[

Capital flow in a two-component dynamical system

Abstract

A model of open economics composed of producers and speculators is investigated by numerical simulations. The capital flows from the environment to the producers and from them to the speculators. The price fluctuations are suppressed by the speculators. When the aggressivity of the speculators grows, there is a transition from the regime with almost sure profit to a very risky regime in which very small fraction of speculators have stable gain. The minimum of price fluctuations occurs close to the transition.

pacs:

PACS numbers: 05.40.-a, 89.90.+n]

I Introduction

Economy is an intriguing complex dynamical system, understanding of which has vital importance to the society [1, 2, 3, 4]. From the point of view of a physicist, it may be seen as a natural phenomenon, whose microscopic “laws of motion” should be discovered and consequences drawn from them, amenable to experimental verification (or falsification). Statistical physics is successfully involved in investigation of various collective dynamic phenomena, which come from interdisciplinary areas, like car traffic [5], city growth [6], pedestrian dynamics [7], forest fires [8], river networks [9] or biological evolution [10].

Like in these problems, numerical simulations of various “minimal” models of economic behavior [11, 12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23, 24, 25, 26, 27, 28, 29] play important role, in parallel with analytical approaches [29, 30, 31, 32, 33, 34, 35, 36]. Even though the hope of detailed prediction of the future market behavior could be (at least very probably) rarely satisfied, the knowledge of parameters, which are crucial for the probabilistic properties of the economic events is very important to the decision-makers on all levels.

One group of models investigated so far is based on threshold dynamics of the players in the market [11, 12, 13] which was shown to be equivalent to a stochastic process with both multiplicative and additive noise [32, 13] which then leads naturally (see e. g. [37, 38, 39, 40]) to the power law tails in the distribution of price changes, which are observed in reality[41]. Similar in spirit are the models based on a diffusion-annihilation process, where buyers and sellers are considered as particles which disappear once they meet [14, 33]. The percolation theory was invoked to account for the herd behavior of market agents [30, 31, 15, 42], which gives a power law distribution truncated by an exponential, if the connectivity of players is close but not exactly at the percolation threshold. This is in accord with the “truncated Lévy” distribution found in more refined recent analyses of stock market data [43, 30, 44, 45]. A model based on non-linear Langevin equation was developed [34] in order to explain the apparent “phase transition” character of market crashes, proposed recently by several authors. (See e. g. [46, 47, 48, 49, 50, 51].)

Another model, which implements on-line adaptation of the community of players [17] is able to reproduce very well also the scaling of price changes [44, 45, 52, 53]. More abstract approach is used in the minority game model [18, 19, 20, 21, 22, 23, 24, 25, 26, 27, 28, 29], where real money is lacking. An important feature of this model is the presence of a transition from chaotic to periodic phase, when the number of players is increased. (It is quite interesting, that similar transition seems to take place also in the threshold dynamics model [13]; when increasing the number of players, we may pass from the intermittent behavior characterized by power-law tails to an ordinary random-walk process. However, this phenomenon was not explicitly investigated in [13].)

In our model, we want to take into account the fact, that there are at least two types of investors. First, there are individuals who product some commodity and need other commodities to keep the production on. It is the latter type of economical subject, that the market was originally designed for. However, the second type of investor comes soon, a speculator, who observes the price changes due to disequilibrium between demand and offer, and makes profit from the information carried by the price signal. However, it is expected, that the influence of speculators is not at all purely negative. When they discover some regularity in the price fluctuations, they make many of it, but at the same time their activity has a feedback effect on the price, so that the very fluctuations the speculators are exploiting are destroyed. In fact, this may lead to overall decrease of price fluctuations, making the market more stable.

The question is, whether this common sense reasoning can be supported by more rigorous arguments. The scope of the present work is to implement a model of market, in which the mutual influence of producers and speculators may be studied.

II Description of the two-component model

Economy is an open system. Like thermodynamic systems can self-organize into a low-entropy state only under condition that there is flow of energy through the system, non-trivial self-organization in the market is driven by the supply of wealth from the surrounding environment. So, first fundamental players in the economic game are producers, which exploit the outside opportunities. In our model, their real economic activity will be mimicked by buying and selling a single commodity in a regular manner. For simplicity, we will call it stock. Each producer is supplied periodically fixed amount of stock and money from the outside.

Real market needs also speculators, which play a positive role in absorbing temporary disequilibrium of demand and offer. The result is a more liquid market with reduced fluctuations. The speculators are selfish, but without any explicit wish, besides the net gain. We may look at them as providers of a service, for which they are paid. However, none of them provides individually a specific service, but their utility stems from a collective effect.

An important feature of our model is the possibility of both producers and speculators to abstain from the game, if they feel that it does not pay to participate. So, the number of players in each group is self-adjusted, depending on the parameters of the model. This is similar in spirit to the grand-canonical ensemble in statistical physics.

Borrowing the biological terminology, the producers are “autotrophs” who live in a symbiosis with “heterotrophic” speculators. Like in biological communities, we implement here also Darwinian evolution of the speculators, so that they adapt collectively to the actions of producers.

Let us be more specific now. The dynamical system we are going to investigate is a simplified model of a market, in discrete time. In each step, some amount of stock is traded. The price of stock as a function of time is the output signal of the market. The price is the manifestation of large amount of “microscopic” activity due to players on the market. Each player is characterized by two dynamical variables, the amount of stock and the amount of money , where index denotes the player. So, the total capital owned at time by ’th player is .

