Generating Functional Analysis of the Dynamics of the

Batch Minority Game with Random External Information

J.A.F. Heimel and A.C.C. Coolen

Abstract

We study the dynamics of the batch minority game, with random external

information,

using generating functional techniques à la De Dominicis. The relevant

control parameter in this model is the ratio of the

number of possible values for the external information over

the number of trading agents. In the limit we calculate the

location of the phase transition (signaling the onset of anomalous response),

and solve the statics for exactly.

The temporal correlations in global market

fluctuations turn out not to decay to zero for infinitely widely separated

times. For the stationary state is shown

to be non-unique. For

we analyse our equations in leading order in

, and find asymptotic solutions with diverging volatility

(as

regularly observed in simulations), but also asymptotic solutions with

vanishing volatility . The former, however, are shown to

emerge only if the agents’ initial strategy valuations are below a specific

critical value.

PACS numbers: 02.50.Le,87.23.Ge,05.70.Ln,64.60.Ht

I Introduction

The minority game has been the subject of much (and at times

heated) debate in the physics literature recently. It was originally introduced

in [1], as a variation of the El Farrol-Bar problem [2],

to serve as a simple model for a market in economics, and has since then attracted much

attention (see e.g. [3]). The players in the minority game are trading agents

who, at every stage of the game, have to make a decision whether to buy or to sell,

on the basis of both publicly available information (i.e. past market

dynamics, weather forecasts, political developments or stock prices) and their personal strategies.

Those agents who find themselves having made the minority decision

make a profit, while those agents which opted for the majority

choice loose money. After each round all agents re-value their

strategies. There are many variations on the precise implementation of this game,

yet most share the same main features of the emerging market fluctuations.

The important control parameter in the model is the ratio of the

number of possible values for the external information over

the number of trading agents. If this ratio is very large, the agents

exhibit essentially random behaviour. This is reflected in the fluctuations of the

total bid, being the sum of all buyers minus the sum of all sellers. If less

external information is available (or used) to base decisions upon, i.e. for reduced , the

mismatch between buyers and sellers is found to decrease, and the market behaves

more efficiently. This behaviour is now understood quite well on the basis of the replica

calculations in [4, 5, 6] and the

crowd-anticrowd theory of [7]. The situation is much less clear, however,

when becomes very small. One possibility is

that the market becomes extremely efficient, and the number of buyers

almost equals the number of sellers.

Another possibility is that the mismatch between buyers and sellers

diverges if the amount of shared (i.e. external) information becomes small, and the market becomes

extremely inefficient (see e.g. [8, 9]).

In this paper we solve the dynamics

for the original many agent model,

using the exact generating functional (or path integral) techniques introduced in [10].

After defining the rules of the game we derive in the limit

an equivalent description in terms of an

effective stochastic non-Markovian single agent process, for which we calculate the first

time steps. For sufficiently large values of , we can solve the statics

exactly under the assumption of absence of anomalous response. We calculate the point

where this assumption breaks down, resulting in a phase transition; our value for

is identical to that found in [4].

The present dynamical approach allows us to study the behaviour of the market

below . In this region there exist persistent non-static

solutions which cannot be studied by the methods of [4].

Below the market is non-ergodic and

the initial conditions of the agents determine

the final stationary state of the market.

For we calculate the market volatility in leading order

in for the case where the agents

are initialised with only weak strategy preferences, leading to a diverging volatility with exactly

the scaling exponent predicted in [9]

on the basis of

heuristic arguments. We find a critical value for the initial

strategy valuations above which this solution no longer

exists, and is being replaced by an alternative solution with a vanishing

volatility of the form .

Our dynamical approach allows in addition for the calculation of the two-time

correlations in the global market fluctuations, by definition

inaccessible with equilibrium methods (replica or otherwise),

which are found

to have a persistent component.

Numerical simulations confirm our theoretical results convincingly.

II Model Definitions

There are agents playing the game. We will only consider the case where

is very large, and ultimately take the limit .

The agents are labeled with Roman indices etc. At each iteration round

all agents are given the same (as yet unspecified)

piece of external information , chosen randomly from a total number

of possible values, i.e. .

In the original model [1] the history of the actual market is used as the information

given to the agents.

Each agent has strategies

at her disposal with which to determine how to

convert the external information into a trading decision, with .

Each component is selected randomly and independently

from before the start of the game, with uniform probabilities, and remains fixed throughout

the game. The strategies thus introduce quenched disorder into the model.

Each strategy of every agent is given an initial valuation or pay-off .

The choice made for these initial values will turn out to be crucial for the emerging behaviour of the

market. Given a choice made for the external information presented at

the start of round , every agent selects the strategy

which for trader has the

highest pay-off value at that point in time, i.e. , and

subsequently makes

a binary bid . The

(re-scaled) total bid at stage is defined as

. Next all agents update the pay-off values of each

strategy on the basis of what would have happened if they had played

that particular strategy:

The minus sign in this expression has the effect that strategies that would have produced a

minority decision are appreciated.

