Anomalous waiting times in high-frequency financial data

Abstract

In high-frequency financial data not only returns, but also waiting times between consecutive trades are random variables. Therefore, it is possible to apply continuous-time random walks (CTRWs) as phenomenological models of the high-frequency price dynamics. An empirical analysis performed on the 30 DJIA stocks shows that the waiting-time survival probability for high-frequency data is non-exponential. This fact imposes constraints on agent-based models of financial markets.

pacs:

05.40.Jc, 89.65.Gh, 02.50.Ey, 05.45.Tp1 Introduction

Starting from the second half of the last decade, due to the availability of large financial databases, there has been an increasing interest on the statistical properties of high-frequency financial data and on market microstructural properties [1, 2, 3, 4, 5, 6]. Various studies on high-frequency econometrics appeared in the literature and among them autoregressive conditional duration models [7, 8, 9, 10].

The basic remark that in high-frequency financial data not only returns but also waiting times between consecutive trades are random variables [11] can already be found in previous literature. For instance, it is present in a paper by Lo and McKinlay published in the Journal of Econometrics [12], but it can be traced at least to papers on the application of compound Poisson processes [13] and subordinated stochastic processes [14] to finance. Compound Poisson processes have been revisited in the recent wave of interest in high-frequency data modelling [15, 16, 17].

Compound Poisson processes belong to the class of continuous-time random walks (CTRWs) [18], which have been recently applied to finance as well (see Sec. 2 for details). To our knowledge, the application of CTRW to economics dates back, at least, to the 1980s. In 1984, Rudolf Hilfer published a book on the application of stochastic processes to operational planning, where CTRWs were used for sale forecasts [19]. The (revisited) CTRW formalism has been applied to the high-frequency price dynamics in financial markets by our research group since 2000, in a series of three papers [20, 21, 22]. Other scholars have recently used this formalism [23, 24, 25]. However, CTRWs have a famous precursor. In 1903, the PhD thesis of Filip Lundberg presented a model for ruin theory of insurance companies, which was further developed by Cramér [26, 27]. The underlying stochastic process of the Lundberg-Cramér model is another example of compound Poisson process and thus also of CTRW.

Among other issues, we have studied the independence between log-returns and waiting times for the 30 Dow-Jones-Industrial-Average (DJIA) stocks traded at the New York Stock Exchange in October 1999. For instance, according to a contingency-table analysis performed on General Electric (GE) prices, the null hypothesis of independence can be rejected with a significance level of 1 % [28]. In this paper, however, the focus is on the empirical distribution of waiting times [29].

This paper is divided as follows: Sec. 2 is devoted to a summary of CTRW theory as applied in finance; the relation of CTRWs to compound Poisson processes will be presented in some detail. In Sec. 3, following our empirical analysis, the reader can convince him/herself of the main result of this paper: for the 30 DJIA stocks in the period considered (October 1999), the waiting-time survival probability for high-frequency data is non-exponential. Finally, in Sec. 4, a possible explanation of this anomaly will be discussed using exponential mixtures as the analytical tool.

2 Theory

The importance of random walks in finance has been known since the seminal thesis of Bachelier [30] which was completed at the end of the XIXth century, more than a hundred years ago. The ideas of Bachelier were further carried out by many scholars [31, 32].

The price dynamics in financial markets can be mapped onto a random walk whose properties are studied in continuous, rather than discrete, time [32]. Here, we shall present this mapping, pioneered by Bachelier [30], in a rather general way. It is worth mentioning that this approach is related to that of Clark [14] and to the introductory notes in Parkinson’s paper [34]. As a further comment, this is a purely phenomenological approach. No specific assumption on the rationality or the behaviour of market agents is taken or even necessary. In particular, it is not necessary to assume the validity of the efficient market hypothesis [35, 36]. Nonetheless, as shown below, a phenomenological model can be useful in order to empirically corroborate or falsify the consequences of behavioural or other assumptions on markets. Moreover, the model itself can be corroborated or falsified by empirical data.

As a matter of fact, there are various ways in which random walk can be embedded in continuous time. Here, we shall base our approach on the so-called continuous-time random walk in which time intervals between successive steps are random variables, as discussed by Montroll and Weiss [18].

