Multifractal returns and Hierarchical Portfolio Theory ††thanks: We are grateful to E. Bacry, U. Frisch and L. Martellini for helpful discussions.

Abstract

We extend and test empirically the multifractal model of asset returns based on a multiplicative cascade of volatilities from large to small time scales. Inspired by an analogy between price dynamics and hydrodynamic turbulence [Ghashghaie et al., 1996; Arneodo et al., 1998a], it models the time scale dependence of the probability distribution of returns in terms of a superposition of Gaussian laws, with a log-normal distribution of the Gaussian variances. This multifractal description of asset fluctuations is generalized into a multivariate framework to account simultaneously for correlations across times scales and between a basket of assets. The reported empirical results show that this extension is pertinent for financial modelling. Two sources of departure from normality are discussed: at large time scales, the distinction between discretely and continuously discounted returns lead to the usual log-normal deviation from normality; at small time scales, the multiplicative cascade process leads to multifractality and strong deviations from normality. By perturbation expansions, we are able to quantify precisely on the cumulants of the distribution of returns, the interplay and crossover between these two mechanisms. The second part of the paper applies this theory to portfolio optimisation. Our multi-scale description allows us to characterize the portfolio return distribution at all time scales simultaneously. The portfolio composition is predicted to change with the investment time horizon (i.e., the time scale) in a way that can be fully determined once an adequate measure of risk is chosen. We discuss the use of the fourth-order cumulant and of utility functions. While the portfolio volatility can be optimized in some cases for all time horizons, the kurtosis and higher normalized cumulants cannot be simultaneously optimized. For a fixed investment horizon, we study in details the influence of the number of periods, i.e., of the number of rebalancing of the portfolio. For the large risks quantified by the cumulants of order larger than two, the number of periods has a non-trivial influence, in contrast with Tobin’s result valid in the mean-variance framework. This theory provides a fundamental framework for the conflicting optimization involved in the different time horizons and quantifies systematically the trade-offs for an optimal inter-temporal portfolio optimization.

1 Introduction

Inspired by an analogy with turbulent cascades in hydrodynamics comparing the energy flow to an information transfer, recent empirical works have shown that return volatilities exhibit long-range correlations organized in a hierarchical way, from large time scales to small time scales [Ghashghaie et al., 1996; Arneodo et al., 1998a; Muzy et al., 2000; Breymann et al., 2000]. The Olsen group in Zurich discovered independently this phenomenon which they called the HARCH effect [Müller et al., 1997; Dacorogna et al., 1998]: in the foreign exchange market, the coarse-grained volatility predicts the fine-grained volatility better than the other way around. They also found this effect for the implied forward rates derived from Eurofutures contracts [Ballocchi et al., 1999].

The underlying cascade or hierarchical structure provides also a natural explanation and a model for the multifractal description of stock market prices documented by several authors [Fisher et al., 1997; Mandelbrot, 1997; Vandewalle and Ausloos, 1998; Brachet et al., 1999; Bershadskii, 1999; Ivanova and Ausloos, 1999; Mandelbrot, 1999; Schmitt et al. 1999; Pasquini and Serva, 2000] (see however Bouchaud et al. (2000)).

The first purpose of the present paper is to provide additional empirical confirmations that such hierarchical description accounts very well for the return statistics, especially for the strong leptokurticity of the probability density functions at small scales and for the volatility serial correlations. This hierarchical framework shares a crucial advantage with models based on the standard geometrical Brownian motions or on Lévy-stable processes, in that it remains a “scale-free” description which can thus be applied to any time scale. As we shall see, this “self-similarity” property is interesting for the problem of portfolio optimization, in particular for the multi-period selection problem.

The portfolio optimization problem consists in finding the optimal diversification on a set of possibly dependent assets in order to maximize return and minimize risk. In its simplest version, one assumes a single period horizon for all investors which, together with the hypothesis that returns are normally distributed, leads to the standard Markowitz’s solution [Levy and Markowitz, 1979; Kroll et al., 1984]. The first results in the theory of optimal multi-period portfolio selection showed that, within the Gaussian hypothesis of return distributions, the investor optimal sequence of portfolio through time is stationary, with constant proportionate holdings of each included asset leading to a constant expected return and risk per unit invested wealth. In other words, the optimal asset weights in the portfolio are time-scale independent. This theorem has been criticised as being not true in general [Stevens, 1972].

Many studies have investigated the impact of time horizon on the portfolio selection. Allowing for investors with different planning horizons, Gressis et al. [1976] have shown that, in absence of the riskless security into the portfolio, the single-period efficient frontier also provides periods efficient frontiers. However, Gressis et al. [1976] find that, with the inclusion of the riskless security, the equivalence among efficient frontiers for different horizons is no longer valid. Departing from the Gaussian model, Arditti and Levy [1975] generalized the mean-variance approach to a three-moment efficiency analysis and showed that all one-period portfolios are not necessarily multi-period efficient because, even if a stock has a symmetric single-period return distribution, its multi-period distribution may be highly skewed. A considerable body of research has explored how portfolio composition depends on the investment horizon. It has been shown that portfolio composition indeed depends on the investment horizon and that any simple characterization of the relationship is treacherous [Gunthorpe and Levy, 1994; Ferguson and Simaan, 1996]. Using a choice criterion that is consistent with the traditional utility approach but which is more amenable to a multiperiod environment, Marshall [1994] has shown that investors should choose progressively less risky single-period portfolios as their investment horizons shorten, even if they do not become more risk averse, both in the presence and in the absence of a riskless asset. Tang [1995] examined the effect of investment horizon on international portfolio diversification using stock indexes of 11 countries. He finds that correlation coefficients between stock indexes increase in general with an increase in the investment horizon, suggesting that diversification benefits are reduced. The fact that various stock markets are more correlated over a longer investment horizon may imply that different stock markets adjust to each other with a delayed pattern. Bierman [1997; 1998] has investigated whether the risk of a stock portfolio increases or decreases as the investment horizon lengthens and whether the portfolio mix depends on the horizon. By moving beyond the logarithmic utility function and by recognizing that different investors have different risk preferences, Bierman [1998] finds that it is possible for stocks to be risky in each time period and to reduce risk by increasing the length of the investment horizon. He also finds that stocks can be rejected if they are to be held for one time period, but can then be accepted if they are to be held for more than one time period. At the origin of these results is the fact that “discrete” returns calculated as the ratio of the price difference over a given time interval over the price are only approximately proportional to times the continuously discounted return . The difference is negligible at short times , corresponding to the validity of the expansion of . At large time scales such that is no more small compared to , the second-order term in the expansion becomes important and effets of non-normality in the distribution of become important. In the present paper, we study another additional cause for non-normality, whose strength grows as short time scales rather than at large time scales.

The paper is organized as follows. In section 2, we recall and make precise the statistical description of the fluctuations of the returns of a single asset in terms of the multiplicative cascade model. The few parameters involved in this model are then interpreted and estimated for a set of high frequency time series. Then, we propose an extension of this framework to vector valued, i.e. multivariate processes corresponding to a basket of assets in a portfolio. This can be done in a very natural way and simple statistical tests are proposed to check for its relevance. In section 3, we address the portfolio problem for such a set of multifractal assets. We first discuss the simplest case of uncorrelated assets where the statistical properties of the portfolio returns can be estimated by means of a cumulant expansion. The problem of portfolio optimization is studied in section 4 using the utility function approach and the higher-order cumulants of the distribution of portfolio returns. A generalisation of the efficient frontier is proposed and studied as a function of time-scales. Section 5 presents the application of the correlated multivariate multifractal model to the portfolio theory. Conclusion and prospects are given in section 6.

