Can One Make Any Crash Prediction in Finance Using the Local Hurst Exponent Idea?

Abstract

We apply the Hurst exponent idea for investigation of DJIA index time-series data. The behavior of the local Hurst exponent prior to drastic changes in financial series signal is analyzed. The optimal length of the time-window over which this exponent can be calculated in order to make some meaningful predictions is discussed. Our prediction hypothesis is verified with examples of ’29 and ’87 crashes, as well as with more recent phenomena in stock market from the period 1995-2003. Some interesting agreements are found.

1 Introduction

Financial markets are nonlinear, complex and open dynamical

systems described by enormous number of free, mostly unknown

parameters. Many of these parameters are exterior for the market,

what makes the full description of the system even more

complicated. Exterior parameters are completely out of control by

investors who are the part of financial system. These parameters

have usually random origin connected with e.g. political

disturbances, terrorist attacks, bankruptcies of leading

companies, wars, etc. There are also investor dependent interior

parameters driving the market even in the absence of other, not

expected exterior phenomena. The full recognition of such interior

parameters

is a big challenge for economists and econophysicists.

All these circumstances mean that detailed time evolution of a

complex financial system is unpredicted. However is the situation

so hopeless? Even if we can not predict the detailed evolution

scenario, we might be able to say something else about the system.

We have learned from statistical mechanics that one does not have

to know where a particular particle of the mechanical system will

be a second or few from now, in order to find equation of state of

this system. The latter is quite sufficient in practical

applications giving us the whole available information about the

macroscopic parameters, like e.g. pressure or temperature, and it

reflects all detailed microscopic, directly inaccessible

information. In many cases this knowledge is sufficient to

indicate direction in which the system is

evolving.

In this article we rise the question if it is possible to find

some macroscopic parameters in financial market which would play

the role of a macroscopic indicator of complex, interior stock

dynamics. In particular, we would like this parameter to be able

to predict that crashes or other drastic changes in the market

signal are coming soon. The task looks hopeless if one assumes

following Fama [1] that investors destroy information while using

it, so that others can not use this information again. In this

spirit market should not exhibit any correlations between returns

at time and at time , where

| (1) |

and is the price of a given stock at time .

It was widely believed for a long time that price changes follow

an independent, zero mean, Gaussian process. However, deviations

from this simple scenario have been observed in the financial

signal in the last few years. Empirical work showed that the

distribution function has tails obeying power law

relation [2-4], contrary to normal

Gaussian distribution. Also the autocorrelation function of the

absolute value of price changes shows long-range persistence

, with [5-7]. A sort of long memory correlations in

financial signal itself has also been revealed [8-12].

Due to large liquidity of currency exchange markets, they seem to

be a natural subject to explore the existence of such correlations

between returns. This has been done for major world and European

currencies in [13-15]. It has also been proven that complexity of

a financial market is not limited to the statistical behavior of

each financial time series forming it but follows from the statics

and dynamics of correlations existing between various stocks in the market [16].

The proven existence of correlations in financial time series

reveals the possibility to apply some global macroscopic approach

to see them. In this paper we address the possibility of searching

for correlations between subsequent returns in financial series

with the use of Detrended Fluctuation Analysis (DFA)[17], applied

for the first time in finances in [18-20]. Our philosophy is

described below.

2 The Search for the Market State with the Use of Local Hurst Exponent

It is well known that the Hurst -exponent [21,22],

extracted from the time series according to DFA method, measures

the level of persistency in the given signal. The value implies the existence of long-range correlations and

corresponds to so called fractional Brownian motion [23]. In

particular, for there is persistence, and for

’antipersistence’ in the series signal. We expect

that dramatic changes in financial signal should be preceded by

excitation state of the market (nervousness), what in turn is

reflected by the shape of subsequent daily changes in the signal.

These changes should become less correlated just before the

dramatic breakdown in the signal trend. Contrary, when the trend

in the market is strong and well determined, an increasing

(decreasing) value of market index in immediate past makes also an

increasing (decreasing) signal in the immediate future more

probable [24]. In other words, one should observe some long-range

correlations in returns and consequently higher values

for strong, long lasting trends (increasing or decreasing ones),

and significant drop in -exponent value if the trend is

going

to change dramatically its direction in very near future.