This setup so far allows for an arbitrary number of strategies . The qualitative

behaviour of the market fluctuations,

however, is found to be very much the

same for all non-extensive number of strategies larger than one

[11]. We therefore present results here only for the model,

where the equations can be simplified considerably upon

introducing for each agent the instantaneous difference between the two strategy valuations,

, as well as the

average strategy and

the difference between the

strategies

. The actually selected strategy in round can now be written

explicitly as a function of ,

viz. , and the

evolution of the difference will now be given by:

(1)

with .

It has been observed in numerical simulations, see e.g.

[12],

that the magnitude of the market fluctuations remains almost unchanged if a

large number of bids are performed before a re-evaluation of the strategies is carried out.

This is the motivation for us to study a modified (and simpler)

version of the dynamics of the game, where, rather than allowing the strategy pay-off valuations to

be changed at each round, only the accumulated effect of a

large number of market decisions is used to change an agent’s strategy

pay-off valuations. This amounts to performing an average in the above dynamic equations

over the choices to be made for the external information. If we also change the time-unit

accordingly

from (which measured individual rounds of the game) to a

new unit which is proportional to the number of pay-off validation updates,

we arrive at

(2)

where and

, and with

;

here . The above particular choice of time

scaling has been made only in view of it giving the simplest equations later.

To make a connection with the original game, one must interpret the

evolution of the as described by (2) as the

accumulated effect of order iterations in the original model.

Equation (2) defines the version of the minority game analysed in this paper.

It has been argued

[12] that (2) can be converted into a continuous time

limit of equation (1), upon replacing by

. Strictly speaking, this is not true. A number of

agents change their preferred strategy at every iteration of

equation (2). The size of their ’s will be of the order of

(half) the step size. In the continuous time limit, in contrast,

this step size is lost; yet any discretisation

used to integrate the continuous time differential equation obtained will

effectively re-introduce an (arbitrary) scale for the . This is not so

relevant when the only appearance of the is in , but it is

of importance in the so-called Thermal Minority game [13], where terms

like appear. We therefore prefer the difference equation

(2) over its continuous counterpart, and regard (2) as the equivalent

of what in the neural networks literature would be called the ‘batch’ version of the

conventional ‘on-line’ minority game. For a more detailed discussion

concerning the validity of a continuous time differential equation for

the TMG we refer to [13, 4, 14].

Finally, the magnitude of the market fluctuations, or volatility, is given by

. From the starting point

and on the time scales of the process (2), one easily derives

(3)

(4)

Purely random trading corresponds to and

.

We will also define a more general object, the volatility matrix

:

(5)

which measures the temporal correlations of the market fluctuations.

Note that .

In the case where

the average bid is zero (which will turn out to happen in the present

model), the volatility measures the efficiency of the market.

Zero volatility

implies that supply and demand are always at the same level, and that

the market is extremely efficient. A large volatility implies large

mismatches between supply and demand, and is the signature of an inefficient

market.

III The Generating Functional

There are two compelling reasons for studying the dynamics of the

minority game. Firstly, dynamical techniques do not rely on the

presence of a Lyapunov-function, so that the MG can be studied for

small . Secondly, it is clear from our

simulations, see the figures below, that, at least on the relevant

time-scales, the stationary state of the minority game can depend

quite strongly on the initial conditions. One canonical tool to deal

with the dynamics of the present problem is generating functional

analysis à la De Dominicis [10], originally developed in

the disordered systems community (to study spin glasses, in

particular). This formalism allows one to carry out the disorder

average (which here is an average over all strategies) and take the

limit exactly. The final result of the analysis is a set

of closed equations, which can be interpreted as describing the

dynamics of an effective ‘single agent’ [10, 15]. Due

to the disorder in the process, this single agent will acquire an

effective ‘memory’, i.e. she will evolve according to a non-trivial

non-Markovian stochastic process.

First we rewrite equation (2) as a Chapman-Kolmogorov equation

describing the temporal evolution of an ensemble of markets:

where, in the absence of noise, the transition probability density is

simply

with the short-hand .

The moment generating functional for a stochastic process of the

present type is defined as

By taking suitable derivatives of the generating functional with respect to the

conjugate variables , one can generate all moments of

at arbitrary times. Upon introducing the two short-hands:

as well as

,

and

(with similar definitions for , and , respectively),

the generating functional takes the following form:

(8)

where we have introduced auxiliary driving forces to generate

averages involving (these can be removed later).

IV Disorder Averaging

At this stage we can carry out the disorder averages, to be

denoted as , which involve the variables

and

only. For times which do not scale with one obtains:

where we

have introduced

,

, and

.

We isolate these functions via the insertion of appropriate

-functions (in integral representation), and define

the corresponding short-hands , and

(with similar definitions for , and ,

respectively).

Upon assuming simple initial conditions of the form , the -dependent terms in the disorder-averaged generating functional (8)

are now found to factorise fully over the traders,

and we arrive at an expression of the following form:

(9)

The sub-dominant term in the exponent is

independent of the generating fields and

.

There are three distinct leading contributions to the exponent in (9).

The first is a

‘bookkeeping’ term, linking the two-time order parameters to their

conjugates:

The second reflects the statistical properties of the players’

arsenal of strategies:

(11)

The third term, which contains the generating fields, will describe the (now

stochastic) evolution of the strategy valuations of a single effective agent:

with and with

,

,

(similar definitions for , and

).

