Statistical Properties of Demand Fluctuation in the Financial Market

Abstract

We examine the out-of-equilibrium phase reported by Plerou et. al. in Nature, 421, 130 (2003) using the data of the New York stock market (NYSE) between the years 2001 –2002. We find that the observed two phase phenomenon is an artifact of the definition of the control parameter coupled with the nature of the probability distribution function of the share volume. We reproduce the two phase behavior by a simple simulation demonstrating the absence of any collective phenomenon. We further report some interesting statistical regularities of the demand fluctuation of the financial market.

Recently a report based on New York stock exchange (NYSE) data between period 1995-1996 ref. Stanley1 reported that the financial market has two phases, namely, the “equilibrium” phase, and the “out-of-equilibrium” phase. Ref. Stanley1 further reported a critical point which is the boundary between a and finite value of the order parameter for the observed phase transition.

In this paper we address the following questions in an effort to understand the observed two phase phenomenon:

-

1.

What is the cause of the observed two phase behavior ?

-

2.

Do large changes of price occur in out-of-equilibrium phase ?

Our study is based on the NYSE Trades and Quotes (TAQ) database for the period 2001–2002 which records every ask, bid, and transaction price.

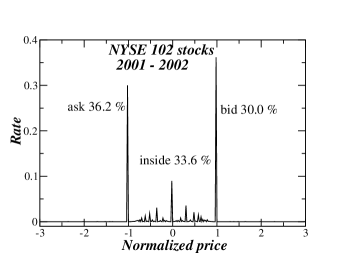

Figure 1 gives an estimate of the percentage of transactions during the period period 2001–2002 that was either at the ask price (scaled to be 1), at the bid price (scaled to be -1), or at an intermediate value between the ask and the bid prices.

Using the method of ref. Stanley1 we first identify a buyer initiated or a seller initiated transaction by a quantity which is defined as follows:

| (1) |

where is a transaction price. Usually a transaction is executed when a new quote hits the lowest ask price or the highest bid price.

As in ref. Stanley1 , we define the volume imbalance and its standard deviation as

| (2) |

| (3) |

where is the share volume of the th transaction within the period .

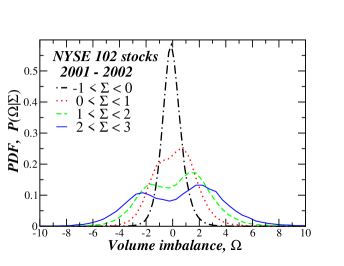

Fig. 2 displays the probability density function (PDF) of for a given . We observe a bi-modal PDF with two extrema when is larger than a critical value. This feature of is reported as an instance of two phase behavior in the financial market [Fig. 1 (a)of ref. Stanley1 ].

We next accumulate the between intervals and to estimate a quantity which measures the number imbalance between buyer and seller initiated trade within the time interval .

The first moment of is defined as

| (4) |

where represents an average in the time interval .

We also define

| (5) |

which measures the average volume of trade per transactions between and .

We estimate , and averaged over 102 stocks which has the largest total volume among all NYSE stocks in 2002 with minutes. 111 Because the second moments of and are expected to diverge, they were scaled in order that first moments, and are equal to 1. Where, means an average over whole period per each stock..

In phase transitions observed in physical systems, the control parameters are independent variables. But in ref. Stanley1 , the control parameter is the magnitude of fluctuation of the order parameter . When fluctuations are large, the underlying PDF of the random variable is wide, leading us to think that we might replicate by simulation.

First we evaluate the empirical correlations present in the database between different variables defined in eq. 1–5. Table 1 tabulates the estimated correlations.

| 1.00 | 0.10 | 0.20 | 0.11 | 0.11 | |

| - | 1.00 | 0.03 | 0.01 | 0.50 | |

| - | - | 1.00 | 0.69 | 0.14 | |

| - | - | - | 1.00 | 0.08 | |

| - | - | - | - | 1.00 |

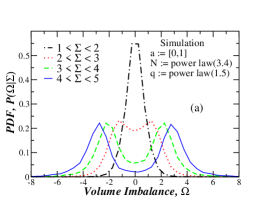

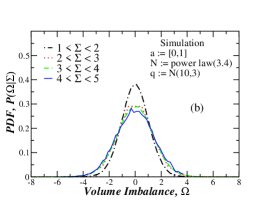

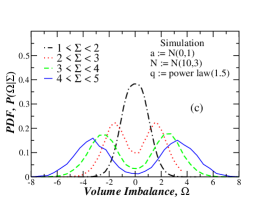

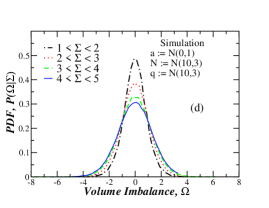

Next, for simulation, we consider , , and to be identically and independently distributed (i.i.d) from two possible PDFs given in Table 2 Stanley2 . We execute the simulation for eight () possible combinations of the set , and .

| random 1,-1 | Normal(0,1) | |

|---|---|---|

| power law | Normal(10,3) | |

| power law | Normal(10,3) |

Since , , and are i.i.d, there are no autocorrelations like that in the TAQ time series, but even then, in we find to have a bi-modal distribution only when the PDF of the share volume is a power law (c.f. Fig 3). This observation can be explained as follows: First note that the PDF of has the functional form of a power law, i.e., . Next note that the has a in its definition, thus the PDF of also has the functional form of a power law. Occurrence of extreme positive and negative events are much more probable when has a fat tail. Since by definition is the standard deviation of the random variable , large values of occur when extreme events (both positive and negative) of are sampled. Thus has two extrema resulting from large positive and negative sampling of the random variable when we choose groups with large values [c.f. Fig. 3(a) and 3(c)].

