LONG MEMORY IN STOCK TRADING

Andrei Leonidov

(a) Theoretical Physics Department, P.N. Lebedev Physics Institute,

119991 Leninsky pr. 53, Moscow, Russia111Research

supported by RFBR grant 02-02-16779 and Scientific School Supprort

grant 1936.2003.02

(b) Netcominvest Financial Investment Company,

109017 Profsoyznaya 3, Moscow, Russia

222Address before May 1 2003: Quantitative Analysis Group, EFOT GmbH, Feuerbachstrasse 26-32,

60325 Frankfurt, Germany

(c) Institute of Theoretical and Experimental Physics

117259 B. Cheremushkinskaya 25, Moscow, Russia

Abstract

Using a relationship between the moments of the probability distribution of times between the two consecutive trades (intertrade time distribution) and the moments of the distribution of a daily number of trades, we show that the underlying point process is essentially non-Markovian. A detailed analysis of all trades in the EESR stock on the Moscow International Currency Exchange in the period January 2003 - September 2003, including correlation between intertrade time intervals is presented. A power-law decay of the correlation function provides an additional evidence of the long-memory nature of the series of times of trades. A data set including all trades in Siemens, Commerzbank and Karstadt stocks traded on the Xetra electronic stock exchange of Deutsche Boerse in October 2002 is also considered.

The new field of econophysics, in particular part of these activities related to the description of financial markets, has drawn considerable attention in recent years [1, 2, 3]. One of the central issues under discussion is understanding fundamental origins of the stock price formation process. The progress in this direction is very rapid, see, e.g., [4, 5, 6, 7, 8, 9, 10] and references therein. The ultimate goal of the quantitative approach to the description of stock price dynamics is constructing a microscopic theory, in which this dynamics originates from the agents’ activity in the financial market generating patterns of demand - supply interaction, resulting in price formation. At a more phenomenological level the description of stock price evolution focuses on the dynamics of accomplished trades.

Among the most important characteristics of financial markets is their activity. On the trade-by-trade basis one can think of two possible ways of characterizing it and thus setting the clock measuring the operational time. The first possibility is to follow the volume traded [11], the second is to analyze the time-dependent frequency of trading operations. Below we shall follow the latter route. The importance of effects related to the varying trading frequency is well recognized. In particular, in [12] it was suggested, that they significantly influence the expected return during intensive speculative trading. In [4] it was also argued that the empirically observed long-range correlations in trading frequency [13, 4] directly induce the observed long-range correlations of volatility. Let us also mention a related topic of great practical interest - a study of seasonality effects (e.g., intraday and intraweek activity patterns) and of the corresponding tuning of trading strategies, see e.g. [14].

Below we shall study the trade dynamics at the smallest level of resolution, focusing ourselves on the properties of a (stochastic) process generating the times of trades. Given a description of such directing point process generating the times of trades , the temporal evolution of quantities of interest such as price or volume is that of a subordinated stochastic process [15] . The form the corresponding evolution equation for the probability distributions of, e.g., price and its characteristic features are thus decisively dependent on the properties of the directing point process . Generically one can distinguish the following possibilities:

-

•

Type 1. The time at which the -th point (trade) takes place is completely independent of the times at which the previous points were generated. In this case one deals with the Poisson distribution of the number of trades in any fixed time interval. This point process is fully characterized by an exponential probability distribution for the intertrade time , . The evolution of the probability density is described by a differential (in time) equation.

-

•

Type 2. The time of the -th trade is correlated with that of the previous, -th, trade, so that the the point process has a unit memory depth (and is thus still Markovian). The point process is still fully characterized by some non-exponential intertrade time probability distribution , but the evolution equation for is no longer differential, but an integral one, of continuous-time random walk type [16] 333The application of CTRW to the analysis of financial data was discussed in a number of papers [18, 19, 20, 21, 22, 23, 24]. The correlation between the number of trades in non-overlapping time windows can in principle be computed [17], but the resulting expressions are quite involved.

-

•

Type 3. The time of the n-th trade depends on times of the previous trades . In this case the point process is a long-range memory non-Markovian one with a memory depth equal to , and the corresponding evolution equation for is a complicated integral one with a kernel depending on arguments. If all temporal scales are effectively involved, is infinite.

