Fluctuations and Market Friction in Financial Trading

Abstract

We study the relation between stock price changes and the difference in the number of sell and buy orders. Using a soft spin model, we describe the price impact of order imbalances and find an analogy to the fluctuation-dissipation theorem in physical systems. We empirically investigate fluctuations and market friction for a major US stock and find support for our model calculations.

pacs:

PACS numbers: 05.45.Tp, 89.90.+n, 05.40.-a, 05.40.FbThe unpredictable up and down movements in the stock market have always captured the interest and imagination of investors. The scientific investigation of these phenomena started with Bachelier’s comparison of stock price dynamics with a random walk [1]. This study has been refined in many respects [2]. Interest has been devoted to the precise shape of the distribution of returns (difference of the logarithm of stock prices at different times), which is characterized by a high probability for large fluctuations [3, 4, 5, 6].

After it was realized that large price fluctuations tend to cluster together in time, stock price returns were described by models of volatility (standard deviation of returns) changing in time [7, 8]. This effect is captured in time series models, in which the volatility at a given time depends on the magnitude of previous returns [9, 10]. It has been actively investigated how the stochastic properties of price dynamics can be related to the market microstructure, i.e. the rules and motivations according to which agents act in a financial market. Although the details of models differ [11, 12, 13, 14, 15] , they have been successful in reproducing the empirical observations.

Here, we follow a different approach motivated by the successful application of physics concepts to study the economy [16, 17, 18]. We investigate the price dynamics on an intermediate or coarse grained time scale , which is long enough to average over the details of market microstructure, but short enough to resolve the trading dynamics. In physical systems, there exists a quantitative relation between the strength of fluctuations of an observable and the rate, at which energy is dissipated when the same observable is pulled by an external force. Einstein discovered this relation first, when he studied the fluctuations of small particles in a fluid [19]. In this case, the variance of position fluctuations is proportional to temperature times the mobility of particles. This relation was later on generalized to a wide class of systems [20] and is known as fluctuation-dissipation theorem.

In this letter, we use an effective model for stock price dynamics to derive a similar relation between the time varying volatility of stock returns and the “friction constant for stock prices” or market liquidity. Market liquidity relates returns to the difference between buy and sell orders (order imbalance), which acts as an external force. We study the dependence of stock price changes on order imbalance empirically by using the method of data analysis and some of the results of [21, 22]. We find that the empirical results agree well with our model.

Model calculation: The observable quantity we are interested in is the logarithmic stock price changes within a time interval

| (1) |

where is the price of a given stock at time . Transaction prices at a stock exchange lie usually in a finite interval between the bid price (the price a trader offers to pay for a stock) and the ask price (the price at which a dealer is willing to buy the stock). In addition, the historical prices studied take only discrete (tick) values. This motivates to model price changes by a spin model, and for the virtue of easier analytical calculations by a soft spin model [23].

The spin variable we use is the “instantaneous return” , where the average time interval between trades sets the time scale of the problem. The observable returns on time scale are related to them via

| (2) |

In an analogous way, we define an instantaneous order imbalance . Here, order imbalance is the number of buy orders minus the number of sell orders divided by the total number of outstanding shares of a given stock. We describe the dynamics of by the following stochastic differential equation

| (3) |

Mathematically, the - and - term enforce the soft spin constraint of finite and discrete price changes. From a finance point of view, the linear term describes relaxation and controls the strength of fluctuations. The cubic term stabilizes the theory in a regime of strong fluctuations (small ). The order imbalance is analogous to the magnetic field in the theory of spins, its coupling constant is in analogy to the magneton in magnetic systems. The Gaussian white noise has the correlator . It represents the influx of news not captured by the news content of the order imbalance. Stochastic differential equations for stock price changes with a quadratic instead of the cubic term were studied in [15, 24]. A generalization of Eq.(3) to many stocks was used to explain correlations between them [25].

The variance of price changes on a time scale is well approximated by

| (4) |

where the average is taken without the cubic term. This approximation is valid as long as the system is not in the vicinity of a critical point. Eq.(4) describes a diffusion process with diffusion constant . In order to describe the stochastic volatility and fat tails observed in empirical data, we must allow for a time dependence of both the frequency of trades and the standard deviation of the price of individual transactions. In Ref. [26] it was shown that price changes of financial transactions can be consistently interpreted in such a framework. When becomes a random variable, is causes multiplicative noise in Eq.(3), which can account for the power law tails of the return distribution [27, 28].

The price impact function describes the functional relation between the expectation value conditioned on the volume imbalance and the volume imbalance itself. We define the susceptibility as the slope of the price impact function close to zero volume imbalance

| (5) |

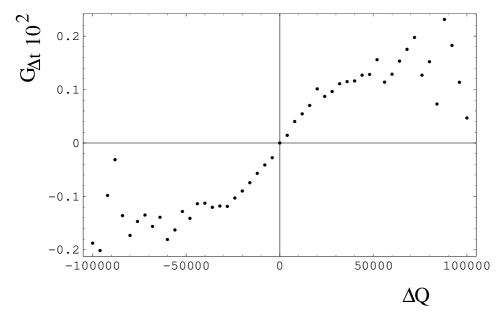

As stocks are traded in discrete units, this limit can in an empirical study only be approximated. The inverse of this susceptibility can be interpreted as market liquidity. For an order imbalance which is constant in the time interval the full price impact function can be calculated analytically for the model Eq.(3) and compares well to the empirical data in Fig. 1. Such a situation could be realized if an informed trader breaks up a large trade into many small ones and trades at a fixed frequency.

