Shareholding Networks in Japan

Abstract

The Japanese shareholding network existing at the end of March 2002 is studied empirically. The network is constructed from 2,303 listed companies and 53 non-listed financial institutions. We consider this network as a directed graph by drawing edges from shareholders to stock corporations. The lengths of the shareholder lists vary with the companies, and the most comprehensive lists contain the top 30 shareholders. Consequently, the distribution of incoming edges has an upper bound, while that of outgoing edges has no bound. The distribution of outgoing degrees is well explained by the power law function with an exponential tail. The exponent in the power law range is . To understand these features from the viewpoint of a company’s growth, we consider the correlations between the outgoing degree and the company’s age, profit, and total assets.

Keywords:

Shareholding network, Power law, Company’s growth:

89.75.Hc, 89.65.Gh1 Introduction

The economy is regarded as a set of activities of irrational agents in complex networks. However, many traditional studies in economics investigate the activities of rational and representative agents in simple networks, i.e., regular networks and random networks. To overcome the limitations of such an unrealistic situation, the viewpoint of irrational agents has emerged. However, simple networks have been adopted in economics and many studies of agent simulation. Recently, the study of complex networks has revealed the true structure of real-world networks barabasi2002 dm2003 . Gross networks such as interindustry relations have been considered in the macro economy, but the detailed structures of networks constructed from entities in the micro economy have not been clearly elucidated sfa2003 sfa2004 sfa2005 gbcsc2003 .

By common practice, if we intend to discuss networks, we must define their nodes and edges. Edges represent the relationships between nodes. In this study, we consider companies as nodes. To define the relationships between companies, we use three viewpoints: ownership, governance, and activity. These three viewpoints have relations with each other. Ownership is characterized by the shareholding of companies, which is the subject of this article. Governance is characterized by the interlocking of directors, and it is frequently represented by a bipartite graph constructed from corporate boards and directors. The activity networks are characterized by many relationships: trade, collaboration, etc.

In this article we consider Japanese shareholding network at the end of March 2002 (see Ref. gbcsc2003 for shareholding networks in MIB, NYSE, and NASDAQ). We use data published by TOYO KEIZAI INC. This data source provides lists of shareholders for 2,765 companies listed on the stock market or the over-the-counter market. The lengths of the shareholder lists vary with the companies. The most comprehensive lists contain information on the top 30 shareholders. Types of shareholders include listed companies, non-listed financial institutions (commercial banks, trust banks, and insurance companies), officers, and other individuals. In this article, we only consider the shareholding network constructed from 2,303 companies listed on the stock market and 53 non-listed financial institutions. Accordingly, the size of this network is , and the total number of edges is .

This paper is organized as follows. In the next section we consider the degree distribution for both incoming edges and outgoing ones and show that the outgoing degree distribution follows a power law function with an exponential cutoff. In the following section, we discuss correlations between the degree and the company’s age, profit, and total assets. This is because we assume that the dynamical change and growth of business networks can be explained by the company’s growth. The last section is devoted to a summary and discussion.

