Statistical properties of the Jakarta and Kuala Lumpur stock exchange indices before and after crash

Abstract

Using the tools developed for statistical physics, we simultaneously analyze statistical properties of the Jakarta and Kuala Lumpur Stock Exchange indices. In spite of the small number of data used in the analysis, the result shows the universal behavior of complex systems previously found in the leading stock indices. We also analyze their features before and after the financial crisis. We found that after the crisis both stocks do not show a same statistical behavior. The impact of currency controls is observed in the distribution of index returns.

pacs:

05.40.Fb, 05.45.Tp, 89.90.+nI Introduction

Recently, there have been considerable efforts to analyze financial data by means of methods developed for statistical physics canning1998 ; mills2000 ; raberto ; liu1999 ; gopi2000 ; mantegna1995 ; mantegna1999 ; plerou1999 ; gopi1999 ; lillo1999 ; lillo2000a ; johansen1998 ; bonanno1999 ; wang2001 . Motivated by the scientific challenge to understand the nature of complex systems, physicists have started to direct their attentions to a huge, and also growing amount of economics data recorded minutes by minutes for decades. Among these interesting data, the fluctuation of stock exchange indices is of special interest, since it might indirectly reflect the economic situation in a certain region and some people happily speculate their money on it. Furthermore, the advancement in computing capabilities has enabled them to handle a large amount of data, unlike almost 40 years ago when Mandelbrot investigated approximately 2000 data points of cotton prices mandelbrot .

It is then expected that such studies could explain the nature of interacting elements in the complex system and, therefore, could help to forecast economic fluctuations in the future. In other words, these studies were intended to produce new results in economics, which might help us to avoid economic “earthquakes” such as what happened in Indonesia a few years ago stanley2000 .

Previous studies in this subject so far have focused only on the long-term behavior of the leading stock indices. This is understandable, since to statistically investigate the universal features in economic activities one has to have a large amount of data. Very little attentions are given to investigate what happen to the stock markets in developing countries (e.g., Indonesia) as well as what happen to the stock indices before, during, and after a financial (or monetary) crash, although in the latter the most important ingredients of the financial market or economic fluctuation could exist lillo1999 ; lillo2000a ; johansen1998 .

It is the objective of this paper to study the general statistical properties of the fluctuation in stock indices in two developing countries, as well as their properties before and after a financial crashes. This study is important in order to investigate the extent of the universality of complex behavior found previously in the leading stock indices, such as S&P 500 and NYSE. Such investigation will naturally shed important information on the variation of the universal constants in the scaling behavior of the stock index. With this information at hand it is then possible to identify the statistical properties that quantify different behaviors in stock markets and those which indicate a crash or stable condition. For this purpose we take two different indices, the Jakarta Stock Exchange Index (abbreviated with IHSG, an acronym of Indeks Harga Saham Gabungan or composite stock exchange price index) and the Kuala Lumpur Stock Exchange index (KLSE), which belong to different countries. Comparing the two indices would be very interesting since both Indonesia and Malaysia underwent the same monetary crisis in 1997, which are then followed by financial crashes in almost all economic sectors, but with quite different economic situations. As has been often discussed, the behavior of two stock indices could be very different although the two stock markets are situated in the same region.

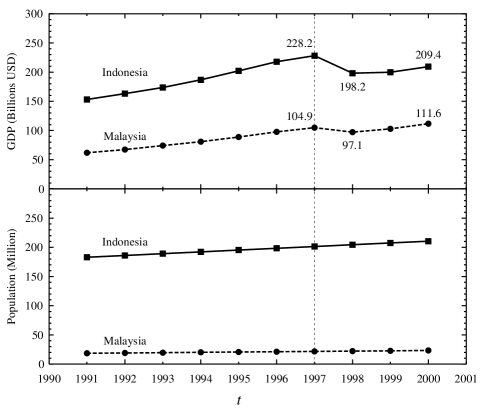

Before proceeding to the analysis, it is worth to glance at the Indonesian and Malaysian Gross Domestic Products (GDP) shown in Fig. 1. Before the crisis the growth rate of the Indonesian GDP seems to be faster than that of Malaysian GDP. The monetary crisis in 1997 has a clear impact on both GDPs. Nevertheless, the impact on Indonesian GDP is more obvious. After the crisis, Malaysia was rather successful to stabilize its economic situation and did not accept the International Monetary Fund (IMF) prescription. Three years after that Malaysia was able to put its GDP slightly above the previous value in 1997. On the other hand, Indonesia was unable to stop the declination of Rupiah against US Dollar and decided to ask the IMF to help stabilizing its monetary condition. Other crises, which followed the monetary crisis, are blamed as the reasons of this.