The form of Eq. (9) is suitable for a saddle-point integration

in the thermodynamic limit .

With a modest amount of foresight we define . Upon taking derivatives with respect to the generating fields

, and using the built-in normalisation , we find that at the relevant saddle-point:

(12)

(13)

(14)

The first two are recognised to represent

disorder-averaged and site-averaged correlation- and response

functions.

At this stage the generating fields are in principle no longer needed. We will

put and , and find our

expression for simplifying to

(16)

Extremisation of the extensive exponent of (9) with respect to

gives the saddle-point equations

(17)

(18)

whereas . The effective single-trader

averages , generated by taking

derivatives of (16), are defined as follows (note: ):

(21)

Upon elimination of via (18),

we have now obtained exact closed equations

for the disorder-averaged correlation- and response functions in the limit: namely

(17), with the effective single trader measure

(21).

V Simplification of the Saddle-Point Equations

The above procedure is quite insensitive to changing model details;

alternative choices made for the statistics of traders’ strategies would

simply lead to a different form for the function

(11), whereas changing the update rules for the strategy valuations of

the traders (e.g. by making these non-deterministic, as in

[13, 4]) would only affect the details of the term

(16). We now work out our equations for the present

choice of model.

Focusing first on , we perform the integrals, yielding

, and after performing the remaining

integrations we get

The Gaussian integration over the gives

where the entries of the matrix are given by .

We now take the derivative of with respect to , as

dictated by (18), and subsequently put all .

This gives

and , so that

We now write our final result in terms of the response function

(13), via the identity , and find

our effective single trader measure of

(21) reducing to

(22)

(23)

This describes a stochastic single-agent process of the form

(24)

Causality ensures that for all

(so that for ), and

is a Gaussian noise with zero mean and with

temporal correlations given by

:

(25)

The correlation- and response functions, defined by

(12,13), are the dynamic

order parameters of the problem, and must be solved

self-consistently from the closed equations

(26)

Note that as given by

(23)

is normalised, i.e. , so

the associated averages reduce to .

The solution of (26)

can be calculated numerically with arbitrary precision, without

finite size

effects, using a technique described in [16].

Finally, in appendix A we

calculate the disorder averaged re-scaled average bid and

volatility matrix ,

for ,

as defined previously in (3) and

(5).

Note that objects such as must asymptotically become self-averaging,

i.e. independent of the microscopic realisation of the

disorder; hence for .

We find the satisfactory result that the average bid is zero, and that the volatility

matrix (and thus also the ordinary single-time volatility

)

is proportional to the covariance matrix

(25) of the noise in the dynamics

(24) of the effective single agent:

(27)

Thus the noise term in the single agent process

(24) represents the overall market

fluctuations, and the covariance matrix

(25) informs us of both single-time volatility and

the temporal correlations of the market fluctuations.

VI The First Time Steps

For the first few time steps it is possible to calculate

the order parameters (correlation- and response functions) and the volatility

explicitly, starting from the effective single trader measure

(23). Note that and that

for any . Significant

simplifications can be made by using causality. For instance, we

always have , with

causality enforcing

(28)

At this immediately allows us to conclude that

.

We now obtain from (23) the joint statistics at times :

(29)

Equation (29), in turn, allows us to calculate

and :

We can now move to the next time step, again using (28), where we need the noise

covariances and :

Although this procedure can in principle be repeated for an arbitrary number of time steps,

generating exact expressions for the various order parameters iteratively,

the results become increasingly complicated when larger times are involved.

It is interesting, however, to inspect further some special limits.

We first turn to the (trivial) case where

is very small, and is finite.

Provided as , we immediately deduce

from the above results that , , and . Hence we find in leading order in that

and . One easily repeats the argument

for larger times, and finds that, without perturbations, both the system variables and the noise variables

will remain frozen for times , the only remaining uncertainty in the noise being the realisation of

:

If ,

the system will ‘de-freeze’

at the first instance where .

Since is a zero average Gaussian

variable, one should therefore for small expect half of the population of traders

(those with non-profitable initial random strategy choices) to

commence strategy chances at time-scales

,

whereas the other half will continue playing the game

with their (for now profitable) initial strategy choices at least up to

.

It is also interesting to analyse the case where the game is initialised

in a tabula rasa manner (which appears to have been common practice in literature),

i.e. with

, and where we have no perturbation fields, i.e. .

Now the above results reduce to

The negative value of the correlation function implies that for short times

the traders will exhibit a tendency to alternate their (two)

strategies.

Let us now inspect the limiting behaviour of the above expressions

for large and small values of . For large one

obtains

In other words, the agents trade independently and randomly; for

larger times this will continue to be the case. For small

, on the other hand, we find

So , whereas

. We also find

from which it follows that , and hence

we can write the first steps of the effective single agent equation (24) as

Thus also

and .

We observe that for small the first two time steps are

driven predominantly by the noise component in

(24). This noise component increases in strength

and starts oscillating in sign, resulting in an effective agent which

is increasingly likely to alternate its strategies.