There are two kinds of players in our model. There are producers and speculators. We denote the total number of players. The producers follow a fixed strategy of buying and selling, irrespective of the current or past price. On the other hand, the decisions of speculators are based on the analysis of the past evolution of price.

The strategies are characterized as follows. Each producer, has its own period and time-scale on which he or she invests. The periods are chosen randomly among numbers 2 to 6, the time-scales randomly from 7 to 10. The investment follows a random but quenched pattern , . In order to avoid a systematic excess on the demand or offer side, we require that the investment is balanced for each producer, . Apart from this constraint, the ’s are drawn from uniform distribution on the interval Finally, all producers are given the same overall amplitude of their investment . At the time step , the producer participates, if he or she has positive capital. In this case, he or she attempts to buy the following amount of the commodity

| (1) |

In this formula, we denote by integer division of by and is the average wealth of the players. The last term with the logarithm expresses the fact, that the stock has its intrinsic value. Its price is measured relatively to the average wealth of the population, so that if the price is larger, the strategy of the producer is slightly biased towards selling, while if the price is lower, the producer is more likely to buy. The use of logarithm follows from the fact, that the evolution of price is a multiplicative process, rather than additive one. Analogical term plays a crucial role also in the analytic approach of Ref. [34]. The parameter measures the strength of the bias caused by the intrinsic value of the commodity. Throughout this article, we use the value .

The speculators differ from the producers in two aspects. First, they do not feel the intrinsic value of the traded product, so that the logarithmic term in the Eq. (1) is missing. But the crucial difference resides in the ability of speculators to analyze the past price signal and decide according to their expectations about the future. As the producers do, the speculators may have their time-scales on which they analyze the signal and also different memory length. However, in the present work we limit ourselves only to the case when all speculators have their time-scale equal to one step of the dynamics and memory is fixed and uniform in the whole community of speculators.

The speculators have memory . It means that they are able to use information of previous values of price, . This sequence is then transformed in a bit string containing the information whether the price went up or down in a given instant in the past. We adopted the convention that 0 means increase and 1 means decrease of the price. Therefore , where is the Heaviside function. The strategy of the -th speculator is the function which prescribes for each bit string, whether the speculator should buy or sell. We adopt the convention, that 0 means selling and 1 buying. Then the strategy is a function with possible values 0 or 1.

The strategy has a score counting its success rate at time . If it predicted correctly the change of the price from step to one point is added to the score, otherwise one point is subtracted. There is in principle a non-trivial question, what we mean by saying “predicted correctly the price change”. In fact, it should be checked a posteriori that the rule we used for distinguishing successful strategies corresponds really to winning behavior. However, in our model, we used a prescription for price change, which enables us to say a priori which strategy did a good job. At this moment, we present the rule of success rate counting and return to the justification of this rule later, when we will speak of the prescription for price change. The essence is, that it is good to buy if the price will go down and vice versa. So, when the player is inserted in the market, its score is set to zero, and in each successive step, the score is updated as follows: if and in the opposite case.

There is a Darwinist selection among speculators. Each 5 steps, the speculator with lowest capital is removed and replaced by new player with newly chosen strategy. However, the capital, amount of stock and money is inherited from the removed player. This amounts to not really remove the player, but rather the player picks new strategy instead of the old doomed one. We define the age of speculator as number of time steps since the last replacement of the strategy. We implemented also random mutations, which affect equally good and bad players. Each 57 steps a player is chosen at random and its strategy is randomly changed.

If the speculator feels, that the strategy is bad, he or she may abstain, in order to avoid losses. For the player to participate, we require that .

Those speculators, who do participate, attempt to buy the following amount of stock:

| (2) |

When we know what amount of stock the players want to buy or sell, we can compute the change of price. It is not clear a priori what precisely the price change should be. The only obvious requirement is, that the price should go up, when there is more demand than offer, and go down, when the offer prevails. The demand is and the offer . In the previous works, two recipes for the price change were used. In [17] the time averages of demand and offer were computed and new price was obtained by multiplying the old price by the ratio of average demand to average offer. Essentially the same prescription is applied in [34].

On the other hand, within the approaches based on threshold dynamics or diffusion-annihilation processes [13, 14] the deal is realized when the bid and ask prices meet, which determines the reported stock price at that moment. (It is interesting to note, that between the deals the price is undefined.)

Here we adopt an approach closer to the former one. The new price is computed by multiplying the old price by a factor, which increases with the ratio .

| (3) |

where the function should obey two conditions, and . The simplest choice consists in taking , but as we have seen in our simulations, this leads to price fluctuations far beyond realistic values. So, we use a non-linear form which suppresses the fluctuations,

| (4) |

which has the property that for close to 1. We have found that gives realistic price fluctuations, so we keep this value throughout the simulations.

There should be conservation of stock in each trade event. Therefore the amount actually traded by a single player is not the same as the attempted volume. If then if , actual change of stock is lower than attempted, . If the actual traded amount is the same as attempted, .

If on the contrary then if , , if , .

After the trade is completed, the new amount of capital, stock and money is

| (5) | |||||

| (6) | |||||

| (7) |

Finally, each 120 steps, the producers receive wealth from outside. The value of the influx is governed by the parameter . The total amount distributed among producers is , but who do not participate in that moment, does not receive anything. If is the fraction of currently participating producers, those who do participate, increase their capital by .

Summarizing the algorithm which defines our model, the following operations are performed in each step.