II General Properties

II.1 Time Series and Index Returns

In our analysis we investigate the daily index returns, which are defined as

| (1) | |||||

with indicates the closing index of the stock at day . Some previous studies mantegna1995 ; mantegna1999 are performed with the return defined as the difference in the index, instead of the difference in the logarithm of index as given by Eq. (1). However, in our analysis we found that the results of calculations by using both methods do not differ significantly.

The available data for the IHSG index are the daily closing index data recorded from January 1988 to April 2002 which consist of 3526 data points. The KLSE data contain also the daily closing index starting from December 1993 and ending with June 2002, which comprise totally 2104 data points. The number of data in both indices seems to be the first obstacle in this analysis, since compared with the previous analysis on the S&P 500 index, e.g. Ref. gopi1999 , which used approximately data points, the number turns out to be extremely small. However, as shown by Mandelbrot in his analysis on the cotton prices, even with about 2000 data points it is still possible to extract a quantitative conclusion from the data.

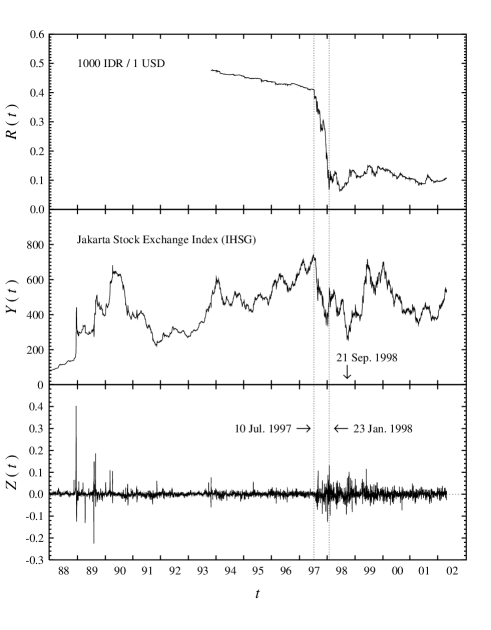

Figure 2 shows the time series of the IHSG index along with the logarithmic returns calculated by using Eq. (1). It is naturally difficult to define when exactly the crisis (or crash) started and when it finished. To get around this difficulty, in Fig. 2 we also display the historical time series of the exchange rate between 1000 Indonesian Rupiah and 1 US Dollar, since the economic crash started with the decline of this rate. The available data do not fill the entire range, nevertheless they are sufficient to locate the period of the crisis. It should be noted that before the monetary crisis the government intervention on this exchange rate was very strong and as a consequence, although the Rupiah was not pegged to US Dollar with a fixed rate, the fluctuation in the exchange rate was relatively tiny.

In Fig. 2 we indicate the period when Rupiah started to continuously drop (10th July 1997) until it reached the minimum point (23rd January 1998). The IHSG index also dropped significantly during this period. However, the index continued to strongly fluctuate and reached another minimum about one year later due to the unfortunate political situation. The same phenomenon also happened in the foreign exchange rate, though with a different scale. In view of this, according to the IHSG index, the duration of financial crisis could be longer than one year.