To check this hypothesis we used DFA technique, rather than other

available methods like spectral analysis or rescaled range

analysis, to extract -exponent. This is because DFA method

avoids detection of long-range correlations being an artefact of

nonstationarity of time series [25]. Then some applications were

performed for

Dow Jones Industrial Average (DJIA) daily closure signal.

For completeness let us briefly remind the main steps of DFA

analysis:

-

1.

The time series of random one variable sequence of length is divided into non-overlapping boxes of equal size . The time variable is discrete and evolves by a single unit between () and . Thus each box contains points and is integer.

-

2.

The linear approximation of the trend in each -size box is found as , with some box dependent constants.

-

3.

In each -size box one defines the ’detrended walk’ as the difference between the original series and the local trend .

-

4.

One calculates the variance about the detrended walk for each box:

(2) and the average of these variances over all boxes of size :

(3) -

5.

A power law behavior is expected:

(4) from which -exponent can be extracted from log-log linear fit.

If one wants to use -exponent to measure the strength of

local correlations in financial time series, one has to use the

local -exponent idea [17, 18]. For a given trading

day , the corresponding -exponent value will be

calculated according to Eq.(4) in the period of length , called an observation box or

time-window. In order to cover the whole time-window length

with -size boxes, we put the last box contributing to Eq.

(3) in the period , where means the integer part. This box partly

overlaps the preceding one but such overlapping does not modify

the local . Moving the time-window every one session, one

is able to reproduce the history of changes in time. Let

us notice that only the past signal of financial series, not

earlier than sessions before a given

trading day , contributes to local value.

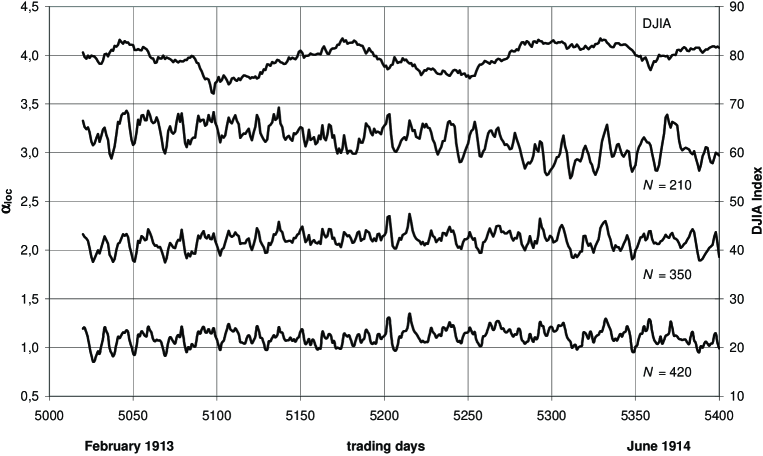

It is not surprising that local -exponent at given moment

depends on the time-window length . It is seen in Fig.1

where we present the example of local -exponent plots for

chosen trading day period of DJIA daily closure values.

Three different choices: , and have been

here made to calculate local . One may notice that plots

for and coincides very well with each other, while

plot shows already some deviations from other two. It

exhibits slightly higher local values in the first half

of discussed period than in the second half. The question arises,

whether this is a real effect outside the statistical

uncertainties range and what the optimal

time-window length should be chosen for further discussion.

The choice of seems to be a matter of intuition, statistics

and economic regards. If is too large, -exponent loses

its locality and may not ’see’ correlations whose characteristic

range, say , is much smaller than the window length

(). This is the main reason why evolution

becomes more smooth if increases. On the other hand, it has

been proven that standard deviation in the local

value, caused by finite-size time-series effects on

long-range correlation, is of order [26]:

| (5) |

Thus, we are stuck with huge statistical

uncertainty with decreasing , what efficiently destroys all predictions.

