A LANGEVIN APPROACH TO STOCK MARKET FLUCTUATIONS AND CRASHES

Orme des Merisiers, 91191 Gif-sur-Yvette Cedex, France

2 Science & Finance, 109-111 rue Victor-Hugo, 92532 France

)

Abstract

We propose a non linear Langevin equation as a model for stock market fluctuations and crashes. This equation is based on an identification of the different processes influencing the demand and supply, and their mathematical transcription. We emphasize the importance of feedback effects of price variations onto themselves. Risk aversion, in particular, leads to an ‘up-down’ symmetry breaking term which is responsible for crashes, where ‘panic’ is self reinforcing. It is also responsible for the sudden collapse of speculative bubbles. Interestingly, these crashes appear as rare, ‘activated’ events, and have an exponentially small probability of occurence. We predict that the ‘shape’ of the falldown of the price during a crash should be logarithmic. The normal regime, where the stock price exhibits behavior similar to that of a random walk, however reveals non trivial correlations on different time scales, in particular on the time scale over which operators perceive a change of trend.

Electronic addresses :

bouchaud@amoco.saclay.cea.fr

cont@ens.fr

1 Introduction

Stock market fluctuations exhibit several statistical peculiarities which are still awaiting for a satisfactory interpretation. More strikingly, many of these statistical properties are common to a wide variety of markets and instruments. The most prominent features are [1, 2, 3, 5, 6, 4]:

-

1.

On short time scales, the variation of stock prices are strongly non-Gaussian.

-

2.

Market ‘volatility’ (i.e. the variance of the fluctuations) is itself time dependent, with a slowly decreasing, power-law like, correlation function.

-

3.

On very long time scales, the log of the price tends to grow linearly with time, with rare, large drops corresponding to market crashes.

The first two properties are observed on a certain range of time scales, ranging from an hour to several weeks, but do not hold for very large time scales (several years) where macroeconomic factors enter into consideration nor for very short time scales (minutes or so, the typical duration of a transaction) where the detailed structure of the market has to be taken into account.

These anomalous events have drawn considerable attention recently, both because of their intrinsic importance, but also because of possible analogies with physical phenomena such as earthquakes or avalanches. The point is that crashes correspond to a collective effect, where a large proportion of the actors in a market decide simultaneously to sell their stocks; it is thus tempting to think of a crash as some kind of critical point where (as in statistical physics models undergoing a phase transition) the response to a small external perturbation becomes infinite, because all the subparts of the system respond cooperatively. Correspondingly, it has been suggested that ‘crash precursors’ might exist, and in particular ‘log-periodic’ oscillations before the crash [7]. However, no microscopic model has been proposed which substantiate such a claim. Actually, there are as yet no convincing model which ‘explains’ the statistical features described above, although many proposals have been put forward [8, 10].

A crucial ingredient in model building is the specification of the level (in our case, the time scale) at which one aims to describes the properties of the system. There are currently two major approaches to market dynamics in the economics and finance literature. One approach is a “temporary equilibrium” approach which assumes that supply and demand equilibrate quickly enough to be considered at instantaneous equilibrium at all times [8]. The other one is that of market microstructure theory [9] which examines the implications of market structure, behavorial assumptions about market participants and specific trading rules on price behavior at the transaction level.

However, our aim here is to describe market dynamics at time scales where, according to empirical observations, some interesting regularities which are common between markets with different microstructures appear [2, 4]. At the same time, these time scales are not long enough to allow the market to reach equilibrium: empirical studies show that at intraday time scales there is an imbalance between supply and demand. The level of description adopted here is therefore intermediate between the macroeconomic level which is that of the market equilibrium models [8] and the individual agent level which is that of the market microstructure theory [9].