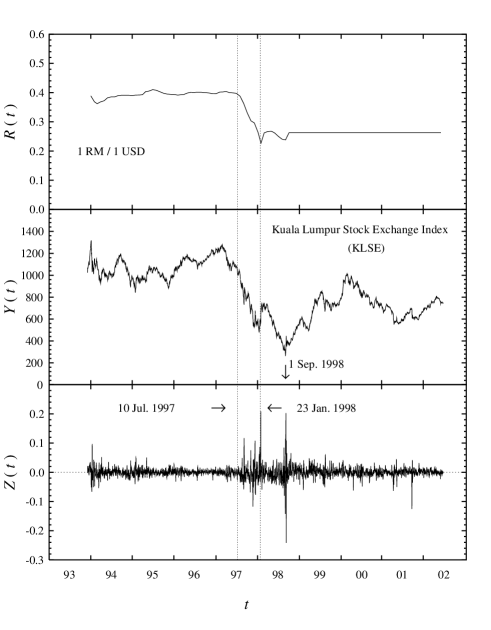

Figure 3 displays the historical time series of the KLSE index along with their logarithmic returns and the ratio between 1 Malaysian Ringgit and 1 US Dollar. Coincidentally, our definition of the crash period fits nicely with the latter. As in the case of IHSG, the KLSE index also significantly dropped during this period. The difference between Indonesian and Malaysian foreign exchange rate is, nevertheless, apparent here, since on 1st September 1998 Malaysia imposed currency controls, the Ringgit was pegged with US Dollar with a fixed rate of 3.80 Ringgit per Dollar, while Indonesia was unable to do that due to the multi-crisis that simultaneously occurred in this country. From Fig. 3 it is not clear whether or not such policy helped to elevate the KLSE index, since comparing with the IHSG fluctuation in Fig. 2 the two indices seem to be strongly correlated, thus other external factors could be more relevant to explain the improvement in the KLSE index. In fact, Ref. muniandy2001 claims that the policy has led to a misposition of the Ringgit relative to its realistic exchange rate. During 1999 the Ringgit was overvalued since the regional currencies such as Japan Yen and Singapore Dollar have all depreciated against US Dollar. As a consequence, Malaysian export became less competitive and eventually this policy led to an economic slowdown in Malaysia.

A quick glance to the index fluctuation in both figures reveals that the fluctuation is more dramatic than that of S&P 500, indicating that in this case the situation is more complex. After the crash the magnitude of returns is obviously larger in both indices, or, in the economics language, the probability to gain or to loose becomes larger than before. In the next section, it will be shown that both indices are clearly more volatile after the crash.

II.2 Scaling the Index Returns

Following previous studies mantegna1995 ; mantegna1999 we investigate the probability density function (PDF or ) of the return to the origin in order to investigate the scaling behavior of the IHSG and KLSE index returns. The advantage of such analysis is obvious, since the number of data included is relatively small, while the probability is largest at , thus reducing the statistical inaccuracies.

Starting with the characteristic function mantegna1999

| (2) |

the Lévy stable distribution is given by

| (3) |

From Eq. (3) the probability of return to the origin reads

| (4) |

where indicates the Gamma function.

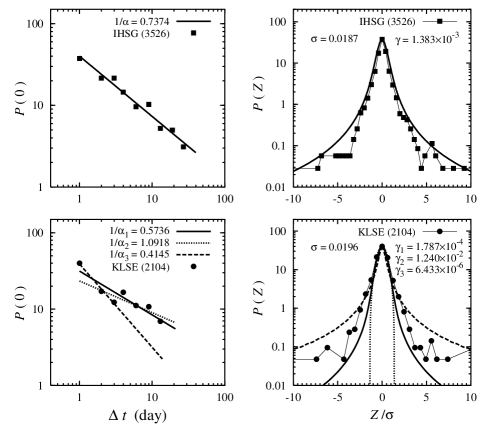

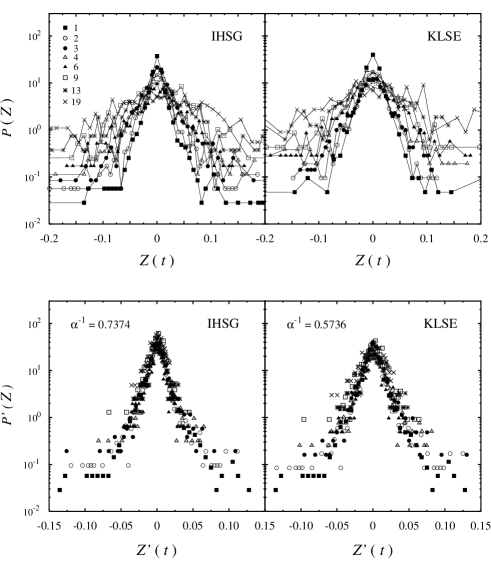

The log-log plots of as a function of the sampling time for both IHSG and KLSE indices are shown in the left panels of Fig. 4. Since the number of data points is relatively small we limit our analysis only up to days for the IHSG index and days for KLSE. In the former (latter) case the number of data points in each set decreases from 3526 (2104) for day to the value of 181 for days (160 for days). These values are already much smaller compared with previous analyses, e.g., for the Hang Seng index wang2001 one ends up with the value of 1481 for minutes.