Let denote the price of an asset or the value of an index at time . In a real market, prices are fixed when buy orders are matched with sell orders and a transaction (trade) occurs. Returns rather than prices are more convenient. For this reason, we shall take into account the variable , that is the logarithm of the price. Indeed, for a small price variation , the return and the logarithmic return virtually coincide.

As we mentioned before, in financial markets, not only prices can be modelled as random variables, but also waiting times between two consecutive transactions vary in a stochastic fashion. Therefore, the time series is characterised by , the joint probability density of log-returns and of waiting times . The joint density satisfies the normalization condition . Both and are assumed to be independent and identically distributed (i.i.d.) random variables.

Montroll and Weiss [18] have shown that the Fourier-Laplace transform of , the probability density function, pdf, of finding the value of the price logarithm (which is the diffusing quantity in our case) at time , is:

| (1) |

where

| (2) |

and is the waiting time pdf.

The space-time version of eq. (1) can be derived by probabilistic considerations [21]. The following integral equation gives the probability density, , for the walker being in position at time , conditioned by the fact that it was in position at time :

| (3) |

where is the so-called survival function. is related to the marginal waiting-time probability density . The survival function is:

| (4) |

The CTRW model can be useful in applications such as speculative option pricing by Monte Carlo simulations or portfolio selection. This will be the subject of a forthcoming paper. Here, it is more interesting to discuss the relation of this formalism to compound Poisson processes. Indeed, compound Poisson processes are an instance of continuous-time random walks in which waiting times and log-returns are independent random variables; moreover, one assumes that the marginal waiting-time density is an exponential density:

| (5) |

Therefore, the probability of getting log-price jumps up to time is given by the Poisson distribution:

| (6) |

that is the jump point process is a Poisson process. The log-price at time is:

| (7) |

where, as above, is the number of jumps occurred up to time . Let denote the marginal log-return density, then the solution of eq. (3) is:

| (8) |

where is the -fold convolution of the density . Eq. (8) can be also derived by purely probabilistic consideration. The interested reader can find more information on a generalization of this case in a recent paper of our group [38]. An important property of CTRWs is that log-returns and waiting times are independent and identically distributed random variables. Still, there can be a dependence between the two random variables. If they are independent, as in the case of compound Poisson processes, the joint pdf is given by the product of the two marginal densities:

| (9) |

if they are not independent, then, according to the definition of conditional probability, one has:

| (10) |

where and are conditional probability densities. Note, however, that autoregressive conditional duration models introduce a dependence between waiting times and this feature cannot be captured by the above formalism, as waiting times are assumed to be i.i.d. random variables (see also ref. [39]).

3 Empirical evidence

3.1 The data set

The data set consists of nearly 800,000 prices and times of execution obtained from the TAQ database of the NYSE. These data were appropriately filtered in order to remove misprints in prices and times of execution and correspond to the high-frequency trades registered at NYSE in October 1999, for the 30 stocks of the Dow Jones Industrial Average Index, namely, at that time: AA, ALD, AXP, BA, C, CAT, CHV, DD, DIS, EK, GE, GM, GT, HWP, IBM, IP, JNJ, JPM, KO, MCD, MMM, MO, MRK, PG, S, T, UK, UTX, WMT, XON. The choice of one month of high-frequency data was a trade off between the necessity of managing enough data for significant statistical analyses and and, on the other hand, the goal of minimizing the effect of external economic fluctuations. The reader can determine the company to which the above symbols correspond just by consulting the NYSE web pages (www.nyse.com).

In order to roughly evidence intraday patterns [4], the data set has been divided into three daily periods: morning (from 9:00 to 10:59), midday (from 11:00 to 13:59) and afternoon (from 14:00 to 17:00). In Table 1, the number of trades for each daily period is given as a function of the stock.

