Heat kernel expansion for a family of stochastic volatility models : -geometry

Paul Bourgade, Olivier Croissant

Ixis-CIB, fixed income quantitative research111The views herein are the authors’ ones and do not

necessarily reflect those of Ixis-cib.

(e-mail: pbourgade@ixis-cib.com, ocroissant@ixis-cib.com)

Abstract. In this paper, we study a family of stochastic volatility processes; this family features a mean reversion term for the volatility and a double CEV-like exponent that generalizes SABR and Heston’s models. We derive approximated closed form formulas for the digital prices, the local and implied volatilities. Our formulas are efficient for small maturities.

Our method is based on differential geometry, especially small time diffusions on riemanian spaces. This geometrical point of view can be extended to other processes, and is very accurate to produce variate smiles for small maturities and small moneyness.

Key words : SABR, Heston, stochastic volatility, smile, heat kernel expansion, Molchanov’s theorem, first and second variation formulas, -geometry.

Mathematics subjects classification : 58J65

JEL classification : G13

References

1. Berestycki Henri, Busca Jérôme and Florent Igor, Computing the Implied Volatility,

Communications on Pure and Applied Mathematics, Vol. LVII, 0001-0022 (2004).

2. Bost Jean Benoit, Courbes elliptiques et formes modulaires, lecture at École Polytechnique.

3. Bourguignon Jean Pierre and Deruelle Nathalie, Relativité générale, lecture at École Polytechnique.

4. Carr Peter and Madan Dilin, Towards a theory of volatility trading, Volatility, ed. R.A. Jarrow, Risk Publications.

5. El Karoui Nicole, Modèles stochastiques en finance : finance, lecture at École Polytechnique.

6. El Karoui Nicole and Gobet Emmanuel, Modèles stochastiques en finance : introduction au calcul stochastique, lecture at École Polytechnique.

7. Gatheral Jim, Stochastic Volatility and Local Volatility, Case Studies in Financial Modelling Course Notes,

Courant Institute of Mathematical Sciences, Fall Term, 2004.

8. Hagan Patrick S., Kumar Deep, Lesniewski Andrew S. and Woodward Diana E., Managing Smile Risk.

9. Hagan Patrick, Lesniewski Andrew, Woodward Diana, Probability Distribution in the SABR Model of

Stochastic Volatility, preprint.

10. Hagan Patrick S. and Woodward Diana E., Equivalent Black Volatilities,

Applied Mathematical Finance 6, 147-157 (1999).

11. Henry-Labordère Pierre, A General Asymptotic Implied Volatility for Stochastic Volatility Models,

preprint.

12. Hsu Elton P., Stochastic Analysis on Manifolds, American Mathematical Society vol. 38,

Graduate Studies in Mathematics, 2001.

13. Jost Jûrgen, Riemannian Geometry and Geometric Analysis, Springer Universitext, 2002.

14. Karatzas Ioannis , Shreve Steven E., Brownian Motion and Stochastic Calculus, Springer.

15. Lang Serge, Fundamentals of Differential Geometry, Springer.

16. Milnor J., Morse Theory, Annals of Math. Studies, Princeton University Press (1963).

17. Minakshisundaram and Pleijel,

Some properties of the eigenfunctions of the Laplace-operator on Riemannian manifolds,

Canadian J. Math. 1 (1949), 242-256.

18. Molchanov S. A., Diffusion Processes and Riemannian Geometry, Russian Math. Surveys 30 : 1 (1975).

19. Pansu Pierre, Cours de géométrie différentielle, département de mathématiques d’Orsay.

20. Tyner David R., Applications of variational methods in Riemannian geometry, department of mathematics and statistics,

Queen’s University, Kingston.

Introduction

In this note, we consider the following process222In the first chapter, with generalities about stochastic volatility problems, we will understand why we consider this particular process with stochastic volatility :

| (1) |

-

•

for , and we get the SABR model;

-

•

for and we get Heston’s model.

A direct application of Feller’s criterion333see Ioannis Karatzas, Steven E. Shreve, Brownian Motion and Stochastic Calculus, Springer., detailed in appendix 1, shows that for there is no explosion for the stochastic volatility, that is to say

This result remains true for if we add the condition .

We suppose in the following that we are in such cases.

Let us write be the density of probability to get to the point , leaving from the point after a time . Then follows the classical differential equation (where and should be adjusted444Jim Gatheral, Stochastic Volatility and Local Volatility, Case Studies in Financial Modelling Course Notes, Courant Institute of Mathematical Sciences, Fall Term, 2004.)

| (2) |

The goal for this note is to get suitable approximations for the -model, for small . There are three steps to get them.

-

•

We first explain how to convert our stochastic problem into a geometrical one. We introduce the Laplace Beltrami operator to have a geometric point of view, and then use a suitable isometry to work in a simpler space, called the -space.