The slopes of linear regressions to these plots equal the negative inverse of the Lévy stable distribution indices . Using this index we calculate the parameter by means of Eq. (4) and plot the “theoretical” PDF as a function of normalized returns , using Eq. (3), where the standard deviation of the distribution, and compare it with the empirical PDF obtained from data in the right panels of Fig. 4. All relevant parameters obtained in this calculation are displayed in Table 1.

| Properties | IHSG | KLSE | ||

|---|---|---|---|---|

| 1 | 2 | 3 | ||

| Standard deviation | 0.0187 | 0.0196 | 0.0196 | 0.0196 |

| Kurtosis | 81.796 | 29.044 | 29.044 | 29.044 |

| Skewness | 3.3987 | |||

| 1.6020 | 1.4985 | 1.5914 | 1.3691 | |

| 3526 | 2104 | 2104 | 2104 | |

In the IHSG case we obtain (corresponds to ) which is slightly smaller than that of the S&P 500 index obtained from the same analysis mantegna1999 (), or using different approach gopi1999 ( – 3.45). The value is also smaller than the result obtained for Hang Seng index () wang2001 . The value indicates that the central part of the IHSG distribution can be described by a Lévy stable process.

In the KLSE case the situation is rather different as depicted by the bottom panel of Fig. 4. The PDF at zero return shows a cross-over at between 1 and 2 and, as a consequence, as shown by the solid line the linear regression to the points does not lead to a satisfactory result. To clarify this, we use the three first points in the second regression and excluding the data point in the third one. The results are compared with the linear regression to all points in the bottom-left panel of Fig. 4. In the first case we obtain , already close to a Gaussian distribution although still within the Lévy stable index. In the second case the index is smaller, indicating that the distribution for small is far from Gaussian. However, in the third case the distribution is already a Gaussian unstable process. From this result, clearly we can conclude that by slightly increasing the KLSE index does not retain its power law and quickly converges to a Gaussian distribution, in contrast to the IHSG index. The PDF behavior for the three cases is clearly seen in the bottom-right panel of Fig. 4.

The standard deviation is known as the historical volatility in financial literatures and quantifies the risk associated with the corresponding stock lillo2000 . As shown in the first line of Table 1, the KLSE stock is slightly riskier than the IHSG one. The kurtosis measures the relative peakedness of the distribution to a Gaussian one. The PDF of the less capitalized stocks is more leptokurtic than the PDF of the more capitalized ones lillo2000 . From Table 1 we can clearly see that the IHSG stock is less capitalized than KLSE. Finally, the skewness characterizes the degree of asymmetry of the distribution from its mean. A positive value of skewness indicates that the stock delivered more profits along its history, whereas a negative value displays more losses hit the investor. Table 1 reveals that the IHSG stock in general gives more profits than the KLSE one.

Although numerical values given in Table 1 could be interesting, the values become much more important when we discuss the behavior of the stock indices before and after the financial crash in the next section.

To further explore statistical properties of the PDF of index returns we follow Refs. mantegna1995 ; mantegna1999 , i.e. we investigate the stability of the distribution for day. Assuming the central part of the distribution can be described by a Lévy stable distribution, then using the scaling variables

| (5) |

and

| (6) |

the empirical PDFs for different time sampling will collapse onto the distribution.

The results for both indices are displayed in Fig. 5, where we perform the analysis for days. In general the data collapse is evident, especially in the case of IHSG. In the KLSE case we use (result from regression to all empirical in Fig. 4), since the value leads to an average behavior. As Ref. wang2001 has reported, we also find that the extent of data collapse is stronger in the center of the distribution. The existence of a cross-over in the KLSE case is also observed here, the scaled are more scattered than that of the IHSG.

II.3 Moments

Reference gopi1999 has pointed out that the use of the return probability to the origin to estimate the Lévy stable distribution index is statistically not optimal, due to discreteness of the distribution. Instead of exploiting such method, Ref. gopi1999 used a different strategy, i.e. calculating by means of the slope of the cumulative distribution tails in a log-log plot. To further test their results on the scaling behavior, Refs. gopi1999 ; plerou1999 analyzed the moments of the distribution of normalized returns

| (7) |

where the normalized returns is defined by

| (8) |

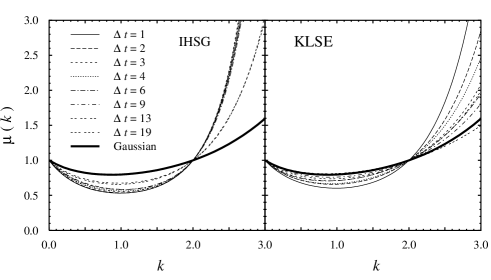

with the time average of over the entire of time series. In the case of the S&P 500 index the result is found to be consistent with the analysis of the tails of cumulative distributions. They pointed out that the change in the moments behavior originates from the gradual disappearance of the Lévy slope in the distribution tails. In our case it is also important to cross-check the results shown in Fig. 4, especially the KLSE slope, which is found to be non-linear in the range of .

