Scaling behavior in economics: I. Empirical results

for company growth

Abstract

We address the question of the growth of firm size. To this end, we analyze the Compustat data base comprising all publicly-traded United States manufacturing firms within the years 1974–1993. We find that the distribution of firm sizes remains stable for the 20 years we study, i.e., the mean value and standard deviation remain approximately constant. We study the distribution of sizes of the “new” companies in each year and find it to be well approximated by a log-normal. We find (i) the distribution of the logarithm of the growth rates, for a fixed growth period of one year, and for companies with approximately the same size displays an exponential form, and (ii) the fluctuations in the growth rates — measured by the width of this distribution — scale as a power law with , . We find that the exponent takes the same value, within the error bars, for several measures of the size of a company. In particular, we obtain: for sales, for number of employees, for assets, for cost of goods sold, and for property, plant, & equipment.

I Introduction

Statistical physics has undergone many changes in emphasis during the last few decades. The seminal works of the ’60s and ’70s on critical phenomena [1, 2] provided physicists with a new set of tools to study nature [2, 3]. Fields such as biophysics, medicine, geomorphology, geology, evolution, ecology or meteorology are now common areas of application of statistical physics.

In particular, several statistical physics research groups have turned their attention to problems in economics [5, 6] and finance [7, 8, 9, 10, 11, 12, 13, 14, 15]. On the other hand, the concepts of statistical physics (e.g., self-organization) have started to penetrate the study of economics [16]. In this article, we extend the study of Ref. [6] on the growth rate of manufacturing companies. One motivation for the present study is the considerable recent interest in economics in developing a richer theory of the firm [17, 18, 19, 20, 21, 22, 23, 24, 25, 26, 27, 28, 29, 30, 31, 32, 33, 34, 35, 36]. In standard microeconomic theory, a firm is viewed as a production function for transforming inputs such as labor, capital, and materials into output [19, 24, 30]. When dynamics are incorporated into the model, the link between production in one period and production in another arises because of investment in durable, physical capital and because of technological change (which in turn can arise from investments in research and development). Recent work on firm dynamics emphasizes the effect of how firms learn over time about their efficiency relative to competitors [23, 37, 38]. The production dynamics captured in these models are not, however, the only source of actual firm dynamics. Most notably, the existing models do not account for the time needed to assemble the organizational infrastructure needed to support the scale of production that typifies modern corporations.

We studied all United States (US) manufacturing publicly-traded firms from 1974 to 1993. The source of our data is Compustat which is a database on all publicly-traded firms in the US. Compustat obtains this information from reports that publicly traded companies must file with the US Securities and Exchange Commission. The database contains a large amount of information on each company. Among the items included are “sales,” “cost of goods sold,” “assets,” “number of employees,” and “property, plant, & equipment.”

Another item provided for each company is the Standard Industrial Classification (SIC) code. In principle, two companies in the same primary SIC code are in the same market; that is, they compete with each other. In practice, defining markets is extremely difficult [39]. More important for our analysis, virtually all modern firms sell in more than one market. Companies that operate in different markets do report some disaggregated data on the different activities. For example, while Philip Morris was originally a tobacco producer, it is also a major seller of food products (since its acquisition of General Foods) and of beer (since its acquisition of Miller Beer). Philip Morris does report its sales of tobacco products, food products, and beer separately. However, companies have considerable discretion in how to report information on their different activities, and differences in their choices make it difficult to compare the data across companies.