-

•

Thanks to this geometric point of view, we then give a first-order asymptotics for the probability density . Moreover, we want this expression to be computed for all and without having to calculate any integral. The main tool for this part is Molchanov’s theorem555S. A. Molchanov, Diffusion Processes and Riemannian Geometry, Russian Math. Surveys 30 : 1 (1975)..

-

•

The third one is to get a first order (in ) approximation for :

-

–

the transition probability from to , where we integrate over because the final volatility is not observed :

This gives us the price for digital options.

-

–

the implied volatility , defined by the equality of the prices of calls for (1) and a Black-Scholes model with volatility :

Actually, we first give an approximation for the local volatility (defined by ) and then use Hagan’s loc/imp formula666Patrick S. Hagan and Diana E. Woodward, Equivalent Black Volatilities, Applied Mathematical Finance 6, 147-157 (1999)..

-

–

Such approximations are given in literature for the SABR model, that is to say . The most successful closed form formula giving an approximation for options is Hagan’s777Patrick S. Hagan, Deep Kumar, Andrew S. Lesniewski and Diana E. Woodward, Managing Smile Risk.. In a preprint888Patrick Hagan, Andrew Lesniewski, Diana Woodward, Probability Distribution in the SABR Model of Stochastic Volatility. Andrew Lesniewski uses a geometrical method (in the hyperbolic plane) to get the density’s asymptotics, but he uses a Dyson formula instead of Molchanov’s theorem. Consequently our results are sensibly different.

Berestycki999Henri Berestycki,

Jérôme Busca and

Igor Florent, Computing the Implied Volatility, Communications on Pure and Applied Mathematics, Vol. LVII, 0001-0022 (2004)

©2004 Wiley Periodicals, Inc. gives an evolution equation for the smile. His PDE is generally difficult to solve

and hides the geometrical aspect of the problem. This is the reason why, for our -model, we do not try to use the available PDE and directly calculate the first order.

Chapter 1 A geometrical view of stochastic volatility problems

We consider the following general process,

with . We call the transition probability density, from a state to a state . Then the backward Fokker Planck equation can be written

The Laplace Beltrami operator is defined as

for a metric . If we consider the upper half-plane with metric

then we have

where is a first-order operator. In order to apply Molchanov’s theorem111and more generally Minakshisundaram-Pleijel recursion formula., we need to be able to calculate the geodesics of the space with metric

The purpose of this chapter is to understand the sufficient conditions for the geodesics to be easy to calculate.

1.1 The isometry

In order to be able to calculate the geodesics easily, we look for a suitable isometry. We impose the -coordinate to be stable (simpler case to keep the upper half-plane stable), so we look for an isometry on the form

Then is diagonal iff

We then have

For to be well defined, the following condition is necessary :

Interesting special cases are for and, more generally for not dependant on .

1.2 Special cases

In this part, we consider special cases showing the interest of this geometrical formulation. The first one confirms results about non-stochastic volatility models. The second one gives a condition on and for both horizontal and vertical lines to be geodesics, which is a very useful case. Finally, the third one shows that the -model is the only -separable model for which we have the homogeneity property.

-

•

(no stochastic volatility) : then the geodesical distance between and is infinite, except if , so the probability of transition is concentrated on this line of the plane : . Varadhan’s theorem in dimension one then gives

-

•

we want to find an isometry between and a simpler space . The most interesting is a function such as

because we then have

However, to find a convenient function , the partial derivatives must follow Schwarz’s theorem of commutation (Poincaré’s criterium for the differential to be exact). This is the case iff does not depend on . So this case is simply not pertinent222However, one can imagine new models where depends on , which seems quite natural. To be able to calculate the geodesics, we then need the relation (), which just necessitates well chosen functions. Moreover, the relation () gives interesting qualitative results : if the correlation is positive, then the volvol decreases with ; the contrary if the correlation is negative..

-

•

if only depends on , then with Schwarz’s relation one can easily check that the function is separable : let us write . Then we also want to find an isometry between and a simpler space . The good function is such as

because we then have

Schwarz’s commutation relation is now true, so we really defined an isometry. We now just need to be able to calculate geodesics in the space . First notice that the metric does not depend on the coordinate , so, using Killing Fields, a system of equations for the geodesics is

with . Thanks to this system, one can check that we have the homogeneity property (if is a geodesic, so is ) iff on the upper half-plane333 Indeed, we have such homogeneity for every geodesic iff the following system is satisfied for every and in (we also suppose that the functions and are strictly positive and on ) : This implies that we also have , so we only need to show that is a power. Moreover, as , we have , so we only need to show that is a power. For , we have , so . The following is straightforward : we also have for , so, as is dense in and is continuous, we have for . If , we then have . For , we also have . As is at , we have , so , and can be written . .

1.3 Summary

Proposition. We consider all isometries of the upper half-plane which are identity for the -coordinate. Then :

-

•

if we want the resulting metric to be diagonal and only -dependant, then must be separable (). One then can effectively find a suitable isometry and the resulting metric is given by If the geodesics follow the homogeneity property, then the only suitable metric is

-

•

one can find other isometries giving the following simpler metric : This necessitates the dependance (so this is not exactly a stochastic volatility model) and the equation .