(i) Calculate amount of the commodity, attempted to buy by producers (Eq. (1)) and speculators (Eq. (2)).

The following actions are performed periodically.

(iv) If the step is a multiple of 57, randomly chosen speculator changes randomly its strategies. If the step is a multiple of 120, wealth is added to producers.

An important property of the above algorithm is that the game has minority character. Indeed, because the price is established after the attempted traded amounts were fixed, it is an advantage to sell, if the price goes up and buy, when the price comes down. Therefore this means that going counter the majority is an. This enables us to decide, what score should be attributed to the strategies: those leading to minority side receive +1 point, those which lead to majority side, receive -1 point. In the abstract minority game [18, 19] it was possible only for less than half players to be on the minority side, of course. The presence of producers, however, makes it possible for any number of speculators to have minority strategy, at least in principle.

III Results

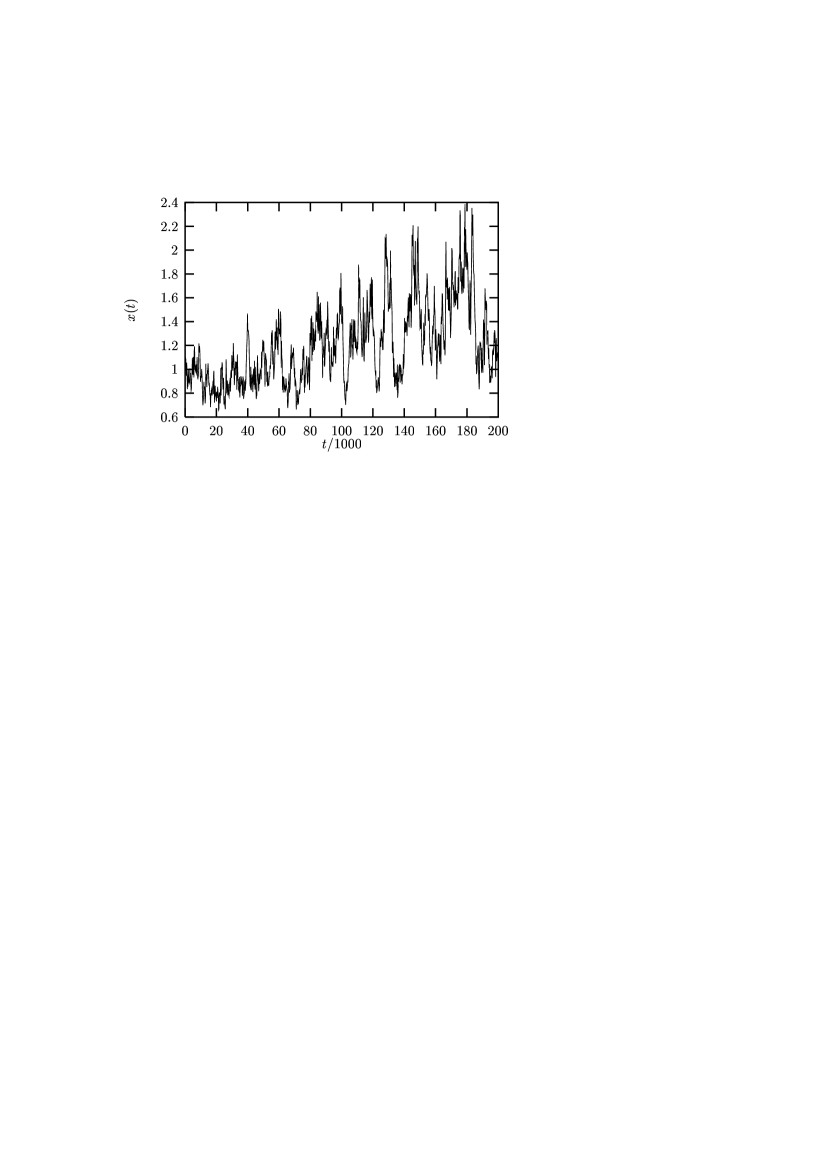

The fundamental variable of our model is the price. A typical time evolution of price is shown in Fig. 1. The long-time average of price grows, due to the fact, that capital is regularly injected into the system. We observed, that the increase of price is higher if the capital influx is higher. We measured also the price fluctuations. We observed, that the relative price fluctuations remain constant in the long-time average, so that the absolute fluctuations grow with time with the same rate as the long-time average of price does.

One of the main questions is, how the relative price fluctuations is changed by the presence of the speculators. We define the the time-averaged relative price fluctuations using exponential averages [17]

| (8) |

where is duration of the simulation run and the parameter was chosen .