In this paper, the only use we make of the primary SIC codes in Compustat is to restrict our attention to manufacturing firms. Specifically, we include in our sample all firms with a major SIC code from 2000–3999. We do not use the data from the individual business segments of a firm, nor do we divide up the sample according to primary SIC codes. We should acknowledge that this choice is at odds with the mainstream of economic analysis. In economics, what is commonly called the “theory of the firm” is actually a theory of a business unit. To build on the Philip Morris example, economists would likely not use a single model to predict the behavior of Philip Morris. At the very least, they would use one model for the tobacco division, one for the food division, and one for the beer division. Indeed, given the available data, they might construct a completely separate model of, say, the sales of Maxwell House coffee. Absent any effect of the output of one of Philip Morris’ products on either the demand for or costs of its other products, the models of the different components of the firm would be completely separate. Because the standard model of the firm applies to business units, it does not yield any prediction about the distribution of the size of actual, multi-divisional firms or their growth rates.

On the other hand, the approach we take in this study is part of a distinguished tradition. First, there is a large body of work by Economics Nobel laureate H. Simon [25] and various co-authors that explored the stochastic properties of the dynamics of firm growth. Also, in a widely cited article (that nonetheless has not had much impact on mainstream economic analysis), R. Lucas, also a Nobel laureate, suggests that the distribution of firm size depends on the distribution of managerial ability in the economy rather than on the factors that determine size in the conventional theory of the firm [26].

In summary, the objective of our study is to uncover empirical scaling regularities about the growth of firms that could serve as a test of models for the growth of firms. We find: (i) the distribution of the logarithm of the growth rates for firms with approximately the same size displays an exponential form, and (ii) the fluctuations in the growth rates — measured by the width of this distribution — scale as a power law with firm size.

The paper is organized as follows: In Sect. II, we review the economics literature on the growth of companies. In Sects. III and IV, we present our empirical results for publicly-traded US manufacturing companies. Finally, in Sect. V, we present concluding remarks and discuss questions raised by our results.

II Background

In 1931, the French economist Gibrat proposed a simple model to explain the empirically observed size distribution of companies [17]. He made the following assumptions: (i) the growth rate of a company is independent of its size (this assumption is usually referred to by economists as the law of proportionate effect), (ii) the successive growth rates of a company are uncorrelated in time, and (iii) the companies do not interact.

In mathematical form, Gibrat’s model is expressed by the stochastic process:

| (1) |

where and are, respectively, the size of the company at times and , and is an uncorrelated random number with some bounded distribution and variance much smaller than one (usually assumed to be Gaussian). Hence follows a simple random walk and, for sufficiently large time intervals , the growth rates

| (2) |

are log-normally distributed. If we assume that all companies are born at approximately the same time and have approximately the same initial size, then the distribution of company sizes is also log-normal. This prediction from the Gibrat model is approximately correct [40, 41].

There is, however, considerable evidence that contradicts Gibrat’s underlying assumptions. The most striking deviation is that the fluctuations of the growth rate measured by the relative standard deviation decline with an increase in firm size. This was first observed by Singh and Whittington [42] and confirmed by others [6, 43, 44, 45, 46, 47]. The negative relationship between growth fluctuations and size is not surprising because large firms are likely to be more diversified. Singh and Whittington state that the decline of the standard deviation with size is not as rapid as if the firms consisted of independently operating subsidiary divisions. The latter would imply that the relative standard deviation decays as [42]. This confirms the common-sense view that the performance of different parts of a firm are related to each other.

The situation for the mean growth rate is less clear. Singh and Whittington [42] consider the assets of firms and observe that the mean growth rate increases slightly with size. However, the work of Evans [43] and Hall [44], using the number of employees to define the company’s size, suggests that the mean growth rate declines slightly with size. Dunne et al. [45] emphasize the effect of the failure rate of firms and the effect of the ownership status (single- or multi-unit firms) on the relation between size and mean growth rate. They conclude that the mean growth rate is always negatively related with size for single-unit firms; but for multi-unit firms, the growth rate increases modestly with size because the reduction in their failure rates overwhelms a reduction in the growth of nonfailing firms [45].

Another testable implication of Gibrat’s law is that the growth rate of a firm is uncorrelated in time. However, the empirical results in the literature are not conclusive. Singh and Whittington [42] observe positive first order correlations in the 1-year growth rate of a company (persistence of growth) whereas Hall [44] finds no such correlations. The possibility of negative correlations (regression towards the mean) has also been suggested [48, 49].