It has been shown in Ref. gopi1999 that Eq. (7) will diverge for . In this study we also constrain within . The result for both indices compared with the moment obtained from a Gaussian distribution are shown in Fig. 6. Obviously the results are consistent with our previous analysis, the IHSG moment retains its scaling up to days, only after the moment starts to deviate toward the Gaussian distribution. In the KLSE case the moment quickly converges to the Gaussian distribution as increases from 1 day and does not show any scaling behavior as in the former case.

II.4 Correlation in the stock index

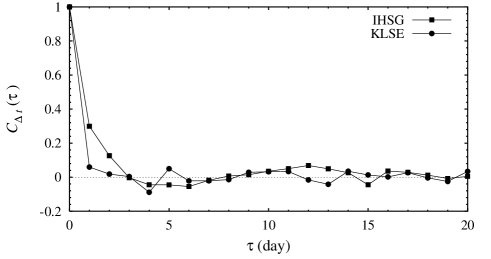

Another interesting behavior of the stock index fluctuation is its short and long time memories which are usually expressed in terms of the autocorrelation. Understanding the power law in the correlation is very helpful in selecting the appropriate model or mechanism to explain the fluctuation process. In Ref. gopi1999 it has been shown that the autocorrelation function of the S&P 500 returns exhibits an exponential decay with a characteristic decay time of approximately 4 minutes, whereas the absolute value of index returns shows a scaling behavior with a power-law exponent of 0.3. In our case it is of course difficult to study such behavior since both indices are recorded daily. However, a qualitative comparison between the two indices might help us to probe the differences in the two stocks.

Following Ref. gopi1999 the autocorrelation function is defined as

| (9) |

where indicates the time lag. The result for short-range autocorrelation is depicted in Fig. 7, where we can observe that the IHSG stock is slightly more correlated than the KLSE one. This result is certainly consistent with the analysis of the scaling and moments behavior. The fluctuation in the KLSE index seems to be more random than that of IHSG, as can be seen also in Fig. 6.

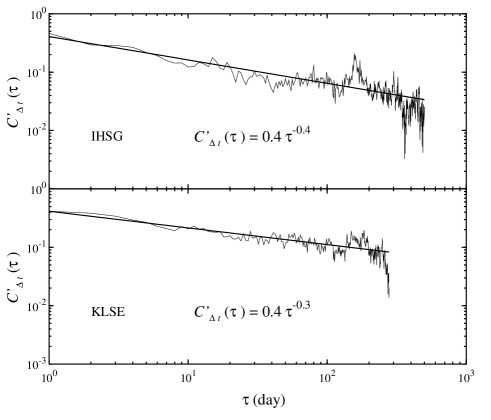

The long-range autocorrelation function obtained by calculating the absolute value of the return in Eq. (9) is shown in Fig. 8. The absolute value of index returns from both stocks show a long-range power law behavior with a time scale up to almost one year. The only difference is observed in the power exponent of the scaling, the IHSG correlation falls off faster than the KLSE one. This is, however, in contrast to their short-range correlation. Note that Refs. liu1999 ; gopi1999 fitted the long-range autocorrelation to the function in the form of . In our analysis we found no significant difference if we used such function.

II.5 How volatile are the two stocks?

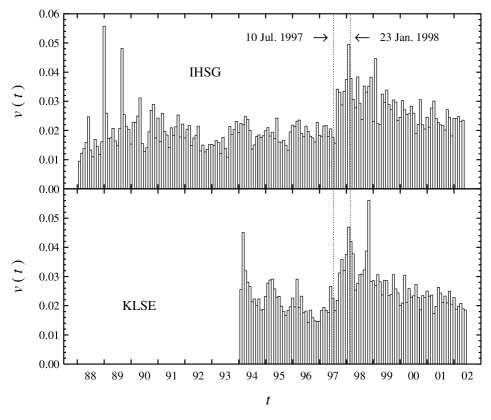

Finally it is also interesting to see the volatility of the two stocks. The volatility of the stock index is a measure of how much the index is likely to fluctuate. Information on the stock volatility is very important for investors since it quantifies the risk factor and it is also an important input of the Black-Scholes option-pricing model. There are many different definitions of the volatility in financial literatures schwert . Here we define the volatility as an average of the absolute return over a time window with length sampled with day,

| (10) |

with is given by Eq. (1).