Chapter 2 The -model : geometrical formulation

In order to have a geometrical vision of the situation, we first change the variables and the function (approximately like in Lesniewski’s preprint111Andrew Lesniewki, Probability Distribution in the SABR Model of Stochastic Volatility, preprint), writing :

-

•

;

-

•

;

-

•

;

-

•

;

-

•

;

-

•

.

Now the Green function, solution of the PDE (2), is solution of the following system (where we have and ):

| (1.1) |

In this part, we first rewrite the PDE (1.1) in terms of the Laplace

Beltrami operator of a suitable space (the important properties of this operator are summarized in appendix 2).

We then use an isometry that

allows us to consider a simpler generic space. Our results are

summarized in a final table.

2.1 Suitable form for the partial differential equation

The metric associated with the PDE (1.1) is

We call the corresponding Riemannian space . We also need the determinant of and the inverse matrix :

The Laplace Beltrami operator is defined as

A simple calculation gives . This is the reason why (1.1), with the suitable normalized initial condition, can be written as

| (1.2) |

with

| (1.3) |

and . The interest of this formulation is that we have separated the intrinsic Laplacian from the first-order term (without changing variables like in Hagan’s paper222Patrick S. Hagan, Deep Kumar, Andrew S. Lesniewski and Diana E. Woodward, Managing Smile Risk.).

2.2 The isometry

We follow here the general methodology of the chapter 1. Let us introduce , the -space with metric

Let us be the application of the upper half-plane

where is a positive constant. Then the jacobian matrix of is

so one can easily check that between the metrics the following relationship holds :

This relationship exactly means that conserves the scalar product : in , for two trajectories and crossing in at ,

.

This local property implies the global result that induces an isometry between and .

The following paragraphs are quite technical : in order to simplify our problem, we find a diffusion equation in equivalent to the one in . We then find the relations between the transition probabilities associated to these diffusion equations.

2.3 Reformulation of the hyperbolic problem

We now consider the following Green problem in :

| (1.4) |

with :

-

•

;

-

•

the Laplace Beltrami operator corresponding to the Riemannian space , therefore ;

-

•

.

If is a solution of (1.4), then is a solution of (1.3) (, which is a normalization constant, is written in the following). Indeed, as does not modify the time ,

Thanks to the normalization constant , follows the condition at , so from the uniqueness of the solution of (1.3) we deduce that

| (1.5) |

2.4 From density to probability of transition

The quantity is a density with respect to the euclidean metric. To be consistant with the next chapter, we now note the corresponding density probability with respect to the metric :

We have then

where is the image of the straight line by the application , that is to say the straight line with equation

So if we define

| (1.6) |

then

In the following we will need the expression of the moment of order of , that is to say

| (1.7) |

If we define

| (1.8) |

then the same calculation as above gives

Here is a table that summarizes the results of the first part.

| From to | ||

|---|---|---|

| The space | ||

| The metric | ||

| The isometry | ||

| The LBO | ||

| The first-order operator | ||

| The diffusion equations | ||

| Link between and | ||

| The transition probability | ||

| The moment | ||

All relationships above imply that we just need to get a suitable approximation for . This is the purpose of the next chapter.

Chapter 3 From Molchanov’s theorem to the -model

We have shown in the previous part that it is sufficient to calculate all probability densities in , the -space. This can be done thanks to the following theorem, expressed in terms of geometric invariants. The necessary calculations and adaptations to the space will be done after.

3.1 Molchanov’s theorem : the 0-order expansion

Molchanov’s theorem gives an asymptotic behavior for the density transition function, for small maturities. More precisely, we use the following notations :

-

•

is the dimension of the space;

-

•

is a specified metric of a space ;

-

•

is the Laplace-Beltrami operator corresponding to the metric ;

-

•

is a first-order operator;

-

•

is the density function (with respect to the element of volume ) corresponding to the diffusion process with initial condition : represents the probability density of getting in , leaving from , after a time , for the metric .

Supposing sufficient conditions of regularity (uniqueness of the geodesic between two points…), we can now formulate the theorem we need.

Molchanov’s theorem. Under all the conditions above, if is the distance between and along the unique geodesic linking them, , then with • where a cone of light from with a solid angle illuminates an area on the geodesic hypersurface orthogonal to at (cf the following figure); • : this is the work of the field along the geodesic.

Proof. A complete proof can be found in Molchanov’s article111S. A. Molchanov, Diffusion Processes and Riemannian Geometry, Russian Math. Surveys 30 : 1 (1975).. However, one can give an intuition of this result if there is no first-order operator, by analogy with the euclidean case.

For a flat space, the above formula is clearly true, and for a curved space the density naturally decreases with , where is the initial angle between geodesics leaving . Indeed, imagine a diffusion in this space, materialized with particles. The particles are diffused in an isotropic way from , and they remain blocked between the geodesics, so is analogous to a one-dimension diffusion density with a density in .