2 Degree distribution in the directed shareholding network

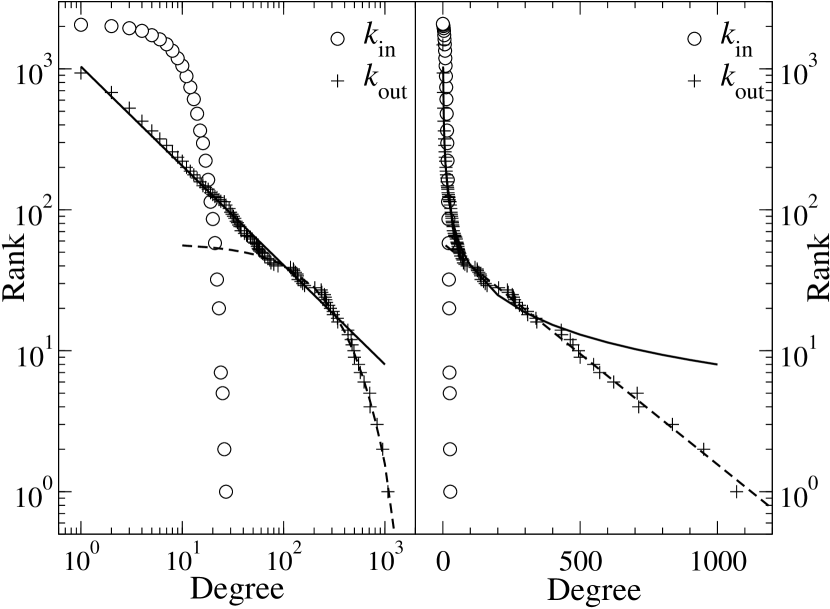

If we draw arrows from shareholders to stock corporations, we can represent a shareholding network as a directed graph. If we count the number of incoming edges and that of outgoing edges for each node, we can obtain the degree distribution for incoming degree, , and that of outgoing degree, . However, as explained above, the lengths of the shareholder lists vary with the companies, and the most comprehensive lists contain the top 30 shareholders. Therefore, the incoming degree has an upper bound, , while the outgoing degree has no bound.

The log-log plot of the degree distribution is shown in the left panel of Fig. 1, and the semi-log plot is shown in the right panel of Fig. 1. In this figure, the horizontal axis corresponds to the degree and the vertical axis corresponds to the rank. The open circles represent the distribution of the incoming degree, and the plus symbols represent that of the outgoing degree. As mentioned above, we can find the upper bound for the incoming degree. In the discussion below, therefore, we consider only the distribution of the outgoing degree.

The solid lines correspond to the fitting by the power law function with the exponent , and the dashed lines correspond to the fitting by the exponential function. We can see that the outgoing degree distribution follows the power law distribution with an exponential cutoff. The exponential part of the distribution is constructed from 40 nodes, which are 38 financial institutions and 2 trading firms. On the other hand, the power law part of the distribution is constructed from 2,316 nodes, and 96% of them represent non-financial institutions.

The above results suggest that different mechanisms work in each range of the distribution. We assume that the dynamics in the range of the exponential distribution is essentially explained by the model proposed in Ref. asbs2000 . This model is based on a so-called BA model ba1999 , i.e., the preferential attachment in growing networks that explains the power law distribution of the degree. Here, we assume that the outgoing degree distribution in the tail part is explained based on the BA model, since financial institutions must invest money as shares. Therefore, financial institutions actively obtain shares of companies newly listed on the stock market or the over-the-counter market. This mechanism is almost the same as preferential attachment. However, we must modify the BA model in order for it to explain the exponential distribution of the outgoing degree. If we consider an extended BA model with aging of the nodes, then we can obtain the exponential degree distribution asbs2000 . However, as explained in the next section, this is not the case. On the other hand, if we consider an extended BA model that includes the cost of adding edges to the nodes or the limited capacity of a node, then we can obtain the exponential degree distribution asbs2000 . As explained in the next section, this is actually the case.

We consider cliques in networks to be important characteristics for constructing a model that can explain the power law distribution of the outgoing degree. Cliques in networks are quantified by a clustering coefficient ws1998 , which is defined in the case of undirected networks. Supposing that a node has edges, then at most edges can exist between them. The clustering coefficient of node , , is the fraction of these allowable edges that actually exist for , i.e., . This has been calculated for an undirected shareholding network by using the same data used in this article sfa2005 , and it has been shown that the clustering coefficient follows the power law distribution, , with the exponent . Such a scaling property of the distribution of clustering coefficients has also been observed in biological networks, and this has motivated the concept of hierarchical networks rsmob2002 rb2003 . We believe that the dynamics in the power law distribution of the outgoing degree is essentially explained by extending the model proposed in Ref. rb2003 .

The clustering coefficient is approximately equal to the probability of finding triangles in the network. The triangle forms the minimum loop. Therefore, if node has a small value of , then the probability of finding loops around this node is low. Consequently, this scaling property of the clustering coefficient suggests that the network is locally tree-like.

3 Correlation between outgoing degree and company’s growth

We consider the correlations between the outgoing degree and the company’s age, profit, and total assets. We believe that knowing the characteristics of nodes is useful for constructing models explaining the dynamics of networks. In many complex networks, it is difficult to quantitatively characterize the nature of nodes. However, in the case of economic networks, especially networks constructed from companies, we can obtain the nature of nodes quantitatively based on balance sheets, and income statements, for example. We consider this a remarkable characteristic of business networks, and it allows us to understand business networks in terms of the company’s growth. We believe that the dynamics of business networks must be explained by the theory of company growth.