The results are shown in Fig. 9. As can be estimated from Figs. 2 and 3 volatility in both stock indices increases after the financial crash. It is obvious that after the drop of the foreign exchange rate finished in 23rd January 1998 volatilities of both indices are still large until the indices reached their minimum values in September 1998. From that on, the volatility decreases gradually although until 2002 the values are still larger than the values before the crash.

It is also obvious from Fig. 9 that before 1997 the IHSG stock had a rather stable volatility variation, while on the other hand the variation in the KLSE case was already dramatic. In general, the two stocks maintain these behaviors after the crash, although in this period the averaged volatilities are larger than before. This might explain why the IHSG stock index is found to be more correlated than the KLSE one.

III Statistical properties before and after crash

| IHSG | KLSE | |||||

| Properties | Before crash | During crash | After crash | Before crash | During crash | After crash |

| Average volatility | 0.0192 | 0.0327 | 0.0260 | 0.0219 | 0.0341 | 0.0237 |

| Standard deviation | 0.0167 | 0.0300 | 0.0185 | 0.0127 | 0.0323 | 0.0197 |

| Kurtosis | 183.421 | 2.849 | 4.377 | 6.775 | 8.152 | 42.925 |

| Skewness | 6.8706 | 0.1417 | 0.7079 | 0.2053 | 1.0644 | |

| 2347 | 296 | 883 | 889 | 284 | 993 | |

In section II we have shown that between July 1997 and September 1998 the index returns of both stocks fluctuate strongly. As shown in Fig. 9, compared with the situations before and after this period, both indices become more volatile. A more quantitative description can be obtained from Table 2, where in the first line we average the index volatility over all times before 10th July 1997, 16 month after that (during which the volatility of both indices is significantly large), and over the rest of data, respectively. The result confirms the finding of Ref. lillo2000 , namely the volatility of a stock index tends to be large right after the crash and in a relatively long period after that. This also happens to both stock indices, i.e. almost five years after the financial crisis both stocks are still more volatile than before.

In the financial literature the volatility is often calculated from the standard deviation of the returns distribution schwert . In Table 2 we also present the standard deviations of the IHSG and KLSE index returns distributions in all three cases. Table 2 indicates that both definitions are consistent in our analysis.

From the kurtosis of stock indices we can see that the IHSG stock is more capitalized after the crash, whereas the KLSE stock displays a very different behavior. Nevertheless, the skewness of their distributions shows a similar tendency, both stocks deliver less profits after the crash, although more profits could be obtained from the KLSE stock during the crash.

