Volatility smile and stochastic arbitrage returns

Sergei Fedotov and Stephanos Panayides

Department of Mathematics, UMIST, M60 1QD UK

Accepted for publication in Physica A on 27 May 2004

Keywords: option pricing, arbitrage, financial markets, volatility smile

Abstract

The purpose of this work is to explore the role that random arbitrage opportunities play in pricing financial derivatives. We use a non-equilibrium model to set up a stochastic portfolio, and for the random arbitrage return, we choose a stationary ergodic random process rapidly varying in time. We exploit the fact that option price and random arbitrage returns change on different time scales which allows us to develop an asymptotic pricing theory involving the central limit theorem for random processes. We restrict ourselves to finding pricing bands for options rather than exact prices. The resulting pricing bands are shown to be independent of the detailed statistical characteristics of the arbitrage return. We find that the volatility “smile” can also be explained in terms of random arbitrage opportunities.

1 Introduction

It is well-known that the classical Black-Scholes formula is consistent with quoted options prices if different volatilities are used for different option strikes and maturities [1]. To explain this phenomenon, referred to as the volatility “smile”, a variety of models has been proposed in the financial literature. These includes, amongst others, stochastic volatility models [2, 3, 4], the Merton jump-diffusion model [5] and non-Gaussian pricing models [6, 7]. Each of these is based on the assumption of the absence of arbitrage. However, it is well known that arbitrage opportunities always exist in the real world (see [8, 9]). Of course, arbitragers ensure that the prices of securities do not get out of line with their equilibrium values, and therefore virtual arbitrage is always short-lived. One of the purposes of this paper is to explain the volatility “smile” phenomenon in terms of random arbitrage opportunities.

The first attempt to take into account virtual arbitrage in option pricing was made by physicists in [10, 11, 12]. The authors assume that arbitrage returns exist, appearing and disappearing over a short time scale. In particular, the return from the Black-Scholes portfolio, where is the option price written on an asset is not equal to the constant risk-free interest rate . In [11, 12] the authors suggest the equation where is the random arbitrage return that follows an Ornstein-Uhlenbeck process. In [13, 14] this idea is reformulated in terms of option pricing with stochastic interest rate. The main problem with this approach is that the random interest rate is not a tradable security, and therefore the classical hedging can not be applied. This difficulty leads to the appearance of an unknown parameter, the market price of risk, in the equation for derivative price [13, 14]. Since this parameter is not available directly from financial data, one has to make further assumptions on it. An alternative approach for option pricing in an incomplete market is based on risk minimization procedures (see, for example, [15, 16, 17, 18, 19]). Interesting ideas how to include arbitrage were developed in [20] where the Black-Scholes pricing model was discussed in a quantum physics setting.

In this paper we follow an approach suggested in [4] where option pricing with stochastic volatility is considered. Instead of finding the exact equation for option price, we focus on the pricing bands for options that account for random arbitrage opportunities. We exploit the fact that option price and random arbitrage return change on different time scales allowing us to develop an asymptotic pricing theory by using the central limit theorem for random processes [21]. The approach yields pricing bands that are independent of the detailed statistical characteristics of the random arbitrage return.

2 Model with random arbitrage return

Consider a model of market that consists of the stock, , the bond, and the European option on the stock, . To take into account random arbitrage opportunities, we assume that this market is affected by two sources of uncertainty. The first source is the random fluctuations of the return from the stock, described by the conventional stochastic differential equation,

| (1) |

where is a standard Wiener process. The second source of uncertainty is a random arbitrage return from the bond described by

| (2) |

where is the risk-free interest rate. Given that there are random arbitrage opportunities, we introduce here the random process, that describes the fluctuations of return around The same mapping to a model with stochastic interest rate is used in [11, 12, 13]. The characteristic of the present model is that we do not assume that obeys a given stochastic differential equation. For example, in [11, 12, 13] follows the Ornstein-Uhlenbeck process [22].