One has to find then a golden point (golden area) where two above

requirements meet together, i.e. where is

sufficiently small, and is not too large. For economic reason

we suggest that should not exceed one trading year ()

in the case of financial series with daily closure signal. This is

to avoid probable seasonal periodicity in supply and demand in the

market, what would introduce artificial contributions to

investigated correlations. Besides, in our opinion, loses

a sens

of the local value for . In order to stay within the scaling

range of Eq. (4) we used the box size .

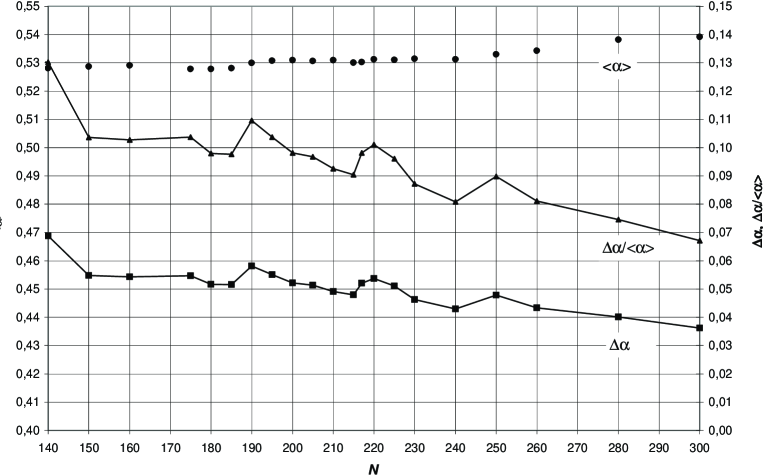

To find the optimal we investigated how far the standard

deviation changes with for . This

has been done for different subseries of DJIA signal, taking

samples for each value of . The results are collected in Fig.

2, where is displayed together with the

respective percentage uncertainty . As one would expect from Eq. (5),

slowly decreases on the average with , but

some departs from this rule are observed. The first local minimum

below appears at . Although this minimum is not

strong, we decided to make further estimations of local

for DJIA series using this particular time-window length. Our

choice corresponds to about ten months trading period. It is worth

to observe that the obtained statistical uncertainty

agrees well with that calculated in [18] for a monetary market. We

have also checked that, for , there exists a substantial

drop of linear regression correlation coefficient , what

additionally justifies our choice. Finally, we found that the

local value is not sensitive to changes in not

exceeding , so that any choice

reproduces qualitatively and quantitatively very similar results.

3 DJIA Signal Tested with DFA Method - Applications

Now we proceed to analyze the local value of -exponent

estimated with the DFA technique for daily closure DJIA signal.

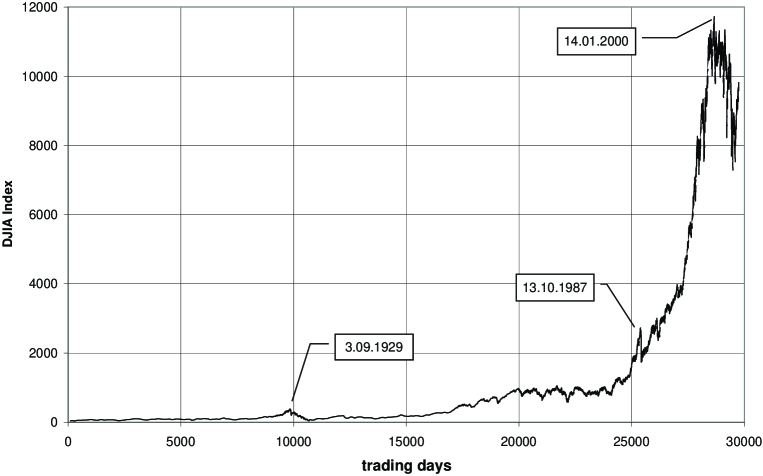

The whole history of this signal is collected in Fig.3. We have

focused attention on the most important events in the market

history. These are: crashes in September 1929, October 1987, July

1998, and the current situation in last three years. All data were taken from [27].