| Stock | n1 (9:00-10:59) | n2 (11:00-13:59) | n3 (14:00-17:00) |

|---|---|---|---|

| AA | 4098 | 5662 | 5298 |

| ALD | 5248 | 7367 | 6504 |

| AXP | 9054 | 12267 | 12988 |

| BA | 5058 | 7080 | 6717 |

| C | 15628 | 21578 | 18541 |

| CAT | 3596 | 5361 | 4790 |

| CHV | 4973 | 6608 | 5591 |

| DD | 5284 | 7363 | 6913 |

| DIS | 7160 | 10504 | 9182 |

| EK | 3218 | 4433 | 4174 |

| GE | 16063 | 20214 | 19372 |

| GM | 16134 | 4340 | 6173 |

| GT | 3124 | 4105 | 3968 |

| HWP | 10278 | 14095 | 12062 |

| IBM | 12534 | 22668 | 16633 |

| IP | 4358 | 6263 | 5590 |

| JNJ | 6693 | 9856 | 8644 |

| JPM | 6410 | 7704 | 7991 |

| KO | 8511 | 12437 | 10575 |

| MCD | 5641 | 7729 | 6895 |

| MMM | 3578 | 5398 | 4996 |

| MO | 9680 | 14565 | 11852 |

| MRK | 9222 | 13462 | 11587 |

| PG | 6809 | 9598 | 8482 |

| S | 4694 | 5838 | 5319 |

| T | 12291 | 18598 | 14391 |

| UK | 2738 | 3305 | 3208 |

| UTX | 3745 | 5765 | 5249 |

| WMT | 8344 | 12446 | 10256 |

| XON | 9321 | 11669 | 10838 |

3.2 Empirical analysis

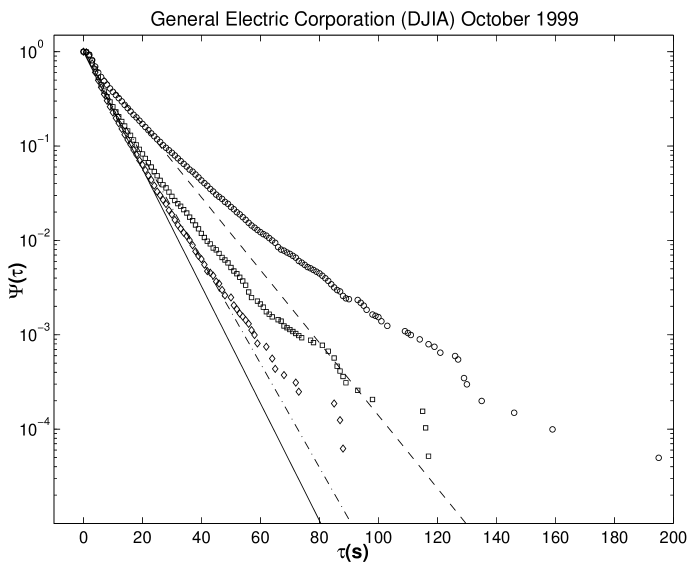

In Fig. 1, the waiting-time complementary cumulative distribution function (or survival function) is plotted for three different periods of the day and for the GE time series of October 1999. In the above formula, represents the marginal waiting-time probability density function. gives the probability that the waiting time between two consecutive trades is greater than the given . The lines are the corresponding standard exponential complementary cumulative distribution functions:

| (11) |

where is the empirical average waiting time. An eye inspection already shows the deviation of the real distribution from the exponential distribution. This fact is corroborated by the Anderson-Darling test [40]. According to this test, for a large number of samples, one has to compute the following statistics, after ordering the samples in ascending order:

| (12) |

where is the total number of samples and is

| (13) |

where is the survival function. In order to test the exponential distribution, one must insert in the above formula the survival function (11) with taken from the empirical estimates in Table 2. In the case of GE (Fig. 1), the Anderson-Darling (AD) values for the three daily periods are, respectively, 352, 285, and 446. Therefore, the null hypothesis of exponential distribution can be rejected at the 1 % significance level as the limit value is 1.957.

In Table 2, the values of the AD statistics are given for all the 30 DJIA stocks traded in October 1999. In all these cases the null hypothesis of exponentiality can be rejected at the 1 % significance level.

It is interesting to observe that the average waiting time is sytematically and significantly larger at midday than in the morning or in the afternoon. This results points to a variable NYSE trade activity and is in agreement with previously reported behaviour in stock markets [44, 45, 46]. This fact has a biological explanation. Around midday the activity is slower as traders move from their desks to eat. In fact, as will be seen, these intra-day variations in trading activity may also account for the reported anomaly in the distribution of waiting times.

