Simple Simulational Model for

Stocks Markets

JUAN R. SANCHEZ 111Email: jsanchez@fi.mdp.edu.ar

Departamento de Física, Facultad de Ingeniería

Universidad Nacional de Mar del Plata

Av. J.B. Justo 4302, 7600 Mar del Plata, Argentina

Abstract

A new model for stocks markets using integer values for each stock price is presented. In contrast with previously reported models, the variables used in the model are not of binary type, but of more general integer type. It is shown how the behavior of the noisy and fundamentalists traders can be taken into account simultaneously in the time evolution of each stock price. The simulated time series is analysed in different ways order to compare parameters with those of real markets.

Recently, several computational models trying to represent the behavior of actual stocks markets have been presented. [1, 2, 3] ¿From these results it seems to be a well established fact that, in order to obtain a good representation of the time evolution of actual markets, two type of traders agents must be included. On one side there are the so called noisy traders which are supposed to follow the local (in space and time) trend of the market. The noisy traders, also called followers, place their buy or sell orders on a given stock following the behavior of other (related) stocks. This kind of attitude seems to be an almost evident practice for someone trying to operate within a market. But, on the other hand, there are also fundamentalists traders which are considered to be responsible of the market turn offs. These kind of traders are supposed to know something more about the market and then are able to develop some kind of more sophisticated strategy to operate. They can take actions to buy or sell according to other indicators; the markets fundamentals. These indicators could depend on other type of information which usually may come from outside of the system. In previous models the two types of agents are represented in a variety of ways. [2, 3] For instance, in reference 2 the influence of the fundamentalists is modeled by including a term that takes into account the tendency in the price changes. This effect stabilizes the prices. On the other hand, in reference 3 the two type of traders are included as separate entities. Then, it is realistic to think that both type of behaviors are acting at the same time and influence the way in which a specific stock price change. ¿From the point of view of simulations, another common characteristic of many of the models just presented seems to be the use of Ising like variables that represent the buy or sell attitude of market agents.

Taking into account all the above mentioned characteristics, a somewhat different modeling approach is presented here. In principle, the model is based in previously reported models of opinion evolution in a closed community. [1] But, instead of using Ising spins, here the community is modeled by a vector of stock prices having integer valued “Potts” components , each one representing the price of a market asset (in arbitrary units). Then, associated with each is a direction of movement value . The components form a vector . This components are of Ising type, i.e., they can take two values and . The vectors and evolve in time according to the following dynamical rules. A randomly chosen component is updated according to the equation

| (1) |

while for the corresponding components the following equation is valid

| (2) |

The value of is obtained by choosing at random among the direction values of each one of the neighbors, i.e., or with equal probability. In principle, the algorithm described by the equations 1 and 2 takes into account the influence of the noisy traders which follow the trend of related stocks in order to buy () or to sell () an specific asset. However, it is not reasonable to think that the prices could take arbitrary positive or negative values. There is no actual market following a given trend for ever. Then in order to take into account the influence of the fundamentalists traders, a threshold is established for the absolute value of each . As it can be seen in equation 2, if at any time the corresponding direction of movement is reversed, . This reversal procedure simulates the influence of the fundamentalists traders which, when the absolute value of a stock reaches a value , consider that the price is low enough so is time to buy or it is high enough and then is time to sell. In equations 1 and 2, is proportional to so the simulation time is incremented by one when all the stocks have, on average, the chance to evolve once.

In order to analyze the behavior of the model, two representative indexes of the market, the mean value time series

| (3) |

and the corresponding returns or change of price, defined here as

| (4) |

are investigated by Monte Carlo simulations. and where used as typical parameters and Monte Carlo steps (MCS) where used in order to obtain most of the reported results. To avoid the existence of initial correlations the simulations are started with the components of the vector distributed randomly between and and with the vector in a complete antiferromagnetic state.

