Do Pareto-Zipf and Gibrat laws hold true?

An analysis with European Firms

Abstract

By employing exhaustive lists of large firms in European countries, we show that the upper-tail of the distribution of firm size can be fitted with a power-law (Pareto-Zipf law), and that in this region the growth rate of each firm is independent of the firm’s size (Gibrat’s law of proportionate effect). We also find that detailed balance holds in the large-size region for periods we investigated; the empirical probability for a firm to change its size from a value to another is statistically the same as that for its reverse process. We prove several relationships among Pareto-Zipf’s law, Gibrat’s law and the condition of detailed balance. As a consequence, we show that the distribution of growth rate possesses a non-trivial relation between the positive side of the distribution and the negative side, through the value of Pareto index, as is confirmed empirically.

keywords:

Pareto-Zipf law , Gibrat law , firm growth , detailed balance , EconophysicsPACS:

89.90.+n , 02.50.-r , 05.40.+j , 47.53.+n1 Introduction

Pareto [1] is generally credited with the discovery, more than a century ago, that the distribution of personal income obeys a power-law in high-income range111See [2] for modern and high-quality personal-income data in Japan.. Firm size also has a skew distribution [3], and quite often obeys a power-law in the upper tail of the distribution. In terms of cumulative distribution for firm size , this states that

| (1) |

for large , with being a parameter called Pareto index. The special case is often referred to as Zipf’s law [4]. In this paper we call it Pareto-Zipf law, the fact that firm size has a power-law distribution asymptotically for large firms.

Even if the range for which eq. (1) is valid is a few percent in the upper tail of the distribution, it is often observed that such a small fraction of firms occupies a large amount of total sum of firm sizes. This means that a small idiosyncratic shock can make a considerable macro-economic impact. It is, therefore, quite important to ask what is the underlying dynamics that governs the growth of those large firms.

Let a firm’s size be at a time and at a later time. Growth rate is defined as the ratio . Law of proportionate effect [5] (see also [6]) is a postulate that the growth rate of a firm is independent of the firm’s attained size, i.e.

| (2) |

where is the probability distribution of growth rate conditional on the initial size . In this paper we call this assumption as Gibrat’s law222Another interesting and related quantity is flow, e.g. profits, rather than stock. See [7] for growth of individual personal-income and [8] for firms tax-income growth, and validity of Gibrat’s law..

These two laws have been extensively studied in industrial organization and related stochastic models [3, 6, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23, 24] (see [25] for review). Recent study in econophysics [26, 27, 28, 29, 30, 31, 32, 33, 34, 35, 36, 37] introduced some notions and concepts of statistical physics into economics (see [38]). Present status related to firm-size growth may be summarized as follows. Firm size distribution is approximately log-normal with deviation from it in the upper tail of the distribution (e.g. [24] for recent data). On the other hand, Gibrat’s law breaks down in the sense that the fluctuations of growth rate scale as a power-law with firm size; smaller firms can possibly have larger fluctuations (e.g. [27, 28]). However, little attention has been paid to the regime of firm size where power-law is dominant rather than log-normality, and to the validity of Gibrat’s law in that regime. More importantly, any kinematic relationship between Pareto-Zipf and Gibrat laws has not been understood explicitly, although there have been a lot of works on stochastic dynamics since Gibrat. This issue is exactly what the present paper addresses.

For our purpose it is crucial to employ exhaustive lists of large firms. Our dataset for European countries is exhaustive in the sense that each list includes all the active firms in each country whose sizes exceed a certain threshold of observation. We show that both of the Pareto-Zipf law and Gibrat’s law do hold for those large firms. As our main result, we prove that Pareto-Zipf law implies Gibrat’s law and vice versa under detailed balance. By showing that the condition of detailed balance also holds in our empirical data, we can show the equivalence of Pareto-Zipf law and Gibrat’s law as a kinematic principle in firms growth, irrespective of the underlying dynamics. Thereby, we conjecture that Gibrat’s law does hold in the regime of Pareto-Zipf for large firms, but does not for smaller firms. Thus our result is not contradictory to the breakdown of Gibrat’s law in previous study, most notably to the recent work by Stanley’s group [27, 28, 29, 30]. Furthermore, in the process of our proof, we also show that the distribution of growth rate possesses a non-trivial relation between the positive side () of the distribution and the negative side (), through the value of Pareto index , which is confirmed empirically.

In section 2, we give a brief review of the study on Gibrat’s law and firm size distribution in economics. In section 3, we describe the nature of our database of firms with large size in European countries. In section 4, using exhaustive lists of large firms in the dataset, we show that Gibrat’s law holds in the power-law regime for which the firm size distribution obeys Pareto-Zipf law. In addition, we uncover that temporal change of individual firm’s size in successive years satisfies what we call time-reversal symmetry, or detailed balance. In section 5, we prove that the two empirical laws of Gibrat and Pareto-Zipf are equivalent under the condition of detailed balance. We summarize our results in section 6.