III Size distribution of publicly-traded companies

In the following sections, we study the distribution of company sizes and growth rates. To do so, one problem that must be confronted is the definition of firm size. If all companies produced the same good (steel, say), then we could use a physical measure of output, such as tons. We are, however, studying companies that produce different goods for which there is no common physical measure of output. An obvious solution to the problem is to use the dollar value of output: the sales. A general alternative to measuring the size of output is to measure input. Again, since companies produce different goods, they use different inputs. However, virtually all companies have employees. As a result, some economists have used the number of employees as a measure of firm size. Three other possibilities involve the dollar value of inputs, such as the “cost of goods sold,” “property, plant & equipment,” or “assets.” As we discuss below, we obtain similar results for all of these measures. We begin by describing the growth rate of sales. To make the values of sales in different years comparable, we adjust all values to 1987 dollars by the GNP price deflator.

Since the law of proportionate effect implies a multiplicative process for the growth of companies, it is natural to study the logarithm of sales. We thus define

| (3) |

and the corresponding growth rate

| (4) |

where is the size of a company in a given year and its size the following year.

Stanley et al. determined the size distribution of publicly-traded manufacturing companies in the US [40]. They found that for 1993, the data fit to a good degree of approximation a log-normal distribution. These results have been recently confirmed by Hart and Oulton [41] for a sample of approximately United Kingdom companies. Here, we present a study of the distribution for a period of 20 years (from 1974 to 1993).

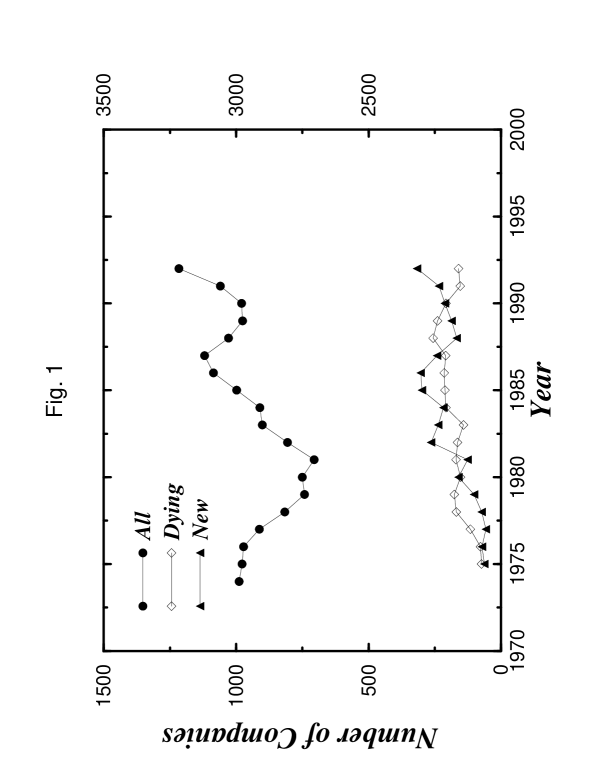

Figure 1 shows the total number of publicly-traded manufacturing companies present in the database each year. We also plot the number of new companies and of “dying” companies (i.e., companies that leave the database because of merger, change of name or bankruptcy).

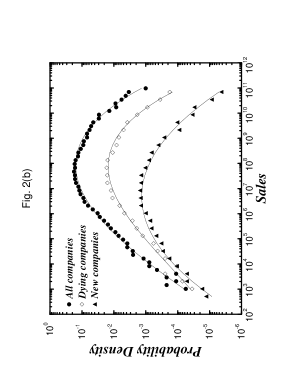

Figure 2(a) shows the distribution of firm size in each year from 1974–1993. Particularly above the lower tails, the distributions lie virtually on top of each other.

