Pricing Virtual Paths with Quality-of-Service Guarantees as Bundle Derivatives

Abstract.

We describe a model of a communication network that allows us to price complex network services as financial derivative contracts based on the spot price of the capacity in individual routers. We prove a theorem of a Girsanov transform that is useful for pricing linear derivatives on underlying assets, which can be used to price many complex network services, and it is used to price an option that gives access to one of several virtual channels between two network nodes, during a specified future time interval. We give the continuous time hedging strategy, for which the option price is independent of the service providers attitude towards risk. The option price contains the density function of a sum of lognormal variables, which has to be evaluated numerically.

1. Introduction

1.1. End-to-end quality of service

Today, most traffic in computer networks is handled by best effort routing; each network router passes on packets as long as it can, and when the buffers are full, it drops incoming packets. When the network load is low, all data streams get a high throughput, and when the load is high, all streams experience equal loss.

This works well for some data streams such as file transfer, but less so for real-time data streams, i.e. when data packets have hard deadlines. Examples are audio/video streams [11], grid computing[16], and interactive data streams. Congestion causes packet losses and retransmissions that result in jitter, suspended computation, and high latency, respectively. These problems arise because the network cannot provide service quality guarantees and different service levels for different kinds of traffic. Ability to provide service guarantees requires that an individual user can reserve some of the capacity in the congestion prone parts of the network, be that routers, network links, or whatever.

The flexibility of today’s computer network is due to the design choice to keep the logic inside the network very simple, and to let all application specific knowledge be handled “at the ends”, by applications on top of the network layer. In this spirit, we advocate that a reservation policy should be implemented outside of the network, and that the network should only be a delivery vehicle for packets. Current attempts to improve throughput rely on more complex internal statistical routing and network maintenance. This “intelligent network” principle is different to the “end-to-end principle”, and intelligent networks have not been as good as end-to-end networks at supporting new applications and uses of the network.

1.2. End-user bandwidth markets

In today’s parlance, discussions of of bandwidth markets often refer to the trading of spare trunk capacity among large telecom companies, Internet service providers, etc. See for instance the bandwidth markets at Band-X, RateXchange, Min-X, etc. In these markets, the purpose of trading is to maximize the profit of the service providers, i.e. to let them fulfill their prior client obligations at a low cost. Since end-users are not affected by the cost, these prices only affect the traffic load on a coarse scale. Service providers can only guess what the best buy would be, since they do not know the network requirements of the applications running on the end-users’ computers.

We propose a somewhat different approach. To make an efficient market, the bandwidth allocation decisions should be a fine grained negotiation about access to the scarce resources, that takes place between the end-users, the actual consumers. This way, someone that really needs a particular resource can bid for it high enough that someone else releases (sells) the resource, and buys another resource instead. In most cases, end-users require complex services, services that require capacity in more than one router, and where these prices interact in a complex way to form the total price of the service.

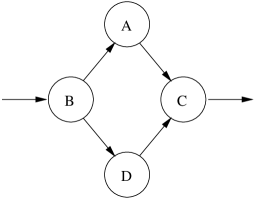

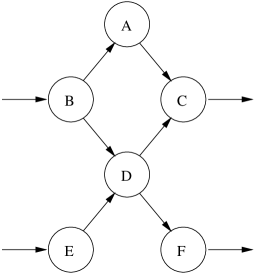

The resource prices are correlated in many ways. In fig. 1, the prices of all resources that are on a potential path affect the decision on whether do buy any of the other resources. In fig. 2, the demand of user 2 affects the price of resource A, not on the user 2’s potential paths.

There are some hurdles to overcome to make the resource negotiation fast and efficient:

-

(1)

The negotiation between the end-users must be kept very simple. Bilateral negotiations [11] is infeasible in real applications.

-

(2)

An end-user does not get a definite price-quote for a complex service such as a path that involves capacity in several routers.

-

(3)

The end-users will generate an extreme amount of network traffic when they buy and sell resources, get price quotes, etc.

These problems are addressed by the method presented here.