2 Multifractal description of asset returns

In the following, we show how multifractal statistics can be described in a simple way using only a few parameters. This description has been developed both for finance data [Arneodo et al., 1998a] and in the field of fully-developed hydrodynamic turbulence [Arneodo et al., 1998b; 1998c, 1999]. As mentionned above, the similarity between turbulence and finance has been suggested by some recent studies [Ghashghaie et al., 1996; Arneodo et al., 1998a; Muzy et al., 2000] and relies on the concept of multiplicative random cascades: the fluctuation at some fine time scale is the product of the fluctuation at a coarser scale by a random factor whose law depends only on the scale ratio . This picture leads to the integral description proposed by B. Castaing and collaborators [Castaing et al., 1990; Chabaud et al., 1994] which links the probability density function (pdf) of fluctuations at scale to the pdf of fluctuations at scale . Let us now introduce this formalism for the pdf’s of asset returns for all time scales.

2.1 Formulation of the multifractal model of the returns of a single asset

Let be the price of asset at time , where time is counted for trading days in multiples of a fundamental unit (say days). With the notation , the return between time and of asset is defined as:

| (1) |

We thus distinguish between the “continuous return” and the “discrete” return . The difference between them is essentially captured by the second order correction , which becomes non-negligible only for large time scales (see below).

We describe the distribution of the variable by using the representation of Castaing et al. [1990; Chabaud et al., 1994] inspired by the above mentionned cascade picture for hydrodynamic turbulence. This distribution is represented, for time scale , as a weighted sum of dilated distributions of the ’s at the intermediate coarser scale ():

| (2) |

where is the mean value of at scale (it is supposed to be linear with consistently with experimental observations) and is the self-similarity kernel whose shape is assumed to depend only on the ratio . As we shall see below, the exponentials are just convenient ways of simplifying the parameterization of the kernel. This model (2) can be derived from a cascade model according to which is written as

| (3) |

where is a -independent Gaussian random variable and the “stochastic volatility” is described by a multiplicative cascade [Arneodo et al., 1998a]:

| (4) |

It is a well-established observation that, at sufficiently large scale, distributions of become Gaussian [Campbell et al., 1997]. Let be such a large scale for which is a Gaussian . Then, for , expression (2) can be rewritten as

| (5) |

is thus a weighted sum of Gaussian distributions and the kernel can be identified with the pdf of the logarithm of the multiplicative weights introduced in Eq.(4), the standard deviation at scale being:

| (6) |

Let and be respectively the mean value and the variance of . We consider the simplest possible case, specifically where is itself Gaussian:

| (7) |

From the semi-group property resulting from the cascade equation, , and using the fact that depends only on the ratio , it is easy to show that and are necessarily linear functions of :

| (8) | |||||

| (9) |

where and are independent of . is the coarse scale defined by a vanishing variance . This time scale is the “integral” scale at which the cascading process of the volatility begins. Performing the change of variable amounts to keep Eq.(5) unchanged and to redefine Eqs (8) and (9) as :

| (10) | |||||

| (11) |

As shown in the next section, these equations account very well for empirical observations.

Let us note that this description (5) with (7) and (11) contains the standard Gaussian random walk model of stock market returns as the special case :

| (12) | |||||

| (13) |

Indeed, for , becomes a delta-function centered on , i.e. the volatility (6) at scale is , which recovers the standard square-root diffusion law. In this case, the pdf of asset “continuous” returns given by Eq.(5) is Gaussian.

2.2 Empirical tests

In order to test the previous formalism empirically, we need to define estimators for the parameters , , and . For this purpose, the so-called “structure functions” or -order moments of the “continuous” returns are very useful quantities (the brackets define the average with respect to a running window along the time series). For the purpose of analyzing data with multiple scales, the dependence of as a function of time scale for various ’s is very rich in information [Frisch, 1995]. For the hierarchical model (5) with the Gaussian ansatz given by Eq.(7), the th-order structure function of the centered variable (whose law is denoted using prime)

| (14) |

can be calculated analytically with the change of variable :

| (15) |

The second factor in the r.h.s. of Eq.(15) is the th-moment of the distribution at the integral scale. All the dependance on the time scale is found in the first factor that can be computed using Eqs (7),(10) and (11):

| (16) |

with

| (17) |

We thus get

| (18) |

The dependence of the th-order moments of “continuous” returns as a function of time scale is a pure power law, resulting from the logarithmic behavior as a function of time scale of both the mean and the variance of the Gaussian self-similarity kernel (Eqs. (10) and (11)). The exponent is related to the cumulant generating function of the kernel, as shown by Eq.(16). In general, the centered moments of odd-orders at the integral scale are vanishing due to the approximate symmetric structure of the pdf’s. In particular, the first-order moment, the centered “continuous” return, is zero by definition. From expression (18), the same property follows for . In order to measure the power law dependence given by the second term of the r.h.s. of Eq.(18), it is convenient to take the absolute value of the “continuous” return and calculate :

| (19) |

In order to determine the two parameters and , we measure the “multifractal spectrum” by performing a linear fit of as a function of , for a wide range of values . The slope of the linear fit gives the exponent . The slope at the origin of as a function of provides an estimation of the parameter . The fit of then provides a check for the importance of the quadratic correction proportional to . Recall that, for a Gaussian pdf of “continuous” returns, and the exponents are linear in . The quadratic dependence, often called “multifractal” in the literature [Frisch, 1995], is a signature of the multi-scale structure.

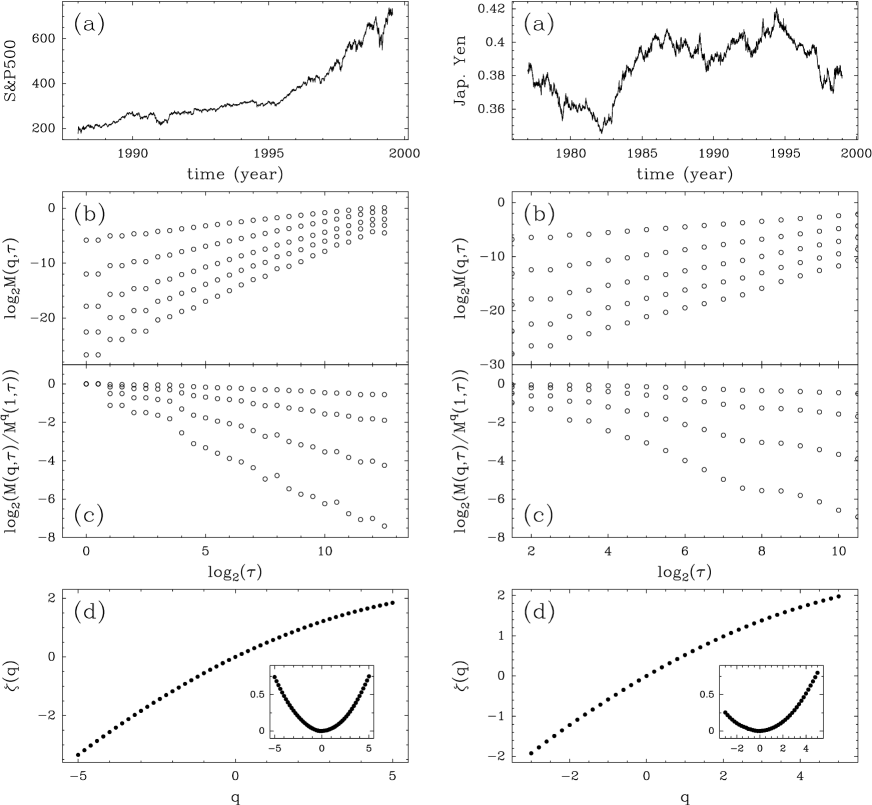

In Fig. 1, we report such an analysis for both the S&P500 index future and Japanese yen/US dollar exchange rate time series shown at the top in the two panels (a). The original intraday series have been sampled at a 10 mn rate and seasonal effects on the volatility have been removed. One can see in Figs 1(b) that the moments do exhibit the predicted scaling (Eq. (19)) over a large range of scales, of which three decades are here shown. The multifractal nature of these series is illustrated in Figs 1(c) which shows the ratio for and in log-log coordinates. For linear functions, the ratios should be constants as a function of time scales. A departure from a constant thus qualifies a multifractal behavior. The dependence of the exponent reported in Figs 1(d) is very well fitted by the parabolic shape given by Eq. (17). We find to a very good approximation for all assets which, according to Eq. (17), ensures that the volatility or variance as for the standard geometrical Brownian model, i.e. does not exhibit an anomalous scaling.