3.1 Outgoing degree and company’s age

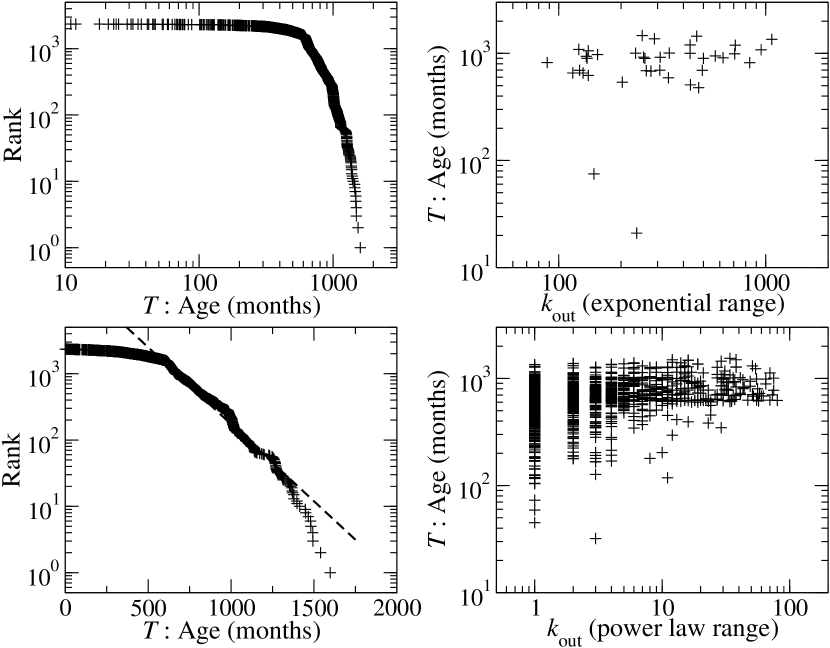

As mentioned in the previous section, we consider the correlation between the outgoing degree and the company’s age in order to clarify whether the BA model with aging of the nodes is applicable to a particular case. In the following, we measure the company’s age in units of months.

The log-log plot of the distribution of the company’s age is shown in the upper left panel of Fig. 2. In this figure, the horizontal axis is the age in the unit of months, and the vertical axis is the rank. This figure shows that the distribution does not fit a simple function such as a power law function.

The semi-log plot of the distribution of the company’s age is shown in the lower left panel of Fig. 2. In this figure, the meaning of the axes is the same as in the upper figure. The dashed line corresponds to the fitting by the exponential function. This means that the distribution of the company’s age approximately follows the exponential distribution. It is expected that the age of a company has a relation with its lifetime, and the lifetime of bankrupted companies follows an exponential distribution fujiwara2004 fagsg2004 .

The upper right panel of Fig. 2 shows a log-log plot of the correlation between the company’s age in months and the outgoing degree that follows the exponential distribution. We can observe that these two quantities have no correlation. To quantify this observation, we calculated Spearman’s rank correlation and Kendall’s rank correlation and obtained and , respectively. These results mean that there is no correlation between the company’s age and the outgoing degree that follows the exponential distribution. This suggests that the BA model with aging of the nodes is not applicable to this case.

The lower right panel of Fig. 2 shows a log-log plot of the correlation between the company’s age in months and the outgoing degree that follows the power law distribution. We can also observe that these two quantities have no correlation. In this case, and . These results mean that there is no correlation between the company’s age and the outgoing degree that follows the power law distribution. Needless to say, the BA model with aging of the nodes is not applicable to this case.

A comparison of these two figures clarifies the independence between the outgoing degree and the company’s age. There are some companies with a few outgoing edges in the range where the lifetime is longer than months.