1.3. Related work

Related work on bandwidth markets to improve performance in networks are generally based on admission control at the edges, as done by Gibbens et al. [6]. A user is not admitted to the network if the network does not provide sufficient service quality. For instance, Kelly [7] models interconnections as reservations along a specified path, and gives Lyapunov functions that show that the system state stabilizes asymptotically, as end-users change their demand according to network load. Courcoubetis [8] models a router as consisting of channels, derives the probability that a certain fraction of the traffic is lost, and prices a call option that bounds the price a user has to pay for capacity in one router. Semret et al. [14] model admission control to a network over an exponential distributed number of minutes as a number of n:th-price auctions on 1 minute time-slot access, and price an access option as the sum of call options on each of the time slots. Lukose, et al. [9] use a CAPM-like model to construct a mixed portfolio of network access with different service classes, in order to reduce the latency variance and mean.

The above models either investigate the asymptotic network behavior, or only model the price for one network resource. We are interested in handling the transient behavior of a network with several interacting nodes.

In neither of the models above do the underlying resources constitute a complete market, i.e. it is not possible to create a momentarily perfectly balanced (risk-less) portfolio of options and underlying resources. The price of the option is therefore dependent on the risk-aversiveness of the network provider. In a complete market, the price is independent of the risk-aversiveness since perfect hedges can be created, and the price can be set more tightly, since anyone can trade and compete for the bids.

We will present a model of a complete continuous time market that allows us to derive the price of an option that extends the capabilities of the above options in several ways

-

•

the price depends on more than one underlying resources

-

•

the actual path, or set of resources assigned, does not have to be specified in advance

-

•

the price is risk-neutral, using the Black-Scholes’ assumptions

Furthermore, we choose a market type in which the resources are traded continuously, rather than in auctions with discrete clearing times since that causes latency.

1.4. Structure of the paper

In section 2 we recapture relevant formulas from the theory of derivative pricing, in sec. 3 we describe the model price process for which we price the derivatives, and models of the market and network resources. In sec. 4 we state the main results, which are the definitions and price formulas for the network option (proofs are deferred to the appendix), and we conclude with a discussion in sec. 5.

2. Preliminaries

2.1. Derivative pricing

A standard way to price derivative contracts, a.k.a “derivatives”, such as options, futures, etc. is to use arbitrage-free portfolio theory, which says that an asset, known to be worth at a future time , is worth today. Here is the continuously compounded interest “risk-free rate”, the loan/interest rate that you get from a bank or a government bond. The reasoning is that if the asset was worth , which is less (more) than , then anyone could make money by borrowing (lending) to the rate , buy (short sell) the resource, wait to sell (buy back) the resource for , pay back (withdraw ) and keep the arbitrage profit (). This cannot be possible in an arbitrage-free market. The argument requires that short selling is allowed, and that transaction fees are negligible.

Derivative pricing often models the asset prices as Itô processes ,

where is a Wiener process, and and are sufficiently bounded functions [15]. The Black-Scholes method [1] prices a derivative of an asset which price follows a particular kind of Itô-process. It is based on constructing a portfolio that invests some part of its money in the option, and some part in the asset. At each instant, the portfolio is balanced in such a way that its value after is known exactly. As time goes and prices change, the portfolio is rebalanced. In short, it is shown that a derivative that is a function of a stochastic process

follows the Black-Scholes equation

which from the Feynman-Kac formula can be seen to have the solution

where is the so called equivalent, or risk-free, martingale measure. The boundary condition, given by the function , specifies the value of the option at the time the derivative expires. For a traditional call option, , where is the strike price.

Under the measure, has the drift term , and hence, under ,

Recall from the definition of Itô processes that is a Wiener process, in other words, is normal distributed with mean 0 and variance given , the knowledge up until . This means that we can price derivatives using Monte-Carlo simulation to solve the differential equations above. Another advantage with Monte-Carlo is that it converges quite fast also for multidimensional problems, something that is not the case for binomial-tree pricing methods.