Equivalently, this implies that in the initial -agent system an increasing

fraction of the population of agents will start alternating their strategies.

Let us finally inspect the initial behaviour of equation

(24) for the intermediate regime where

with , to which (as we have seen) also for

about half of the traders

will automatically be driven in due course.

We now put and find in leading

order:

Thus we have ,

so also ,

in leading order for .

This then, together with (which

immediately follows from (29)), leads us to

We thus find that also for the initial conditions are

more or less washed out by the internal noise generated by the process,

within just two iteration steps.

VII The Stationary State for

For general , not necessarily small, the arguments used in

the second part of the previous section do not hold. In a

stationary state, along with agents that will change strategy

(almost) every cycle, there will generally also be agents finding

themselves consistently in the minority group, which will

consequently play the same strategy over and over again. For the

latter ‘frozen’ group (a term introduced in [17]),

the differences between the valuations of

the two available strategies (i.e. the values of ) will grow more

or less linearly in time, whereas the ‘fickle’ agents will have

values for very close to zero. In order to separate the two

groups efficiently we introduce the re-scaled values

. Frozen agents will be those for which

. Similarly the effective

single agent process (24) is transformed via

, where now the quantity

will give the asymptotic fraction of ‘frozen’ agents in the

original -agent system, for . The dynamical

equation of the re-scaled effective agent can be written as

(31)

If the game has reached a stationary state, then

,

and , by

definition. We will in this section assume that the stationary

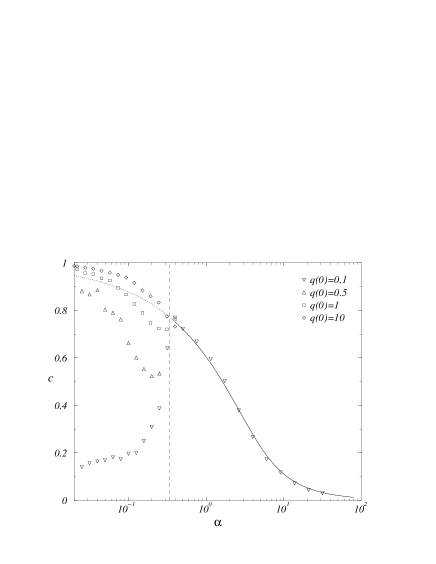

FIG. 1.:

Asymptotic average

of the stationary covariance. The

markers are obtained from individual simulation runs performed with a system of

agents and various

homogeneous initial valuations (where ), and in excess of 1000 iteration steps.

The solid curve to the right of the

critical point is the theoretical prediction, given by the solution of

(36).

The dotted curve to the left is its continuation into the regime

(where it should no longer be correct).

state

is one without anomalous response, i.e. temporary perturbations will

not influence the stationary state and

decay sufficiently fast, such that

exists. This condition will be met if

there is just one ergodic component; it is the dynamical equivalent of replica symmetry

being stable (see e.g. [18]) in a detailed balance model.

We now define

(assuming this limit exists) and take the limit in Eqn.

(31). Under the assumption of absent anomalous response,

we can use the two lemmas in appendix B to simplify the result to

(32)

with the averages and

.

The variance of the zero-average Gaussian random variable

follows from

(25):

(33)

(34)

(35)

Note that .

The effective agent is frozen if , in which case

. This solves equation (32) if and

only if . If

, on the other hand, the

agent is not frozen; now

and

.

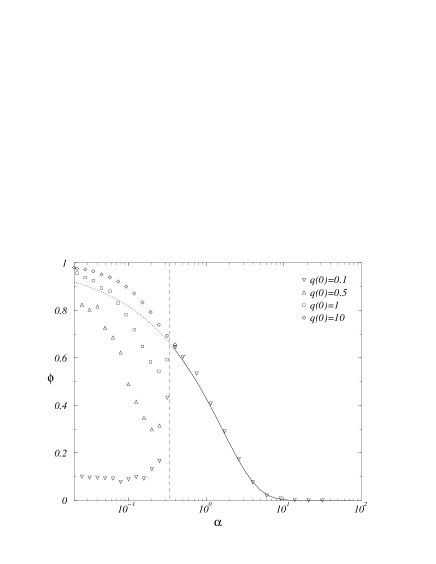

FIG. 2.:

Fraction of frozen agents

in the stationary state.

The markers are obtained from individual simulation runs performed with a

system of agents and various

homogeneous initial conditions, where , and

in excess of 1000 iteration steps.

The solid line to the right of

the critical point is the theoretical prediction, obtained from

the solution of (36).

The dotted curve to the left is its continuation into the regime

(where it should no longer be correct).

We can now calculate self-consistently, upon distinguishing

between the two possibilities:

Working out the Gaussian integrals describing the statics of

,

with variance (35), then gives

(36)

From this equation the value of can be solved numerically.

For large the solution behaves

as .

In figures 1

and 2

we show the solution of

(36) and the fraction

of frozen agents, given according to the theory by

,

as functions of , together with the

values for and as obtained by carrying out numerical simulations

of the minority game.

One observes excellent agreement between theory and experiment

above a critical value , which we will calculate below.