2 Gibrat and Pareto-Zipf Laws in Economics

Industrial organization literature has long been focused on two

empirical facts

[3, 6, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23, 24]

(see [25] for review):

(i) skew distribution of firms size

(ii) validity or invalidity of Gibrat’s law for firm growth

Gibrat formulated the law of proportionate effect for growth rate to explain the empirically observed distribution of firms. The law of proportionate effect states that the expected increment to a firm’s size in each period is proportional to the current size of the firm. Let and be, respectively, the size of a firm at time and , and denote the proportionate rate of growth. The the postulate is expressed as

Gibrat assumed (a) that is independent of (Gibrat’s law), (b) that has no temporal correlation, and (c) that there is no interaction between firms. Then, after a sufficiently long time , since

follows a random walk. Assuming that is small, one has

Gibrat’s model has two consequences concerning the above points (i) and (ii). Since the growth rate defined by has its logarithm as the sum of independent variables , the growth rate is log-normally distributed. In addition, assuming that all the firms have approximately the same starting time and size, the distribution of firms size is also also log-normal with mean and variance given by and , respectively, where is the mean of and is the variance of .

The assumptions (a)–(c) in Gibrat’s model are in disagreement with empirical evidence. Among others, the Gibrat’s law (a) is incompatible with the fact that the fluctuations of growth rate measured by standard deviation decreases as firm size increases [12, 13, 16, 18, 19]. Especially, the recent work [27, 28] by Stanley’s group showed that the distribution of the logarithm of growth rates, for each class of firms with approximately the same size, displays an exponential form (Laplace distribution) rather than log-normal. They also show that the fluctuations in the growth rates characterized by the standard deviation of the distribution decreases for larger size of firms as a power-law, , with the exponent is less than a half. The latter point suggests a new viewpoint about the interplay of different parts of a firm, an industrial sector, or an organization [29, 30].

In contrast to the standard deviation, the measure by mean growth rate has been disputed. There were studies which showed that smaller firms grow faster [19] or slower [15, 20] than bigger ones. However, it is generally thought that the proportional rate of growth of a firm (conditional on survival) is decreasing in size, as far as small and medium firms are concerned, which share a large fraction of industrial sectors in number. However, the remaining larger firms constitute a small fraction in number, but occupy a large fraction of total sum of firms size. This is due to the effect of heavy tail, much heavier than expected from log-normal regime. See recent works [26, 24]333[26] observed that log-normal distribution overestimates the upper-tail of size distribution based on Computat in U.S. As noted in the paper, the dataset is consisting of only publicly-traded firms. This can be a possible cause of their observation. [24] used much larger dataset in U.K. Though their plot showed a power-law regime over several orders of magnitude, they rejected the hypothesis of power-law due to the presence of super-giant firms. We consider that both of the these points deserve further investigation.. This is the Pareto-Zipf regime which we focus on in this paper.

On the other hand, the assumption (b) about temporal correlation between successive growth rates are not investigated with definite conclusions. [17], for example, showed that the distribution of growth rates shows a first-order positive autocorrelation: the growth process will result faster for firms which recorded a sharp growth in previous years. ([17] also furnished a test test for the validity of Gibrat’s Law that takes into account the “historical memory” of the growth process.)

Gibrat’s work also opened up a stream of theoretical models and ideas. Kalecki noted that Gibrat’s model leads to “unrealistic” feature, that is, the variance of the size distribution would increase indefinitely with time. He considered several models, one of which assumed that the expected rate of growth increased less than proportionately, leading to a log-normal distribution with constant variance.

Herbert Simon considered it more important that the firm size distribution has heavy tail in upper-region of size, which was better fitted by Yule distribution or asymptotically a Pareto-Zipf law. In order to explain such a distribution, based on his earlier work [11] for the explanation of Zipf’s law in word frequency, he assumed Gibrat’s law (in a much weaker form than ours) with a boundary condition for entry and exit of firms. In conformity with preceding work by Champernowne for personal income [10], Simon could show that the emergence of power-law behavior is quite robust irrespectively of modification of the stochastic process (see [3] for collection of related papers). Simon modeled the process of entry corresponding to new firms which compete with existing firms to catch market opportunities. This line of models was followed by [21] which relaxes the assumption of Gibrat’s law, and also by [37] which explained the Laplace distribution for growth rate. Simon also extended his model incorporating merger and acquisition process (see also [22] for recent work). These works attempted to take into account the direct and indirect interactions among firms, which was ignored in the assumption (c) above.