Rebalancing a portfolio, or obtaining/selling assets to decrease its variance is called ’hedging’ the portfolio. The Black-Scholes hedging method produces a self-financing hedge, i.e. no additional capital is needed to balance the risk of the portfolio. Another interesting effect of Black-Scholes hedging is that the formula for the optimal continuous-time hedge at given does not involve the drift function . Hence, the continuous-time hedging is the same for the mean-reverting and the exponential drift processes.

2.2. Applied pricing

The assumption that a portfolio can be continuously rebalanced is violated in real markets. Market frictions, such as transaction fees, often make it too costly to rebalance a portfolio very often. For bandwidth markets, we can eliminate market friction all together, since we are free to design the market to our own liking. We cannot however guarantee that we can rebalance the portfolio at every instant, since there are others that want to trade concurrently with ourselves, and multiple other trade events may occur between the rehedging events.

To understand the effect of interval hedging compared to continuous time hedging, we show the effect on the portfolio value of hedging and rehedging a call option on a single asset for three different price processes, hedged continuously and at intervals.

2.2.1. Continuous time hedging

The lognormal Brownian motion process is often used to model stock stock price . Its dynamics is

| (1) |

A derivative contract, on an underlying asset obeying (1) and under , can be hedged in continuous time by creating a portfolio of derivatives and assets. A perfectly hedged, self financing, portfolio with a derivative contract depending on assets has the value

follows (for lack-of-arbitrage reasons) the value of a safe investment, , where is the risk-free continuously compounded interest rate. The hedging strategy is

