Scalable Principal–Agent Contract Design via Gradient-Based Optimization

Abstract

We study a bilevel max–max optimization framework for principal–agent contract design, in which a principal chooses incentives to maximize utility while anticipating the agent’s best response. This problem, central to moral hazard and contract theory, underlies applications ranging from market design to delegated portfolio management, hedge fund fee structures, and executive compensation. While linear–quadratic models such as Holmström–Milgrom admit closed-form solutions, realistic environments with nonlinear utilities, stochastic dynamics, or high-dimensional actions generally do not.

We introduce a generic algorithmic framework that removes this reliance on closed forms. Our method adapts modern machine learning techniques for bilevel optimization—using implicit differentiation with conjugate gradients (CG)—to compute hypergradients efficiently through Hessian–vector products, without ever forming or inverting Hessians. In benchmark CARA–Normal (Constant Absolute Risk Aversion with Gaussian distribution of uncertainty) environments, the approach recovers known analytical optima and converges reliably from random initialization. More broadly, because it is matrix-free, variance-reduced, and problem-agnostic, the framework extends naturally to complex nonlinear contracts where closed-form solutions are unavailable, such as sigmoidal wage schedules (logistic pay), relative-performance/tournament compensation with common shocks, multi-task contracts with vector actions and heterogeneous noise, and CARA–Poisson count models with . This provides a new computational tool for contract design, enabling systematic study of models that have remained analytically intractable.

1 Introduction

The design of incentive mechanisms is a central problem in economics, finance, and operations research (Bolton and Dewatripont, , 2005; Lazear and Gibbs, , 2014; Milgrom and Roberts, , 1992; Jensen and Meckling, , 1976; Cachon, , 2003; Laffont and Martimort, , 2002). In many settings, a principal (e.g., an employer, regulator, firm, or portfolio manager) seeks to influence the actions of an agent (e.g., an employee, contractor, or service provider) whose choices directly affect the principal’s payoff (Grossman and Hart, , 1983). A key challenge is that the principal cannot directly dictate the agent’s decision; instead, they must offer a contract specifying how the agent will be compensated based on observable outcomes (Salanié, , 2017; Holmström, , 1979; Holmström and Milgrom, , 1987). The agent, upon observing the contract, chooses an action that maximizes their own utility, which may diverge from that of the principal.

This interaction leads naturally to a bilevel optimization problem in which both levels are maximization problems: the principal optimizes contract parameters in the outer problem, anticipating the agent’s best-response in the inner problem (Colson et al., , 2007). Such models appear throughout the literature on moral hazard (Holmström, , 1979; Grossman and Hart, , 1983; Holmström and Milgrom, , 1987), mechanism design (Myerson, , 1981), and industrial organization.

A canonical example is the linear–quadratic principal–agent model of Holmström and Milgrom (Holmström and Milgrom, , 1987), in which the principal offers a linear contract , consisting of a fixed payment and a performance-based incentive . The agent chooses an effort level that is costly to exert, and output is noisy. Under quadratic cost of effort and mean–variance preferences, this model admits a closed-form solution for (Holmström and Milgrom, , 1987). While this structure is analytically tractable, real-world contracts often involve nonlinear utilities, richer stochastic dynamics, and high-dimensional actions for which closed-form solutions do not exist (Sannikov, , 2008).

When and are differentiable, a natural computational strategy is to use gradient-based optimization (Domke, , 2012). However, in bilevel settings the outer objective depends on the contract parameters both directly and indirectly through the agent’s optimal response . Differentiating through the inner maximization requires computing hypergradients that involve inverting the Hessian of with respect to the agent’s action, a computational bottleneck in high dimensions (Gould et al., , 2016).

1.1 Related Work

Principal–agent theory and contract design. Classic insight into incentive contracts arises from hidden–action models of moral hazard (Holmström, , 1979; Grossman and Hart, , 1983; Holmström and Milgrom, , 1987) and the broader mechanism–design tradition (Myerson, , 1981). These foundations have been synthesized in comprehensive works spanning labor economics, industrial organization, management, and finance (Bolton and Dewatripont, , 2005; Laffont and Martimort, , 2002; Salanié, , 2017; Lazear and Gibbs, , 2014; Milgrom and Roberts, , 1992; Bard, , 2008; Ho et al., , 2014). In the canonical CARA–Normal, linear–contract framework, the Holmström–Milgrom model offers closed-form solutions under analytical tractability (Holmström and Milgrom, , 1987). Extensions have preserved tractability while adding features such as multitask incentives (Holmström and Milgrom, , 1991), imperfect or multiple performance measures (Baker, , 1992; Laffont and Martimort, , 2002), and insurance with prevention trade-offs (Ehrlich and Becker, , 1972; Shavell, , 1979). While these classical models frequently admit closed-form solutions, they do so under restrictive assumptions—quadratic costs, Gaussian uncertainty, and linear contracts—that constrain their applicability in nonlinear or high-dimensional settings.

Algorithmic contract theory. Since closed-form solutions are often infeasible, the emerging field of algorithmic contract theory (Duetting et al., , 2024; Dütting and Talgam-Cohen, , 2019) develops computational tools for a broader range of principal–agent settings. Much of this literature focuses on discrete action spaces. One strand analyzes the performance of linear contracts, establishing approximation and robustness guarantees relative to the optimal benchmark (Dütting et al., , 2019). Another examines combinatorial and multi-agent contracts, where the exponential size of the action space motivates approximation algorithms, query-complexity analyses, and hardness results (Dütting et al., , 2021; Ezra et al., , 2024; Cacciamani et al., , 2024). Typed-agent models motivate menu-based contracts, yielding welfare and approximation guarantees under single-dimensional and thin-tail assumptions (Alon et al., , 2021, 2023).

Beyond these discrete formulations, more recent work leverages learning and continuous optimization. Data-driven approaches provide regret bounds and statistical guarantees, while neural methods approximate the principal’s utility and optimize over contract spaces. For example, Wang et al., (2023) learn piecewise-affine surrogates of payoffs and use gradient-based inference to recover contracts, while the differentiable economics framework (Dütting et al., , 2022) parameterizes mechanisms with neural networks and trains them end-to-end via stochastic gradient descent. Other directions explore contracts for strategic effort in machine learning (Babichenko et al., , 2024), ambiguous or incomplete contracts (Duetting et al., , 2023). Collectively, these results chart a broad algorithmic landscape that complements classical theory by emphasizing approximation, learnability, and computational tractability.

Bilevel optimization and differentiable methods. Abstractly, principal–agent models can be cast as bilevel max–max programs where the principal’s optimization anticipates the agent’s best response. Bilevel optimization has a long tradition in operations research (Colson et al., , 2007) and has become central in machine learning—powering hyperparameter tuning, meta-learning, data reweighting, and differentiable programming (Lorraine et al., , 2020; Rajeswaran et al., , 2019; Ren et al., , 2018). Early methods differentiated through the inner solver by unrolling optimization steps (Domke, , 2012), which is memory-intensive and prone to truncation bias. More scalable approaches apply implicit differentiation to the inner optimality conditions, reducing the task to solving linear systems involving Hessians or Jacobians (Gould et al., , 2016; Lorraine et al., , 2020). Modern techniques combine automatic differentiation for Hessian–vector products with Krylov solvers like conjugate gradient (CG) (Hestenes and Stiefel, , 1952; Barrett et al., , 1994), enabling scalable, matrix-free hypergradient computation (Maclaurin et al., , 2015; Rajeswaran et al., , 2019).

