Critical Crashes

Anders Johansen1 and Didier Sornette1,2,3

1 Institute of Geophysics and Planetary Physics

University of California, Los Angeles, California 90095

2 Department of Earth and Space Science

University of California, Los Angeles, California 90095

3 Laboratoire de

Physique de la Matière Condensée

CNRS UMR6622 and Université des

Sciences, B.P. 70, Parc Valrose

06108 Nice Cedex 2, France

Abstract : The authors argue that the word “critical” in the title is not purely literary. Based on their and other previous work on nonlinear complex dynamical systems, they summarize present evidence, on the Oct. 1929, Oct. 1987, Oct. 1987 Hong-Kong, Aug. 1998 global market events and on the 1985 Forex event, for the hypothesis advanced three years ago that stock market crashes are caused by the slow buildup of long-range correlations between traders leading to a collapse of the stock market in one critical instant.

1 Crashes are outliers

It is well-known that the distributions of stock market returns exhibit “fat tails”, deviating significantly from the time-honored Gaussian description : a dayly loss occurs approximately once every two years while the Gaussian framework would predict one such loss in about a thousand year.

Crashes are of an even more extreme nature. We have measured the number of times a given level of drawn down has been observed in this century in the Dow Jones daily Average [1]. A draw down is defined as the cumulative loss from the last local maximum to the next minimum. is well fitted by an exponential law

| (1) |

However, we find that three events stand out blatantly. In chronological order: World War 1 (the second largest), Wall Street Oct. 1929 (the third largest) and Wall Street Oct. 1987 (the largest). Each of these draw down lasted about three days. Extrapolating the exponential fit (1), we estimate that the return time of a draw down equal to or larger than would be more than centuries. In contrast, the market has sustained two such events in less than a century. This suggests a natural unambiguous definition for a crash, as an outlier, i.e., an extraordinary event with an amplitude above [1].

Large price movements are often modeled as Poisson-driven jump processes. This accounts for the bulk of the statistics. However, the fact that large crashes are outliers implies that they are probably controlled by different amplifying factors, which can lead to observable precursory signatures. Here, we propose that large stock market crashes are analogous to “critical points”, a technical term in Physics which refers to regimes of large-scale cooperative behavior such as close to the Curie temperature when the millions of tiny magnets in a bar magnet start to influence each other and eventually end up all pointing in one direction. We present the theory and then test it against facts.

2 A rational imitation model of crashes

Our model contains the following ingredients [2] :

-

1.

A system of traders who are influenced by their “neighbors”;

-

2.

Local imitation propagating spontaneously into global cooperation;

-

3.

Global cooperation among traders causing crash;

-

4.

Prices related to the properties of this system.

The interplay between the progressive strengthening of imitation controlled by the three first ingredients and the ubiquity of noise requires a stochastic description. A crash is not certain but can be characterized by its hazard rate , i.e., the probability per unit time that the crash will happen in the next instant if it has not happened yet.

The crash hazard rate embodies subtle uncertainties of the market : when will the traders realize with sufficient clarity that the market is overvalued? When will a significant fraction of them believe that the bullish trend is not sustainable? When will they feel that other traders think that a crash is coming? Nowhere is Keynes’s beauty contest analogy more relevant than in the characterization of the crash hazard rate, because the survival of the bubble rests on the overall confidence of investors in the market bullish trend.

A crash happens when a large group of agents place sell orders simultaneously. This group of agents must create enough of an imbalance in the order book for market makers to be unable to absorb the other side without lowering prices substantially. One curious fact is that the agents in this group typically do not know each other. They did not convene a meeting and decide to provoke a crash. Nor do they take orders from a leader. In fact, most of the time, these agents disagree with one another, and submit roughly as many buy orders as sell orders (these are all the times when a crash does not happen). The key question is to determine by what mechanism did they suddenly manage to organise a coordinated sell-off?