3.2 Outgoing degree and company profit

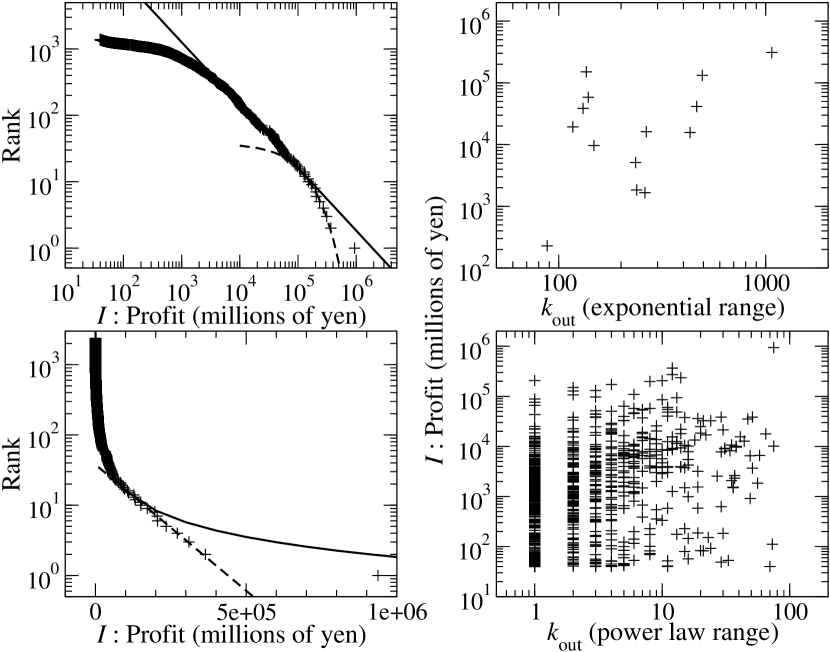

We consider the correlation between the outgoing degree and the company’s profit. Here the company’s profit is the amount of money that the company gains when it is paid more for something than it cost to make, get or do it. Hence the profit includes information on the flow in the network. Here, we consider the company’s profit as an amount of money stored in the period from the beginning of April 2001 to the end of March 2002.

The log-log plot of the distribution of the company’s profit is shown in the upper left panel of Fig. 3. In this figure, the horizontal axis is profit in units of million yen, and the vertical axis is the rank. The solid line corresponds to the fitting by the power law function. This is represented by the probability density function (pdf), as with the exponent . This shows that the distribution in the profit in the middle range follows the power law distribution. The dashed line corresponds to the fitting by the exponential function. The exponential distribution in the high-profit range is better clarified by the semi-log plot.

The semi-log plot of the distribution of the company’s profit is shown in the lower left panel of Fig. 3. The meanings of axes, solid line, and dashed line are the same as those in the upper panel. This figure shows that the profit in the tail part follows an exponential distribution. However, the number of companies within this range is small.

The upper right panel of Fig. 3 shows a log-log plot of the correlation between the company’s profit in the unit of million yen and the outgoing degree that follows the exponential distribution. As mentioned previously, the exponential part of the outgoing degree distribution contains 40 nodes, which are 38 financial institutions and 2 trading firms. Almost all of these financial institutions are not listed on the stock market, and we could not obtain their profit data. Needless to say, there is also a possibility that the profit of these financial institutions was negative. Therefore, the total number of data point is less than 40. We can see that these two quantities have no or only weak correlation. Spearman’s rank correlation and Kendall’s rank correlation are and , respectively. These results mean that there is no or only weak correlation between the company’s profit and the outgoing degree that follows the exponential distribution.

The lower right panel of Fig. 3 shows a log-log plot of the correlation between the company’s profit and the outgoing degree that follows the power law distribution. We can see that these two quantities also have no or only weak correlation. In this case, and . These results mean that there is no or only weak correlation between the company’s profit and the outgoing degree that follows the power law distribution.

Here, we consider the profits of the companies comprising the network. Therefore, the distribution of profit, i.e., the upper left panel of Fig. 3, is not so impressive. However, the profit of Japanese companies has remarkable properties: (i) It is confirmed that in the period after 1970 the high-profit range followed the power law , i.e., Pareto-Zipf’s law, and was stable mktt2002 . (ii) It is confirmed for the years 2000 and 2001 that detailed balance was maintained for the top 70,000 companies in the high-profit range asf2003 . (iii) It is also confirmed for the years 2000 and 2001 that Gibrat’s law was maintained for the top 70,000 companies in the high-profit range asf2003 . Here, Gibrat’s law means that the growth rate of profit is independent of the profit in the initial year. (iv) These characteristics are related to each other asf2003 .

