Collective Origin of the Coexistence of Apparent RMT Noise

and Factors

in Large Sample Correlation Matrices

Abstract

Through simple analytical calculations and numerical simulations, we demonstrate the generic existence of a self-organized macroscopic state in any large multivariate system possessing non-vanishing average correlations between a finite fraction of all pairs of elements. The coexistence of an eigenvalue spectrum predicted by random matrix theory (RMT) and a few very large eigenvalues in large empirical correlation matrices is shown to result from a bottom-up collective effect of the underlying time series rather than a top-down impact of factors. Our results, in excellent agreement with previous results obtained on large financial correlation matrices, show that there is relevant information also in the bulk of the eigenvalue spectrum and rationalize the presence of market factors previously introduced in an ad hoc manner.

Since Wigner’s seminal idea to apply random matrix theory (RMT) to interpret the complex spectrum of energy levels in nuclear physics Wigner , RMT has made enormous progress Mehta with many applications in physical sciences and elsewhere such as in meteorology SP01 and image processing SM . A new application was proposed a few years ago to the problem of correlations between financial assets and to the portfolio optimization problem. It was shown that, among the eigenvalues and principal components of the empirical correlation matrix of the returns of hundreds of asset on the New York Stock Exchange (NYSE), apart from the few highest eigenvalues, the marginal distribution of the other eigenvalues and eigenvectors closely resembles the spectral distribution of a positive symmetric random matrix with maximum entropy, suggesting that the correlation matrix does not contain any specific information beyond these few largest eigenvalues and eigenvectors Laloux . These results apparently invalidate the standard mean-variance portfolio optimization theory Marco consecrated by the financial industry riskmetrics and seemingly support the rationale behind factor models such as the capital asset pricing model (CAPM) CAPM and the arbitrage pricing theory (APT) APT , where the correlations between a large number of assets are represented through a small number of so-called market factors. Indeed, if the spectrum of eigenvalues of the empirical covariance or correlation matrices are predicted by RMT, it seems natural to conclude that there is no usable information in these matrices and that empirical covariance matrices should not be used for portfolio optimization. In contrast, if one detects deviations between the universal – and therefore non-informative – part of the spectral properties of empirically estimated covariance and correlation matrices and those of the relevant ensemble of random matrices, this may quantify the amount of real information that can be used in portfolio optimization from the “noise” that should be discarded.

More generally, in many different scientific fields, one needs to determine the nature and amount of information contained in large covariance and correlation matrices. This occurs as soon as one attempts to estimate very large covariance and correlation matrices in multivariate dynamics of systems exhibiting non-Gaussian fluctuations with fat tails and/or long-range time correlations with intermittency. In such cases, the convergence of the estimators of the large covariance and correlation matrices is often too slow for all practical purposes. The problem becomes even more complex with time-varying variances and covariances as occurs in systems with heteroskedasticity Engle or with regime-switching regimeswitch . A prominent example where such difficulties arise is the data-assimilation problem in engineering and in meteorology where forecasting is combined with observations iteratively through the Kalman filter, based on the estimation and forward prediction of large covariance matrices Kalman .

As we said in the context of financial time series, the rescuing strategy is to invoke the existence of a few dominant factors, such as an overall market factor and the factors related to firm size, firm industry and book-to-market equity, thought to embody most of the relevant dependence structure between the studied time series fama . Indeed, there is no doubt that observed equity prices respond to a wide variety of unanticipated factors, but there is much weaker evidence that expected returns are higher for equities that are more sensitive to these factors, as required by Markowitz’s mean-variance theory, by the CAPM and the APT Roll . This severe failure of the most fundamental finance theories could conceivably be attributable to an inappropriate proxy for the market portfolio, but nobody has been able to show that this is really the correct explanation. This remark constitutes the crux of the problem: the factors invoked to model the cross-sectional dependence between assets are not known in general and are either postulated based on economic intuition in financial studies or obtained as black box results in the recent analyses using RMT Laloux .

