Wavelet Correlation Coefficient of ’strongly correlated’ financial time series

Ashok Razdan

Nuclear Research Laboratory

Bhaba Atomic Research Centre

Trombay, Mumbai- 400085

Abstract :

In this paper, wavelet concepts are used to study two ’strongly correlated’ financial time series. Apart from obtaining wavelet spectra, We also calculate wavelet correlation coefficient and show that strong correlation or strong anti-correlation depends on scale.

Introduction:

In recent times lot of activity has been witnessed in the the field of econophysics [ 1]. Various concepts and methods of Physics and Mathematics have been applied to study financial time series both for long range and short range studies. The probability distribution function for money has been found to follow Boltzman Gibbs laws displaying typical equilibrium state of maximum entropy [2]. It has been found that financial time series (like stock indices, currency exchange rates etc) have either fractal or multi-fractal features [3,4 and references therein]. Earlier it was assumed that stock market returns follow random walk model and indices are normally distributed [5]. However, it been proved in recent times that indices are not normally distributed but have higher peaks and fatter tails [6,7,8]. Such distributions are known as stable paretians which have infinite or undefined variance. The presence of fatter tails indicate memory effects which arise due to non-linear stochastic processes. Another important feature that has been observed in recent times is that stock market indices can be represented by fractional Brownian motion instead of classical Brownian motion [3]. The similarity between fluid turbulence and financial markets is well known[ 9 ,10 ]. The information transfer in financial markets is similar to energy flow in hydrodynamics [ 11].

Correlation studies in Indian stock markets:

The cross-correlation coefficient r which is a measure of linear association between two variables is defined as

| (1) |

A positive value of coefficient r indicates, that as one value increases the other tends to increase whereas a negative value indicates as one variable increases the other tends to decrease.

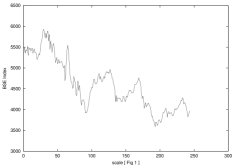

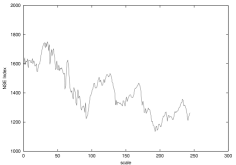

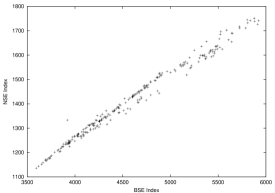

In this paper we study correlation between Bombay stock exchange Index ( BSE) and National stock exchange index (NSE). Both of these stock exchanges belong to India and open and close at the same time i.e. they are synchronous. BSE index and NSE index are known to be strongly correlated. Bombay stock exchange is the oldest stock exchange in whole of Asia. It was started in the year 1875. BSE index is market capitalization weighted index of 30 stocks of sound Indian and multinational companies. National stock exchange was established to provide access to investors from all across India. NSE started equity operations in November 1994 and operations in derivatives in June 2000. NSE index also known as NIFTY is determined from 50 stocks of companies taken from 23 sectors of economy. Figure 1 shows BSE index and NSE index for the year 2000. It is clear from figure 1 that BSE and NSE indices are very similar and correlated. The calculated value of correlation coefficient ( equation 1) between BSE and NSE indices is r =0.993100822. This value of r also indicates that BSE index is strongly correlated with NSE index. This is also evident from figure 2 which shows BSE and NSE indices highly correlated.

In recent times wavelets have been used to quantify various parameters in various scales. In this paper we use wavelet based correlation coefficient to study correlation between Bombay stock exchange Index ( BSE) and National stock exchange index (NSE).

Wavelet correlation coefficient:

Wavelet analysis is being used increasingly to study given structures in different scales [12,13,14]. Wavelets can detect both the location and a scale of a structure. Wavelets are parameterized both by scale a 0 (dilation parameter) and a translation parameter b such that

| (2) |

The wavelet domain of one dimensional function is rather two dimensional in nature; one dimension corresponds to scale and other to translation. The continuous wavelet transform for one dimensions is defined as

| (3) |

where a is the scale. Here f(x) is one dimensional function and (* is complex conjugate) is the analyzing wavelet or also known as mother wavelet. We choose a Mexican hat wavelet as a possible analyzing wavelet [20]

| (4) |

Mexican wavelet is an isotropic wavelet having minimum number of oscillations. An important property of wavelet to be used as analyzing wave,it must have zero mean value i.e. dx=0. is also required to be orthognal to some lower order polynomials i.e.

| (5) |

where . Here n is the upper limit related to the order of wavelet.

