Zipf Law in Firms Bankruptcy

Abstract

Using an exhaustive list of Japanese bankruptcy in 1997, we discover a Zipf law for the distribution of total liabilities of bankrupted firms in high debt range. The life-time of these bankrupted firms has exponential distribution in correlation with entry rate of new firms. We also show that the debt and size are highly correlated, so the Zipf law holds consistently with that for size distribution. In attempt to understand “physics” of bankruptcy, we show that a model of debtor-creditor dynamics of firms and a bank, recently proposed by economists, can reproduce these phenomenological findings.

keywords:

Zipf law , firm growth , bankruptcy , balance-sheet , EconophysicsPACS:

89.90.+n , 02.50.-r , 05.40.+j , 47.53.+n1 Introduction

It is a challenging task to model aggregate dynamics of firms in econophysics. As such dynamics for firms with considerable amount of money flow is concerned, one can now have evidence of several phenomenological facts about the dynamics of firms [1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12], which are not only interesting in physics, but also have quite significance in macroeconomics [5, 10].

Among those facts are size distribution and growth of firms. Distribution of firm size such as sales, number of employees, total assets follows a power-law, or Pareto-Zipf law [1, 3, 7, 8, 12]. As for the growth of firms, the distribution of the logarithm of growth rates has an exponential form and that the fluctuations in the growth rates scale with the firm size [2, 3, 4, 6, 7, 9]. While these observation concerns about stock of a firm, no less important is flow such as profits, whose properties of distribution and growth rates have recently observed in empirical works [11, 12].

While these phenomenological facts have been found for living firms, little is known about the death in aggregate dynamics of a large number of firms. That is exactly what the present work concerns about. It is important to uncover phenomenology of how firms die in order to understand the firms growth dynamics.

In section 2, we make observation of Japanese bankruptcy by using an exhaustive list of bankrupted firms in a year. We show phenomenological findings about the distribution of total liabilities or debts when bankrupted, the life-time of bankrupted firms, and correlation between the firm’s debt and size. These are the main results of this paper. In section 3, we describe a firm’s financial activity in terms of balance-sheet dynamics. A model for debtor of firms and creditor of a bank, recently proposed by economists [17], after briefly recapitulated, is shown to be able to reproduce our findings about bankruptcy. Summary and discussion is given in section 4. In appendix, we give description about the nature of bankruptcy dataset employed in this paper.

2 Firms Bankruptcy in Japan

Our data, provided by a domestic data-bank company (Tokyo Shoko Research, Ltd.), is an exhaustive list of Japanese bankrupted firms in 1997. The data is exhaustive in the sense that any bankrupted firm with total amount of debt exceeding 10 million yen (roughly 80,000 euros/dollars) is listed in it. The number of such firms in the year is 16,526. The data contains information of debt, sales, business sector, number of employees, primary bank when bankrupted, dates of establishment and failure, and stockholders fund when established. Two remarks immediately follow.

First, bankruptcy or business failure is not a legal term, but should be understood as a critical financial insolvency of a debtor. Typical case and classification of different types are given in appendix. What is important for our purpose here, however, is that most of the cases in the dataset, whatever the types are, is basically caused by financial insolvency state of the firm. Indeed, out of the total 16,526 cases, the most frequent one is suspension of bank transactions (13,850). This liquidity problem (see appendix for details) is considered as the main cause for other legal and private procedures of bankruptcy.

Second, debt refers to the total sum of liabilities in the credit (“right-hand”) side of balance-sheet. This quantity, when the firm goes bankrupted, is relatively easy to measure in comparison with other balance-sheet quantities such as total asset and equity111Debt here is not net liabilities defined by the total liabilities minus the amount of assets not hypothecated, which is difficult to know.. Since each item in debt has a creditor outside of the firm, so the quantity is not basically hidden inside. Actual measurement of the amount of debt is based either on legal documents or on investigation of current/non-current liabilities in balance-sheet plus the amount of bills discounted and transfers by endorsement, according to legal and private procedure for bankruptcy, respectively.

We used the entire dataset in what follows.