Here, we show that the existence of factors results from a collective effect of the assets, similar to the emergence of a macroscopic self-organization of interacting microscopic constituents. For this, we unravel the general physical origin of the large eigenvalues of large covariance and correlation matrices and provide a complete understanding of the coexistence of features resembling properties of random matrices and of large “anomalous” eigenvalues. Through simple analytical calculations and numerical simulations, we demonstrate the generic existence of a self-organized macroscopic state in any large system possessing non-vanishing average correlations between a finite fraction of all pairs of elements.

Let us first consider a large system of size with correlation matrix in which every non-diagonal pairs of elements exhibits the same correlation coefficient for and . Its eigenvalues are

| (1) |

with multiplicity and with in order for the correlation matrix to remain positive definite. Thus, in the thermodynamics limit , even for a weak positive correlation (with ), a very large eigenvalue appears, associated with the delocalized eigenvector , which dominates completely the correlation structure of the system. This trivial example stresses that the key point for the emergence of a large eigenvalue is not the strength of the correlations, provided that they do not vanish, but the large size of the system.

This result (1) still holds qualitatively when the correlation coefficients are all distinct. To see this, it is convenient to use a perturbation approach. We thus add a small random component to each correlation coefficient:

| (2) |

where the coefficients have zero mean, variance and are independently distributed (There are additional constraints on the support of the distribution of the ’s in order for the matrix to remain positive definite with probability one). The determination of the eigenvalues and eigenfunctions of is performed using the perturbation theory developed in quantum mechanics cohen up to the second order in . We find that the largest eigenvalue becomes

| (3) |

while, at the same order, the corresponding eigenvector remains unchanged. The degeneracy of the eigenvalue is broken and leads to a complex set of smaller eigenvalues described below.

In fact, this result (3) can be generalized to the non-perturbative domain of any correlation matrix with independent random coefficients , provided that they have the same mean value and variance . Indeed, it has been shown FK81 that, in such a case, the expectations of the largest and second largest eigenvalues are

| (4) | |||||

| (5) |

Moreover, the statistical fluctuations of these two largest eigenvalues are asymptotically (for large fluctuations ) bounded by a Gaussian distribution according to the following large deviation theorem

| (6) |

for some positive constant KV00 .

This result is very different from that obtained when the mean value vanishes. In such a case, the distribution of eigenvalues of the random matrix is given by the semi-circle law Mehta . However, due to the presence of the ones on the main diagonal of the correlation matrix , the center of the circle is not at the origin but at the point . Thus, the distribution of the eigenvalues of random correlation matrices with zero mean correlation coefficients is a semi-circle of radius centered at .

The result (4) is deeply related to the so-called “friendship theorem” in mathematical graph theory, which states that, in any finite graph such that any two vertices have exactly one common neighbor, there is one and only one vertex adjacent to all other vertices Erdos . A more heuristic but equivalent statement is that, in a group of people such that any pair of persons have exactly one common friend, there is always one person (the “politician”) who is the friend of everybody. The connection is established by taking the non-diagonal entries () equal to Bernouilli random variable with parameter , that is, and . Then, the matrix , where is the unit matrix, becomes nothing but the adjacency matrix of the random graph KV00 . The proof of Erdos of the “friendship theorem” indeed relies on the -dependence of the largest eigenvalue and on the -dependence of the second largest eigenvalue of as given by (4) and (5).

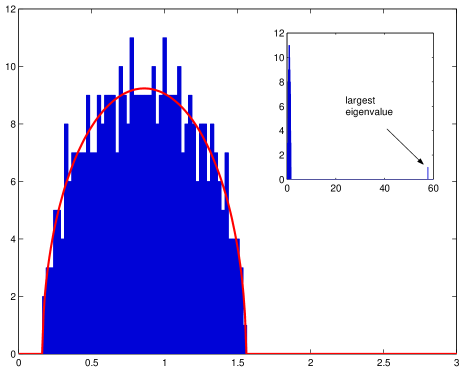

Figure 1 shows the distribution of eigenvalues of a random correlation matrix. The inset shows the largest eigenvalue lying at the predicting size , while the bulk of the eigenvalues are much smaller and are described by a modified semi-circle law centered on , in the limit of large . The result on the largest eigenvalue emerging from the collective effect of the cross-correlation between all pairs provides a novel perspective to the observation Rollcrash that the only reasonable explanation for the simultaneous crash of 23 stock markets worldwide in October 1987 is the impact of a world market factor: according to our demonstration, the simultaneous occurrence of significant correlations between the markets worldwide is bound to lead to the existence of an extremely large eigenvalue, the world market factor constructed by … a linear combination of the 23 stock markets! What our result shows is that invoking factors to explain the cross-sectional structure of stock returns is cursed by the chicken-and-egg problem: factors exist because stocks are correlated; stocks are correlated because of common factors impacting them.