From Eq.(3) we find . Combining this with Eq.(4) for the volatility, we obtain for the linear regime of small fluctuations

| (6) |

This relation and its empirical test are our central results. The square root on the r.h.s. is essentially the square root of the number of trades in the time interval and in analogy to the temperature in physical systems. The relation Eq.(6) differs from the Einstein relation in that the standard deviation of fluctuations appears on the l.h.s. instead of the variance. The reason for this is the difference in “experimentally” relevant time scales: as was assumed to be much larger than the microscopic time scale in our coarse grained description of stock price dynamics, is proportional to the zero frequency Fourier component of the instantaneous return, and not to the integral over all frequency components as in the derivation of the Einstein relation.

Empirical Results: The empirical test of Eq.(6) uses the method of data analysis and some of the results of [21, 22]. The present author got to know about the shape of the empirical price impact function and its similarity to the magnetization curve of spin systems from the authors of [21, 22], and only later on learned about related work in the economics literature [29].-

In the framework of the efficient market hypothesis the price of a stock reflects present and discounted future earnings of the underlying company. The estimation of these earnings depends on information about that company. Information may be disseminated by a news release, a press article, or by rumors. In addition, traders extract information about a company (or at least information about the beliefs of other traders concerning that company) from the order imbalance. This is reasonable under the assumption that somebody selling the stock might do that because he has superior knowledge about the underlying company and expects its value to drop. Hence, one can assume that the order imbalance will have impact on the price of a stock.

We analyze stock prices of General Electric, a major American company for the year 1997. Price, volume, bid and ask price of all transactions of this stock are recorded in the Trades and Quotes (TAQ) data base published by the New York Stock exchange. We analyzed a total number of transactions contained in that data base. The question, whether a trade is buyer or seller initiated is difficult to answer, as there is a buyer and a seller for each trade. We try to answer it by finding out which one is more eager to do the trade, i.e. we compare the transaction price to the bid and ask price [21, 22, 29, 30, 31]. First, we try to match the price of a trade with quotes at the same stock exchange with a time stamp at least two seconds prior to the transaction time. In this way we account for possible time lags in the reporting of prices. If the trade occurs at the bid price, it is classified as seller initiated, if it occurs between bid and ask price it is classified as neutral, and a trade at the ask price is classified as a buyer initiated. If the transaction price is lower than the bid price or higher than the ask price the trade is discarded as not matched.

Having classified all trades, we can give a sign to the volume of each trade. A buyer initiated trade has a positive sign, a seller initiated trade a negative sign. As our analysis does not focus on the market microstructure, we average both volume and price changes over a sampling time . This averaging is analogous to the concept of coarse graining in physics, which also averages over microscopic model details and allows the derivation of effective theories. In the finance context, the choice of the sampling time is influenced by the following considerations. If the sampling time is chosen too short, the effects of individual trades will not be smoothed out, if it is chosen too long it is not clear that there is still a causal relation between order imbalance and price change: price changes will influence traders and in this way have an effect on the order imbalance. For our analysis we choose as five minutes. In this way we generate for each stock a time series of returns and order imbalances (measured relative to the total number of outstanding stocks of a company).

To visualize this information, we plot the average price change for a given order imbalance against the order imbalance (price impact function) in Fig.1. It agrees with the results of [21, 22, 29]. Its characteristic form with a linear part for small and a less steep part for large is described by a hyperbolic tangent [21, 22] and can be well approximated by the functional form resulting from Eq.(3).

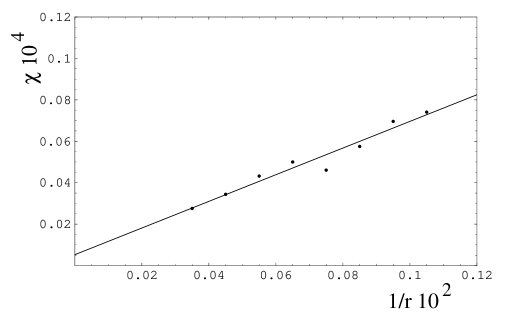

Next, we sort the 5 minute intervals according to the average fluctuation ( in terms of the Langevin model) per trade and calculate a price impact function for each fluctuation strength. We calculate the slope in its linear region and thus generate a series of susceptibilities depending on the local volatility. This data set is shown in Fig.2. The full line is a least square fit to the data points. The good quality of the fit is illustrated by the high regression coefficient . Thus the empirical analysis supports well the linear relationship between fluctuation strength and susceptibility suggested by Eq.(6).