Our work is in affinity with Simon’s view in the points that the upper-tail of size distribution, Pareto-Zipf law, is focused rather than the log-normal regime, and that the origin of it is related to Gibrat’s law and boundary condition of entry-exit of firms. It is interesting to point out that Mansfield [14], following Simon’s model, empirically showed that the Gibrat’s law seemed to hold only above a certain minimum size of firms. (See also [25] for the influence of [14] onto later work.)

At the end of this brief survey, let us point out why recent advent of econophysics can have important impact on economics. The econophysics approach attempts to treat the whole industrial organization as a complex system, in which firms are interacting atoms, that exhibits universal scaling laws [38].

Concerning firm size, the Pareto-Zipf power-law distribution has a long history since the seminal work by Herbert Simon, but its study extending to the details of growth rate was only recently facilitated by modern datasets with good abundance and quality. In this line of research, resent findings (e.g. [34, 36]) showed that power-law distribution gives a very good fit for different samples of firm size. In this paper we shall not only confirm this fact with different European countries and for different measures of size, but also uncover the underlying kinematics that relates Pareto-Zipf law to Gibrat law explicitly. Following the notion of self-organized criticality [39, 40], the occurrence of a power-law reveals that a deep interaction among system’s subunits, reacting to idiosyncratic shocks, leads to a critical state in which no attractive points nor states emerge. Such interaction and critical states are so important notions with that of self-organized criticality. Under economic point of view, interaction means that it is not possible to define a representative agent because the dynamics of the system is originated just from the interaction among heterogeneous agents. Moreover, in consequence of critical state, equilibrium exists only as asymptote, along which the system moves from an unstable critical point to another. The authors believe that economics can enjoy these ideas coming from econophysics on heterogeneous interacting agents (see [41][42] for an example).

3 Dataset of European Firms

We use the dataset, Bureau van Dijk’s AMADEUS, which contains descriptive and balance data of about 260,000 firms of 45 European countries for the years 1992–2001. For every firm are reported a number of juridical, historical and descriptive data (as e.g. year of inclusion, participations, mergers and acquisitions, names of the board directors, news, etc.) and a series of data drawn from its balance and normalized. It reports the current values (for several currencies) of stocktaking, balance sheet (BS), profit and loss account (P/L) and ratios. The descriptive data are frequently updated while the numerical ones are taken from the last available balance. Since balance year does not always match conventional year, the number of firms included may vary during the year if one of the excluded firms in last recording satisfy one of the criteria described below. The amount and the completeness of available data differs from country to country. To be included in the data set firms must satisfy at least one of these three dimensional criteria:

-

•

for U.K., France, Germany, Italy, Russian Federation and Ukraine

-

–

operating revenue equal to at least 15 million Euro

-

–

total assets equal to at least 30 million Euro

-

–

number of employees equal to at least 150

-

–

-

•

for the other countries

-

–

operating revenue equal to at least 10 million Euro

-

–

total assets equal to at least 20 million Euro

-

–

number of employees equal to at least 100

-

–

As a proxy for firm size, we utilize one of the financial and fundamental variables; total-assets, sales and number of employees. We use number of employees as a complementary variable so as to check the validity and robustness of our results. Note that the dataset includes firms with smaller total-assets, simply because either the number of employees or the operating revenue (or both of them) exceeds the corresponding threshold. We thus focus on complete sets of those firms that have larger amount of total-assets than the threshold, and similarly those for number of employees. For sales, we assume that our dataset is nearly complete since a firm with a small amount of total-assets and a small number of employees is unlikely to make a large amount of sales. For our purposes, therefore, we discard all the data below each corresponding threshold for each measure of firm size. This procedure makes the number of data points much less. However, for a several developed countries, we have enough amount of data for the study of Gibrat’s law. In what follows, our results are shown for UK and France, although we obtained similar results for other developed countries. The threshold for total-assets in these two countries is 30 million euros, and that for number of employees is 150 persons, as described above. For sales, we used 15 million euros per year as a threshold. We will also show results for Italy and Spain in addition to U.K. and France only when examining the annual change of Pareto indices.

It should be remarked that other problems in treating these data takes origin from the omission, in the on-line dataset of AMADEUS, of the date of upgrade, so that it is often not clear when a firm changed its juridical status, or went bankrupted or inactive. For some countries the indication activity/inactivity is not shown at all, so that it was impossible, even indirectly, to individuate the year of exit. Therefore, our study should be taken as the analysis conditional on survival of firms.

4 Firm Growth

In this section, our results are shown for UK and France, and for total-assets, number of employees and sales. Each list of firms is exhaustive in the way we described in the preceding section.

