Economics: the next physical science?

Abstract

We review an emerging body of work by physicists addressing questions of economic organization and function. We suggest that, beyond simply employing models familiar from physics to economic observables, remarkable regularities in economic data may suggest parts of social order that can usefully be incorporated into, and in turn can broaden, the conceptual structure of physics.

I Physics and economics

In the last decade or so physicists have begun to do academic research in economics in a newly emerging field often called “econophysics”. Perhaps a hundred people are now actively involved, with two new journals111The new journals are The International Journal of Pure and Applied Finance and Quantitative Finance. Quantitative Finance was started by the Institute of Physics and later sold to a commercial firm. and frequent conferences. At least ten books have been written on econophysics in general or specific subtopics (We are restricted by citation limits here, but an extensive bibliography of the books and archived articles is maintained on the econophysics website, http://www.unifr.ch/econophysics). Ph.D. theses are being granted by physics departments for research in economics, and in Europe there are several professors in physics departments specializing in econophysics. There is even a new annual research prize, titled the “Young Scientist Award for Social and Econophysics”. Is this just a fad, or is there something more substantial here?

If physicists want to do research in economics, why don’t they just get degrees in economics in the first place? Why don’t the econophysicists retool, find jobs in economics departments and publish in traditional economics journals? Perhaps this is just a temporary phenomenon, driven by a generation of physicists who made a bad career choice. Is there any reason why research in economics should be done in physics departments as an on-going activity, or why economics departments should pay heed to the methods of physics? What advantage, if any, is conferred by a background in physics? And most important, how does econophysics differ from economics, and what unique contribution can it make, if any?

One is naturally suspicious that the emergence of econophysics is just a reflection of a depressed job market. It is certainly true that during the last two decades a large number of physicists have been lured to Wall St, and that this has been an important stimulus. But this is not the main focus. Econophysics is primarily an academic endeavor, whose participants are employed by universities. It offers no special advantages in the job market – in fact, quite the opposite: It is even more competitive than mainstream fields of physics. No permanent positions in econophysics have ever been offered in an American university. Papers submitted to Physical Review Letters require special justification concerning their relevance to physics. While the situation in Europe is a little better than in the U. S., jobs are still very scarce. The tenuous existence of econophysics relies on senior professors who have redirected their interests from other areas, as well as a few bold students and postdocs.

The involvement of physicists in social science has a long history, going back at least to Daniel Bernoulli, who in 1738 introduced the idea of utility to describe people’s preferences. In his Essai philosophique sur les probabilites (1812), Laplace pointed out that events that might seem random and unpredictable, such as the number of letters that end up in the Paris dead-letter office, can in fact be quite predictable and can be shown to obey simple laws. These ideas were further amplified by Quetelet, a student of Fourier, who in 1835 coined the term “social physics”, and studied the existence of patterns in data sets ranging from the frequency of different methods for committing murder to the chest size of Scottish men. Analogies to physics played an important role in the development of economic theory through the nineteenth century, and some of the founders of neoclassical economic theory222“Neoclassical economics” refers to a representation of individual decision making in terms of scalar “utility” functions, whose gradients are imagined to be like forces directing people to trade, and from which economic equilibria arise as a kind of “force balance” among different people’s trading wishes. From the economist’s point of view neoclassical economics clarified and extended the work of the classical economists, Smith, Mill, Ricardo and others by formalizing the notions of competition, marginal utility and rent, as well as producing separate theories of the firm and consumer.” , such as Irving Fisher, a student of Willard Gibbs, were originally trained as physicists. Ettore Majorana in 1938 presciently outlined both the opportunities and pitfalls in applying statistical physics methods to the social sciences.

The range of topics that have been addressed spans many different areas of economics. Finance is particularly well represented; sample topics include the empirical observation of regularities in market data, the dynamics of price formation, the understanding of bubbles and panics, methods for pricing derivatives such as options, the construction of optimal portfolios, and many other subjects. Broader topics in economics include the distribution of income, theories of how money emerges, and implications of symmetry and scaling to the functioning of markets.