From the time-averaged asymptotic correlation we next move on

to calculate the integrated response

. Since the occurrence of

the Gaussian noise term in Eqn.

(24) is (apart from a factor ) similar to that of

an external field, we can write the response function as

. Integration by parts in this expression generates

and hence

(37)

Averaging over the two times and now gives

in a stationary state, upon using again the assumption of absent

anomalous response

(and the familiar notational conventions and ):

(38)

(39)

The variance is given in

(35). We calculate the remaining object

similarly to our calculation of , by

distinguishing between frozen and non-frozen agents and by using

the two identities (for frozen agents) and

(for the non-frozen ones), both of

which follow immediately from (32).

This results in

Insertion into (39), together with

(35), then gives the desired expression for

the integrated response:

(40)

with the value of to be determined by solving Eqn.

(36). Equivalently,

using we get

(41)

The integrated response is positive and finite, and hence our solution

(based on this property) is exact, for . Here

is the point at which diverges, which is found to happen when

the fraction of fickle agents equals . According to

(36,40) we can write as , where

is the solution of the transcendental equation

(42)

The resulting value

is identical to that found in [4]

(for a stochastic version of the game) using replica calculations. Below

there might well be multiple ergodic components,

i.e. more than one stationary solution of our fundamental order

parameter equations (26).

VIII Stationary Volatility for

In contrast to the persistent order parameter and its

relative , the volatility matrix (5), to be calculated within

our theory from expressions (25,27)

and in a stationary state of the Toeplitz form

,

generally involves both

long-term and short-term fluctuations.

This becomes apparent when we work out using

(25) and the results of

appendix B.

We separate in the functions and the persistent from the

non-persistent terms, i.e. and

(there is no persistent response for ),

and find

(44)

Clearly, the asymptotic (stationary)

value of the volatility

cannot be

expressed in terms of persistent order parameters only.

It requires solving our

coupled saddle-point equations (26) for

and for large times but finite

temporal separations .

The persistent market correlations,

however, are found to be expressible in terms of persistent order

parameters:

(45)

In order to find the volatility we separate

the correlations at stationarity in a ‘frozen’ and a ‘fickle’ contribution:

We note

that the sum

, is

the retarded self-interaction term in equation

(24). Such a term is a familiar ingredient

of disordered systems with ‘glassy’ dynamics (see e.g. [19]),

and generally acts as the mechanism

which drives the system to a ‘frozen’ state.

Hence, self-consistency of the distinction between frozen

FIG. 3.: The volatility as a function of the relative number of

possible values for the external information.

The markers are obtained from individual simulation runs performed with a

system of agents and various

homogeneous initial conditions, where , and

in excess of 1000 iteration steps. The solid

curve for is the approximate expression

(50). Below the approximate asymptotic solutions

of Eqns. (80) (solid) and (81) (dashed) are drawn.

and

fickle traders dictates that the retarded self-interaction

term can be large for frozen traders, but must be

small (if not absent) for fickle ones.

Our approximation now consists in consequently disregarding

the retarded self-interaction for the fickle traders:

Thus we retain for fickle traders

only the instantaneous term in

, and find the (exact)

expression (49) being replaced by the

approximation

(50)

This turns out to be a surprisingly accurate

approximation of the volatility for ,

as can be observed in Fig. 3.

Only in the limit can we expect to be able to

go beyond (45) and (50), and work out

expressions (44) and (49) exactly. This requires

calculating the response function for small

, which we will set out to do next.

Since we assume absent anomalous response we may choose

trivial initial conditions. We also choose the perturbation

fields to be non-zero only for a given time , where .

From (24) we now derive

(52)

Hence, for vanishingly small perturbations , and

upon taking

the limit:

We observe that is precisely the

condition for a trader to be fickle, in the language of the

effective single agent. Secondly, from

causality it follows that

.

Hence our result can in a stationary state be written as

(53)

For our stationary order parameter

equations give .

Furthermore, for all traders will become fickle, so

. This leaves for only the trivial solution

for equation (53):

for all .

Insertion into our exact expression (44) for the

stationary volatility matrix

gives

and hence

(54)

This is the random trading limit.

IX The Stationary State For

When the amount of external information available for agents to base their

actions upon (i.e. the value of ), becomes small, the behaviour of the

market is found to become strongly dependent on initial conditions.

Numerical simulations show that below the sequence is

unbounded, and that within the limits of experimental accuracy:

(55)

(56)

(with , by definition).

Figure 4 shows the

asymptotic values of as measured during numerical simulations,

for different values of and .

One clearly observes the dependence on initial

conditions.

FIG. 4.:

The oscillatory component of the covariance (see equation (56)). The

markers represent the results of individual simulations, performed with agents and various

homogeneous initial conditions, where , and after in excess of 1000 iteration steps.

We will now use (55,56) as

ansätze, i.e. we will construct special self-consistent

stationary state solutions of the

fundamental order parameter equations (26) which

obey (55,56), as well as the

stationary state conditions and

.