4.1 Pareto-Zipf distribution

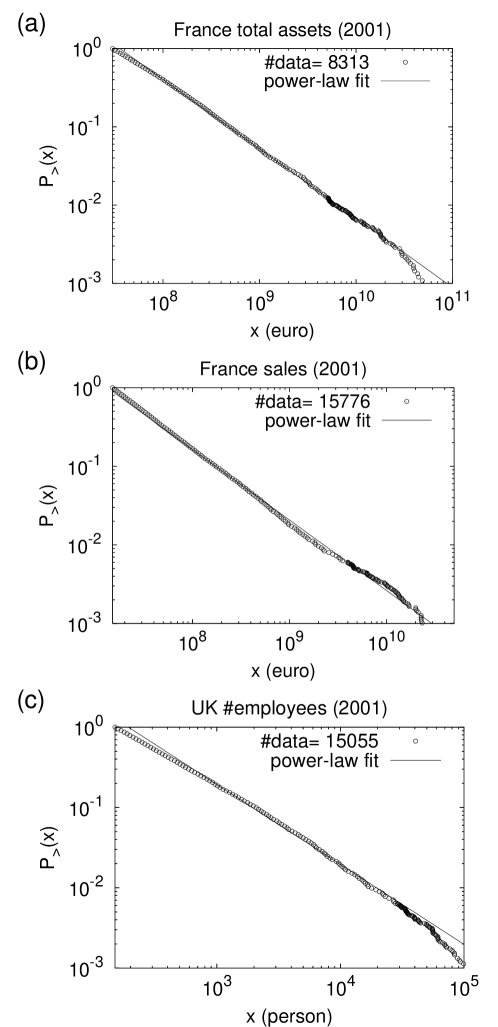

First we show that the distribution of firm size obeys a power-law in the range of our observation whatever we take as a variable for firm size. Fig. 1 depicts the cumulative distributions for total-assets in France (a), sales in France (b), and number of employees in UK (c). The number of data points is respectively (a) 8313, (b) 15776 and (c) 15055.

Pareto-Zipf law states that the cumulative distribution for firm size follows eq. (1). The power-law fit for , where denotes the threshold mentioned above for each measure of firm size, gives the values of ; (a) 0.8860.005, (b) 0.8960.011, (c) 0.9950.013 (standard error at 99% significance level). is close to unity. Note that the power-law fit is quite well nearly three orders of magnitude in size of firms.

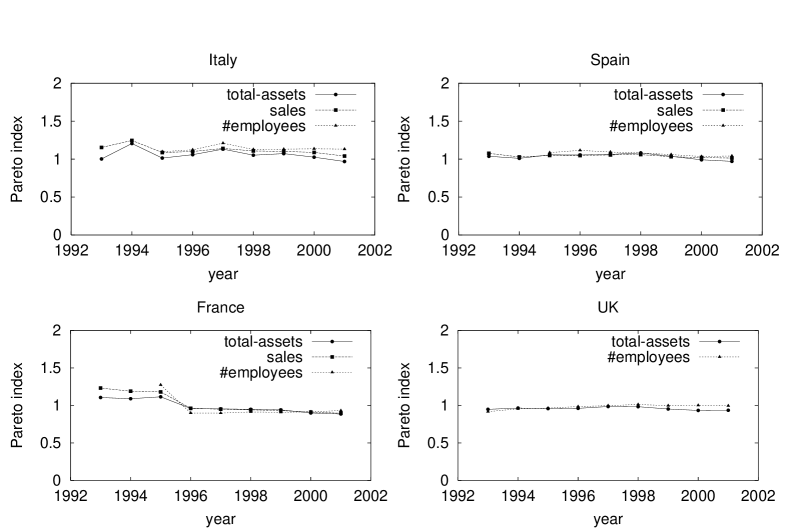

Pareto index is surprising stable in its value. Fig. 2 is a panel for the annual change of Pareto indices for four countries, Italy, Spain, France and U.K. estimated from total-assets, number of employees and sales (except U.K.). Different measures of firm size give reasonably same behavior. It is observed that the value is quite stable being close to unity in all the countries.

