Zdzisław Burda

Jerzy Jurkiewicz

Bartłomiej Wacław

Mark Kac Center for Complex Systems Research and

Marian Smoluchowski Institute of Physics,

Jagellonian University, ul. Reymonta 4, 30-059 Krakow, Poland

Abstract

We present an analytic method to determine

spectral properties of the covariance matrices

constructed of correlated Wishart random matrices.

The method gives, in the limit of large matrices,

exact analytic relations between the spectral moments

and the eigenvalue densities of the covariance matrices

and their estimators.

The results can be used in practice

to extract information about the genuine

correlations from the given experimental realization

of random matrices.

Wishart random matrices play an important role in the

multivariate statistical analysis w ; a .

They are useful in some problems

of fundamental physics dj ,

communication and information theory mea ; sm1 ; s ,

internet trading mz

and quantitative finance lcbp ; pea ; bj .

A Wishart ensemble of correlated random matrices is

defined by a Gaussian probability measure:

(1)

where is a real rectangular matrix of

dimension . It has two types of indices:

an -type index runnig over the set

and a -type index over .

Throughout the paper the -type indices will be denoted

by Latin letters and the -type by Greek ones.

denotes the transpose of .

The matrices and are

symmetric square matrices of dimensions and ,

respectively. They are positive definite.

is a normalization constant:

(2)

chosen to have .

Let be a quantity depending on .

The average of over the random matrix ensemble (1)

is defined as:

(3)

In particular, the two-point correlation function is:

(4)

as directly follows from the Gaussian integration. In this paper

we are interested in the spectral behaviour,

the eigenvalue distribution and the spectral moments

of the following random matrices:

(5)

These matrices can be used as estimators of

the correlation matrices and if some

realizations of random matrices are given. We will refer to

and as to covariance matrices or

statistically dressed correlation matrices.

We will present an analytic method to determine

the eigenvalue distribution and the spectral moments

of and in the limit of large matrix size.

Another method of calculating the eigenvalue density of correlated

Wishart matrices has been recently discussed in sm2 .

In parallel to (1) one can define a Wishart

ensemble of correlated complex matrices:

(6)

The matrices and are now Hermitean and positive definite.

denotes the Hermitean conjugate of .

The normalization constant is now

.

In the analysis of the complex ensemble the estimators

(5) of the correlation matrices

are replaced correspondingly by

(7)

Notice that the factor one half in front of the trace

in the measure for real matrices (1) is dropped

in (6). With this choice of the measure

the two-point correlations take a similar form

as for real matrices (4):

(8)

The star stands for

the complex conjugation. Additionally we also have:

(9)

As a consequence, as we shall discuss towards the end of the paper,

the matrices and (5) in the real ensemble

have an identical large behaviour

as the corresponding matrices (7) in the complex ensemble.

Since we are interested here only in the large

behaviour it is sufficient to consider one of the two

ensembles and draw conclusions for the other. We will focus

the presentation on the ensemble of real matrices.

An example of a problem which can

be formulated in terms of Wishart random matrices

(1) is the following.

Imagine that we probe a statistical system of correlated

degrees of freedom by doing measurements. We store the

measured values of the -th degree of freedom

in the -th measurement in a rectangular

matrix . The degrees of freedom

as well as the measurements may be correlated.

This is expressed by the equation (4), which tells us

that the covariance matrix for the correlations between

degrees of freedom in the system is and for the

(auto)correlation between measurements is .

Note that in general the correlations between

and may have a more complicated form:

, where the matrix has

double indices. Such a situation takes place

if the autocorrelations are different for various degrees

of freedom. We shall not discuss this case here.

Moreover, we shall assume that only Gaussian effects are important

for the studied system.

A perfect example of the situation described above

is the problem of optimal portfolio assessment - one of

the fundamental problems of quantitative finance. The portfolio

assessment is based on the knowledge of the covariance matrix

for stocks returns ret .

