,

A logistic map approach to economic cycles

I. The best adapted companies

Abstract

A birth-death lattice gas model about the influence of an environment on the fitness and concentration evolution of economic entities is analytically examined. The model can be mapped onto a high order logistic map. The control parameter is a (scalar) ”business plan”. Conditions are searched for growth and decay processes, stable states, upper and lower bounds, bifurcations, periodic and chaotic solutions. The evolution equation of the economic population for the best fitted companies indicates ”microscopic conditions” for cycling. The evolution of a dynamic exponent is shown as a function of the business plan parameters.

keywords:

non-equilibrium, birth-death process, external fieldPACS:

05.45.-a, 05.45.Ra, 89.65.-s, 89.65.Gh1 Introduction

Economic cycles (EC) (see ) have been noticed ca. 1930 [1, 2]. They have received some political economy foundation [3, 4, 5, 6, 7, 8], and are often said to be due to time delayed competition between ”macroscopic variables”, investment, production, profit, credit conditions, … basically controlled by the interest rate [7, 8, 9]. EC have not always been well described or defined [10, 11, 12]. Cycles are sometimes confused with oscillations, or even noise, in economic data. The measurement of the ”period” of a cycle is even far from what would be expected in standard physical measurements.

Economists admit that EC periods are ill defined [10, 11, 12] and do depend on what goods, assets, … are considered. Following averaging procedures one can consider some constancy (3-4 years) in some EC like from the 1994 NBER table. Sometimes not constant periods are said to be the rule, and their values checked for according to various data analysis techniques [13, 14].

EC have recently received some renewed attention in the econophysics community [15, 16, 17, 18]. One approach that can be thought of is through the stochastic resonance phenomenology in which noise and (or) shocks might lead and/or induced a stability state, or some dissipative structure [19], smoothly evolving [20], - an oscillating trend. A modern econophysics approach would also bear upon self-organization [21, 22], a notion already thought of by economists [23].

Many analytical and simulation approaches are based on the Kaldor – Kalecki model [1, 2] or generalizations like in [5, 24]. With as many parameters one can write coupled Langevin equations for fluxes or rates [25]. The main difficulties rests in measuring the coupling parameters.

A simulation with cellular automata or neural networks might lead to a description of EC, but there are many caveat in these approaches since they also contain parameters or black boxes which are either ad hoc ingredients or simply far from so called ”first principles”.

Another modern approach implies a microscopic-like description for such a macroeconomic problem. This can be at departure from usual continuous time evolution equations but the less so if some algorithm is analytically rewritten as here below.

Our analysis stems from a numerically analyzed model [26] considering the evolution of a set of entities (agents or companies) under changing economic, or more generally environmental, conditions. A question raised was in fact whether the system can have bifurcation points. The model is a lattice gas in which mobile entities are described by a scalar variable degree of freedom, itself compared to what is called a field [26], - controlling the most probable state of the system. The degree of freedom evolution depends also on the environment of the entity. The economic evolution of the entities is imposed to have a Lamarckian feature as often admitted in economy circles [27]. A Verhulst attrition-like term is inserted through the company business plan which serves for outlining the birth-death process. A statistical physics approach based on the logistic map seems thus suitable for describing so called economic-like cycles. A posteriori one might wonder why it has not been used, since the logistic map ingredients, in the original Verhulst work, stems indeed from socioeconomic considerations [28]. Recall that a pedagogical example of a logistic map application is the interest rate effect on savings account [28]. It will be found that such ”microscopic” ingredients lead to stable states, bifurcations, periodic and chaotic (turbulent-like) regimes. Therefore it is pointed out that so called EC belong to a class of self-organized systems and may have simply controllable features. Quite importantly it seems that the macroscopic ingredients of usual EC theories can be replaced by more microscopic inputs. We are of course aware of the present simplicity of the model. EC are not due to a birth and death process only.