4.2 Gibrat’s law

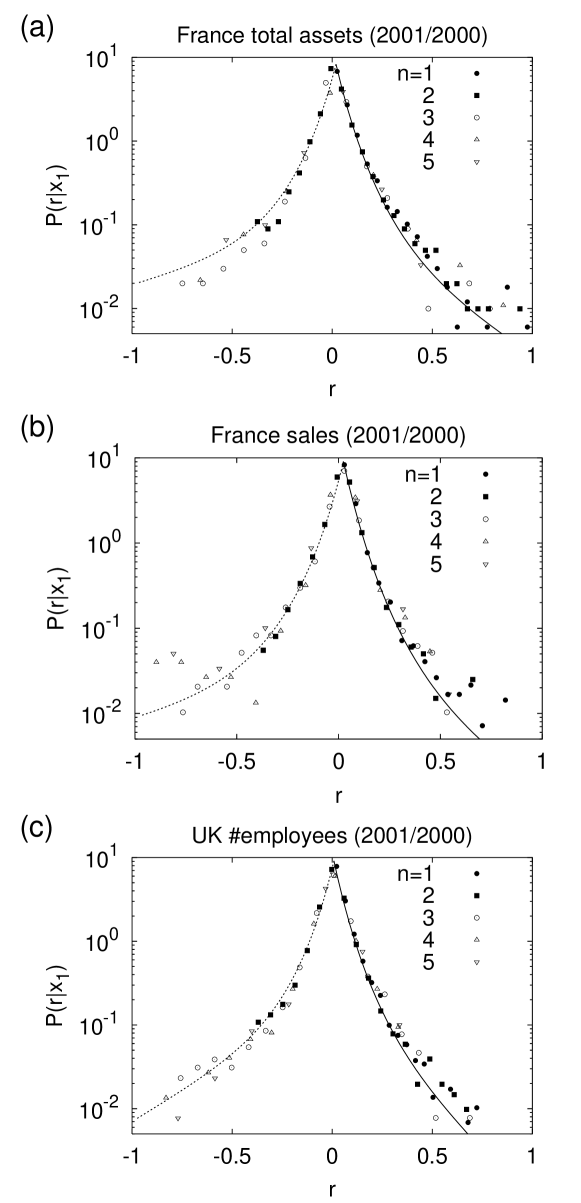

Let us denote a firm’s size by and its two values at two successive points in time (i.e., two consecutive years) by and . Growth rate is given by . We also express the rate in terms of its logarithm, . We examine the probability density for the growth rate on the condition that the firm size in an initial year is fixed.

For the conditioning we divide the range of into logarithmically equal bins. For the total-assets in the dataset (Fig. 3 (a)), the bins are taken as (euros) with . For the sales in (b), (euros) with . For the number of employees in (c), (persons) with . In all the cases, the range of conditioning covers two orders of magnitude in each variable. We calculated the probability density function for for each bin, and checked the statistical dependence on by graphical method.

Fig. 3 is the probability density function for each case. It should be noted that due to the limit and , the data for large negative growth are not available. In all the cases, it is obvious that the function has little statistical dependence on , since all the curves for different collapse on a single curve. This means that the growth rate is independent of firm size in the initial year. That is, Gibrat’s law holds.

4.3 Time-reversal symmetry

The validity of Gibrat’s law in the Pareto-Zipf regime appears to be in disagreement with recent literature on firm growth. In the next section, we will show that this is not actually the case by proving that Gibrat and Pareto-Zipf are equivalent under an assumption. The assumption is detailed balance, whose validity is checked here.

Let us denote the joint probability distribution function for the variable and by . The detailed balance, or what we call time-reversal symmetry, is the assumption that . The joint probabilities for our datasets are depicted in Fig. 4 as scatter-plots of individual firms.

We used two different methods to check the validity of time-reversal symmetry. One is an indirect way to check a non-trivial relationship between the growth-rate in positive side () and that in negative (). That is, as we shall prove in the next section, the probability density distribution in positive and negative growth rates must satisfy the relation given by eq. (27), if the property of time-reversal symmetry holds. We fitted the cumulative distribution only for positive growth rate by a non-linear function, converted to density function, and predicted the form of distribution for negative growth rate by eq. (27) so as to compare with the actual observation (see Appendix for details). In each plot of Fig. 3, a solid line in the side is such a fit, and a broken line in the side is our prediction. The agreement with the actual observation is quite satisfactory, thereby supporting the validity of time-reversal symmetry.

The other way we took is a direct statistical test for the symmetry in the two arguments of . This can be done by two-dimensional Kolmogorov-Smirnov (K-S) test, which is not widely known but was developed by astrophysicists [43, 44, 45]. This statistical test is not strictly non-parametric (like the well-known one-dimensional K-S test), but has little dependence on parent distribution except through coefficient of correlation. We compare the scatter-plot sample for with another sample for and interchanged by making the null hypothesis that these two samples are taken from a same parent distribution. We used the logarithms and , and added constants to and so that the average growth rate is zero. This addition (or multiplication in and ) is simply subtracting the nominal effects due to inflation, etc. We applied two-dimensional K-S test to the resulting samples. The null hypothesis is not rejected in 95% significance level in all the cases we studied.

5 Pareto-Zipf’s law and Gibrat’s law under detailed balance

In the preceding section, we have shown that both of Pareto-Zipf and Gibrat’s laws hold for large firms. This suggests that these two laws are closely related with each other. We show in this section that in fact they are equivalent to each other under the condition of detailed balance.