In practice, the covariance matrix is estimated from the historical data

which are stored in a rectangular matrix representing

historical values of stocks.

Fluctuations of returns are well described by the Gaussian

ensemble (1).

The estimator of the covariance matrix is given by (5).

Another problem of modern financial analysis

which can be directly cast into the form (1) is

the problem of taste matching mz . This problem is encountered

for instance in the large-scale internet trading.

It is worth mentioning that the

random matrix framework may also be used in a statistical description

of data generated in Monte Carlo simulations

for a system with many degrees of freedom, in particular of data

concerning the correlation functions. One frequently

encounters such a problem in Monte-Carlo simulations of

lattice field theory, where the field is represented

by correlated numbers distributed on a lattice. Usually,

one is forced to use a dynamical Monte Carlo algorithm

to sample such a system. The basic idea standing behind

a dynamical algorithm is to

generate a Markov chain – a sort of a

random walk – in the space of configurations. The degrees

of freedom on the lattice as well as the successive

configurations are usually correlated. Outside a critical region

no long range correlations are observed and the fluctuations

can be treated as Gaussian.

Complex random matrices are useful

for instance in telecommunication

or information theory mea ; sm1 ; s .

Let us come back to the ensemble of real matrices (1).

As we mentioned the matrices (5) can be treated as estimators

of the correlation matrices and . Indeed,

from equation (4) we see that:

(10)

(11)

where

and .

This notation will be explained later.

The last equation tells us that measuring the average of

over the ensemble (1)

we obtain the matrix up to a constant. In other words

having a realization of random matrices we can use

(5) to estimate .

Similarly, we can use to estimate .

Notice that the measure (1) is invariant under

the transformation and

, where is an

arbitrary positive real number. In particular

and

are independent of the

rescaling factor . This independence is ensured by the

presence of the factors and in

equations (10,11). In practical calculations,

if and are not specified,

one can remove the redundancy with respect to the rescaling

by , setting .

In this case the constants can be determined

from the data by evaluating the traces of or :

While considering the covariance matrices for

the Wishart ensemble we can formulate two reciprocal problems,

which we shall call direct and inverse problem.

In the direct problem

we want to learn as much as possible about

the probability distribution of the estimators and (5)

assuming that the matrices and are given.

In particular, we want to calculate the eigenvalue density

functions:

where and are eigenvalues of and ,

respectively. The determination of the eigenvalue density functions

is equivalent to the determination of all their spectral moments:

The moments are related to each other:

(12)

where , as follows from the cyclicity of the trace:

In the inverse problem we want to learn as much

as possible about the genuine correlations in the system,

which are given by and ,

using a measured sample of random matrices .

We can do this by computing the estimators and (5)

and relating them to matrices .

In particular we would like to estimate the eigenvalue

distributions and the moments of :

where and are eigenvalues

of and , respectively.

The inverse problem is very important for practical applications,

since in practice it is very common to reconstruct the properties of

the underlying system from the experimental data.

In the analysis of the spectral properties of the matrices

and it is convenient to apply the

Green’s function technique. One can define Green’s functions

for the correlation matrix and its statistically

fluctuating counterpart :

(13)

(14)

and correspondingly and for and .

The symbol stands for the identity matrix.

A corresponding symbol appears in the definition of

and .

The Green’s functions are related to the generating functions

for the moments:

(15)

(16)

or inversely:

(17)

The analogous relations exist for and .

The Green’s functions can be used for finding the densities of eigenvalues:

(18)

and similarly for .

The eigenvalue densities and

are not independent.

As follows from (12) the corresponding generating

functions (16) fulfill the equation:

The meaning of the last term on the right hand side of this equation

is that there are zero modes in the matrix

if . The zero modes disappear when .

Moving the term containing the delta function

to the other side of equation, dividing both sides of the

equation by and substituting the parameter

by we obtain:

(22)

Therefore, for the zero modes

appear in the spectrum .