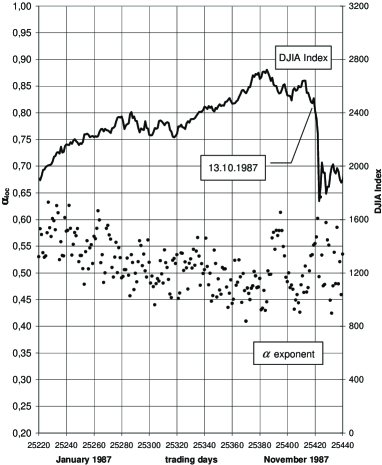

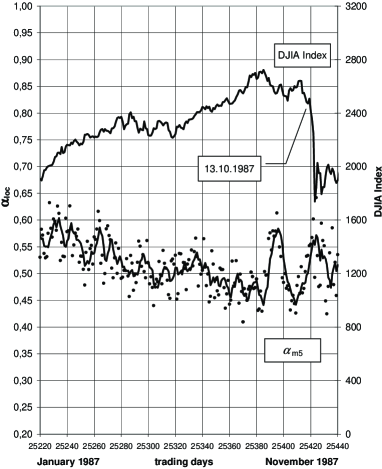

First let us consider the ’29 crash shown in details in Fig.4. The

DJIA signal had been in clear increasing mode for about months

- from session up to the session

(3.09.1929) when the trend in market index changed its direction.

The crash took place 40 days later. The detailed

-exponent structure of this period is shown in Fig.4a,

where dots denote respective local values calculated

session by session from the last index values. To see more

effectively the evolution of local , the moving average

value of -exponent taken from five last

sessions (one trading week) has been drawn in Fig.4b. A very clear

decreasing trend in local is visible. It had started

about one month before the DJIA index reached its maximal value on

3.09.1929, but did not terminate with this date. Small corrections

in local around the session can be

explained as a result of change in DJIA index trend at that time.

The -exponent has reached a deep and clearly seen local

minimum two weeks before the crash, contrary to

very high value from which it started several

months earlier. The statistical uncertainty in the difference

between initial () and final () values is at

most - twice smaller than the respective change . Hence, statistics is unable to

explain this particular trend-like pattern in -exponent

values.

To see if it was a chance, we checked two other major crashes in

American market in 1987 and 1998. The scenario found for them is

revealed in Fig.5 and Fig.6. The ’87 crash has also clear

decreasing trend in local for the whole one year period

preceding the crash point (see details in Fig.5). At the same

time, DJIA signal constantly rises. These two contradicting trends

suggest that investors were becoming gradually more sceptic about

the market future at that time, despite the market index has been

rising.

The local had started to reach the value below

since the session . Soon after, the DJIA index also

changed drastically its trend on 25.08.87 (session ). A comparison of increase later on, with

simultaneous drop in DJIA signal between sessions

and , can be read as the confirmation of decreasing

trend in the market. It is worth to observe that the local

gains again even deeper minimum just

before the October crash. This minimum reveals again that the

market is very ’nervous’ and that the increase of DJIA index,

initiated by session , is only a small correction

before the forthcoming crash. The percentage drop

between maximal and minimal value in the trend is about the same as in ’29 crash.