It is reasonable to assume that random variations of arbitrage return are on the scale of hours. Let us denote this characteristic time by This time can be regarded as an intermediate one between the time scale of random stock return (infinitely fast Brownian motion fluctuations), and the lifetime of the derivative (several months): . In what follows, we exploit this difference in time scales and develop an asymptotic pricing theory involving the central limit theorem for random processes.

Now we are in a position to derive the equation for Let us consider the investor establishing a zero initial investment position by creating a portfolio consisting of a long position of one bond, shares of the stock, and a short position in one European option, with an exercise price, and a maturity, The value of this portfolio is

| (3) |

The Black-Scholes dynamic of this portfolio is given by two equations, and (see [1]). The application of Ito’s formula to (3) together with (1) and (2) with leads to the classical Black-Scholes equation:

| (4) |

The natural generalization of is a simple non-equilibrium equation:

| (5) |

where is the characteristic time during which the arbitrage opportunity ceases to exist (see [10]).

By using a self-financing condition, and Ito’s lemma, one can derive from (1) and (2) the equation involving the option and the portfolio value ,

| (6) |

Note that this equation reduces to (4) when and

To deal with the forward problem we introduce the non-dimensional time

| (7) |

and a small parameter

| (8) |

This parameter plays a very important role in what follows. In the limit the stochastic arbitrage return becomes a function that is rapidly varying in time. It is convenient to use the following notation, (see [4]). It follows from (5) that the value of the portfolio decreases to zero like Thus, one can assume that in the limit We find from (6) that the associated option price, obeys the following stochastic PDE

| (9) |

subject to the initial condition:

| (10) |

for a call option, where is the strike price. Here, for simplicity, we keep the same notations for the non-dimensional volatility and the interest rate The same PDE is used in [11, 12], but with the Ornstein-Uhlenbeck process for

3 Asymptotic analysis: pricing bands for the options

To analyze the stochastic PDE (9), we have to specify the statistical properties of the random arbitrage return . Suppose that is a stationary ergodic random process with zero mean, such that,

| (11) |

is finite. The key feature of this paper is that we do not assume an explicit equation for unlike the works [11, 12, 13], where the random arbitrage return follows the Ornstein-Uhlenbeck process.

According to the law of large numbers, converges in probability to the Black-Scholes price, as One can split into the sum of the Black-Scholes price, , and the random field with the scaling factor giving

| (12) |

Substituting (12) into (9), and using the equation for , we get the following stochastic PDE for ,

| (13) |

Our objective here is to find the asymptotic equation for as One can see that Eq. ( 13) involves two stochastic terms proportional to and . Ergodic theory implies that the first term in its integral form converges to zero as while the second term converges weakly to a white Gaussian noise with the correlation function

| (14) |

where the intensity of white noise, is determined by (11) (see [21] and Appendix A). Thus, in the limit the random field converges weakly to the field that obeys the asymptotic stochastic PDE:

| (15) |

with the initial condition . This equation can be solved in terms of the classical Black-Scholes Green function, to give

| (16) |

where

| (17) |

(see, for example, [25]).

It follows from (16) that since is the Gaussian noise with zero mean, is also the Gaussian field with zero mean. The covariance

| (18) |

satisfies the deterministic PDE:

| (19) |

with (see Appendix B). The pricing bands for the options for the case of arbitrage opportunities can be given by

| (20) |

where

| (21) |

The variance quantifies the fluctuations around the classical Black-Scholes price. It should be noted that it is independent of the detailed statistical characteristics of the arbitrage return. The only parameter we need to estimate is the intensity of noise which is the integral characteristic of random arbitrage return (see (11)). One can conclude that the investor who employs the arbitrage opportunities band hedging sells the option for

| (22) |

where can be found from (16) or (19) to be

| (23) |

(see Appendix C).