2.1 Distribution of debt

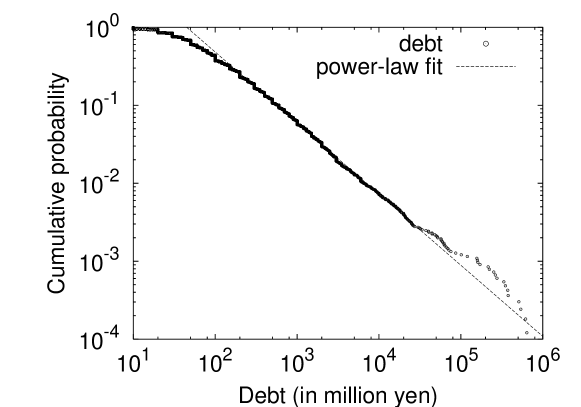

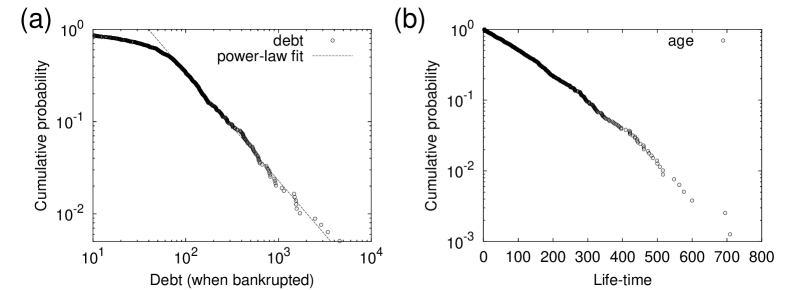

Fig. 1 shows the cumulative probability distribution of debt when the firm was bankrupted. For large debts exceeding yen, we can observe a power-law distribution over three orders of magnitude or even more. The probability that a given bankrupted firm has debt equal to or greater than , denoted by , obeys

| (1) |

with a constant , the so-called Pareto index for bankruptcy. The index was estimated as (by least-square-fit for samples equally spaced in logarithm of rank in the power-law region; error is 90% level). This phenomenological finding is what we call Zipf-law for debt of firms bankrupted. It was pointed out in [13] that debt may obey Zipf-law, but unfortunately with a quite limited number of data (corresponding to the tail more than yen of debt).

2.2 Life-time of bankrupted firms

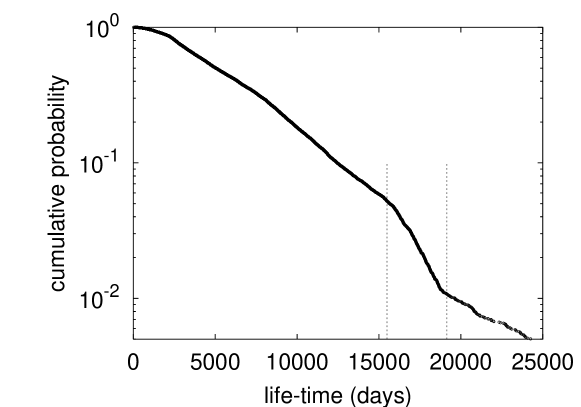

No less interesting than how large a firm can fail is the problem of how long a failed firm lived. Fig. 2 gives the cumulative distribution of life-time , , for the same set of bankrupted firms. With this plot being semi-log, it is observed that the entire distribution follows an exponential distribution. We also see that the distribution has a sudden drop and kink in the shape.

In order to quantify the shape of , let us introduce a function defined by

| (2) |

It is easily seen from the right-hand side expression of eq. (2) that for a sufficiently small time-interval , is the probability that the life-time satisfies under the condition that . This function has a similar notion as hazard rate function in probability (see [15] for example). If is constant , then . has the physical dimension of inverse of time.

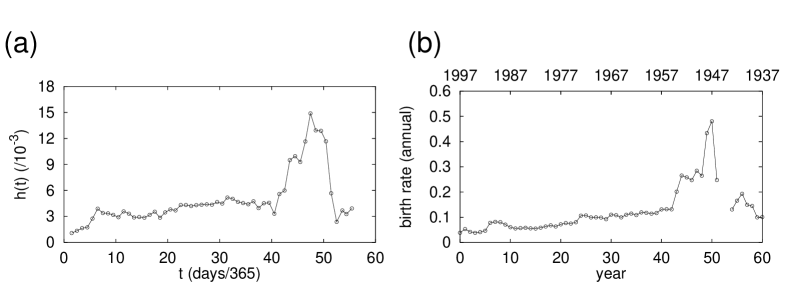

From in Fig. 2, we estimate the derivative in eq. (2) by doing moving-average of stepwise slopes over one year. The resulting is given in Fig. 3 (a). is nearly constant over 30 years, but takes large values for about 10 years right after the World War II. In general, the number of firm years old can be estimated by multiplying the number of firms born years ago by the probability of survival of a firm to an age of years. Therefore, if the process of survival is homogeneous in time, the time-scale in comes from entry rate of new firms. Fig. 3 (b) is the historical record of entry of firms [16]. One can observe that the 10 years period of high corresponds to the period of extremely high birth-rate right after the world war II for about 10 years. This was brought about by the dissolution of zaibatsu (corporate alliances) monopoly under the government by U.S. General Headquarters (from 1945 to 1952). One can also note that has the same order of magnitude as the entry rate of firms by converting time from days to years all over the history.