In order to test for the existence of a cascading process and to estimate the integral time , we refer to [Arneodo et al., 1998a] where it is shown that, for a cascade process, the covariance of the logarithms of the ’s at all scales should decrease as a logarithmic function. More precisely, if one defines the magnitude of asset at scale and time as , then one should have, for :

| (20) |

This behavior is checked for the S&P500 and JPY/USD series in Fig. 2 where we have plotted versus with mn. The linearity of these plots is reasonably well verified. The values of and can be obtained respectively from the slope and the intercept of these straight lines. In Table 1, we have reported the estimates of the parameters , , and for a set of high frequency future time series and the mean values of those parameters for daily time series of stocks composing the Dow Jones Industrial Average index and the french CAC40 index. Let us note that the errors on the estimates of can be very large since we get only one estimator of . For all series, we have checked that the relationship is reasonable so we have not reported the estimated values of . We can remark that the values of are relatively close to and the values of are in the range years. These values can thus be considered as representative of market multifractality.

| Series | (year) | (year-1) | (year-1) | |

|---|---|---|---|---|

| German Government Bond (F) | 0.028 | 1.2 | -1.6 | 1.7 |

| FT-SE 100 Index (F) | 0.017 | 1.1 | -3.3 | 7.6 |

| Japanese Yen (F) | 0.032 | 1.0 | -1.1 | 3.8 |

| S&P 500 (F) | 0.018 | 4.5 | 5.7 | 1.8 |

| Japanese Government Bond (F) | 0.121 | 1.3 | 9.2 | 4.0 |

| Nikkei 225 (F) | 0.030 | 1.5 | 5.5 | 3.9 |

| French CAC40 (mean) (S) | 0.020 | 1.9 | 1.2 | 5.6 |

| Dow-Jones (mean) (S) | 0.010 | 1.7 | 1.7 | 4.6 |

2.3 The multivariate multifractal model

Up to now, our emphasis has been on the correlation structure within each asset separately. We have not investigated the impact of correlations across assets and have quantified only the “diagonal” multifractal features as it is the case for uncorrelated assets. Since one of the natural applications of the characterization of distributions of returns is the quantification and selection of portfolios made of a basket of assets, it is important to generalize our framework to account for the possible existence of inter-asset correlations, in addition to the multi-scale time correlations. As it is well-known, optimizing a portfolio relies on two effects, the law of large numbers and the possibility to counter-act the negative effect of one asset by using (anti-) correlations. Towards a practical implementation of our model, it is thus essential to offer a generalization of the multifractal cascade model that accounts for the correlations across assets.

When dealing with Gaussian processes, the lack of independence is entirely embodied in the correlation function. Along this line of thought, we now propose a phenomenological model that extends the previous one to the case of correlated assets. We would like to generalize Eqs. (5), (7), (8) and (9) to multivariate distributions. In this purpose, let us write the line vector , where the subscript t stands for ‘transpose’, and we suppose that there exists a time scale for which the multivariate distribution is Gaussian with covariance matrix . The multivariate Gaussian mixture that generalizes Eq.(5) can be written as

| (21) |

where is the diagonal dilation matrix and is some multivariate probability distribution function. This description corresponds to a multivariate cascading process where the multiplicative weights associated with different assets can be correlated. This form (21) is the multivariate generalization of (5).

As in the previous section, let us make a Gaussian ansatz for the joint law of the logarithm of these weights, i.e.,

| (22) |

where the mean vector and the covariance matrix are supposed to behave as:

| (23) | |||||

| (24) |

with the “integral times” defined by

| (25) |

Within the cascade model, the times are the time scales at which some cascading process begins. If one considers two assets and , it seems natural to assume that only two situations occur:

-

i/

the cascade on and has the same “economic” origin, and then ;

-

ii/

the cascades on and are independent and thus , but, a priori, .

The returns can be thus organized by “classes” in such a way that the matrix is a block diagonal matrix:

| (26) |

where is the number of indenpendent subspaces (cascades) of dimension (). At fixed , one can always redefine such that Eqs. (23) and (24) become :

| (27) | |||||

| (28) |

To demonstrate that this multifractal multivariate model is compatible with the empirical observations, we first define an estimator of the elements of the covariance matrix . Let us denote the magnitude, i.e., the logarithm of the “continuous” return for asset at scale : . In the multivariate framework, the structure function at scale can be extended to order , where is a vector of values, in the following way:

| (29) |

where is the vector constructed from the ’s at scale . Using Eq. (21), the behavior of the structure function as a function of can be estimated:

where is the kernel quantifying the cascade from the integral scales to scale . Using our assumption that is normal with mean and covariance , the characteristic function of , defined as the last term in the previous expression, is

From the logarithmic behavior in Eqs (23) and (24), one deduces:

| (30) |

with

| (31) |

The constant depends on the values of the integral scales , , and on the multivariate distribution at the large integral scales. This power law (30) can be explicitely used to estimate the values of the elements of the covariance matrix defined by the kernel , by using different set of ’s.

If one sets for , and in the expression (30), one can show that the covariance between the magnitudes and simply behaves as:

| (32) |

where depends on , and .

Alternatively, one can test the multivariate cascade ansatz from the behavior of the lagged magnitude covariance: in full analogy with the monovariate case, it should behave as:

| (33) |

for . This equation provides other simple estimators of both and .