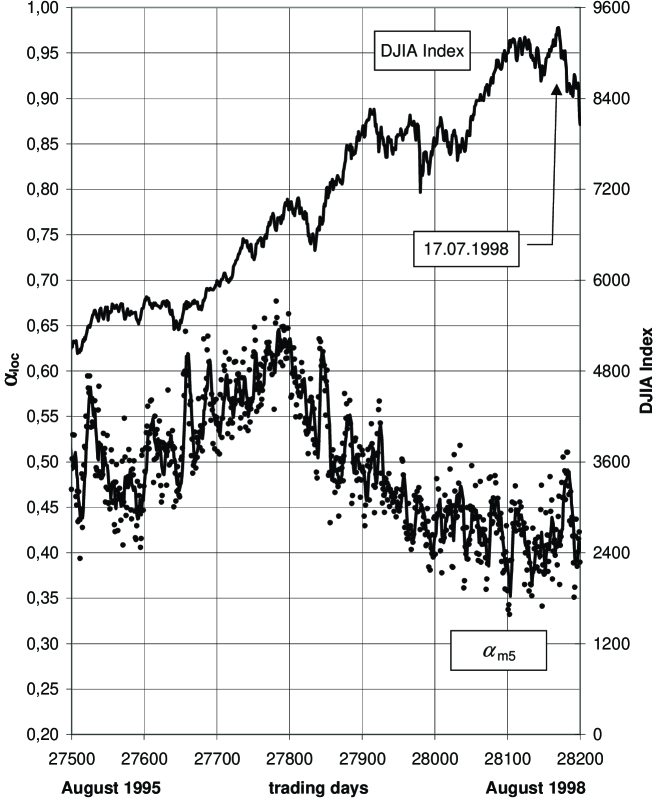

The same phenomena occurs for ’98 crash if we make its ’X-ray’

with the use of local -exponent as seen in Fig.6. The

market is much more nervous at that time (the DJIA index plot is

jagged much more than ever before). This leads to much smaller

values gained by in its decreasing trend before

the crash.

In this particular case it is interesting to see what happened

next, i.e. after July 1998. The DJIA index run in the period

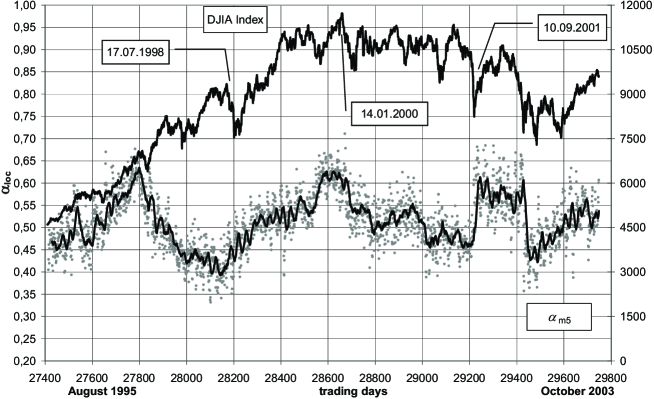

1995-2003 is displayed in Fig.7. We notice that just after the ’98

crash, market entered into globally increasing, but very nervous

trend lasting up to January 2000. The -exponent increases

in this period, however, it probably gets many noise signals

coming from the frequently changing DJIA index value within

time-window length from the immediate past. In other words

the correlation range is too short with respect to and

-exponent loses its sensitivity to detect them. Therefore

the prediction of market signal evolution with the use of local

-exponent becomes difficult in the period 1995-2003.

4 Conclusions

We think that the careful analysis of local -exponent

signal may significantly help to determine in which mode (strong

increasing, decreasing or unpredicted one) a market is at given

moment. As we have shown, the collected data suggest that very

clear trends can be distinguished not only for the financial

series signal but also for the local Hurst exponent. In

particular, we tested that value drops significantly

before any crash in the DJIA signal is going to happen. This

confirms that local Hurst exponent may be used as a measure of

actual excitation state of the market. However, one has to

remember that strong, exterior phenomena not controlled by

investors are able to decelerate or accelerate predicted process,

drastically change its depth, or even its direction. Such sudden

exterior phenomena

can not, of course, be predicted by the local behavior.

The best results in prediction of forthcoming drastic changes in

the market seem to be obtained if ’quiet’ situation exists within

considered time-window length, i.e. if one has clear long-lasting

trends in market index before the crash. This situation took place

in 1929, 1987 and 1998. Otherwise, the -exponent contains

artifacts from the rapidly changing market index within

time-window over which it is calculated. In the latter case

predictions are troublesome.

We have checked that the above analysis, based on the local

-exponent, works well also for other market indices, like

the Warsaw Stock Exchange Index (WIG 20) [28], however different

time-window length should be used in that case. We believe that

observation and analysis of local Hurst exponent may play a

significant role as an additional hint for market investors, apart

from other technical indicators like moving average or momentum.

It could be a novel part of the classical technical analysis in

finances.

Acknowledgements

One of the autor (D.G) would like to thank M. Ausloos for helpful comments and discussion while this article was in preparation.

References

- [1] E.F. Fama, J. Finance 25, 383 (1970).

- [2] T. Lux, Appl. Financial Econom. 6 (1996) 463-475.