2.3 Correlation between firm size and debt when bankrupted

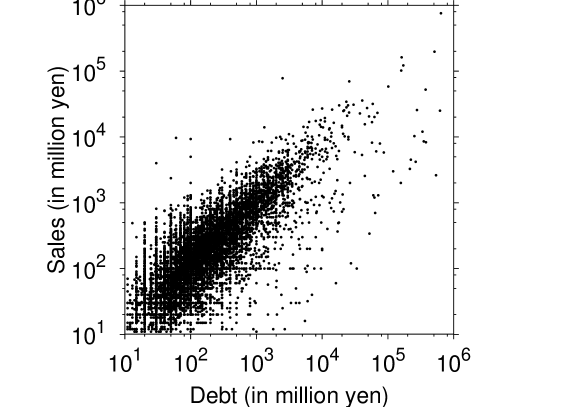

Since it has been known222But see also another paradigm [14]. that firm size follows Zipf law [1, 3, 7, 8, 12], let us take a look at relation between firm size and firm debt right before bankruptcy. Fig. 4 shows a clear correlation between them. Here the firm size is measured by sales right before bankruptcy. The number of employees, as a proxy of firm size, gives similar result as for sales. The bigger a firm is, the larger its debt is when failed.

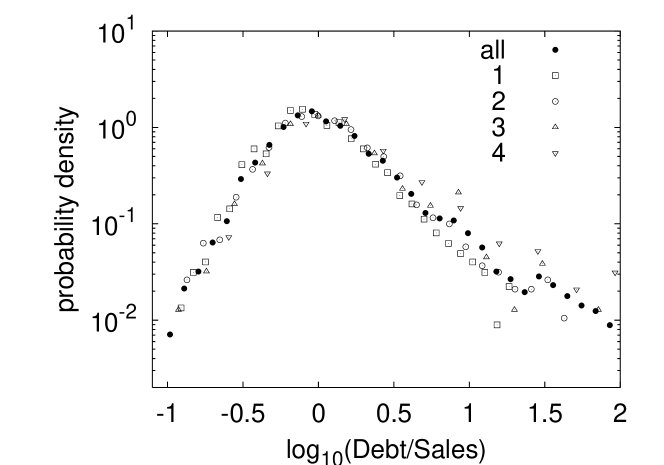

To quantify this relation, denoting sales of a bankrupted firm by , we use the ratio where debt and sales are given in the same units of money. Introduce the logarithm of as , and we examined the probability density of , , in Fig. 5 (filled dots) by using all the data (yen), which corresponds to the Pareto-Zipf range in eq. (1). It is found that the probability density function is exponential distribution with skewness, i.e., with different slopes for and . The side of is fatter than the other side because a positive means that the firm is nearer to the state of insolvency.

Furthermore, we show that the ratio does not depend statistically on which range of debt is being observed. Preparing bins as yen (), we can examine the conditional probability density, , for each bin of . Fig. 5 shows that statistical dependence of the ratio on the value of debt is very weak. This means that the relation between firm size and debt is multiplicative with multiplying factor drawn from the distribution given in Fig. 5. If the statistical independence between and holds over the entire range of the variables, the probability density for is equal to the convolution of the one for and the one for . If has a power-law distribution with a Pareto index, then will have a power-law with the same Pareto index. Though being a non-rigorous argument because of the breakdown of power-law under some threshold and of the statistical independence, this give us a basic idea that the Zipf law for firm size and that for firm debt when bankrupted are closely related to one another.

3 Balance-sheet dynamics of firm

3.1 What is a firm?

In order to understand how firms die, let us consider the activity of a firm from the viewpoint of money flow.

A firm makes activity by producing goods or services in anticipation to be demanded by consumers, and to yield profit. For the firm to realize the production and selling of goods and services, it must usually invest more money than what it actually possesses with a fund by the firm’s owners or stockholders. The investment is done not only for cost of sales, expenses of selling, etc. but also for additional facility, production line, employment etc.