The main question is, of course, whether the times of trades correspond to a long-range memory process with past events strongly influencing the new ones. Let us first consider a standard, although not very reliable, measure of the amount of memory present in the series - the (normalized) correlation function of the intertrade time intervals

| (1) |

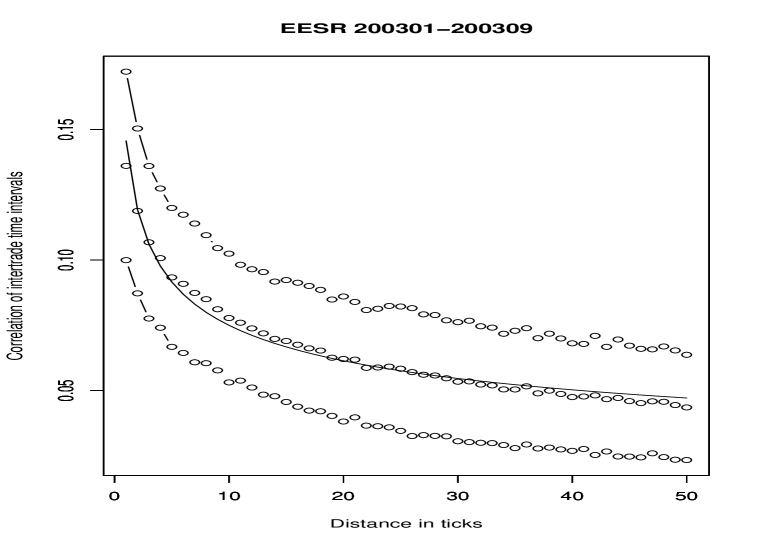

The correlation is computed by first averaging over all intervals separated by a fixed number of intervals for a given day and then averaging over all days. The correlation (1) for all trades, from January 2003 till September 2003, in the EESR stock traded on the MICEX stock exchange is shown, together with the errorbars characterizing its variation on the day-to-day basis, in Fig. 1.

The correlation function shown in Fig. 1 is clearly powerlike, , thus demonstrating a behavior typical for long-range processes.

To get a somewhat more precise picture of the memory - related pattern of the set of times of trades, let us consider a relation between the moments of the distribution of a number of trades in some given time interval and those of the intertrade time distribution that holds for the unit memory depth point process in the large – limit [17]. More specifically, for the processes of Type 1 and Type 2 there exist, for a sufficiently large time interval , a relation between the first two moments of the distribution of the number of trades within this interval and and the first two moments of the intertrade time distribution and [17]:

| (2) |

Corrections to the relation (2) are of order . Equivalently,

| (3) |

so that if the underlying point process is indeed of Type 1 or Type 2, one should have . Let us note, that in the simplest poissonian case . Let us also stress that provided the underlying point process has unit memory length, the equation (3) holds for any intertrade time probability distribution having a finite second moment . Derivation of Eq. (3) is sketched in the Appendix.

Equation (3) provides a straightforward possibility of establishing the nature of the point process by computing the quantities in its left- and right-hand side from an observed distribution of a number of trades in some fixed interval and a corresponding underlying distribution of the intertrade times. In particular in the case of the ensemble of independent points (Poisson case) , in the case of the CTRW - type process having unit memory depth a more general relation of Eq. (3) holds and, finally, for the long-range memory process the relation in Eq. (3) should break down.

In the data set used for our analysis the interval corresponds to one trading day (10.30 - 18.45 on the MICEX exchange and 9.00 – 20.00 on the Xetra electronic exchange of Deutsche Boerse in Frankfurt), and the considered ensemble of trades consists of all trades in EESR in January - September 2003 (MICEX) and Siemens, Commerzbank and Karstadt (liquid, medium liquid and relatively illiquid stock) in October 2002 on Xetra. The results are summarized in Table 1:

Table 1

| Und | (seq) | ||||

|---|---|---|---|---|---|

| EESR | 6823 | 4.5 | 10.3 | 492.8 | 109.4 |

| SIE | 4364 | 9.1 | 3.8 | 124.8 | 32.8 |

| CBK | 1856 | 21.3 | 3.1 | 274.4 | 88.5 |

| KAR | 373 | 104.1 | 4.5 | 39.7 | 8.8 |

From the results presented in Table 1 it is clear, that poissonian Type 1 and CTRW Type 2 processes are excluded as candidate point processes generating the times of the trades. This leaves us with the only remaining possibility of Type 3 non-Markovian long-range memory process. This conclusion is in obvious agreement with the long-range correlation between the intertrade time intervals for EESR shown in Fig. (1).

To provide some statistical backing to this conclusion, we have generated the times of trades using the empirically observed distribution over intertrade times as the EESR data. The thus generated set of points is characterized by the observed distribution, but is otherwise uncorrelated 444The distributions over intertrade time intervals were studied in a number of papers [20, 23, 24]. The considered number of trade intervals was equal to the number of trading days in the EESR data. This simulation effectively reconstructs a unit memory depth CTRW process. The results of this simulation are shown in Table 2:

Table 2

| Und | (seq) | ||||

|---|---|---|---|---|---|

| EESR (data) | 6823 | 4.5 | 10.3 | 492.8 | 109.4 |

| EESR (sim.) | 6816 | 4.5 | 12.4 | 8.2 | 0.66 |

We see, that although due to statistical limitations (finite size corrections, etc.) the simulation does not reproduce the theoretical value of , it is sufficiently close to it, while at the same time missing the experimental ratio by two orders of magnitude.

Conclusion

We conclude that the point process generating the times of trades is of long-range memory non-Markovian nature. This excludes random walk and continuous-time random walk (CTRW) processes as models describing high frequency stock price dynamics in real time.