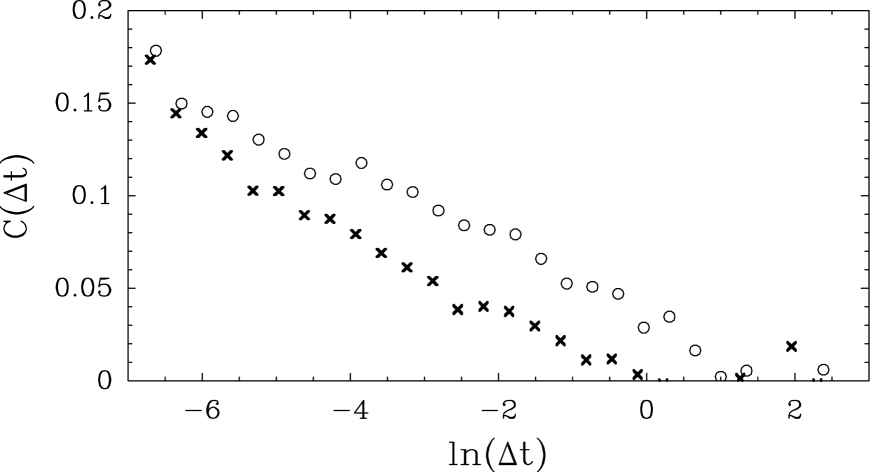

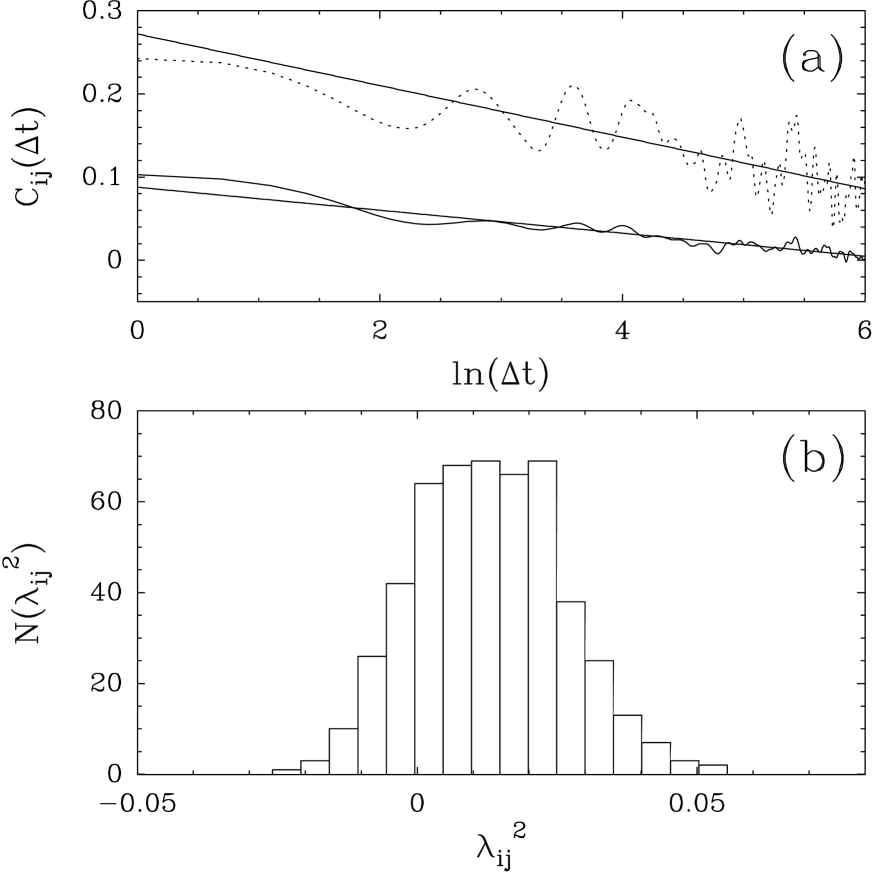

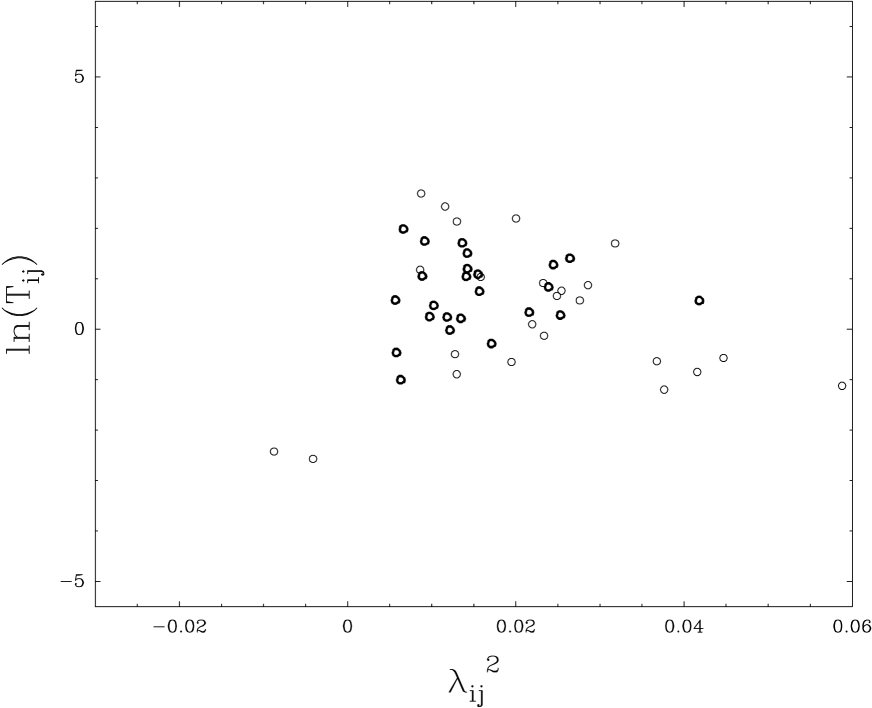

We were not able to use intraday data to test these predictions because the formalism requires that the different time series should be sampled at the same times. This can be alleviated in the future by a suitable pre-treatment that ensures the coincidence of the sampling times. Here, we present results for daily returns on the magnitude covariance functions for stocks taken from the French CAC40 index (over the period from 1992 to 1999). In Fig. 3(a), we report in dotted line the typical behavior of versus for two assets of the CAC40 index (CCF and MICHELIN). Despite the relatively poor statistical convergence, one clearly sees a slow decay which is compatible with the logarithmic law (33). From the slope and the intercept of this curve, one gets an estimate of and for these two assets. In solid line, we have plotted the average of performed over all the pairs of assets in the CAC40 index. The logarithmic decay of the magnitude covariance is thus a remarkably stable feature among all pairs of assets constituting the CAC40. In Fig. 4(b), we show the histogram of the values of estimated for 253 pairs of stocks belonging to the CAC40 index. Even though our estimates exhibit a large dispersion, one clearly sees that the distribution of is centered around . This value, which is very close to the estimates of determined in the previous section with the mono-asset analysis, can be considered as typical of financial stocks. This is confirmed in Fig. 4 which shows the estimates of versus the estimates of for pairs of stocks taken both from the CAC40 and the Dow-Jones indices. Moreover, one sees in Fig. 4 that the integral time scales are clustered around years.

3 Characterization of the distribution of portfolio returns

Consider a portfolio with shares of asset whose initial wealth is

| (34) |

A time later, the wealth has become and the wealth variation is

| (35) |

where

| (36) |

is the fraction in capital invested in the th asset at time . Using the definition (1), this justifies to write the return of the portfolio over a time interval as the weighted sum of the returns of the assets over the time interval

| (37) |

3.1 Cumulants of the variables

The portfolio is completely characterized by the distribution of its returns for all possible time scales . When the assets are assumed to be independent, expression (37) shows that the pdf of is obtained by the convolution of the pdf’s of the returns of the individual assets. A standard strategy is to calculate the characteristic functions of the pdf’s of the returns , from which one extracts the cumulants and use their additive properties to get the cumulants of the distribution of . In this section 3 and in section 4, we use the model of sections 2.1 and 2.2 of independent multifractal assets and turn in section 5 to the case of correlated multifractal assets described by the formalism of section 2.3. Let us thus estimate the cumulants of each asset return at scale .

In that purpose, let us compute the cumulants of the “continuous” returns ’s. The characteristic function of is obtained from Eq.(5) with Eq.(7) :

| (38) |

From this equation, we see that the moment of order of the centered variable can be easily computed

| (39) |

where is the n-th moment of the Gaussian law at the integral scale. The integrals in (38) and (39) are proportional to the Laplace transform of the normal distribution.

Using Eqs. (10) and (11), we obtain the following expressions for the moments of the centered variables :

| (40) | |||||

| (41) |

Expression Eq.(40) is the same as Eq.(18) with (17) for . We can then easily retrieve the moments of the (non-centered) variables by using the definition of and inverting it as . Thus,

| (42) |

for integer orders .

Note that the knowledge of the moments do not allow a unique reconstruction of the pdf. This is related to the fact that the characteristic function of the lognormal distribution cannot be expanded in a Taylor series based on the moments, because the moments grow too fast (as ) and lead to a diverging series. Holgate [1989] has shown how to make sense of such expansion by either using a finite Taylor series or resumming formally the divergent moment expansion. Using the entire function or moment constant method and Hardy’s formula, one obtains [Holgate, 1989]

| (43) |

where is the Laplace transform of the lognormal distribution, which is taken at exponentially increasingly spaced points. Its fast decay ensures the convergence of the series against the rapidly diverging moments and a unique characterization of the pdf.

The first six cumulants are linked to the moments as [Ord, 1994]:

| (44) | |||||

| (45) | |||||

| (46) | |||||

| (47) | |||||

| (48) | |||||

| (49) | |||||

Using Eqs (40), (41) and (42), we then determine the six first cumulants of . Notice that the cumulants of order larger than are invariant with respect to the translation and the centered moments (40), (41) can thus be used directly in expressions (45-49):

| (50) | |||||

| (51) | |||||

| (52) | |||||

| (53) | |||||

| (54) | |||||

| (55) |

Expression (50) retrieves the linear dependence of the mean value as a function of the time interval . This result is independent of the model. Expression (51) shows a more interesting structure: for we retrieve also a linear dependence of the variance as a function of time scale . This linear dependence occurs in absence of or for weak correlations of the returns. As this is a ubiquitous property confirmed by all empirical studies [Campbell et al., 1997; Mantegna and Stanley, 2000], this leads to the empirical constraint

| (56) |

which is remarkably well verified (see Fig. 1).

