Correcting the Minimization Bias in Searches for Small Signals

Abstract

We discuss a method for correcting the bias in the limits for small signals if those limits were found based on cuts that were chosen by minimizing a criterion such as sensitivity. Such a bias is commonly present when a ”minimization” and an ”evaluation” are done at the same time. We propose to use a variant of the bootstrap to adjust the limits. A Monte Carlo study shows that these new limits have correct coverage.

keywords:

confidence intervals, coverage, Monte Carlo, sensitivity, bootstrap, branching ratio, Rolke-Lopez1 Introduction

The standard method for quoting limits of small signals involves finding cuts that eliminate as much background as possible while not reducing the number of signal events significantly. A common measure for the performance of a certain cut set is the sensitivity as discussed in Feldman and Cousins Cousins-Feldman [1] and in Review of Particle Physics Particle Data Group [2]. The sensitivity is defined as the average of the upper limits for an ensemble of experiments all with the same cut set and with no true signal. We adjust this concept by dividing by the detection efficiency and use this ”experimental sensitivity” as our figure of merit. It can be thought of as a measure for the size of an effect that could be discovered by a certain experiment using a certain cut set. The smaller the sensitivity of a cut set, the more likely we are to discover a signal that is truly present.

In recent years researchers have begun to realize that the choice of the optimum cut set should be done ”blind”, that is, it should not be based on the events in the signal region as this tends to bias the results by overemphasizing statistical fluctuations. Instead one obtains an estimate of the level of background in the signal region by either using real events not in the signal region but assumed to have similar characteristics to those in the signal region or simulated background events. We will call this sample of events the background estimator sample.

Unfortunately, even in a blind analysis one is not safe from introducing biases. The one we will consider in this paper stems from the fact that the background estimator sample usually has limited statistics and there exists the possibility of grossly underestimating the background by optimizing on a negative statistical fluctuation. To be more precise, in the first analysis step, which we shall call the minimization step, we choose a cut set by searching through a large number of them and finding the one with the lowest sensitivity. This procedure favors cut sets with low background levels. Having settled on just one cut set we look into the signal region and see how many events are still left after it is applied. Using this number and the estimated background level, the signal limits are found. We shall call this second step the evaluation step. The problem here is that the estimated background level used in the evaluation step is that which resulted from the minimization step which is systematically an underestimate.

This type of bias introduced by combining a minimization and an evaluation step into one procedure is quite common in Statistics. As one example, consider the problem of fitting a parametric curve to a histogram. Here we usually start by estimating the parameters of the parametric function to be fit, for example by finding the estimates of the parameters that yield the lowest . This is the minimization step. Then we want to know whether our fit is sufficiently good, so we proceed to find the confidence level of the statistic. This is the evaluation step. But in fact the , and therefore the confidence level, will be biased because the parameter estimates were chosen to make the as small as possible. In the next section we will give the results of a Monte Carlo study that shows the presence of this type of bias in the search for small signals.

Of course we have known for almost a century how to adjust for this bias in the case of the , namely by adjusting the degrees of freedom of the distribution. Unfortunately, in general it is very difficult to find an analytic correction for this type of bias. In this paper we will propose a numerical method, namely a variant of the bootstrap, for this purpose. The bootstrap was popularized about 15 years ago, and it is fair to say that it has revolutionized Statistics during the last decade. We will give a brief introduction to the bootstrap in this paper, and then we will show how a variation of the bootstrap which we will call the dual bootstrap can be used to adjust for the bias discussed above. Finally, a Monte Carlo is used to study the performance of the dual bootstrap.

2 The Bias

The bias described in the introduction will always be present when a minimization and an evaluation step are combined, but whether this bias is large or small compared to the statistical error is a different question. In the analysis of small signals the end result is typically a confidence limit, either a two sided confidence interval or just an upper limit. Whether or not a method to compute confidence intervals works correctly has to be judged solely based on the true coverage rate of the limits. For example, if we generate data sets from a Poisson distribution with mean and then use some method to compute confidence intervals for for each of these data sets, then at least of these confidence intervals should contain the true value . If two or more methods with correct coverage are available, then one may use other criteria to make the choice of method. For example, in physics one might prefer to use a method that never yields an empty interval, or one might prefer a method that yields on average, the shortest intervals. Such a choice has to made before examining the data, of course.

