has been shown [17] that very large data sets are required in order to distinguish between a multifractal and power law tailed process and a stochastic volatility model. In this paper we, therefore, deal with the mesoeconomic dynamics as it would be described by the Heston model with stochastic volatility and exponential tails.

Recently, a semi-analytical solution for the Fokker-Planck equation describing the distribution of log-returns in the Heston model has been proposed [8]. The authors were able to show a satisfactory agreement between return distributions of a number of developed market stock indices and the model for time scales spanning a wide interval ranging from 1 to 100 days. More recently, the same model has also been employed to describe single stocks intraday fluctuations with relative success [10].

In this paper we show evidence that the Heston model is also capable of describing the fluctuation dynamics of an emerging market price index, the Brazilian São Paulo Stock Exchange Index (IBOVESPA). We employ for the analysis 37 years of data since IBOVESPA inception in January, 1968 and approximately four years of intraday data as well. In this period the Brazilian economy has experienced periods of political and economical unrest, of hyperinflation, of currency crises and of major regulatory changes. These distinctive characteristics make the IBOVESPA an interesting ground for general modelling and data analysis and for testing the limits of description of the Heston model.

This paper is organized as follows. The next section surveys the Heston model, its semi-analytical solution and its connection to Ehrenfest urn models. Section 3 discusses the pre-processing necessary for isolating the fluctuations to be described by the Heston model from exogenous effects. Section 4 describes the data analysis at low (from daily fluctuations) and high (intraday fluctuations) frequencies. Conclusions and further directions are presented in Section 5.

2 The Heston Model

2.1 Semi-analytical solution

The Heston Model describes the dynamics of stock prices as a geometric Brownian motion with volatility given by a Cox-Ingersoll-Ross (or Feller) mean-reverting dynamics. In the Itô differential form the model reads:

| (1) | |||||

where represents the square of the volatility and are Wiener processes with:

| (2) |

The volatility reverts towards a macroeconomic long term mean squared volatility with relaxation time given by , represents a drift at macroeconomic scales, the coefficient prevents negative volatilities and regulates the amplitude of volatility fluctuations.

As we are mainly concerned with price fluctuations, we simplify equation (1) by introducing log-returns in a window as . Using Ito’s lemma and changing variables by making we obtain a detrended version of the return dynamics that reads:

| (3) |

The solution of the Fokker-Planck equation (FP) describing the unconditional distribution of log-returns was obtained by Drgulescu and Yakovenko [8] yielding:

| (4) |

where

| (5) | |||||

| (6) | |||||

| (7) | |||||

| (8) |

This unconditional probability density has exponentially decaying tails and the following asymptotic form for short time :

| (9) |

where is the modified Bessel function of order .

2.2 Volatility autocorrelation, volatility distribution and leverage function

The volatility can be obtained by integrating (1) and is given by:

| (10) |

A simple calculation gives the stationary autocorrelation function:

| (11) |

The probability density for the volatility can be obtained as the stationary solution for a Fokker-Planck equation describing and reads:

| (12) |

implying that is required in order to have a vanishing probability density as .

The leverage function describes the correlation between returns and volatilities and is given by [13]:

| (13) |

where is given by (3), is the Heaviside step function and:

| (14) |

To simplify the numerical calculations we employ throughout this paper the zeroth order appoximation . The approximation error increases with the time lag but is not critical to our conclusions.

2.3 Relation to Ehrenfest Urn Model

The Ehrenfest Urn (EU) as a model for the market return fluctuations has been studied in [18], in this section we observe that Feller processes as (1) can be produced by a sum of squared Ornstein-Uhlenbeck processes (OU), and that OU processes can be obtained as a large urn limit for the EM.

To see how those connections take shape we start by supposing that are OU processes:

| (15) |

where describe independent Wiener processes. In this case the variable is described by a Feller process as (1) [19]. The volatility process in (1) emerges from OU processes by applying Itô’s Lemma to get:

| (16) |

Using the definition of and the properties of the Wiener processes it follows that:

| (17) |

The volatility process in (1) can be recovered with a few variable choices: , and . A dynamics with vanishing probability of return to the origin requires the volatility to be represented by a sum of at least two elementary OU processes, equivalently we should have .