3.3 Independent results corroborating this study

Our study demonstrates that the marginal density for waiting times is definitely not an exponential function. After the publication of our paper series [20, 21, 22], different waiting-time scales have been investigated in different markets by various authors. All these empirical analyses corroborate the waiting-time anomalous behaviour. A study on the waiting times in a contemporary FOREX exchange and in the XIXth century Irish stock market was presented by Sabatelli et al. [41]. They were able to fit the Irish data by means of a Mittag-Leffler function as we did before in a paper on the waiting-time marginal distribution in the German-bund future market [21]. Kyungsik Kim and Seong-Min Yoon studied the tick dynamical behavior of the bond futures in Korean Futures Exchange (KOFEX) market and found that the survival probability displays a stretched-exponential form [42]. Moreover, just to stress the relevance of non-exponential waiting times, a power-law distribution has been recently detected by T. Kaizoji and M. Kaizoji in analyzing the calm time interval of price changes in the Japanese market [43].

| Stock | ||||||

|---|---|---|---|---|---|---|

| AA | 27.1 | 40.0 | 28.8 | 29.2 | 66.0 | 44.8 |

| ALD | 21.2 | 30.8 | 23.4 | 21.8 | 55.5 | 33.8 |

| AXP | 11.8 | 18.5 | 11.7 | 81.7 | 102.5 | 130.7 |

| BA | 22.0 | 32.0 | 22.6 | 17.4 | 20.2 | 21.2 |

| C | 7.1 | 10.5 | 8.2 | 252.2 | 142.8 | 210.7 |

| CAT | 29.2 | 42.4 | 31.6 | 72.3 | 128.7 | 64.6 |

| CHV | 22.1 | 34.3 | 27.1 | 104.4 | 121.5 | 64.9 |

| DD | 20.3 | 30.8 | 22.1 | 22.9 | 44.3 | 36.1 |

| DIS | 15.2 | 20.8 | 16.6 | 53.4 | 53.4 | 74.7 |

| EK | 34.1 | 51.2 | 36.3 | 24.8 | 34.8 | 44.3 |

| GE | 7.0 | 11.3 | 7.9 | 351.9 | 284.7 | 445.6 |

| GM | 24.6 | 36.6 | 27.0 | 22.4 | 60.8 | 40.9 |

| GT | 34.3 | 55.5 | 37.9 | 73.7 | 95.7 | 54.1 |

| HWP | 10.4 | 16.1 | 12.7 | 94.8 | 77.8 | 100.8 |

| IBM | 8.9 | 10.0 | 9.2 | 409.6 | 472.5 | 489.5 |

| IP | 24.8 | 36.3 | 27.0 | 25.0 | 37.2 | 19.4 |

| JNJ | 16.1 | 23.0 | 17.7 | 30.4 | 35.6 | 38.0 |

| JPM | 17.0 | 29.5 | 19.0 | 33.0 | 85.2 | 85.8 |

| KO | 12.9 | 18.3 | 14.4 | 44.5 | 37.8 | 44.1 |

| MCD | 19.4 | 29.3 | 22.1 | 40.9 | 72.7 | 44.1 |

| MMM | 30.1 | 42.0 | 30.4 | 80.1 | 86.8 | 37.5 |

| MO | 11.4 | 15.6 | 12.9 | 74.2 | 89.0 | 75.2 |

| MRK | 11.7 | 16.8 | 13.2 | 133.1 | 136.0 | 189.8 |

| PG | 16.2 | 23.6 | 17.9 | 43.5 | 37.2 | 48.8 |

| S | 23.4 | 38.8 | 28.6 | 40.1 | 23.0 | 41.6 |

| T | 8.8 | 12.2 | 10.6 | 193.2 | 179.1 | 208.9 |

| UK | 40.4 | 69.1 | 46.7 | 33.8 | 72.4 | 47.2 |

| UTX | 28.5 | 39.3 | 29.0 | 33.7 | 62.9 | 58.0 |

| WMT | 12.5 | 18.2 | 14.9 | 105.2 | 110.6 | 139.1 |

| XON | 12.0 | 19.6 | 14.1 | 104.8 | 121.4 | 129.0 |

4 Discussion and conclusions

Why should we care about these empirical findings on the waiting-time distribution? This has to do both with the market price formation mechanisms and with the bid-ask process. A priori, one could argue that there is no strong reason for independent market investors to place buy and sell orders in a time-correlated way. This argument would lead one to expect a Poisson process. If price formation were a simple thinning of the bid-ask process, then exponential waiting times should be expected between consecutive