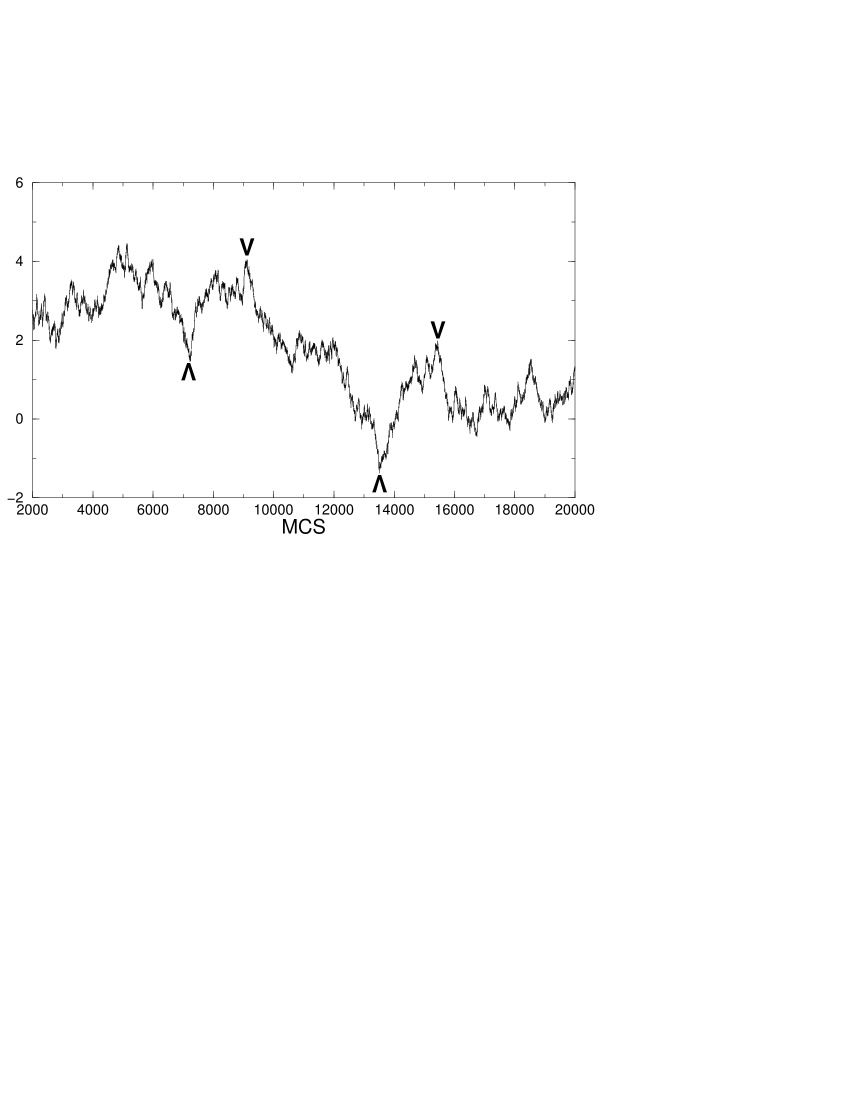

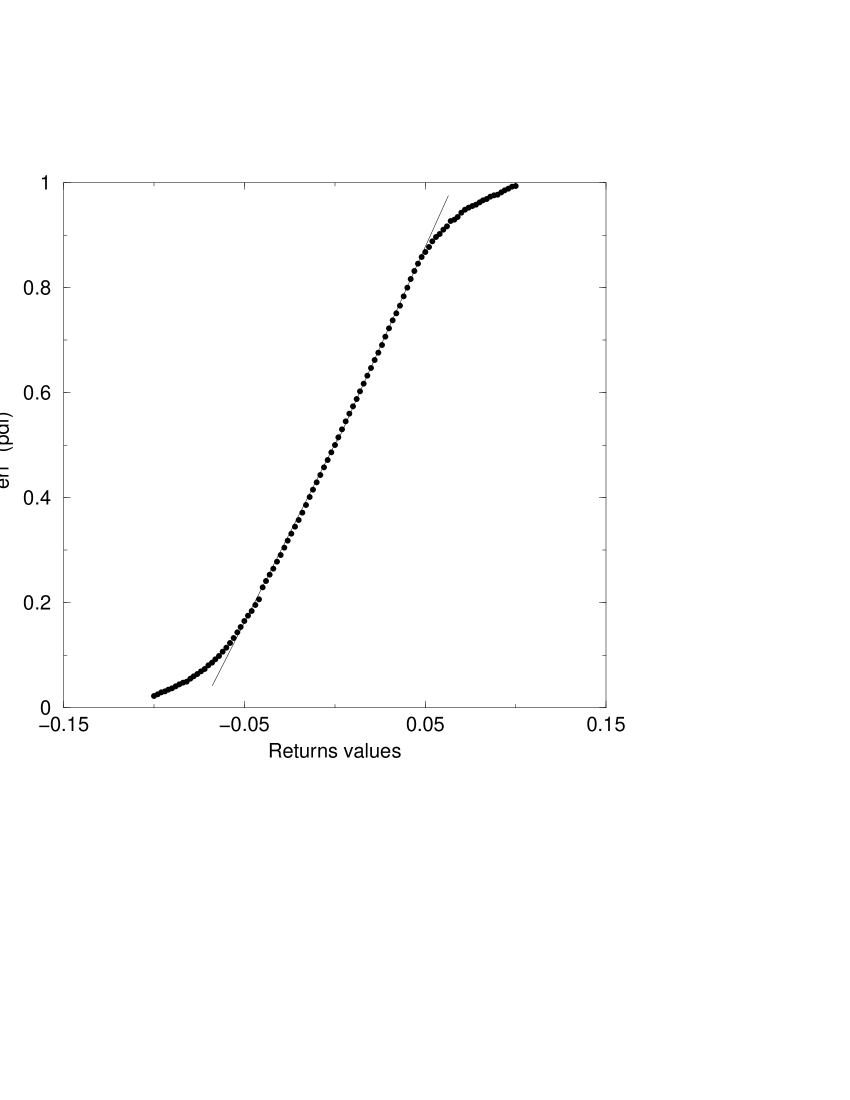

A typical path of the simulated price series is shown in Fig. 1. The sequence shows the well known noisy shape. The market turn offs have been indicated in the figure. This turn offs have a self-organized character, since they result from the time evolution of the model and their occurrence cannot be explicitly predicted from the dynamic equations. Previous analysis of actual markets time series suggest that the probability distribution of daily returns are not of Gaussian type, but they are fat-tailed. [4] This characteristic can be noticed if the probability distribution function (PDF) of the returns is plotted on the scale of the cumulative Gaussian distribution function. Normal distributions appear as straight lines in such representation while the fat-tail of other type of distributions result in a departure of the straight line. For the model presented here, the PDF of the price returns is plotted in Fig. 2 and the tails are clearly visible .