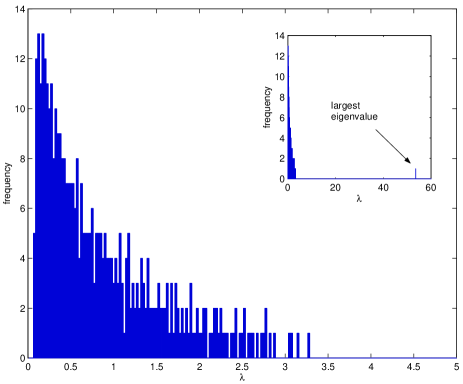

Figure 2 shows the eigenvalues distribution of the sample correlation matrix reconstructed by sampling time series of length generated with a given correlation matrix with theoretical spectrum shown in figure 1. The largest eigenvalue is again very close to the prediction while the bulk of the distribution departs very strongly from the semi-circle law and is not far from the Wishart prediction, as expected from the definition of the Wishart ensemble as the ensemble of sample covariance matrices of Gaussian distributed time series with unit variance and zero mean. A Kolmogorov test shows however that the bulk of the spectrum is not in the Wishart class, in contradiction with previous claims lacking formal statistical tests Laloux . This result holds for different simulations of the sample correlation matrix and different realizations of the theoretical correlation matrix with the same parameters (, ). The statistically significant departure from the Wishart prediction implies that there is actually some information in the bulk of the spectrum of eigenvalues, which is intimately coupled with the existence of the largest eigenvalue. We have also checked that these results remain robust for non-Gaussian distribution of returns as long as the second moments exist. Indeed, correlated time series with multivariate Gaussian or Student distributions with three degrees of freedom (which provide more acceptable proxies for financial time series Gopikrishnan ) give no discernible differences in the spectrum of eigenvalues. This is surprising as the estimator of a correlation coefficient is asymptotically Gaussian for time series with finite fourth moment and Lévy stable otherwise MS2 .

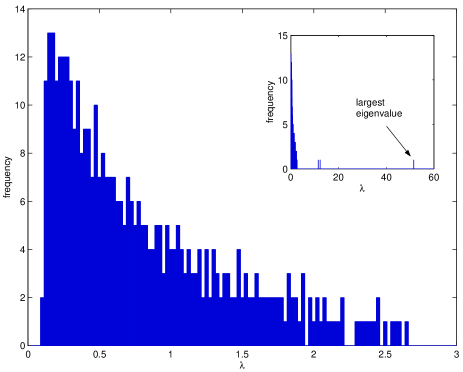

Up to now, we have focused on the collective mechanism at the origin of the very large eigenvalue of order . Empirically Laloux , a few other eigenvalues have an amplitude of the order of that deviate significantly from the bulk of the distribution. These eigenvalues cannot be obtained by a matrix of the form (2) with identically independently distributed coefficients ’s. Our analysis provides a very simple constructive mechanism for them. The solution consists in considering, as a first approximation, the block diagonal matrix with diagonal elements made of the matrices of sizes with , constructed according to (2) such that each matrix has the average correlation coefficient . When the coefficients of the matrix outside the matrices are zero, the spectrum of is given by the union of all the spectra of the ’s, which are each dominated by a large eigenvalue . The spectrum of then exhibits large eigenvalues.