3.3 Outgoing degree and company’s total assets

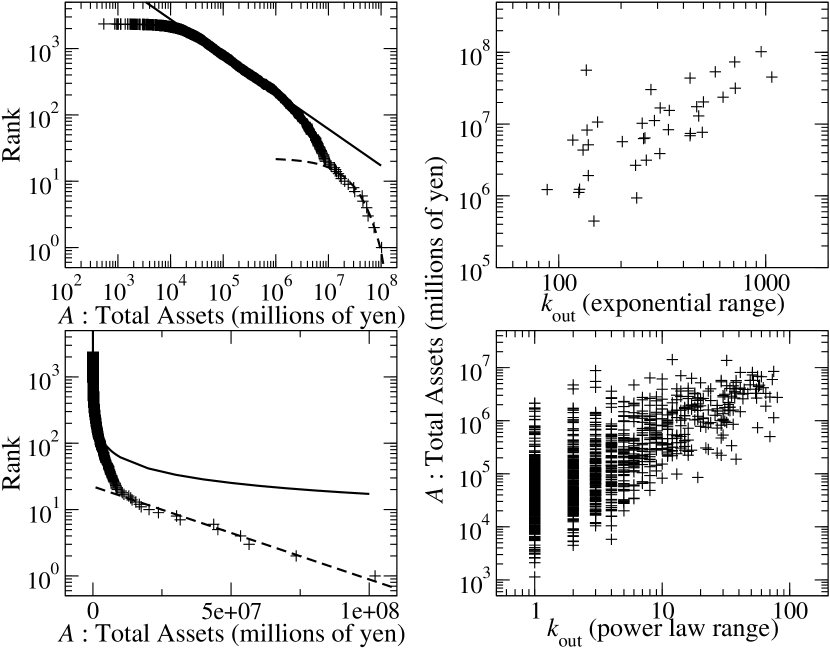

We next considered the correlation between the outgoing degree and the company’s total assets. The company’s total assets are naively regarded as the amount of profit. A portion of the company’s total assets is invested in shares. Accordingly, it is expected that the company’s total assets have a relation with the cost of adding edges to the nodes or with the limited capacity of a node.

The log-log plot of the distribution of the company’s total assets at the end of March 2002 is shown in the upper left panel of Fig. 4. In this figure, the horizontal axis is the total assets in the units of million yen, and the vertical axis is the rank. The solid line corresponds to the fitting by the power law function with the exponent . This figure shows that the level of total assets in the middle range follows the power law distribution. The dashed line corresponds to the fitting by the exponential function.

The semi-log plot of the distribution of the company’s total assets is shown in the lower left panel of Fig. 4. The meanings of axes, solid line, and dashed line are the same as in the upper panel. This figure shows that the level of the total assets in the tail part of the distribution follows the exponential distribution. However, the change from the power law distribution to the exponential distribution is not smooth.

The upper right panel of Fig. 4 shows a log-log plot of the correlation between the company’s total assets at the end of March 2002 in units of million yen and the outgoing degree that follows the exponential distribution. Contrary to the case of the company’s profit, we can obtain data on the company’s total assets for the non-listed financial institutions. This figure shows that these two quantities strongly correlate. Spearman’s rank correlation and Kendall’s rank correlation are and , respectively. These results mean that there is strong correlation between the company’s total assets and the outgoing degree that follows the exponential distribution. This suggests that the BA model incorporating the cost of adding edges to the nodes or the limited capacity of a node is applicable to this case.

The lower right panel of Fig. 4 shows a log-log plot of the correlation between the company’s total assets and the outgoing degree that follows the power law distribution. We can see that these two quantities also have strong correlation. In this case, and . These results mean that there is strong correlation between the company’s total assets and the outgoing degree that follows the power law distribution.

This suggests that the level of the company’s total assets has strong correlation with the outgoing degree. In particular, it is assumed that the outgoing degree distribution in the tail part is explained by the BA model incorporating the cost of adding edges to the nodes or the limited capacity of a node. However to confirm this assumption, we must study the accumulation process of the company’s total assets.