Despite their long history of association, we see the substantial contributions of physics to economics as still in an early stage, and find it fanciful to forecast what will ultimately be accomplished. Almost certainly, “physical” aspects of theories of social order will not simply recapitulate existing theories in physics, though already there appear to be overlaps. The development of societies and economies is potentially contingent on accidents of history, and at every turn hinges on complex aspects of human behavior. Nonetheless, striking empirical regularities such as those we survey below suggest that at least some social order is not historically contingent, and perhaps is predictable from first principles. The role of markets as mediators of communication and distributed computation, and the emergence of the social institutions that support them, are quintessentially economic phenomena. Yet the notions of their computational or communication capacity, and how these account for their stability and historical succession, may naturally be parts of the physical world as it includes human social dynamics. In the context of human desires, markets and other economic institutions bring with them notions of efficiency or optimality in satisfying those desires. While intuitively appealing, such notions have proven hard to formalize, and the examples below show some progress in this area. As with most new areas of physical inquiry, we expect that the ultimate goals of a “physical economics” will be declared with hindsight, from successes in identifying, measuring, modeling and in some cases predicting empirical regularities.

II Data analysis and the search for empirical regularities

Economists are typically better trained in statistical analysis than physicists, so this might seem to be an area where physicists have little to contribute. However, differences in goals and philosophy are important. Physics is driven by the quest for universal laws. In part, because of the extreme complexity of phenomena in society, in the postmodern world where relativist philosophies of science enjoy disturbingly widespread acceptance, this quest has been largely abandoned. Modern work in social science is largely focused on documenting differences. Although this trend is much less obvious in economics, a typical paper in financial economics, for example, might study the difference between the NYSE and the NASDAQ stock exchanges, or the effect of changing the tick size of prices (the unit of the smallest possible price change). Physicists have (perhaps naively) entered with fresh eyes and new hypotheses, and have looked at economic data with the goal of finding pervasive regularities, emphasizing what might be common to all markets rather than what might make them different. This work has been opportunistically motivated by the the existence of large data sets such as the complete transaction histories of major exchanges over timespans of years, which in some cases contain hundreds of millions of events.

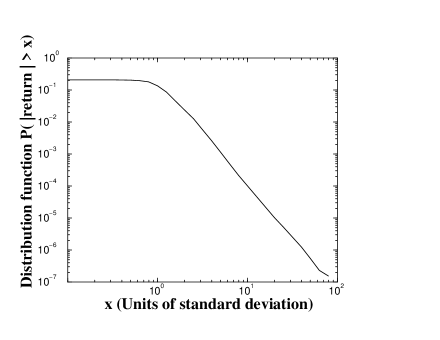

Much of the work by physicists in economics concerns power laws. A power law is an asymptotic relation of the form , where is a variable and is a constant. In many important cases is a probability distribution. Power laws have received considerable attention in physics because they indicate scale free behavior and they are characteristic of critical or nonequilibrium phenomena. In fact, the first power law distribution (in any field) was observed in economics (see Box A), and the existence of power laws in economics has been a matter of debate ever since. In 1963 Benoit Mandelbrot Mandelbrot97 observed that the distribution of cotton price fluctuations follows a power law. Further observations of power laws in price changes were subsequently noted by Rosario Mantegna and Eugene Stanley Mantegna99 , who coined the term “econophysics”. Fig. 1 shows the striking fidelity often found in economic power laws. The existence of power laws in price changes is interesting from a practical point of view because of its implications for the risk of financial investments, and from a theoretical point of view because it suggests scale independence and possible analogies to nonequilibrium behavior in the processes that generate financial returns.

Since then many other power laws have been discovered by physicists. These include the variance in the growth rates of companies as a function of their size Amaral97 , the distribution function for the number of shares in a transaction, the distribution for the number of trading orders submitted at a price away from the best price offered, the size of the price response to a trade as a function of the size of the company being traded, and many other examples. The question of why power laws are so ubiquitous in financial markets has stimulated a great deal of theoretical work.