In this case it is more convenient to use the

parameter instead of .

The zero modes appear in the

eigenvalue distribution of either or .

The two equations (21)

and (22) are dual to each other.

For they are identical.

Because of the duality it is sufficient to solve the problem

for . We will present a solution for the limit

and

neglecting effects of the order .

Using a diagrammatic method fz ; sm3 ; bgjj one

can write down a closed set of equations for

the Green’s function (14):

(23)

The set contains four equation for four unknown matrices

including which we want to calculate, and

three auxiliary ones:

, , (see Appendix 1).

Each of them can be interpreted in terms of a generating function for

appropriately weighted diagrams with two external lines:

for all diagrams

and

for one-line-irreducible diagrams fz ; sm3 ; bgjj (see Appendix 1).

In the limit the weights of

non-planar diagrams vanish at least as .

Thus in this limit only planar diagrams give a contribution

to the Green’s function.

Therefore the large limit is alternatively called

the planar limit. The diagrammatic equations (23)

hold only in this limit. An analogous set of equations

can be written for the Green’s function . The equations

are identical to those of (23) if one

exchanges ,

and . The two sets can be solved

independently of each other. However, as follows

from the duality (20) it is sufficient to solve

only one of them and deduce the solution of the other.

The equations (23) can be solved for

by a successive elimination of

, and .

However, the resulting equation is very entangled sm3 :

(24)

and cannot be easily used in practical calculations

of the moments or spectral density .

Another way of solving the equations (23)

was proposed in bgjj .

It relies on introducing a new complex variable

conjugate to which is defined by the equation:

(25)

At the first glance this equation looks useless because

it refers to an unknown function which we actually

want to determine. Quite contrary to this,

as we shall see, the introduction of the conjugate

variable allows us to write down

a closed functional equation for .

First, let us illustrate how the method works

for bgjj .

In this case, the elimination of the auxiliary functions

(23) leads to

(26)

or equivalently to

(27)

Suppose we solve the direct problem. In this case

we know the matrix and hence also the generating function

. Inserting (26) to (25)

we obtain a closed compact functional relation

for :

(28)

If has a simple form,

one can solve the equation for analytically bgjj .

In general, one can write a numerical program to calculate

the eigenvalue density from the last

equation. In case of solving the inverse problem, we assume

that we can determine moments from the data

and hence that we can approximate the generating

function . Then we can insert (27)

to (25) and obtain a functional

equation for :

(29)

The problem is solved in principle. However, in practical

terms the inverse problem is much more difficult, because one

cannot compute all experimental moments with an

arbitrary accuracy, unless one has an infinitely long series

of measurements. But one never has.

In practice one can estimate only a few lower moments

with a good accuracy. Because of this practical

limitation one cannot entirely solve the inverse problem.

However, as we discussed in bj the inverse problem

can be partially solved even in specific practical applications

using a moments method. Let us sketch this method below.

We can gain some insight into the spectral

properties of the correlation matrix by determining

the relation between the moments and .

Expanding the functions and in (28)

in using (15,16) and comparing

the coefficients at we obtain:

(30)

We can also invert the equations for .

The result of inversion gives a set of equations which

can be directly obtained from the expansion of the functions

in the equation (29)

which is the inverse transform of (28).

We can also determine the corresponding relations

for ’negative’ moments and ,

that is for , or determine the spectral

density bgjj .

Using a computer tool for symbolic calculations

one can easily write a program which successively

generates the relations between spectral moments (30)

from the equation (28).

The calculations get more complicated in the general

case when both and are arbitrary.

The guiding principle is the same, though. We introduce the conjugate

variable (25) and, using it, write down

the solution of the equations (23).

In the direct problem we assume that

the generating functions and are known.