A wavelet transform is the inner-product of the function with scaled and translated wavelet. A wavelet transform decomposes a given function into coefficients from which original function can be reconstructed. By using equation (3) wavelet spectrum can be defined as [15]

| (6) |

Wavelet spectrum has a power law behavior

| (7) |

Wavelet spectrum M(a) defines energy of wavelet coefficients for scale ’ a’. Here is an exponent, value of which is decided by power of a. Wavelet cross-correlation coefficient has been defined as [25]

| (8) |

The relationship between correlation coefficient and wavelet correlation coefficient can be written as

| (9) |

The concept of wavelet correlation coefficient has been applied to study scale dependence in various galaxies [15].

Results and Discussion:

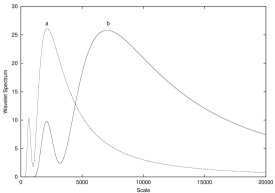

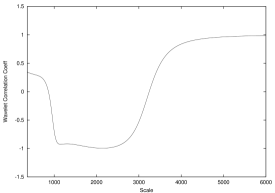

In figure 3 we have plotted wavelet spectra of BSE (figure a) and NSE (figure b) indices. The wavelet spectra of two indices have similar features. Both spectra have two maxima and one minima. Maxima of both spectra corresponds to maximum values of indices and minimum in the spectra corresponds to a value which is difference between maximum and minimum of indices. Figure 4 displays wavelet cross correlations of BSE and NSE indices. It is evident from this figure that for smaller scales (i.e. between 1000 and 2700 approximately )the indices have negative correlation. Very strong anti-correlation corresponds to value of 2100. This scaling value of 2100 corresponds to difference between average value of BSE index and average value of NSE index.

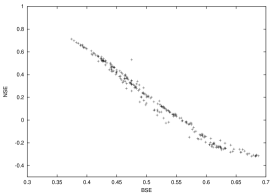

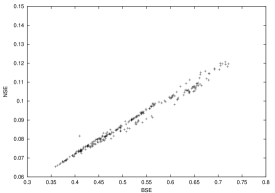

In figure 5 we have plotted wavelet coefficient w of BSE and NSE indices for scaling value of 2000. Figure 6 has been obtained by plotting wavelet coefficient of BSE and NSE index for scaling value of 6000. From figure 5 it is clear that data scatter corresponds to highly anti-correlated value and in figure 6 data scatter depicts strong correlated value. While in figure 2 data scatter represents classical picture of correlated scatter but in figures 5 and 6 wavelet coefficients corresponding to BSE and NSE indices have been plotted and represent anti-correlated scatter and correlated scatter respectively. Figures 5 and 6 confirm the observations made from figure 3 that BSE and NSE indices can be highly correlated or less correlated or anti-correlated depending on scale.

Studies involving relationships between various stock exchanges have become important because of globalization. It is very complex problem to study influences and links between various stock exchanges because stock exchanges world over open and close at different times and each individual stock exchange, trades in portfolios which may be unique to its local economy and nature of currency involved is also different. Yet it has been possible to [16] to study taxonomy of various stock indices. It has been shown that open-closure return of New York stock exchange at day t and open-closure return of Tokyo stock exchange at day t+1 are strongly correlated [17]. A detailed study involving quasi-synchronous correlation coefficient between indices of various markets in the world have been done to evolve hierarchical tree [16]. Using correlation coefficient Mantegna et al [6,18] have studied minimum spanning tree of economical data. From MST it is possible to obtain ultra metric space and hierarchy of various indices. MST approach has been earlier used to describe various complex systems like spin glass etc. MST results have shown that portfolios of technology ,software ,energy, food etc form clusters and each cluster turns out to be branch of MST tree [18] and this clustering sometimes extends even to global scale. Vandewalla et al [19] extended this studies by investigating specific topology of financial MST where it has been shown that markets follow critical self organized topology. This hierarchical structure is believed to result in cascade of information and clusters of buy-sell orders [20,21] and sometimes to crashes [22]. It has been shown that tree length shrinks during a stock market crisis [23].The time dependent properties of minimum spanning tree gives deep insights in market dynamics [24] because markets have been characterized as evolving complex system [25].