We propose the following answer [2] : all the traders in the world are organised into a network (of family, friends, colleagues, etc) and they influence each other locally through this network : for instance, an active trader is constantly on the phone exchanging information and opinions with a set of selected colleagues. In addition, there are indirect interactions mediated for instance by the media. Specifically, if I am directly connected with other traders, then there are only two forces that influence my opinion: (a) the opinions of these people and of the global information network; and (b) an idiosyncratic signal that I alone generate. Our working assumption here is that agents tend to imitate the opinions of their connections. The force (a) will tend to create order, while force (b) will tend to create disorder. The main story here is a fight between order and disorder. As far as asset prices are concerned, a crash happens when order wins (everybody has the same opinion: selling), and normal times are when disorder wins (buyers and sellers disagree with each other and roughly balance each other out). We must stress that this is exactly the opposite of the popular characterisation of crashes as times of chaos. Disorder, or a balanced and varied opinion spectrum, is what keeps the market liquid in normal times. This mechanism does not require an overarching coordination mechanism since macro-level coordination can arise from micro-level imitation and it relies on a realistic model of how agents form opinions by constant interactions.

In the spirit of “mean field” theory of collective systems [3], the simplest way to describe an imitation process is to assume that the hazard rate evolves according to the following equation :

| (2) |

where is a positive constant. Mean field theory amounts to embody the diversity of trader actions by a single effective representative behavior determined from an average interaction between the traders. In this sense, is the collective result of the interactions between traders. The term in the r.h.s. of (2) accounts for the fact that the hazard rate will increase or decrease due to the presence of interactions between the traders. The exponent quantifies the effective number equal to of interactions felt by a typical trader. The condition is crucial to model interactions and is, as we now show, essential to obtain a singularity (critical point) in finite time. Indeed, integrating (2), we get

| (3) |

The critical time is determined by the initial conditions at some origin of time. The exponent must lie between zero and one for an economic reason : otherwise, as we shall see, the price would go to infinity when approaching (if the bubble has not crashed in the mean time). This condition translates into : a typical trader must be connected to more than one other trader. There is a large body of literature in Physics, Biology and Mathematics on the microscopic modeling of systems of stochastic dynamical interacting agents that lead to critical behaviors of the type (3) [4]. The macroscopic model (2) can thus be substantiated by specific microscopic models [2].

The critical time signals the death of the speculative bubble. We stress that is not the time of the crash because the crash could happen at any time before , even though this is not very likely. is the most probable time of the crash. There exists a finite probability

| (4) |

of “landing” smoothly, i.e. of attaining the end of the bubble without crash. This residual probability is crucial for the coherence of the model, because otherwise agents would anticipate the crash and not remain in the market.

Assume for simplicity that, during a crash, the price drops by a fixed percentage , say between and of the price increase above a reference value . Then, the dynamics of the asset price before the crash are given by:

| (5) |

where denotes a jump process whose value is zero before the crash and one afterwards. In this simplified model, we neglect interest rate, risk aversion, information asymmetry, and the market-clearing condition.

As a first-order approximation of the market organization, we assume that traders do their best and price the asset so that a fair game condition holds. Mathematically, this stylized rational expectation model is equivalent to the familiar martingale hypothesis:

| (6) |

where denotes the price of the asset at time and denotes the expectation conditional on information revealed up to time . If we do not allow the asset price to fluctuate under the impact of noise, the solution to Equation (6) is a constant: , where denotes some initial time. can be interpreted as the price in excess of the fundamental value of the asset.

| (7) |

In words, if the crash hazard rate increases, the return increases to compensate the traders for the increasing risk. Plugging (7) into (5), we obtain a ordinary differential equation. For , its solution is

| (8) |

This regime applies to the relatively short time scales of two to three years prior to the crash shown below.

The higher the probability of a crash, the faster the price must increase (conditional on having no crash) in order to satisfy the martingale (no free lunch) condition. Intuitively, investors must be compensated by the chance of a higher return in order to be induced to hold an asset that might crash. This effect may go against the naive preconception that price is adversely affected by the probability of the crash, but our result is the only one consistent with rational expectations.

Using (3) into (8) gives the following price law:

| (9) |

where and is the price at the critical time (conditioned on no crash having been triggered). The price before the crash follows a power law with a finite upper bound . The trend of the price becomes unbounded as we approach the critical date. This is to compensate for an unbounded crash rate in the next instant.