- [3] V. Plerou, P. Gopikrishnau, L.A.N. Amaral, M. Meyer, H.E. Stanley, Phys. Rev. E 60 (1999) 6519-6529.

- [4] U.A. Muller, M.M. Dacorogna, O.V. Pictet in: R.J. Adler, R.E. Feldman, M.S. Taqqu (Eds.), A Practical Guide to Heavy Tails, Birkha̋user, Basel, 1998, pp. 83-311.

- [5] C.W.J. Granger, Z. Ding, J. Econometrics 73 (1996) 61.

- [6] Y. Liu, R. Gopikrishnan, P. Cizeau, M. Meyer, C.-K. Peng, H.E. Stanley, Phys. Rev. E 60 (1999) 1390-1400.

- [7] M. Lundin, M.M. Dacorogna, U.A. Muller, Financial Markets Tick by Tick, Wiley, New York, 1999, p.91.

- [8] Z. Ding, C.W.J. Granger, R.F. Engle, J. Emp. Finance 1, 83 (1993).

- [9] R.T. Baillie, T. Bollerslev, J. Int. Money & Finance 13, 565 (1994).

- [10] P. De Lima, N. Crato, Economic Lett. 45, 281‘(1994).

- [11] A. Pagan, J. Emp. Finance 3, (1996) 15.

- [12] R.T. Baillie, J. Econometrics 73, (1996) 5.

- [13] M. Ausloos, K. Ivanova, Int. J. Mod. Phys. C 12, (2001) 169.

- [14] K. Ivanova, M. Ausloos, Eur. Phys. J. B 27, 239-247 (2002).

- [15] R. Baviera, M. Pasquini, M. Serva, D. Vergni, A. Vulpiani, Eur. Phys. J. B 20, 473-479 (2001).

- [16] F. Lillo, R.N. Mantegna, arXiv: cond-mat/0006065.

- [17] C.-K. Peng, S.V. Buldyrev, S. Havlin, M. Simons, H.E. Stanley, A.L. Goldgerger, Phys. Rev. E 49 (1994) 1691-1695.

- [18] N. Vandewalle, M. Ausloos, Physica A 246, (1997) 454-459.

- [19] M. Ausloos, N. Vandewalle, Ph. Boveroux, A. Minguet, K. Ivanova, Physica A 274 (1999) 229-240.

- [20] N. Vandewalle, M. Ausloos, Int. J. Comput. Anticipat. Syst. 1 (1998) 342-349.

- [21] H.E. Stanley, S.V. Buldyrev, A.L. Goldberger, S. Havlin, C.-K. Peng, M. Simmons, Physica A 200 (1996) 4-24.

- [22] S.V. Buldyrev, N.V. Dokholyan, A.L. Goldberger, S. Havlin, C.-K. Peng, H.E. Stanley, G.M. Viswanathan, Physica A 249 (1998) 430-438.

- [23] B.B.Mandelbrot, The Fractal Geometry of Nature, W.H.Freeman, New York, 1982

- [24] M. Ausloos, K. Ivanova, arXiv: cond-mat/0108013.

- [25] H.E. Stanley, L.A.N. Amaral, S.V. Buldyrev, A.L. Goldberger, S. Havlin, H. Leschhorn, P. Maass, H.A. Makse, C.-K. Peng, M.A. Salinger, M.H.R. Stanley, G.M. Viswanathan, Physica A 231 (1996) 20-48.

- [26] C.-K.Peng, S.V.Buldyrev, A.L.Goldberger, S.Havlin, M.Simons, H.E.Stanley, Phys.Rev. E 47 (1993) 3730-3733

- [27] http://www.djindexes.com

- [28] D.Grech, Z.Mazur, unpublished

(a) All local values calculated session after session are marked as dots.

(b) The moving average of last five sessions. The significant drop in between sessions and is striking.

(a) The local evolution calculated as before for .

(b) The moving average line explains how the decreasing trend in is formed.

The decreasing trend in is much deeper () than before. The investors seem to be very enthusiastic till the beginning of 1997 (), but they become pessimistic and nervous just one year later (), despite the DJIA index still grows. The -exponent reaches its deep minimum () in the half of 1998. This is a good moment for crash to appear(!).