An OU process can be obtained as a limit for an Ehrenfest urn model (EM). In an EM numbered balls are distributed between two urns and . At each time step a number is chosen at random and the selected ball changes urn. We can specify as the system microstate at instant , where indicates that the ball is inside urn if , we also can define the macrostate , which dynamics is described by a Markov chain over the space with transition matrix given by , and if . An imbalance in the population between the two urns generates a restitution force and, consequently, a mean reverting process for . Applying the thermodynamic limit , rescaling time to and introducing a rescaled imbalance variable as:

| (18) |

we recover an OU process:

| (19) |

Using this connection we could speculate on a possible microscopic model that would generate a stochastic dynamics as described by the Heston model. Supposing that market agents choose at each time step between two regimes (urns) that may represent different strategies, such as technical and fundamental trading or expectations on future bullish or bearish markets, imbalances between populations in each regime would be a source of volatility. In this picture, the condition would imply that at least two independent sources of volatility would be driving the market. We shall develop this connection further elsewhere.

3 Data Pre-processing

3.1 The data

Two data sets have been used: IB1 consisting of daily data from IBOVESPA inception on January, 1968 to January, 2005 and IB2 consisting of high-frequency data sampled at 30 second intervals from March 3, 2001 to October 25, 2002 and from June 6, 2003 to August 18, 2004.

3.2 Inplits and Inflation

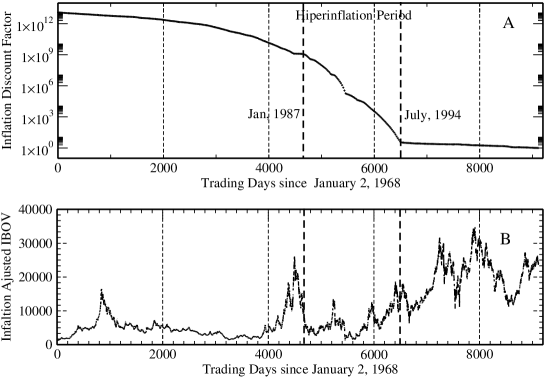

The dataset IB1 has been adjusted for eleven divisions by 10 (inplits) introduced in the period for disclosure purposes [20] and also for inflation by the General Price Index (IGP) [21]. In figure 1A we show the discount factor from date to current date , , used for correcting past prices as . Figure 1B shows the resulting inflation adjusted prices. The hiperinflation (average of per month) period from January 1987 to July 1994 is also indicated in both figures by dashed lines.

3.3 Detrending

For our analysis of price fluctuations it would be highly desirable to identify macroeconomic trends that may be present in the data. A popular detrending technique is the Hodrick-Prescott (HP) filtering [22] which is based on decomposing the dynamics into a permanent component, or trend , and into a stochastic stationary component as by fitting a smooth function to the data. Any meaningful detrending procedure has to conserve statistical properties that define the fluctuations. However, in our experiments we have noticed that the HP filtering may introduce subdiffusive behavior at long time scales as an artifact when applied on first differences of a random walk. In this paper, in the absence of a reliable detrending procedure, we assume that the major long term trend is represented by inflation.