This does not leads us to the exact formula (because particles come from the other side of ), but it

gives an intuition of the origin of the function .

From a computational point of view, we need a definition of relatively to coordinates. Let be a base of the orthogonal to in . Let us (, ) be the Jacobi field222see Jûrgen Jost, Riemannian Geometry and Geometric Analysis, Springer Universitext, 2002. along such as and , and . Then

Indeed, represents the area engendered by a polyhedra of sides , so represents the infinitesimal area engendered by the geodesics at time , fo a solid angle . ∎

What we will need in reality is both of the following corollaries.

Corollary 1 : dimension 2 (for the -model). In the plane, we consider the following system, where is the Gauss curvature for the point of the geodesic linking and . Then

Proof. We only need to show that the the evolution of the length of the unique vector of is governed by the equation above. The evolution equation for a Jacobi field is

for each of the composants , where :

-

•

is the Riemann tensor;

-

•

is a base of the orthogonal hyperplane of at ;

-

•

is the parallel transport of along relatively to the field ;

-

•

is the composant of the Jacobi field on .

We also know that the parallel transport relatively to transforms in the orthogonal of , with norm , written . So the evolution equation can be written, in dimension 2,

From the definition of the Gauss curvature, , which completes the proof. ∎

Corollary 2 : dimension 2 and constant Gauss curvature (for the -model with : SABR). If the plane has a constant gaussian curvature , then

Proof. Immediate from the corollary 1. ∎

3.2 The first-order expansion

We can get a better approximation for the probability density . Indeed, one can show that for a sufficiently regular diffusion and space, admits the following expansion333see Elton P. Hsu, Stochastic Analysis on Manifolds, American Mathematical Society vol. 38, Graduate Studies in Mathematics, 2001, theorem 5.1.1 p.130., for any :

Our purpose is to give the equation verified by in the case of the geometry, and then evaluate its solution for a point near from .

The expansion above can be written at first order as

| (2.1) |

Injecting (2.1) in the diffusion equation , we successively get the following diffusion equations satisfied by the functions , and , for the diffusion in the space :

| (2.2) | |||||

| (2.3) | |||||

| (2.4) |

Here , and reference respectively the euclidean norm, the euclidean scalar product and the euclidean gradient (), and . These equations need some comments :

-

•

(2.2) just traduces that ;

-

•

(2.3) is a transport equation that can be solved by integration along the geodesic : the explicit solution is given by Molchanov’s theorem :

-

•

(2.4) is also a transport equation, that can be solved by integration along lines directed by instead of : the knowledge of the geodesics is not sufficient anymore. This is the reason why we will just calculate its initial value (), which will be a sufficient correction for us in the following.

A great calculation (see appendix 2.3) gives us the following result for :

The main result of this part is then the following expansion, in the -space :

with :

-

•

the functions and computed in , thanks to the homogeneity property of the -space (cf. appendix 2.4);

-

•

the function easily computed as the integral of a known function along a known path.

-

•

given by the formula above.

Remark 1. When , our result for is a special case of a general formula : in any riemannian space we have

where is the scalar curvature.

Remark 2. A formula by Minakshisundaram and Pleijel444S. Minakshisundaram and Pleijel, Some properties of the eigenfunctions of the Laplace-operator on Riemannian manifolds, Canadian J. Math. 1 (1949), 242-256. gives a general asymptotic expansion for to any order, but it is too complex and non effective for the second order.

Chapter 4 Applications of the previous asymptotics

In this chapter, we integrate the asymptotic expression obtained previously. This leads directly to digital option prices.

Then, using Hagan’s local volatility formula111Patrick S. Hagan and Diana E. Woodward, Equivalent Black Volatilities, Applied Mathematical Finance 6, 147-157 (1999)., we compute, through equivalent local volatility, vanilla option prices.

4.1 The Laplace transformation

We want to evaluate and defined by (1.6) and (1.8). We use here a Laplace expansion of order 2 : for and sufficiently regular functions, and with minimum at and non-zero second derivative, we have

In the case of and we need to calculate the ordinate of such as is minimal. This is done in appendix 2.5.

Unfortunately, we are unable to calculate the third and fourth variations of for any strike, but this can be done for , at the money; including these results in the 1-order term above will be sufficient : the effect of the 1-order correction is more important a the money.

To sum up, we will take the following approximation for :

with the following formulas :

-

•

where the sign depends on the following configurations.

This second variation for the -model is the most important result of this part because it gives the leading order for pricing the digital options.

-

•

;

-

•

;

-

•

These results are justified in appendix 2.5.

4.2 The transition probability : pricing digital options

All the previous results give a methodology to calculate the transition probability for any . For instance, in the case , the explicit calculations are done at the end of this paragraph. What is done here for can be done for any : the trajectories of -geometry and the Jacobi fields calculations are given in appendix.