3 Log-periodicity

The last ingredient of the model is to recognize that the stock market is made of actors which differs in size by many orders of magnitudes ranging from individuals to gigantic professional investors, such as pension funds. Furthermore, structures at even higher levels, such as currency influence spheres (US$, Euro, YEN …), exist and with the current globalisation and de-regulation of the market one may argue that structures on the largest possible scale, i.e., the world economy, are beginning to form. This means that the structure of the financial markets have features which resembles that of hierarchical systems with “traders” on all levels of the market. Of course, this does not imply that any strict hierarchical structure of the stock market exists, but there are numerous examples of qualitatively hierarchical structures in society. Models [2, 5] of imitative interactions on hierarchical structures recover the power law behavior (9). But in addition, they predict that the critical exponent can be a complex number! The first order expansion of the general solution for the hazard rate is then

| (10) |

Once again, the crash hazard rate explodes near the critical date. In addition, it now displays log-periodic oscillations. The evolution of the price before the crash and before the critical date is given by:

| (11) |

where is another phase constant. The key feature is that oscillations appear in the price of the asset before the critical date. The local maxima of the function are separated by time intervals that tend to zero at the critical date, and do so in geometric progression, i.e., the ratio of consecutive time intervals is a constant

| (12) |

This is very useful from an empirical point of view because such oscillations are much more strikingly visible in actual data than a simple power law : a fit can “lock in” on the oscillations which contain information about the critical date . Note that complex exponents and log-periodic oscillations do not necessitate a pre-existing hierarchical structure as mentioned above, but may emerge spontaneously from the non-linear complex dynamics of markets [6].

In Natural Sciences, critical points are widely considered to be one of the most interesting properties of complex systems. A system goes critical when local influences propagate over long distances and the average state of the system becomes exquisitely sensitive to a small perturbation, i.e., different parts of the system becomes highly correlated. Another characteristic is that critical systems are self-similar across scales: in our example, at the critical point, an ocean of traders who are mostly bullish may have within it several islands of traders who are mostly bearish, each of which in turns surrounds lakes of bullish traders with islets of bearish traders; the progression continues all the way down to the smallest possible scale: a single trader [7]. Intuitively speaking, critical self-similarity is why local imitation cascades through the scales into global coordination.