Thus the distribution is stable over this period. This is surprising because there is no existing theoretical reason to expect that the size distribution of firms could remain stable value slightly smaller than the average of all companies. One might as the economy grows, as the composition of output changes, and as factors that economists would expect to affect firm size (like computer technology) evolve. It is also important because it contradicts the predictions of the Gibrat model. Equation (1) implies that the distribution of sizes of companies should get broader with time. In fact, the variance of the distribution should increase linearly in time. Thus, we must conclude that other factors, not included in Gibrat’s assumptions, must have important roles.

One obvious factor not captured by the Gibrat assumption is the entry of new companies. Figure 2(b) shows that the size distribution of new publicly-traded companies is approximately a log-normal with an average expect new companies to be much smaller on average than existing ones. However, new companies can come about through the merger of two existing companies, in which case the new company is bigger than either of the pre-existing companies. Another way that new companies come into existence is that very large companies divest themselves of divisions that are, by themselves, large businesses. An example is AT&T’s recent divestiture of its manufacturing division (Lucent) and its computer division (NCR).

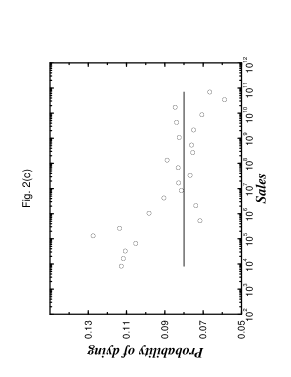

Another factor not included in Gibrat’s assumptions is the “dying” of companies. As shown in Fig. 2b, this distribution is quite similar to the distribution for all companies. Thus, it suggests that the probability for a company to leave the market, whether by merger, change of name, or bankruptcy, is nearly independent of size, Fig. 2c.

When analyzing the data, it is important to consider the high level of the noise in the tails. In building a histogram from the data, the most straightforward method is to use equally spaced bins. However, doing so creates noisy results in the tails because of the small number of data points in these regions. One way to solve this problem, especially if some knowledge of the shape of the distribution exists, is to take bins chosen with such lengths that all of them receive approximately the same number of data points. In fact, we used equally spaced bins on a logarithmic scale, i.e., all firms with sales values falling into an interval between and with an integer belong to one bin.

IV The distribution of growth rates

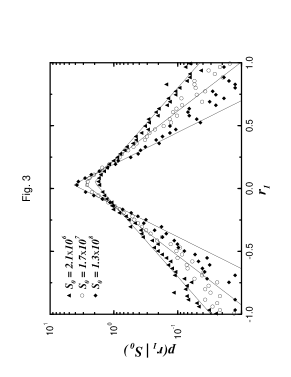

The distribution of the growth rates from 1974 to 1993 is shown in Fig. 3 for three different values of the initial sales. Remarkably, these curves can be approximated by a simple ”tent-shaped” form. Hence the distribution is not Gaussian — as expected from the Gibrat approach [17] — but rather is exponential [6],

| (5) |

The straight lines shown in Fig. 3 are calculated from the average growth rate and the standard deviation obtained by fitting the data to Eq. (5). The tails of the distribution in Fig. 3 are somewhat fatter than Eq. (5) predicts. This deviation is the opposite of what one would find if the distribution were Gaussian. We find that the data for each annual interval from 1974–1993 also fit well to Eq. (5), with only small variations in the parameters and .