For discrete distributions (like the Poisson) we have the added difficulty that we can not achieve the desired coverage rate precisely. We will instead require that the true coverage rate be at least as large as the nominal rate for any value of the parameter, even if that will result in overcoverage for many of the values.

We will use the method of Rolke and López Rolke-Lopez [3] to compute the confidence intervals. This is the only published method that treats the uncertainty in the background rate as a statistical error. Like Feldman and Cousins Cousins-Feldman [1] it solves the ”flip-flop” problem, and it always results in physically meaningful limits. Later Feldman and Cousins Feldman2 [4] independently solved the problem of an unknown background rate by proposing a modification to the unified method. The bias problem described here as well as its solution, though, do not depend on what method of computation is used for either the sensitivity or the limits. As long as there is some uncertainty in the background rate the bias would be equally present if we had used for example Feldman and Cousins Cousins-Feldman [1] with their modification or a Bayesian method.

To get an idea of the size of the bias we performed a Monte Carlo study of the analysis of the decay using the data from FOCUS link [5]. One problem in doing this MC is obtaining a large sample of background events. In our study this sample was obtained by assuming the background was due to other particles being misidentified as muons. A large sample resulted from applying all base cuts except for muon identification to a set of real data events. In this sample the events were weighted by the muon misidentification probabilities which had been determined independently. Although this may not be a perfect characterization of the real background, it is good enough to study the question at hand which is more related to the statistics than to the physics. The dimuon signal was generated with the full FOCUS simulation program.

Fake data sets were generated by randomly choosing events from the simulated signal set and events from the background set. For the purpose of this study we chose the number of background events from a Poisson distribution with mean as in the real dimuon data, and was chosen from a Poisson distribution with mean , where was varied from (meaning no signal was present) to . For each value of we generated fake data sets in this manner. To each of these data sets we applied each of cuts. The cuts used for this simulation were the same cuts that had previously been chosen as appropriate for this analysis, that is, each individual cut took on a reasonable range of values. In the next step we found the cut that had the lowest sensitivity. This cut was then applied to the signal region and the Rolke-López method was used to find the corresponding confidence limits. Finally those confidence limits were used to calculate the true coverage rates. To make sure that any observed bias is really due to the minimization-estimation problem, we also randomly chose individual cuts and always applied those same cuts to the fake data. In this case no minimization was done, and hence no bias was expected.

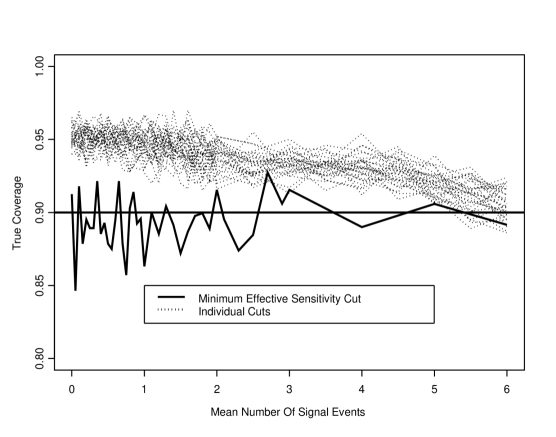

The results of this MC study are shown in figure 1. As expected the limits for the individual cuts have correct coverage, with the true coverage not dropping much below the nominal value of . That a few of the coverage rates on the right side of the graph are below the 0.9 line is due to random fluctuations in the MC as well as the discrete nature of the Poisson distribution. The apparent drop in the coverage rates from the left to the right does not continue, with the rates for larger than all just above . This was verified by running the MC for various values of up to .

Correct coverage is not the only characteristic an optimum methodology should have. It is also important to obtain the strictest limits possible. That is what the minimum sensitivity cut methodology attempts to do but in the limits for these cuts we clearly see coverage rates well below the nominal rate. The graph is based on 15 values for and it would be pure coincidence if the lowest true coverage were obtained for one of those values. Therefore the worst coverage should be expected to be well below the worst one observed of about . We can therefore conclude that we have a sizable bias in our confidence limits due to the minimization-evaluation problem.

3 A Brief Introduction to the Bootstrap

The bootstrap method is a non-parametric alternative for finding error and bias estimates in situations where the assumption of a Gaussian distribution is not satisfied and where it is difficult or even impossible to develop an analytic solution. Note that we are referring to the statistical method and not to the S-matrix bootstrap as used in quantum field theory. In this section we will present the reasoning behind the statistical bootstrap method and how it is applied in practice.