Table 3 tabulates the estimated correlations between the pairs , , and , for the case of TAQ database and simulation. We find correlation values for the TAQ database and simulation to be statistically similar when and are power law distributed, which further demonstrates that the observed two phase effect is not a signature of hidden collective phenomena within financial market. An explanation similar to the one above is reported in ref. Bouchaud .

| Correlation | ||

|---|---|---|

| TAQ 2000-2001 database | 0.69 | 0.01 |

| Simulation with , | ||

| distributed as in Fig 3a | 0.95 | 0.00 |

| Simulation with , | ||

| distributed as in Fig 3b | 0.08 | 0.03 |

| Simulation with , | ||

| distributed as in Fig 3c | 0.71 | 0.00 |

| Simulation with , | ||

| distributed as in Fig 3d | 0.19 | 0.11 |

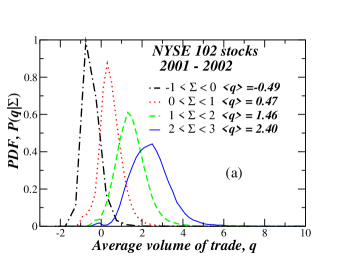

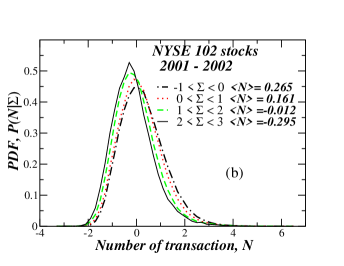

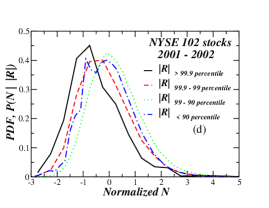

To examine this in closest detail, we next estimate the PDF of and for a given from the TAQ database. Fig.4(a) show, that is large for large . Fig.4(b) shows that is almost independent of . By this, we can infer that the bi-modal PDF is caused by the transactions of large investors with large number of shares. The small decrease in as increases has a simple explanation, which was pointed out by our referee. In normal markets the specialist, whose role is to maintain a fair and orderly market, crosses the book via his clerk very regularly in an almost automated fashion. When fluctuations become large the specialist must take a close look at the electronic order book and at the order from the floor before he may decide which and at what price it is fair to cross the orders. This manual intervention takes time and is a plausible cause of the decrease in the number of trades.

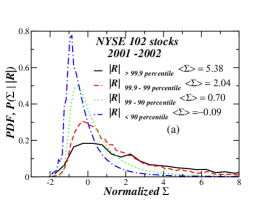

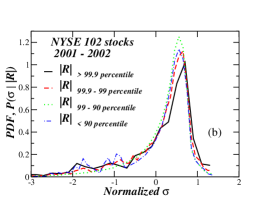

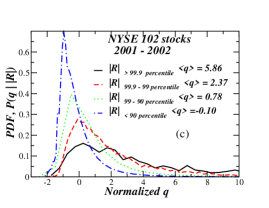

To have a better understanding of how the absolute value of the price fluctuations effects , we next study the PDF for given using the TAQ database. First we sort the database of items ( 102 stocks, 26 terms per a day, about 400 days in two years) with respect to . Next we divided these items into four groups bordered by 99.9 percentile, 99 percentile and 90 percentile. Figure 5 plots the PDF of each of these groups.

We observe that even though is not correlated to or [c.f table 1], the PDF exhibits significant differences among different groups of . This is because rarely occurring large causes large fluctuations but does not significantly contribute to correlation.

In contrast other quantities such as and show there is not so much of a difference. Fig.5(d) again shows the same effect as seen in Fig.4(b) where large fluctuations decrease the number of transactions within a specified time interval.

In conclusion it can be inferred that the “two-phase behavior” as reported in Stanley1 gives no evidence as to whether critical phenomena exist in the financial market or not. The observed out of equilibrium phase is a feature of the power law PDF of the share volume. The absolute value of price fluctuation causes a large fluctuation in the share volume, and large fluctuation of the absolute price causes a decrease in the number of trades in a specified time interval.

We thank S. V. Buldyrev, Y. Lee for helpful discussions and suggestions and K. M thanks the NSF for financial support.

References

- (1) V. Plerou, P. Gopikrishnan, and H. E. Stanley. Nature, 421, 130 (2003).

- (2) X. Gabaix, P. Gopikrishnan, V. Plerou, and H. E. Stanley, Nature, 423, 267 (2003).

- (3) M. Potters. M and J. P. Bouchaud, preprint cond-mat/0304514.