4.2.1 Calculation of the field and its work

If ( : the case , needed for Heston’s model, can be handled apart, the same way), the function has the following inverse,

Moreover,

From -geometry, we know that the hyperbolic space (ie the case ) has constant Gauss curvature : this specificity makes all its interest, we can apply the corollary 2. We know that geodesics are circles, so . We can then calculate explicitly the work of on these circles. Simplifying by , we get

This expression does not depend of the choice of time, which is normal for the work of a field on a trajectory.

4.2.2 The 1-order expression of : the SABR case

We first need a primitive (in ) of the function

We will note it as . An explicit formula for is

We then have

where the first-order term has been calculated thanks to the previous variations. The notations are given in the following.

4.2.3 Graphics

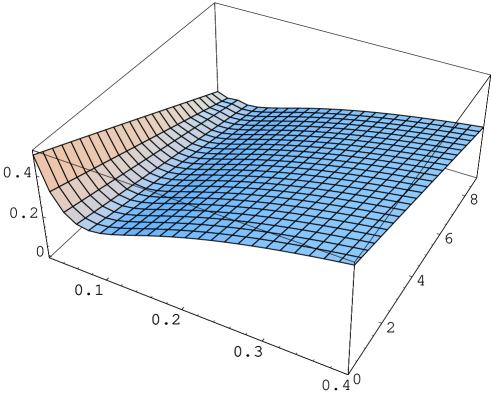

In the SABR case, here are the evolution of the transition probability and an example of a digital option that we got.

![[Uncaptioned image]](/html/cs/0511024/assets/x1.png)

![[Uncaptioned image]](/html/cs/0511024/assets/x2.png)

The 1-order expression for seems to be relevant approximatively for , as shown in the following graphic : for , the 0-order expression is more stable : it remains aproximatively a distribution function, whereas the first-order does not.

4.3 The implied volatility

4.3.1 The local volatility : first order asymptotics

Local volatility can be defined as

In the case of the -model, (1) implies that

If we introduce the transition function , then a simple consideration such as (except that we reason here with densities and zero-probability events) shows that

| (2.4) |

where

-

•

is the marginal probability distribution;

-

•

is the conditional moment of order .

At the leading order and have almost the same asymptotic expansion (as we can see with a saddle point method) :

| (2.5) |

with :

-

•

;

-

•

;

-

•

the point of the straight line with equation

minimizing the distance to the point .

We can conclude with (1) and (2) that

Unfortunately, we don’t have a closed form for the distance from a point to a straight line in any -space. However, we can express in terms of a new 2-arguments function.

For this, imagine the following problem. In a -space, a rocket is thrown perpendicularly to a straight line and crashes on another one. Then we define

The function is well-defined because if is a geodesic, so is

If we take and such as

-

•

,

-

•

,

then

If (no stochastic volatility), one can check that we have the expected value

4.3.2 From local to implied volatility

The previous calculation made it possible to transform the original stochastic volatility problem in a local volatility problem.

This is the reason why we can use a formula established by P. Hagan222Patrick S. Hagan and Diana E. Woodward, Equivalent Black Volatilities,

Applied Mathematical Finance 6, 147-157 (1999)..

Hagan’s formula. For a process , the log-normal implied volatility, at leading order in , is given by

with usually and .

We now consider that for us can be replaced by . Indeed, for small times

if is defined by

Rather than , one should take, for small times,

Indeed this is the value that we got for a log-normal model () (see appendix 3).

Remark. Pierre Henry-Labordère gave a different formula for the implied volatility smile333Pierre Henry-Labordère, A General Asymptotic Implied Volatility for Stochastic Volatility Models, preprint..

4.3.3 Smiles

The formulae above give us the exact asymptotic value of the smiles for :

with :

-

•

;

-

•

;

-

•

.

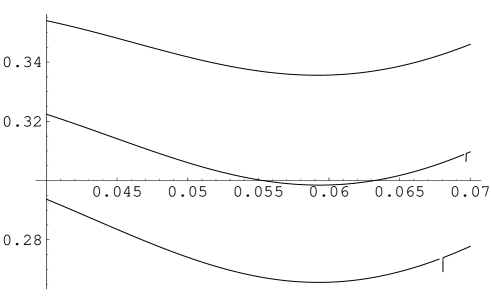

For different values of , we get for instance the following smiles (Fig 3.4).

With all the previous results, one also can compute a first-order (in ) approximation of the smiles, which gives for example the following evolution (Fig 3.5).

Chapter 5 Appendix 1 : conditions for non-explosion of the volatility

Let us first remind Feller’s Test for Explosions. We consider a process

on a segment of . We suppose that the functions and are Borel-measurable and follow the conditions of non-degeneracy and local integrability :

-

•

;

-

•

;

The scale function is defined, for a constant , as

One can then define the function

The exit time from is

We now can write the theorems we need111For a demonstration,

the reader can read Ioannis Karatzas, Steven E. Shreve, Brownian Motion and Stochastic Calculus, Springer..