Let us assume we are interested in estimating a certain parameter such as the width of a signal or a branching ratio. Let us also assume that we have observations from a distribution that depends on . Furthermore we have a method for finding an estimate of , say . The estimator might be as simple as computing the mean of the observations or as complicated as fitting a Dalitz plot.

Now, in addition to we will also need an error estimate as well as an idea of the bias in the estimator . If is fairly simple we might be able to find its distribution and get an error and a bias estimate analytically. If the situation is more complicated we might instead try a Monte Carlo study. To do this we would simulate sampling from the distribution , generating many (say ) independent samples of size , apply the estimator to each and thereby get a sample of estimators . Then we can look at a histogram of the estimators, compute their standard deviation, and so on.

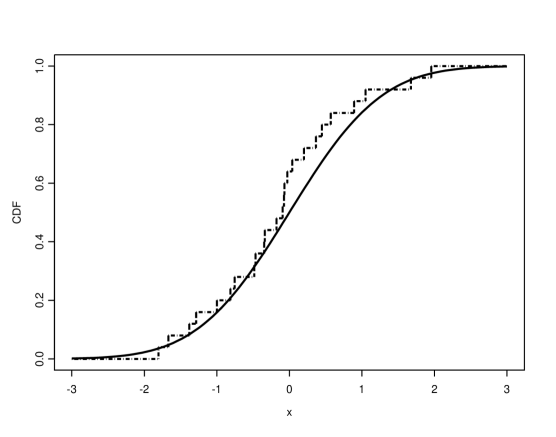

But what can we do if we do not know the distribution ? In that case the data is all we have, and any analysis has to be based on these observations. The best estimate of the distribution function is the empirical distribution function given by , that is the percentage of events smaller than . Figure 2 shows a Gaussian distribution together with the empirical distribution function of a sample of size . The basic idea of the bootstrap is to replace the distribution in the MC study above by its empirical distribution function . How does one sample from the empirical distribution function? It is easy to show that this amounts to sampling with replacement from the observations . So, if the (ordered) observations are , then a bootstrap sample might be . A bootstrap sample has the same sample size as the original data. It might include an original observation more than once (such as in our example) or not at all (such as ). As in the MC study, we will draw many (say ) of these bootstrap samples, apply the estimator to each of them and thereby get bootstrap estimates of . We can then study these bootstrap estimates to get an idea of the error and the bias of .

The bootstrap method as described above was first developed by B. Efron in Efron [6]. Since then a great deal of theoretical work has been done to show why and when the bootstrap method works, see for example Hall Hall [7], and it has been successfully used in a wide variety of areas. Previous applications of the bootstrap in High Energy Physics can be found in Hayes, Perl and Efron Hayes [8] and in Alfieri et al. Alfieri [9]. For a very readable introduction to the subject see Efron and Tibshirani EfronandTibshirani.

4 The Dual Bootstrap and Bias Corrected Limits

The bias observed in section 2 comes from combining a minimization and an evaluation step. We will use a version of the bootstrap to decouple those two steps. One possible solution for this bias problem would be to use a split sample approach: Randomly divide the data set into two pieces, use one part to find the cut with the smallest sensitivity and use the other part to find the limits of the branching ratio. Unfortunately this method has a number of problems: first there is the question how large a portion of the sample should be used to find the best cut. There does not appear to be any theory guiding this choice at this time. Another difficulty in searches for small signals is that we are already working with very few events, and to split those up even further does not seem to be a good idea. Finally the split sample method introduces an additional random error: because we only have very few events in the sideband it might well make a difference whether a specific event ends up in the sample used to find the best cut combination, or whether it gets put into the sample used to find the limits.

All these problems can be avoided if we proceed as follows: we draw one bootstrap sample from the data and find the cut with the smallest sensitivity for this bootstrap sample, then we will draw another bootstrap sample, conditional on the data but independent from the first, to find the limits. This procedure will then be repeated times, with a of about . In this manner we will get lower and upper limits. Finally we will use the median of the lower and the median of the upper limits as our estimates. We use the median because it is less sensitive than the mean to a few unusually large observations. Also, in the case where the signal rate is zero, if even a few of the bootstrap estimates of the lower limit are positive, the mean would also be positive (and wrong), whereas the median is still zero (and therefore correct).