3.4 Autocorrelation of Returns

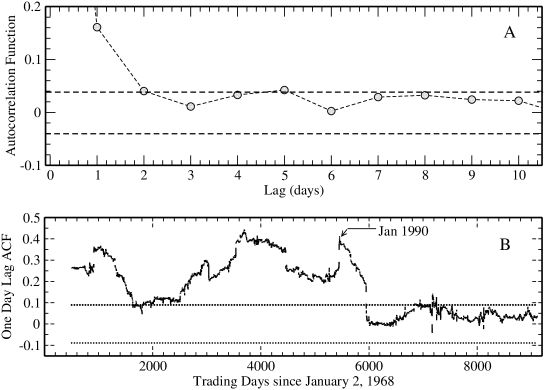

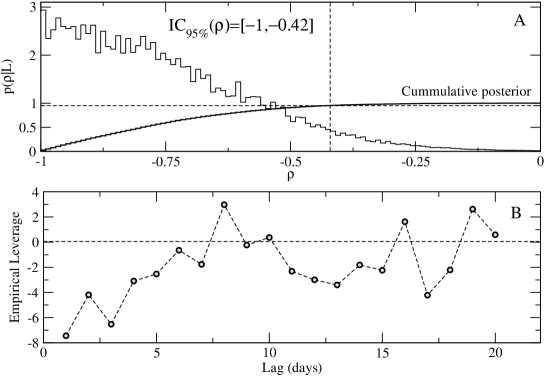

In the period span by data set IB1 the Brazilian economy (see [23] for a brief historical account) has experienced a number of regulatory changes with consequences for price fluctuations. In [23] it has been observed that the Hurst exponent for daily IBOVESPA returns shows an abrupt transition from an average compatible with long memory () to a random walk behavior () that coincides with major regulatory changes (known as the Collor Plan). We have confirmed the presence of memory by measuring the autocorrelation function for the entire time series (figure 2A). We have also measured the historical autocorrelation for one day lags using a 250 days moving window and confirm an abrupt behavior change coinciding with the Collor Plan in 1990 (figure 2B). As the Heston model assumes uncorrelated returns and this feature only became realistic after the Collor Plan, the following analysis is restricted to a data set consisting of daily data from January 1990 to January 2005 (IB3).

3.5 Extreme Events and Abnormal Runs

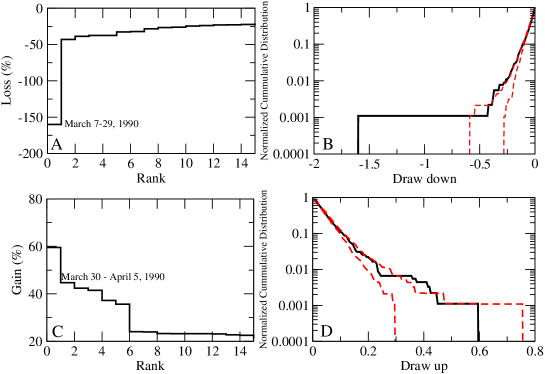

Abnormal runs are sequences of returns of the same sign that are incompatible with the hypotheses of uncorrelated daily returns. We follow [24] and calculate for the data set IB3 the statistics of persistent price decrease (drawdowns) or increase (drawups). We then compare empirical distributions of runs with shuffled versions of IB3. In figure 3B we show that a seventeen business days drawdown from March 7, 1990 to March 29,1990 is statistically incompatible, within a confidence interval, with equally distributed uncorrelated time series. Observe that the largest drawup shown in figure 3C correponds to the subsequent period from March 30, 1990 to April 5, 1990 and that the Collor Plan was launched in March 1990. We therefore expunged from data set IB3 abnormally correlated runs that took place in March, 1990.

4 Data Analysis

4.1 Low Frequency

After deflating prices and expunging autocorrelated returns, four independent parameters have to be fit to the data: the long term mean volatility , the relaxation time for mean reversion , the amplitude of volatility fluctuations and the correlation between price and volatility . It has become apparent in [9] that a direct least squares fit to the probability density (4) yields parameters that are not uniquely defined. The data analysis adopted in this work consists in looking for statistics predicted by the model that can be easily measured and compared. In the following subsections we describe these statistics.

4.1.1 Long term mean volatility

A straightforward calculation yields the second cummulant of the probability density (4) as:

where

| (21) |

As we drop terms of or superior. A non-biased estimate for the above cummulant can be calculated easily from data using:

| (22) |

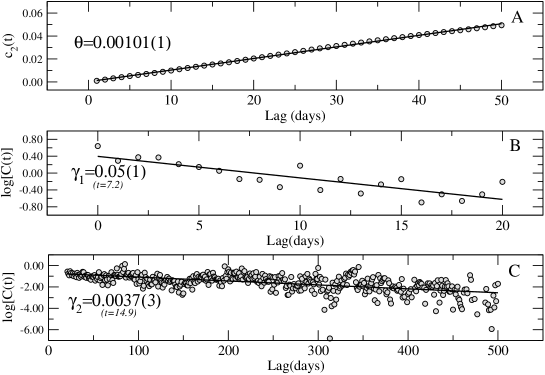

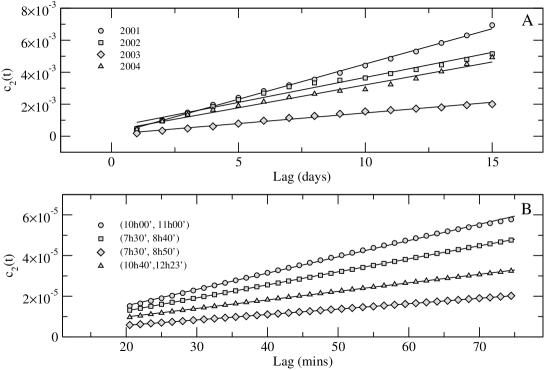

where stands for -days detrended log-returns. The long term mean volatility is estimated by a linear regression over the function as shown in figure 4A.