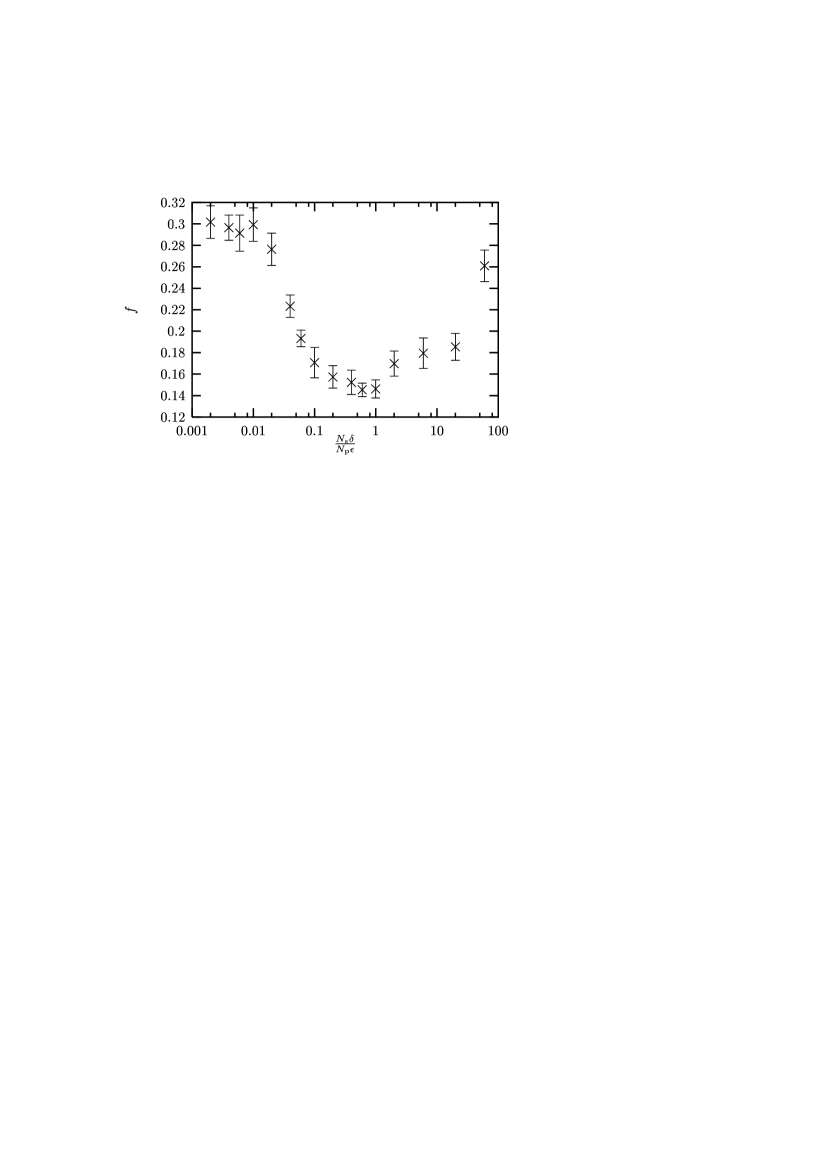

The relative weight of the speculators compared with the producers is the quantity . Figure 2 shows the dependence of the time-averaged relative price fluctuations on . We can see a pronounced minimum around , which suggests, that from the point of view of the price stability, there is an optimal weight of the speculators.

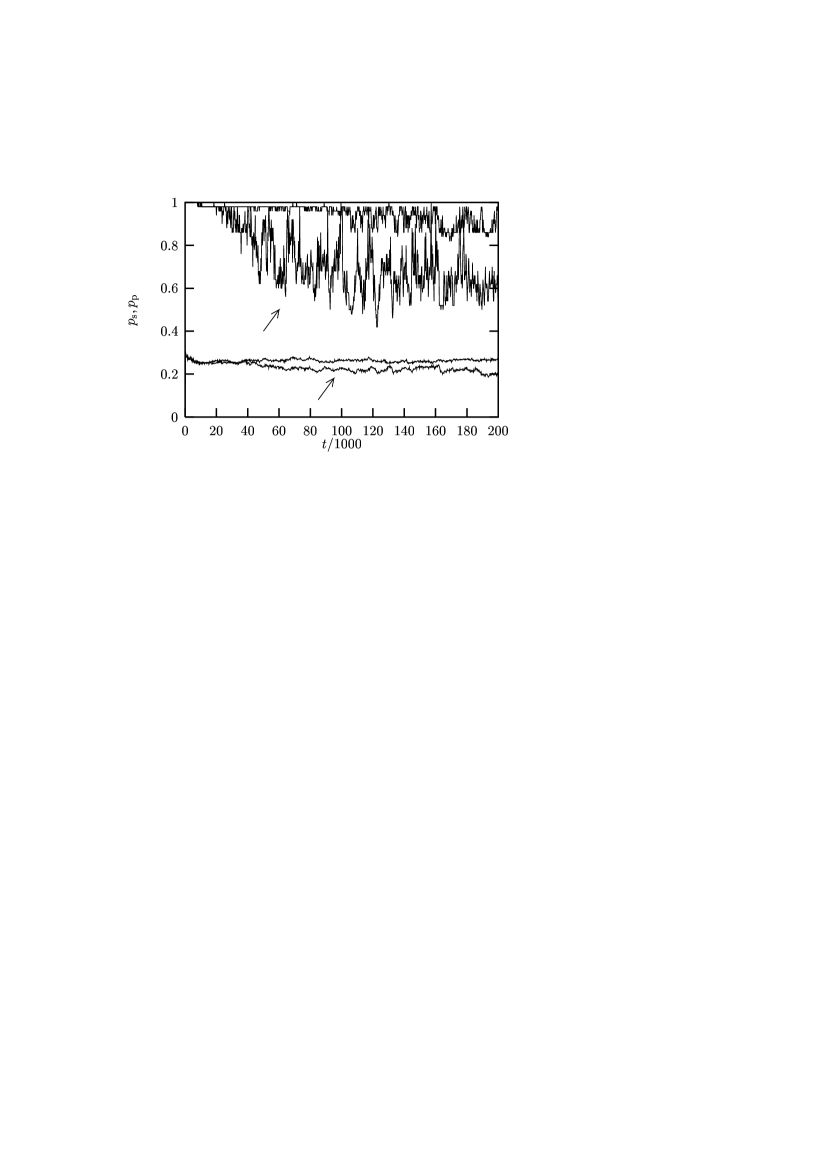

This phenomenon can be better understood, when we observe the participation of producers () and speculators (), defined as the percentage of those, who take part in the trading. The Fig. 3 shows the time dependence of the participation in a typical run.