Proposition 1. If a process follows the conditions above, with , then

-

•

if and then : the process is recurrent;

-

•

if and then ;

-

•

if and then ;

-

•

if and then ;

Proposition 2 : Feller’s Test for Explosions. If a process follows the conditions above, with , then

The case that interests us is

with and . We will apply Feller’s test successively for and , then and .

5.1 If and

We have

We then have

We will look for equivalents of or in the following cases, to apply the proposition 1 or 2.

If

In this case, one can write

because , which is integrable in 0. So we have : by proposition 2 .

If

An analogous calculation as above gives , so there is no explosion in a finite time. However, if (no mean reversion) we have . If , and , so by proposition 1 the process is recurrent.

If

We now have

for large enough. So . In , we have, if ,

So, in this case : . If , then

which is integrable in . So, in this case, .

Moreover, one can check that for , we are in the first case of proposition 1, so the process is recurrent.

5.2 If or

Simple calculations (where logarithms appear) show that, for these limit cases:

-

•

for there is no explosion and the process is recurrent;

-

•

for there is no explosion if and only if ; in such a case the process is recurrent.

5.3 Summary

The cases for which there is no explosion and/or limit for the process are :

-

•

with mean reversion;

-

•

with .

From a practical point of view, we consider in our note the case with no condition on , and , because our asymptotics are given for short times : the cases of explosions in the interval would be very pathological.

Chapter 6 Appendix 2 : -geometry

In this part, we recall some useful results of Riemannian geometry, and we apply it to the special case or the upper half plane () with the metric

with . We will be particularly interested in the cases and .

6.1 Generalities about Riemannian spaces

In this section, we note the coefficients of a metric , and we will use Einstein’s summation conventions.

6.1.1 Christoffel symbols

The Christoffel symbols are defined as

6.1.2 Curvatures

The Riemann tensor, the Ricci tensor and the scalar curvature are successively defined by

where , denotes the partial derivative face to . The Gauss curvature is defined in dimension 2 by

that is to say, for and orthogonal vectors with norm 1,

It coincides with the scalar curvature, in dimension 2.

In dimension 2, one can show that

with the determinant of .

6.1.3 Isometries

Let be a function from to , with respective metrics and . Then is said to be an isometry iff for every and in

This global definition is equivalent to the following local condition : for every point ,

6.1.4 Geodesics

Minimization of length

The length of a curve in a Riemannian space , between and , is defined by the integral

which is clearly not dependant of the parametrization.

For sufficiently regular spaces (for instance spaces with scalar curvature always negative, as in -geometry), there exists an unique curve minimizing the length between and along . This length, , is the geodesic distance between and . A non-trivial property is that this length coincides with the minimal energy between and , that is to say the minimum along all ways of

under the normalization condition .

The parametric equation

Let be the position of a point at time . Then an application of the Euler’s perturbation formula gives

In a coordinates system , this can be written, for all

6.1.5 Killing fields

A field that preserves the metric is said to be a Killing field. In terms of the Lie derivative, this means that

so for all fields and

In particular, if the metric is invariant along the direction , then is a killing field. The previous equation then implies, for a way , . If is a geodesic, we then have

So, for a given geodesic, one can associate to any Killing field an invariant quantity along the geodesic :

6.1.6 Jacobi Fields

A field along a geodesic is said to be a Jacobi Field if and only if

where is the Riemann tensor.

This abstract definition becomes more intuitive thanks to the following proposition (see

Lang111Serge Lang, Fundamentals of Differential Geometry, Springer. for a demonstration).

Proposition. Let be a variation of a geodesic such as for every is a geodesic. Then

is a Jacobi Field. Furthermore, to every Jacobi Field along one can associate such a variation.

6.1.7 The Laplace Beltrami operator

The traditional Laplacian is defined as . In the euclidean case, this allows to write the relation for any sufficiently regular function with compact support.

For any Riemannian space , with dimension and metric , we want to find an expression of the Laplacian that verifies Stoke’s theorem, that is to say

where is the volume element of the Riemannian space (we know222Jûrgen Jost, Riemannian Geometry and Geometric Analysis, Springer Universitext, 2002. that it is given by .) Let be the determinant of the metric . As we have (we use Einstein’s summation convention)

it is necessary and sufficient to define the Laplace Beltrami operator as

One of the advantages of this intrinsic formulation of the Laplacian is that it is invariant by isometry. More precisely, if is an isometry between two spaces and , then for every function from to this diagram is commutative :

Indeed, as an isometry conserves the scalar product (so the volume element, too), we have for every sufficiently regular function from to with compact support,

As is any sufficiently regular function with compact support, this gives the commutation relationship.

6.2 A special case : the -geometry

The -geometry is defined on the upper half plane () with the metric

with . We will represent it with the matrices

6.2.1 The geodesics

After some calculation, the only Christoffel symbols that are not equal to 0 are :

-

•

;

-

•

;

-

•

.

Parametric equations

The parametric equation for geodesics is here

Another (equivalent but more practical) differential system is the following,

This system needs some explanation :

-

•

the first equation expresses that is constant;

-

•

the second one expresses that is a killing field : the metric coefficients do not depend on .