Let be a firm’s size, and let its two values at two successive points in time (i.e., two consecutive years) be denoted by and . We denote the joint probability distribution function (pdf) for the variable and by . The joint pdf of and the growth rate is denoted by . Since under the change of variables from to , these two pdf’s are related to each other as follows:

| (3) |

We define conditional probabilities:

| (4) | |||||

| (5) |

Both and are marginal:

| (6) | |||||

| (7) |

since the following normalizability conditions are satisfied:

| (8) | |||||

| (9) |

Three phenomenological properties can be summarized as follows.

-

(A)

Detailed Balance (Time-reversal symmetry):

The joint pdf is a symmetric function:(10) -

(B)

Pareto-Zipf’s law:

The pdf obeys power-law for large :(11) for with .

-

(C)

Gibrat’s law:

The conditional probability is independent of :(12) We note here that this holds only for large , because we confirmed it in actual data only in that region, and because otherwise it leads to an inconsistency, as we will see shortly. This relation was called Universality in [7, 8, 46, 47]. All the arguments below is restricted in this region.

Before starting our discussion of interrelation between these properties, let us first rewrite the detailed balance condition (A) in terms of :

| (13) | |||||

where eq. (10) was used in the second line, and eq. (3) was used in the first and the third line. The above relation may be rewritten as follows by the use of the conditional probability in eq. (5);

| (14) |

In passing, it should be noted that eq. (13) leads to the following:

| (15) | |||||

where eq. (13) was used in the second line, and the third line is merely change of integration variable. This relation between the marginal growth-rate pdf for positive growth () and negative growth () leads to the following relation, as it should:

| (16) |

5.1 (A)+(C)(B)

Let us first prove that the properties (A) and (C) lead to (B). By substituting the Gibrat’s law eq. (12) in eq. (14), we find the following:

| (17) |

This relation can be satisfied only by a power-law function eq. (11).

[Proof]

Let us rewrite eq. (17) as follows:

| (18) |

where denotes , and denotes the right-hand side of eq. (17), i.e.

| (19) |

We expand this equation around by denoting with as

| (20) | |||||

where we used the fact that . We also assumed that the derivatives and exists in the above, whose validity should be checked against the results. From the above, we find that the following should be satisfied

| (21) |

whose solution is given by

| (22) |

This is the desired result, Pareto-Zipf’s law, and is consistent with the assumption made earlier that exists. By substituting the result eq. (22) in eq. (19) and eq. (17), we find that

| (23) |

which is consistent with the assumption that exists.

[Q.E.D.]

From eq. (19) we may calculate in terms of derivatives of . It should, however, be noted that has a cusp at as is apparent in Fig. 3, and therefore is expected not to be continuous at . Bearing this in mind, we calculate for as follows:

| (24) | |||||

where we denoted the right-derivative and left-derivative of at by the signs and in the superscript, respectively. From the above, we find that

| (25) |

From eq. (22) and eq. (25), we find that

| (26) |

From eqs.(19) and (23), we find the following relation:

| (27) |

which should be in contrast to eq. (15). This is related to the point that we mentioned in eq. (12): If the Gibrat’s law eq. (12) holds for all , then from eq. (7). If so, eq. (27) contradicts to eq. (15) since . Besides, the Pareto-Zipf’s law we derived from Gibrat’s law is not normalizable if it holds for any . Therefore, Gibrat’s law should hold only for large .

5.2 (A)+(B) ?

Let us next examine what we obtain if we had only Pareto-Zipf’s law instead of Gibrat’s law under the detailed balance.

In this case, substituting the Pareto-Zipf’s law eq. (11) into eq. (14) we find that

| (28) |

where we denote by and by . We now define a function as

| (29) |

It should be noted that this does not constrain in any way: arbitrary function of the variable and can be written in the form of eq. (29). By substituting eq. (29) into eq. (28), we find that

| (30) |

which means that the function has the following invariance property.

| (31) |

Other than this constraint and some trivial constraint such as continuity, there is no nontrivial constraint on or .

5.3 (B)+(C)(A)?

Let us discuss the last question: Under Pareto’s and Gibrat’s laws, what can we say about the detailed balance? In order to answer this, we use eq. (11) and eq. (12) to write for large as follows:

| (33) |

where is a proportionality constant. According to eq. (13), the detailed balance is satisfied if this is equal to

| (34) |

where we used eq. (33). Therefore, we find that the detailed balance condition is equivalent to eq. (27) in this case.

Summarizing this section, we have proved that under the condition of detailed balance (A), if the Pareto-Zipf law (B) holds in a region of firm size, then the Gibrat’s law (C) must hold in the region, and vice versa. The condition (A) means detailed-balance. On the other hand, if both of (B) and (C) hold, (A) follows provided that eq. (27) holds. eq. (27) is our prediction which gives a non-trivial relation between positive growth () and negative (). This kinematic relation was empirically verified in Fig. 3. See also previous work [7, 8, 46, 47] for the validity of this relation in personal income and firms tax-income in Japan.