1.2 Contributions

In contrast to approaches that learn neural surrogates of the principal’s utility and then optimize them via gradient-based inference (Wang et al., , 2023), or that parameterize mechanisms with neural networks and train them end-to-end using stochastic gradient descent (Dütting et al., , 2022), our method directly addresses the bilevel max–max structure of hidden-action problems. Whereas surrogate-based methods approximate the objective and depend on network training to suggest good contracts, our framework computes exact hypergradients through the agent’s best-response conditions using implicit differentiation. This distinction is crucial: it enables a general-purpose solver for principal–agent problems that (i) recovers classical closed-form solutions with minimal approximation error, and (ii) scales to nonlinear and high-dimensional settings without discretization.

2 Problem Setup

|

|

|

|

|

|

|

|

|

|

|

|

We study the problem of contract design in a principal–agent relationship (Grossman and Hart, , 1983; Holmström, , 1979). In this framework, a principal (e.g., an employer, firm, or regulator) seeks to design an incentive scheme that shapes the behavior of an agent (e.g., an employee, contractor, or service provider).

The interaction has four defining features: (a) the principal cannot directly dictate the agent’s action (e.g., effort); (b) instead, the principal offers a contract that specifies a fixed payment together with performance-based incentives; (c) the agent, after observing , selects to maximize their own utility , which includes both rewards and penalties (e.g., costs of effort); and (d) the principal’s utility depends on and on the induced action .

Formally, denotes the contract parameters and the agent’s action. Outcomes are stochastic: we write for exogenous uncertainty with law that may depend on . The expected utilities are

| (1) |

where represents the agent’s penalty (e.g., effort cost, disutility, or risk). Anticipating the agent’s response, the principal solves the bilevel max–max problem

| (2) | |||

| (3) |

This formulation imposes no specific wage rule, production technology, or participation constraint; the only structural requirement is that utilities are expressed as expectations under a possibly decision-dependent .

In classical linear–quadratic models (e.g., Holmström–Milgrom), the forms of and yield closed-form expressions for and . Outside these highly structured settings, however, realistic models involve nonlinearities, multidimensional actions, and additional constraints, precluding analytic solutions. We therefore seek a numerical method that (i) treats expectation-valued objectives faithfully, (ii) remains valid when depends on decisions, and (iii) scales to high-dimensional actions without forming or inverting Hessians. The central challenge is thus clear: How can we design efficient optimization algorithms to solve general bilevel max–max problems when no analytical solution is available?

3 Method

We propose a generic bilevel max–max optimizer that integrates four key components: (i) sample-average approximation (SAA) for expectation-valued objectives; (ii) implicit differentiation of the inner argmax via matrix-free Hessian–vector products (HVPs) and conjugate gradients (CG); (iii) variance reduction using common random numbers (CRN); and (iv) bound-aware updates for the outer variables.

Throughout, we treat (agent variables) and (contract variables) as tensors of arbitrary shape. We assume that is differentiable and locally strictly concave in at the inner solution, while is differentiable in both arguments. Under these assumptions, the Hessian block is negative definite at a local maximum of the inner problem, which ensures that is symmetric positive definite (SPD). This property is crucial, as it guarantees the stability of the CG solve used to compute implicit gradients.

3.1 Monte Carlo estimation with decision-dependent sampling

We approximate the expectations in (1) using a sample-average approximation (SAA). Given and i.i.d. samples , the estimator is

| (4) |

When the sampling distribution depends on decisions, with density , the gradient of decomposes into explicit and score function terms. For and under standard regularity conditions,

| (5) |

If a reparameterization with exists (independent of learned parameters), we may instead compute gradients pathwise by differentiating . In practice, we apply automatic differentiation directly to the SAA estimator (4), ensuring that analytic and Monte Carlo models share the same code path and that both score-function and pathwise gradients are handled seamlessly.

Common Random Numbers (CRN) and consistent evaluation. To reduce variance in hypergradients, we employ common random numbers (CRN). Each outer iteration generates a single randomness payload (mini-batch or latent seed) that is reused for all evaluations of , their gradients, and all HVPs. Optionally, the seed is refreshed every steps, and antithetic augmentation ( with ) can be applied. For evaluation and reporting, we construct a single held-out batch that remains fixed throughout training. This consistent evaluation ensures that reported trajectories reflect parameter changes rather than sampling noise.

3.2 Implicit differentiation of the inner maximum

Theoretical derivation. Let denote a local maximizer of the agent’s objective . At such a point, the first-order optimality condition and local curvature are

| (6) |

where the negative definiteness of reflects that is a strict local maximum.

The dependence of on the contract can be characterized using the implicit function theorem. Differentiating the optimality condition yields

| (7) |

which provides the sensitivity of the best response to changes in the contract.

Substituting this expression into the chain rule gives the hypergradient of the outer objective

| (8) |

Thus, computing the hypergradient requires solving a linear system involving .

Since is negative definite at the inner maximum, is symmetric positive definite (SPD). We therefore solve for in the damped SPD system

| (9) |

where a small damping parameter improves conditioning, with vanishing bias as .

Finally, the mixed Hessian term is computed without explicitly forming Hessians, by applying the standard Hessian–vector product (HVP) identity

| (10) |

This matrix-free formulation enables efficient computation at scale.

3.3 Practical Considerations

Approximating . In practice, the agent’s exact best response cannot be computed. Instead, we approximate it by running a short gradient ascent on , reusing the same CRN payload at every step to control variance. The ascent is terminated once the stationarity condition is satisfied, or after at most iterations. The resulting iterate serves as an approximation of and also provides a natural warm start for the next outer iteration. Under mild regularity assumptions, the bias introduced by inexact solves vanishes as .

Hypergradient via implicit differentiation. The hypergradient (8) is evaluated at rather than . To avoid explicitly inverting the inner Hessian , we introduce an auxiliary vector defined as the solution of the damped SPD system

| (11) |

which is solved approximately using at most iterations of conjugate gradient. The mixed Hessian term is then recovered in matrix-free form using the standard Hessian–vector product identity,

| (12) |

Combining these pieces yields the estimator

with optional norm clipping for numerical stability.

SPD fix and damping. At a local maximum of the inner problem, the curvature matrix is negative definite. Replacing it by therefore yields a symmetric positive definite system, which is well suited for solution by CG. Adding a small damping term further improves conditioning, while the bias induced by damping vanishes in the limit .

Variance reduction with CRN. Within each outer iteration, all evaluations of , , their gradients, and every HVP reuse the same randomness payload (either a mini-batch or a latent seed). This reuse substantially stabilizes both the right-hand side of the CG system and the mixed HVP, yielding smoother optimization. In practice, seeds may be refreshed periodically (every steps), and antithetic augmentation (using and ) can further reduce variance. For evaluation and reporting, a single fixed held-out batch is used throughout training to ensure comparability across iterations.

Bounds and projections. We support user-specified projections ; otherwise we apply box constraints . Outer updates use an active-set scheme: coordinates strictly inside their bounds update freely, while boundary coordinates are clamped. This preserves feasibility and avoids tangential drift along the constraint surface.

Computational cost. Let , , and the SAA batch size. Per outer iteration we compute gradients w.r.t. , HVPs with , one mixed HVP for , and the first-order gradients . Under dense autodiff, a gradient/HVP w.r.t. the -block scales linearly in , and a gradient w.r.t. the -block scales linearly in . Hence the per-iteration work is , with no Hessian formed or inverted. Memory is for CG vectors (plus model activations), and projection/active-set operations are . Thus the method avoids the costs of explicit Hessians and scales linearly in , , and .