One of the most famous and most used models of prices is the random walk. The random walk was originally introduced for prices in 1900 by Louis Bachelier, a student of Poincaré, five years before Einstein introduced it to describe Brownian motion. This forms the basis for the Black-Scholes theory of option pricing Bouchaud00 , which won a Nobel prize in economics in 1997 (see Box B). One of the interesting and surprising properties of the random walk of real prices is that its diffusion rate is not constant. The size of price changes is strongly positively autocorrelated in time, a phenomenon called clustered volatility333The autocorrelation function of a time series is defined as , where , denotes a time average and the standard deviation. “Volatility” is the term used in finance to refer to the variance or size of price shifts.. The autocorrelation of the size of price changes decays as a power law of the form . Since , this is a long-memory process. Long-memory processes display anomalous diffusion and very slow convergence of statistical averages.

Physicists have recently discovered that volatility is just one of several long-memory-processes in markets. One of the most surprising concerns fluctuations in supply and demand Bouchaud04 . If one assigns to an order to buy and to an order to sell, the resulting series of numbers has a positive autocorrelation function that decays as a power law with an exponent , which persists at statistically significant levels across tens of thousands of orders, for periods of time lasting for weeks. This implies that changes in supply and demand obey a long-memory process. This has interesting implications.

One of the most fundamental principles in financial economics is called market efficiency. This principle takes many forms: A market is informationally efficient if prices reflect all available information; it is arbitrage efficient if it is impossible for investors to make “excess profits”, and it is allocationally efficient if prices are set so that they in some sense maximize everyone’s welfare. One of the consequences of informational efficiency is that prices should not be predictable. In reality this is not a bad approximation; even the best trading strategies exploit only very weak levels of predictability.

The coexistence of the long-memory of supply and demand with market efficiency creates an interesting and as yet unresolved puzzle. Long-memory processes are highly predictable using a simple linear algorithm. Since the entrance of new buyers tends to drive the price up, and the entrance of new sellers tends to drive it down, this naively suggests that price changes should also be long-memory, which would violate market efficiency. To prevent this from happening, the agents in the market must somehow collectively adjust their behavior to offset this, for example by creating an asymmetric response of prices, so that when there is an excess of new buyers the price response to new buy orders is smaller than it is to new sell orders. How this comes about, and why it comes about, remains a mystery. This may be related to the cause of clustered volatility.

There is a great deal of other empirical work using methods and analogies from physics that we do not have the space to describe in any detail. For example, random matrix theory Burda (developed in nuclear physics) and the use of ultrametric correlations have proved useful for understanding the correlation between the movement of prices of different companies. An analogy to the Omori law for seismic activity after major earthquakes has proved to be useful for understanding the aftermath of large crashes in stock markets, and other analogies from geophysics has led to a controversial hypothesis about why markets crash Sornette02 . The statistics of price movements have been noted to bear a striking resemblance to those of turbulent fluids, which has led to what may now be the best empirical models available for predicting clustered volatility. Such examples speak to the universality of mathematics in its applications to the world.

III Modeling the behavior of agents

The most fundamental difference between a physical system and an economy is that economies are inhabited by people, who have strategic interactions. Because people think, plan, and make decisions based on their plans, they are much more complicated to understand than atoms. This is a problem that physics has never coped with, and it has caused the mathematical techniques and modeling philosophy in economics to diverge from those in physics. While this is clearly necessary, many physicists would argue that the gap is wider than it should be.

The central approach to the problem of strategic interactions in neoclassical economics is the theory of rational choice. The economists’ stylized version of individual rationality is to maximize some measure of one’s personal (usually material) welfare, having perfect knowledge of the world and of other agents’ goals and abilities, and the ability to perform computations of any complexity. When agent A considers any strategy, agent B knows that A is considering that strategy, and A knows that B knows that A knows, and so on. This infinite regress appears very complicated. However, a key simplifying result is that in any game there exists at least one Nash equilibrium, which is a set of strategies with the property that each is the optimal response to all of the others.