4.1.2 Relaxation time for mean reversion

The relaxation time is also estimated by a linear regression over the logarithm of the empirical daily volatility autocorrelation function (11) given by:

| (23) |

We observe in figure 4B and 4C that IB3 data can be fit to two relaxation times: at we fit days and at we fit days.

The second relaxation time can be introduced into the original Heston model by making the long-term volatility fluctuate as a mean reverting process like:

| (24) |

where is an additional independent Wiener process. The autocorrelation function for the two time scales model acquires the following form [25]:

| (25) |

with , where stands for the average of given .

The autocorrelation function fit in figure 4C indicates that relaxation times are of very different magnitudes and that it may be possible to solve the Fokker-Planck equation for such model approximately by adiabatic elimination. We pursue this direction further elsewhere. It is worth mentioning that another tractable alternative for introducing multiple time scales for the volatility is a superposition of OU processes as described in [26].

4.1.3 Amplitude of volatility fluctuations

From (5) the amplitude of volatility fluctuations is given by:

| (26) |

The long term volatility and the relaxation time have been estimated in the previous sections. As discussed in section 2.3, the constant is related to the number of independent OU processes composing the stochastic volatility process as . To avoid negative volatilities, is required. We, therefore, assume and calculate the amplitude of volatility fluctuations from (26) yielding .

4.1.4 Correlation between prices and volatilities

A nonzero correlation between prices and volatilities in (2.1) leads to an asymmetric probability density of returns described by (4). This asymmetry can be estimated either by directly computing the empirical distribution skewness or by calculating the empirical leverage function (13). Both procedures imply in computing highly noisy estimates for third and fourth order moments. In this section we propose estimating a confidence interval for by computing the posterior probability , where corresponds to a data set containing the empirically measured leverage function for a given number of time lags. Bayes theorem [27] gives the following posterior distribution:

| (27) |

where is a data dependent normalization constant. We assume ignorance on the parameter and fix its prior distribution to be uniform over the interval , so that . The maximum entropy prior distributions , and for the remaining parameters are gaussians, since their mean and variance have been previously estimated. The model likelihood for time lags is approximately given by:

where the first term inside the exponencial represents the empirical leverage function with being the daily returns in the data set IB3. We choose to be uniform representing our level of ignorance on the acceptable dispersion of deviations between data and model. Having specified ignorance priors and the likelihood (4.1.4), we evaluate the posterior (27) by Monte Carlo sampling. In figure 5 we show the resulting posterior probability density and find the confidence interval to be , what is strong evidence for an asymmetric probability density of returns.

4.1.5 Probability density of returns

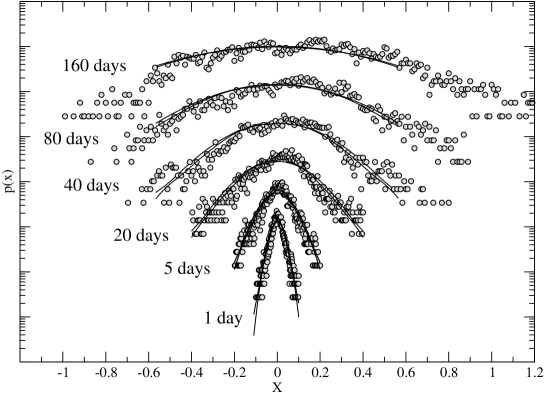

Confidence intervals for the probability density of returns can be obtained by Monte Carlo sampling a sufficiently large number of parameter sets with appropriate distributions and numerically integrating (4) for each set. Distribution features for each of the relevant parameters are summarized in the following table:

| Parameter | Mean | Standard Deviation |

|---|---|---|

| distributed as in fig. 5. | ||

| fixed by theoretical arguments. |

We have independently sampled gaussian distributions on the parameters ,, and a uniform distribution for the parameter . In figure 6 we compare empirical probability densities with theoretical confidence intervals at finding a clear agreement at time scales ranging from 1 to 160 days.