2 ACP model

Let us precise the basic ingredients of the model [26], as used here. A set of entities (called ”companies”) is originally placed at random on a (square symmetry) lattice. Each company is characterized by a real, scalar degree of freedom . This parameter denotes how well a company is adapted to the economic environment, itself characterized by a (real) field . The system is e.g. described by the concentration of companies, . The concentration is defined in a usual way , where is the number of companies on the lattice at time and is the volume (the number of sites on the lattice) of the system. The time is discrete and counted in Monte Carlo steps (MCS). The companies may diffuse one lattice spacing at a time. Although in the original model [26] the field was space and time dependent, it will be taken constant in space and time here. Unlike in [26], where the system was described by the position and state of each individual company, within this paper, the system is described through a distribution function – the number of companies characterized by at time . In this case the total number of firms existing in the environment at time is given by:

| (1) |

In one MCS a number of companies equal to that at the beginning of the step is picked at random and possibly displaced by one lattice site. After each move the following changes are allowed, if possible:

-

1.

The company may disappear due to ”difficult economic conditions” as measured by ; the probability of surviving is

(2) where is a positive parameter describing the ”selection pressure”. This means that the largest survival probability is when the enterprise satisfies the condition: ; it is a best adapted company;

-

2.

companies may merge. If company has a nearest neighbor , either with a probability both form a new company on site while disappears with

(3) where is a random number, ;

-

3.

or with a probability , companies survive and create one (or two) new firm(s), depending on the available space in the Moore neighborhood of the –company, each with a specific random .

3 Mean field approximation

Averaging over a MCS such that

taking into account the modification in the state distribution caused by (ii), i.e. and considering all possible events in a mean field sense the evolution equation of the system can be written as the sum of two terms,

| (4) |

where (dropping the index in ) :

| (6) |

and

| (7) |

Eq.(4) can be iterated back until the initial point

| (8) |

where each coefficient is the sum of time oriented products of and , i.e.

| (9) |

where and denotes all possible permutations of the set .

4 Logistic map

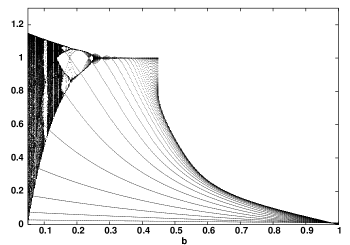

The evolution equation for the total number of the best adapted companies has the form of a logistic map [28, 29], with a control parameter . Therefore the model may reveal some periodic or chaotic behavior. The best adapted company concentration evolution, starting from a small initial value, is shown at fixed ’s in Fig. 1 for different values.

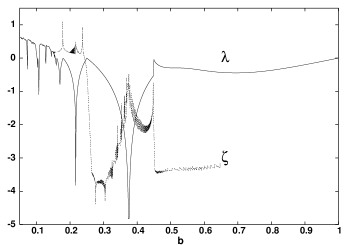

The corresponding Lyapunov exponent is shown in (Fig. 2). Five main regions can be distinguished in Fig. 2. Only one stable solution (with ) exists for , i.e. due to the frequent merging process, there is no overpopulation of the system. The stable state is achieved as a dynamic equilibrium between merging and spin-off creation process. For other values some ”convergence” is found toward one or several states characterized by bifurcations and limit cycles with various periodicity down to , where a chaotic region appears containing narrow stability windows.

In order to better understand the dynamics we calculated

-

1.

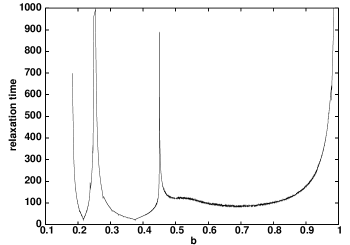

the time needed before a stable orbit (state) is reached, Fig. 3, and

-

2.

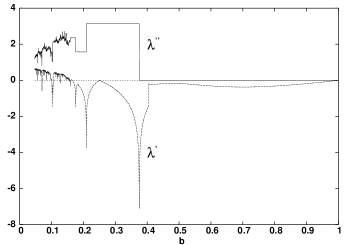

a variant of the Lyapunov exponent in order to emphasize both the convergence (or divergence) of the trajectory, a possible oscillatory behavior, through the so called real () and imaginary () part of a ”generalized” in conventional notations, but without absolute values before taking the logarithm, Fig. 4.

For the time required for the system to attain the stable state remains (approximately) on the same level until . However for the time required for the system to reach the stable state increases rapidly (Fig. 3). This corresponds to the behavior of the Lyapunov exponent (Fig. 2), which is for . Especially interesting is the range : damping properties are superposed to an oscillating behavior. Oscillations are also visible in Fig. 4, where the finite imaginary part of shows that the system may cycle. Notice the value of equal to , , ,… in various stability regions, but taking bizarre values in chaotic regions. This is another way to find characteristics of stability windows in the ”turbulent regimes”.