trades as well [37]. Eventually, even if empirical analyses should show that time correlations are already present at the bid-ask level, it would be interesting to understand why they are there. In other words, the empirical results on the survival probability set limits on statistical market models for price formation. A possibly correlated result has been recently obtained by Fabrizio Lillo and Doyne Farmer, who find that the signs of orders in the London Stock Exchange obey a long-memory process [47] as well as by Jean Philippe Bouchaud and coworkers [48]. Further studies on market microstructure will be necessary to clarify this point.

However, it is possible to offer a simple explanation of the anomalous behaviour in terms of exponential mixtures due to variable activity during the trading day.

Let us introduce a toy model of variable activity during a trading day. The trading day can be divided into subintervals where waiting times follow an exponential distribution with different average waiting times . Just recalling that the rate is the inverse of the average waiting time: , one has that the survival function is given by:

| (14) |

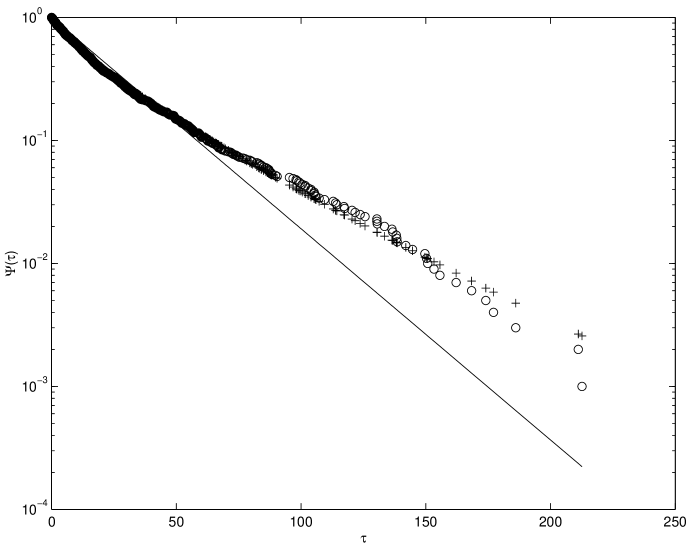

where are suitable weights whose sum must be 1, to fulfill the condition . This sum of exponential components is itself non-exponential. For illustrative purposes, in Fig. 2, the reader can find the comparison between eq. (14) and simulated data in which the day had been divided into 10 intervals of equal weight. In each interval the average waiting time between trades was a constant and the waiting times followed an exponential distribution. The value of the constant increased from 10 to 50 seconds in the first five intervals and then decreased from 40 to 5 seconds in the last five intervals, so that the sequence of waiting times (in seconds: 10,20,30,40,50,40,30,20,10,5) is a rough representation of the activity in a real financial market. The open circles are the survival function of the Monte Carlo simulation, the solid line represents the single exponential fit of the survival function, whereas, the crosses are values of the survival function computed according to eq. (14) with . Even if for long waiting times, the tail of the distribution is again exponential with rate , the exponential mixture can describe deviations from the single exponential law for short and intermediate waiting times.

The probability density corresponding to eq. (14) can be formally written in the following way:

| (15) |

Eq. (15) can be readily extended to a continuous spectrum of rates, :

| (16) |

where the condition must hold. Indeed, the integral equation (16) reduces to eq. (15) if has the following form:

| (17) |

where is Dirac’s generalized function and .

In conclusion, we have shown that, in October 1999, waiting times between consecutive trades in the 30 NYSE DJIA stocks were non-exponentially distributed. We have summarized other recent results pointing to the same conclusions for different markets. We have argued that this fact has implications for market microstructural models that should be able to reproduce such a non-exponential behaviour to be realistic. Finally, we have offered a possible explanation in terms of variable trading activity during the day.