First we analyse the statistical properties of the Gaussian noise

in the single agent

equation (24). From

(55,56) it follows that the noise

covariance matrix (25) obeys

(58)

in which

(59)

From (58) one can derive, in turn, that the

noise variables must asymptotically take the form:

(60)

where and are zero-average Gaussian variables,

with , , and

Due to (55) we know that , i.e. in the stationary state the decorrelate for large

temporal separations.

For sufficiently large , and without external perturbations, equation (24)

now acquires the form

(62)

Frozen agents are those for which is independent

of time; due to (55) these will not experience the

last term in (62).

However, due to the properties of the noise in the

regime (and in contrast to the situation with ), even

frozen agents will now have

.

Insertion into Eqn.

(62) shows that frozen solutions of the following form

exist:

(63)

provided for all , so and must obey

(64)

Oscillating agents, on the other hand, are those for which , with .

Insertion into Eqn.

(62) shows that oscillating solutions of the following form

exist:

(65)

provided for all , so and must obey

(66)

Note that, if rigorously frozen and/or rigorously oscillating agents were to be

asymptotic solutions of

(62), then the correlations would have come

out as (with , as before, denoting the

fraction of frozen agents), and we would have found .

Figures 1 and 4, however, show that this

simple relation holds only near . Away from there will therefore

be solutions describing fickle agents which change strategy at

intervals intermediate between one (oscillating) and infinity

(frozen).

This can be understood on the basis of

(62), where due to the noise term (with

a finite temporal correlation length) there will for always be a non-zero probability

of nearly frozen agents changing strategy occasionally, and of nearly

oscillating agents not changing strategy occasionally.

X The Limit

Let us finally investigate the situation near more

closely, where we may use the experimental observation

that , which implies that all agents will be either

frozen or oscillating. We put (the fraction of frozen agents) and

, and choose homogeneous initial conditions with

. We now find

and

our two solution types given by:

provided the following respective conditions for existence are met:

(67)

(69)

Near we also know, due to , that

(70)

(71)

and that

.

In order to eliminate the remaining parameters and

we note that time translation invariance guarantees the validity

of the relation

, and hence

(72)

The quantity can, in turn, be expressed in terms of upon inserting

(70,71) into

(37). We obtain

Working out the average in the right-hand side, by separating frozen from

fickle solutions, gives for large :

Since in a stationary state the correlation function

can only depend on

, we must conclude that

and that either

(73)

(in leading order for ).

Multiplication of both sides of the second equation in (73) by shows that

it automatically ensures the validity of

the second condition of (69).

The first equation of (73) will satisfy

the second condition of (69) as long as .

In order to proceed we need to calculate the persistent term in

the proposed solutions, which can be seen as representing their ‘effective initial conditions’.

It incorporates both the true initial

conditions and the effects of the transients of the dynamics, which initially

will not be of the

simple form (62). Exact evaluation would

require solving our order parameter equations for arbitrary times,

which is not feasible. However, one can for now proceed on the

basis of the postulate that the properties of the long-term attractors (viz. the Gaussian

variable ) are uncorrelated with the value of .

The conditions (67,69)

then simply state whether a value of , generated independently of according to

some distribution ,

is compatible with a given attractor.

Although we will not be able to generate all possible

stationary solutions of the process (24), we

will show how two qualitatively different solutions, one with a diverging volatility for and one with

a vanishing volatility for , can both be extracted from our

equations.

The first type of solution is obtained for . Now one finds, in leading order in

, that and that .

The conditions (67,69)

reduce in leading order to the complementary pair

(74)

(75)

This, in turn, allows us to calculate and :

We eliminate in favour of

and end up with the following simple closed equation for :

(76)

The associated value for then follows from:

(77)

Finally we can use our observations

regarding the first few time-steps (section VI) of the process in order to obtain an estimate for .

These showed for small that

initially

(i) for small the system is driven towards

the oscillating state, (ii) for large the

system tends to freeze, (iii) the transient processes are

dominated by the (Gaussian) noise term in (24),

and

FIG. 5.:

Experimental evidence in support of the existence of a critical value

for the initial strategy valuation below

which a high-volatility solution exists.

The connected markers represent the results of measuring the volatility

in individual simulations, performed with agents and initial conditions where ,

and after in excess of 1000 iteration steps.

CPU and memory limitations prevent us from doing reliable and

conclusive

experiments for ; the available data, however, are

clearly not in conflict with

our theoretical prediction

(vertical dashed line), which follows from equation

(78).

(iv) the noise term is automatically being ‘amplified’ (either

via a diverging response function, or via accumulation over time)

to an effective

contribution.

Note that (i) and (ii) confirm that can indeed be

seen as the sum of and the net effect of the transient

processes, and that (iii) and (iv) subsequently suggest

representing the transient processes by adding a single effective Gaussian

variable.

Hence for small it would appear sensible to write

,

which converts (76,77)

into

We conclude that can be written in terms of the solution of a

transcendental equation

(78)

For we find that ,

hence we must obviously require .

The associated value for then follows from:

(79)

Since we cannot calculate or estimate the width

of the effective Gaussian noise term without solving our order parameter equations for short times

( could even depend on ),

it is quite satisfactory that

several interesting properties of the solution are found to be independent

of . For instance, one always finds a diverging volatility of the form ,

and there is a critical value such that for

the solution no longer exists.

