Economic Fluctuations and Diffusion

Abstract

Stock price changes occur through transactions, just as diffusion in physical systems occurs through molecular collisions. We systematically explore this analogy [1] and quantify the relation between trading activity — measured by the number of transactions — and the price change for a given stock, over a time interval . To this end, we analyze a database documenting every transaction for 1000 US stocks over the two-year period 1994–1995 [2]. We find that price movements are equivalent to a complex variant of diffusion, where the diffusion coefficient fluctuates drastically in time. We relate the analog of the diffusion coefficient to two microscopic quantities: (i) the number of transactions in , which is the analog of the number of collisions and (ii) the local variance of the price changes for all transactions in , which is the analog of the local mean square displacement between collisions. We study the distributions of both and , and find that they display power-law tails. Further, we find that displays long-range power-law correlations in time, whereas does not. Our results are consistent with the interpretation that the pronounced tails of the distribution of [3, 4, 5, 6, 7, 8, 9, 10, 11, 12] are due to , and that the long-range correlations previously found [13, 14, 15, 16, 17] for are due to .

Consider the diffusion [18, 19, 20] of an ink particle in water. Starting out from a point, the ink particle undergoes a random walk due to collisions with the water molecules. The distance covered by the particle after a time is

| (2) |

where are the distances that the particle moves in between collisions, and denotes the number of collisions during the interval . The distribution is Gaussian with a variance , where the local mean square displacement is the variance of the individual steps in the interval .

For the classic diffusion problem considered above: (i) the probability distribution is a “narrow” Gaussian, i.e., has a standard deviation much smaller than the mean , (ii) the time between collisions of an ink particle are not strongly correlated, so at any future time depends at most weakly on at time —i.e., the correlation function has a short-range exponential decay, (iii) the distribution is also a narrow Gaussian, (iv) the correlation function has a short-range exponential decay and (v) the variable is uncorrelated and Gaussian-distributed. These conditions result in being Gaussian distributed and weakly correlated.

An ink particle diffusing under more general conditions would result in a quite different distribution of , such as in a bubbling hot spring, where the characteristics of bubbling depend on a wide range of time and length scales. In the following, we will present empirical evidence that the movement of stock prices is equivalent to a complex variant of classic diffusion, specified by the following conditions: (i) is not a Gaussian, but has a power-law tail, (ii) has long-range power-law correlations, (iii) is not a Gaussian, but has a power-law tail, (iv) the correlation function is short ranged, and (v) the variable is Gaussian distributed and short-range correlated. Under these conditions, the statistical properties of will depend on the exponents characterizing these power laws.

Just as the displacement of a diffusing ink particle is the sum of individual displacements , so also the stock price change is the sum of the price changes of the transactions in the interval ,

| (3) |

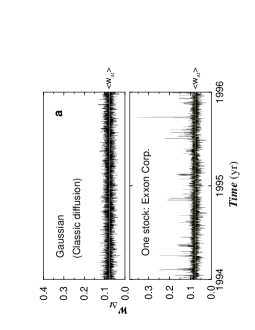

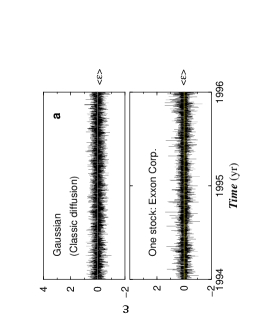

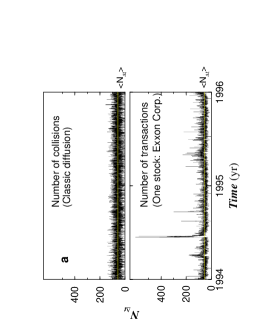

Figure 1a shows for classic diffusion and for one stock (Exxon Corporation). The number of trades for Exxon displays several events the size of tens of standard deviations and hence is inconsistent with a Gaussian process [21, 22, 23, 24, 25, 26].