4 Experiments

Experimental setup. Our experiments evaluate whether implicit differentiation with conjugate gradient (CG) reliably recovers optimal contracts in principal–agent bilevel problems. We benchmark across two classes of environments:

-

•

Canonical CARA–Normal linear–contract models with closed-form solutions: (1) the Holmström–Milgrom linear–quadratic benchmark (Holmström, , 1979), (2) insurance with prevention (self-protection) (Ehrlich and Becker, , 1972; Shavell, , 1979), (3) imperfect performance measurement with a single noisy signal (Laffont and Martimort, , 2002), (4) aggregation of two noisy signals (Laffont and Martimort, , 2002; Baker, , 1992), (5) separable multitask contracting (Holmström and Milgrom, , 1991). These environments admit closed-form optima , and (6) relative performance (peer benchmark), enabling direct error measurement.

-

•

Nonlinear signal environments without closed-form solutions: Beyond the linear–quadratic CARA–Normal benchmarks, we also evaluate nonlinear environments motivated by the First-Order-Approach (FOA) literature, where explicit analytical solutions are unavailable. These include logistic and Poisson signal models and nonlinear wage utilities, which have been used as canonical worked examples in Jewitt’s FOA analysis (Jewitt, , 1988).

Full derivations of the CARA–Normal cases and details of the grid-search approximation for nonlinear signals are provided in Appendix B.1.

Settings. For each environment, we fix baseline parameters (e.g., cost , noise ) and vary one parameter of interest (e.g., risk aversion ) over a grid. Contract parameters and actions are initialized independently as . We solve the bilevel problem (2)–(3) using Alg. 1. The agent’s problem is solved by gradient ascent on with step size for at most iterations, terminating when . The principal’s parameters are updated for (linear) and (nonlinear) steps with step size . Hypergradients are computed via CG with iterations and damping . Each inner solve is warm-started from the previous . To control estimator variance, we use common random numbers (CRN): within each outer iteration we reuse a Sobol–QMC batch of size (with antithetic pairing), refreshing it every iterations.

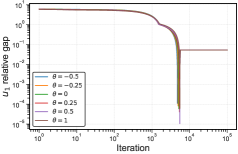

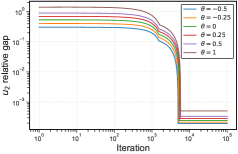

Evaluation metrics. For evaluation, we fix a Sobol–QMC batch of size from the signal distribution and use it consistently to compute expected utilities. On this held-out batch, we report four primary metrics: the relative action and contract errors , and the principal’s normalized utility gap and . Here, is a small constant for numerical stability (we used across all of the experiments).

Ground-truth approximation. For environments lacking closed-form solutions, we approximate the optimal contract by nested grid search. Specifically, we discretize the contract space over a box derived from the setting parameters, and for each candidate contract compute the agent’s best response by maximizing on a dense action grid. Utilities and are estimated by Monte Carlo expectation on a fixed Sobol–QMC batch of samples from the relevant signal distribution (e.g., Logistic or Laplace). To reduce variance and ensure fair comparisons, the same random draws are reused across all grid points (common random numbers) and paired antithetically. The principal’s payoff is then evaluated at each candidate, and the maximizing pair is taken as the approximate ground-truth solution. For example, in the logistic–signal case we discretize over a rectangular box that scales with the signal scale (e.g. , ) using a grid. For each , the best-response action is approximated on a -point grid spanning . For per-setting details, see App. B.1.

For settings with multiple contract slopes, only the incentive coefficients are optimized by grid search, while fixed transfers are set post hoc to satisfy the participation constraint at equality. Wages are always floored at to maintain numerical stability under or utilities. Together, these design choices yield stable and reproducible approximate optima that serve as a consistent reference for benchmarking our gradient-based solver.