A firm’s activity has three facets in general:

-

1.

finance

borrowing money from banks, market investors -

2.

investment

spending money in anticipation of future return of profits -

3.

collecting

earning profits from the sales of good and services

In other words, these three facets imply (1) the presence of creditor (borrower), (2) that investment can be a source of risk, because (3) return of profits has uncertainty in realization.

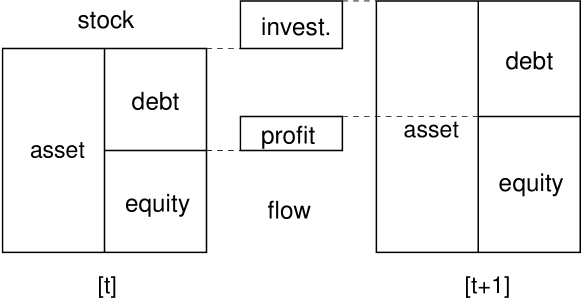

The above description can be formulated in terms of stock and flow of money. Flow is inflow of money in a period of time, and stock is the accumulation of flow over time. Stock of a firm is its balance sheet which consists of asset, debt and equity (see Fig. 6). Here asset refers to all the assets possessed by the firm which are expected to yield profits. The asset can be classified into equity and debt according to how it is financed, either by stockholders or by loan from banks and market, respectively.

Temporal change of balance-sheet is determined by flow. One source of flow is profit which is basically given by sales minus cost of sales, finance, and others. The other flow is investment which is determined by the firm’s decision based on anticipation of profits. Since the investment is covered by additional debt, it also depends on creditor’s activity.

Balance sheet dynamics is the temporal change of asset and debt. Debt is necessary for making profits, but is a source of risk since it can diminish equity and can dominate the balance sheet. Financial fragility can be measured either by flow variable such as insolvency (the ratio between debt commitments to profits) or by stock variable such as liquidity (the ratio between debt and capital). Persistent state of insolvency results in liquidity problem. Actually the most cases of bankruptcies (see Appendix) are due to the problem of liquidity.

3.2 Aggregate dynamics of creditor and debtors

Recently a model for the dynamics of balance sheets of a bank and firms are proposed in [17], which is based on their previous model for aggregate dynamics of firms [18]. This model of creditor-debtor dynamics has two elements; competition between firms by their sizes, and debtor-creditor relation between a bank and each firm.

In this section, let us briefly recapitulate the model (see [17] for details) and show by simulation that our phenomenological findings about bankruptcy can be reproduced in the model.

A firm has, at time , asset , debt and equity which satisfy the identity:

| (3) |

where is the number of firms. In the period of time from time to , the firm makes the following activity with to be determined below. It produces an output (), which is to yield revenue with uncertainty. At the same time, the firms has financial cost, comprised of dividend for equity and interest rate for debt. The profit in the current period is

| (4) |

where is interest-rate for the firm . Here is a stochastic variable representing the uncertainty in making profit. In the second term, the ratio of dividend to equity is assumed to be equal to the interest rate.

Supposing is a parameter, the firm plans the amount of investment during the current period. Since the profit is proportional to the total asset , the firm could increase its size by investment. But the bigger the size is, the larger the risk of insolvency or bankruptcy is, in the presence of uncertainty for profit. As a simplest form, the objective function for determining the investment is assumed to have a quadratic term of . Namely, the maximization of the expectation:

| (5) |

yields an optimal value of . Then the investment in the current term is

| (6) |

for the realization of which the firm demand loan of the amount

| (7) |

In this model the demand is assumed to be always fulfilled by bank with an appropriate interest-rate. Therefore balance sheet updates by , , and , once the interest rate is determined as shortly given.

Bank is monopolistic and responsible for all the loans to firms. Its balance sheet is composed of loan as asset, deposit as debt, and equity of itself:

| (8) |

The total supply of loans is usually determined by the ratio of asset to equity, so is assumed here as

| (9) |

with a parameter . The supply of loan to each firm is assumed to be based of collateral of firm asset.

| (10) |

This is where competition between firms is in effect. Then the interest-rate for each firm is determined by . The bank’s profit is revenue from interests minus the financial cost of the bank

| (11) |

where

| (12) |

and is a parameter for profit markup.

