Inverse Cubic Law for the Distribution of Stock Price Variations

Abstract

The probability distribution of stock price changes is studied by analyzing a database (the Trades and Quotes Database) documenting every trade for all stocks in three major US stock markets, for the two year period Jan 1994 – Dec 1995. A sample of 40 million data points is extracted, which is substantially larger than studied hitherto. We find an asymptotic power-law behavior for the cumulative distribution with an exponent , well outside the Levy regime .

pacs:

PACS numbers: 89.90.+nThe asymptotic behavior of the increment distribution of economic indices has long been a topic of avid interest [1, 2, 3, 4, 5, 6]. Conclusive empirical results are, however, difficult to obtain, since the asymptotic behavior can be obtained only by a proper sampling of the tails, which requires a huge quantity of data. Here, we analyze a database documenting each and every trade in the three major US stock markets, the New York Stock Exchange (NYSE), the American Stock Exchange (AMEX), and the National Association of Securities Dealers Automated Quotation (NASDAQ) for the entire 2-year period Jan. 1994 to Dec. 1995 [7]. We thereby extract a sample of approximately data points, which is much larger than studied hitherto.

We form 1000 time series , where is the market price of company (i.e. the share price multiplied with the number of outstanding shares), is the rank of the company according to its market price on Jan. 1, 1994. The basic quantity of our study is the relative price change,

| (1) |

where the time lag is min. We normalize the increments,

| (2) |

where the volatility of company is measured by the standard deviation, and is a time average [8].

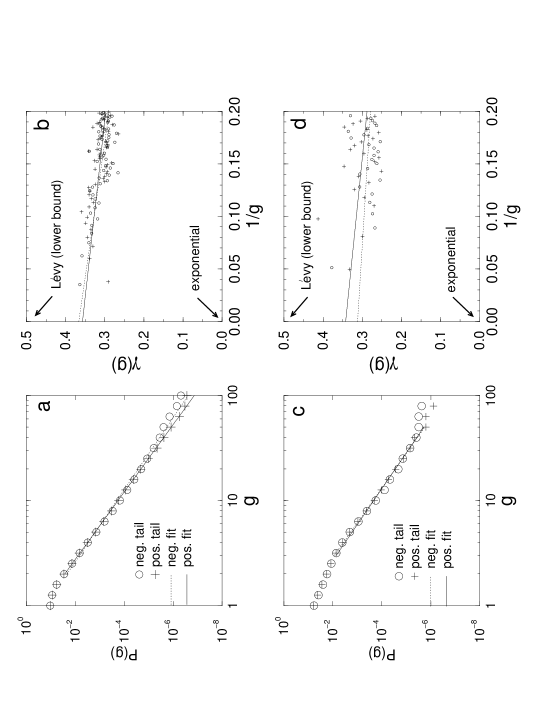

We obtain about 20,000 normalized increments per company per year, which gives about increments for the 1000 largest companies in the time period studied. Figure 1a shows the cumulative probability distribution, i.e. the probability for an increment larger or equal to a threshold , , as a function of . The data are well fit by a power law

| (3) |

with exponents (positive tail) and (negative tail) from two to hundred standard deviations.

In order to test this result, we calculate the inverse of the local logarithmic slope of , [9]. We estimate the asymptotic slope by extrapolating as a function of to . Figure 1b shows the results for the negative and positive tail respectively, each using all increments larger than 5 standard deviations. Extrapolation of the linear regression lines yield for the positive and for the negative tail. We test this method by analyzing two surrogate data sets with known asymptotic behavior, (a) an independent random variable with and (b) an independent random variable with . The method yields the correct results 3 and respectively.

To test the robustness of the inverse cubic law , we perform several additional calculations: we change the time increment in steps of 5 min up to 120 min, we analyze the S&P500 index over the 13y-period Jan. ’84 – Dec. ’96 using the same methods as above (Fig. 1c and d), we replace definition of the volatility by other measures, such as . The results are all consistent with . These extensions will be discussed in detail elsewhere [10].

To put these results in the context of previous work, we recall that proposals for have included a Gaussian distribution [1], a Lévy distribution [2, 11, 12], and a truncated Lévy distribution, where the tails become “approximately exponential” [3]. The inverse cubic law differs from all three proposals: Unlike and , it has diverging higher moments (larger than 3), and unlike and it is not a stable distribution.

Acknowledgements: We thank X. Gabaix, S. Havlin, Y. Liu, R. Mantegna, C.K. Peng and D. Stauffer for helpful discussions, and DFG and NSF for financial support.

REFERENCES

- [1] L. Bachelier, Ann. Sci. École Norm. Sup. 3, 21 (1900).

- [2] B. B. Mandelbrot, J. Business 36, 294 (1963).

- [3] R. N. Mantegna and H. E. Stanley, Nature 376, 46 (1995).

- [4] S. Ghashgaie, W. Breymann, J. Peinke, P. Talkner, and Y. Dodge, Nature 381, 767 (1996).

- [5] A. Pagan, J. Empirical Finance 3, 15 (1996), and references therein.

- [6] J.P. Bouchaud and M. Potters, Theorie des Risques Financieres, (Alea-Saclay, Eyrolles 1998); R. Cont, Europ. Phys. J. B (1998), in press. (cond-mat/9705075).

- [7] The Trades and Quotes Database, 24 CD-ROM for ’94-’95, published by the New York Stock Exchange.

- [8] In order to obtain uncorrelated estimators for the volatility and the price increment at time , the time average extends only over time steps .

- [9] B. M. Hill, Ann. Stat. 3, 1163 (1975).

- [10] P. Gopikrishnan, M. Meyer, L. A. N. Amaral, and H. E. Stanley, to be published.

- [11] V. Pareto, Cours d’Économie Politique (Lausanne and Paris, 1897).

- [12] P. Lévy, Théorie de l’addition des variables aléatoires (Gauthier-Villars, Paris, 1937).