4.1 Results

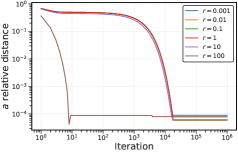

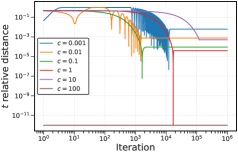

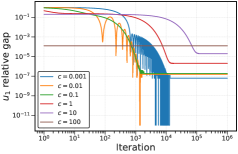

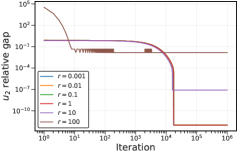

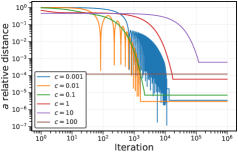

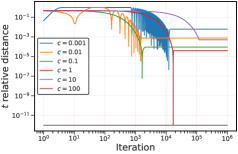

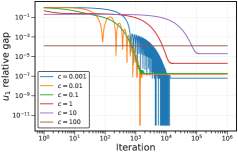

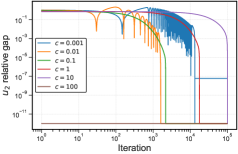

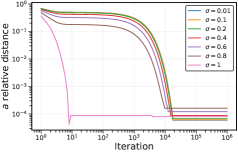

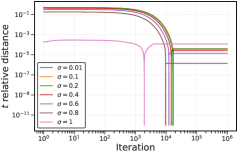

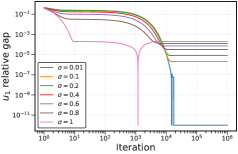

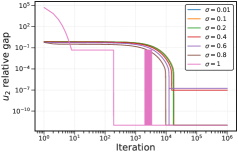

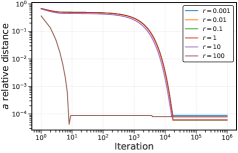

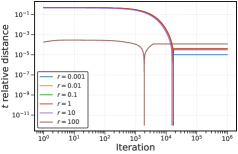

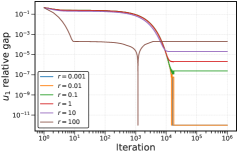

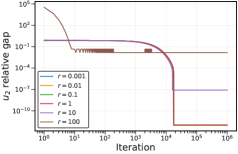

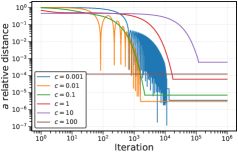

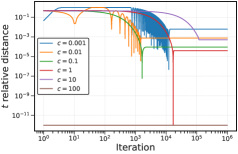

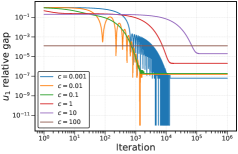

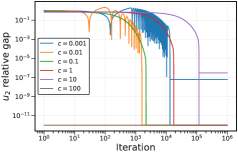

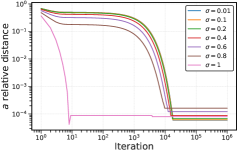

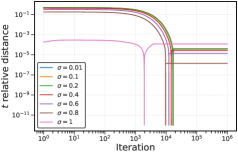

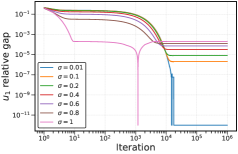

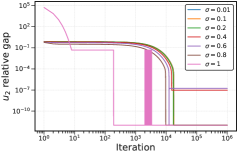

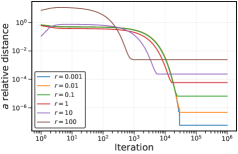

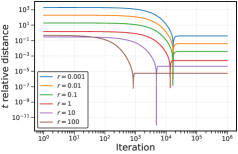

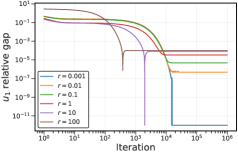

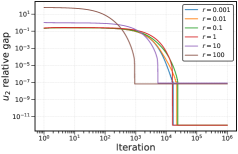

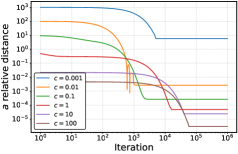

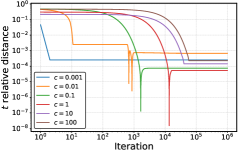

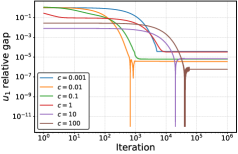

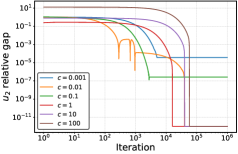

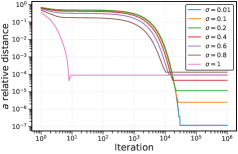

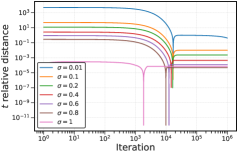

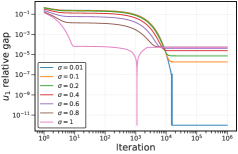

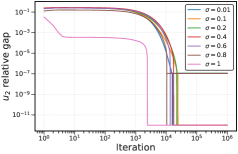

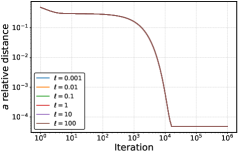

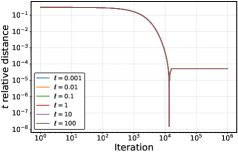

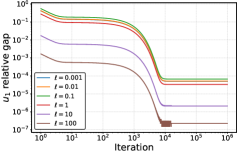

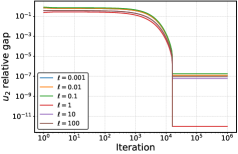

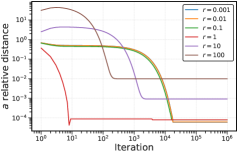

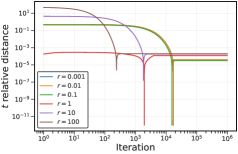

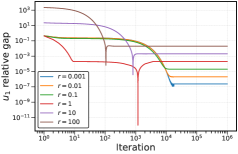

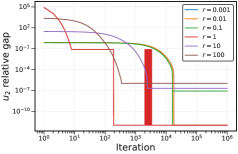

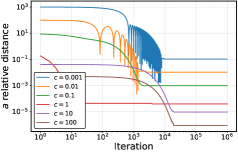

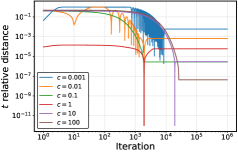

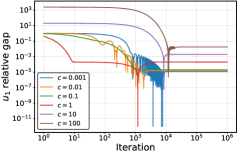

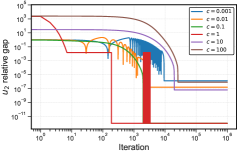

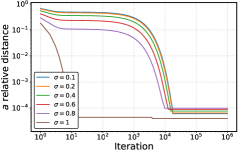

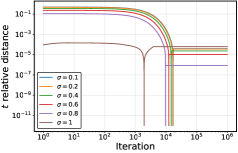

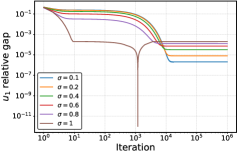

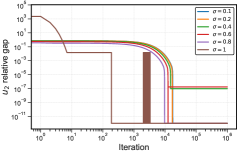

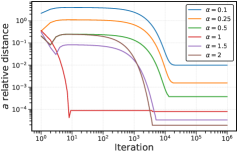

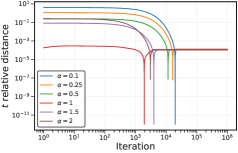

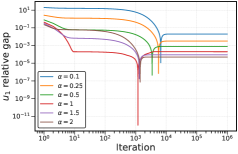

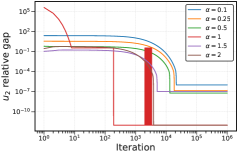

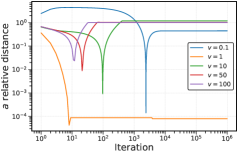

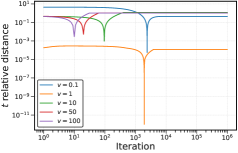

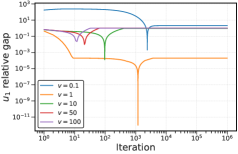

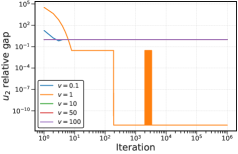

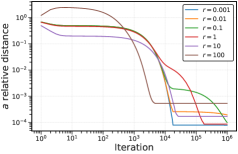

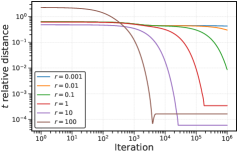

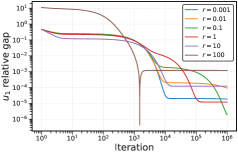

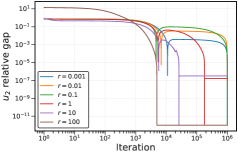

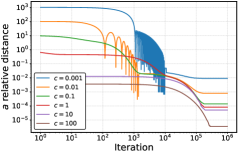

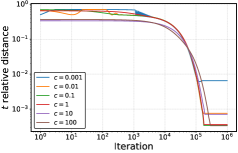

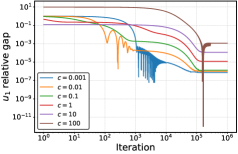

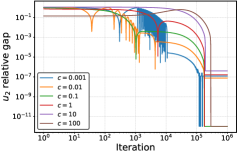

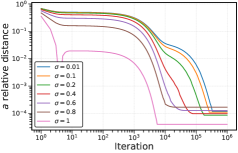

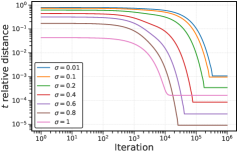

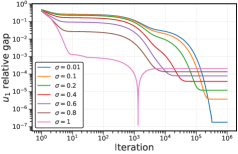

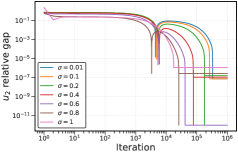

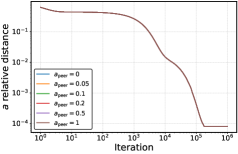

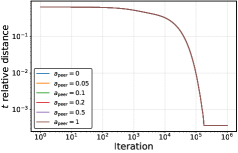

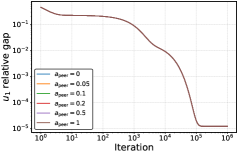

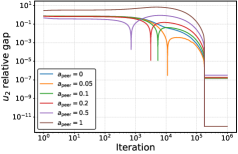

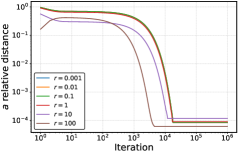

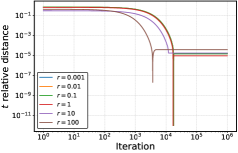

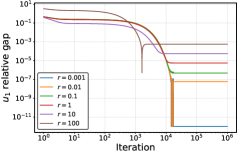

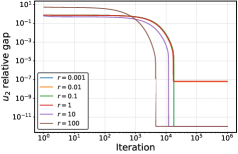