Acknowledgements

We would like to acknowledge useful discussions with Sergio Focardi of The Intertek Group. This work was supported by grants from the Italian M.I.U.R. Project COFIN 2003 “Order and Chaos in nonlinear extended systems: coherent structures, weak stochasticity and anomalous transport” and by the Italian M.I.U.R. F.I.S.R. Project “Ultra-high frequency dynamics of financial markets”.

References

References

- [1] C. Goodhart and M. O’Hara, High-frequency data in financial markets: Issues and applications, Journal of Empirical Finance 4, 73–114 (1997).

- [2] M. O’Hara Making market microstructure matter, Financial Management 28, 83–90 (1999).

- [3] A. Madhavan Market microstructure: A survey, Journal of Financial Markets 3, 205–258 (2000).

- [4] M.M. Dacorogna, R. Gençay, U.A. Müller, R.B. Olsen, O.V. Pictet, An Introduction to High Frequency Finance, (Academic Press, 2001).

- [5] M. Raberto, S. Cincotti, S.M. Focardi, M. Marchesi, Agent-based simulation of a financial market, Physica A 299, 320–328 (2001).

- [6] H. Luckock, A steady-state model of the continuous double auction, Quantitative Finance 3, 385–404 (2003).

- [7] R. Engle and J. Russel Forecasting the frequency of changes in quoted foreign exchange prices with the autoregressive conditional duration model, Journal of Empirical Finance 4, 187–212 (1997).

- [8] R. Engle and J. Russel, Autoregressive conditional duration: A new model for irregularly spaced transaction data, Econometrica 66, 1127–1162 (1998).

- [9] L. Bauwens and P. Giot The logarithmic ACD model: An application to the bid-ask quote process of three NYSE stocks, Annales d’Economie et de Statistique 60, 117–149 (2000).

- [10] A. Lo, C. MacKinley and J. Zhang, Econometric model of limit-order executions, Journal of Financial Economics 65, 31–71 (2002).

- [11] G.O. Zumbach, Considering time as the random variable: the first hitting time, Neural Network World 8, 243–253 (1998).

- [12] A. Lo and C. MacKinley, An econometric analysis of nonsynchronous trading, Journal of Econometrics 45, 181–212 (1990).

- [13] S.J. Press, A compound events model for security prices, Journal of Business 40, 317–335 (1967).

- [14] P.K. Clark, A subordinated stochastic process model with finite variance for speculative prices, Econometrica 41, 135-156 (1973).

- [15] T.H. Rydberg and N. Shephard, Dynamics of trade-by-trade price movements: Decomposition and models, Nuffield College, Oxford, working paper series 1998-W19 (1998).

- [16] T.H. Rydberg and N. Shephard, Modelling trade-by-trade price movements of multiple assets using multivariate compound Poisson processes, Nuffield College, Oxford, working paper series 1999-W23 (1999).

- [17] T.H. Rydberg and N. Shephard, A modelling framework for the prices and times of trades made at the New York stock exchange, in W.J. Fitzgerald, R. Smith, A.T. Walden, P. Young (Editors): Nonlinear and nonstationary signal processing, (Cambridge University Press, 2000).

- [18] E.W. Montroll and G.H. Weiss, Random walks on lattices, II, J. Math. Phys. 6, 167–181 (1965).

- [19] R. Hilfer, Stochastische Modelle für die betriebliche Planung, (GBI-Verlag, Munich, 1984).

- [20] E. Scalas, R. Gorenflo and F. Mainardi, Fractional calculus and continuous-time finance, Physica A 284, 376–384 (2000).

- [21] F. Mainardi, M. Raberto, R. Gorenflo and E. Scalas, Fractional calculus and continuous-time finance II: the waiting-time distribution, Physica A 287, 468–481, (2000).

- [22] R. Gorenflo, F. Mainardi, E. Scalas and M. Raberto Fractional calculus and continuous-time finance III: the diffusion limit, in M. Kohlmann and S. Tang (Editors): Trends in Mathematics - Mathematical Finance, pp. 171–180 (Birkhäuser, Basel, 2001).

