The Values Distribution in a Competing Shares Financial Market Model

Abstract

We present our competing shares financial market model and describe it’s behaviour by numerical simulation. We show that in the critical region the distribution avalanches of the market value as defined in this model has a power-law distribution with exponent around . In this region the price returns distribution is truncated Levy stable.

Introduction and Model

Recent studiesMS1 of the S&P500 financial market index have

shown that financial markets are not appropriately described by the

Efficient Market Hypothesis which predicts a Gaussian type behaviour

of the price changes time series.pet1 In this paper we will

present a reinterpretation of our toy financial market model which was

presented in PA2 . That model was a trader based model, here

however we re-present that model as a share based system. That model

was a simplified mean-field version of our neural-network type

financial market model presented in PA1 . Although this model

was developed independently, it is a variant of the Minority

GameCZ , with however some fundamental differences. We explain

this model here as follows.

There are shares labeled (or commodities etc)

in a competetive market. Each share at time can be in one of two

states which classify the majority ownership crowd of the

share , ‘bull’, ‘bear’. Bulls have

bought the share, hoping to sell it later at a profit, bears have sold

the share hoping to buy it back later at a profit. The price returns

of each share are given by,

| (1) |

that is like excess demand, with price returns change being proportional to the ‘size’ of the market . Each share also has a generally perceived value , which ranks the shares . High valued shares have recognized long term price trend with therefore stuck, low volatility, states . Low valued shares on the other hand are short term risky states with high volatility. The state update dynamic is Darwinian competition; we choose two shares at random, say and with , then,

| (2) |

The shares therefore define a jammed flow of investors, long term

investors up the values, short term investors down the values. The

high valued shares become stuck in bull(bear) states because nobody

wants to sell(buy) them. In other words investors looking for long

term investments look for the low volatility high valued shares, and

therefore reinforce these shares price trends by trying to

take the corresponding position on them. Low valued shares on the

other hand are left in fluctuating states without any well-defined

price trend and therefore have high-volatilty since nobody knows which

way they are going. In this model therefore, both price trend and high

volatilty self-reinforce themselves. Hence the spin update dynamic

Eq.2, which basically says that high valued are low

volatility and low valued high volatility.

In reality a shares value is a complex function of individual company

news (affecting each share separately), macroscropic news(affecting

all shares), personal traits, the weather etc. However in this model

we model only the speculative behaviour of traders. The shares values

are therefore defined as follows,

| (3) |

where and our variable

‘groupthink’ is the overall market (macroeconomic) state, and

is the share index price return. Therefore the stuck shares (a)

have slowly decreasing value due to rise(fall) in the price of

bull(bear) states. Risky shares (b) however, which are the domain of

speculators and gamblers, increase in value when they move into the

minority state of the overall market. Here we are assuming that

the macroeconomic bull/bear state is coupled to the individual

share states in the same way as the usual Minority Game,

except on a larger scale.

This values update rule Eq.3 implies that the two main

observables for investors picking between shares are the individual

shares volatilities, which are related to the first term, and the

individual shares price trends, which are related to the second

term. Indeed long term investors may ‘play’ the observed price trends,

while short term speculators may ‘play’ the volatility.

Now we generalise the Darwinian evolution dynamic by defining a

probability for dynamic or update in Eq.2,i.e.

| (4) |

where is a kind of inverse temperature parameter, and

is the relative value, with

the mean-value (market-value).

This implies that indeed high valued shares are low volatility and low

valued shares high volatility, with a volatility gradient which

depends on the parameter . This simply replaces our dynamic of

randomly choosing two shares and and comparing the values.

This evolution dynamic is similar to co-evolution on coupled fitness

landscapesKauff1 ; BS ; SM1 , since the relative values

can change due to changes in or in a co-evolutionary sense

by changes in .

\epsfilefile=xn25ts.eps,height=9cm,width=15cm

Our dynamic is then that we first calculate and

and then we update all shares and according to

probability given by Eq.4. By putting we

obtain the deterministic system where if then

and otherwise . For the initial conditions for which we choose

uniformly randomly and uniformly

randomly.

A more general version of this model defines the

price changes by extending the definition Eq.1, to,

| (5) |

where are the relative values, which we believe is more realistic than the simple definition Eq.1. However in this paper we confine to Eq.1, since the study of Eq.5 is still in progress. This model resembles the MG. However it is different in two fundamental ways. 1) We only apply the minority rule when the state changes, that is the amount a shares value is updated according to the minority rule is proportional to it’s volatility across any time period. 2) There is no strategy space. We simply map straight from the values to the state update rule.