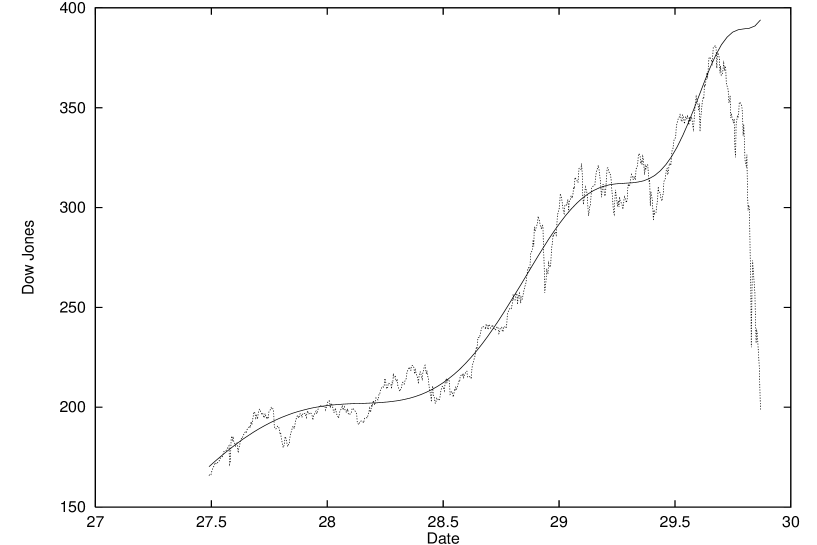

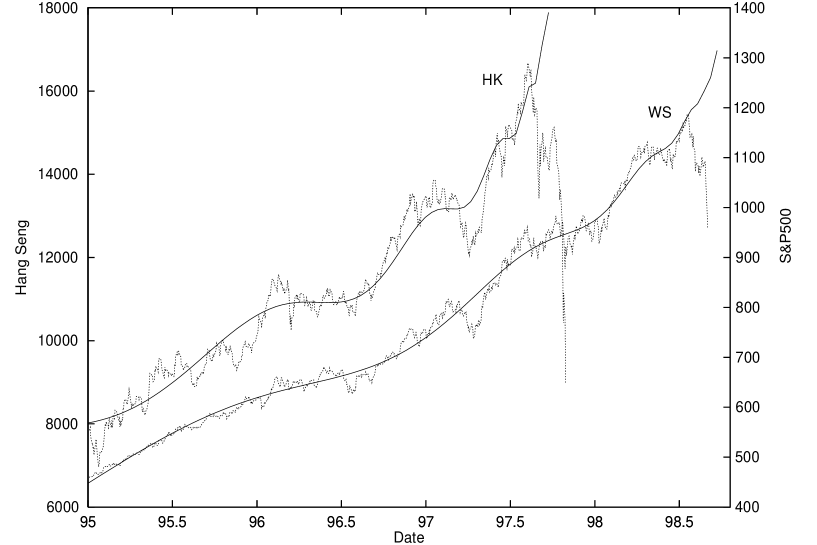

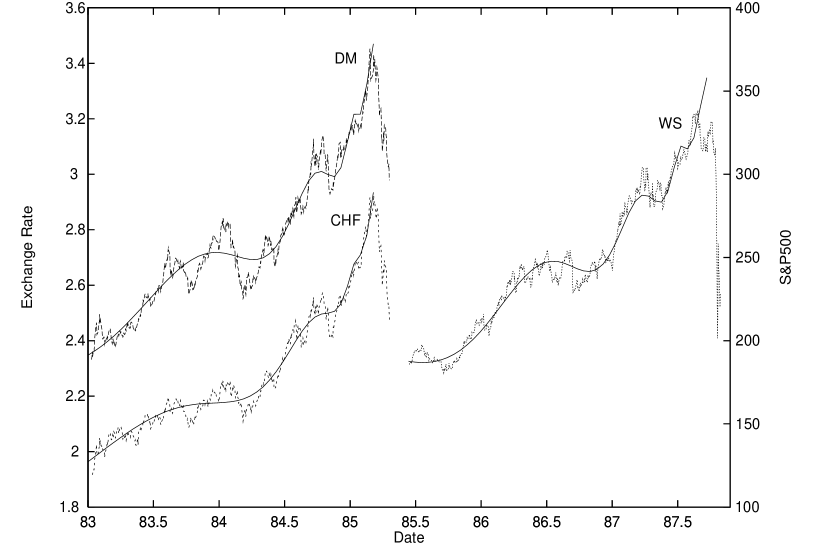

4 Fitting the crashes

Details on our numerical procedure are given in [2]. Figures 1-3 show the behavior of the market index prior to the four crashes of Oct. 1929 (Fig.1), Aug. 1998, Oct. 1997 (Hong-Kong) (Fig.2) and of Oct. 1987 (Fig.3). In addition, Fig. 3 shows the US $ expressed in DEM and CHF currencies before the collapse of the bubble in 1985. A fit with Eq. (11) is shown as a continuous line for each event. The table summarises the key parameters. Note the small fluctuations in the value of the scaling ratio for the 4 stock market crashes. This agreement constitutes one of the key test of our theory. Rather remarkably, the scaling ratio for the DEM and CHF currencies against the US$ is comparable.

| crash | drop | ||||||

| 1929 | |||||||

| 1985 (DEM) | |||||||

| 1985 (CHF) | |||||||

| 1987 | |||||||

| 1997 (H-K) | |||||||

| 1998 |

Table : is the critical time predicted from the fit of the market index to the Eq. (11). The other parameters , and of the fit are also shown. The fit is performed up to the time at which the market index achieved its highest maximum before the crash. is the time of the lowest point of the market. The percentage drop is calculated from the total loss from to .

In order to investigate the significance of these results, we picked at random fifty -week intervals in the period 1910 to 1996 of the Dow Jones average and launched the fitting procedure described in [2] on these surrogate data sets. The results were very encouraging. Of the eleven fits with a quality of fit comparable with that of the other crashes, only six data sets produced values for and which were in the same range. All six fits belonged to the periods prior to the crashes of 1929, 1962 and 1987. The existence of a “crash” in 1962 was before these results unknown to us and the identification of this crash naturally strengthens the case. We refer the reader to [2] for a presentation of the best fit obtained for this “crash”.