4 Numerical results

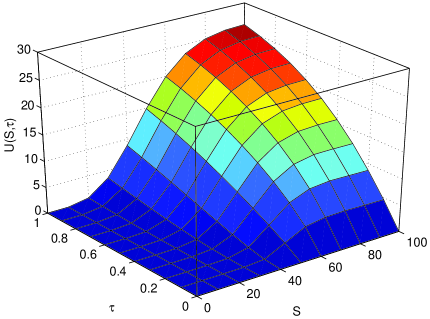

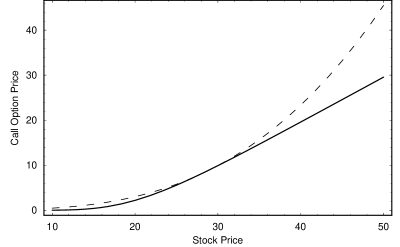

To determine how the random arbitrage opportunities affect the option price, we solve equation (19) numerically. Figure 1 shows a graph of the variance, , as a function of both time, , and asset price, . From this graph, we observe that the uncertainty regarding the option value is greater for deep-in-the money options. This finding is consistent with the empirical work given in [23]. In Figure 2, we plot the effective option price given by (22) for , and compare it with the Black-Scholes price. Note that deep-in-the money options deviate the most from the Black-Scholes option price. As we move near at-the-money options the deviation decreases.

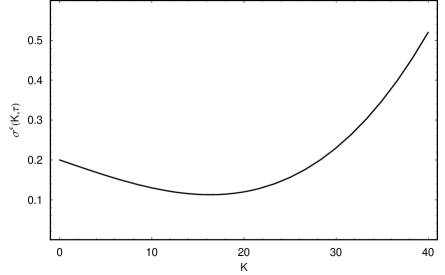

Now we are in a position to discuss the ”smile” effect, that is, the implied volatility is not a constant, but varies with strike price and time Let us denote the implied Black-Scholes volatility by The formula (22) for the effective option price implies

| (24) |

This equation can be solved for with and fixed. It follows from (22) that as Fig.3 illustrates the ‘smile’ effect, when implied volatility increases for deep-in and out-of-the money options. Similar results are given in [24] where the characteristic time depends on moneyness . Numerical results give a similar smile curve where the implied volatility becomes greater as we move away from at-the-money.

5 Conclusions

In this paper, we investigated the implications of random arbitrage return for option pricing. We extended previous works by using a stationary ergodic process for modelling random arbitrage return. We considered the case where arbitrage return fluctuates on a different time scale to that of the option price. This allowed us to use asymptotic analysis to find option pricing bands rather than the exact equation for option value. We derived the asymptotic equation for the random field that quantifies the fluctuations around the classical Black-Scholes price and showed that it is independent of the detailed statistical characteristics of the arbitrage return. In particular, we showed that the risk from the random arbitrage returns is greater for deep-in and out-of-the money options. This gives an explanation of the “smile” effect observed in the market in terms of the random arbitrage return.

Appendix A

The random process defined as

| (A-1) |

converges weakly to the Brownian motion as . It means that converges weakly to a white Gaussian noise with the correlation function (note that

The purpose of this Appendix is to show that

| (A-2) |

It follows from (A-1) that

| (A-3) |

By using the well-known formula for stationary process with zero mean

| (A-4) |

one finds that

| (A-5) |

In the limit the second term tends to zero, and so we must have

where

| (A-6) |

Appendix B

In this Appendix we derive the equation (19) for the covariance

| (B-1) |

First, let us find the derivative of with respect to time

| (B-2) |

Substitution of the derivatives and from equation (15) into (B-2) and averaging give

| (B-3) | |||||

This equation involves the correlation functions and that can be found as follows. Since the random process is Gaussian, one can use the Furutsu-Novikov formula to find

| (B-4) |

(see [26]). By using delta-correlated function for given by (14), and equation (15), we can find the variational derivative

Appendix C

References

- [1] J. C. Hull, Options, Futures and Other Derivatives, 4th Edition, Prentice-Hall, London (2000).

