Dynamical Minority Games in Futures Exchange Markets

Abstract

We introduce the minority game theory for two kinds of the Korean

treasury bond (KTB) in Korean futures exchange markets. Since we

discuss numerically the standard deviation and the global

efficiency for an arbitrary strategy, our case is found to be

approximate to the majority game. Our result presented will be

compared with numerical findings for the well-known minority and

majority game models.

: 05.20.-y, 89.65.64, 84.35.+i

: Minority game, Standard deviation, Korean treasury

bond

∗Corresponding author. Tel.:+82-51-620-6354; fax:+82-51-611-6357.

: kskim@pknu.ac.kr (K.Kim).

I Introduction

More than one decade, the minority game is a simple and familiar model that has received considerable attention as one interdisciplinary field between physicists and economists. There has primarily been concentrated on calculating and simulating in various ways for the game theories such as the evolutionary minority game , the adaptive minority game , the multi-choice minority games , the -game model , and the grand canonical minority games. Challet et al have introduced the stylized facts that the stock prices are characterized by anomalous fluctuations and exhibited the fat tailed distribution and long range correlation. Moreover, it reported from previous works that the grand canonical minority game reveal the important stylized facts of financial market phenomenology such as return changes and volatility clusterings. Ferreira and Marsili studied the dynamical behavior of statistical quantities between different types of traders, using the minority games, the majority game, and the -game.

Recently, researchers have treated mainly with Arthor’s bar model, the seller and buyer’s model in financial markets, and the passenger problem in the metro and bus, etc. They have considered several ways of rewarding the agent’s strategies and compared the resulting behaviors of the configurations in minority game theory. De Almeida and Menche have also investigated two options rewarded in standard minority games that choose adaptive genetic algorithms, and their result is found to come close to that of standard minority games. Kim et al analyzed the minority game for patients that is inspired by de Almeida and Menche’s problem.

Recent studies based on approaches of statistical physics have applied the game theory to financial models. To our knowledge, it is of fundamental importance to estimate numerically and analytically the Korean options. In this paper, we present the minority game theory for the transaction numbers of two kinds of KTB in the Korean futures exchange market. For the sake of simplicity, we limit ourselves to numerically discuss the standard deviation and the global efficiency for particular strategies of our model, using the minority game payoff. In Section , we discuss market payoffs and statistical quantities in the game theory. We present some of the results obtained by numerical simulations and concluding remarks in the final section.

II Minority and majority games

First of all, we will introduce the dynamical mechanism of both the minority game and the majority game. We assume that the agents can decide independently whether to buy or to sell the stock at round m. When the information and the strategy take, respectively, the value and at time , the action of the -th agent is presented in terms of . one agent can submit an order (buy) or (sell), and the aggregate value, i.e., the sum of all action of agents, is given by . The payoffs and for minority game and majority game models are, respectively, represented in terms of

| (1) |

and

| (2) |

From the aggregate value , the standard deviation of is defined by

| (3) |

where the bar denotes the average taken over realizations. The statistical quantities and are, respectively, the volatility of and the global efficiency.

To evaluate the statistical quantity , i.e., the ratio of autocorrelation to the volatility, two points of view are characterized as follows: The agents become the fundamentalists, who believe that the stock price fluctuate around the equilibrium value for the case of , included the minority group and the payoff of Eq. . On the contrary, the agents called chartists, who believe that the stock price has a trend followed as , included the majority group and the payoff of Eq. . In the -game, its numerical behavior of the statistical quantities such as the autocorrelation and the volatility are well known to follow the minority game or the majority game.

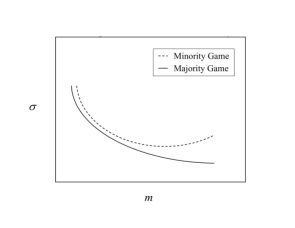

In order to assess the dynamical behavior for the minority game, the majority game, and the -game, we can extend to obtain statistical quantities such as the standard deviation, the volatility, the auto correlation, the self-overlap, and the entropy, etc. We expect that these statistical quantities lead us to more general results. Generally, Fig. shows functional forms for the standard deviation as a function of the round in both the minority game and the majority game.