| (2) | |||||

| (3) |

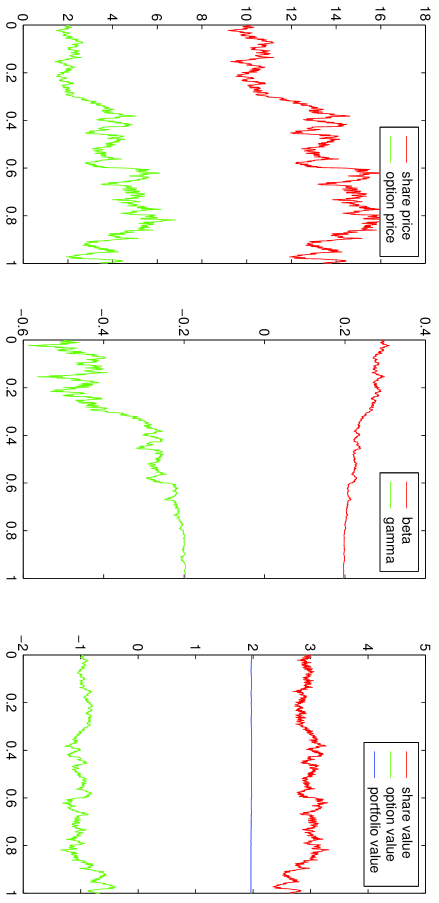

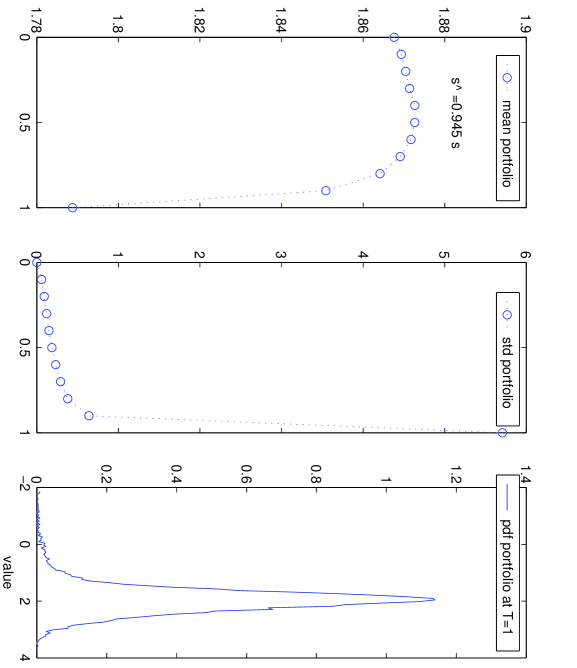

Consider a share whose price follows a lognormal Brownian motion, see fig. 3. The price is plotted in the left graph, together with the price of a call option with strike price 10 that expires at The middle graph shows the composition of a perfectly hedged portfolio. The topmost curve is , the parts of the portfolio part invested in shares, and under it is , the part invested in options. A negative number means that the option should be sold short. To the right is a plot of the total value of the portfolio that initially consisted of one option. Above and below are plots of the total value of the portfolio holdings, in shares and options, respectively. Here , so the value of the portfolio should be constant even though the share and option prices fluctuate. Since the portfolio value is constant in the rightmost plot, the hedging works, and the portfolio yields the risk-free rate.

A well known result of the Black-Scholes pricing is the somewhat surprising result that the derivative prices is not dependent of the drift term. This is because it is based on a first order approximation, and the drift term is while the diffusion term is . Since the drift term is the only difference between the lognormal process and the mean-reverting process with multiplicative noise, the hedging scheme works as equally well for both processes.

2.2.2. Interval time hedging

For hedging at discrete events with an interval rather than in continuous time, the above formula does not give a complete hedge.

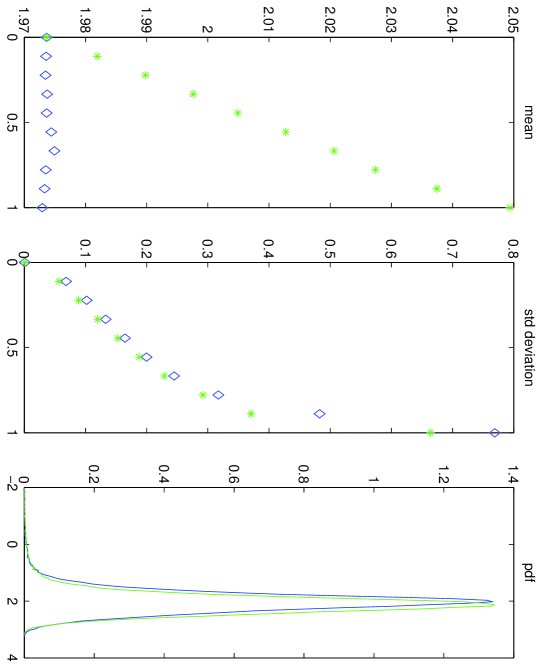

The effect of hedging a call option with an unmodified strategy is shown, for two different underlying processes, in fig. 4. Above to the left, is a plot of the average portfolio value from a Monte-Carlo simulation, of a lognormal process, and a mean-reverting process with multiplicative noise. The middle plot shows the variance of the portfolio value at the 10 rebalancing times. The variance increases with time, and the variance is higher for the mean-reverting process than for the lognormal process. To the right is the density function for the portfolio value at . The rebalancing of the portfolio is only done every 100 steps, i.e. . It is apparent that the portfolio value for the mean-reverting process is not constant. It is hence possible to make a statistical arbitrage profit on the derivatives. However, the deviation in expected value is only a few percent, so a small increase in the derivative price can protect the issuer from the arbitrage risks.

For some processes a modified hedging strategy can be derived. Cornalba, Bouchaud et al. [3] have considered time correlated stochastic processes and shown that for the Ornstein-Uhlenbeck process

the same hedging strategy can be used, but with a modified variance. A similar derivation, inspired by Bouchaud, gives that . This is based on a first order approximation, hence the modified volatility is appropriate only for small . For many processes, such as processes with multiplicative noise, we do not have modified strategies.

Fig. 5 shows plots, similar to fig. 4, of the values for a mean-reverting process that is hedged with the modified measure of variance , and it can be seen that the adjustment is not perfect, but still only a few percent off. Its dynamics are more complex, and we do not know of a strategy with modified variance that makes the portfolio value process replicate that of a risk-free portfolio.