- [2] J. P. Fouque, G. Papanicolaou, and K. R. Sircar, Derivatives in Financial Markets with Stochastic Volatility, Cambridge University Press (2000).

- [3] A. Lewis, Option Valuation under Stochastic Volatility, Finance Press, Newport Beach, CA (2000).

- [4] G. C. Papanicolaou and K. R. Sircar, Stochastic Volatility, Smiles and Asymptotics, Applied Mathematical Finance 6 (1999) 107-145.

- [5] R. C. Merton, Continuous-Time Finance, Blackwell (1992).

- [6] L. Borland, Theory of Non-Gaussian Option Pricing, Quantitative Finance 2 (2002) 415-431.

- [7] L. Borland and J.P. Bouchaud, Non-Gaussian Option Pricing Model with Skew, cond-mat/0403022.

- [8] D. Galai, Tests of market Efficiency and the Chicago Board Option Exchange, J. Business 50 (1997) 167-197.

- [9] G. Sofianos, Index Arbitrage Profitability, NYSE working paper 90-04, J. Derivatives 1(N1) (1993).

- [10] A. N. Adamchuk and S. E. Esipov, Collectively Fluctuating Assets in the Presence of Arbitrage Opportunities and Option Pricing, Physics - Uspekhi 40(12) (1997) 1239-1248.

- [11] K. Ilinski, How to Account for the Virtual Arbitrage in the Standard Derivative Pricing, preprint, cond-mat/9902047.

- [12] K. Ilinski and A. Stepanenko, Derivative Pricing with Virtual Arbitrage, preprint, cond-mat/9902046.

- [13] M. Otto, Stochastic Relaxational Dynamics Applied to Finance: Towards Non-Equilibrium Option Pricing Theory, Eur. Phys. J. B. 14 (2000) 383-394.

- [14] M. Otto, Towards Non-Equilibrium Option Pricing Theory, Internal J. Theoret. & Appl. Fin. 3(3) (2000) 565.

- [15] E. Aurell and S. Simdyankin, Pricing Risky Options Simply, Int. J. Theoretical and Applied Finance 1(1) (1998) 1-23.

- [16] J. P. Bouchaud and D. Sornette, The Black-Scholes Option Pricing Problem in Mathematical Finance: Generalization and Extensions for a Large Class of Stochastic Processes, J. Phys. 4(I) (1994) 863-881.

- [17] S. Fedotov and S. Mikhailov, Option Pricing for Incomplete Markets via Stochastic Optimization: Transaction Costs, Adaptive Control and Forecast, Int. J. Theoretical and Applied Finance 4(1) (2001).

- [18] M. Schäl, On Quadratic Cost Criteria for Option Hedging, Math. Oper. Res. 19 (1994) 121-131.

- [19] M. Schweizer, Variance-Optimal Hedging in Discrete Time, Math. Oper. Res. 20 (1995) 1-32.

- [20] E. Haven, A discussion on embedding the Black-Scholes Option Pricing Model in a Quantum Physics Setting, Physica A (2002) 507-524.

- [21] M. I. Freidlin and A. D. Wentzell, Random Perturbations of Dynamical Systems, Springer-Verlag, New York (1984).

- [22] B. Oksendal, Stochastic Differential Equations, 4th edition, Springer, New York (1998).

- [23] G. Bakshi, C. Cao, and Z. Chen, Empirical Performance of Alternative Option Pricing Models, The Journal of Finance (1997) 2003-2049.

- [24] M. Otto, Finite Arbitrage Times and the Volatility Smile, Physica A (2001) 299-304.

- [25] R. Courant, and D. Hilbert, Methods of Mathematical Physics, Volume II, Partial Differential Equations, Wiley (1989).

- [26] F. Moss, and P. V. E. McClintock (eds) Noise in Nonlinear Dynamical Systems, Vol. 1, Cambridge University Press, Cambridge (1989).

- [27] R. P. Feynman and A. R. Hibbs, Quantum Mechanics and Path Integrals, McGraw Hill, NY (1965).