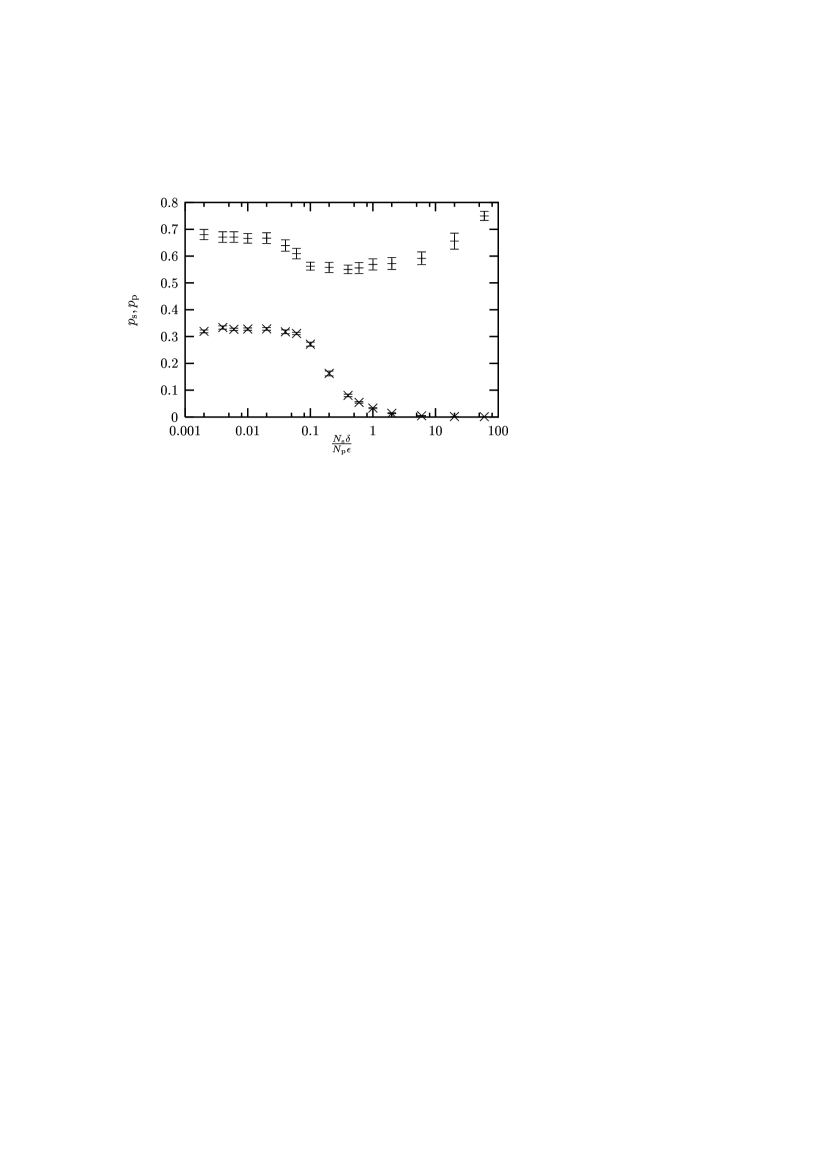

After a transient period, the participation fluctuates around a stationary value, which grows with the capital influx . The dependence of the time-averaged participation on the parameter is shown in the Fig. 4. The most important observation is the substantial decrease of the participation of the speculators for the value of close to . The participation of producers has a shallow minimum around the same value , which is also close to the position of the minimum in the relative price noise.

The following picture arises from these observations. If the speculators are too prudent (small ), the price fluctuations are high, because of the demand-offer disequilibrium. The price changes follow a periodic pattern induced by the periodic quenched pattern of trading of each individual producer. Speculators are able to extract the information about the periodic price changes and use it to make profit. Because they trade with little capital (low ) they do not influence much the price and many speculators can gain. On the other hand, the gain is also small.

If the investors became more aggressive, by increasing , they have larger influence on the price, which leads to the suppression of the price fluctuations, but at the same time their ability to use the periodic price fluctuations to make profit is also suppressed. This results in the fact, that less speculators have successful strategy and less speculators participate.

There is a transition between the low-aggressivity regime, where many speculators make little profit, and the high-aggressivity regime, where few speculators can make large profit. The transition occurs around and it is characterized by optimum of the relative price noise and also by the minimum of the participation of the producers, which means that less producers are able to gain. The advantage is more stable price, the disadvantage is less profit for the producers. This is a manifestation of the common sense consideration, repeated in all economics literature, stating that higher profit is more risky.