The aim of this paper is to propose an alternative description of the dynamics of speculative markets with a simple Langevin equation. This equation is built from general arguments, encapsulating what we believe to be the essential ingredients; in particular, the feedback of the price fluctuations on the behaviour of the market participants. We try to motivate as much as possible each term in the equation, and the value of the corresponding parameters is estimated by comparing with empirical data. Our basic idea is that although the modelling of each individual participants (‘agents’) is impossible in quantitative terms, the collective behavior of the market and it’s impact on the price in particular can be represented in statistical terms by a few number of terms in a (stochastic) dynamical equation. Our approach is in the spirit of many phenomenological, ‘Landau-like’ approaches to physical phenomena [11].

2 A phenomenological Langevin equation

We denote the price of the stock at time as . At any given instant of time, there is a certain number of ‘buyers’ which we call (the demand) and ‘sellers’, (the supply). The first dynamical equation describes the effect of an offset between supply and demand, which tends to push the price up (if ) or down in the other case. In general, one can write:

| (1) |

where is an increasing function, such that . In the following, we will frequently assume that is linear (or else that is small enough to be satisfied with the first term in the Taylor expansion of ), and write

| (2) |

where is a measure of market depth i.e. the excess demand required to move the price by one unit. When is high, the market can ‘absorb’ supply/demand offsets by very small price changes. Now, we try to construct a dynamical equation for the supply and demand separately. Consider for example the number of buyers . Between and , a certain fraction of those get their deal and disappear (at least temporarily). This deal is usually ensured by market makers, which act as intermediaries between buyers and sellers. The role of market markers is to absorb the demand (and supply) even if these do not match perfectly. Of course, the market makers will absorb buy orders more quickly if they know that the number of sellers is high, and vice-versa. The effect of market makers (mm) can thus be modelled as:

| (3) |

where are rates (inverse time scales). We assume that market makers act symmetrically, i.e, that . To lowest order in , we write:

| (4) |

On liquid markets, the time scale before which a deal is reached is short; typically a few minutes (see also below for another interpretation of ).

There are several other effects which must be modeled to account for the time evolution of supply and demand. One is the spontaneous (sp) appearance of new buyers (or sellers), under the influence of new information, individual need for cash, or particular investment strategies. This can be modelled as a white noise term (not necessarily Gaussian):

| (5) |

where have zero mean, and a short correlation time . is the average increase of demand (or supply), which might also depends on time through the time dependent anticipated return and the anticipated risk . It is quite clear that both these quantities are constantly reestimated by the market participants, with a strong influence of the recent past. For example, ‘trend followers’ extrapolate a local trend into the future. On the other hand, ‘fundamental analysts’ estimate what they believe to be the ‘true’ price of the stock; if the observed price is above this ‘true’ price, the anticipated trend is reduced, and vice-versa. In mathematical terms, these effects can be represented as:

| (6) |

where is a certain kernel (of integral one) defining how the past average trend is measured by the agents, and is a mean-reversion force, towards the average (over the fundamental analysts) ‘true price’ 111Note that is actually itself time dependent, although its evolution in general takes place over rather long time scales (years)..

Similarly, the anticipated risk has a short time scale contribution. It is well known that an increase of volatility is badly felt by the agents, who immediately increase their estimate of risk. Hence, we write:

| (7) |

Correspondingly, expanding to lowest order, one has:

| (8) |

where the signs of the different coefficients are set by the observation that is an increasing function of return and a decreasing function of risk , and vice versa for . Eq. (8) contains the leading order terms which arise if one assumes that the agents try to reach a tradeoff between risk and return: the demand for an asset decreases if is recent evolution shows high volatility and increases if it shows an upward trend. This is the case for example if the investors follow a mean-variance optimisation scheme with adaptive estimates of risk and return [12].

Yet another contribution to the change of demand and supply comes from the existence of option markets, where traders hedge their option positions by buying or selling the underlying stock. The Black-Scholes rule for hedging relates the number of stock to be held to the price of the underlying by a non linear formula [13]. A change of price thus leads to an increase in the demand or supply which can also be represented by and type of terms, reflecting an average of the so-called ‘’s’ and the ‘’s’ of the different options [13]. In particular, the Black-Scholes hedging strategy is a positive feedback strategy of the trend following type.