We note that, by construction of the superposition (5) of Gaussian pdf’s, all odd-order cumulants (except the first cumulant corresponding to the average “continuous” return) are zero. The present hierarchical model cannot account for possible skewness in the distribution of the “continuous” returns . But as shown in the next section, this does not implies that the skewness of return distribution is zero. A small value of the skewness is indeed observed in empirical studies of data sets [Campbell et al., 1997].

If one assumes that, for all assets , then the two sources of statistical non-normality for , i.e. non zero high order cumulants, are according to our model the intermittency parameter and the integral time : “quasi-Gaussian” statistics is recovered if the scale is very close to or if the intermittency parameter is small enough so that the fluctuations of the variances at different scales are small. Conversely, the distribution of “continuous” returns exhibits heavy tails if is large or if the time scale is small compared to integral scale .

3.2 Portfolio cumulants: perturbation expansion and multifractal corrections to the log-normal portfolio

In the standard portfolio theory [Markovitz, 1959; Merton, 1990], asset price time series are represented by geometric Brownian motions, i.e the statistics of “continuous” returns is exactly Gaussian while that of the “discrete” returns can be approximated by Gaussian distributions by means of an expansion where the small parameter is time measured in year. This results from the definition (1) showing that the difference between and is equal to to leading order. Since the typical magnitude of is given by the variance of and since the mean and the variance of are both of the order 0.1 (see stock examples in Table 1) when the time is measured in year, and are indistinguishable in practice for times of the order of or smaller than 1 year. An alternative way of saying the same thing is that the lognormal distribution of reduces to its approximate Gaussian representation for times less than or of the order of a year. Thus, the smaller the time scale , the more precise is the normal approximation for assuming a perfect Gaussian statistics for and the smaller are high-order cumulants of , since they quantify the departure from normality. This is the classical point of view for the existence of non-normal returns as studied in the financial literature. This is equivalent in our model to setting the parameters and .

Non-trivial multifractal corrections arise when is not negligible and thus departs from . For the statistical properties of (both “discrete” and “continuous”) returns, these multifractal corrections to the log-normal picture are stronger at fine scales: the finer the scale, the larger the values of high order cumulants. With respect to time scales, this phenomenon thus acts in the way opposite to the previous effect of the difference between “discrete” returns and “continuous” returns . Due to multifractality, we do not expect to observe normality for returns at small time scales, in contradiction with the standard geometrical Brownian model.

To sum up, due to the difference between “discrete” returns and “continuous” returns , normality is expected at small scales while deviations from normality is predicted at large time scales. Due to multifractality, non-normality is expected at small scale and Gaussian statistics are predicted at large time scales, beyond the “integral” scale. Putting the two effects together, non-normality must be the rule at all time scales, with a cross-over from small to large time scales, from non-normality induced by multifractility to non-normality induced by the difference between continuous and discrete returns. Thus, we expect high order return cumulants to be non zero both at large scales because of the log-normality and also at small scales because of multifractality of .

Let us now quantify these effects. In this purpose, we compute the cumulants of the portfolio returns using an expansion where the small parameter is (measured in year), which takes multifractal corrections into account. From Eq.(37), the cumulants of the portfolio can be expressed in terms of the cumulants of the returns for each individual asset as weighted sums over them:

| (57) | |||||

| (58) |

Using Eqs. (50-56) and from the definition , after some algebra we find, to the leading orders in the time expansion,

| (59) | |||||

| (60) | |||||

| (61) | |||||

| (62) | |||||

| (63) | |||||

| (64) |

where we have set (in year-1). We can see how the multifractal corrections arise in the high order cumulants. Using the typical values and , one can compute, according to the value of , which term from the log-normal expansion or from the multifractal correction dominates the cumulant. For the first two cumulants and , it can be shown that multifracal corrections are always negligible. For the third-order cumulant , for time scales larger than a few seconds, the multifractal nature of is not important. However, for cumulants of order larger than or equal to 4, the multifractal corrections are very important for time scales as large as several months: for instance, using the previous values for the parameters, we find that the multifractal term is dominating for all times smaller than 6 months.

From the structure of the cumulants given by Eqs (51,53,55) and their generalization to higher order, it is easy to show by recurrence that the multifractal correction to the -th order cumulant behaves, for , as

| (65) |

to leading order. As a consequence, the corrections to the Gaussian description brought by the multifractal model are all the more important than the order of the cumulant is higher, i.e. than one looks further in the tail of the return distribution. We retrieve a common observation that the deviations from the Gaussian model are all the more important for large risks quantified by the behavior of the tails of the portfolio return distribution [Sornette, 1998; Sornette et al., 2000].

If we neglect the higher order cumulants in the previous expansion, we retrieve that the portfolio return and variance are both proportional to time scale . Hence, the portfolio optimization of the asset weights are independent of the investment horizon in the absence of the riskless asset. This is the well-known result underlying Gaussian portfolio optimization [Markovitz, 1959; Merton, 1990]. In contrast, in the hierarchical model, cumulants of order 4 and higher have a different dependence on the investment time horizon . This implies that large risks exhibit a non-trivial time dependence: it will therefore not be possible to optimize the asset weights for all time scales simultaneously. This is the novel ingredient captured by our hierarchical model: a portfolio optimization which is concerned with large risks has to optimize its investment time horizon in a manner that we are now going to investigate.

3.3 Excess kurtosis

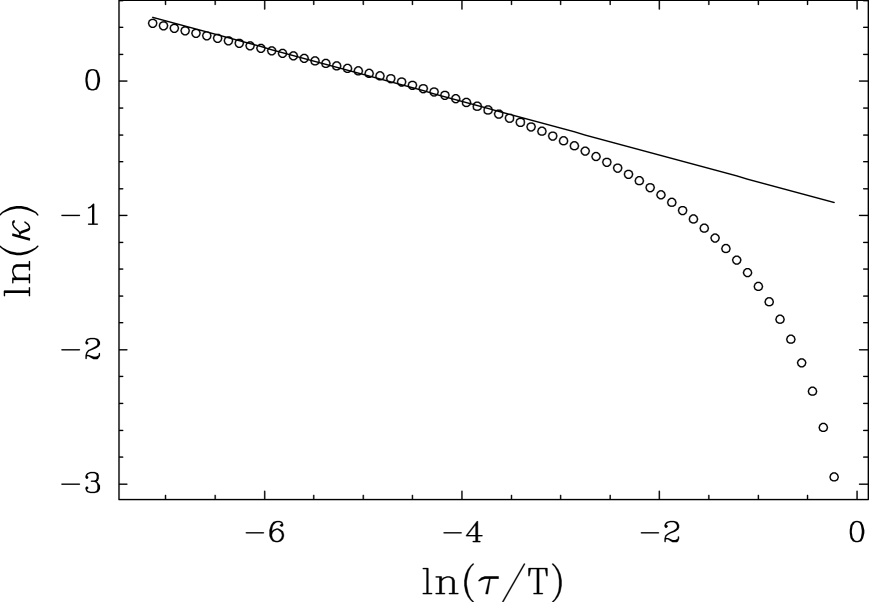

The absence of volatility correlations and the validity of the log-normal model would imply, as already said, that the variance of the volatilities vanishes. As seen from expressions (62-64), all cumulants of order larger than would then be of order , i.e. very small at small time scales, as expected for a Gaussian distribution of returns. Actually, for instance for the US S&P500 index, there is a residual hierarchical correlation structure, quantified by and and year. With these values, we predict an excess kurtosis by using Eq. (60) and (62) for a single asset (the S&P500 index)

| (66) |

This expression makes clear that the size of the variance of the volatilities at different scales quantifies the distance from the log-normal paradigm. The excess kurtosis at small time scale is negligible for . In contrast, in the presence of multifractality (), the excess kurtosis is predicted to be very large at small time scales. The dependence of the excess kurtosis is shown in Fig. 5. This figure shows that the excess kurtosis given by Eq. (66) can be represented approximately as a power law decay over more than three decade with a small exponent , in excellent agreement with previous determinations [Dacorogna et al., 1993; Ding et al., 1993; Bouchaud et al., 2000]. To confirm the relevance of Eq. (66), one thus needs to investigate the excess kurtosis for time scales large enough as compared to the integral scale . It is important to contrast this decay of the excess kurtosis as a function of the time scale with what one would expect from a model without correlations across scales: in that case, all cumulants are linear in and . The anomalous law (66) is a clear signature of long-range correlations in the volatilities.