We will show that in this case the solution of (23)

takes a form of an explicit equation for , where the function

depends on the functions and . Inserting

this solution back to (23) we eventually obtain

a functional equation from which we can

extract the function .

where are eigenvalues of . It can

be rewritten as:

(32)

and can be formally solved for :

(33)

where is the inverse function of .

Thus we have obtained an explicit equation for

in terms of the known functions and .

One can easily check that for the last equation

reduces to (27). In this case ,

.

Combining the equation for given by (33) with

(25) we arrive at a closed equation for

the generating function . It can be used

for example to calculate the moments

’s (see Appendix 2). The calculations

yield a set of equations expressing ’s in terms

of the bare moments and :

Using the relations (12) we can also determine the

moments of the matrix . It is more convenient to write them

using the variable – the dual counterpart of –

instead of itself:

(35)

The equations are completely symmetric to (34)

with respect to the change

(which amounts to ),

and , .

Using this method one can obtain equations (34) and (35)

to an arbitrary order.

The above relations are useful for computing the dressed moments

for given matrices or inversely,

the genuine moments from the experimental data.

As mentioned, the spectral moments give us in principle

full information about the eigenvalue distribution.

In practice the reconstruction of the eigenvalue

density may be difficult, because to do it

we would need to know all moments with a very good precision.

Usually, in practical applications one can accurately evaluate

only a few lower moments.

In some special cases if we can make some extra assumptions

about the form of the matrices or we can improve

significantly the reconstruction of the eigenvalue density.

In the previous work bgjj we have analysed the case of

and of the matrix which had only a few distinct eigenvalues.

In this case the Green’s function is given by an

algebraic equation of the order which is equal to the number

of distinct eigenvalues. It can be analytically solved when

this number

is less or equal four. If it is larger the problem can be

handled numerically. The duality tells us that the solution

also holds when we change the roles of and .

Below we will discuss the case of exponential autocorrelations.

Exponential correlations are encountered in many situations.

The general solution, which we have discussed so far, simplifies

in this case to a more compact relation for the Green’s function,

which allows us to find analytically an approximate form of the

eigenvalue density of the random matrices and .

The approximation becomes exact in the large limit.

We consider purely exponential autocorrelations given by

the autocorrelation matrix:

(36)

where controls the range of autocorrelations.

The inverse of the matrix reads:

(37)

We have introduced here a shorthand notation

, and .

The spectrum of this matrix can be

approximated by the spectrum of a matrix :

(38)

whose eigenvalues can be found analytically:

The corresponding eigenvectors are given by the Fourier

modes. The matrix can be viewed as of a sum:

, of

a unity matrix multiplied by a constant and a

discretized one-dimensional Laplacian

for a cyclic chain of length . The matrix

can be obtained from by adding to it a perturbation

: ,

where has only four non-vanishing elements:

and .

The first order corrections to the eigenvalues of ,

which stem from the perturbation , behave as .

The perturbation can be viewed as a change of a boundary

condition of the Laplacian. As usual, boundary conditions

affect mostly the longest (small momentum) modes.

Indeed, a careful analysis shows that the two diagonal terms

of the perturbation matrix, , introduce a constant

correction independent of of the lowest eigenvalues which

does not vanish when goes to infinity.

However, since the differences between unperturbed eigenvalues

of and the corresponding perturbed eigenvalues of

disappear for all other eigenvalues,

we expect that for the spectral properties of

can be well approximated by the eigenvalues of :

(39)

In this limit we can also approximate the

sum (31) by an integral:

(40)

Where and the symbol

is introduced for brevity. Note that

in the definition of we have replaced ,

which would rather be dictated by (31), by

. This change is legitimate due to (25).

The integral (40) can be done:

(41)

Setting back we eventually obtain:

(42)

This is an explicit equation for which can be now

inserted into giving us a compact

relation for

in the presence of the exponential autocorrelations (36):

(43)

In the limit , the parameters

, and increase

to infinity and . As a consequence,

the form of equation (42) simplifies to (26), which

corresponds to the case without autocorrelations, as expected.