A Mean growth rate

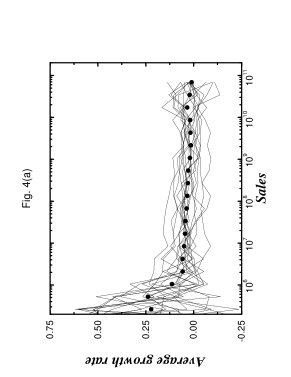

Economists typically have studied the relationship between mean growth rate and firm size by running a regression of growth rates on firm size sometimes with other control variables included. Rather than using regression analysis, we undertake a graphical analysis of the mean growth rate. Figure 4(a) displays as a function of initial size for several years. Although the data are quite noisy, they suggest that there is no significant dependence of the mean growth rate on . Least squares fits of the individual curves to a form lead to estimates of the proportionality constant which are very small in magnitude (), and whose sign can be positive or negative depending on the year. Our analysis suggests that if a dependence exists, it is very weak for any range of sizes where other factors, such as a bias of the sample towards successful companies, could be disregarded.

The analysis for the average of the nineteen 1-year periods, which is displayed in Fig. 4(b), confirms this observation. Furthermore, the figure suggests that the results do not change when we consider other definitions of the size of a company.

B Standard deviation of the growth rate

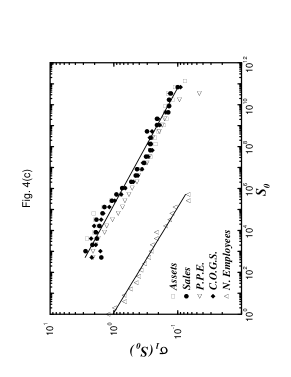

Next, we study the dependence of on . As is apparent from Figs. 3-4, the width of the distribution of growth rates decreases with increasing . We find that is well approximated for 8 orders of magnitude (from sales of less than dollars up to sales of more than dollars) by the law [6]

| (6) |

where . Equation (6) implies the scaling law

| (7) |

Figure 4(c) displays vs. , and we can see that Eq. (7) is indeed verified by the data.

C Other Measures of Size

In order to test further the robustness of our findings, we perform a parallel analysis for the number of employees. We find that the analogs of and behave similarly. For example, Fig. 4(c) shows the standard deviation of the number of employees, and we see that the data are linear over roughly 5 orders of magnitude, from firms with less than employees to firms with almost employees. The slope is the same, within the error bars, as found for the sales.

V Discussion

What is remarkable about Eqs. (5) and (7) is that they approximate the growth rates of a diverse set of firms. They range not only in their size but also in what they manufacture. The conventional economic theory of the firm is based on production technology, which varies from product to product. Conventional theory does not suggest that the processes governing the growth rate of car companies should be the same as those governing, e.g., pharmaceutical or paper firms.

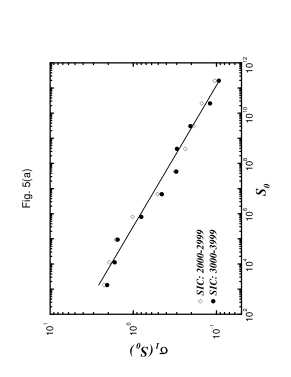

Indeed, our findings are reminiscent of the concept of universality found in statistical physics, where different systems can be characterized by the same fundamental laws, independent of “microscopic” details. Thus, we can pose the question of the universality of our results: Is the measured value of the exponent due to some averaging over the different industries, or is it due to a universal behavior valid across all industries? As a “robustness check,” we split the entire sample into two distinct intervals of SIC codes. It is visually apparent in Fig. 5(a) that the same behavior holds for the different samples of industries.

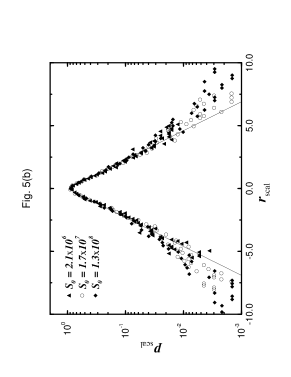

In statistical physics, scaling phenomena of the sort that we have uncovered in the sales and employee distribution functions are sometimes represented graphically by plotting a suitably “scaled” dependent variable as a function of a suitably “scaled” independent variable. If scaling holds, then the data for a wide range of parameter values are said to “collapse” upon a single curve. To test the present data for such data collapse, we plot in Fig. 5(b) the scaled probability density as a function of the scaled growth rates of both sales and employees . The data collapse relatively well upon the single curve . Our results for (i) cost of goods sold, (ii) assets, and (iii) property, plant & equipment are equally consistent with such scaling. The high degree of similarity in the behavior of sales, the number of employees, and of the other measures of size that we studied points to the existence of large correlations among those quantities, as one would expect.