4 Portfolio optimization with time-scale dependent risks

4.1 The expected utility approach

Starting the period with initial capital , the investor is assumed to have preferences that are rational in the von-Neumann-Morgenstern [1944] sense with respect to the end-of-period distribution of wealth . His preferences are therefore representable by a utility function determined by the wealth variation at the end-of-period . The expected utility theorem states that the investor’s problem is to maximize , where denotes the expectation operator :

| (67) |

The utility function has a positive first derivative (wealth is prefered) and a negative second derivative (risk aversion). Use of the utility maximization in portfolio optimization can be found in [Levy and Markowitz, 1979; Kroll et al., 1984].

Here, we consider a simple case of a constant absolute measure of risk aversion (where the primes denote the derivatives), for which . With a very good approximation for large initial wealths, we can take . This gives

| (68) |

which is nothing but the Fourier transform of the probability distribution function (with imaginary argument ):

| (69) |

By definition of the cumulants, this reads

| (70) |

Maximizing the expected utility thus amounts to minimizing the argument of the second exponential in the r.h.s. of (70) with respect to the weights .

Keeping in mind that the time is the small parameter of the problem, we express the optimal asset weights as equal to the optimal Markowitz results denoted (obtained by droping all multifractal corrections) plus the multifractal corrections. Keeping only the cumulants of order up to 4 (this approximation is valid not only in the small time limit but for a risk aversion not too large). The problem is thus to minimize

| (71) | |||||

with respect to the asset weights ’s. The term is a Lagrange multiplier ensuring the normalization . This optimization amounts to finding the roots of a third order polynomial and one can thus obtain closed expressions for the weights .

In order to quantify the influence of multifractal corrections and to handle simple expressions, let us neglect the corrections due to the difference between “continuous” and “discrete” returns which are unimportant at small time scales up to 6 months. In this approximation, the problem is to minimize

| (72) |

Then, in absence of the last terms proportional to , i.e. for all ’s equal to zero, we get the “Markowitz” solution

| (73) |

where is determined from the normalization condition. In the simple case where is the same for all assets, this gives

| (74) |

where is the mean return averaged over all assets: assets with better than average returns have thus more weight in the portfolio, with a leverage controlled by the risk .

Using this solution (73), we get the general solution of the weights up to second order in powers of

| (75) |

where

| (76) |

The expression of the weigths valid to first-order in the multifractal corrections for as a function of time horizon is then

| (77) |

Returning to the general solution (75), we see that assets with integral time scales (where is the base of the natural logarithm) will be the most depleted compared to the Gaussian solution, as the factor is negative with a maximum amplitude for . Both for small and for approaching , the solution is close to the Gaussian solution as it should : small do not lead to large absolute risks; leads to the Gaussian regime for . The worst case occurs for intermediate values of the time horizon compared to the integral time scale. Such stocks will be unfavored in the portfolio selection.

This result is actually more general than this section would lead us to believe. This can be seen from the structure of the cumulants of order given by Eq. (65): the dependence in given by shows that, for large , the cumulants are the largest when is the largest. This is exactly the same term that controls the corrections to the Gaussian case quantified by the parameters .

4.2 Efficient frontiers for multi-period portfolio optimization

As recalled in the introduction, the multiperiod portfolio problem as been addressed by several studies. This problem is a natural application of our multi-scale description of returns. The problem we investigate is to minimize a risk measure represented by a cumulant of order for a fixed mean return. For instance, one can choose to minimize the value of the cumulant at fixed mean return (this amounts to find the set of ’s that minimize the pseudo-utility function ), thus defining the efficient frontier [Andersen and Sornette, 2000]. The previous cumulant perturbative expansion at different time scales allows us to estimate the shape of the generalized optimal frontiers for all periods, given a fixed horizon .

For the sake of simplicity, we will suppose that all the assets are characterized by the same integral time values year, which is a reasonable value as revealed by the empirical analysis of section 2. Denoting the investment horizon and the number of periods, we will consider the portfolio returns at scale . Moreover, we will explicitely make the so-called “rebalancing assumption”: periodic rebalancing supposes that, at the end of each period, portfolio composition is adjusted in order to restore the original weights. We will assume that doing so the returns associated to each period are statistically independent.

Once again, in order to quantify the influence of multifractal corrections and to handle simple expressions, we will neglect here the corrections due to the difference between “continuous” and “discrete” returns which are unimportant at small time scales up to 6 months (above which they are dominated by the log-normal corrections). One can easily show using and the “rebalancing assumption” that the cumulants of the portfolio returns for a given multiperiod strategy have exactly the same expression as in Eqs. (59)-(64) where and become respectively and and the multifractal corrections become . Using this rule, it is easy to show that, if one estimates the risk using the variance of portfolio returns, the results are independent of the number of periods at fixed horizon . Fig. 6 represents the standard efficient frontier as a function of for various ’s. As expected, it is clearly apparent that the efficient frontiers are independent of time , i.e. of the number of periods. This is nothing but Tobin’s result [1965] that the single-period minimum variance set and the multi-period minimum variance set are identical.

In contrast, the generalized efficient frontiers with a risk measure represented by higher order cumulants will involve multifractal corrections and both portfolio composition and efficient frontiers will depend on the number of periods. Let us illustrate this results for the minimization problem. In that case, the optimum weight of asset can be written for as:

| (78) |

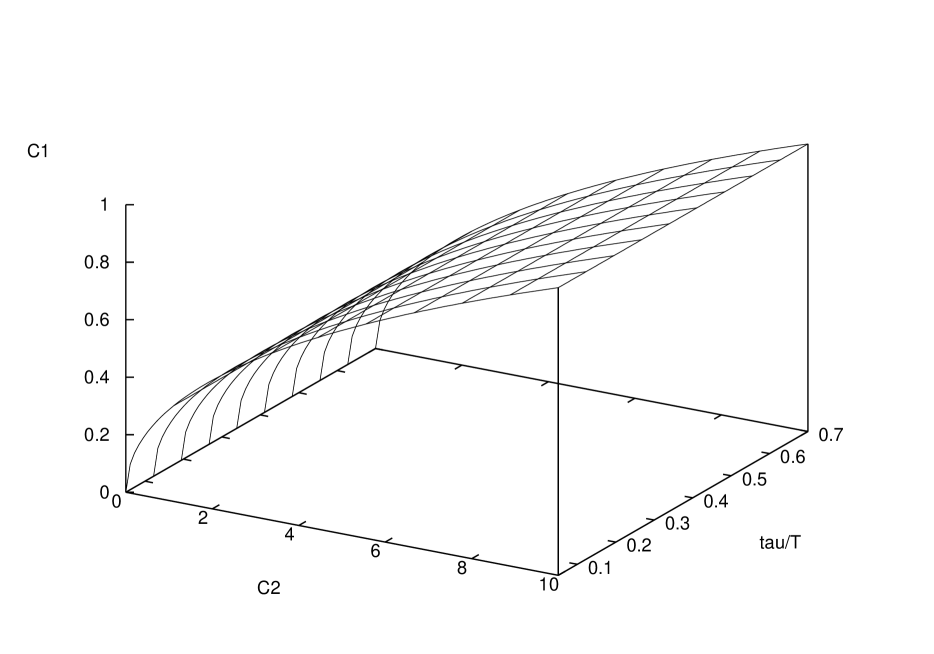

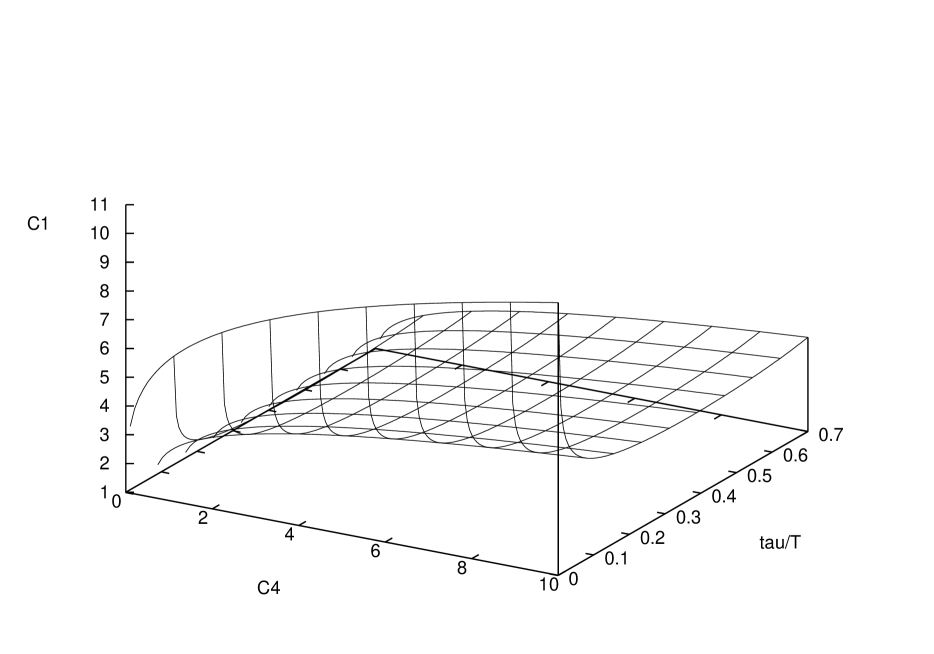

where is the Lagrange parameter associated with the fixed mean return. For a large number of periods (i.e. small time scale ), assets with small multifractal parameter are prefered. Using these weights, Fig. 7 shows the efficient frontiers as a function of for various periods. We have considered the simplest case of a single risky asset with parameters for the mean return, for the standard deviation and for the multifractal parameter. Denoting the return of the riskless asset, the parametric equation for the efficient frontier for an horizon and a number of periods is:

| (79) | |||||

| (80) |

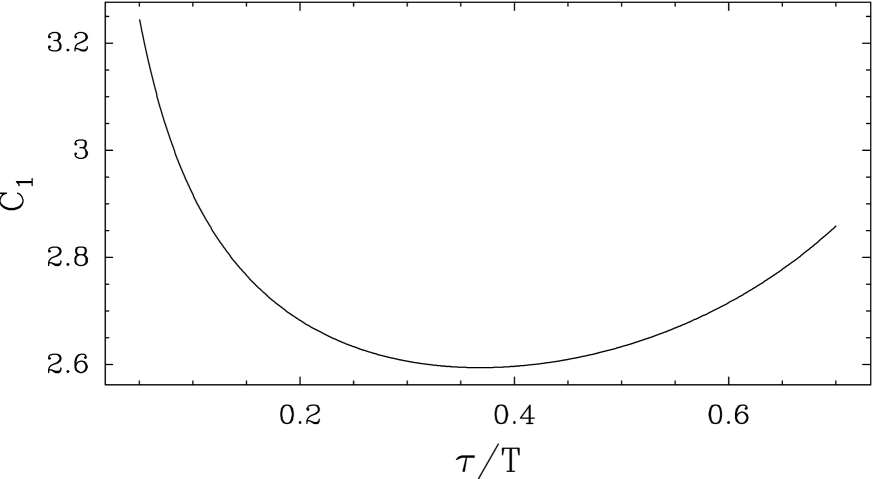

Fig. 7 exhibits a measurable dependence on the time scale , in contrast with the standard mean-variance efficient frontier as a function of . For a fixed risk , the return is seen to be increasing at both ends as a function of time scale , i.e., for and for . There is thus a worst choice for the time-horizon and for the rebalancing of the portfolio, approximately given by one fifth of the integral time scale . For this time scale, the return is minimum for a given (large) risk and the risk is maximum for a given return. One the other hand one can see that the shorter the rebalancing period, the lower is the risk for a given return. As a matter of facts, the risk is here quantified by the fourth cumulant which goes to zero as (Gaussian statistics). The limiting factor for small ’s is then transaction cost. Fig. 8 makes more precise this effect by plotting as a function of for a given value of the accepted risk.

5 Distribution of returns of a portfolio of correlated assets within the multifractal multivariate cascade framework

In order to discuss portfolio optimization in presence of correlated assets, let us make the approximation (valid for small enough) that . Moreover, for the sake of simplicity, let us assume that the ’s are centered, i.e., . Using the notations of section 2.3, the characteristic function of the portfolio can be written as

| (81) |

where we have denoted the vector of the weights . Let us consider the orthogonal matrices and that diagonalize respectively the matrices (and thus also the matrix by virtue of Eq. (28), showing that is independent of ) and :

| (82) | |||||

| (83) |

where and are the diagonal matrices formed of the eigenvalues of and . Let us set . If we denote the vector , the previous equation can be rewritten as:

| (84) |

where are the eigenvalues of and is the standard monovariate Gaussian law. After calculating the second integral, we obtain the following expression for the characteristic function:

| (85) |

From this equation, one can immediately see that, if all the cascades are uncorrelated, i.e, is diagonal, the characteristic function is the same as in the case of independent assets where the weights have been replaced by the weights . This is the same situation as in classical (Gaussian) portfolio theory where the case of correlated assets is reduced to the uncorrelated one by such a simple change of variable on the weights.

When the covariance matrix is non trivial, the situation is more complicated. Let us consider the case where each matrix in the block decomposition (26) is singular, i.e, . This case corresponds to the existence of degrees of freedom in the problem for which one can compute the characteristic function under the form:

| (86) | |||||

This case corresponds to independent assets whose integral scale variances are .

6 Conclusion

We have extended a statistical model of price returns and volatility correlations based on the idea of information cascades from large time scales to smaller time scales. Empirical tests performed on intra-day as well as daily data on the CAC40 and S&P500 indices, on their constituting stocks as well as on bonds and currencies validate satisfactorily the model. The calibration give a robust and seemingly consistent value for the two key parameters: the integral time-scale is found in the range of one to two years and the variance of the multiplicative kernel is approximately for all stocks and indices that have been investigated. Our results show that the evidence for multifractality is fully consistent with a simple cascade origin, flowing from large time-scales to shorter time-scales. The multifractal cascade model offers an intuitive explanation for the observation that the detection of “abnormal” states or crises in the stock market requires an index constructed over many different horizon times [Zumbach et al., 2000].

We have also offered an extension of the cascade model into a multi-variate framework to account for correlations between assets, in addition to the correlations in time-scales. Future works will exploit this novel formalism, in particular for multi-period portfolio characterization and optimization.

In a second part, we have shown how to characterize the distribution of returns of a portfolio constituted of assets with returns distributed according to such multifractal cascade distributions. In particular, explicit analytical expressions for the first six cumulants are offered. We also show that, within a utility approach with a constant absolute measure of risk aversion (exponential utility function), the problem of portfolio optimization amounts to maximize a sum over cumulants weighted by powers of the risk aversion coefficient. Working in the space of (return, fourth-order cumulant) or of (return, sixth-order cumulant) generalizes the mean-variance approach and underlines the impact of the investor horizon-time. The most important consequence of the theory is that the optimal portfolio depends on the time-scale. In addition, it is not possible to simultaneously optimise all the components of risks with respect to the choice of the investment time scale. This result extends to the investment horizon dimension previous results obtained from a decomposition of the risk into a spectrum from small to large risks quantified by the cumulants of the distribution of portfolio returns [Sornette et al., 2000].

In principle, our portfolio theory allows one to quantify how much diversification can be obtained by buying different assets and managing them optimally with respect to their possibly different integral time scales: indeed, our results suggest that reallocation of assets in the portfolio should be performed with different time-horizon depending upon the assets. This is related to the “time-diversification” concept introduced by Martellini [2000] for option hedging in the presence of transaction costs. A quantification and tests of these strategies will be reported elsewhere.

REFERENCES :

J.V. Andersen and D. Sornette, Have your cake and eat it too: increasing returns while lowering large risks! preprint at http://xxx.lanl.gov/abs/cond-mat/9907217.