Using the equation (43) we can recursively generate

equations for the consecuitive moments:

(44)

where .

The coefficients on the right hand side, which depend

on , can be directly expressed in terms of

the moments of the matrix .

Approximating again a sum by an integral

in the large limit we can write:

The integrals can be calculated yielding:

(51)

We see that if we insert these coefficients into the equations

(34) we obtain (44). This is a consistency

check for the approximation which we use here.

The quality of this approximation can also be checked

by comparing the moments of the matrix

(36) for finite with the result (51)

which corresponds to . We expect that for

the numerical values shall approach the result (51).

The results of this comparison confirm our expectations (see table 1).

Table 1: The moments , and

of the matrix (36) for three values of the

autocorrelation length calculated numerically

for finite size and by the analytic formula

(51) which corresponds to . The finite size

values approach the values given by (51) as tends

to infinity.

Thus we see that the formula (44) for

in the presence of the exponential autocorrelations

becomes exact in the limit .

This formula allows us to compute the eigenvalue distribution

of the random matrices and (5). Let us illustrate

this on the simplest example of the system which has no

correlations: and

.

In this case the equation (43) for

takes the form:

(52)

where we have used the notation .

For () this equation

reduces to:

(53)

which has a solution:

(54)

where , which leads to the well-known

result for the uncorrelated Wishart ensemble:

(55)

For it is still possible to find analytically

a solution of (52).

Let us rewrite (52) as a polynomial equation:

It has two trivial solutions . Dividing out

the polynomial we get:

(56)

This is a quartic equation which can be solved analytically

by the Ferrari method. We will not present the formal solution

which is neither transparent nor informative.

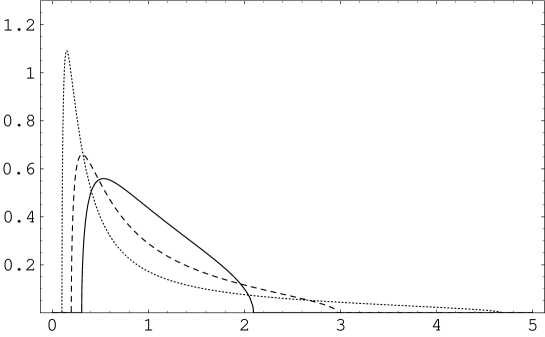

Instead, we show in Fig. 1

the eigenvalue density functions , for

different , resulting from this solution.

The lower part of the distribution

approaches zero when increases, but zero modes do

not appear in the distribution as long as .

Figure 1: The density of eigenvalues

for exponential matrix , and for three

different autocorrelation times : (solid line),

(dashed line) and (dotted line).

The formula (43) applies to any correlation

matrix but in the general case one has to use a numerical

procedure to calculate from it the density function.

Let us stop here the presentation of results for

the ensemble of real matrices. As we

mentioned all results in the large limit hold also in

the ensemble of complex matrices if the covariance matrices

(5) are replaced by (7). The reason why it is

so is related to the fact that

the moments of

in the ensemble of complex matrices (6)

are equal to

the moments of

in the real ensemble (1) up to a corrections

which disappear in the large limit:

(57)

Let us illustrate this by explicit calculations

of the second moment. Using the Wick’s theorem for Gaussian

integrals and the equation (4) for the two-point correlation

function, we have:

The corresponding calculations

for the complex ensemble read:

The difference between the two calculations appears in

the third term which in the real ensemble gives a contribution

of the order while in the complex ensemble disappears by virtue

of (9). We recognize that

which are the leading terms in the expansion are identical as in the

second equation in the set (34). Generally one can show

that the leading contributions which correspond to the planar

diagrams in the expansion of are identical for both

ensembles. Non-planar diagrams are different but they contribute

in the subleading orders: it turns out that in the diagrammatic

expansion of the Green’s function for the complex matrix

ensemble (6), which would be a counterpart of

(58) in the appendix, all diagrams which contain

a double arc with dashed and solid line crossed

are identically equal zero since such an

arc corresponds to the propagator

or

.