The process of achieving a stable state has been also studied by assuming a power law decay for the -distance evolution in the form . The plot of the exponent as a function of is shown in Fig. 2.

5 Conclusions

The above results, for a simple model, lead toward interesting conclusions concerning stable or not economic states. We do not - of course claim that EC are due to a merging – spin off microscopic process only. What is intended is to search whether a discrete microscopic model has some interesting ingredients for some macroeconomic evolution. The evolution of the model depends on the three microscopic-like parameters the environmental condition , the selection pressure and the merging probability having a physical sense in contrast to macroscopic (economic) ones . The influence of the environment and the selection pressure control the time required for the system to achieve a stable state. Moreover the environmental condition decides also on the type of companies surviving in the system. The first parameter is essentially of political and/or global origin. The second can be taken as the inverse of temperature in thermodynamics, and leads as in other non equilibrium systems to consider an intrinsic noise controlling the existence of dissipative structures [19, 28]. If the selection pressure is ”strong” then the ”weak” companies are removed from the system and the distribution function converges to the ”best adapted companies” case . This is also similar to results found in Darwinian-like economic evolutions [30, 31]. The last parameter is more subtle, and concerns business plans: it controls the asymptotic concentration value of companies and the cyclic or chaotic behavior of the system. We have constrained to be a constant though a dynamic economic policy usually requests a time dependent .

Concentrating on the best adapted companies for small the system reveals chaotic properties, i.e. . It means that at low merging the system becomes unstable. This is an apparently new interesting feature which seems reasonable but nevertheless requests economic studies and considerations. The system is especially stable at where the damping parameter attains its largest value. In such a case, the system has only one stable solution, which is achieved in the shortest possible time. Therefore a merging philosophy, or politics, is a stabilization factor for economic systems. , it should leads to a monopolistic situation which is stable and ”cycling” as long as the goods of such a company are needed, - if there is no spin-off process.

Finally, the above numbers and findings should truly be taken with caution since they pertain to a model studied on a 2D lattice with a given symmetry. The period of cycles depends on the economic plan parameter , but also on the Moore neighborhood hereby chosen for the evolution and the information flow between companies. A posteriori it is understood why ”EC periods”, either global or for specific activity fields, are poorly defined [3, 4, 12]. Interestingly it appears again that the connectivity of the ”lattice” on which an economic process takes place is markedly relevant for defining economic oscillations. This has already been noticed in the case of financial crashes [22, 32]. Whence some EC appear to be self-organized systems and have simply controlled (and controllable) features, similar to turbulent processes.

6 Acknowledgments

This work is partially financially supported by FNRS convention FRFC 2.4590.01. J. M. would like also to thank GRASP for the welcome and hospitality.

References

- [1] N. Kaldor, A Model of the Trade Cycle, Econ. J. 50 (1940) 78.

- [2] M. Kalecki, A Macrodynamic Theory of the Business Cycle, Econometrica 3 (1935) 327; M. Kalecki, A Theory of the Business Cycle, Rev. Econ. Studies 4 (1937) 77; M. Kalecki, Theory of Economic Dynamics: An essay on cyclical and long-run changes in capitalist economy, (Monthly Review Press, New York, 1965).

- [3] J.B. Long and C.I. Plosser, Real Business Cycles, J. Polit. Econ. 91 (1983) 39

- [4] S. Basu and A.M. Taylor, Business cycles in international historical perspective, J. Econom. Perspect. 13 (1999) 45

- [5] P. Temin , The Causes of American Business Cycles: An Essay in Economic Historiography, (NBER, New York, 1998)

- [6] M.C. Guisan, E. Aguayo, Economic Growth and Cycles in Latin American Countries in 20th Century, Review on Economic Cycles 4 (2002)

- [7] J.S. Duesenberry, Business Cycles and Economic Growth, (McGraw-Hill, New York, 1958); V. Zarnowitz, Business Cycles: Theory, History, Indicators, and Forecasting, (U. Chicago Press, Chicago, 1992)

- [8] G. Gabisch and H.W. Lorenz, Business Cycle Theory: A survey of methods and concepts, (Springer-Verlag, Berlin, 1989)