Correlation coefficient forms an important input to study taxonomy, MST or time dependent dynamics of markets. All such studies have been carried out using equation (1) which characterizes data at global level. But interest lies in studying correlation ratio from one scale to another scale which has been achieved by defining wavelet based correlation coefficient. By using wavelet scale dependent correlation ratio it may be interesting to study taxonomy, MST etc. which may give further insights in market dynamics.

Conclusions:

By using wavelet concepts in this paper, we have shown that correlation between BSE and NSE indices is scale dependent. They are strongly correlated or less correlated or strongly anti-correlated depending on scale.

References:

-

1.

N.Vandewalle, M. Ausloos in Econophysics -an Emerging Sciences Edited by J.Kertesz,I.Kondor (Kluwer,Dordrecht 1999 Edition)

-

2.

V.M.Yakovenko, cond-mat/0302270,13feb 2003

-

3.

Ashok Razdan,Pramana -Journal of Physics 58(2002)537

-

4.

M. Ausloos and K.Ivanova, cond-mat/0108394,24 aug 2001

-

5.

E.F.Femma, J.Finance (1970) 383-417

-

6.

R.N.Mantegna, H.E. Stanely , An Introduction to Econophysics Cambridge University Press ,2000.

-

7.

E.E.Peters, Chaos and Order in Capital Markets, Wiley,New York,1991

-

8.

E.E.Peters, Fractal Market Analysis,Wiley,New York,1994

-

9.

S.Ghashghaie, W.Breymann,J.Pineke, P.Talkner and Y.Dodge, Nature 381(1996)767

-

10.

R.N.Mantegna and H.Stanley, Nature 383(1996)587

-

11.

N.Vandewalle and M.Ausloos, Physica A 246(1997)454

-

12.

I.Daubechies,Commun. Pure Appl. Math., 41(1988)909

-

13.

I.Daubechies , Ten Lectures in Wavelets 1992, Vol 61 CBMS-NSF series in Applied Mathematics

-

14.

A.Razdan,A.Haungs,H.Rebel and C.L.Bhat, Astroparticle Physics 17(2002)497, Astroparticle Physics 12(1999)145

-

15.

P.Frick, R.Bcek, E.M.Berkhuijsen and I.Patrickeyev, Astro-ph/0109017,3 sept 2001

-

16.

G.Bonanno, N.Vandewalle,R.N.Mantegna ,cond-mat/0001268 11 aug 2000

-

17.

K.G.Becker,J.E.Finnerty and M.Gupta, Journal of Finance XLV (1990)1297

-

18.

R.N.Mantegna, Eur. Phys. J B 11(1999)193

-

19.

N.Vandewalle , F.Brisbois and X. Tordoir ,cond-mat/0009245 16 sept 2000

-

20.

A. Arneodo ,J.F.Muzy and D.Sornette, Eur.J Phys. B 2(1998)277

-

21.

M.Pasquini and M.Serva, Eur. J.Phys. B 16(2000)195

-

22.

E.Canessa , J. Phys. A: Math. Gen. 33(2000)3637

-

23.

J.-P.Onnela, A. Chakraborti,K.Kaski and J.Kertesz,cond-mat/0212037,2 Dec 2002

-

24.

J.-P.Onnela, A. Chakraborti,K.Kaski,J.Kertesz and A.Kanto,cond-mat/0302546,26 Feb2003

-

25.

W.B.Arthur,S.N.Durlauf and D.A.Lane (eds.), The economy as an evolving complex sustem II, Addison Wesley (1997)