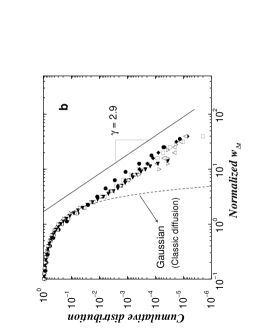

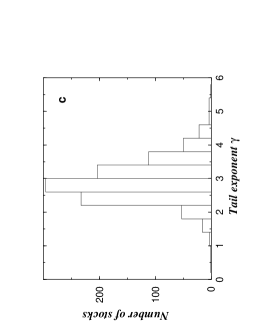

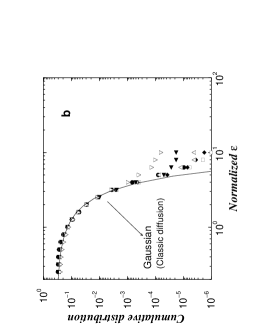

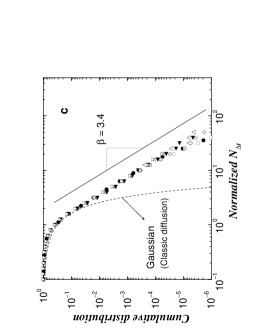

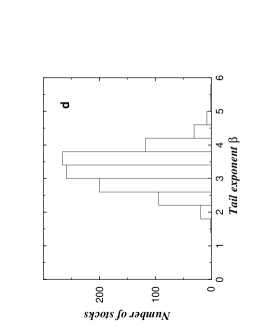

(i) We first analyze the distribution of . Figure 1c shows that the cumulative distribution of displays a power-law behavior . For the 1000 stocks analyzed, we obtain a mean value (Fig. 1d). Note that is outside the Lévy stable domain .

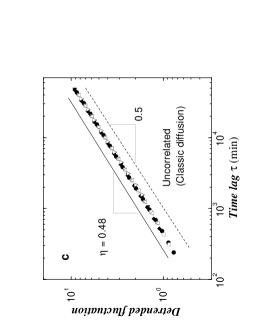

(ii) We next determine the correlations in . We find that the correlation function is not exponentially decaying as in the case of classic diffusion, but rather displays a power-law decay (Fig. 1e,f). This result quantifies the qualitative fact that if the trading activity () is large at any time, it is likely to remain so for a considerable time thereafter.

(iii) We then compute the variance of the individual changes due to the transactions in the interval (Fig. 2a). We find that the distribution displays a power-law decay (Fig. 2b). For the 1000 stocks analyzed, we obtain a mean value of the exponent (Fig. 2c).

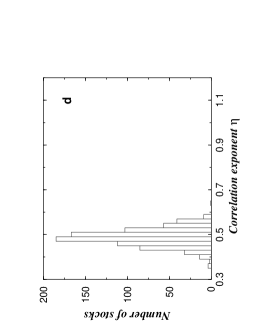

(iv) Next, we quantify correlations in . We find that the correlation function shows only weak correlations (Fig. 2d,e). This means that at any future time depends at most weakly on at time .

(v) Consider now chosen only from the interval , and let us hypothesize that these are mutually independent and with a common distribution having a finite variance . Under this hypothesis, the central limit theorem implies that the ratio

| (4) |

must be a Gaussian-distributed random variable with zero mean and unit variance [27]. Indeed, for classic diffusion, is Gaussian-distributed and uncorrelated (Fig. 3a). We confirm this hypothesis by analyzing (a) the distribution , which we find to be consistent with Gaussian behavior (Fig. 3b), and (b) the correlation function , for which we find only short-range correlations (Fig. 3c,d).

Thus far, we have seen that the data for stock price movements support the following results: (i) the distribution of decays as a power-law, (ii) has long-range correlations, (iii) the distribution of decays as a power-law, (iv) displays only weak correlations, and (v) the price change at any time is consistent with a Gaussian-distributed random variable [21, 22, 23, 24, 28, 29, 30, 31] with a time-dependent variance , that is, the variable is Gaussian-distributed and uncorrelated.

Next, we explore the implications of our empirical findings. Namely, we show how the statistical properties [5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15] of price changes can be understood in terms of the properties of and . We will argue that the pronounced tails of the distribution of price changes [5, 6, 7, 8, 9, 10, 11, 12] are largely due to and the long-range correlations previously found [13, 14, 15, 16, 17] for are largely due to the long-range correlations in . By contrast, in classic diffusion and do not change the Gaussian behavior of because they have only uncorrelated Gaussian-fluctuations [21, 27].

Consider first the distribution of price changes , which decays as a power-law with an exponent [8, 9, 10, 11, 12]. Above, we reported that the distribution with (Fig. 1c,d). Therefore, with . Equation (4) then implies that alone cannot explain the value . Instead, must arise from the distribution of , which indeed decays with approximately the same exponent (Fig. 2b,c). Thus the power-law tails in appear to originate from the power-law tail in .