Acknowledgements

I am grateful to Alain Guillot, Stefan Iglesias, Larry McLerran and Axel Vischer for reading the manuscript and useful comments. I would also like to thank the referee for constructive and helpful remarks.

References

- [1] R.N. Mantegna and H.E. Stanley, An Introduction to Econophysics, Cambridge, 2000

- [2] J.-P. Bouchaud and M. Potters, Theory of Financial Risks, Cambridge, 2001

- [3] D. Sornette, Why Stock Markets Crash, Princeton, 2003

- [4] V. Plerou, P. Gopikrishnan, L. Amaral, X. Gabaix and H.E. Stanley, Economic Fluctuations and Diffusion, Phys. Rev. E62 (2000) (Rapid Comm.), R3023 [arXiv:cond-mat/9912051].

- [5] X. Gabaix, P. Gopikrishnan, V. Plerou and H.E. Stanley, A theory of power-law distributions in financial markets, Nature 423 (2003), 267-270

- [6] J.-P. Bouchaud, Y. Gefen, M. Potters and M. Wyart, Fluctuations and response in financial markets: the subtle nature of ”random” price changes, [arXiv:cond-mat/0307332]

- [7] F. Lillo and J.D. Farmer, The long memory of the efficient market, [arXiv:cond-mat/0311053]

- [8] J.D. Farmer, L. Gillemot, F. Lillo, S. Mike and A. Sen, What really causes large price changes?, [arXiv:cond-mat/0312703]

- [9] P. Weber and B. Rosenow, Order book approach to price impact, [arXiv:cond-mat/0311457]

- [10] P. Weber and B. Rosenow, Large stock price changes: volume or liquidity?, [arXiv:cond-mat/0401132]

- [11] P.Clark, A subordinated stochastic process model with finite variance for speculative prices, Econometrica 41 (1973), 135-159

- [12] E. Derman, The Perception of Time, Risk and Return During Periods of Speculation, [arXiv:cond-mat/0201345]

- [13] G. Bonanno, F. Lillo and R.N. Mantegna, Dynamics of the Number of Trades in Financial Sequrities, Physica A 280 (2000), 136-141; [arXiv:cond-mat/9912006]

- [14] M.M. Dracorogna, R. Gencay, U. Muller, R.B. Olsen and O.V. Pictet, An Introduction to High Frequency Finance, Academic Press, 2001

- [15] W. Feller, An Introduction to Probability Theory and Its Applications, Vol. II, Wiley and Sons, 1966

- [16] E. Montroll and M. Shlesinger, The Wonderful World of Random Walks, in Nonequilibrium Phenomena II, From Stochastics to Hydrodynamics, Studies in Statistical Mechanics, North Holland, Amsterdam, 1984

- [17] C. Domb, The Statistics of Correlated Events - I., Phil. Mag. 41 (1950), 969-982.

- [18] E. Scalas, R. Gorenflo and F. Mainardi, Fractional calculus and continuous-time finance, Physoca A284 (2000), 376-384; [arXiv:cond-mat/0001120]

- [19] F. Mainardi, M. Raberto, R. Gorenflo and E. Scalas, Fractional calculus and continuous - time finance II: the waiting - time distribution, Physica A287 (2000), 468-481; [arXiv:cond-mat/0012155]

- [20] M. Raberto, E. Scalas and F. Mainardi, Waiting-times and returns in high-frequency financial data: and empitical study, Physica A314 (2002), 749-755; [arXiv:cond-mat/0203596]

- [21] J. Masoliver, M. Montero and G.H. Weiss, A continuous time random walk model for financial distributions, [arXiv:cond-mat/0210513]

- [22] J. Masoliver, M. Montero, J. Perello amd G. Weiss, The CTRW in finance: Direct and inverse problem, [arXiv:cond-mat/0308017]

- [23] E. Scalas, R. Gorenflo, F. Mainardi, M. Mantelli and M. Raberto, Anomalous waiting times in high-frequency financial data, [arXiv:cond-mat/0310305]

- [24] P. Repetowicz and P. Richmond, Modeling of waiting times and price changes in currency exchange data, [arXiv:cond-mat/0310351]

Appendix A Derivation of Eq. (3)

In this Appendix we sketch, following [17], the derivation of Eq. (3). The probability of having trades in the interval is conviniently written as a convolution of a probability of having trades in the interval (the -th trade falling into the infinitesimal vicinity of ) and a probability of having no trades in the remaining interval :

| (A.1) |

so that the Laplace transform of reads

| (A.2) |

where we took into account that in the considered unit memory depth case all probabilities in question are fully determined by the intertrade (waiting) time distribution , so that 555Here we assume that there is always a first trade at the beginning of the time interval in question and, for we have, recalling that , .

To compute the moments of trade’s multiplicity distribution it is convenient to introduce a generating function

| (A.3) |

so that the moments are given by its derivatives at the origin

| (A.4) |