The Nash equilibrium is a fixed point in the space of strategies, which circumvents the infinite regress problem by imposing self-consistency as a defining criterion. Subject to several caveats, rational players who are not cooperating with each other will choose a Nash strategy. This is the operational meaning of rational choice. The assumption that decisions of real human beings can be approximated in this way dominated economic thinking about individual choices (called microeconomics) from 1950 until the mid-1980s, though it is clearly implausible for all but the simplest cognitive tasks. It also leaves unaddressed the problem of aggregation of individual choices and the behavior of large populations (called macroeconomics).

IV The quest for simple models of non-rational choice

In the last twenty years economics has begun to challenge the assumptions of rational choice and perfect markets by modeling imperfections such as asymmetric information, incomplete market structure, and bounded rationality. Several new schools of thought have emerged. The behavioral economists attempt to take human psychology into account by studying people’s actual choices in idealized economic settings. Another school uses idealizations of problem solving and learning ranging from standard statistical methods to artificial intelligence to address the problem of bounded rationality. Agent-based modeling makes computer simulations based on idealizations of human behaviors and focuses on the complexity of economic interactions. Yet another approach assumes that some agents (called noise traders) have extremely limited reasoning capabilities while others are perfectly rational. Physicists have joined with many economists in seeking new theories of non-fully-rational choice, bringing new perspectives to bear on the problem.

An early effort using both agent based modeling and artificial intelligence is called the Santa Fe Stock Market. This grew out of a conference in 1986 organized by Ken Arrow, Phil Anderson and David Pines Anderson88 that brought together physicists and economists. Presaging the modern move toward behavioral economics, the physicists all expressed disbelief in theories of rational choice and suggested that the economists should take human psychology and learning more into account. The Santa Fe Stock Market was a collaboration between economists, physicists and a computer scientist that grew out of this conference. It replaced the rational agents in an idealized market setting with an artificial intelligence model Arthur97 . It showed that this leads to qualitative modifications of the statistics of prices, such as fat tailed distributions of price change and clustered volatility, and suggested that non-rational behavior plays an important part in generating these phenomena.

The problem with this approach is that it is complicated, and while it captures some qualitative features of markets, the path to more quantitative theories is not clear. Agent based models tend to require ad hoc assumptions that are difficult to validate. The hypothesis of rational choice, in contrast, has the great virtue that it is parsimonious, making strong predictions from simple hypotheses. From this point of view it is more like theories in physics. This perspective has inspired the search for other simple parsimonious alternatives. One such approach is often called zero intelligence. This amounts to the assumption that agents behave more or less randomly, subject to constraints such as their budget. Zero intelligence models can be used to study the properties of market institutions, and to determine which properties of a market depend on intentionality and which don’t. This provides a benchmark to avoid getting lost in the large space of realistic human behaviors. Once a zero intelligence model has be made, it can be modified by incorporating more realistic assumptions, adding a little intelligence based on empirical observations or models of learning. Where rational choice enters the wilderness of bounded rationality from the top, zero intelligence enters it from the bottom.

The zero intelligence approach can be traced back to the work of Herbert Simon, a Nobel laureate in economics and pioneer in artificial intelligence. Its main champions in recent years have been physicists, who have used analogies to statistical mechanics to develop new models of markets. A good example is the work of Per Bak, Maya Paczuski, and Martin Shubik (two physicists and an economist), who studied the impact of random trading orders on prices within an idealized model of price formation. They assumed that traders simply place orders to buy or sell at random above or below the prices of the most recent transactions. They then modify their orders from time to time, moving them toward the middle until they generate a transaction. The result is mathematically analogous to a reaction diffusion model for the reaction that was developed by the physicist John Cardy. While this model is highly unrealistic, with a few modifications it produces some qualitative features, such as heavy tailed price distributions, that resemble their counterparts in real markets.