Results

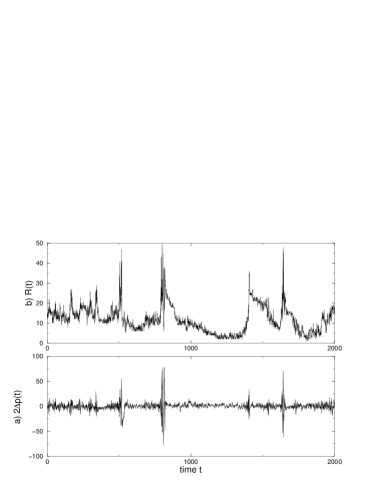

First we describe time series behaviour of the deterministic systemPA2 ; PA4 . Shown in Fig.1 are time series for . For small and large the values shows ‘Punctuated Equilibrium’GE type behaviour reminiscent of ecodynamics, i.e. avalanches and stasis periods.

In fact the avalanches are, to varying degrees, bursts of partial global synchronization where most of the share values cluster into 2 or more groups and interleave the mean-value, growing rapidly in a co-operative way (see Fig.Results), and represent an unstable attractor for the system. A few shares are left out and because this synchronization behaviour rapidly increases the values deviation we call these bursts ‘flights to quality’, like the phenomena which occur in real financial markets from time to time, such as the Russian Crisis in 1998.

They

occur due to the driving term decreasing and eventually

causing one value to cross the mean-value thereby possibly starting an

avalanche, and occur at small when the market is susceptible to

fluctuation (here internally generated by chaos).

Indeed at times of small nobody knows what is best to

invest in and panics and stampedes may occur due to wild speculation

(irrespective of the actual information contained in the item of news

which hit the market). These bursts show up as oscillations

(Fig.Results(b)) in the price changes time series , we

call them ‘market rollercoasters’. In fact the slightly oscillatory

nature of financial time series has been notedpet1 ; mand1 . The

price time series shown (Fig.Results(c)) is very reminiscent of the

technical-analysts ‘double tops’ and other recognized formations. In

this view a market will interpret rumour as good or bad dependent on

the current state , rather than on the value of the news itself,

such as when the meeting of James Baker and Tariq Aziz before the Gulf

War went on a little too long and caused a market rollercoaster. In

fact when a market is over-bought (most people in bull states) the

only way it can go is into sell mode and it is not so surprising that

momentum may carry it into an over-sold state.

\epsfilefile=xn26btcha.eps,height=8cm,width=16cm

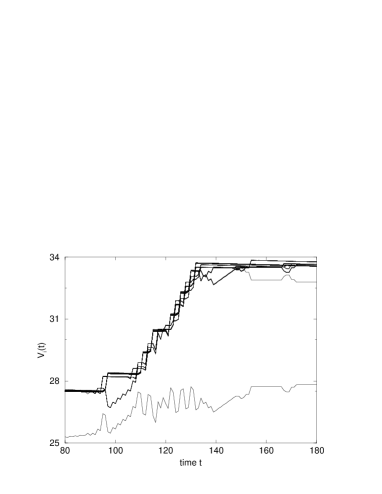

The most fundamental variables in our model are the values

rather than the prices and so we study their behaviour. A mean-values

time series is shown in Fig.Results. InPA2 we showed

that for small this system is critical in the sense that

avalanches, defined as size of changes in , have a power law

distribution with a peak due to the almost periodic state. Here we

show that the stasis periods also show such behaviour. Shown in

Fig.4(a) is the distribution of where is

the time between successive events , they are

normalized by dividing by the whole time series length

, after discarding a long transient. Only one

time series is included in this figure, so periods of stasis of all

sizes (limited by the system size) are always present. The slope of

the line is very near 1, which is a good fit for the longer

however at small there is an increase in probability due to

time spent in the almost periodic states. This shows that total

market value itself has a Punctuated Equilibrium time behaviour,

independent of ‘external’ information. External information may

however initiate an avalanche itself as mentioned above.