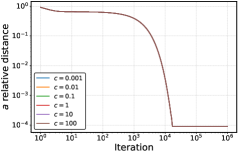

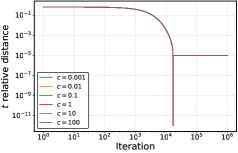

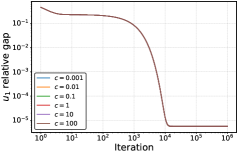

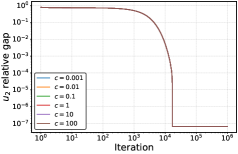

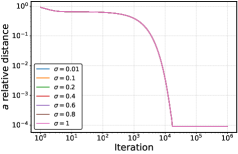

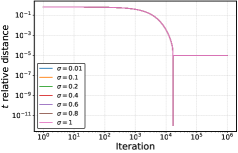

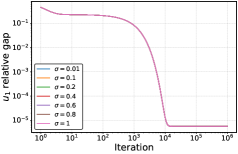

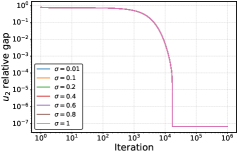

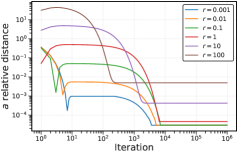

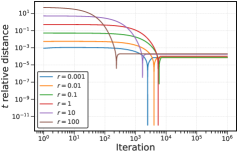

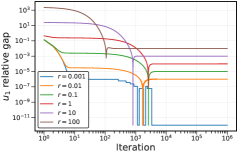

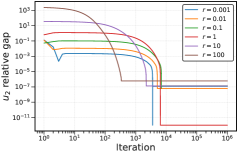

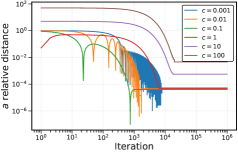

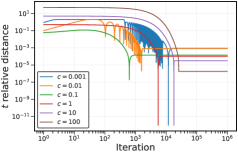

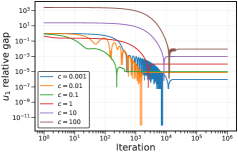

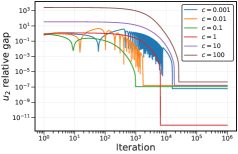

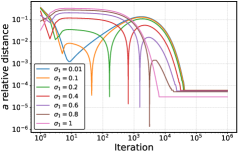

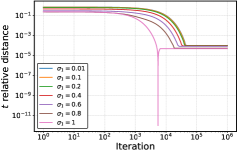

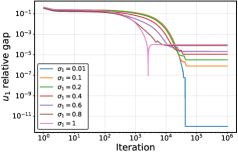

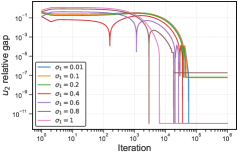

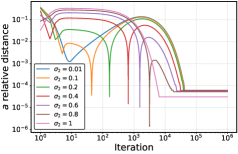

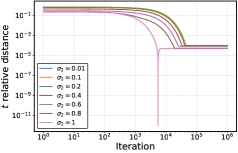

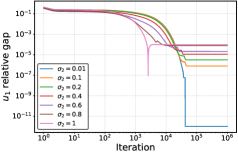

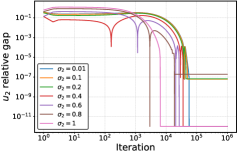

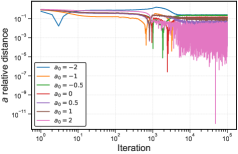

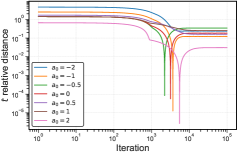

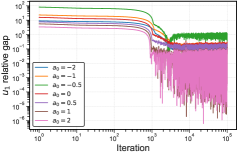

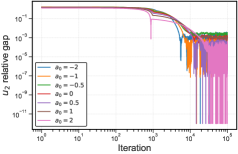

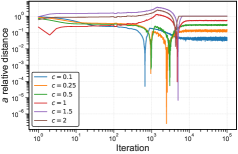

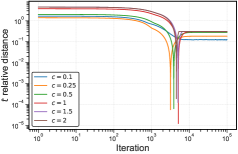

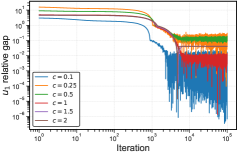

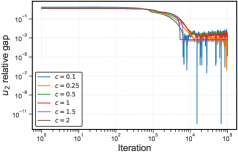

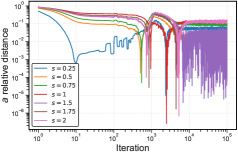

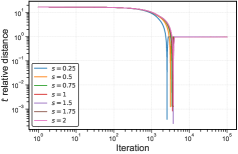

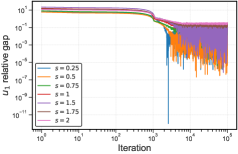

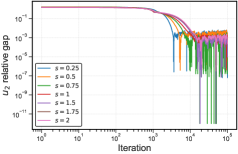

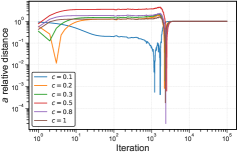

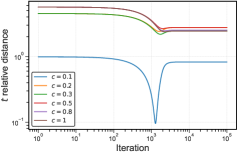

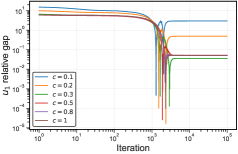

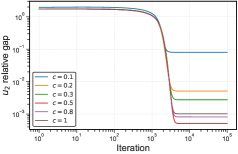

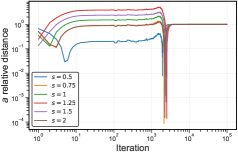

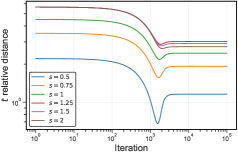

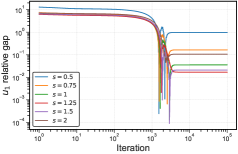

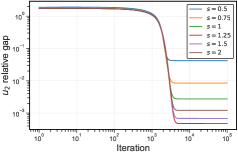

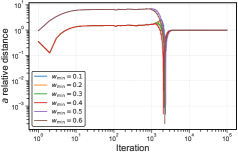

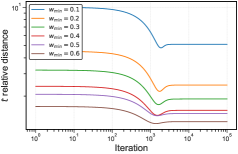

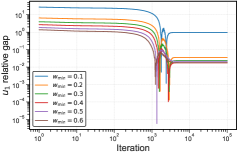

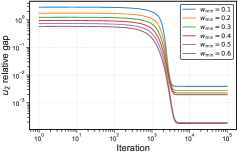

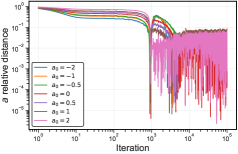

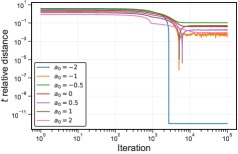

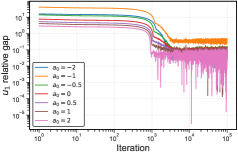

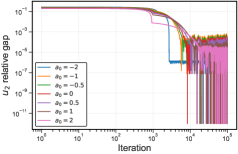

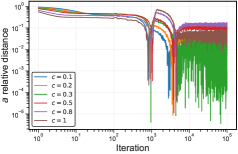

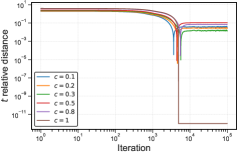

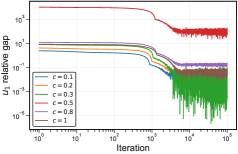

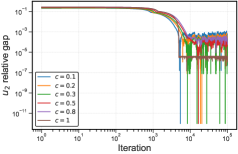

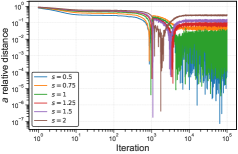

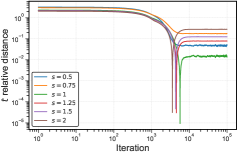

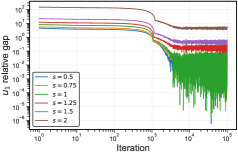

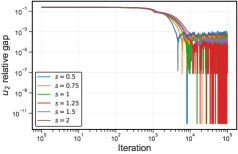

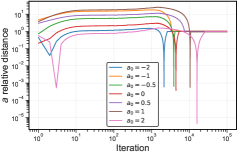

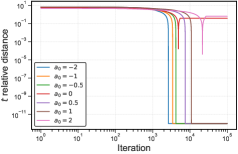

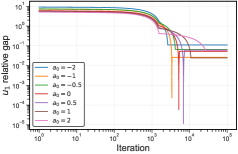

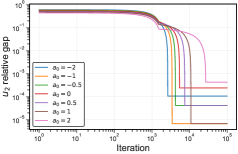

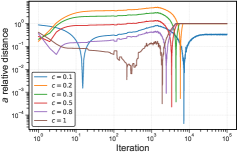

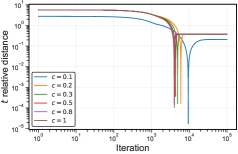

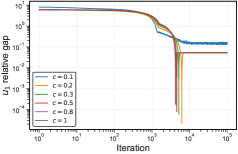

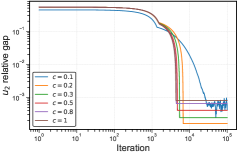

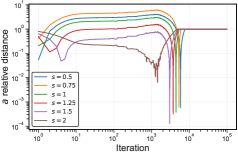

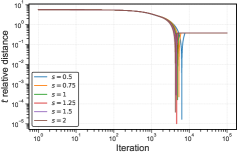

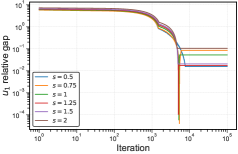

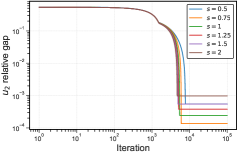

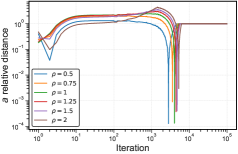

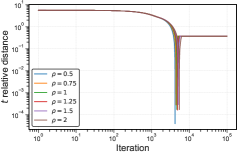

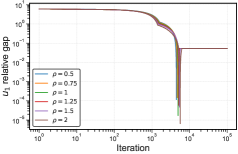

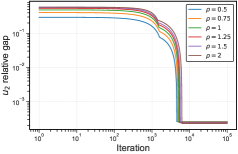

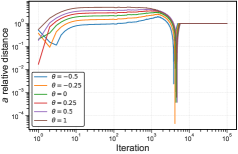

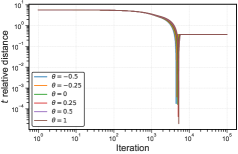

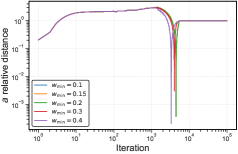

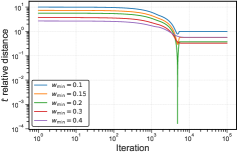

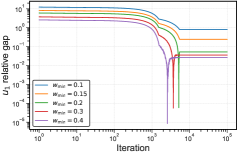