- [9] D. Guha, L. Hiris, The Aggregate Credit Spread and the Business Cycle, Int. Rev. Fin. Anal. 11 (2002) 219

- [10] A. Krawiec and M. Szydlowski, The Kaldor-Kalecki Model of Business Cycle, J. Nonlin. Math. Phys. 8 (2001) 266

- [11] C.D. Romer, Remeasuring Business Cycles, J. Econo. Hist., 54 (1994) 573

- [12] A.M. Burns, W.C. Mitchell, Measuring Business Cycles, (NBER, New York, 1946)

- [13] F. Portillo Pérez de Viñaspre, P.A. Pérez Pascual, Harmonic Analysis: The Application of ’Theoretical Cycles’ to the Economic Analysis, Review on Economic Cycles 1 (2001)

- [14] D. J. Pedregal, Analysis of Economic Cycles Using Unobserved Components Models, Review on Economic Cycles 2 (2001) 77

- [15] M. Aoki, Asymmetrical Cycles and Equilibrium Selection in Finitary Evolutionary Economic Models, in Cycles, Growth, and Structural Changes, L. Punzo Ed., (Routledge, London, 2001) Ch. 8 ; ibid.,A simple model of asymmetrical business cycles: Interactive dynamics of a large number of agents with discrete choices, Macroeconomic Dynamics 2 (1998) 427; ibid., Stochastic Views on Diamond Search Model: Asymmetrical Cycles and Fluctuations, Macroeconomic Dynamics 4 (2000) 487

- [16] X. Gabaix, Power laws and the origins of the business cycle, at

- [17] R. Weron, Energy price risk management, Physica A 285 (2000) 127

- [18] P. Ormerod, C. Mounfield, Power law distribution of duration and magnitude of recessions in capitalist economies: breakdown of scaling, Physica A 293 (2001) 573

- [19] P. Glansdorff and I. Prigogine, Structure, Stabilité et Fluctuations, (Masson, Paris, 1971)

- [20] C. Nicolis and G. Nicolis, Passage through a barrier with a slowly increasing control parameter, Phys. Rev. E 62 (2000) 197

- [21] P. Bak, How Nature Works: the Science of Self-organized Criticality, (Oxford University Press, Oxford, 1997).

- [22] D. Sornette, Chaos, Fractals, Self-organization and Disorder: Concepts & Tools (Springer, Heidelberg, 2000).

- [23] J. Foster, Competitive selection, self-organization and Joseph A. Schumpeter, J. Evol. Economics 10 (2000) 311

- [24] D. M. Dubois, Extension of the Kaldor-Kalecki model of business cycle with a computational anticipated capital stock, International Journal of Organisational Transformation and Social Change, 1 (2003) 63

- [25] J. Solvay, M. Sanglier, P. Brenton, Modeling the Growth of Corporations: Applications for Managerial Techniques and Portfolio Analysis, (Palgrave, New York, 2001)

- [26] M. Ausloos, P. Clippe, and A. Pȩkalski, Simple model for the dynamics of correlation in the evolution of economic entities under varying economic conditions, Physica A 324 (2003) 330

- [27] E.L. Khalil, Beyond natural selection and divine intervention: The Lamarckian implication of Adam Smith’s invisible hand, J. Evol. Economics 10 (2000) 373

- [28] H.G. Schuster, Deterministic Chaos, (Physik-Verlag, Weinheim, 1984)

-

[29]

M. Feigenbaum, The Universal Metric Properties of Nonlinear

Transformations, J. Stat. Phys. 21 (1979) 69 - [30] K. Yamasaki, K. Kitakaze and M. Sekiguchi, Evolutionary Adaptation Method against Dynamic Environments Considering Characteristics of Changes and Similarities to Multi-objective Optimization, IPSJ JOURNAL 44 No.03-048 (2003).

- [31] G.M. Hodgson, Darwinism in economics: from analogy to ontology, J. Evol. Economics 12 (2002) 259

- [32] M. Ausloos, K. Ivanova and N. Vandewalle, Crashes: symptoms, diagnoses and remedies, in Empirical sciences of financial fluctuations. The advent of econophysics, H. Takayasu, Ed. (Springer Verlag, Berlin, 2002) pp. 62