In fact more realistically we may study the stochastic system

defined by setting . We found that as we change

we see a phase transition, similar to that seen in the more

general MGCZ , of which this is model is a restricted

versionPA3 . Furthermore in the transition region the price

returns distribution defined by Eq.1 shows a Levy

distributionLP1 ; LP2 for the central values, while for values

after about four standard deviations from the mean there is a drop-off

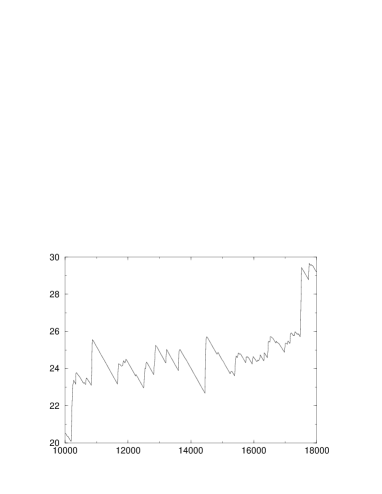

of the probability.PA3 Time series in this region at

are shown in Fig.Discussion.

The parameter characterising the Levy distribution we found was about 1.5 which is very similar to the actual distribution for the measured by Mantegna and StanleyMS1 . Here we show that the corresponding mean-value changes distributions at still show a good scaling behaviour, where however the exponents have changed. Shown in Fig.4(b) is the distribution and in Fig.6 the distribution of changes , divided into both positive and negative contributions. Again only one time series of length was included. The exponents have changed from near 1 for the deterministic system to around as shown in the figure captions.

\epsfilefile=xn26btposneg.eps,height=7cm,width=16cm

Recent workGOP has studied price returns distributions for the and found that while the central region of the distribution may be characterised by a Levy stable distribution with parameter between 1.35-1.8 the tails fall off with an exponent of around 3. We are at present studying the behaviour of the tails of the price returns distributions for both Eq.1 and Eq.5, which may be more appropriate, to see if they give the correct results.

Discussion

This model may seem naive but it seems to well-reproduce many observed characteristics of financial market time series, including qualitative features. Furthermore it is built on fairly simple assumptions and can explain results that other models based on a single share cannot, for example the fact that usually all shares crash together, and that all individual shares have similar distributions.Pler . This should be investigated further. This model predicts many interesting relationships between share prices, especially the values deviation . To what extent the behaviour of corresponds with reality is under investigation.

References

- (1) A. Ponzi and Y. Aizawa, Chaos, Solitons and Fractals (received 1999.1). A.Ponzi, Masters Thesis, Waseda University, (1996) (Unpublished)

- (2) A. Ponzi and Y. Aizawa, Chaos, Solitons and Fractals (received 1999.3).

- (3) A. Ponzi and Y. Aizawa, submitted to Physica A.

- (4) A. Ponzi and Y. Aizawa, submitted to Physical Review.

- (5) R.N Mantegna, H. Eugene Stanley, Nature 376 46-49 (1995)

- (6) D.Challet and Y-C. Zhang, Physica A 256 514-532, (1998). D.Challet and Y-C. Zhang, cond-mat/9904071.

- (7) S.A.Kauffman and S.Johnsen, J.Theor.Biol. 49 467-505, (1991)

- (8) P. Bak and K. Sneppen, Phys. Rev. Lett. 71 4, 4083-4086, (1993). H. Flyvbjerg, K. Sneppen, P. Bak, Phys. Rev. Lett. 71 24, 4087-4090, (1993).

- (9) R.V. Sole and S.C. Manrubia, Phys. Rev. E, 55 4, 4500-4507. (1997)

- (10) S.J. Gould, N. Eldredge, Nature. 366 223, (1993).

- (11) E.E.Peters, Fractal Market Analysis: Applying Chaos Theory to Investment and Economics. John Wiley. (1994)

- (12) B.B Mandlebrot, J.Business 36 394-419 (1963)

- (13) M.F. Schlesinger, U. Frisch and G. Zaslavsky,(eds) Levy Flights and Related Phenomena in Physics Springer, Berlin 1995.

- (14) J.P Bouchaud and A. Georges, Anomalous Diffusion in Disordered Media Phys. Rep 195 127-293, (1990)

- (15) P. Gopikrishnan, Vasiliki Plerou, L.A.Nunes Amaral, Martin Meyer, H.Eugene Stanley, cond-mat/9905305

- (16) V.Plerou, P.Gopikrishnan, .A.Nunes Amaral, Martin Meyer, H.Eugene Stanley, cond-mat/9907161