4.2 High Frequency

4.2.1 Autocorrelation of intraday returns

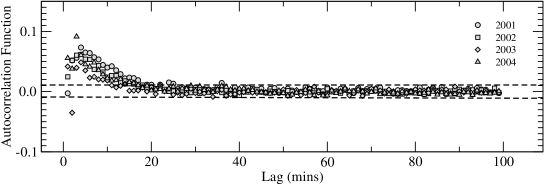

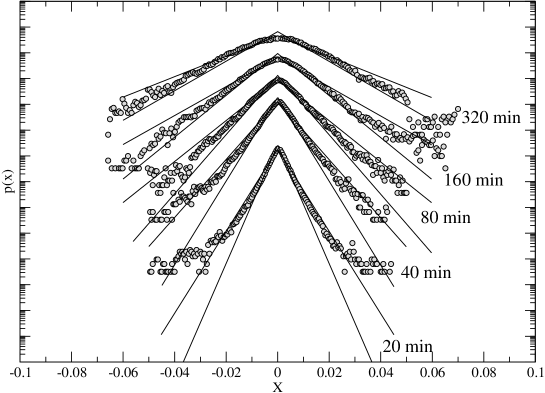

Our main aim is to describe the fluctuation dynamics at intermediate time scales of formed prices (mesosconomic time scales) by a model which assumes uncorrelated returns. The price formation process occurs at time scales from seconds to a few minutes where the placing of new orders and double auction processes take place. We propose to fix the shortest mesoeconomic time scale to be the point where the intraday autocorrelation function vanishes. In figure 7 we show that the intraday return autocorrelation function vanishes at about 20 minutes for each of the 4 years composing data set IB2. We, therefore, consider as mesoeconomic time scales over 20 minutes.

4.2.2 Effective duration of a day

At first glance, it is not clear whether intraday and daily returns can be described by the same stochastic dynamics. Even less clear is whether aggregation from intraday to daily returns can be described by the same parameters. To verify this latter possibility we have to transform units by determining the effective duration in minutes of a business day . This effective duration must include the daily trading time at the São Paulo Stock Exchange and the impact of daily and overnight gaps over the diffusion process. The São Paulo Stock exchange opens daily for electronic trading from 10 a.m. to 5 p.m. local time and from 5:45 p.m. to 7 p.m. for after-market trading, totalizing 8h15min of trading daily.

To estimate in minutes we observe that the daily return variance is the result of the aggregation of 20 minute returns, so that, considering a diffusive process, we would have:

| (29) |

It has been already observed that the volatility fluctuation dynamics are mean reverting with at least two time scales days and year. Considering the longest relaxation time we estimate by estimating the mean daily volatility for each one of the years in IB2. In figure 8A we show linear regressions employed for estimating the mean daily variance for each year in IB2 following the procedure described in section 4.1.1.. In figure 8B we show linear regressions employed to estimate , the effective duration confidence intervals are obtained from (29). The mean confidence interval over the 4 years analysed results in 9h10min, 9h56min what is consistent with 8h15min of daily trading time plus an effective contribution of daily and overnight gaps.

4.2.3 Probability density of intraday returns

For evaluating the probability density of intraday returns we have reestimated the mean volatility and the amplitude of volatility fluctuations along the period 2001-2004 represented in the data set IB2. We then have rescaled the dimensional parameters as , and . Having rescaled the distributions describing our ignorance on the appropriate returns we have employed Monte Carlo sampling to compute confidence intervals for the short time lags appoximation of the theoretical probability density described in (9). In figure 9 we compare the resulting confidence intervals and the data. We attain reasonably good fits for the longer time scales, as we approach the microeconomic time scales the theoretical description of the tails breaks with the empirical data showing fatter tails.

5 Conclusions and Perspectives

We have studied the Heston model with stochastic volatility and exponential tails as a model for the typical price fluctuations of the Brazilian São Paulo Stock Exchange Index (IBOVESPA). Prices have been corrected for inflation and a period spanning the last 15 years, characterized by memoryless returns, have been chosen for the analysis. We also have expunged from data a drawdown inconsistent with the supposition of independence made by the Heston model that took place in the transition between the first 22 years of long memory returns to the memoryless time series we have analysed.

The long term mean volatility has been estimated by observing the time scaling of the log-returns variance. The relaxation time for mean reversion has been estimated by observing the autocorrelation function of the log returns variance. We have verified that a modified version of the Heston model with two very different relaxation times ( days and year) is required for describing the autocorrelation function correctly. We have used the minimum requirement for a non-vanishing volatility to calculate the scale of the variance fluctuation . Finally, we employed the Bayesian statistics approach for estimating a confidence interval for the volatility-return correlation , as it relies on a small data set to calculate a noisy estimate of higher order moments. The quality of the model is visually inspected by comparing the empirical probability density at time scales ranging from 1 day to 160 days, with confidence intervals obtained by a Monte Carlo simulation over the maximum ignorance parameter distributions. We have also shown that the probability density functions of log returns at intraday time scales can be described by the Heston model with the same parameters given that we introduce an effective duration for a business day that includes the effect of overnight jumps and that we consider the slow change of the volatility due to the longer relaxation time .