The bank faces uncertainty of firms bankruptcy. A firm goes into bankruptcy when its equity becomes negative. Bankrupted firms are replaced with new ones with initial and same balance sheet. The update for the bank’ is thus given by

| (13) |

where is for every firm bankrupted (), otherwise 0.

The dynamics of this system was investigated by simulation in [17]. It was found that the model has, in a stationary phase, skewed distribution of firms sizes with power-law, Laplace distributed growth rates, and that small idiosyncratic shocks generate large aggregate fluctuations. We used the same set of parameters: , , , except the number of firms (much larger than in original). The stochastic variable obeys a uniform distribution with support (0,2). The results of simulation are robust with other set of parameters, and with the number of firms.

Our new findings from the simulation is given in Fig. 7. We can observe that the distributions of debt and life-time for bankrupted firms have the same qualitative results as in the real data. These results are also robust for different parameters.

4 Summary and Discussion

Firms growth and failure are the two sides of the same coin. In this paper, we have uncovered the phenomenology of firms bankruptcy by using an exhaustive list of Japanese bankruptcies in 1997. Namely, for high-debt regime

-

1.

debt of bankrupted firms follows Zipf distribution

-

2.

debt and size of such firms are related by multiplicative factor independent of the amount of debt

-

3.

bankrupted firms have life-time whose distribution is exponential but correlates with entry rate of new firms

The origin of Zipf law in firms bankruptcy might be well captured in the model [17], which was shown to reproduce the phenomenological properties in bankruptcy. Indeed the model shares the aspect of self-organized criticality [19] (see also [20]) as discussed briefly in what follows.

Failure of a firm can have tremendous influence to economic activities in macroscopic scale. This is because the default of a single firm can propagate its effect through a network of creditor-debtor relationship. In the model, a bankrupted firm leaves the market without paying back its debt and debt commitments to bank. Then the banking system suffers from a capital loss, resulting in the shrink of credit supply. Such shrink accompanied with rise of interest rates is likely to strengthen the competition between firms for seek of more credit and then to deteriorate the firms balance-sheets. But this results in the growing probability of bankruptcy. This is a “domino effect”. The model also shows the opposite case of financially infragile or sound state of firms and bank which leads growth of the total credit and so that of total production (since the system is assumed to have enough money supply when necessary).

During this process of debtor-creditor dynamics, all the firms are competing in their sizes having the risk of bankruptcies. The risk is shared by the bank who attempts to make profit by interest rate. Note that the model has essentially no fine-tuning parameter for having in eq. (1) and the Zipf law in firms size. In this respect, the model differs from the traditional approach of stochastic processes for firms growth and failure (see [21] for mid-60’s nice review) including entry-exit processes, collective risk theory, etc. Rather it is the heterogeneous interacting and competing agents that brings about critical state in the aggregate dynamics of firms (see [22] for this new direction).

References

- [1] Y. Ijiri, H.A. Simon, Skew Distributions and the Sizes of Business Firms (North-Holland, New York, 1977).

- [2] M.H.R. Stanley, L.A.N. Amaral, S.V. Buldyrev, S. Havlin, H. Leschhorn, P. Maass, M.A. Salinger, H.E. Stanley H.E. Nature 379 (1996) 804.

- [3] L.A.N. Amaral, S.V. Buldyrev, S. Havlin, H. Leschhorn, P. Maass, M.A. Salinger, H.E. Stanley, M.H.R. Stanley, J. Phys. (France) I 7 (1997) 621.

- [4] S.V. Buldyrev, L.A.N. Amaral, S. Havlin, H. Leschhorn, P. Maass, M.A. Salinger, H.E. Stanley, M.H.R. Stanley, J. Phys. (France) I 7 (1997) 635.

- [5] J. Sutton, J. Econ. Lit. 35 (1997) 40.

- [6] L.A.N. Amaral, S.V. Buldyrev, S. Havlin, M.A. Salinger, H.E. Stanley, Phys. Rev. Lett. 80 (1998) 1385.

- [7] K. Okuyama, M. Takayasu, H. Takayasu, Physica A 269 (1999) 125.

- [8] R.L. Axtell, Science 293 (2001) 1818.

- [9] M. Mizuno, M. Katori, H. Takayasu, M. Takayasu, in Empirical Science of Financial Fluctuations: The Advent of Econophysics, H. Takayasu, Ed. (Springer-Verlag, Tokyo, 2002), pp.321–330.

- [10] X. Gabaix, “Power laws and the origins of the business cycle”, MIT, Department of Economics, preprint (2002).