We are now in position to write an equation for the supply/demand offset by summing all these different contributions:

| (9) | |||||

with . Note in particular that reflects the fact that agents are risk averse, and that an increase of the local volatility always leads to negative contribution to . This feature will be crucial in the following. For definiteness, we will consider to be gaussian and normalize it as:

| (10) |

where measure the susceptibility of the market to the random external shocks, typically the arrival of information. In principle, should also depend on the recent history, reflecting the fact that an increase in volatility induces a stronger reactivity of the market to external news. In the same spirit as above, one could thus write:

| (11) |

For simplicity, we will neglect the influence of in the following sections, but comment on its effect in the concluding section.

Finally, let us note that Eq. (9) can be extended to allow for agents with different reaction times. For example, the term can be generalized as :

| (12) |

where the have different ranges. As we shall discuss below, the empirical data suggests that there is a population of very fast traders (probably market makers themselves) which in a contrarian way ().

3 Analysis of the linear theory. Liquid vs. Illiquid markets

Let us consider the linear case ‘risk neutral’ case where . We will assume for simplicity that , and first consider the local limit where is much larger that (short memory time). In this case, the equation for becomes that of an harmonic oscillator 222In an oral seminar given in Jussieu in June 1997, Doyle Farmer also presented a second-order equation for the price. We are not aware of the existence of a written version, and do not know to what extend his analysis is similar to ours.:

| (13) |

where has been absorbed into a redefinition of . For liquid markets, where and are large enough, the ‘friction’ term is positive. In this case the market is stable, and the price oscillates around an equilibrium value , which is higher than the average fundamental price if the spontaneous demand is larger than the spontaneous supply (i.e. is positive), as expected when the overall economy grows. One can also compute the time correlation function of the price fluctuations. The important parameter is:

| (14) |

For liquid markets, . The correlation is found to be the sum of two exponentials, with correlation times :

| (15) |

and amplitudes such that . Thus, on a time scale , the correlation function falls to a very small value . This allows one to identify with the correlation time observed on liquid markets, which is of the order of several minutes [2], thereby fixing the order of magnitude of . Thus, on time scales such that , the stock price behaves as a simple biased random walk with volatility , before feeling the confining effect of the ‘fundamental’ price. Since the fundamental price is surely not known to better than – say – , and that the typical variation of the price of a stock is also around per year, it is reasonnable to assume that the time scale beyond which ‘fundamental’ effects (as represented by the harmonic term) play a role is of the order of a year 333Beyond the year time scale, however, the evolution of itself cannot be neglected.. This leads to . Hence, for liquid markets, the role of the confining term can probably be neglected, at least on short time scales.

The situation is rather different for illiquid markets, or when trend following effects are large, since can be negative. In this case, the market is unstable, with an exponential rise or decay of the stock value, corresponding to a speculative bubble. However, in this case, grows with time and it soon becomes untenable to neglect the higher order terms, in particular the risk aversion term proportional to . We will comment on this case below. Let us however start by analyzing the role of for liquid markets for which, as explained above, it is reasonnable to set .

4 Risk aversion induced crashes as activated events

Setting and still focusing on the limit where the memory time is very small, one finds the following non linear Langevin equation:

| (16) |

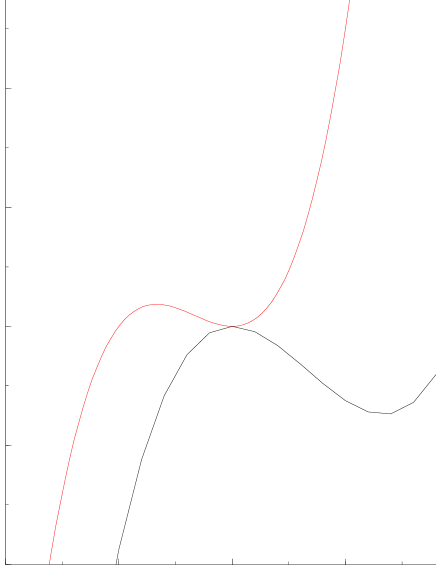

This equation represents the evolution of the position of a viscous fictitious particle in a potential represented in Fig. 1.