A crossing of two arcs is however allowed and leads

to a factor .

To summarize: in the paper we have considered an Wishart ensemble of

correlated random matrices.

We have obtained in the limit of large matrices a closed set of equations

relating the Green’s function or equivalently the moments’

generating functions and for statistically

dressed correlations to the generating functions for genuine

correlation matrices and . The equations in

the large limit are the same for the ensemble of real and complex matrices.

Using these equations we can write down exact relations between genuine and

experimental spectral moments of correlation functions of an arbitrary

order. The relations can be used in practical problems to learn about

correlations in the studied system from the experimental samples.

In the case of exponential correlations we have also found an explicit

form the spectral density function of the covariance matrix.

A natural generalization of the work presented here is to consider

a more general type of time correlations than purely

exponential (36). If the correlations are of the form which

depends on the time difference

and if they are short-ranged

then one can apply Fourier transform to determine

in the large limit an approximate spectrum of the matrix

and approximate values of its spectral moments. Another interesting

issue which can be addressed in the future is the determination of the

probability distribution for individual elements of the covariance

matrices and similarly as it was done for the

uncorrelated case jn .

Acknowledgments

We thank R. Janik, A. Jarosz and M.A. Nowak for discussions.

This work was partially supported by

the Polish State Committee for

Scientific Research (KBN) grants

2P03B 09622 (2002-2004) and 2P03B-08225 (2003-2006),

and by EU IST Center of Excellence ”COPIRA”.

Appendix 1

For completeness we recall here the graphical

representation of the Green’s function. The details

of the diagrammatic method can be found in fz ; sm3 ; bgjj .

The Green’s function can be represented as

a sum over diagramms:

where the -type and -type indices of are denoted

by filled and empty circles, respectively.

The matrix is denoted by an ordered pair of neighbouring

filled and empty circles, while is drawn as an pair

of such circles in the reverse order.

A horizontal solid line stands for , a dashed line for

, a solid arc for and a dashed arc for .

The two point function (4) is drawn as a double arc.

Matrices on a line are multiplied in the order of appearance on

this line. If a line is closed, the trace is taken.

In the thermodynamical limit only planar diagrams give

contribution to . In particular the last term in

(58) vanishes. The Green’s function

is represented by an identical set of diagrams with dashed

and solid lines exchanged. It is convenient to introduce

one-line irreducible diagrams and corresponding generating

functions and . The

Green’s functions can be expressed in terms of

and as follows:

In the planar limit there are two additional equations

which relate the sums over one-line irreducible diagrams to

the Green’s functions:

(61)

Analogous diagrammatic equations can be written

for with the only difference that the solid

line shall denote the propagator and the dashed line

.

Appendix 2

We use the equations (33) and (25)

to determine the relations (34).

As for the case we shall do this using expansion.

The function is given by the series:

(62)

Let us determine the expansion

for the inverse function

as a series around zero:

(63)

The coefficients of the series can be directly calculated

from the condition:

(7) S. Maslov, Y.C. Zhang Phys. Rev. Lett. 87 248701 (2001).

(8) L. Laloux, P. Cizeaux, J.-P. Bouchaud and M. Potters, Phys. Rev.

Lett. 83 1467 (1999).

(9) V. Plerou, et al., Phys. Rev. Lett. 83 1471 (1999).

(10) Z. Burda and J. Jurkiewicz, cond-mat/0312496,

to appear in Physica A.

(11) S.H. Simon, A.L. Moustakas, math-ph/0401038.

(12) Because of the multiplicative nature of

the price changes instead of the changes:

themselves,

in the financial analysis one rather uses

returns as random variables.

(13) J. Feinberg, A. Zee, Jour. Stat. Phys.87 473 (1997).