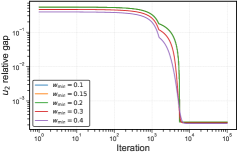

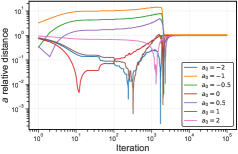

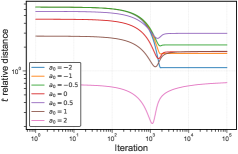

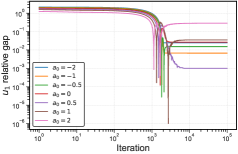

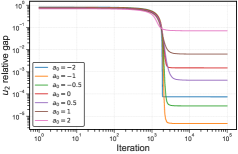

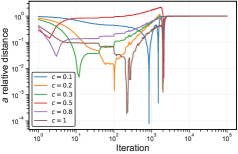

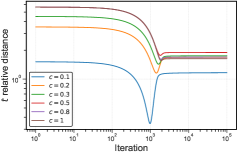

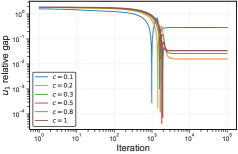

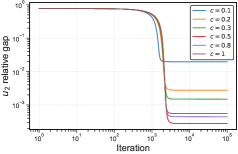

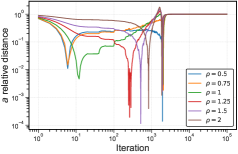

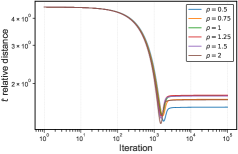

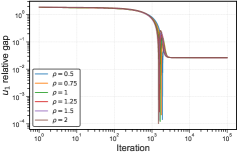

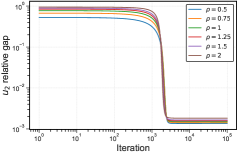

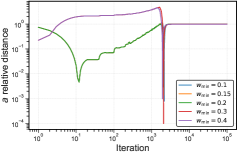

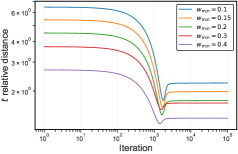

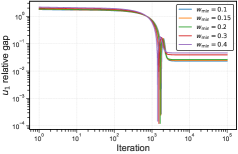

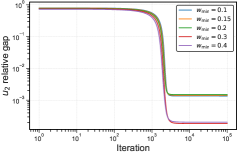

Our experiments reveal a sharp distinction between linear and nonlinear environments. We first consider the family of linear CARA–Normal benchmarks. These settings admit closed-form solutions, allowing us to directly assess whether the learning dynamics recover both utilities and contract parameters. In every linear environment we studied, the results are unambiguous: the utility gaps converges very close to zero (e.g., 9, 12) and the distances for the learned contract parameters and the ground-truth parameters vanish (e.g., Figs. 8, 10, 14) as well as the distance between the learned action and the corresponding optimal action. This demonstrates that the proposed bilevel solver with implicit differentiation is able to recover the analytic solution to high precision.

A key feature of these linear results is their robustness. Across sweeps in cost coefficients, levels of risk aversion, and signal noise, the algorithm consistently converges to the exact solution (see for instance Figs. 2-4). Neither extreme values of the parameters nor variations across different benchmark structures degrade performance (e.g., Figs. 4, 8, 9). This uniformity underscores that conjugate-gradient hypergradients remain stable throughout the optimization, yielding unbiased updates even when the problem is highly conditioned. In short, whenever the underlying model has a unique optimum, the solver reliably recovers it.

The nonlinear signal environments, in contrast, exhibit different behavior. Here the optimization succeeds in recovering the utilities: the agent and principal payoffs converge to the grid-search reference across a wide range of parameters (e.g., Figs. 37, 39). However, the corresponding contract parameters show a different trajectory. Their distances decrease initially but oftentimes plateau at non-negligible values, indicating that the learned contract does not always coincide with the specific reference solution (e.g., Figs. 28, 41). This divergence is not a numerical artifact but a reflection of the underlying setting.

Nonlinear signal models of the FOA type are not uniquely identifiable. Multiple contracts can implement the same distribution of outcomes, or at least equally good outcomes, and hence deliver identical utilities to the principal and agent. The plateauing of parameter distances we observe is the empirical manifestation of this non-identifiability. The algorithm converges to one of many payoff-equivalent optima, preserving the utilities but not the contract parameters themselves. Thus, in nonlinear environments, the method should be judged primarily on whether it recovers the correct utilities rather than the precise contract form.