In this way for each bootstrap sample we get a cut set that is optimal for the first bootstrap sample but not necessarily for the second, which is representative of the underlying distribution. We can therefore expect to get unbiased estimates of the limits or, in other words, limits with the correct coverage rate.

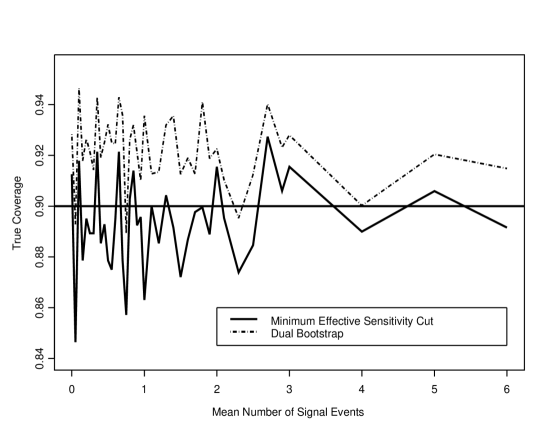

We repeated the MC study discussed in section 2, now using the dual bootstrap method. Figure 3 shows that the dual bootstrap method yields limits with the correct coverage, effectively removing the minimization-evaluation bias. Similar MC studies with different nominal coverage rates and different background rates, both smaller and larger than the rate of shown here, have confirmed this conclusion.

5 Presenting Results

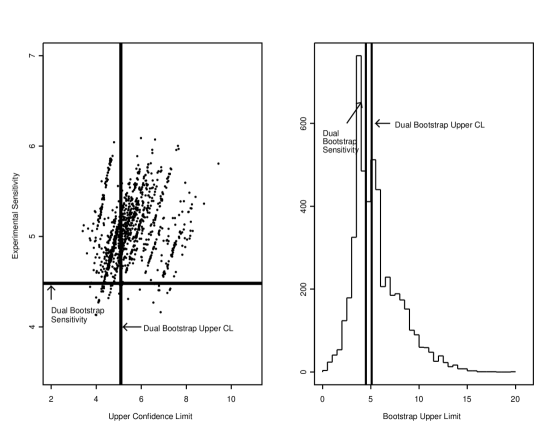

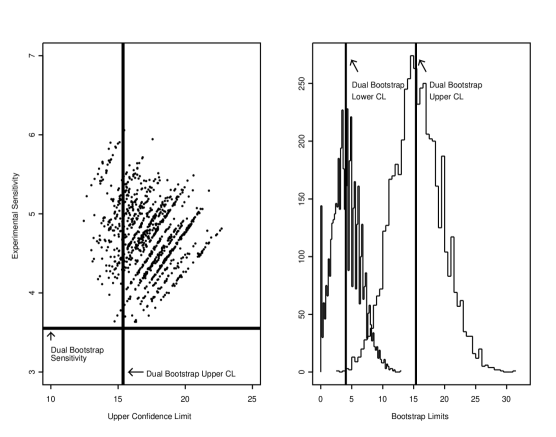

We would recommend to publish two graphs to present the results of a dual bootstrap analysis. On the one hand we suggest a scatter plot of the upper confidence limits versus their experimental sensitivities for each cut combination, together with lines showing the medians of the dual bootstrap upper limits and sensitivities. This graph should show that the quoted results are ”reasonable” when compared to what would have been quoted if only one cut combination had been used, that is, the lines should be inside the range of values from the individual cuts. On the other hand we would suggest to plot the histograms of the bootstrap estimates of the lower and upper limits, so that the reader can get an idea of the variation in those limits. As an illustration we have generated two fake data sets, similar to those used in the simulation study above. In the first case we generated a data set without a signal and then ran the dual bootstrap times. The median bootstrap lower limit is , and so we draw the histogram of the bootstrap upper limits only, together with the median bootstrap upper limit and the median bootstrap sensitivity. The result is in figure 4. In figure 5 we have the results for a data set with a signal rate of . Here we draw both the histograms of the lower and the upper bootstrap limits, together with the corresponding medians.