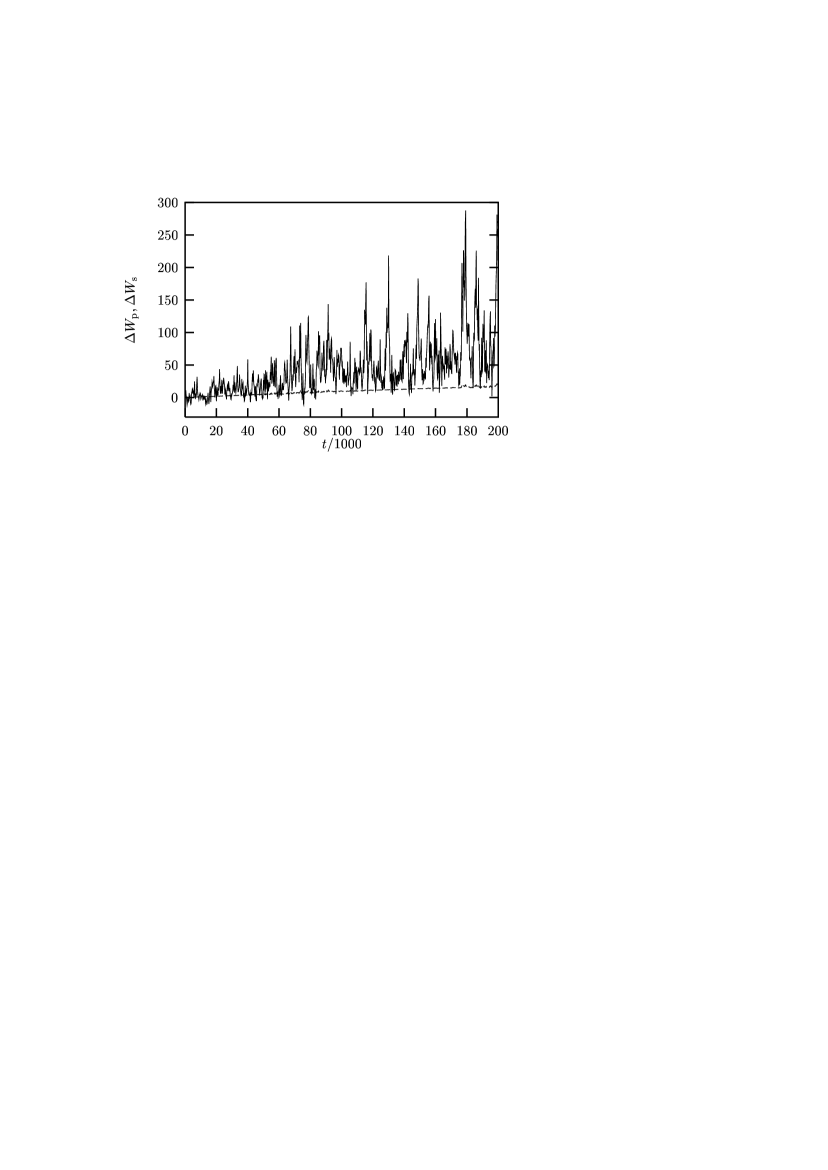

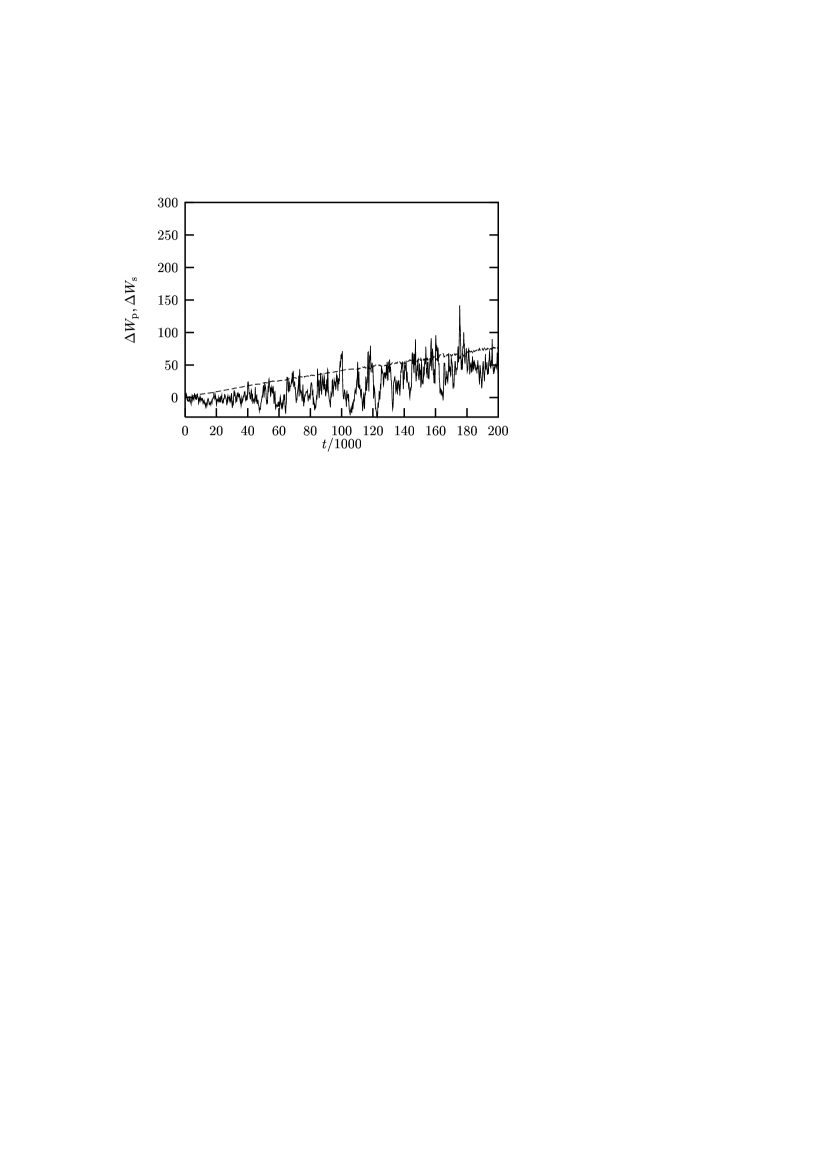

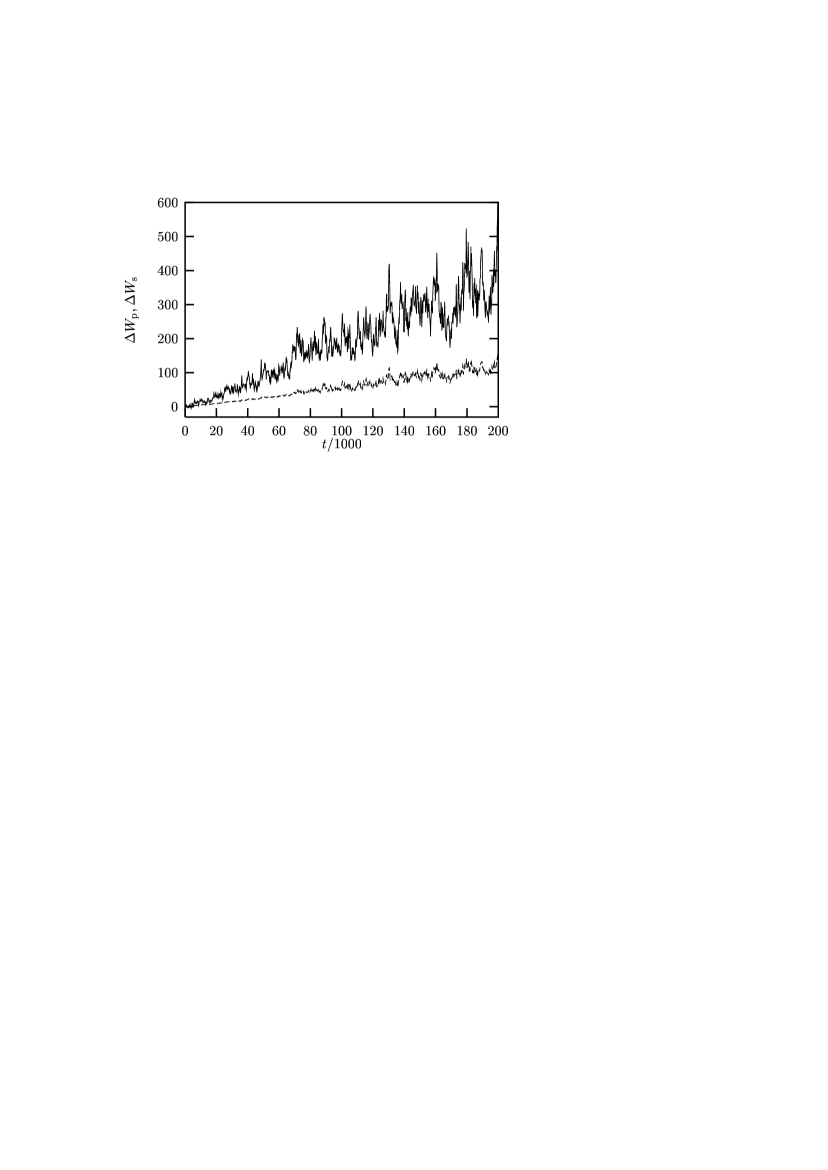

In Figs. 5 and 6 the situation is illustrated by time evolution of the increase of the total wealth of producers and speculators, defined by

| (9) | |||||

| (10) |

Lower (Fig. 5) is characterized by large fluctuations of the capital of the producers, while capital of the speculators grows slowly. When the is larger (Fig. 6), the capital of producers fluctuates less, but the speculators have significantly larger profit.

The influence of the influx of capital into the system, measured by the parameter , can be seen by comparing the Figs. 6 and 7. The picture remains the same qualitatively, however larger influx means larger profit preferably for the producers, while the increase of the profit of the speculators is much lower. The Fig. 3 shows, that the participation of the producers is much more influenced by the parameter than the participation of the speculators.

IV conclusions

We introduced and studied a model of open economics. The influx of capital leads to the coexistence of producers and speculators. We showed, that the presence of the speculators can be useful to the economics, by suppression of the price fluctuations. If we increase the aggressivity of the speculators, there is a smooth transition from the regime with small, but less risky profit for the speculators, to the regime with larger profit, but accessible to smaller fraction of the set of the speculators. The transition occurs close to the minimum of the price fluctuations, which is the optimal state for the producers. If we accept the supposition, that the optimal strategy for the speculators should be derived by a compromise of the mutually exclusive requirements of risk and profit, we can conclude, that the optimum for the speculators lies also in the transition region. As a result, the optima for producers and speculators lie close one to the other, and their mutual coexistence should be better described as symbiosis than parasitism.

Acknowledgements.

We acknowledge the support from the European TMR Network-Fractals c.n. FMRXCT980183. F.S. wishes to thank the University of Fribourg, Switzerland, for the financial support and kind hospitality.REFERENCES

- [1] P. W. Anderson, K. J. Arrow, and D. Pines (eds.), The Economy as an Evolving Complex System (Addison Wesley, 1988).

- [2] J.-P. Bouchaud, P. Cizeau, L. Laloux, and M. Potters, Phys. World 12 (January 1999) 25.