- [23] J. Masoliver, M. Montero, and G.H. Weiss, Continuous-time random-walk model for financial distributions, Phys. Rev. E 67, 021112/1–9 (2003).

- [24] J. Masoliver, M. Montero, J. Perello. and G.H. Weiss, The CTRW in finance: Direct and inverse problem http://xxx.lanl.gov/abs/cond-mat/0308017

- [25] R. Kutner and F. Switala, Stochastic simulation of time series within Weierstrass-Mandelbrot walks, Quantitative Finance 3, 201–211 (2003).

-

[26]

F. Lundberg,

Approximerad Framställning av Sannolikehetsfunktionen. AAterförsäkering av Kollektivrisker, (Almqvist & Wiksell, Uppsala, 1903). - [27] H. Cramér, On the Mathematical Theory of Risk, (Skandia Jubilee Volume, Stockholm 1930).

- [28] M. Raberto, E. Scalas and F. Mainardi, Waiting times and returns in high-frequency financial data: an empirical study, Physica A 314, 749–755 (2002).

- [29] E. Scalas, R. Gorenflo, H. Luckock, F. Mainardi, M. Mantelli and M. Raberto. On the intertrade waiting-time distribution, Finance Letters, in press.

- [30] L.J.B. Bachelier Theorie de la Speculation, (Gauthier-Villars, Paris, 1900, Reprinted in 1995, Editions Jaques Gabay, Paris, 1995).

- [31] P.H. Cootner (ed.) The Random Character of Stock Market Prices, (MIT Press, Cambridge MA, 1964).

- [32] R.C. Merton, Continuous Time Finance, (Blackwell, Cambridge, MA, 1990).

- [33] P. Lévy, Théorie de l’Addition des Variables Aléatoires, (Gauthier–Villars, Paris, 1937).

- [34] M. Parkinson, Option pricing: The american put, Journal of Business 50 21–36 (1977).

- [35] E.F. Fama, Efficient capital markets: A review of theory and empirical work, The Journal of Finance 25, 383–417 (1990) .

- [36] E.F. Fama, Efficient capital markets: II, The Journal of Finance 46, 1575–1617 (1991).

- [37] D. Cox and V. Isham Point Processes, (Chapman and Hall, London, 1979).

- [38] E. Scalas, R. Gorenflo and F. Mainardi, Uncoupled continuous-time random walks: Solution and limiting behavior of the master equation, Phys. Rev. E 69, 011107(1-8) (2004).

- [39] M. Salmon and I. Marsh, Lecture Notes on: Market Micro Structure and High Frequency Econometrics, Working Paper, Department of Banking and Finance, City University Business School, London (2001).

- [40] M.A. Stephens, EDF statistics for goodness of fit and some comparison, Journal of the American Statistical Association 69, 730–737 (1974).

- [41] L. Sabatelli, S. Keating, J. Dudley and P. Richmond, Waiting time distribution in financial markets, Eur. Phys. J. B 27, 273–275 (2002).

- [42] K. Kim and S.-M. Yoon, Dynamical behavior of continuous tick data in futures exchange market, Fractals 11, 131–136 (2003).

-

[43]

T. Kaizoji and M. Kaizoji,

Power law for the calm-time interval of price changes,

Physica A 336, 563–570 (2004). - [44] M. Raberto, E. Scalas, G. Cuniberti and M. Riani, Volatility in the Italian stock market: an empirical study, Physica A 269 148–155 (1999).

- [45] V. Plerou, P. Gopikrishnan, L.A.N. Amaral, X. Gabaix and H.E. Stanley Economic fluctuations and anomalous diffusion, Phys. Rev. E 62 R3023–R3026 (2000).

- [46] W. Bertram, An empirical investigation of Australian Stock Exchange Data, preprint.

-

[47]

F. Lillo and J. Doyne Farmer,

The long memory of the efficient market,

http://xxx.lanl.gov/abs/cond-mat/0311053. - [48] J.P. Bouchaud, Y. Gefen, M. Potters, M.Wyart, Fluctuations and Response in Financial Markets: The subtle nature of ‘random’ price changes, Quantitative Finance 4, 176–190 (2004).