Another subtlety in the nonlinear case is that convergence in utilities is less uniform. For some parameter regimes, the utility gaps shrink smoothly to near zero (e.g., Figs. 37, 39), while for others they remain noisy and hover at more moderate error levels (e.g., Figs. 28, 30). We attribute this to a combination of evaluation variance and sensitivity to the reference solution. Nonetheless, the trend is consistent across settings: the learned contracts deliver utilities close to optimal even when the parameter recovery is imperfect. This reinforces the view that the algorithm captures the economically relevant objects—payoffs—despite the absence of parameter identifiability.

Overall, the experiments show a dichotomy: on linear CARA–Normal benchmarks we exactly recover utilities and parameters; on nonlinear signals we are utility-consistent—matching optimal payoffs even when parameters aren’t uniquely identified. Thus, the method gives exact recovery with unique solutions and payoff consistency when multiple contracts implement the outcome.

Conclusions. We introduced a scalable solver for principal–agent contract design by formulating hidden-action problems as bilevel max–max programs and applying implicit differentiation with conjugate gradients. The method avoids forming Hessians, recovers linear–quadratic optima to high precision, and extends to nonlinear and higher-dimensional settings where closed forms are unavailable. In nonlinear environments, it matches the economically relevant objects — the principal and agent utilities — even when several payoff-equivalent contracts exist. This establishes a practical bridge between classic contract theory and modern differentiable optimization.

Limitations and scope. Our analysis assumes smooth, correctly specified primitives for utilities, outcome laws, and constraints; non-smooth penalties or misspecification can challenge the regularity behind implicit differentiation. We study a locally concave inner problem (negative-definite Hessian block); flat or non-unique best responses may ill-condition the linear system, though damping and CG tolerances help. The present scope is static and single-agent; extending to dynamic, repeated, and multi-agent/competing-principal settings is a natural next step. Institutional frictions (limited liability, participation/renegotiation, budget balance, enforcement) can be added via tailored projections or penalties, with possible effects on convergence. In nonlinear signal models, utilities are identifiable but contract parameters need not be, so we target payoff consistency rather than exact recovery. Finally, estimates use sample-average approximation with common random numbers; hypergradients carry Monte Carlo noise but are stable with sensible batch sizes, damping, and CG tolerances. Finally, our grid-search references are reliable in low dimension yet motivate more scalable baselines.

5 Reproducibility Statement

We have aimed to make all components of our results easy to reproduce. The algorithmic details—including the sample-average approximation, implicit differentiation, CG solver, and common-random-numbers variance reduction—are specified in Sec. 3 and Algorithms 1–5, with all hyperparameters (learning rates/step sizes, iteration budgets, tolerances, CG damping, projections) reported in Sec. 4. Closed-form benchmarks (e.g., Holmström–Milgrom and extensions) and their derivations appear in App. B.1, which also describes the nonlinear environments and our grid-search ground-truth procedure (contract/action grids, boxes, and Monte Carlo/QMC settings). For stochastic estimation, we fix Sobol–QMC seeds and reuse common random numbers across all evaluations, as documented in Secs. 3.1–3.2. We provide, as anonymized supplementary material, a code repository containing: (i) reference implementations of Algs. 1–5 (matrix-free HVP/CG), (ii) environment generators and evaluators (CARA–Normal and nonlinear), (iii) exact-solution checkers for the closed-form cases, (iv) experiment configurations are documented in the captions of each experiment, and (v) plotting scripts to recreate the figures. We provide a readme file that describes how to reproduce some of the results in the paper. Assumptions for all theoretical claims are stated inline with each result, and complete proofs/derivations are included in the main text.

References

- Alon et al., (2023) Alon, T., Duetting, P., Li, Y., and Talgam-Cohen, I. (2023). Bayesian analysis of linear contracts. In EC, page 66.

- Alon et al., (2021) Alon, T., Dütting, P., and Talgam-Cohen, I. (2021). Contracts with private cost per unit-of-effort. In Proceedings of the 22nd ACM Conference on Economics and Computation, EC ’21, page 52–69, New York, NY, USA. Association for Computing Machinery.

- Babichenko et al., (2024) Babichenko, Y., Talgam-Cohen, I., Xu, H., and Zabarnyi, K. (2024). Information design in the principal-agent problem. In Proceedings of the 25th ACM Conference on Economics and Computation, EC ’24, page 669–670, New York, NY, USA. Association for Computing Machinery.

- Baker, (1992) Baker, G. P. (1992). Incentive contracts and performance measurement. Journal of Political Economy, 100(3):598–614.

- Bard, (2008) Bard, J. F. (2008). Bilevel programming in management. In Floudas, C. and Pardalos, P., editors, Encyclopedia of Optimization. Springer, Boston, MA.

- Barrett et al., (1994) Barrett, R., Berry, M., Chan, T. F., Demmel, J., Donato, J. M., Dongarra, J., Eijkhout, V., Pozo, R., Romine, C., and van der Vorst, H. A. (1994). Templates for the Solution of Linear Systems: Building Blocks for Iterative Methods. Other Titles in Applied Mathematics. SIAM, Philadelphia, PA.

- Bolton and Dewatripont, (2005) Bolton, P. and Dewatripont, M. (2005). Contract Theory. MIT Press.

- Cacciamani et al., (2024) Cacciamani, F., Bernasconi, M., Castiglioni, M., and Gatti, N. (2024). Multi-agent contract design beyond binary actions. In Proceedings of the 25th ACM Conference on Economics and Computation, EC ’24, page 1293, New York, NY, USA. Association for Computing Machinery.

- Cachon, (2003) Cachon, G. P. (2003). Supply chain coordination with contracts. In Handbooks in Operations Research and Management Science, volume 11. Elsevier.

- Colson et al., (2007) Colson, B., Marcotte, P., and Savard, G. (2007). An overview of bilevel optimization. Annals of Operations Research, 153(1):235–256.

- Domke, (2012) Domke, J. (2012). Generic methods for optimization-based modeling. In Proceedings of the Fifteenth International Conference on Artificial Intelligence and Statistics, pages 318–326. PMLR.

- Duetting et al., (2023) Duetting, P., Feldman, M., and Peretz, D. (2023). Ambiguous contracts. In Proceedings of the 24th ACM Conference on Economics and Computation, EC ’23, page 539, New York, NY, USA. Association for Computing Machinery.

- Duetting et al., (2024) Duetting, P., Feldman, M., and Talgam-Cohen, I. (2024). Algorithmic contract theory: A survey.

- Dütting et al., (2022) Dütting, P., Feng, Z., Narasimhan, H., Parkes, D. C., and Ravindranath, S. S. (2022). Optimal auctions through deep learning: Advances in differentiable economics. J. ACM, 71(1).

- Dütting et al., (2019) Dütting, P., Roughgarden, T., and Talgam-Cohen, I. (2019). Simple versus optimal contracts. In Proceedings of the 2019 ACM Conference on Economics and Computation, EC ’19, page 369–387, New York, NY, USA. Association for Computing Machinery.

- Dütting et al., (2021) Dütting, P., Roughgarden, T., and Talgam-Cohen, I. (2021). The complexity of contracts. SIAM J. Comput., 50(1):211–254.

- Dütting and Talgam-Cohen, (2019) Dütting, P. and Talgam-Cohen, I. (2019). Tutorial: “contract theory: A new frontier for agt”. YouTube video. Available at https://www.youtube.com/watch?v=JQsqPXCehOU and https://www.youtube.com/watch?v=k_c-aZdpeBo.

- Ehrlich and Becker, (1972) Ehrlich, I. and Becker, G. S. (1972). Market insurance, self-insurance, and self-protection. Journal of Political Economy, 80(4):623–648.