This solution is clearly the type of volatile state which has been reported regularly (see e.g.

[8, 9])

upon observing numerical simulations. We have now found, however, that

whether or not it will

appear depends critically on the choice made for the initial conditions.

Numerical simulations indeed appear to support the existence and predicted magnitude of a

critical value (see figure 5); fully conclusive

experiments, however (with even smaller values of ),

would require impractical amounts of CPU and/or memory

in order to meet the requirements and for

increasingly small values of , and are presently ruled out.

In the limit one can easily carry out the integrals in

(79), giving

. Elimination of

via insertion into

then leads to the simple relation

(80)

This is the high-volatility solution shown in the regime of figure

3, with as measured in simulations

(see e.g. figure 2). The power of in (80) is

observed to be correct. The observed difference between theory and experiment

with regard to the prefactor can be understood as a

reflection of our approximation ; this amounts to

disregarding deviations from the idealized ‘purely frozen’ or

‘purely oscillating’ behaviour, which can indeed be expected to

give an approximate theory which (even for small ) slightly under-estimates the

volatility.

We note that the condition for the above reasoning to apply

can in fact be

weakened to .

The above solution ceases to hold, however, at the point where the fraction of frozen agents

scales as , in which case we

have to turn to the first option in

(73), rather than the second.

This is consistent with our previous observation that small values of

lead to a relatively small fraction of frozen agents (and a large volatility),

whereas for large such a solution will break down

in favour of states with a larger fraction of frozen agents.

Since we can now no longer use the second equation in

(73) to determine , and hence find

the volatility ,

we have to return to (72). A fully frozen state,

which for will indeed be described by this second type of solution

(since ), must necessarily have

. This is consistent with our ansätze, since

it gives

which implies , provided

. We can now calculate from (72) and

find .

Thus we obtain, provided :

FIG. 6.:

Experimental evidence for the existence of the limit

for the low-volatility solution. The

markers are obtained from individual simulation runs performed with a system of

agents and initial valuations of the form (to evoke the low-volatility state),

and in excess of 1000 iteration steps.

The solid curve to the right of the

critical point is the theoretical prediction, obtained from

the exact equations (36) and

describing the regime.

The dotted curve to the left is its continuation into the regime

(where it should indeed no longer be correct).

We also note that the scaling property

implies that , since

all values of order

will contribute to the fraction of fickle

agents, giving .

We can now calculate upon explicitly inspecting

the effect of a perturbation of a frozen state. In view of

we may restrict ourselves to considering the effect on

of a perturbation at time , giving in leading order for :

Hence, since the frozen state has , we find and

(81)

Explicit calculation of the prefactor in

(81) would require taking our calculations beyond the

leading order in , in order to determine to find .

Equation (81)

is the low-volatility solution shown in the regime of figure

3, with as measured in simulations

(see e.g. figure 6). Again the power of in (81) is

observed to be correct. The remaining difference between theory and experiment

with regard to the prefactor can again be understood as a

reflection of our approximation , which induces a structural under-estimation of the

volatility.

XI Discussion

In this paper we have solved a ‘batch’ version of the

minority game with random external information, using

generating functional analysis (or dynamic mean field theory)

á la De Dominicis, which allows one to carry out the disorder averages in a dynamical context.

Since the dynamics of the game is not described by a detailed balance type stochastic process, equilibrium

statistical mechanical tools can not be applied directly. Phase

transitions (if present) must be of a dynamical nature.

The disorder in the minority game consists of the microscopic realisation of the

repertoire of randomly drawn trading strategies of the agents. Upon taking the limit

(where denotes the number of agents playing the game) one ends up with an exact non-Markovian

stochastic equation describing the dynamics of an effective single agent (24),

whose statistical properties are identical to those of the

original system (averaged over all realisations of the disorder).

The key control parameter in this problem is the ratio

of the number of possible values of the external information over

the number of agents.

We find a phase transition at , signaled by the

onset of anomalous response, in agreement with the value reported

recently in [4]. The method used in

[4] depends on the fact that for their stochastic

version of the minority game a Lyapunov function exists. Our approach

does not have this constraint and can be easily applied to those

variations of the game where a Lyapunov function is not available,

thus opening up a wider range of models for analysis (see

e.g. [3]). Above (where anomalous response is

absent) we can solve the stationary state of the system exactly,

giving exact expressions for quantities such as the fraction of frozen

agents (which is zero for but increases with

decreasing ), the persistent two-time correlations, and the

persistent correlations in the total bid. The volatility (which is

itself not an order parameter of the system) can be calculated to a

very good approximation. Above , our method and that of

[6, 4] are likely to describe the same

behaviour [20]. Below , i.e. in the region of

complex dynamics (inaccessible by the replica approach

[14]), our present method still applies. In this region

we demonstrate the existence of multiple stationary states, and derive

expressions for the relevant observables in leading order in

as . We show, more specifically, that the occurrence and

practical observability of a diverging volatility for

(as reported in e.g. [8, 9]) is

crucially dependent on the overall degree of a priori preference

for specific strategies exhibited by the agents at , which may

explain the different observations regarding the

behaviour which have been reported in literature

[12]. More specifically, our theory points at the

existence of a critical value for the initial strategy valuations,

above which the system will revert to a state with vanishing

volatility. Our theoretical predictions find quite satisfactory

confirmation in numerical simulations.