In the last few weeks before a crash, the market indices shown in Fig. 1-3 depart from the final acceleration predicted by Eq. 5 : this is the regime where the hazard rate becomes extremely high, the market becomes more and more sensitive to “shocks” and the market idiosyncrasies are bound to have an increasing impact. Within the theory of critical phenomena, it is well-known that the singular behavior of the observable, here the hazard rate or the rate of change of the stock market index, will be smoothed out by the finiteness of the market. Technically, this is referred to as a “finite-size effect”.

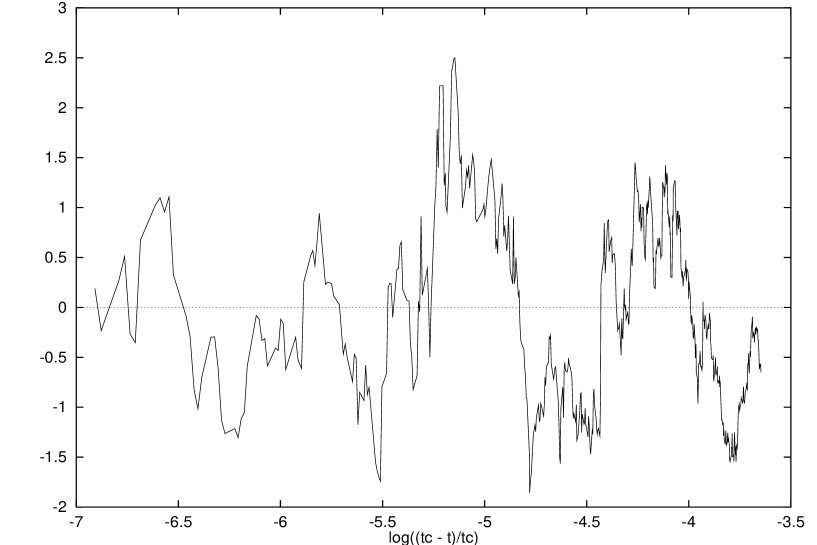

In order to qualify further the significance of the log-periodic oscillations in a non-parametric way, we have eliminated the leading trend from the price data by the following transformation

| (13) |

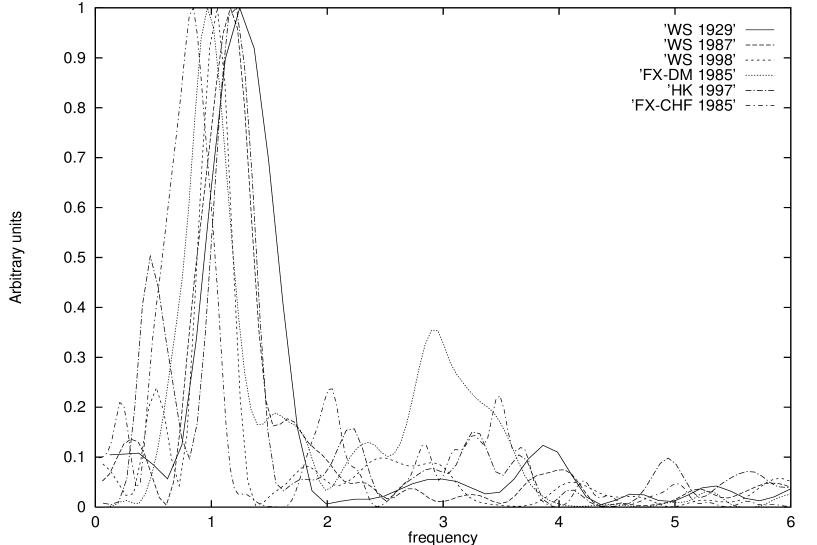

which should leave us with a pure if no other effects were present. In figure 4, we see this residue prior to the 1987 crash with a very convincing periodic trend as a function of . We estimated the significance of this trend by using a so-called Lomb periodogram for the four index crashes and the two bubble collapse on the Forex considered here. The Lomb periodogram is a local fit of a cosine (with a phase) using some user chosen range of frequencies. In figure 5, we see a peak around for all six cases corresponding to in perfect agreement with the previous results. We note that only the relative level of the peak for each separate periodogram should be regarded a measure of the significance of the oscillations. Since the nature of the “noise” is unknown and very likely different for each crash, we cannot estimate the confidence interval of the peak and compare the results for the different crashes. We also note, the the strength of the oscillations is of the leading power law behaviour for all 6 cases signfiying that they cannot be neglegted.