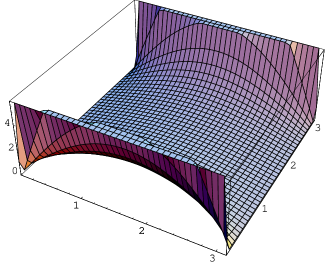

With these equations we can get the graph of these geodesics, leaving from with a speed and for (Fig 5.1 and 5.2).

Explicit equation

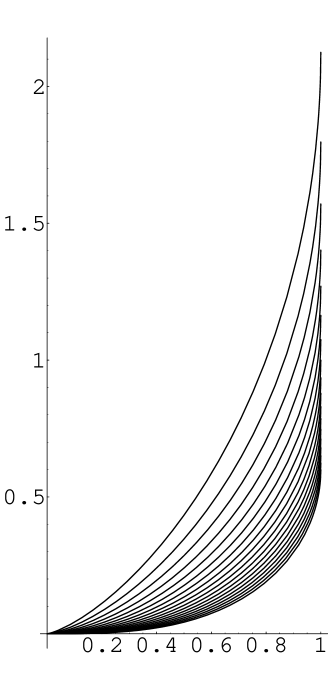

Eliminating in the second system of the previous paragraph, we get (imposing a maximal possible equal to 1)

An integration gives the following expression for , imposing :

We get the following graphic for different values of (Fig 5.3).

An interesting point is that for (), Mathematica always finds an explicit formula.

| Explicit formulae for | |

|---|---|

| 1 | |

| 1/2 | |

| 1/3 | |

| 1/4 | |

6.2.2 Curvatures

For our metric, the only non-zero curvatures are

6.2.3 Homogeneity

Notice first that if is a line of the upper half plane (not necessarily a geodesic), then one can easily know the length of ():

Another important homogeneity property is that if is a geodesic, so is : replacing and in the parametric equations defining the geodesics by and keeps the equalities true.

6.2.4 Distance from a point to a straight line

For our metric, one can easily check that vertical lines are geodesics, so the distance from a point to a vertical is gotten when the geodesic is perpendicular to the vertical axis.

So the homogeneity properties make it possible to calculate this length.

We have a point . If the smallest geodesic is a reference geodesic then one can calculate the abscisse of the intersection of on the schema. Then

6.3 The first-order expansion at the origin.

To give at the origin , we need to evaluate the terms in (2.4). In this equation can be replaced by . First notice that . Moreover, from the differential equation in the corollary 1, we have so

| (2.1) |

for near points and . We also need an expansion of up to the third order. This is quite technical but necessary. We consider the points and , and we note . Then a classical Taylor expansion gives

The evaluation of the partial derivatives with respect to is straightforward, because we know that the vertical lines are geodesics for the space (cf appendix 2). More precisely,

so

and

The evaluation of the partial derivatives with respect to is more complicated, because the geodesic between and is not a straight line anymore. Anyway, we will show that the calculation is the same as if it was a straight line indeed; to do so, we will use the symmetry with respect to the line of points with abscise (cf appendix 2).

A simple look at the geodesics in -geometry shows that the following schema is true : if is the length of the straight line, then the length of the geodesic is and the height is .

Let us (resp ) be the work of the field along the geodesic (resp the straight line). We now show that

The key point is that the geodesic has a symmetry axis, which implies . This allows us to write

Thus we have

which can be easily calculated, like for the partial derivatives with respect to . We finally get

We now can evaluate (2.4). We have , so the equation (2.4) at the point becomes

that is to say, for ,

We now have to evaluate each term :

-

•

from (2.5) one can easily conclude that and ;

-

•

the first-order approximation for gives and ;

-

•

the second-order evaluation of gives

We then finally have

6.4 Two new functions

Thanks to the above homogeneity properties, we only need to calculate the distances and the Jacobi fields on the standard geodesic (symmetric with respect to the ordinates axis and ). Here is the natural way to do all the necessary calculations on the standard geodesic :

-

•

the function Sind gives the position that minimizes the distance from a point to a line;

-

•

the distance function is specially easy to compute on the standard geodesic : we have a formula with only the coordinates of the end points;

-

•

then, to compute the Jacobi fields,we use the fact that it is a 2-dimensional linear space.

6.4.1 The function sind

We write the function such as

Geometric definition of function sind

The intuitive definition of function sind is given by the following drawing.

Analytical definition of function sind

For , we have

so

A simple calculation then gives

Then the function is the unique solution of the following equation :

| (2.2) |

Differential properties of function sind

The equation (1) defines sind in an implicit way. One can now get the differentials of sind, differentiating (1). The equations should be different in 4 zones of , but we just have 2 such zones in reality.

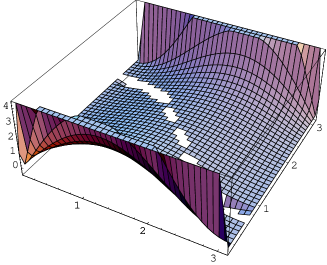

Examples of function sind

One can check that for (geodesics are circles) the .