In order to keep the mathematical form simple, we set the average trend to zero (no net average offset between spontaneous demand and spontaneous supply); this does not qualitatively change the following picture, unless is negative and large. The potential can then be written as:

| (17) |

which has a local minimum for , and a local maximum for , beyond which the potential plumets to . The ‘barrier height’ separating the stable region around from the unstable region is given by:

| (18) |

The nature of the motion of in such a potential is the following: starting at , the particle has a random harmonic-like motion in the vicinity of until an ‘activated’ event (i.e. driven by the noise term) brings the particle near . Once this barrier is crossed, the fictitious particle reaches in finite time. In financial terms, the regime where oscillates around and where can be neglected, is the ‘normal’ random walk regime discussed in the previous paragraph. (Note that the random walk is biased when ). This normal regime can however be interrupted by ‘crashes’, where the time derivative of the price becomes very large and negative, due to the risk aversion term which enhances the drop in the price. The point is that these two regimes can be clearly separated since the average time needed for such crashes to occur can be exponentially long, since it is given by the classical Arrhenius-Kramers formula [14, 15]:

| (19) |

where is the variance of the noise and . Taking years, per day, and minutes, one finds that the characteristic value beyond which the market ‘panics’ and where a crash situation appears is of the order of in ten minutes, which not unreasonnable. The ratio appearing in the exponential can also be written as the square of ; it thus compares the value of what is considered to be an anomalous drop on the correlation time () to the ‘normal’ change over this time scale ().

Note that in this line of thought, a crash occurs because of an improbable succession of unfavorable events, and not due to a single large event in particular. Furthermore, there are no ‘precursors’ - characteristic patterns observed before the crash: before has reached , it is impossible to decide whether it will do so or whether it will quietly come back in the ‘normal’ region . Note finally that an increase in the liquidity factor reduces the probability of crashes. This is related to the stabilizing role of market makers, which appears very clearly.

An interesting prediction concerns the behaviour of the price once one enters the crash regime i.e. once becomes larger (in absolute value) than . Neglecting the noise term, one finds that the stock price is given by:

| (20) |

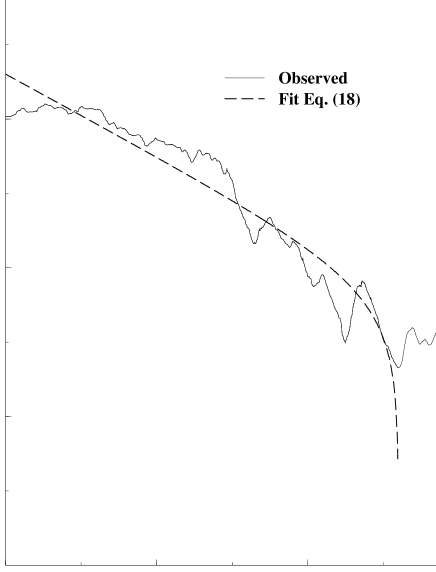

which diverges logarithmically towards when reaches a final time . Of course, in practice, this divergence is not real since when the price becomes too low, other mechanisms, which we have not taken into account in the model, come into play (for example the action of a regulating authority). One thus expects that some external mechanism interrupts the crash, which in the Langevin language, correspond to a ‘reinjection’ of the particle around . Formula (20) is compared in Fig. 2 to the observed price of the S&P index during the 1987 October crash, where we have fixed to be the time when the price reaches its minimum. This leads to (in minutes-1) and (S&P points), from which we estimate S&P points per hour (more than per hour). The last figure is not unreasonable; however, the order of magnitude found for is much smaller than expected, on the basis that is ten minutes or so. We shall come back to this point below, in section (6)