- Ezra et al., (2024) Ezra, T., Feldman, M., and Schlesinger, M. (2024). On the (In)approximability of Combinatorial Contracts. In Guruswami, V., editor, 15th Innovations in Theoretical Computer Science Conference (ITCS 2024), volume 287 of Leibniz International Proceedings in Informatics (LIPIcs), pages 44:1–44:22, Dagstuhl, Germany. Schloss Dagstuhl – Leibniz-Zentrum für Informatik.

- Gould et al., (2016) Gould, S., Fernando, B., Cherian, A., Anderson, P., Cruz, R. S., and Guo, E. (2016). On differentiating parameterized argmin and argmax problems with application to bi-level optimization. ArXiv, abs/1607.05447.

- Grossman and Hart, (1983) Grossman, S. J. and Hart, O. D. (1983). An analysis of the principal-agent problem. Econometrica, 51(1):7–45.

- Hestenes and Stiefel, (1952) Hestenes, M. R. and Stiefel, E. (1952). Methods of conjugate gradients for solving linear systems. Journal of Research of the National Bureau of Standards, 49(6):409–436.

- Ho et al., (2014) Ho, C.-J., Slivkins, A., and Vaughan, J. W. (2014). Adaptive contract design for crowdsourcing markets: bandit algorithms for repeated principal-agent problems. In Proceedings of the Fifteenth ACM Conference on Economics and Computation, EC ’14, page 359–376, New York, NY, USA. Association for Computing Machinery.

- Holmström, (1979) Holmström, B. (1979). Moral hazard and observability. The Bell Journal of Economics, 10(1):74–91.

- Holmström and Milgrom, (1987) Holmström, B. and Milgrom, P. (1987). Aggregation and linearity in the provision of intertemporal incentives. Econometrica, 55(2):303–328.

- Holmström and Milgrom, (1991) Holmström, B. and Milgrom, P. (1991). Multitask principal-agent analyses: Incentive contracts, asset ownership, and job design. Journal of Law, Economics, & Organization, 7:24–52.

- Jensen and Meckling, (1976) Jensen, M. C. and Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4):305–360.

- Jewitt, (1988) Jewitt, I. (1988). Justifying the first‐order approach to principal‐agent problems. Econometrica, 56(5):1177–1190.

- Laffont and Martimort, (2002) Laffont, J.-J. and Martimort, D. (2002). The Theory of Incentives: The Principal–Agent Model. Princeton University Press.

- Lazear and Gibbs, (2014) Lazear, E. P. and Gibbs, M. (2014). Personnel Economics in Practice. John Wiley & Sons, 3 edition.

- Lorraine et al., (2020) Lorraine, J., Vicol, P., and Duvenaud, D. (2020). Optimizing millions of hyperparameters by implicit differentiation. In Proceedings of the 23rd International Conference on Artificial Intelligence and Statistics, volume 108 of Proceedings of Machine Learning Research, pages 1540–1552. PMLR.

- Maclaurin et al., (2015) Maclaurin, D., Duvenaud, D., and Adams, R. P. (2015). Gradient-based hyperparameter optimization through reversible learning. In Proceedings of the 32nd International Conference on Machine Learning, pages 2113–2122. PMLR.

- Milgrom and Roberts, (1992) Milgrom, P. and Roberts, J. (1992). Economics, Organization and Management. Prentice Hall.

- Myerson, (1981) Myerson, R. B. (1981). Optimal auction design. Mathematics of Operations Research, 6(1):58–73.

- Rajeswaran et al., (2019) Rajeswaran, A., Finn, C., Kakade, S. M., and Levine, S. (2019). Meta-learning with implicit gradients. In Advances in Neural Information Processing Systems, volume 32.

- Ren et al., (2018) Ren, M., Zeng, W., Yang, B., and Urtasun, R. (2018). Learning to reweight examples for robust deep learning. In Dy, J. and Krause, A., editors, Proceedings of the 35th International Conference on Machine Learning, volume 80 of Proceedings of Machine Learning Research, pages 4334–4343. PMLR.

- Salanié, (2017) Salanié, B. (2017). The Economics of Contracts: A Primer. MIT Press, 3 edition.

- Sannikov, (2008) Sannikov, Y. (2008). A continuous-time version of the principal–agent problem. The Review of Economic Studies, 75(3):957–984.

- Shavell, (1979) Shavell, S. (1979). On moral hazard and insurance. The Quarterly Journal of Economics, 93(4):541–562.

- Wang et al., (2023) Wang, T., Duetting, P., Ivanov, D., Talgam-Cohen, I., and Parkes, D. C. (2023). Deep contract design via discontinuous networks. In Thirty-seventh Conference on Neural Information Processing Systems.

Appendix A LLM Usage Statement

Large Language Models (LLMs) were used solely as an assistive tool for improving the clarity and presentation of the manuscript (e.g., editing grammar, refining phrasing). All technical content, including theoretical derivations, proofs, experimental design, and analysis, was developed entirely by the authors. No parts of the paper were written or ideated by an LLM in a way that would constitute substantive scientific contribution, and no LLM was used to generate or fabricate results.

Appendix B Additional Results

To expand on the main-text experiments, we conducted a wide range of experiments with the settings outlined below.

B.1 Settings

We study hidden–action principal–agent models in which a risk–neutral principal offers a (possibly nonlinear) contract to a risk–averse agent who chooses an unobservable action . Outcomes are noisy, compensation depends on observables, and the agent incurs a quadratic effort cost. We group environments into linear settings with closed-form optima and nonlinear settings where we compute reference solutions numerically.

Ground-truth estimation and search domains for nonlinear contract-design settings. When closed forms are unavailable, we approximate ground truth via a nested grid search: for each contract parameters on a rectangular grid, we estimate the agent’s best response on a 1D action grid and then pick the that maximizes the principal’s objective at . Unless stated otherwise, we use common random numbers (CRN) within each search to reduce variance.

We reuse the following generic boxes (chosen to enforce wage floors for nonlinear utilities and to cover essentially all mass of given the noise scale):

The contract grid is ; the action grid has 200 points. When a different box is used (e.g., CRRA), we state the change explicitly below.

B.1.1 Linear Settings

Holmström–Milgrom.

Output with and linear pay . With CARA agent (risk aversion ) and effort cost ,

Imposing participation yields

Insurance with prevention (self–protection).

Loss , , linear indemnity , premium .

Closed-form optimum:

Imperfect performance measurement.

Signal , ; contract .

Closed-form optimum:

Relative performance (peer benchmark). Two agents with common shock and idiosyncratic noise. Contract . Let . Then

and from participation.

Separable multitask. tasks with signals , . Contract . Then, task-wise,

and is pinned down by participation:

Two signals. Output is observed through two independent noisy signals with variances ; the contract is . Let the effective variance be the harmonic-mean aggregate

Define . The optimal slopes split in proportion to signal precisions:

and the induced action is . The transfer is pinned down by the participation constraint.

B.1.2 Nonlinear Settings

Logistic signal. We use with and floor . Output takes the form (distribution varies by setting). The principal’s objective is ; the agent’s utility varies below.

Logistic signal with square-root wage utility. , . Ground truth via the generic boxes above; CRN with a single Logistic batch.

Logistic signal with CRRA wage utility. , (log in the limit). Here we tighten the contract box to keep well within a stable range:

We keep the same grid resolutions and CRN scheme.

Laplace signal with thresholded wage utility. , with curvature and reference . We use the generic boxes; the action range covers of the mass under Laplace noise. CRN with a single Laplace batch.

Poisson signal. Counts with mean are approximated as , . Agent is CARA over wages: . We use the generic contract box and center the action window at with width (independent of here due to the reparameterization). CRN with a single Normal batch.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|