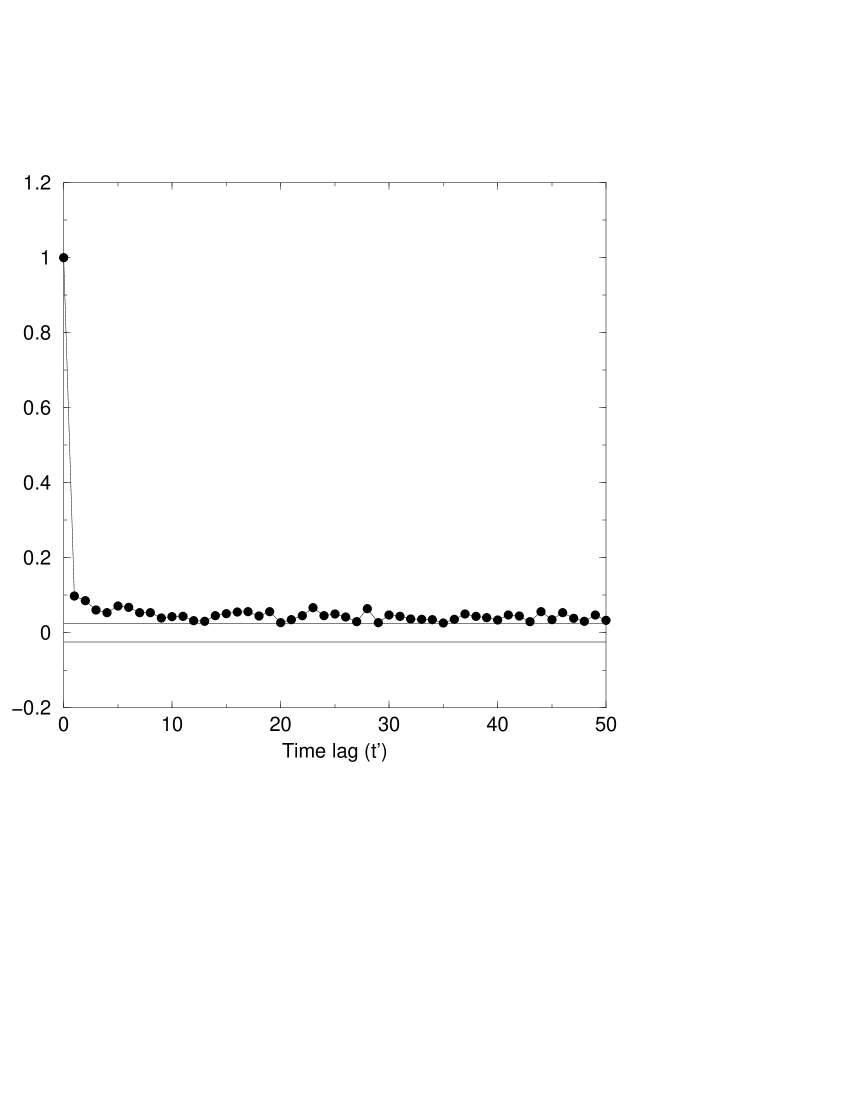

According to previous results, it is known that actual markets time series cannot be modeled by series of independent and identically distributed realizations of random variables with a given distribution (fat-tailed or not). This is a consequence of the existence of non-stationarity in the process that generate the series. It has been shown that a direct method exists in order to detect the non-stationarity, it is the calculation of the autocorrelation function [3, 5]

| (5) |

of the absolute value of the returns . For Brownian motion the of , and fluctuates around zero for . In Fig. 3 the for the time series generated by the model is plotted up to . The horizontal lines represent the confidence interval of a Brownian random walk. Clearly, it is shown that the simulated series has a certain degree of non-stationarity very similar of those just reported for actual markets time series.

Another parameter that can reflect the deviation of a time series from the Gaussian distribution is the excess kurtosis, defined as

| (6) |

where is the fourth central moment and is the standard deviation of the series under study. is defined to be zero for a normal distribution, but ranges between and for daily returns of actual stock markets data have been reported. [6, 7] An average value of was obtained when the kurtosis is calculated on the absolute values of the returns. The value was obtained by averaging over independent runs of MCS.