- [11] Y. Fujiwara, H. Aoyama, W. Souma, in Proceedings of Second Nikkei Symposium on Econophysics, H. Takayasu, Ed. (Springer-Verlag, Tokyo, 2003), in press.

- [12] H. Aoyama, Y. Fujiwara, W. Souma, in Proceedings of Second Nikkei Symposium on Econophysics, H. Takayasu, Ed. (Springer-Verlag, Tokyo, 2003), in press.

- [13] H. Aoyama, W. Souma, Y. Nagahara, M. P. Okazaki, H. Takayasu, M. Takayasu, Fractals 8 (2000) 293.

- [14] J. Laherrere, D. Sornette, Stretched Exponential Distributions in Nature and Economy. Eur. Phys. J. B 2 (1998) 525.

- [15] S. M. Ross, Stochastic Processes (John Wiley & Sons, New York, 1996).

- [16] Historical data for entry of firms was prepared from two sources for 61 years of 1937–1997. The total number of corporations in each year is taken from the record for corporate tax provided by National Tax Administration Agency (NTA). The number of new firms is assumed to be equal to the number of corporations registered at branch offices of Ministry of Justice (MOJ) in each year. In both records, corporations refer to the same set of firms, called ordinary corporations by NTA, composed of joint stock companies, limited and unlimited companies. The present number of firms approximates 2.5 million, while that in 1937 was only 92,255. Both data are accessible from NTA and MOJ.

- [17] M. Gallegati, G. Giulioni, N. Kichiji, in Proceedings of 2003 International Conference in the Computational Sciences and Its Application, M. L. Gavrilova, V. Kumar, P. L’ecuyer, C. J. K. Tan, Ed.

- [18] D. Delli Gatti, M. Gallegati, A. Palestrini, in Interaction and Market Structure, D. Delli Gatti, M. Gallegati and A. Kirman, Ed. (Springer-Verlag, Berlin, 2000).

- [19] P. Bak, How Nature Works (Copernicus, New York, 1996).

- [20] D. Sornette, Critical Phenomena in Natural Sciences (Springer-Verlag, Heidelberg, 2000).

- [21] J. Steindl, Random Processes and the Growth of Firms (Griffin, London, 1965).

- [22] M. Aoki, Modeling Aggregate Behaviour and Fluctuations in Economics (Cambridge Univer. Press, New York, 2002).

Appendix A Bankruptcy data

Bankruptcy or business failure is not a legal term, but should be understood as a commonly used term to describe a state of critical financial insolvency of a debtor. A typical case of bankruptcy is a suspension of banking transactions (see below). What are also termed bankruptcy are: filing to the court for bankruptcy proceedings or a corporate rehabilitation procedure, or informing the aggravation of financial condition of the debtor and delegating creditors to handle it.

Types of bankruptcy are legally divided into legal and private procedures. The former procedure has purpose for rehabilitation or liquidation. Rehabilitation is done by either of Corporate Reorganization Law, Civil Rehabilitation Law (since 2000), Corporate Arrangement under the Commercial Code, or Composition Law (abandoned in 2000). Liquidation is done by Special Liquidation or by “Bankruptcy”. Private procedure, on the other hand, refers to either Suspension of Bank Transactions or Internal Arrangement. The number of each bankruptcy types in 1997 is as follows:

| bankruptcy type | number |

|---|---|

| private procedure | |

| Suspension of Bank Transactions | 13850 |

| Internal Arrangement | 501 |

| legal procedure for rehabilitation | |

| Composition Law | 195 |

| Corporate Reorganization | 23 |

| Corporate Arrangement | 12 |

| legal procedure for liquidation | |

| “Bankruptcy” | 1877 |

| Special Liquidation | 68 |

| total | 16526 |

The most frequent case is suspension of bank transactions. Concerning with the bill and check clearings, clearing houses practice a punishment system against the entity who committed dishonored bills or checks in order to maintain the public credibility. The bills or checks which a debtor fails to settle within the term shall be “dishonored”. The second dishonor within six months after the first one shall result in publishing the debtor’s name on the ”the report on suspension of banking transactions.”

Then the debtor shall be barred from transactions with any member financial institutions of the same clearinghouse for two years from the date of suspension, being prohibited from opening trade accounts, drawing bills or checks, and receiving loans. In actuality, this is equivalent to bankruptcy of the firm.

In summary, we regard this case as liquidity problem, and also consider that other legal and private procedures are basically due to the same problem (debt growth).