It is surprising and non-trivial that a single stochastic model may be capable of describing the statistical behavior of both developed and emerging markets at a wide range of time scales, despite the known instability and high susceptibility to externalities of the latter. We believe that this robust statistical behavior may point towards simple basic mechanisms acting in the market microstructure. We regard as an interesting research direction to pursue the derivation of the Heston model as a limit case for a microeconomic model like the minority game [28]. For this matter we believe that the connection between the Heston model and Ehrenfest urns may be valuable.

Perhaps the search for underlying symmetries and simple basic mechanisms that can explain empirical observations should be regarded as the main contribution of Physics to Economics. This contribution might be particularly useful to the field of Econometrics in which a common view is that a theory built from data ‘should be evaluated in terms of the quality of the decisions that are made based on the theory’ [29]. Clearly, these two approaches should not be considered as mutually exclusive.

References

- [1] J.P. Fouque, G. Papanicolaou, K.R. Sircar, Derivatives in Financial Markets with Stochastic Volatility, Cambridge University Press, Cambridge, 2000.

- [2] J. Hull, A. White, Journal of Finance 42 (1987) 281.

- [3] E.M. Stein, J.C. Stein, Review of Financial Studies 4 (1991) 727.

- [4] S.L. Heston, Review of Financial Studies 6 (1993) 327.

- [5] B.M. Roehner, Patterns of Speculation, Cambridge University Press, Cambridge, 2002.

- [6] P. Mirowski, More Heat Than Light, Cambridge University Press, Cambrigde, 1989.

- [7] R.N. Mantegna, H.E. Stanley, An Introduction to Econophysics, Cambridge University Press, Cambridge, 2000.

- [8] A.A.Drgulescu, V.M. Yakovenko, Quantitative Finance 2 (2002) 443.

- [9] A.C. Silva, V.M. Yakovenko, Physica A 324 (2003) 303.

- [10] A.C. Silva, R.E. Prange, V.M. Yakovenko, Physica A 344 (2004) 227.

- [11] R.F. Engle, A.J. Patton, Quantitative Finance 1 (2001) 237.

- [12] J.-P. Bouchaud, A. Matacz, M. Potters, Physical Review Letters 87 (2001) 228701-1.

- [13] J. Perelló, J. Masoliver, Physical Review E 67 (2003) 037102.

- [14] M. Boguñá, J. Masoliver, Preprint cond-mat/0310217 (2003).

- [15] B. LeBaron, Journal of Applied Econometrics, 7 (1992) S137.

- [16] T. Di Matteo, T. Aste, M.M. Dacorogna, Journal of Banking and Finance, 29 (2005) 827.

- [17] B. LeBaron, Quantitative Finance, 1 (2001) 621.

- [18] H. Takahashi, Physica D 189 (2004) 61.

- [19] S. Shreve, Lectures on Stochastic Calculus and Finance.

- [20] BOVESPA Index, http://www.bovespa.com.br.

- [21] Fundação Getúlio Vargas, http://www.fgvdados.fgv.br/.

- [22] A.C. Harvey, A. Jaeger, Journal of Applied Econometrics 8 (1993) 231.

- [23] R.L. Costa, G.L. Vasconcelos, Physica A 329 (2003) 231.

- [24] A. Johansen, D. Sornette, European Physical Journal B 1 (1999) 141.

- [25] J. Perelló, J. Masoliver, J.-P. Bouchaud, Applied Mathematical Finance 11 (2004) 27.

- [26] O. E. Barndorff-Nielsen, N. Shephard, J. Royal Statistical Society 63(2) (2001) 167.

- [27] D.S. Sivia, Data Analysis: A Bayesian Tutorial, Oxford Univerisity Press, Oxford, 2000.

- [28] D. Challet, M. Marsilli, Y.-C. Zhang, Minority Games, First Edition, Oxford University Press (2004).

- [29] C.W.J. Granger, Empirical Modelling in Economics, First Edition, Cambridge University Press (1999).