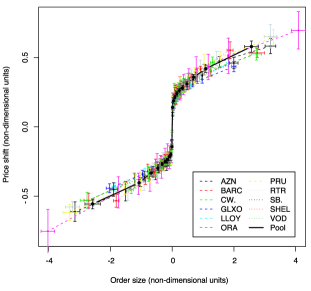

Many variations of the BPS model have now been explored. One variation simply assumes that agents place and cancel trading orders at random. After performing a dimensional analysis based on prices, shares and time, the resulting model can be shown to obey simple scaling laws that relate statistical properties of trading order placement to statistical properties of prices. These laws are restrictions on state variables similar to the ideal gas law, but in this case the variables on one side are properties of trading orders, such as the rates for order placement and cancellation, and the variables on the other side are statistical properties of prices, such as the diffusion rate in Bachelier’s random walk model. These scaling laws have been tested on data from the London Stock Exchange and have been shown to be in surprisingly good agreement with it Farmer05 . The model also gives insight into the shape of supply and demand curves, as shown in Fig 2.

V The El Farol bar problem and the minority game

Another alternative approach is to develop highly simplified models of strategic interaction that do a better job of capturing the essence of the collective behavior in a financial market. Brian Arthur’s El Farol bar problem provides an alternative to conventional game theory. The name El Farol comes from a bar in Santa Fe that is often crowded. Each day agents decide whether or not to go hear music; if there is room in the bar they are happy, and if it is too crowded they are disappointed. By definition only a minority of the people can be happy, which leads to a phenomenon analogous to frustration - some desires are necessarily unsatisfiable and as a result an astronomically large number of equilibria can emerge. The El Farol model was simplified and abstracted by Challet and Zhang as the minority game Challet05 , in which an odd number of agents repeatedly choose between two alternatives, which can be labeled or . Their decisions are made independently and simultaneously. Agents whose choice is the minority value are rewarded (awarded “payoffs”, in game-theoretic terminology). Typically agents are capable of remembering the outcomes of prior rounds of play, and maintain an inventory of strategies (random lookup tables) dictating a next move for each history. For example, for a possible lookup table would be , , , , meaning in the first case, “If the previous majority choices were in both previous rounds of the game, choose on the next round”. The strategy chosen is that with the best cumulative performance.

Minority games exhibit phase transitions for , in the ratio , of the number of resolvable pasts to the number of agents, as shown in Fig. 3.

For a critical value, the population is in a symmetric phase, where the outcome of the next move is unpredictable from the history of play. For , in contrast, agents sparsely sample the space of strategies, the next outcome is predictable, and the population is in a symmetry-broken phase that can be understood analytically with replica methods. The variance in the number of winners about the optimum, , measures the failure of “allocative efficiency”, and is minimized at .

The minority game is readily extended to incorporate more features of real financial markets, such as payoffs that increase as the size of the winning group gets smaller (much as buyers or sellers of stocks can reap larger profits when they are providing the more scarce of supply or demand), or the “grand canonical” version in which players are permitted to enter and leave. With these enhancements the game self-organizes around the critical point , the payoff series exhibits fluctuations that display clustered volatility, and they have a distribution with a power law tail, reminiscent of a real market. The minority game provides a fascinating example of how a very simple game can display a rich set of properties as soon as one moves away from the rational choice paradigm.

VI Entropy methods

Finance is not the only area of economics where physicists are active. In economics as in physics it is traditional to distinguish open from closed systems, which give rise to different notions of equilibrium. Markets considered merely as conduits for goods produced or consumed elsewhere are described with theories of “partial equilibrium”, largely specified by open-system boundary conditions. Financial markets are open in this sense. Economists also try to determine the “general equilibria” of whole societies, taking into account not only trade, but production, consumption, and to some extent regulation by government.

The understanding of relaxation to equilibrium, including when equilibria are possible and whether they are unique, has grown in economics and in physics together. In both fields mechanical models were used first, followed by statistical explanations Mirowski89 . Some recent work SmithFoley has shown which subset of economic decision problems have an identical structure to that of classical thermodynamics, including the emergence of a phenomenological principle equivalent to entropy maximization, while the more general equilibration problems usually considered by economists correspond to physical problems with many equilibria, such as granular, glassy, or hysteretic relaxation. The idea that equilibria correspond to statistically most-probable sets of configurations has led to attempts to define price formation in statistical terms. A related observation, that income distribution seems consistent with various forms of entropy maximization, recasts the problem of understanding income inequality, and interpreting how much it really tells about the social forces affecting incomes (see box A).