5 Towards a prediction of the next crash?

How long time prior to a crash can one identify the log-periodic signatures? Not only one would like to predict future crashes, but it is important to further test how robust our results are. Obviously, if the log-periodic structure of the data is purely accidental, then the parameter values obtained should depend heavily on the size of the time interval used in the fitting. We have thus carried out a systematic testing procedure [2] using a second order expansion of the hazard rate [8] and a time interval of 8 years prior to the two crashes of 1929 and 1987. The general picture we obtain is the following. For the Oct. 1987 crash, a year or more before a crash, the data is not sufficient to give any conclusive results. Approximately a year before the crash, the fit begins to lock-in on the date of the crash with increasing precision and our procedure becomes robust. However, if one wants to actually predict the time of the crash, a major obstacle is the fact that several possible dates are possible. In addition, the fit in general “over-shoot” the true day of the crash. For the Oct. 1929 crash, we have to wait until approximately month before the crash for the fit to lock in on the date of the crash, but from that point the picture is the same as for the crash in Oct. 1987. We caution the reader that jumping in the prediction game may be hazardous and misleading : one deals with a delicate optimization problem that requires extensive back and forward testing. Furthermore, the formulas given here are only “first-order” approximations and novel improved methods are needed [9]. Finally, one must never forget that the crash has to remain in part a random event in order to exist!

A general trend for the analysis of the five crashes presented here is that the critical obtained from fitting the data tends to over-shoot the time of the crash. This observation is fully consistent with our rational expectation model of a crash. Indeed, is not the time of the crash but the most probable value of the skewed distribution of the possible times of the crash. The occurrence of the crash is a random phenomenon which occurs with a probability that increases as time approaches . Thus, we expect that fits will give values of which are in general close to but systematically later than the real time of the crash. The phenomenon of “overshot” that we have clearly documented [2] is thus fully consistent with the theory.

It is a striking observation that essentially similar crashes have punctuated this century, notwithstanding tremendous changes in all imaginable ways of life and work. The only thing that has probably little changed are the way humans think and behave. The concept that emerges here is that the organization of traders in financial markets leads intrinsically to “systemic instabilities”, that probably result in a very robust way from the fundamental nature of human beings, including our gregarious behavior, our greediness, our reptilian psychology during panics and crowd behavior and our risk aversion. The global behavior of the market, with its log-periodic structures that emerge as a result of the cooperative behavior of traders, is reminiscent of the process of the emergence of intelligent behavior at a macroscopic scale that individuals at the microscopic scale have not idea of. This process has been discussed in biology for instance in animal populations such as ant colonies or in connection with the emergence of consciousness [10].

anders@moho.ess.ucla.edu

sornette@cyclop.ess.ucla.edu

References

- [1] A. Johansen and D. Sornette, Eur. Phys. J. B 1, 141-143 (1998) (http://xxx.lanl.gov/abs/cond-mat/9712005)

- [2] A. Johansen, O. Ledoit and D. Sornette, Crashes as critical points, preprint 1998 (http://xxx.lanl.gov/abs/cond-mat/9810071)

- [3] N. Goldenfeld, Lectures on phase transitions and the renormalization group. (Addison-Wesley, Reading, Mass., 1992).

- [4] T.M. Liggett, Interacting particle systems (New York : Springer-Verlag, 1985).

- [5] D. Sornette and A. Johansen, A Hierarchical Model of Financial Crashes, Physica A 261. 581-598 (1998)

- [6] D. Sornette, Physics Reports 297, 239-270 (1998).

- [7] K.G. Wilson, Scientific American 241(2), 158–179 (1979).

- [8] D. Sornette and Johansen, A., Physica A 245, 411–422 (1997).

- [9] Sornette, D. and A. Johansen, in preparation.

- [10] P.W. Anderson, Arrow K. J. and Pines D. (ed), The economy as an evolving complex system (Addison-Wesley, New York, 1988)