Since the portfolio cannot be made risk-free over all of , the future portfolio value is uncertain. In terms of mathematical finance, the market is incomplete. In complete markets, options can be priced in a way that does not depend on the risk-aversiveness of individual participants, something that is not the case in an incomplete market. However in a technical system, designed to be controlled by a market, we can require there to always be one or more trading programs that behave risk-neutrally, or that charge a specified risk premium. That guarantees that derivatives are traded at prices that make the market efficient, in the sense that they maximize the expected utility of the end-users by providing low option prices.

3. Model

3.1. Price processes

In a computer network, end-users share the limited capacity of the routers and links. To be able to provide QoS-dependent services, these resources must be managed by the end-users. To each end-user, the system load appears to fluctuate stochastically, as the end-user does not have access to the complete system state.

Our approach is to view the state of the system as stochastic processes, and to control the use of scarce resources by trading the usage right at spot markets. On these markets, prices will appear to be stochastic processes. The prices present an an aggregated view of the system. With this view, controlling a technical system with interacting subunits (not necessarily a network), boils down to developing suitable derivatives and hedging schemes for the different services that the system should provide. The implementation requires market-places for the individual resources, and third party middle-men that sell derivatives to end-users and do the actual trading on the resource level.

An average, sporadic end-user is not willing to take the risk of paying an excessive amount for a network service, but rather get a definite price quote. Trading derivative contracts is a trade of risk, where one part gets the risk and a premium, and the other part gets a fixed cash flow. With suitable market models, derivative contracts can be priced objectively, at least when the price processes can be described sufficiently well. So, instead of trading the actual resources, the end-users buy derivative contracts of a third party. The contract guarantees the delivery of the required set of resources. The contract may specify both future delivery of some resources, and deliveries that are contingent on future prices, or functions thereof.

In a previous paper [13], we have simulated a simple bandwidth market without derivatives, to determine the properties of the resulting stochastic price process. It was found to be very well described by a correlated mean-reverting process with multiplicative noise,

| (4) |

where the price correlation . We gave estimations of the parameters based on price history data from the simulation. Since this modeling was possible, it appears feasible to represent complex network services in terms of derivative contracts on certain complex combinations of resources. Since in general, introducing new assets in a market modifies the price dynamics, hence the parameters must be re-estimated when new derivatives are added.

The mean-reverting process drifts back towards with a rate determined by . As opposed to lognormal processes, mean-reverting processes are auto-correlated processes, and their the variance per time unit, decreases with increasing for the mean-reverting process, while it is constant for the lognormal process. It is the fact that the price process has “memory” that causes the deviation in the expected value of the portfolio for interval hedging.

3.2. Farmer markets

The market places where resource trading are of a special kind designed for very rapid markets that we call Farmer markets, as the original inspiration was found in [5]. Each market handles one resource, and is run by a market maker that at each instance guarantees to accept bids both to buy and to sell.

There is no back-log of pending “limit orders”, only bids “at market” are accepted. This guarantees that the trading can take place with very little overhead for the market maker. Since only bids at-market are accepted, the bidder does not know at what price resources will be traded, but prices can be estimated from the price-quote history.

The central idea of this market design is that the resources are exchanged on these markets, and that all more complex contracts are expressed as derivative contract on these resources. For instance, a limit order, i.e. an order to buy if the price is less than a specified amount, is a risky contract since the bidder does not know if the deal will go through or not.

3.3. Resource shares

The capacity of each resource is divided into equal well defined shares, that gives the owner the right to send a certain amount of traffic on a short time if he pays . From here on, we assume . The total capacity of the shares must not surpass the total capacity of the resource. Without the payment from the resource holder to the market maker, a holder of the resource would have no incentive to avoid congested resources, which is shown in the pricing of the bundle options below.

For routers, statistical multiplexing has shown to give a large throughput increase, hence it seems reasonable to mix two traffic classes. A router has two traffic classes, 1) the guaranteed class, and 2) the best-effort class. Packets in the first class are guaranteed not to be dropped in case of congestion, while packets without valid credentials are handled in traditional best-effort manner. As with the Metro Pricing Scheme by Odlyzko [10], we only requires two traffic classes, but in the Metro Pricing scheme, prices are determined outside of the system in such a way that there is no congestion in the first class, while in our model, prices are determined by demand, and first class packets get to go first if there is congestion.