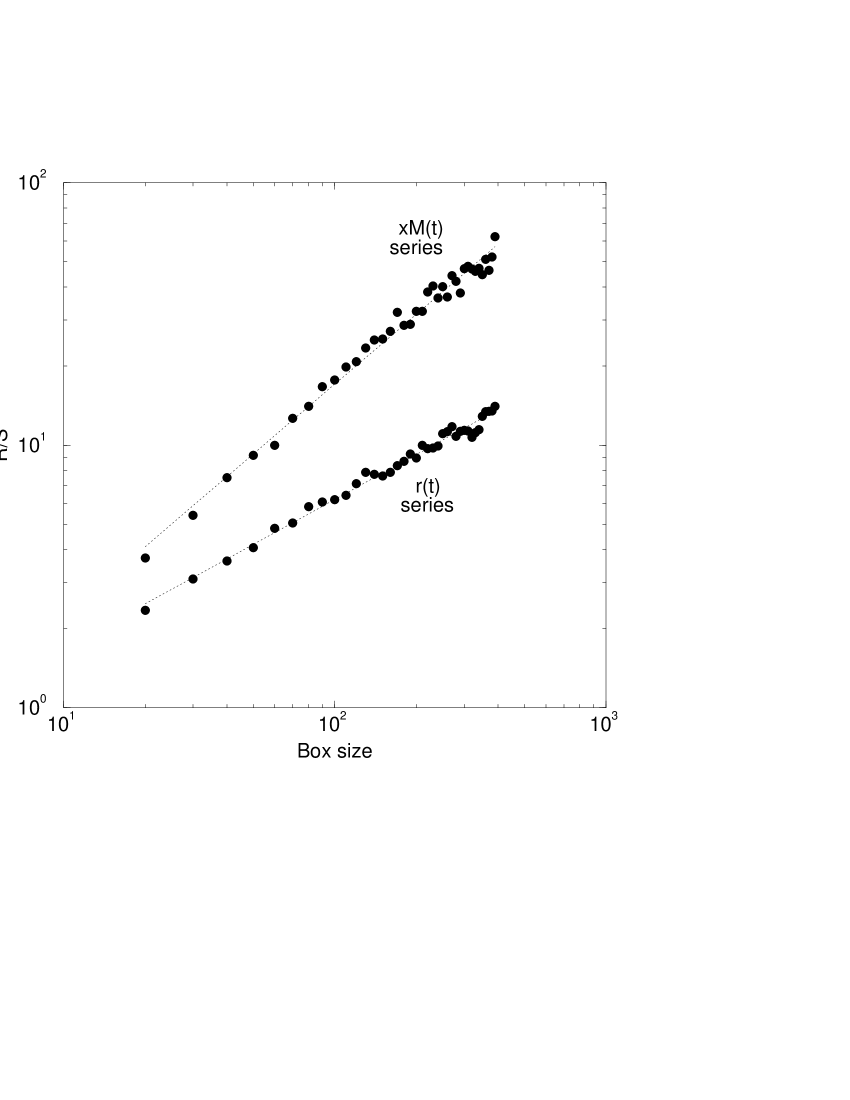

Finally, the simulated series was analyzed using the Hurst R/S method. [4] The R/S analyses begins with dividing the time series in segments of equal length and normalizing the data in each segment by subtracting the sample mean. Then, the rescaled range (range/standard deviation) is log-log plotted against the segment size. By linear regression of the plot the Hurst exponent is obtained. The values of the exponent reflect some characteristics of the series: for the series is said to be persistent, if the series represent a normal distributed random walk, while for the series is considered to have anti-persistent characteristics. The R/S analysis for the price and returns series is presented in Fig. 4. The straight lines through the points indicates that the Hurst exponent is for the series and for the series. Since the values are greater than both series show a persistent character which results from the existence of long term correlations in both distributions. In particular, the value of is very close to the value of the Hurst exponent calculated on the returns of the USD/DEM exchange rate.

Although several other analysis could be made, the above presented results show that the simulated time series obtained from the operation of the dynamic rules 1 and 2 can be considered as a good approximation of the behavior of actual stock markets. Also, the discrete nature of the price variables follow closely the same characteristic of actual stocks prices. Further refinement could be made on the model in order to reproduce more closely some particular characteristic of a given market.

This work was partially supported by a research grant from Universidad Nacional de Mar del Plata (Mar del Plata, Argentina).

References

- [1] H. Levy, M. Levy and S. Solomon, Microscopic Simulation of Financial Markets, Academic Press, San Diego (2000). G.W. Kim and H.M. Markowitz, J. Portfolio Management 16, 45 (1989). P. Bak, M. Paczuski and M. Shubik Physica A 246, 430 (1997). T.Lux and M. Marchesi, Nature 397, 498 (1999).

- [2] D. Sornette and K. Ide, cond-mat/0106054. K. Ide and D. Sornette, cond-mat/0106047.

- [3] K. Sznajd-Werron, J. Sznajd, cond-mat/0101001 (2000).

- [4] E.E. Peters, Fractal Market Analysis (Wiley, New York, 1994).

- [5] J. Beran, Statistics for Long-Memory Processes (Chapman & Hall, New York, 1997).

- [6] J. Campbell, A.H. Lo, C. McKinlay, The Econometrics of Financial Markets (Princeton Univ. Press, 1997).

- [7] A. Pagan, J. of Empirical Finance, 3, 15 (1996).