We expect that maximum-ignorance principles will grow into a conceptual foundation in economics as they have in physics, and that with this change, the roles of symmetry, conservation laws, and scaling will become increasingly important Shubik_Smith . Efforts to explain which aspects of market function or regulatory structure converge on predictable forms, relatively free of historical contingency, are likely to require characterization in these more basic terms.

VII Future directions

Within the next few years we expect that in some physics and economics departments a basic course teaching the essential elements of both physics and economics will be designed (much as in biophysics; see Physics Today March 2005). We believe physics will continue to contribute to economics in a variety of different directions, ranging from macroeconomics to market microstructure, and that such work will have increasing implications for economic policy making.

One area of opportunity, where the applicability of physics might not be at all obvious a priori, concerns the construction of economic indices, such as the Consumer Price Index or the Dow Jones Industrial Average. Though these indices provide only crude one dimensional summaries of very complex phenomena, they play an important role in economic decision making. For example, pension and wage payments are referenced to the CPI. Such indices are currently constructed using essentially ad hoc methods. We believe that the accuracy of such indices could be improved by careful thinking in terms of dimensional analysis, combined with better data analysis correlating prices and other factors to the phenomena, such as wages and pensions, for which the indices are designed. This is ultimately related to the question of why the economy exhibits so many scale free behaviors, such as the distribution of wealth or the size of firms. To shed light on this we need a better understanding of the natural dimensions of economic life, and the use of systematic dimensional analysis is likely to be very useful in revealing this. Dimensional and scaling methods were a cornerstone in the understanding of complex phenomena like turbulence in fluids, and all the constituents that make fluid flow complex – long time correlations, nonlinearity, and chaos – are likely to be even greater factors in the economy.

At the other end of the spectrum, ideas from statistical mechanics could make practical contributions to problems in market microstructure. For market design, for example, some physics-style models suggest that changing the rules to create incentives for patient trading orders vs. those that demand immediate transactions could lower the volatility of prices. A related practical problem concerns the optimal strategy for market makers, i.e. agents that simultaneously buy and sell, and make a profit by taking the difference. Though markets are increasingly electronic, the design of automated market makers is still done in a more or less ad hoc manner. The opportunity is ripe to create a theory for market making based on methods from statistical mechanics. This could result in lowering transaction costs and generally making markets more efficient.

We are reminded that several key ideas in physics are actually of economic origin. A prejudice that the books should balance was likely responsible for Joule’s accounting for the energy content of heat before it was well-supported by data. The concept of a “currency”, which we still think of primarily in economic metaphor, guides our understanding of the role of energy in complex systems and particularly in biochemistry. Understanding the dynamics and statistical mechanics of agency promises similarly to expand the conceptual scope of physics.

Appendix A Income distributions (BOX)

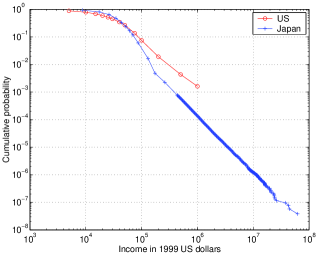

The first identification of a power law distribution – in any field – was made by Vilfredo Pareto in 1897 for the distribution of income among the highest earning few percent of inhabitants of the UK, and all income distributions asymptotically of this form are known in economics as “Pareto distributions”. Subsequent studies by Pareto for Prussia, Saxony, Paris, and few Italian cities confirmed these results, which continue to hold up very well (see Fig. 4). More recent studies incomes have shown that not only is the income of the wealthy regular, but so is the income of the majority of wage earners, and the two groups follow different distributions. The low- and medium-income body of the distribution is either exponential or lognormal (variable among data sets), with a transition to the Pareto law for large incomes, at a level that varies with time, tax laws, and other factors, as yet unknown.

As striking as the fact that the large-income distribution is scale free, is the fact that the overall distribution is so featureless, being described by four (or five) parameters: mean income, Pareto exponent, transition point between low- and high-income ranges, and the exponential constant (or mean and variance of the lognormal) in the low range. Pareto, lognormal, and exponential distributions are all limiting distributions of simple random processes, and can also be derived as maximum-entropy distributions for either income or its logarithm, subject to appropriate boundary conditions on the (arithmetic or geometric) mean income Yakov .