Each block can be interpreted as a sector of the economy, including all the companies belonging to a same industrial branch and the eigenvector associated with each largest eigenvalue represents the main factor driving this sector of activity Mantegnapath . For similar sector sizes and average correlation coefficients , the largest eigenvalues are of the same order of magnitude. In order to recover a very large unique eigenvalue, we reintroduce some coupling constants outside the block diagonal matrices. A well-known result of perturbation theory in quantum mechanics states that such coupling leads to a repulsion between the eigenstates, which can be observed in figure 3 where has been constructed with three block matrices , and and non-zero off-diagonal coupling described in the figure caption. These values allow us to quantitatively replicate the empirical finding of Laloux et al. in Laloux , where the three first eigenvalues are approximately , and . The bulk of the spectrum (which excludes the three largest eigenvalues) is similar to the Wishart distribution but again statistically different from it as tested with a Kolmogorov test. There is thus significant deviation from the predictions of RMT not only for the largest eigenvalues but also in the bulk.

As a final remark, expressions (3,4) and our numerical tests for a large variety of correlation matrices show that the delocalized eigenvector , associated with the largest eigenvalue is extremely robust and remains (on average) the same for any large system. Thus, even for time-varying correlation matrices – as in finance with important heteroskedastic effects – the composition of the main factor remains almost the same. This can be seen as a generalized limit theorem reflecting the bottom-up organization of broadly correlated time series.

This work was partially supported by the James S. Mc Donnell Foundation 21st century scientist award/studying complex system.

References

- (1) Wigner, E.P., Ann. Math. 53, 36 (1951).

- (2) Mehta, M.L., Random matrices, 2nd ed. (Boston: Academic Press, 1991).

- (3) Santhanam, M.S. and P. K. Patra, Phys. Rev. E 64, 016102 (2001).

- (4) Setpunga, A.M. and P.P. Mitra, Phys. Rev E 60, 3389 (1999).

- (5) Laloux, L. et al., Phys. Rev. Lett. 83, 1467 (1999); Plerou, V., et al., Phys. Rev. Lett. 83, 1471 (1999); Phys. Rev. E; Maslov, S., Physica A 301, 397 (2001); Plerou, V. et al., Phys. Rev E 6506 066126 (2002).

- (6) Markowitz, H., Portfolio selection: Efficient diversification of investments (John Wiley and Sons, New York, 1959).

- (7) RiskMetrics Group, RiskMetrics (Technical Document, NewYork: J.P. Morgan/Reuters, 1996).

- (8) Sharpe, W.F., J. Finance (September), 425 (1964); Lintner, J., Rev. Econ. Stat. (February), 13 (1965); Mossin, J., Econometrica (October), 768 (1966); Black, F., J. Business (July), 444 (1972).

- (9) Ross, S.A., J. Economic Theory (December), 341 (1976).

- (10) Engle, R.F. and K. Sheppard, NBER Working Paper No. W8554 (2001).

- (11) Schaller, H. and van Norden, S., Appl. Financial Econ. 7, 177 (1997).

- (12) Brammer, K., Kalman-Bucy filters (Gerhard Siffling, Norwood, MA: Artech House, 1989).

- (13) Fama, E.F. and Kenneth R., J. Finance 51, 55 (1996); J. Financial Econ. 33, 3 (1993); Fama, E.F. et al., Financial Analysts J. 49, 37 (1993).

- (14) Roll, R., Financial Management 23, 69 (1994).

- (15) Cohen-Tannoudji, C., B. Diu and F. Laloe, Quantum mechanics (New York: Wiley, 1977).

- (16) Fr̈edi Z. and J. Komlós, Combinatorica 1, 233-241 (1981).

- (17) Krivelevich, M. and V. H. Vu, math-ph/0009032 (2000).

- (18) Erdos, P. et al., Studia Sci. Math. 1, 215 (1966).

- (19) R. Roll, Financial Analysts J. 44, 19 (1988).

- (20) Gopikrishnan, P. et al., Eur. Phys. Journal B 3̱, 139 (1998); Guillaume, D.M., et al., Finance and Stochastics 1, 95 (1997); Lux, L., Appl. Financial Economics 6, 463 (1996); Pagan, A., J. Emp. Fin. 3, 15 (1996).

- (21) Davis, R.A. and J.E. Marengo, Commun. Statist.-Stochastic Models 6, 483 (1990); Meerschaert, M.M. and H.P. Scheffler, J. Time Series Anal. 22, 481 (2001).

- (22) Mantegna, R.N., Eur. Phys. J. 11, 193 (1999); Marsili, M., Quant. Fin. 2, 297 (2002).