6 Summary

The distribution of firm size is quite often dominated by power-law in the upper tail over several orders of magnitude. This regime of Pareto-Zipf law is different from log-normal distribution in the lower and sometimes wider regime of firm size. The upper tail is occupied by a small number of firms, but they dominate a large fraction of total sum of firm size.

By using exhaustive datasets of those large firms and with different measures of firm size in Europe, we show that the Pareto-Zipf law holds as in eq. (1) for firm size larger than observational threshold , and that Gibrat’s law of proportionate effect holds as in eq. (2) for successive sizes and exceeding , stating that the growth rate of each firm is independent of initial size. We also find that detailed balance holds which means that the frequency of transition from to is statistically the same as that for its reverse process. The Gibrat’s law, Pareto-Zipf’s law and detailed balance condition are related to each other. We prove various relationships among them. It follows as one of the consequences that there exists a relation between the positive and negative sides of the distribution of growth rate via the Pareto index. The relation is confirmed empirically in our dataset of European firms.

References

- [1] V. Pareto, Le Cours d’Économie Politique (Macmillan, London, 1897).

- [2] H. Aoyama, W. Souma, Y. Nagahara, M. P. Okazaki, H. Takayasu, M. Takayasu, Fractals 8 (2000) 293.

- [3] Y. Ijiri, H.A. Simon, Skew Distributions and the Sizes of Business Firms (North-Holland, New York, 1977).

- [4] G. K. Zipf, Human Behavior and the Principle of Least Effort (Addison-Wesley, Cambridge, 1949).

- [5] R. Gibrat, Les inégalités économiques (Sirey, Paris, 1932).

- [6] J. Steindl, Random processes and the growth of firms: A study of the Pareto law, (Griffin, London, 1965).

- [7] Y. Fujiwara, W. Souma, H. Aoyama, T. Kaizoji, M. Aoki, Physica A 321 (2003) 598.

- [8] H. Aoyama, W. Souma, Y. Fujiwara, Physica A 324 (2003) 352.

- [9] M. Kalecki, Econometrica 45 (1945) 161.

- [10] D.G. Champernowne, Econometric J. 63 (1953) 318.

- [11] H. A. Simon, Biometrika 42 (1955) 425.

- [12] P. E. Hart, S. J. Prais, J. Roy. Statist. Soc. A119 (1956) 150.

- [13] S. Hymer, P. Pashigian, J. Polit. Econ. 70 (1962) 556.

- [14] E. Mansfield, Amer. Econ. Rev. 52 (1962) 1023.

- [15] J.M. Samuels, Rev. Econ. Stud. 32 (1965) 105.

- [16] A. Singh, G. Whittington, Rev. Econ. Stud. 42 (1975) 15.

- [17] A. Chesher, J. Ind. Econ. 27 (1979) 403.

- [18] B. H. Hall, J. Ind. Econ. 35 (1987) 583.

- [19] D. S. Evans, J. Ind. Econ. 35 (1987) 567.

- [20] T. Dunne, M. J. Roberts, L. Samuelson, Rand J. Econ. 19 (1988) 495.

- [21] J. Sutton, “The Size Distribution of Businesses, Part I.” STICERD Discussion Paper No. EI/9, London School of Economics, (1995).

- [22] P. McLoughan, Amer. Econ. Rev. 43 (1995) 405.

- [23] P. E. Hart, N. Oulton, Econ. J. 106 (1996) 1242.

- [24] P. E. Hart, N. Oulton, Applied Econ. Lett. 4 (1997) 205.

- [25] J. Sutton, J. Econ. Lit. 35 (1997) 40.

- [26] M.H.R. Stanley, S.V. Buldyrev, S. Havlin, R.N. Mantegna, M.A. Salinger, H.E. Stanley, Econ. Lett. 49 (1995) 453.

- [27] M.H.R. Stanley, L.A.N. Amaral, S.V. Buldyrev, S. Havlin, H. Leschhorn, P. Maass, M.A. Salinger, H.E. Stanley H.E. Nature 379 (1996) 804.

- [28] L.A.N. Amaral, S.V. Buldyrev, S. Havlin, H. Leschhorn, P. Maass, M.A. Salinger, H.E. Stanley, M.H.R. Stanley, J. Phys. (France) I 7 (1997) 621.

- [29] S.V. Buldyrev, L.A.N. Amaral, S. Havlin, H. Leschhorn, P. Maass, M.A. Salinger, H.E. Stanley, M.H.R. Stanley, J. Phys. (France) I 7 (1997) 635.