III Numerical results and concluding remarks

To estimate numerically the standard deviation and the volatility, N agents choose one among two possible options, i.e., or ( buy and sell ) at each round m. The agents obtain the score if the return belongs to be smaller (larger) than zero. The agent’s action behaves independently without any communication or interaction. All available information is other agent’s actions, that is, the memory of the past rounds. There are possible different memories for each of the rounds, and all different strategies is well known to contain values. Our model can extend to several values of strategy, but we limit ourselves to only two strategies and .

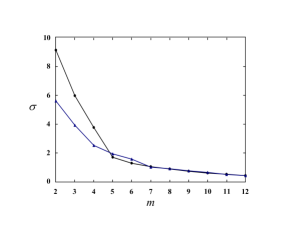

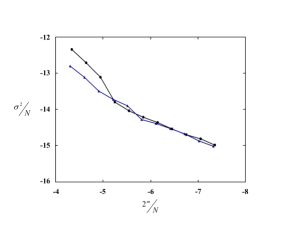

From now, we introduce tick data of KTB and KTB transacted in Korean futures exchange market. We here consider two different delivery dates: September KTB and December KTB. The tick data for KTB were taken from April to September , while we used the tick data of KTB transacted for six months from July . The Korean futures exchange market opens for 6 hours per one day except for weekends, and the total tick data of one-minutely transactions are, respectively, about (KTB) and (KTB). For two kinds of KTB in Korean futures exchange market, we found results of standard deviation versus for the strategy in Fig. , after we estimate numerically the volatility from Eq. . Our result is expected to behavior in a way which is similar to the minority game, but the dynamical behaviors for standard deviation and the global efficiency is found to be similar to the patterns of the majority game. The global efficiency is found to take the decreasing value near zero as the round goes to large value, as shown in Fig. . For , the standard deviation and the global efficiency are also found to take similar values of Figs. 3 and 4.

In conclusions, our case is found to be approximate by the majority game model for two kinds of the KTB and KTB. It is really found that the dynamical behavior of the standard deviation and the global efficiency for our model is similar to those for the majority game while the El Farol bar model and the patient model belong to a class of the minority game. In future, it is expected that the detail description of the minority game theory will be used to study the extension of financial analysis in other financial markets.

Acknowledgements.

This work was supported by Korea Research Foundation Grant(KRF-2004-002-B00026).References

- (1) W. B. Arthur, Amer. Econ. Review 84 (1994) 406.

- (2) D. Challet and Y.-C. Zhang, Physica A246 (1997) 407; Y.-C. Zhang, Peurophys. News 29 (1998) 51.

- (3) R. Savit, R. Manuca and R. Riolo, Phys. Rev. Lett. 82 (1998) 2203.

- (4) D. Challet, M. Marsili and R. Zecchina, Phys. Rev. Lett. 84 (2000) 1824; D. Challet1 and M. Marsili, Phys. Rev. E60 (1999) R6271.

- (5) D. Challet, M. Marsili and G. Ottino, cond-mat/0306445.

- (6) E. Burgos, H. Ceva and R.P.J. Perazzo, Physica A337 (2003) 635.

- (7) L. Ein-Dor, R. Metzler, I. Kanter and W. Kinzel, Phys. Rev. E63 (2001) 066103.

- (8) M. Sysi-Aho, A.Chakraborti and K. Kaski, cond-mat/0305283.

- (9) F. F. Ferreira and M. Marsili, Physica A345 (2005) 657; J. V. Anderson and D. Sornette, Eur. Phys. J. B. 31, 141 (2003).

- (10) D. Challet, M. Marsili and A. de Martino, cond-mat/0401628.

- (11) D. Challet and M. Marsili, Phys. Rev. E68 (2003) 036132.

- (12) P. Jefferies, M. L. Hart, P. M. Hui, N. F. Johnson, Int. J. Theor. Appl. Fin. 3 (2003) 3.

- (13) P. Jefferies, Eur. Phys. J. B20 (2001) 493.

- (14) D. Challet, M. Marsili and Y.-C. Zhang, Physica A294 (2001) 514.

- (15) J. M. L. de Almeida and J. Menche, cond-mat/030818; 0308249.

- (16) K. Kim, S.-M. Yoon and M. K. Yum, Physica A344 (2004) 30.