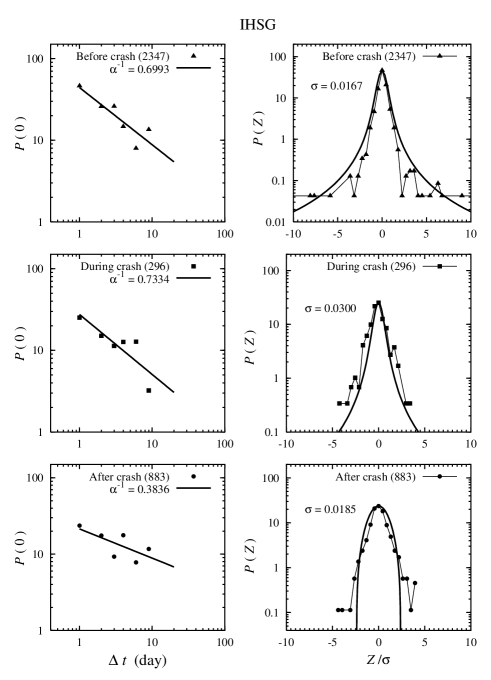

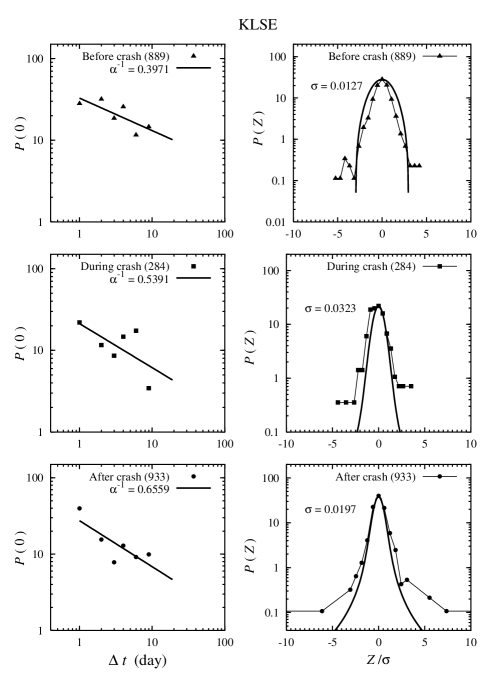

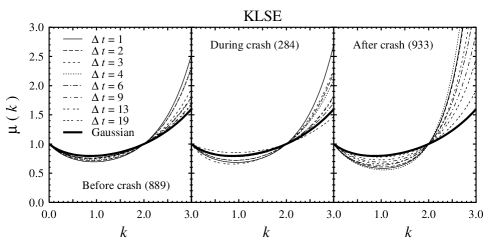

It is clearly tempting to investigate whether or not the universal properties found in section II still exist in all periods and to ask what kind of differences might quantify these conditions. The answer can be found in Figs. 10 and 11. Obviously in all cases the statistical accuracies are not as good as in the previous section, when we used all data in our analyses. Nevertheless, in spite of the very limited data points used in our analysis, the message from Figs. 10 and 11 is clear, the universal properties of the returns distribution retain their existences in all cases. Linear regression to the IHSG probability of the return to the origin reveals the fact that the distribution turns from Lévy to Gaussian after the crash. Surprisingly, the KLSE stock index shows a contrary result, the distribution alters from a Gaussian to a Lévy one after the crash.

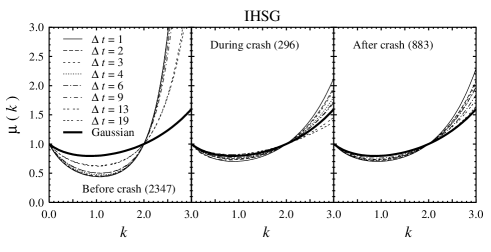

A cross-check to the result shown in Figs. 10 and 11 is inevitable, since the number of data could significantly limit statistical accuracies in this case. For this purpose in Figs. 12 and 13 we display the moments of both stock indices in the case of before, during, and after the financial crash. A consistent result is obtained from these figures, in the case of IHSG the distribution becomes closer to Gaussian during and after crash, whereas the KLSE moments move away from the Gaussian distribution after the crash.

Another important finding obtained from Fig. 12 is that the scaling behavior up to shown by the IHSG case in the previous section originates from the period before crash. After the crash, the IHSG moments quickly converge to a Gaussian distribution. In fact, this phenomenon has already been seen in the left panels of Fig. 10, where the empirical probability of return to the origin is more scattered in the crash periods and after that.

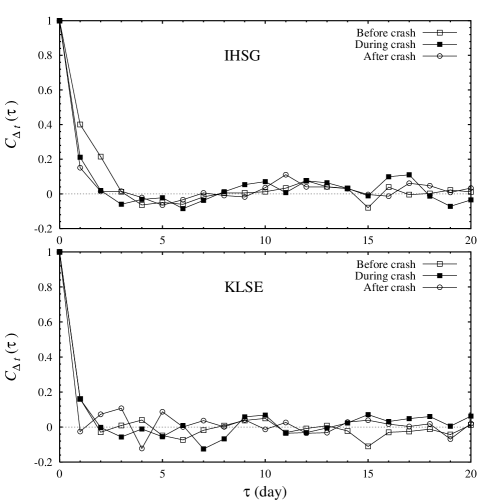

As in the previous section, investigation of the autocorrelation function from both stocks might also be of interest. The corresponding autocorrelation is shown in Fig. 14. Although it is difficult to see how long the KLSE stock maintains its correlation, the IHSG stock index obviously becomes less correlated during and after the crash. This result can be understood by looking back to Fig. 12, i.e. after the crash the returns distribution becomes more random and therefore the index losses its memory.