4. Results

In a computer network, end-users want to establish virtual paths with certain guaranteed properties, such as loss, latency, etc. The user wants to have the resources at and to sell them again at . This can be implemented as an option that delivers the resources at together with a bundle of options that lets the user sell the resources at a guaranteed price. To find the price of this option, we first establish the following corollary. All proofs are deferred to the appendix.

Corollary.

(1) The price of a future to buy shares of the resources on the cheapest path between two network nodes at a that are resold at is zero.

However, to balance the load, the price of the derivative must depend on the resource prices, therefore the so-called bundle future above is not suitable for load-balancing. Instead, we define a network option, in the following way.

Definition.

A network call-option gives the holder the right to send packets with a specified intensity through nodes on a path between two network routers from time to time , if the fee is paid at .

The call-option price depends on the price of the shares in all routers that are on any of the possible paths. The following is a very useful theorem for deriving prices of options based on the correlated price processes.

Theorem.

(3) Let be an -dimensional lognormal price process with correlation under probability measure . Then

where

This shows that linear derivatives can be priced as expected values of an adjusted process .

With the help of this theorem, we can derive the value of the network call-option, and its partial derivatives, and calculate the optimal rebalance strategy for a portfolio for the continuous time hedge strategy, using Eq. (2) and (3).

Corollary.

(3) The value of a network call-option with strike price is

where

is the adjusted cost of path , after the Girsanov transform to eliminate resource ,

with .

Corollary.

There is no closed form for the sum of lognormal variables [17], which makes it difficult to reduce the -terms further, but since has a closed form under the risk neutral measure , the option price can be approximated with Monte-Carlo simulation. Note that under the risk neutral measure one, can be simulated without having to simulate the individual price trajectories for the mean-reverting process, something that is required for pricing techniques using the natural measure, and which is very time consuming.

5. Discussion

In the proposed network model, access to each node is traded in a different market. This way, applications at the edge of the network can combine the resources in which way they choose, i.e. build broadcast trees, or failure safe multi-path routing. By choosing to trade capacity shares rather than time-slotted access as the fundamental commodity, we have only one market per router instead of one per router and minute.

In the most popular alternative model, network access is handled only at the edge of the network, hence applications at the edges cannot create new services. The cost of a more fine grained control scheme is of course more overhead, but with the proposed scheme, the routers are relieved of much work, since the packets are source routed.

The central idea is that simple resources are exchanged on very fast markets, and that all more complex services are expressed as derivative contract on these resources. Since we use Farmer markets, the trading generates very little overhead but incurs a price risk for the trader, which must be hedged. Since end-users do not hedge their risks themselves, but instead buy derivatives, the network will not be flooded by bids and quotes between all end-users and all markets. When a user requires a service, or a combination of services, the user simply tells a middle-man that it is willing to pay a certain amount for a derivative that models the service, and the user can be informed directly whether or not it got the service, and of the marginal cost.

The capacity prices are assumed to be correlated Itô processes with multiplicative drift. We show how use a Martingale technique to price options on one-of-several linear combinations of assets by proving a theorem on a Girsanov transform that can be used to price several other options, and give a continuous time hedge strategy that can be used by a trader to balance out all risk. We have not found a complete adjusted strategy for the mean-reverting price process when the portfolio is infrequently rebalanced. A potential possibility to find an adjusted strategy is to look into pricing of Bessel processes [2].

The proposed hedge scheme builds on the assumptions made in the Black-Scholes model, i.e. that the portfolio is self-financing, without arbitrage possibilities, and that short selling is allowed. Other hedge schemes use different assumptions, such as CAPM [18], which aims to minimize the variance of the portfolio value while maximizing its expected value. The proposed scheme has the advantage that the price is invariant of risk-attitude, and can be efficiently evaluated using Monte-Carlo techniques.

Future work will consist of simulations of the complete bandwidth market in order to determine the effect of the network options on the price processes, to find better models for the financial risk of trading in Farmer markets, and to model other network services as derivative services.

