On a possible dynamical scenario leading to a generalised Gamma distribution

Abstract

In this report I present a possible scenario which can lead to the emergence of a generalised Gamma distribution first presented by C Tsallis et al. as the distribution of traded volumes of stocks in financial markets. This propose is related with superstatics and the notion of moving average commonly used in econometrics.

I The -distribution

The -distribution is a general distribution that is verified in processes where the waiting times between variables that follow a Poisson distribution are significant. It involves two free parameters, usually labeled by and and defined as [1],

| (1) |

A special case of -distribution is to consider and . In this case the distribution is called -distribution and represents the probability of get a value of a variable that is obtained by the summation of independent squared variables associated with the Gaussian distribution with null mean and unitary variance [1],

| (2) |

The same form presented in Eq. (1) can be obtained as the stationary solution of the following differential stochastic equation

| (3) |

Considering the Itô convention for stochastic differentials I am able to write the Fokker-Planck equation [2],

| (4) |

whose stationary solution is

| (5) |

with . Performing a simple variable change , it is possible to transform Eq. (5) into Eq. (1) and the Itô-Langevin equation (3)

| (6) |

For a question of simplicity let me represent as . So Eq. (1) will be written as,

| (7) |

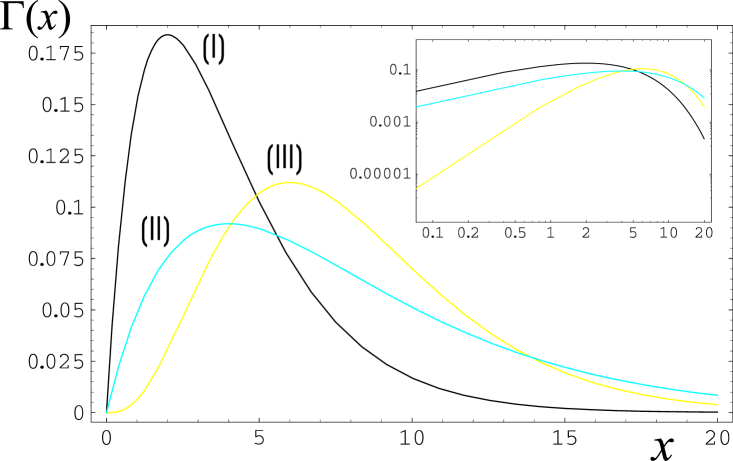

In figure 1 are depicted some examples of distributions.

II Introducing the generalised -distribution

Let one now suppose that parameter in Eq. (3) is in fact a stochastic variable on time scale larger than the characteristic time scale . This means that is, for this case, a conditional probability density function . If the random process for is associatd with a SPDF, , then the SPDF for variable, , is simply given by

| (8) |

Among the various distributions for non-negative variables let one consider that is associated, itself, with a -distribution,

| (9) |

which can be associated to a microscopic equation similar to Eq. (6).

Calculating the integral presented in equation (8) one gets,

| (10) |

Defining and , Eq. (10) can be rewritten as,

| (11) |

| (12) |

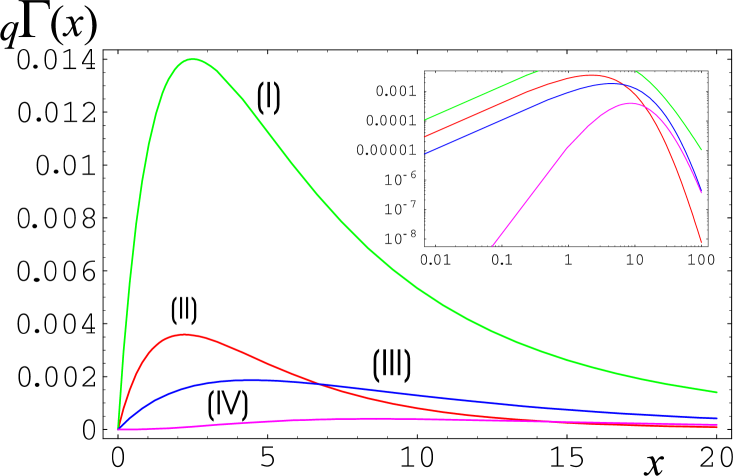

which I will call the -distribution. This kind of distribution was already verified, at least, for the distribution of traded volumes of stocks in financial markets [3]. For the limit , the usual -distribution is recovered, which corresponds to . Some examples of -distribution are presented in Fig. 2,

. The same form is presented in Figs. 7 and 8 of Ref. [3].

This problem of fluctuations in some intensive parameter of the dynamical equation(s) that describe(s) the evolution of a system [4] was recently studied by C. Beck in the context of Langevin equation with fluctuating temperature [5] and extended together with Eddie G.D. Cohen [6] who defined it as superstatistics (a statistic of statistics). This superstatistics presents a close relation to the non-extensive statistical mechanics framework based on the entropic form [7, 8],

| (13) |

For the problem of the distribution of traded volume of stocks in financial markets the presence of fluctuations in , or the mean value of the scaled variable , it is similar to the problem of the moving average in the analysis of the volatility useful in the reprodution of some empirical facts like the autocorrelation function and the so-called leverage efect, see e.g. Ref. [9].

REFERENCES

- [1] M.V. Jambunathan, Ann. Math. Stat. 25 (1954) 401;

- [2] H. Risken, The Fokker-Planck Equation - Methods of Solution and its Applications, edition, (Springer-Verlag, Berlin) 1989;

- [3] R. Osório, L. Borland and C. Tsallis, Distributions of High-Frequency Stock-Market Observables in; M. Gell-Mann and C. Tsallis, Nonextensive Entropy - Interdisciplinary Applications (Oxford University Press, New York, 2004);

- [4] G. Wilk and Z. Włodarczyk, Phys. Rev. Lett. 84 (2000) 2770;

- [5] C. Beck, Phys. Rev. Lett. 87 (2001) 180601;

- [6] C. Beck and E.G.D. Cohen, Physica A 322 (2003)267;

- [7] C. Tsallis, J. Stat. Phys. 52 , 479 (1988). A regularly an updated bibliograhy on the subject is avaible at http://tsallis.cat.cbpf.br/biblio.htm;

- [8] M. Gell-Mann and C. Tsallis, Nonextensive Entropy - Interdisciplinary Applications (Oxford University Press, New York, 2004);

- [9] J. Perelló, J. Masoliver and J.P. Bouchaud, cond-mat/0302095 (preprint, 2003).