In summary, we study publicly-traded US manufacturing companies from 1974 to 1993. We find that the distribution of the logarithms of the growth rate decays exponentially. Furthermore, we observe that the standard deviation of the distribution of growth rates scales as a power law with the size of the company. Our results support the possibility that the scaling laws used to describe complex but inanimate systems comprised of many interacting particles (as occurs in many physical systems) may be usefully extended to describe complex but animate systems comprised of many interacting subsystems (as occurs in economics). Furthermore, the kind of scaling laws found in this study can be viewed as empirical evidence supporting some hypothesis regarding the self-organization of the economy [16].

Acknowledgements.

We thank R. N. Mantegna for important help in the early stages of this work, and JNICT (L.A.), DFG (H.L. and P.M.), and NSF for financial support.REFERENCES

- [1] M. E. Fisher, Rep. Progr. Phys. 30, 615–731 (1967); M. E. Fisher, Critical Phenomena [Proc. 1970 Enrico Fermi Int. School of Physics, Course No. 51, Varenna, Italy], edited by M. S. Green (Academic Press for Ital. Phys. Soc., New York, 1971), pp. 1-99.

- [2] K. G. Wilson, The 1982 Nobel Lectures (World Scientific Press, Singapore, 1982).

- [3] P.-G. de Gennes, The 1991 Nobel Lectures (World Scientific Press, Singapore, 1991); Scaling Concepts in Polymer Physics (Cornell University Press, Ithaca, 1979).

- [4] B. B. Mandelbrot, The Fractal Geometry of Nature (W.H. Freeman, New York, 1983).

- [5] P. Bak, K, Chen, J. A. Scheinkman and M. Woodford, Richerche Economichi 47, 3 (1993); J. A. Scheinkman and J. Woodford, American Economic Review 84 417 (1994).

- [6] M. H. R. Stanley, L. A. N. Amaral, S. V. Buldyrev, S. Havlin, H. Leschhorn, P. Maass, M. A. Salinger, and H. E. Stanley, Nature 379, 804 (1996).

- [7] M. Levy, H. Levy, and S. Solomon, Economics Letters 45, 103 (1994).

- [8] J.-P. Bouchaud and D. Sornette, J. Phys. I (France) 4, 863 (1994); D. Sornette, A. Johansen, and J.-P. Bouchaud, J. Phys. I (France) 6, 167 (1996).

- [9] R. N. Mantegna and H. E. Stanley, Nature 376, 46 (1995).

- [10] S. Ghashghaie, W. Breymann, J. Peinke, P. Talkner, and Y. Dodge, Nature 381, 767 (1996); see also R. N. Mantegna and H. E. Stanley, Nature 383, 587 (1996), and A. Arneodo et al. (preprint).

- [11] M. Levy and S. Solomon, “Power laws are logarithmic Boltzmann laws” (preprint, 1996).

- [12] P. Bak, M. Paczuski, and M. Shubik, “Price variations in a stock market with many agents” (preprint, 1996).

- [13] M. Potters, R. Cont, J.-P. Bouchaud, “Financial markets as adaptative systems” (preprint, 1996).

- [14] H. Takayayasu, H. Miura, T. Hirabayashi, and K. Hamada, Physica A 184, 127–134 (1992).

- [15] T. Hirabayashi, H. Takayayasu, H. Miura, and K. Hamada, Fractals 1, 29–40 (1993).