Another advantage of the bootstrap method is apparent from these graphs, namely that we can get an idea of the variation in the confidence limits and the sensitivities. That confidence limits are themselves random entities and therefore have an error is often underappreciated. These errors can be easily computed from the bootstrap samples, although it would be advisable to use a robust estimate of the standard deviation rather than the usual formula, because the bootstrap estimates are clearly skewed to the right. A good estimator of the error would be the interquartile range, defined by percentile - percentile)/. The constant here makes the interquartile range equivalent to the standard deviation in the case of Gaussian data. These errors might be useful in comparing and combining the confidence intervals of different experiments.

6 Claiming a Discovery

An important issue is the question on how to decide whether one should claim a discovery. From a statistical point of view this should be done by performing a hypothesis test with the null hypothesis :”There is no signal present”. Because of the duality of confidence intervals and hypothesis tests we can actually do this by simply finding confidence intervals with the appropriate , say . corresponding to a effect or . corresponding to a effect, and deciding that a signal is real if the lower limit is greater than . By running the dual bootstrap with a variety of ’s we can even get an estimate of the size of the effect, or what is called a p-value in statistics, namely the probability of claiming a signal when there really is none. As an example consider one the data sets used in our simulation study. This data set was generated with a signal rate of . The dual bootstrap estimate of the lower limit was for and for , based again on bootstrap runs. By equivalence to confidence intervals from a Gaussian distribution this amounts to a effect.

If a signal is present, an obvious estimator for the signal rate is the maximum likelihood estimator , where is the number of events in the signal region, is the number of background events, is the size of the background region relative to the size of the signal region and is the detection efficiency of the cut. Of course this estimate suffers from the same cut-selection bias, and would generally lead to estimates of the signal rate that are too large. Again we can use the dual bootstrap method to adjust for this bias, by computing for each dual bootstrap sample and using the median as the point estimate.

7 Conclusion

We have shown that selecting a cut set based on the smallest sensitivity and then using it to find the limits of the branching ratio (or generally of any other quantity) introduces a bias. In the case of the decay in FOCUS a MC study indicates that this bias is quite large, certainly too large to ignore. It is reasonable to assume that a sizable bias is present whenever the minimization criterion is related to the evaluation criterion, for example if both are related to the signal to noise ratio. We have developed a method based on the bootstrap technique from Statistics that corrects for this type of bias. A MC study for the decay shows that this new method performs very well. Showing the histograms of the bootstrap samples together with the median also gives an idea of the variation in these estimates.

FORTRAN routines for the dual bootstrap method as well as for computing the Rolke-López limits are available from the authors by sending an email to w_rolke@rumac.uprm.edu.

8 Acknowledgements

We would like to thank Daniel Engh of Vanderbilt University for suggesting the scatter plot which is very useful for presenting the results.

References

- [1] R.D. Cousins, G.J. Feldman, ”A Unified Approach to the Classical Statistical Analysis of Small Signals”, Phys. Rev, D57, (1998) 3873.

- [2] C. Caso et al. (Particle Data Group), Eur. Phys. J. C 3, 1 (1998) 177.

- [3] W.A. Rolke, A.M. López, ”Confidence Intervals and Upper Bounds for Small Signals in the Presence of Background Noise”, Nucl. Inst. and Methods A458 (2001) 745-758

- [4] G. Feldman, ”Multiple measurements and parameters in the unified approach”, talk at Fermilab Workshop on Confidence Limits 27-28 March, 2000, http://conferences.fnal.gov/cl2k/ , p.10-14.

- [5] J. M. Link et al., Proceedings of Heavy Quarks at Fixed Target 1998, AIP Conf. Proc. 459, eds. H. W. K. Cheung and J. N. Butler (1998) 261

- [6] B. Efron, ”Bootstrap methods: another look at the jacknife”, Ann. Statistics, 7, (1979) 1-26.

- [7] P. Hall, The Bootstrap and Edgeworth Expansion, Springer Verlag, (1992)

- [8] K.G. Hayes, M. L. Perl, B. Efron, ”Application of the Bootstrap Statistical Method to the Tau Decay Mode Problem”, Phys.Rev. D39: (1989) 274

- [9] R. Alfieri et al., ”Understanding stochastic perturbation theory: toy models and statistical analysis”, hep-lat/0002018 (2000) B. Efron, R.J. Tibshirani, An Introduction to the Bootstrap, Chapman & Hall, (1993)

9 Appendix