Next, consider the long-range correlations found for [13, 14, 15, 16, 17]. Above, we reported that displays long-range correlations, whereas does not (Figs. 1–2). Therefore, the long range correlations in should arise from those found in . Hence, while the power-law tails in are due to the power-law tails in , the long-range correlations of are due to those of .

In sum, we have shown that stock price movements are analogous to a complex variant of classic diffusion. Further, we have empirically demonstrated the relation between stock price changes and market activity, i.e., the price change at any time is consistent with a Gaussian-distributed random variable with a local variance . What could be the interpretations of our results for the number of transactions and the local standard deviation ? Since measures the trading activity for a given stock, it is possible that its power-law distribution and long-range correlations may be related to “avalanches” [32, 33, 34, 35]. The fluctuations in reflect several factors: (i) the level of liquidity of the market, (ii) the risk-aversion of the market participants and (iii) the uncertainty about the fundamental value of the asset.

REFERENCES

- [1] Bachelier, L., Théorie de la spéculation. Ann. Sci. École Norm. Sup. III-17, 21–86 (1900).

- [2] The Trades and Quotes Database, 24 CD-ROMs for 1994-95, published by the New York Stock Exchange.

- [3] Bouchaud, J.-P. & Potters, M., Theory of Financial Risk (Cambridge University Press, Cambridge 2000)

- [4] Farmer, J. D., Physicists Attempt to Scale the Ivory Towers of Finance. Computing in Science & Engineering 26, November Issue.

- [5] Mandelbrot, B. B., The variation of certain speculative prices. J. Business 36, 394–419 (1963).

- [6] Mantegna, R. N. & Stanley, H. E., Scaling behavior in the dynamics of an economic index. Nature 376, 46–49 (1995).

- [7] Ghashgaie, S., Breymann, W., Peinke, J., Talkner, P., & Dodge, Y., Turbulent cascades in foreign exchange markets. Nature 381, 767–770 (1996).

- [8] Pagan, A., The econometrics of financial markets. J. Empirical Finance 3, 15–102 (1996).

- [9] Lux, T., The stable Paretian hypothesis and the frequency of large returns: An examination of major German stocks. Applied Financial Economics 6, 463-75 (1996).

- [10] Loretan, M. & Phillips, P. C. B., Testing the covariance stationarity of heavy-tailed time series. J. Empirical Finance 1, 211–248 (1994)

- [11] Muller, U. A., Dacorogna, M. M. & Pictet, O. V., Heavy tails in high-frequency financial data. A Practical Guide to Heavy Tails, Adler, R. J., Feldman, R. E. & Taqqu, M. S. (eds.) 283–311 (Birkhäuser Publishers, 1998).

- [12] Plerou, V., Gopikrishnan, P., Amaral, L. A. N., Meyer, M. & Stanley, H. E., Scaling of the distribution of price fluctuations of individual companies. Phys. Rev. E. 60, 6519-6529 (1999).

- [13] Ding, Z., Granger, C. W. J. & Engle, R. F., A long memory property of stock market returns and a new model. J. Empirical Finance 1, 83–105 (1993).

- [14] Liu, Y., Cizeau, P., Meyer, M., Peng, C.-K & Stanley, H. E., Quantification of correlations in economic time series. Physica A 245, 437–440 (1997).

- [15] Lundin, M., Dacorogna, M. M., & Muller, U. A., in Financial Markets Tick by Tick, P. Lequeux (ed.), 91–126, (John Wiley & Sons, 1999).

- [16] Anderson, T., Bollerslev, T., Diebold, F. & Labys, P., The distribution of exchange rate volatility. NBER Working Paper WP6961 (1999).

- [17] Arnoedo, A., Muzy, J.-F. & Sornette, D., Causal cascade in the stock market from the “infrared” to the “ultraviolet”. Eur. Phys. J. B 2, 277–282 (1998).

- [18] Chandrasekhar, S., Stochastic problems in Physics and Astronomy. Rev. Mod. Phys. 15 1–91 (1943), in Selected Papers on Noise and Stochastic Processes, Wax, N. (ed.) (Dover Publications Inc., New York, 1954).

- [19] Montroll, E. W. & Shlesinger, M. F., The wonderful world of random walks, in Nonequilibrium Phenomena II. From Stochastics to Hydrodynamics Lebowitz, J. L. & Montroll, E. W. (eds.) 1-121 (North-Holland, Amsterdam, 1984).

- [20] Bouchaud, J.-P. & Georges, A., Anomalous diffusion in disordered media: statistical mechanisms, models, and physical applications. Phys. Rep. 195, 127 (1990).