- [16] P. R. Krugman, The Self-Organizing Economy (Blackwell Publishers, Cambridge, 1996).

- [17] R. Gibrat, Les Inégalités Economiques (Sirey, Paris, 1931).

- [18] R. H. Coase, Economica 4, 386 (1937).

- [19] P. E. Hart and S. J. Prais, J. Royal Statistical. Society, Series A 119, 150 (1956).

- [20] H. A. Simon and C. P. Bonini, American Economical Review 48, 607 (1958).

- [21] W. Baumol, Business Behavior, Value, and Growth (MacMillan, New York, 1959).

- [22] S. Hymer and P. Pashigian, J. Political Economics 52, 556 (1962).

- [23] R. Cyert and J. March. A Behavioral Theory of the Firm (Prentice-Hall, Englewood Cliffs, New Jersey, 1963).

- [24] M. C. Jensen and W. H. Meckling, Journal Financial Economics. 3, 305 (1976).

- [25] Y. Ijiri and H. A. Simon, Skew Distributions and the Sizes of Business Firms (North Holland, Amsterdam, 1977).

- [26] R. Lucas, Bell J. Economics 9, 508 (1978).

- [27] B. Jovanovic, Econometrica 50, 649 (1982).

- [28] R. R. Nelson and S. G. Winter, An Evolutionary Theory of Technical Change (Harvard University Press, Cambridge, Massachusetts, 1982).

- [29] A. Golan, A Discrete Stochastic Model of Economic Production and a Model of Fluctuations in Production – Theory and Empirical Evidence (Ph.D. Thesis, University of California, Berkeley, 1988).

- [30] H. R. Varian, Microeconomics Analysis (Norton, New York, 1978).

- [31] B. R. Holmstrom and J. Tirole, in Handbook of Industrial Organization Vol. 1, eds. R. Schmalensee and R. Willig, 61 (North Holland, Amsterdam, 1989).

- [32] O. E. Williamson, in Handbook of Industrial Organization Vol. 1, eds. R. Schmalensee and R. Willig, 135 (North Holland, Amsterdam, 1989).

- [33] P. Milgrom and J. Roberts, Economics, Organization, and Management (Prentice-Hall, Englewood Cliffs, New Jersey, 1992).

- [34] R. Radner, Econometrica 61, 1109 (1993).

- [35] A. Golan, Advances in Econometrics 10, 1 (1994).

- [36] D. Shapiro, R. D. Bollman, and P. Ehrensaft, American J. Agricultural Economics 69, 477 (1987).

- [37] A. Pakes and P. McGuire, Rand Journal 25, 555 (1994).

- [38] R. E. Ericson and A. Pakes, Review of Economic Studies 62, 53 (1995).

- [39] F. M. Scherer and D. R. Ross, Industrial Market Structure and Economic Performance (Houghton Mifflin, Boston, 1990).

- [40] M. H. R. Stanley, S. V. Buldyrev, R. Mantegna, S. Havlin, M. A. Salinger, and H. E. Stanley, Economics Letters 49, 453 (1995).

- [41] P. Hart and N. Oulton, The Economic Journal (in press).

- [42] A. Singh and G. Whittington, Review Economical Studies 42, 15 (1975).

- [43] D. S. Evans, J. Political Economics 95, 657 (1987).

- [44] B. H. Hall, J. Industrial Economics 35, 583 (1987).

- [45] T. Dunne, and M. Roberts, and L. Samuelson, Quaterly J. Economics 104, 671 (1989).

- [46] S. J. Davis and J. Haltiwanger, Quaterly Journal Economics 107, 819 (1992).

- [47] S. J. Davis, J. Haltiwanger, and S. Schuh, Job Creation and Destruction (MIT Press, Cambridge, Massachusetts, 1996).

- [48] J. Leonard, National Bureau of Economic Research, working paper no. 1951, (1986).

- [49] M. Friedman, J. Economical Literature 30, 2129 (1992).