5 Illiquid markets: speculative bubbles and collapse

Suppose now that the trend following tendency is strong so that . The potential has a minimum for which is now positive, and a maximum for . The price increment oscillates around a positive value unrelated to , which means that there is a non zero trend not based on true growth but entirely induced by the fact that a price increase motivates more people to buy – this is called a speculative bubble. After a time , the price has risen on average by an amount . If this increase is too large, it becomes illegitimate to neglect the role of the ‘fundamental’ price . The full potential in which evolves is actually given by . It is easy to see that this potential has a local minimum (which leads to the above sustained growth) only when:

| (21) |

but that this minimum disappears for larger values of . Assuming that , we thus find a time where the bubble has to collapse, since the (metastable) equilibrium around is no longer present. The lifetime of the bubble is given by:

| (22) |

As could be expected, the stronger the damping term pulling the price back towards the fundamental value , the shorter will be the duration of speculative bubbles.

6 Memory effects

Up to now, we have assumed that the impact of a change of price on the behaviour of the market participants was instantaneous, i.e. that the kernels and used to estimate the average return and risk have a typical memory time shorter than any other time scale in the problem, in particular . Since we have argued that is of the order of a few minutes on liquid markets, this assumption is not very realistic: it is more reasonable to assume that agents judge the evolution of risk and return on longer time scales, at least several days. We are thus actually in the opposite limit where . Fortunately the case of an exponential memory kernel still leads to a tractable model. It is easy to show that the dynamical equation now reads:

| (23) |

which indeed leads back to Eq. (16) in the limit . Eq. (23) governs the evolution of a massive particle in the very same potential as the one above (Fig 1). One can show that in this case, for , and in the limit where , the correlation function of the increment is given by:

| (24) |

(with ) which thus decays rapidly (on a time ) to a (small) value which can be negative if , before slowly going to zero on time scales . Interestingly, the empirical correlation function of short time increments indeed shows a negative minimum on time scales of the order of 15 minutes [2, 4]. The relative amplitude of this minimum (as compared to ) is of the order of a few . This could thus be interpreted as the effect of fast ‘contrarian’ traders superposed to the regulatory action of the market maker (contributing to a negative ).

For , one still has a sharp distinction between a ‘normal’ regime, where the stock price performs a random walk with volatility (except that, as just discussed, the increment correlation function has a small tail decaying on time scales ), and a ‘crash’ regime, when the ‘particle’ manages to reach the top of the potential barrier. The theory of activated processes can be extended to massive particles. In the limit , the average time between crashes is given by a formula very close to the one above [14, 15]:

| (25) |

i.e., only the prefactor of the exponential is changed. Note that, as could be expected intuitively, the fact that there is a delay in the reaction of traders tends to stabilize the market, since the crash time is multiplied by a factor .

Finally, the dynamics of the price when the crash has started is also affected by the presence of a memory. The truly asymptotic behaviour of Eq. (23) (for zero noise) is given by:

| (26) |

which leads to a divergence of the price itself. However, as noticed above, this divergence is certainly interrupted by effects which our model cannot describe. In order to compare with empirical data, in particular that of the crash of 1987, one can notice that the time scale over which the crash took place (days) is much larger than . It is thus reasonnable to neglect the second derivative term as compared to the first. In the limit where , we are thus led to:

| (27) |

the solution of which being of the same form as the one without memory, except for the coefficients:

| (28) |

The same fit as in Fig. 2 is thus adequate. However, interestingly, one finds that it is now , rather than , which appears in the exponential. In other words, the time scale during which the crash develops is much longer; from the fit we find (see Fig 2): minutes (half a day). The estimate of , as , is however unaffected.