- [30] L.A.N. Amaral, S.V. Buldyrev, S. Havlin, M.A. Salinger, H.E. Stanley, Phys. Rev. Lett. 80 (1998) 1385.

- [31] H. Takayasu, K. Okuyama, Fractals 6 (1998) 67.

- [32] K. Okuyama, M. Takayasu, H. Takayasu, Physica A 269 (1999) 125.

- [33] J.J. Ramsden, Gy. Kiss-Haypál, Physica A 277 (2000) 220.

- [34] R.L. Axtell, Science 293 (2001) 1818.

- [35] M. Mizuno, M. Katori, H. Takayasu, M. Takayasu, in Empirical Science of Financial Fluctuations: The Advent of Econophysics, H. Takayasu, Ed. (Springer-Verlag, Tokyo, 2002), pp.321–330.

- [36] E. Gaffeo, M. Gallegati, A. Palestrini, Physica A 324 (2003) 117.

- [37] G. Bottazzi, A. Secchi, Physica A 324 (2003) 213.

- [38] H.E. Stanley, L.A.N. Amaral, P. Gopikrishnan, V. Plerou, Physica A 283 (2000) 31.

- [39] P. Bak, How Nature Works (Copernicus, New York, 1996).

- [40] S.F. Nørrelykke, P. Bak, Phys. Rev. E 65 (2002) 036147.

- [41] X. Gabaix, “Power laws and the origins of the business cycle”, MIT, Department of Economics, preprint (2002).

- [42] M. Gallegati, G. Giulioni, N. Kichiji, in Proceedings of 2003 International Conference in the Computational Sciences and Its Application, M. L. Gavrilova, V. Kumar, P. L’ecuyer, C. J. K. Tan, Ed.

- [43] W. H. Press, S. A. Teukolsky, W. T. Vetterling, B. P. Flannery, Numerical Recipes in C: the art of scientific computing, second edition, (Cambridge University Press, Cambridge, 1992).

- [44] J. A. Peacock, Mon. Not. Roy. Astr. Soc. 202 (1983) 615.

- [45] G. Fasano, A. Franceschini, Mon. Not. Roy. Astr. Soc. 225 (1987) 155.

- [46] Y. Fujiwara, H. Aoyama, W. Souma, in Proceedings of Second Nikkei Symposium on Econophysics, H. Takayasu, Ed. (Springer-Verlag, Tokyo, 2003), in press.

- [47] H. Aoyama, Y. Fujiwara, W. Souma, in Proceedings of Second Nikkei Symposium on Econophysics, H. Takayasu, Ed. (Springer-Verlag, Tokyo, 2003), in press.

Appendix A Fitting distribution of growth rate

For the purpose of fitting probability density function of positive growth rate (), we used cumulative distribution of positive growth rate, defined by

can be estimated, as usual, by size versus rank plot restricted only for as follows. Let the number of all firms with be , and sort their growth rates in descending order: . Then the estimate is given by

where ( is the observational threshold mentioned in section 4.1), and is the normalization:

Using the observational fact that eq. (12) holds in the region , the above equation for reads

| (35) |

where the normalization factor is written by

| (36) |

By taking derivative of eq. (35) with respect to , it follows that

| (37) |

We empirically found that the rank-size plot can be well fitted by a non-linear function of the form:

| (38) |

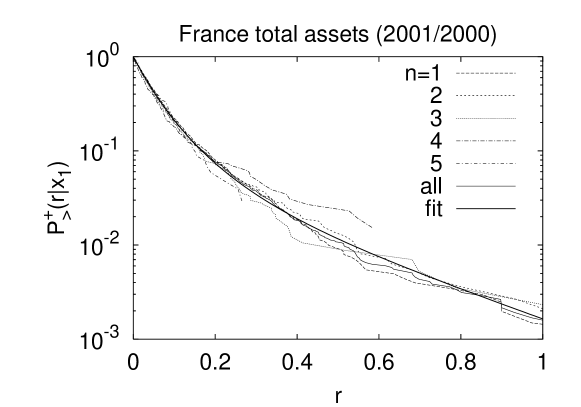

where , and are parameters. An example is given in Fig. 5 for France total-assets (2001/2000). Cumulative probabilities (the left-hand side of eq. (38)) conditioned on an initial year’s total-assets are shown for each of the same bins used in Fig. 3 (a), but restricted to the data with positive . The non-linear fit done by eq. (38) is represented by a solid and bold line in the figure. Note also that the curves for different bins almost collapse because of the statistical independence of .

Under the change of variable, , the probability density for defined by is related to that for by

| (39) |

Therefore it follows from eq. (37) and eq. (39) that

| (40) |

In each plot of Fig. 3, the solid curve is given by eq. (40), where denotes the probability density function for , conditioned on an initial year’s size .