The undefined values appearing on the frontier above is due to the difficulties Mathematica has to solve the equation (2.1) for

6.4.2 The distance

Thanks to the homogeneity properties, we only need to know the distance between the point (0,1) and any other point of the standard geodesic. This distance is exactly

thanks to links between hypergeometric functions.

6.4.3 The Jacobi field

The equation giving the Jacobi field on any geodesic is linear, so it is sufficient to evaluate it on the standard geodesic. In order to evaluate the Jacobi field on the standard geodesic with any initial point and initial increase, we just need to calculate two specific geodesics and then use linear combinations. The most natural initial conditions are :

-

•

and ;

-

•

and ;

The differential equation giving the evolution of a Jacobi field (we just need to know its length because it remains orthogonal to the geodesic) is

For , the equation above has the evident solution . For , we need to reformulate the equation above in terms of the coordinate . We get

The problem is that this equation is not lipschitzian for . This is the reason why, to get a great approximation of the solution, we use the initial conditions

with small enough (typically ). If we take the -coordinates, we then just need to take :

-

•

if , , if , ;

-

•

if , , if , .

Then, linear combinations of and give any Jacobi Field.

6.5 Variation formulas for the -model

The reader who does not know anything about the following variation calculations may read the famous books by Milnor333J. Milnor, Morse Theory, Annals of mathematics studies, Princeton university press. or Lang444Serge Lang, Fundamentals of Differential Geometry, Springer..

6.5.1 The first variation formula : minimization implies orthogonality

We consider sufficient conditions of regularity (uniqueness of the geodesic between two points etc). Then the distance from a point to a line is minimal in a point (with vector along the geodesic and along the line directed by ) if and only if

As is locally euclidean, this is equivalent to the usual orthogonality. Let us justify this relationship. For a variation (where represents the proper time, that is to say the length), if is a geodesic for every , then the length and the energy are equal, that is to say

This is a simple consequence of the definition of the proper time : . We then can write

| (2.3) | |||||

| (2.5) | |||||

| (2.7) |

The calculation above requires some explanation :

-

•

(2.1) : we use the well-known relation ;

-

•

(2.2) : the connection is torsion-free;

-

•

(2.3) : we also use the relationship ;

-

•

(2.4) : is a geodesic for every , so ;

-

•

(2.5) : the initial point does not move with the variation, so .

6.5.2 Second variation for any strike

In the following, we will have to calculate partial derivatives with respect to , so for simplicity we will write . We will then often use the following expression for the connection with direction ,

| (2.8) |

where is the angle between the straight line and the abscises axis.

To calculate the second derivative, we derive it from the expression (2.5),

| (2.9) |

where we use that the connection is torsion-free, and the relationship of derivation of the scalar product. Let us evaluate each of both terms.

-

•

We first have to calculate the covariant derivative

at the point where is the angle between the abscises axis and . Moreover,

where the sign + or - depends on which side the point is with respect to . So we have

-

•

As parallel transport keeps orthogonality, we have , where is the orthogonal of the speed vector with norm 1 (no matter its direction). So we have

To sum up, we have

where the sign depends on the following configurations.

6.5.3 Second, third and fourth variations at the money

We will also need the second, third and fourth derivatives, for .

-

•

we have ;

-

•

, so we have to calculate the third derivative of the distance. Let us derive it from the formula (2.7) :

We have and . The term (3) is more difficult to evaluate : it represents the variation with of the Jacobi-field increase, which is clearly maximum for ; this is the reason why the only term that remains in the calculation of (3) is the Christoffel part of the covariant derivative. A simple calculation then gives

-

•

Unfortunately, at this time, we don’t have properly derived a good expression for . However, an analogy with the case makes us believe that

Anyway, this expression is exact for .

Chapter 7 Appendix 3 : calculation of for the implied volatility formula

We describe hereafter the derivation of introduced in [Hagan [10]] as we need it in chapter 4.3.

We consider the process (), and we want to calculate the value defined by

7.1 The solution of the process

We know that is a martingale, with explicit value

This is the reason why

with . We now just need to know the conditional law of with respect to . This is a problem that evokes the brownian bridge, as seen in next part.

7.2 An equivalent to the brownian bridge

Lemma The law of is the same as the law of

Proof. We follow the traditional proof of the brownian bridge.

-

•

first of all, and are independant, because :

-

–

is a gaussian process, so is a gaussian vector;

-

–

so its coordinates are independant iff their covariance is zero; this is true (the coefficient has been chosen for it);

-

–

-

•

let us be a sufficiently regular and bounded function. We know that, if U and V are independant processes, then . So we can write

This means exactly the result of the lemma : both processes have the same law. ∎

7.3 Final calculation

We now can directly calculate the expectation (here is the suitable function depending on or )

This is how we get the final expression for :

One can check, after tedious calculations, that

If one does not want such a complicated expression, it can be approximated, for , by .