- [21] Clark, P. K., A subordinated stochastic process model with finite variance for speculative prices. Econometrica 41, 135–155 (1973).

- [22] Mandelbrot, B. B. & Taylor, H., On the distribution of stock price differences. Operations Research 15, 1057–1062 (1962).

- [23] Epps, T. W. & Epps, M. L., The stochastic dependence of security price changes and transaction volumes: Implications of the mixture-of-distributions hypothesis. Econometrica 44, 305-321 (1976).

- [24] Tauchen, G. & Pitts, M., The price variability-volume relationship on speculative markets. Econometrica 57, 485–505 (1983).

- [25] Stock, J., Estimating continuous time processes subject to time deformation. Journal of the American Statistical Association 83 77–85 (1988).

- [26] Guillaume, D. M., Pictet, O. V., Muller, U. A. & Dacorogna, M. M., Unveiling non-linearities through time scale transformations. Olsen group preprint OVP.1994-06-26 (1995), available at http://www.olsen.ch.

- [27] Feller, W., An Introduction to Probability Theory and its Applications (John Wiley, New York, 1966).

- [28] Engle, R. F., (ed.) ARCH: Selected Readings (Oxford University Press, Oxford, 1995).

- [29] Ghysels, E., Harvey, A. & Renault, E., Stochastic Volatility. Handbook of Statistics Vol. 14, Statistical Methods in Finance, G. S. Maddala (ed.), 119–191 (North-Holland, Amsterdam, 1996).

- [30] Jones, C., Gautam, K. & Lipson, M., Transactions, volumes and volatility. Reviews of Financial Studies 7, 631–651 (1994).

- [31] Ane, T. & Geman, H., Order flow, transaction clock and normality of asset returns. Journal of Finance, forthcoming (2000).

- [32] Lux, T. & Marchesi, M., Scaling and criticality in a stochastic multi-agent model of a financial market. Nature 397, 498–500 (1999).

- [33] Cont, R. & Bouchaud, J.-P., Herd behavior and aggregate fluctuations in financial markets. Macroeconomic Dynamics, forthcoming; preprint cond-mat/9712318.

- [34] Bouchaud, J.-P. & Cont, R., A Langevin approach to stock market fluctuations and crashes. Eur. Phys. J. B 6, 543–550 (1998).

- [35] Easley, D. & O’Hara, M., Time and the process of security price adjustment. Journal of Finance 47, 905–927.

- [36] Peng, C.-K., et. al., Mosaic organization of DNA nucleotides. Phys. Rev. E 49, 1685–1689 (1994).

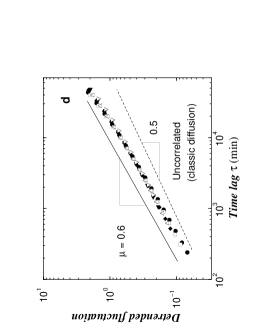

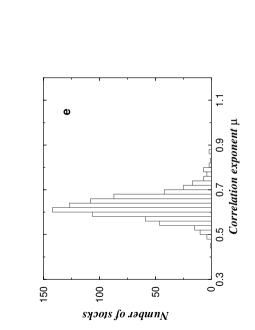

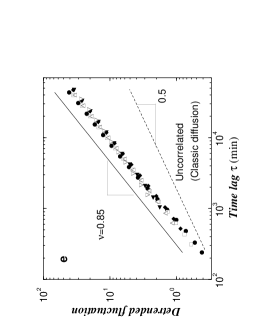

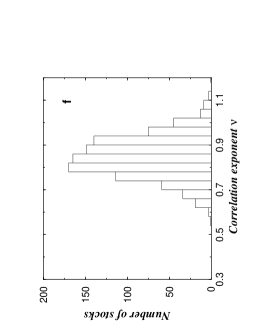

e) In order to accurately quantify time correlations in , we use the method of detrended fluctuations [36] often used to obtain accurate estimates of power-law correlations. We plot the detrended fluctuations as a function of the time scale on a log-log scale for each of the 6 groups. Absence of long-range correlations would imply , whereas with show power-law correlations with long-range persistence. For each group, we plot averaged over all stocks in that group. In order to detect genuine long-range correlations, the U-shaped intraday pattern for has been removed by dividing each by the intraday pattern [14]. For , correlation function exponent and are related through . f) The histogram of the exponents obtained by fits to for each of the 1000 stocks shows a relatively narrow spread of around the mean value .