7 Concluding remarks

We hope to have convinced the reader that the above Langevin equation, which is based on an identification of the different processes influencing supply and demand, and their mathematical transcription, captures many of the features seen on markets. We have in particular emphasized the role of feedback, in particular through risk aversion, which leads to an ‘up-down’ symmetry breaking non linear term . This term is responsible for the appearance of crashes, where ‘panic’ is self reinforcing; it is also responsible for the sudden collapse of speculative bubbles. Interestingly, however, these crashes are rare events, which have an exponentially small probability of occurence (see Eq. (19)). We predict that the ‘shape’ of the falldown of the price during a crash should be logarithmic (see Eq. (28)), which is compatible with empirical data (Fig. 2). The ‘normal’ regime, where the stock price behaves as a random walk, reveals non trivial correlations on the time scale over which operators perceive a change of trend. In particular, a small negative dip related to the existence of contrarian traders can appear. In this respect, it is important to stress that within these models lead, in principle, to simple winning strategies. It is however easy to convince oneself that if the level of correlations is small (for example, as seen above, of order of a few percent after tens of minutes), the transaction costs are such that arbitrage cannot be implemented in practice [2]. Therefore, we believe that non trivial correlations can be observed on financial data, and do actually arise naturally when feedback effects are included.

Before closing, we would like to discuss briefly several other points. The first one concerns the fact that we have considered to be the price, rather than the log of the price. Of course, on short time scales, this does not matter, and actually a description in terms of the price itself is often preferable on short time scales [2]. On longer time scales, however, the log of the price should be prefered since it describes the evolution of prices in relative rather than absolute terms. However, on these long time scales, one should also take into account the evolution of the model’s parameters (such as the fundamental price , or the average trend ), which is related to true economics, and thus not amenable to such a simple statistical treatment as we have argued for psychology. Second, we have identified a ‘normal’ regime, where oscillates around zero, and a crash regime for . In the model presented above, the ‘normal’ fluctuations are gaussian 444Note that in our model, ‘normal’ fluctuations and crashes describe two very different regimes of the same dynamical equation. In this sense, we agree with the idea that market crashes are indeed ‘outliers’ from a statistical point of view [16] if is gaussian and if the relation between price changes and supply/demand unbalance is linear. In order to account for the large kurtosis observed on markets during ‘normal’ periods (i.e. excluding crashes), one necessarily has to take into account either the non linearity of the price change and/or the non-normal nature of the ‘noise’, in particular the role of the feedback term introduced in Eq. (11), which can indeed be shown to lead to ‘fat tails’ [17]. Although the quantitative formulae given above are affected by such effects, the qualitative picture will remain.

Finally, the above model, where crashes appear as activated events, suggests a tentative interpretation for ‘log-periodic’ oscillations seen before crashes [7]. Imagine that each time reaches – by accident – an anomalously negative value (but above ), the market becomes more ‘nervous’. This means that its susceptibility to external disturbances like news will increase. In our model, this can be described by an increase of the parameter , through the term in Eq. (11). If increases by a certain value at every accident and since appears in an exponential, this implies that the average time before the next ‘accident’ is decreased by a certain factor which, to linear order in , is constant:

| (29) |

This leads to a roughly log-periodic behaviour, which indeed predicts that the time difference between two events is a geometric series. However, our scenario is not related to a critical point: the crash appears when exceeds , and not when , i.e., when crash events accumulate. In this respect, it should be noted that according to the critical log periodic theory, there should have been another crash near the end of November 1997, and then again roughly 10 days later, which did not occur [18].

Acknowlegments. We would like to thank J.P. Aguilar, S. Galluccio, L. Laloux and especially M. Potters for many discussions on the problem of stock market fluctuations and crashes.