It might be more interesting if we compare results in this section with currency controls shown in the top panels of Figs. 2 and 3. The government interventions on the exchange rate seem to create non natural economics activities which have a direct influence on the fluctuation of stock indices. Once the currency is under-controlled, the fluctuations tend to significantly deviate from the Gaussian distribution, which can be clearly seen in the IHSG moment before crash (Fig. 12) and the KLSE one after crash (Fig. 13). From the investors point of view this is obvious, a less fluctuating exchange rate reduces the number of variables considered in estimating the future stock price.

IV Conclusions

We have analyzed the IHSG and KLSE stock index returns using the methods developed for statistical physics. In spite of the limited number of data used in our analysis, we still found that both stock indices show the universal properties previously observed in the leading stocks such as S&P 500 and NYSE, i.e. the scaling properties. The difference is, nevertheless, found in the time scale, the IHSG stock retains its scaling property longer than the KLSE one. As a consequence, the former is more correlated than the latter.

By investigating their statistical properties before, during, and after the financial crash it is found that the scaling behavior of the IHSG index originates from its fluctuation before the crash period. During and after the crash periods the index distributions are closer to Gaussian and do not show a stable process. In the KLSE case, the return distributions in all periods show an unstable process and depart from Gaussian after the crash. One possible explanation to these different behaviors could be the currency control. Besides these differences, both stock indices show some similarities, namely both stocks become more volatile during and after the crash and their return moments become closer to Gaussian during the crash.

Acknowledgements.

This work was supported in part by the Quality for Undergraduate Education (QUE) project. The author thanks Dwi Arsono for collecting the IHSG data and to Dr. Chairul Bahri for careful reading of the manuscript and critical comments.References

- (1) D. Canning, L.A.N. Amaral, Y. Lee, M. Meyer, and H.E. Stanley, Econ. Lett. 60, 335 (1995).

- (2) T.C. Mills, Physica A 293, 566 (2000)

- (3) M. Raberto, E. Salas, G. Cuniberti, and M. Riani, arXiv:cond-mat/9903221.

- (4) Y. Liu, P. Gopikrishnan, P. Cizeau, M. Meyer, C.-K. Peng and H.E. Stanley, Phys. Rev. E 60, 1390 (1999).

- (5) P. Gopikrishnan, V. Plerou, X. Gabaix, and H.E. Stanley, Phys. Rev. E 62, R4493 (2000).

- (6) R.N. Mantegna and H.E. Stanley, Nature (London) 376, 46 (1995).

- (7) R.N. Mantegna and H.E. Stanley, An Introduction to Econophysics: Correlations and Complexity in Finance (Cambridge University Press, Cambridge, 1999)

- (8) V. Plerou, P. Gopikrishnan, L.A.N. Amaral, M. Meyer, and H.E. Stanley, Phys. Rev. E 60, 6519 (1999).

- (9) P. Gopikrishnan, V. Plerou, L.A.N. Amaral, M. Meyer, and H.E. Stanley, Phys. Rev. E 60, 5305 (1999).

- (10) F. Lillo and R.N. Mantegna, arXiv:cond-mat/9909302.

- (11) F. Lillo and R.N. Mantegna, Eur. Phys. J. B 15, 603 (2000).

- (12) A. Johansen and D. Sornette, Eur. Phys. J. B 1, 141 (1998).

- (13) G. Bonanno, F. Lillo and R.N. Mantegna, arXiv:cond-mat/9912006.

- (14) B.H. Wang and P.M. Hui, Eur. Phys. J. B 20, 573 (2001).

- (15) B.B. Mandelbrot, J. Business 36, 394 (1963).

- (16) H.E. Stanley, Physica A 285, 1 (2000).

- (17) The Energy Information Administration home page, United States Department of Energy.

- (18) S.V. Muniandy, S.C. Lim, and R. Murugan, Physica A, 407 (2001).

- (19) OANDA FXTrade, http://www.oanda.com.

- (20) Jakarta Stock Exchange Market (BEJ), see the BEJ web site at http://www.jsx.co.id.

- (21) Yahoo Finance, http://table.finance.yahoo.com.

- (22) W.H. Press, S.A. Teukolsky, W.T. Vetterling, B.P. Flannery, Numerical Recipes in Fortran (Cambridge University Press, Cambridge, 1992).

- (23) F. Lillo and R.N. Mantegna, Phys. Rev. E 62, 6126 (2000).

- (24) See e.g., G.W. Schwert, J. Fin. Serv. Res. 3, 153 (1989); J. Finance 44, 1115 (1989).