- [3] Y.-C. Zhang, Europhysics News 29 (1998) 51.

- [4] M. Ausloos, Europhysics News 29 (1998) 70.

- [5] K. Nagel and M. Paczuski, Phys. Rev. E 51 (1995) 2909.

- [6] M. Marsili and Y.-C. Zhang, Phys. Rev. Lett. 80 (1998) 2741.

- [7] D. Helbing, F. Schweitzer, J. Keltsch, and P. Molnar, Phys. Rev. E 56 (1997) 2527.

- [8] B. Drossel and F. Schwabl, Phys. Rev. Lett. 69 (1992) 1629.

- [9] J. R. Banavar, F. Colaiori, A. Flammini, A. Giacometti, A. Maritan, and A. Rinaldo, Phys. Rev. Lett. 78 (1997) 4522.

- [10] M. Paczuski, S. Maslov and P. Bak, Phys. Rev. E 53 (1996) 414.

- [11] H. Takayasu, H. Miura, T. Hirabayashi, and K. Hamada, Physica A 184 (1992) 127.

- [12] T. Hirabayashi, H. Takayasu, H. Miura, and K. Hamada, Fractals 1 (1993) 29.

- [13] A.-H. Sato and H. Takayasu, Physica A 250 (1998) 231.

- [14] P. Bak, M. Paczuski, and M. Shubik, Physica A 246 (1997) 430.

- [15] D. Stauffer and T. J. P. Penna, Physica A 256 (1998) 284.

- [16] C. Busshaus and H. Rieger, cond-mat/9903079.

- [17] G. Caldarelli, M. Marsili, and Y.-C. Zhang, Europhys. Lett. 40 (1997) 479.

- [18] D. Challet and Y.-C. Zhang, Physica A 246 (1997) 407.

- [19] D. Challet and Y.-C. Zhang, Physica A 256 (1998) 514.

- [20] R. Savit, R. Manuca, and R. Riolo, Phys. Rev. Lett. 82 (1999) 2203.

- [21] N. F. Johnson, S. Jarvis, R. Jonson, P. Cheung, Y. R. Kwong, and P. M. Hui, Physica A 258 (1998) 230.

- [22] R. Manuca, Y. Li, R. Riolo, and R. Savit, adap-org/9811005.

- [23] N. F. Johnson, M. Hart, P. M. Hui, cond-mat/9811227.

- [24] N. F. Johnson, P. M. Hui, R. Jonson, and T. S. Lo, Phys. Rev. Lett. 82 (1999) 3360.

- [25] M. A. R. de Cara, O. Pla, and F. Guinea, cond-mat/9811162.

- [26] A. Cavagna, Phys. Rev. E 59 (1999) R3783.

- [27] A. Cavagna, J. P. Garrahan, I. Giardina, and D. Sherrington, cond-mat/9903415.

- [28] D. Challet and M. Marsili, cond-mat/9904071.

- [29] D. Challet, M. Marsili, and R. Zecchina, cond-mat/9904392.

- [30] J.-P. Bouchaud and M. Potters, Théorie des risques financiers (Aléa, Saclay, 1997).

- [31] R. Cont and J.-P. Bouchaud, cond-mat/9712318.

- [32] H. Takayasu, A.-H. Sato, and M. Takayasu, Phys. Rev. Lett. 79 (1997) 966.

- [33] D. Eliezer and I. I. Kogan, cond-mat/9808240.

- [34] J.-P. Bouchaud and R. Cont, Eur. Phys. J. B 6 (1998) 543.

- [35] S. Galluccio, J.-P. Bouchaud, and M. Potters, Physica A 259 (1998) 449.

- [36] M. Marsili and Y.-C. Zhang, Physica A 245 (1997) 181.

- [37] I. T. Drummond, J. Phys. A: Math. Gen. 25 (1992) 2273.

- [38] D. Sornette and R. Cont, J. Phys I France 7 (1997) 431.

- [39] D. Sornette, Physica A 250 (1998) 295.

- [40] D. Sornette, Phys. Rev. E 57 (1998) 4811.

- [41] R. N. Mantegna, Physica A 179 (1991) 232.

- [42] D. Chowdhury and D. Stauffer, cond-mat/9810162.

- [43] R. N. Mantegna and H. E. Stanley, J. Stat. Phys. 89 (1997) 469.

- [44] R. Cont, M. Potters, and J.-P. Bouchaud, cond-mat/9705087.

- [45] J.-P. Bouchaud, cond-mat/9806101.

- [46] D. Sornette, A. Johansen and J.-P. Bouchaud, J. Phys. I France 6 (1996) 167.

- [47] D. Sornette and A. Johansen, Physica A 245 (1997) 411.

- [48] N. Vandewalle, M. Ausloos, Ph. Boveroux, and A. Minguet, Eur. Phys. J. B 4 (1998) 139.

- [49] D. Sornette and A. Johansen, Physica A 261 (1998) 581.

- [50] L. Laloux, M. Potters, R. Cont, J.-P. Aguilar and J.-P. Bouchaud, Europhys. Lett. 45 (1999) 1.

- [51] A. Johansen and D. Sornette, Eur. Phys. J. B 9 (1999) 167.

- [52] R. N. Mantegna and H. E. Stanley, Nature 376 (1995) 46.

- [53] S. Galluccio, G. Caldarelli, M. Marsili, and Y.-C. Zhang, Physica A 245 (1997) 423.