The fact that we can analyse the stationary state of

Eqn. (24), in spite of it describing a non-Markovian

stochastic process, suggests that the present method should also be

suitable to deal with models where the external information depends on

time, or on the previous behaviour of the agents, as in the original

model [1].

ACKNOWLEDGMENTS

We would like to thank Andrea Cavagna and David

Sherrington for introducing us to the Minority Games and Matteo

Marsili for a discussion of previous work done. JAFH wishes to thank

King’s College London Association for financial support.

REFERENCES

[1]

D. Challet and Y.-C. Zhang, Physica A 246, 407 (1997).

[2]

W. Arthur, Am. Econ. Assoc. Papers and Proc. 84, 406 (1994).

[3]D. Challet, http://www.unifr.ch/econophysics/minority (an

extensive commented collection of work on the minority game).

[4]

D. Challet, M. Marsili, and R. Zecchina, Phys. Rev. Lett. 84, 1824

(2000), cond-mat/9904392.

[5]

M. Marsili, D. Challet, and R. Zecchina, Physica A 280, 522 (2000),

cond-mat/9908480.

[6]

A. D. Martino and M. Marsili, cond-mat/0007397 (unpublished).

[7]

N. Johnson, M. Hart, and P. Hui, cond-mat/9811227, (unpublished).

M. Hart, P. Jefferies, P. Hui, and N. Johnson, to appear in Eur.J.Phys. B,

cond-mat/0008385.

M. Hart, P. Jefferies, and N. Johnson, to appear in J.Phys.A, cond-mat/0005152.

[8]

R. Savit, R. Manuca, and R. Riolo, Phys. Rev. Lett. 82, 2203 (1999).

[9]

R. Manuca, Y. Li, R. Riolo, and R. Savit, Technical Report No. pscs-98-11-001,

University of Michigan, (unpublished),

www.pscs.umich.edu/RESEARCH/pscs-tr.html.

[10]

C. De Dominicis, Phys. Rev. B 18, 4913 (1978).

[11]

A. Cavagna, Phys. Rev. E 59, R3783 (1999).

[12]

J. Garrahan, E. Moro, and D. Sherrington, Phys. Rev. E 62, R9 (2000),

cond-mat/0004277.

[13]

A. Cavagna, J. Garrahan, I. Giardina, and D. Sherrington, Phys. Rev. Lett. 83, 4429 (1999), see also the comments by Challet et al. 2000

cond-mat/0004308 and the reply by Cavagna et al. 2000 cond-mat/0005134.

[14]

M. Marsili and D. Challet, to appear in Adv. in Complex Sys., cond-mat/0004376.

[15]

H. Sompolinsky and A. Zippelius, Phys. Rev. B. 25, 6860 (1982).

[16]

H. Eissfeller and M. Opper, Phys. Rev. Lett. 68, 2094 (1992).

[17]

D. Challet and M. Marsili, Phys. Rev. E 60, R6271 (1999),

cond-mat/9904071.

[18]

M. Mézard, G. Parisi, and M. Virasoro, Spin Glass Theory and Beyond

(World Scientific, Singapore, 1987).

[19]

K. H. Fischer and J. A. Hertz, Spin Glasses (University Press, Cambridge,

1991).

[20]

Private communication with M. Marsili.

A Expressions for Average Bid and Volatility

First we calculate

using expression (3).

We note that we obtain simply by making the replacement

in

the right-hand side of Eqn. (8).

The disorder average is carried out as before, but instead of Eqn. (9)

we now obtain

where we have used permutation invariance with respect to

(after the disorder average). The integral is dominated by the familiar saddle-point.

Since the term in the

exponent is identical to that in (9), we can

now simply use the identity to show that

(A2)

(A3)

The last step follows immediately from the anti-symmetry

of the integrand under overall reflection.

To determine the disorder-averaged volatility matrix, which for

becomes identical to due to

(A3) and the self-averaging property,

we first work out

the dominant terms in (5). Using , we obtain the relatively simple

expression

We calculate this average by making the replacement

in

the right-hand side of Eqn. (8).

Repeated integration by parts over the shows that we may equivalently put

.

Following the steps we also took in calculating

now gives

(A5)

(A6)

(A7)

B Consequences of Absence of Anomalous Response

Lemma 1

Consider two bounded sequences of real numbers and .

Because is bounded, there exists a number such

that . Define ,

and assume that . Then

Proof

Upon substituting of we find

The sequences and are bounded, so there exist

numbers and such that and for all

. The sequence converges to , so for any

there exists an such that for all :

. We now choose such that for all ,

and

. Then we find for all :

Hence the limit is as claimed.

Lemma 2

Suppose , where for all and

with , and suppose

. Then for

all :

Proof

The proof proceeds by induction. For , the statement is trivially true.

Suppose now that it is true for all . Then

The sequence

satisfies the conditions of the preceding

lemma, application of which gives

Hence the claim holds for , and

by induction it is now proved for all .