Acknowledgement.

The author wishes to thank Erik Aurell for advice and many constructive comments on the topic of financial mathematics, and Sverker Janson for helpful discussions on agent based models. This work is funded in part by Vinnova/Nutek, The Swedish Agency for Innovation Systems, program PROMODIS, and in part by SITI, The Swedish Institute for Information Technology, program Internet3.

References

- [1] Fischer Black, and Myron Scholes, The Pricing of Options and Corporate Liabilities, Journal of Political Economy, (81:3), pp. 637-654, (1973).

- [2] Hélyette Geman, and Mark Yor, Bessel Processes, Asian Options, and Perpetuities, Mathematical Finance, 3/4, (1993)

- [3] Lorenzo Cornalba, Jean-Philippe Bouchaud, and Marc Potters, Option Pricing and Hedging with Temporal Correlations, Nov (2000). http://xxx.lanl.gov/abs/cond-mat/0011506

- [4] James F. Kurose, and Rahul Simha, A Microeconomic Approach to Optimal Resource Allocation in Distributed Computer Systems, IEEE Trans. on Computers, (38) no. 5, May (1989).

- [5] J. Doyne Farmer, Market force, ecology, and Evolution, submitted to Journal of Economic Behavior and Organization, Feb. (2000). http://www.santafe.edu/~jdf/

- [6] Richard J. Gibbens, and Frank P. Kelly, Resource pricing and the evolution of congestion control, Automatica, 35, (1999) http://www.statslab.cam.ac.uk/~frank/evol.html

- [7] Frank P. Kelly, Mathematical modelling of the Internet. In "Mathematics Unlimited - 2001 and Beyond" (Editors B. Engquist and W. Schmid). pp. 685-702, Springer-Verlag, Berlin, (2001) . http://www.statslab.cam.ac.uk/~frank/mmi.html

- [8] Costas Courcoubetis, Antonis Dimakis, and Marty Reiman, Providing Bandwidth Guarantees over a Best-effort Network: Call-admission and Pricing, Proc. of Infocom 2001. http://infocom.ucsd.edu/papers/231.pdf

-

[9]

Rajan M. Lukose, and Bernardo A. Huberman, A Methodology for Managing Risk in

Electronic Transactions over the Internet, Proc. of the Third Int. Conf on Computational

Economics, Palo Alto, June 1997.

http://www.parc.xerox.com/istl/groups/iea/abstracts/ECommerce/banking.html -

[10]

Andrew M. Odlyzko, Paris Metro Pricing for the Internet, Proceedings

of the ACM Conference on Electronic Commerce, pp. 140-147, (1999).

http://www.research.att.com/~amo/doc/paris.metro.pricing.ps - [11] Peyman Faratin, Nicholas Jennings, R. R. Buckle, and Carlos Sierra, Automated negotiation for provisioning virtual private networks using FIPA-compliant agents, Proc. of 5th Int. Conf. of Practial Applications of Intelligent Agents and Multi-Agent Systems, Manchester, UK, (2000).

- [12] Pierre Collin Dufresne, William Keirstead, and Michael P. Ross, Pricing Derivatives the Martingale Way, May (1996). http://www.berkeley.edu/finance/WP/rpfabstract.html

- [13] Lars Rasmusson, and Erik Aurell, A Price Dynamics in Bandwidth Markets for Point-to-point Connections, unpublished, subm. to IEEE/Trans. on Networking, Jan 2001. http://xxx.lanl.gov/abs/cs.NI/0102011

-

[14]

Nemo Semret, and Aurel A. Lazar, Spot and derivative markets in admission

control, in Proc. of ITC 16, P. Key and D. Smith, Eds. June 1999, pp. 925-941,

Elsevier.

http://citeseer.nj.nec.com/semret99spot.html - [15] Peter E. Kloeden, and Eckhard Platen, Numerical Solution of Stochastic Differential Equations, Springer Verlag, Berlin, 1999.