Income distribution is a hot topic economically and politically, because it lies at the heart of a society’s notions of egalitarianism, opportunity, or social insurance. Not surprisingly, causes of income inequality are asserted, such as distinctions between capital ownership and wage labor, with major policy implications. Maximum-entropy interpretations of income distribution place conceptual as well as quantitative bounds on these arguments. They suggest that the many detailed features of a society that could in principle affect incomes somehow average so that their individual characteristic scales are not imprinted on the aggregate distribution; the ultimate constraints may be conservation laws or boundary conditions reflected in at most a few parameters. Such featureless averaging, like the scaling relations we have noted above, may suggest that a form of universality classification is fundamental to understanding economics, as it has been to thermodynamics and field theory.

Appendix B Option pricing (BOX)

Bachelier’s random walk was a triumph of quantitative finance, and became the basis of modern portfolio analysis, and later the Black-Scholes model for option pricing Bouchaud00 . The and coefficients published in every security analysis are mean and covariance coefficients from fits to a random walk. However, the heavy tails of real price fluctuations, under-predicted by the Gaussian distribution resulting from accumulation of an uncorrelated random walk, can lead to disastrous mis-estimates of risk. This has been an important problem in financial mathematics which has received a great deal of attention.

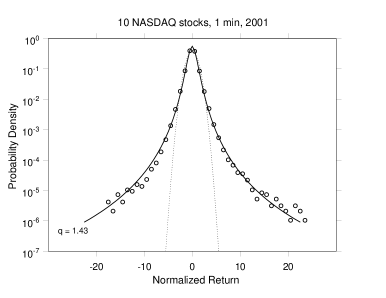

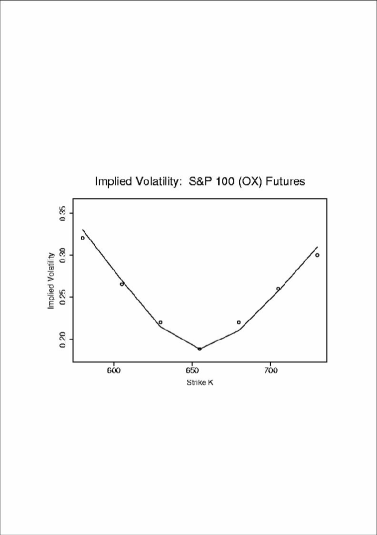

More recent work by physicists extends analytic methods for pricing options to take the heavy tails and volatility bursts of real prices into account. Inspired by the work of Constantino Tsallis on non-extensive statistical mechanics Gell-Mann04 , (see Fig. 5) Lisa Borland Borland02 has developed a new pricing formula that corrects the standard Black-Scholes model. For three decades option-pricing practitioners have recognized that random-walk estimates were too conservative, and compensated by altering the parameters of the Black-Scholes model depending on the strike price of the option. The “implied volatility” assigned in this way makes a well-known “smile” when plotted versus the strike prices (see Fig. 6). The Borland option-pricing formula provides a rational basis for pricing of rare events, and nicely reproduces the volatility smile. While there are a large number of other generalizations of the Black-Scholes theory that address the problem of the smile, Borland’s has the significant advantage that it gives a closed form solution.

The self-consistency condition on which all rational option pricing is based – arbitrage-free hedging of risk – is a classically reductionist principle relating derivatives to their underlying assets. It is noteworthy that economic practice has chosen to adhere to the specific Black-Scholes formula based on an empirically invalid model of the underlying, and to introduce the phenomenological curve of “implied volatility” to bring the formula in line with data. The Borland construction avoids such mixing of reductionism and phenomenology; its single additional parameter describes the observed fluctuations in the underlying asset price, separating the problem of explaining these from that of pricing their derivatives.

References

- (1) B. Mandelbrot. Fractals and Scaling in Finance. Springer-Verlag, New York, 1997.