References

- [1] C. W. J. Granger, Z. X. Ding, “Stylized facts on the temporal distributional properties of daily data from speculative markets”, Working Paper, University of California, San Diego (1994). Guillaume D.M., Dacorogna M.M., Davé R.R., Müller U.A., Olsen R.B., Pictet O.V. (1997) “From the birds eye to the microscope: a survey of new stylized facts of the intra-day foreign exchange markets” Finance and Stochastics, 1, 95-130. R. Mantegna & H. E. Stanley Nature, 376, 46-49 (1995).

- [2] J.P. Bouchaud, M. Potters, Théorie des Risques Financiers, Aléa-Saclay/Eyrolles (1997).

- [3] Cont R., Potters M. & Bouchaud J.P. (1997) “Scaling in stock market data: stable laws and beyond” in Scale invariance and beyond, B. Dubrulle, F. Graner & D. Sornette Editors, EDP-Springer (1998) Cont, R. (1997) “Scaling properties of intraday price changes” Science & Finance Working Paper 97-01 (cond-mat/9705075).

- [4] R. Cont, Statistical Finance: empirical study and theoretical modeling of price fluctuations in financial markets, PhD dissertation, Université de Paris XI (1998).

- [5] P. Cizeau, Y. Liu, M. Meyer, C.K. Peng, H.E. Stanley, preprints cond-mat/9708143 and 970621.

- [6] M. Potters, R. Cont, J.P. Bouchaud, Financial markets as adaptive systems, cond-mat/9609172, to appear in Europhys. Lett.

- [7] D. Sornette, A. Johansen, J.P. Bouchaud, J. Physique 6 (1996) 167; J.A. Feigenbaum, P.G.O. Freund, Int. J. Mod. Phys. 10 (1996) 3737; M. Ausloos, P. Boveroux, A. Minguet, N. Vandewalle, Universal and complex behaviour of prerupture signals in stock market indices, Université de Liège, preprint.

- [8] Brock W.A., Hsieh D.A. & LeBaron, B. (1991) Nonlinear dynamics, chaos and instability: statistical theory and economic evidence, Cambridge MA: MIT Press; Grandmont, J.M. “Temporary equilibrium theory” in Arrow, K.J. & Intriligator, M.D. (ed.) (1981) Handbook of mathematical economics, Elsevier; Brock, W.A. & Hommes, C.F. (1997) ”Rational routes to randomness” Econometrica, 65, 1059.

- [9] For a review of market microstructure theory see: O’Hara, M. (1995) Market microstructure theory, Blackwell Publishers.

- [10] For recent work in the physics community, see: Bak P., M. Paczuski & M. Shubik (1997) “Price variations in a stock market with many agents”, Physica A. Santa Fe Institute Working Paper; Caldarelli G., Marsili M. & Zhang Y.C. (1997) “A prototype model of stock exchange”, Europhysics Letters, 40 479; R. Cont, J.P. Bouchaud, “Herd behavior and aggregate fluctuations in financial markets”, preprint cond-mat/9712318.

- [11] For a ‘manifesto’ defending such an approach in the physical context, see, e.g. T. Hwa, M. Kardar, Phys. Rev. A 45, 7002, (1992).

- [12] H. Markowitz, Portfolio Selection: Efficient Diversification of Investments (J.Wiley and Sons, New York, 1959); E.J. Elton and M.J. Gruber, Modern Portfolio Theory and Investment Analysis (J.Wiley and Sons, New York, 1995).

- [13] for a review, see: Hull, J. (1997) Options, futures and other derivative securities, Prentice-Hall. For a physicist approach, see [2].

- [14] S. Chandrasekhar, in Noise and Stochastic Processes, N. Wax Editor, Dover, 1954.

- [15] P. Hanggi, P. Talkner, M. Borkovec, Rev. Mod. Phys. 52 (1990) 251.

- [16] A. Johansen, D. Sornette, Stock Market crashes are outliers, preprint cond-mat/9712005.

- [17] J.P. Bouchaud, R. Cont, in preparation.

- [18] L. Laloux, M. Potters, J.P. Bouchaud, unpublished.