4 Summary

In this paper we considered the Japanese shareholding network existing at the end of March 2002. Although we could not clarify the detailed characteristics of the incoming degree distribution, we could obtain useful information on the outgoing degree distribution: (i) The outgoing degree distribution follows the power law with an exponential cutoff. (ii) The important factor in the growth of the business network is not the company’s age but its total assets. This means that old companies do not necessarily have large total assets. (iii) It is expected that the dynamics of the tail part of the outgoing degree distribution, i.e. the exponential distribution range, can be explained by the BA model incorporating the cost of adding edges to the nodes or the limited capacity of a node. However, the mechanism for the power law part of the outgoing degree distribution is still not known. We believe that the dynamical change and growth of business networks must be explained by the company’s growth. Consequently, knowing the dynamics of the company’s growth is a key concept in considering the growth of economic networks fgags2004 afs2004 .

We would like to conclude with two observations. The first concerns degree correlation. In this article, we considered the shareholding network as a directed graph. However, if we ignore the direction of edge, we can calculate many quantities to obtain the characteristics of networks. For example, the nearest neighbors’ average degree of nodes with degree , , is an important quantity pvv2001 . This was calculated by Ref. sfa2005 for the Japanese shareholding networks at the end of March 2002, in which was obtained with the exponent . This means that hubs are not directly connected to each other in this network, i.e., it’s a degree non-assortative network.

The second observation concerns the spectrum of the graph. It has recently been shown through an effective medium approximation that the probability density function of the eigenvalue for the adjacency matrix, , is asymptotically represented by that of the degree distribution , i.e., , if the network has a local tree-like structure dgmc2003 . As mentioned previously, the shareholding network has this characteristic. Therefore, if asymptotically follows the power law distribution, also asymptotically follows the power law distribution. In addition, we can derive the scaling relation . At the end of March 2002, the tail part of the eigenvalue for the adjacency matrix of the undirected Japanese shareholding network followed with the exponent . On the other hand, the degree distribution in this case is with the exponent . Therefore, the scaling relation is guaranteed sfa2005 .

References

- (1) A.-L. Barabási, Linked: The New Science of Networks, Perseus Press, Cambridge, MA, 2002.

- (2) S. N. Dorogovtsev, and J. F. F. Mendes, Evolution of Networks: From Biological Nets to the Internet and WWW, Oxford University Press, Oxford, 2003.

- (3) W. Souma, Y. Fujiwara, and H. Aoyama, Physica A, 324, 396–401 (2003).

- (4) W. Souma, Y. Fujiwara, and H. Aoyama, Physica A, 344, 73–76 (2004).

- (5) W. Souma, Y. Fujiwara, and H. Aoyama, “Heterogeneous economic networks,” in Economics and Heterogeneous Interacting Agents, co-edited by A. Namatame, et al., Springer-Verlag, Tokyo, 2005, to be published. arXiv:physics/0502005.

- (6) D. Garlaschelli, et al., to be published in Physica A. arXiv:cond-mat/0310503.

- (7) L. A. N. Amaral, et al., PNAS, 97, 11149–11152 (2000).

- (8) A.-L. Barabási, and R. Albert, Science, 286, 509–512 (1999).

- (9) D. J. Watts, and S. H. Strogatz, Nature, 393, 440–442 (1998).

- (10) E. Revasz, et al., Science, 297, 1551–1555 (2002).

- (11) E. Revasz, and A.-L. Barabási, Phys. Rev. E, 67, 026112 (2003).

- (12) Y. Fujiwara, Physica A, 337, 219–230 (2004).

- (13) Y. Fujiwara, et al., Physica A, 344, 112–116 (2004).

- (14) T. Mizuno, et al., “Statistical laws in the income of Japanese Companies,” in Empirical Science of Financial Fluctuations: The Advent of Econophysics, edited by H. Takayasu, Springer-Verlag, Tokyo, 2002, pp. 321–330.

- (15) H. Aoyama, W. Souma, and Y. Fujiwara, Physica A, 324, 352–358 (2003).

- (16) Y. Fujiwara, et al., Physica A, 335, 197–216 (2003).

- (17) H. Aoyama, Y. Fujiwara, and W. Souma, Physica A, 344, 117–121 (2004).

- (18) R. Pastor Satorras, A. Vázquez, and A. Vespignani, Phys. Rev. Lett., 87, 258701 (2001).

- (19) S. N. Dorogovtsev, et al., Phys. Rev. E, 68, 046109 (2003).