- (2) R. N. Mantegna and H. E. Stanley. Introduction to Econophysics: Correlations and Complexity in Finance. Cambridge University Press, Cambridge, 1999.

- (3) Gabaix, Xavier, Parameswaran Gopikrishnan, Vasiliki Plerou, H. Eugene Stanley ”A Theory of Power Law Distributions in Financial Market Fluctuations”, Nature, 2003, vol. 423, p. 267-70.

- (4) M. H. R. Stanley, L. A. N. Amaral, S. V. Buldyrev, S. Havlin, H. Leschhorn, P. Maass, M. A. Salinger, and H. E. Stanley, ”Scaling Behavior in the Growth of Companies,” Nature 379, 804-806 (1996).

- (5) J-P. Bouchaud and M. Potters. Theory of Financial Risk:From Statistical Physics to Risk Management. Cambridge University Press, Cambridge, 2000.

- (6) J-P. Bouchaud, Y. Gefen, M. Potters, and M. Wyart, “Fluctuations and response in financial markets: The subtle nature of “random” price changes”, Quantitative Finance 4(2): 176-190 (2004); F. Lillo and J. D. Farmer, “The long memory of the efficient market”, Studies in Nonlinear Dynamics and Econometrics 8 (3), Article 1(2004).

- (7) Z. Burda, J. Jurkiewicz, and M. A. Nowak, “Is Econophysics a Solid Science?”, cond-mat 0301096.

- (8) Didier Sornette. Why Stock Markets Crash: Critical Events in Complex Financial Systems. Princeton University Press, Princeton, 2002.

- (9) P. W. Anderson, K. J. Arrow, and Pines D., editors. The Economy as an Evolving Complex System. Addison-Wesley, Redwood City, 1988.

- (10) W. B. Arthur, J. H. Holland, B. LeBaron, R. Palmer, and P. Tayler. Asset pricing under endogenous expectations in an artificial stock market. In W. B. Arthur, S. N. Durlauf, and D. H. Lane, editors, The Economy as an Evolving Complex System II, pages 15–44. Addison-Wesley, Redwood City, 1997.

- (11) J. D. Farmer, P. Patelli, and Ilija Zovko. The predictive power of zero intelligence in financial markets. Proceedings of the National Academy of Sciences of the United States of America, 102(6):2254–2259, 2005.

- (12) Damien Challet, Matteo Marsili, and Yi-Cheng zhang. Minority Games. Oxford University Press, Oxford, 2005; (if we have to discard one it should be the following) N. F. Johnson, P. Jeffries, and P. M. Hui. Financial Market Complexity. Oxford University Press, Oxford, 2003.

- (13) P. Mirowski. More Heat than Light: Economics as Social Physics, Physics as Nature’s Economics. Historical Perspectives on Modern Economics. Cambridge University Press, Cambridge, 1989.

- (14) E. Smith and D. K. Foley, “Is utility theory so different from thermodynamics?”, SFI preprint # 02-04-016 (2004).

- (15) E. Smith and M. Shubik “Strategic Freedom, Constraint, and Symmetry in One-Period Markets with Cash and Credit Payment”, Economic Theory 25, 513-551 (2005); M. Shubik and E. Smith, “The physics of time and dimension in the economics of financial control”, Physica A 340, 656-667 (2004).

- (16) M. Nirei and W. Souma, “Income Distribution and Stochastic Multiplicative Process with Reset Events”, in Gallegati, Kirman, Marsili eds, The Complex Dynamics of Economic Interaction, Springer, 2003; Figure from M. Nirei and W. Souma, “Two factor model of income distribution dynamics”, SFI preprint # 04-10-029.

- (17) A. Dragulescu and V. M. Yakovenko, “Statistical mechanics of money”, Eur. Phys. J. B 17, 723-729 (2000).

- (18) M. Gell-Mann and C. Tsallis. Nonextensive Entropy- Interdisciplinary Applications. Oxford University Press, New York, 2004.

- (19) L. Borland, “A theory of non-Gaussian option pricing, Quant. Fin. 2, 415-431 (2002).