F.D. Arditti and H. Levy, Portfolio efficiency analysis in three moments - the multiperiod case, Journal of Finance 30, 797-809 (1975).

A. Arneodo, J.F. Muzy and D. Sornette, “Direct” causal cascade in the stock market, Eur. Phys. J. B 2, 277-282 (1998a).

A. Arneodo, E. Bacry, S. Manneville and J.F. Muzy, Analysis of random cascades using space-scale correlation functions, Phys. Rev. Lett. 80, 708-711 (1998b).

A. Arneodo, S. Manneville and J.F. Muzy, Towards log-normal statistics in high Reynolds number turbulence, Eur. Phys. J. B 1, 129-140 (1998c).

A. Arneodo, S. Manneville, J.F. Muzy and S.G. Roux, Revealing a lognormal cascading process in turbulent velocity statistics with wavelet analysis, Phil. Trans. Royal Soc. London Series A 357, 2415-2438 (1999).

G. Ballocchi, M. M. Dacorogna and R. Gencay, Intraday statistical properties of Eurofutures by Barbara Piccinato, Derivatives Quarterly 6 (2), 28-44 (1999).

A. Bershadskii, Multifractal critical phenomena in traffic and economic processes, Eur. Phys. J. B 11, 361-364 (1999).

H. Bierman, Jr., Portfolio allocation and the investment horizon, Journal of Portfolio Management 23, 51-55 (1997).

H. Bierman, Jr., A utility approach to the portfolio allocation decision and the investment horizon, Journal of Portfolio Management 25, 81-87 (1998).

J.-P. Bouchaud, M. Potters and M. Meyer, Apparent multifractality in financial time series, Eur. Phys. J. B 13, 595-599 (2000).

M.-E. Brachet, E. Taflin and J. M. Tcheou, Scaling transformation and probability distributions for financial time series, preprint cond-mat/9905169 (1999).

W. Breymann, S. Ghashghaie and P. Talkner, A stochastic cascade model for FX dynamics, preprint cond-mat/0004179 (2000).

J.Y. Campbell, A.W. Lo and A.C. MacKinlay, The econometrics of financial markets (Princeton University Press, Princeton, New Jersey, 1997).

B. Castaing, Y. Gagne and E.J. Hopfinger, Velocity probability density functions of high Reynolds number turbulence, Physica D 46, 177-200 (1990).

B. Chabaud, A. Naert, J. Peinke, F. Chilla and B. Castaing, Transition towards developed turbulence, Phys. Rev. Lett. 73, 3227-3230 (1994).

M.M. Dacorogna, U.A. Müller, R.J. Nagler, R.B. Olsen et al., A geographical model for the daily and weekly seasonal volatility in the foreign exchange market, Journal of International Money & Finance 12, 413-438 (1993).

M.M. Dacorogna, U.A. Müller, R.B. Olsen and O.V. Pictet, Modelling short-term volatility with GARCH and HARCH models, in “Nonlinear Modelling of High Frequency Financial Time Series,” by C. Dunis and B. Zhou (John Wiley & Sons, 1998).

Z. Ding, C.W.J. Granger and R.F. Engle, A long memory property of stock market returns and a new model, J. Empirical Finance 1 (1), 83-106 (1993).

R. Ferguson and Y. Simaan, Portfolio composition and the investment horizon revisited, Journal of Portfolio Management 22, 62-67 (1996).

A. Fisher, L. Calvet and B.B. Mandelbrot, Multifractality of the deutschmark/us dollar exchange rate, Cowles Foundation Discussion Paper, 1997.

U. Frisch, “Turbulence: the legacy of A.N. Kolmogorov” (Cambridge, New York: Cambridge University Press, 1995).

S. Ghashghaie, W. Breymann, J. Peinke, P. Talkner and Y. Dodge, Turbulent cascades in foreign exchange markets, Nature 381, 767-770 (1996).

N. Gressis, G.C. Philippatos et al., Multiperiod portfolio analysis and the inefficiency of the market portfolio, Journal of Finance 31, 1115-1126 (1976).

D. Gunthorpe and H. Levy, Portfolio composition and the investment horizon, Financial Analysts Journal 50, 51-56 (1994).

P. Holgate, The lognormal characteristic function, Commun. Statist.-Theory Meth. 18, 4539-4548 (1989).

K. Ivanova and M. Ausloos, Low q-moment multifractal analysis of Gold price, Dow Jones Industrial Average and BGL-USD exchange rate, Eur. Phys. J. B 8, 665-669 (1999); erratum Eur. Phys. J. B 12 613 (1999).

Y. Kroll, H. Levy and H.M. Markowitz, Mean-Variance versus direct utility maximization, The Journal of Finance, vol. XXXIX, N 1, 47-61 (1984).

H. Levy and H.M. Markowitz, Approximating expected utility by a function of mean and variance, American Economic Review 69, 308-317 (1979).

B.B. Mandelbrot, Fractals and scaling in finance : discontinuity, concentration, risk, Selecta volume E (with foreword by R.E. Gomory, and contributions by P.H. Cootner et al.), New York : Springer, 1997.

B.B. Mandelbrot, A multifractal walk down Wall Street, Scientific American 280 N2:70-73 (1999 FEB).

R.N. Mantegna and H.E. Stanley, An introduction to econophysics: correlations and complexity in finance (Cambridge, U.K.; New York: Cambridge University Press, 2000).

H. Markovitz, Portfolio selection : Efficient diversification of investments (John Wiley and Sons, New York, 1959).

J.F. Marshall, The role of the investment horizon in optimal portfolio sequencing (an intuitive demonstration in discrete time), Financial Review 29, 557-576 (1994).

L. Martellini, Efficient option replication in the presence of transaction costs, in press in Review of Derivatives Research (2000).

R. C. Merton, Continuous-time finance (Blackwell, Cambridge,1990).

U.A. Müller, M.M. Dacorogna, R. Dav , R.B. Olsen, O.V. Pictet and J.E. von Weizs cker, Volatilities of different time resolutions - Analyzing the dynamics of market components, Journal of Empirical Finance 4, No. 2-3, 213-240 (1997).

J.-F. Muzy, J. Delour and E. Bacry, Modelling fluctuations of financial time series: from cascade process to stochastic volatility model, submitted to Eur. Phys. J. B, preprint cond-mat/0005400 (2000).

J.K. Ord, Kendall’s advanced theory of statistics. 6th ed., Edward Arnold, London and Halsted Press, New York (1994).

M. Pasquini and M. Serva, Clustering of volatility as a multiscale phenomenon, Eur. Phys. J. B 16, 195-201 (2000).

F. Schmitt, D. Schertzer and S. Lovejoy, Multifractal analysis of foreign exchange data, preprint. Mc Gill University, Montreal (1999).

D. Sornette, Large deviations and portfolio optimization, Physica A 256, 251-283 (1998).

D. Sornette, Critical Phenomena in Natural Sciences (Chaos, Fractals, Self-organization and Disorder: Concepts and Tools) 432 pp., 87 figs., 4 tabs (Springer Series in Synergetics) Date of publication: August 2000.

D. Sornette, P. Simonetti and J.V. Andersen, -field theory for Portfolio optimization: “fat tails” and non-linear correlations, Physics Report 335 (2), 19-92 (2000).

G.V.G. Stevens, On Tobins multiperiod portfolio theorem. Review of Economic Studies V39, 461-468 (1972).

G.Y.N. Tang, Effect of investment horizon on international portfolio diversification, International Journal of Management 12, 240-246 (1995).

J. Tobin, The theory of portfolio selection, in “The Theory of Interest Rates”, F. Hahn and F. Breechling (eds), London: Macmillan (1965).

N. Vandewalle and M. Ausloos, Multi-affine analysis of typical currency exchange rates, Eur. Phys. J. B 4, 257-261 (1998).

J. von-Neumann and O. Morgenstern, Theory of games and economic behavior (Princeton, Princeton University Press, 1944).

G. Zumbach, M. Dacorogna, J. Olsen and R. Olsen, Shock of the new, RISK, pp. 110-114 (March 2000).