Discussion: The linear relation between fluctuation strength and liquidity implies that large price changes are not only due to a large volume of trades but also to a large price impact of a given volume. In the soft spin model Eq.(3), the time changing volatility is proportional to the square root of the number of trades times the liquidity. In Ref.[26] it was shown that changes in the trading frequency cannot account for the appearance of large price fluctuations. Hence we conclude that large price fluctuations are caused by changes in the market liquidity.

The inverse susceptibility appears as the -term in our model Eq.(3). For this reason, large price fluctuations associated with a large liquidity are described by the soft spin model in a critical state. In a critical spin model, even small changes in the external magnetic field cause huge fluctuations in magnetization. From this point of view, it is not large “external” influences which cause large price fluctuations, but the strong response of the system itself.

In summary, we have studied both theoretically and experimentally the relation between the strength of stock price fluctuations and the friction constant, which relates order imbalance and price changes. We have modeled stock price dynamics on a coarse grained time scale by a soft spin model and found an analogy to the fluctuation-dissipation theorem in physics, which is supported by our empirical study.

Acknowledgements: We acknowledge several stimulating discussions with V. Plerou, P. Gopikrishnan, X. Gabaix, and H.E. Stanley and thank them for making available the results of [22] prior to publication. We acknowledge helpful conversations with A. Kempf, T. Nattermann, D. Stauffer, and L. Viceira.

REFERENCES

- [1] L. Bachelier, Annales Scientifiques de l’Ecole Normale Supérieure III-17, 21 (1900).

- [2] J. Campbell, A. Lo, and C. MacKinlay, The Econometrics of Financial Markets, Princeton University Press (1997).

- [3] B.B. Mandelbrot, Journal of Business 36, 394 (1963).

- [4] R.N. Mantegna and H.E. Stanley, Nature (London) 376, 46 (1995).

- [5] T. Lux, Appl. Financial Economics 6, 463(1996); M. Loretan and P.C.B. Phillips, J. Empirical Finance 1, 211 (1994)

- [6] P. Gopikrishnan, M. Meyer, L.A.N. Amaral, and H.E. Stanley, Eur. Phys. J. B 3, 139 (1998).

- [7] G.W. Schwert, J. Finance 44, 1115 (1989).

- [8] For a review see, e.g. T. Bollerslev, R. Chou, and K. Kroner, J. Econometrics 52, 5 (1992).

- [9] R.F. Engle, Econometrica 50, 987 (1982).

- [10] T. Bollerslev, J. Econometrics 31, 307 (1986).

- [11] M. Lévy, H. Lévy, and S. Solomon, J. Physics I 5, 1087, (1995).

- [12] D. Challet and Y.-C. Zhang, Physica A 246, 407 (1997).

- [13] R. Cont and J.P. Bouchaud, Macroeconomic Dynamics 4, 170 (2000).

- [14] T. Lux and M. Marchesi, Nature 397, 498 (1999).

- [15] J.D. Farmer, International Journal of Theoretical and Applied Finance 3, 425 (2000).

- [16] J.D. Farmer, Computing in Sci. and Eng. 1, 26 (1999).

- [17] J.-P. Bouchaud and M. Potters, Theory of Financial Risk (Cambridge University Press, Cambridge 2000).

- [18] R.N. Mantegna and H.E. Stanley, An Introduction to Econophysics ( Cambridge University Press, Cambridge 2000).

- [19] A. Einstein, Ann. Physik 17, 549 (1905).

- [20] H.B. Callen and R.F. Welton, Phys. Rev. 86, 702 (1952).

- [21] I am grateful to V. Plerou, P. Gopikrishnan, X. Gabaix, and H.E. Stanley for making available their results now published in [22] in several discussions in July 2000.

- [22] V. Plerou, P. Gopikrishnan, X. Gabaix, and H.E. Stanley, eprint cond-mat/0106657.

- [23] S.K. Ma, Modern Theory of Critical Phenomena, Benjamin New York (1976); P.C. Hohenberg and B.I. Halperin, Rev. Mod. Phys. 49, 435 (1977).

- [24] R. Cont and J.-P. Bouchaud, Eur. Phys. J. B 6, 543 (1998).

- [25] P. Gopikrishnan, B. Rosenow, V. Plerou, and H.E. Stanley, Phys. Rev. E (Rapid Comm.), in press.

- [26] V. Plerou, P. Gopikrishnan, X. Gabaix, L.A.N. Amaral, and H.E. Stanley, Phys. Rev. E. 62, R3023 (2000).

- [27] C.G. Champenowne, Economic Journal 63, 318 (1953); for a recent presentation see, e.g., H. Takayasu, A.-H. Sato, and M. Takasu, Phys. Rev. Lett. 79, 966 (1997).

- [28] H. Takayasu and M. Takayasu, Physica A 269, 24 (1999).

- [29] A. Kempf and O. Korn, Journal of Financial Markets 2, 29 (1999).

- [30] J. Hausmann, A. Lo, and C. MacKinlay, Journal of Financial Economics 31, 319 (1992).

- [31] M. Blume, C. MacKinlay, and B. Terker, Journal of Finance 44, 827 (1989).