-

[16]

Klaus Krauter, and Muthucumaru Maheswaran, Architecture for a Grid Operating

System, Proc. of 1st IEEE/ACM Int. Workshop on Grid Computing, Bangalore, India,

LNCS 1971, Springer Verlag, Dec. 2000.

http://www.csse.monash.edu.au/~rajkumar/Grid2000/grid2000/book/19710064.ps - [17] Moshe Arye Milevsky, and Steven E. Posner, Asian Options, the Sum of Lognormals, and the Reciprocal Gamma Distribution, Journal of Financial and Quantitative Analysis Vol. 33, No. 3, September 1998

- [18] Zvi Bode, AlexKane, and Alan J. Marcus, Investments, Irwin/McGraw-Hill, Boston, 1996.

Appendix A

Here we give the proofs of the theorems and lemmas needed for pricing the network option.

A.1. Bundle futures

Definition 1.

A bundle future gives the holder a set of resource shares between and , given that an event occurs at . Let be the equivalent martingale measure.

Theorem 1.

The price of the bundle future is zero.

Lemma 1.

If W(T) is a Wiener process, then , where is the natural filtration up to .

Lemma 2.

The price of a future to buy a single resource at that is sold at is zero.

Proof: At , the future is worth . Hence the price at is

∎

Lemma 3.

The price of a derivative that delivers the future defined in lemma 2, given that event occurs at , is also zero.

Proof: At the derivative is worth . Hence the option price at is

where is the probability of under the probability measure . ∎

Corollary 1.

The price of a future to buy shares of the resources on the cheapest path between two network nodes at a that are resold at is zero.

Proof: Let be the amount of router required on path , and let be the event that path is the cheapest path at . The corollary follows from Theorem 1. ∎

A.2. Network option (step one)

Definition 2.

A network option gives the holder the right to send packets with a specified intensity through nodes on a path between two network routers from time to time , if the fee is paid at .

Lemma 4.

The price of an arithmetic average (Asian) call option with strike price zero and maturity at is

which becomes in the limit of .

Proof: At , the option is worth , so

∎

Theorem 2.

Let be the cost of the resources for alternative at . The price of a network option is

where , for which .

Proof: The cost to send traffic consists of buying the required router shares at , pay the send fee from to and sell back the shares at . This amounts to a bundle option and an Asian option from to on some path between the source and the destination. The cheapest option is the option over the least cost path, i.e. where at . At the network option is worth the sum of Asian options for the resources on the cheapest path minus if the option is in-the-money, else it is worth 0. Hence, on

∎

A.3. The 1-dimensional Girsanov transform

We start by showing the usefulness of the so-called Girsanov transform for a one-dimensional stochastic process, in order to simplify the presentation of the proof of the -dimensional transform. The one-dimensional pricing of a call option was based on Dufresne et al. [12].

Lemma 5.

Proof:

where . ∎

Corollary 2.

The value of a call option with strike price , and maturity at , is

where , is the cumulative density function for the standard normal distribution, the current time and .

Proof: From the definition of the indicator function, . The corollary follows from seeing that

and from the lemma,

and

by doing a Girsanov transform, and using that is normal distributed with variance . ∎

A.4. The -dimensional Girsanov transform of

Lemma 6.

Let , , where are standard normal distributed variables, correlated with under the measure , and uncorrelated under the measure . Then

where , and is the Cholesky factorization of , i.e. .

Proof: Since , then . The substitution makes , , and .

∎

Lemma 7.

The multidimensional variant of the elimination of for an uncorrelated N-dimensional random variable is

where .

Proof:

where , therefore

∎

Lemma 8.

.

Theorem 3.

Let be an -dimensional lognormal price process with correlation under probability measure . Then

where .

A.5. Network option (step two)

Corollary 3.

The value of a network call-option with strike price is

where is the adjusted cost of path , after the Girsanov-transform to eliminate resource .

Corollary 4.

The partial derivative of the network option with strike-price is

and

Proof: The first statement follows from that nearly everywhere, for all and , for both cases when , and when . The second follows trivially from the value of the network call-option and the first statement.∎