Generative AI in Finance

Mitigating Model Drift in Developing Economies

using Synthetic Data and Outliers

Abstract

Machine learning models in finance are highly susceptible to model drift, where predictive performance declines as data distributions shift. This issue is especially acute in developing economies such as those in Central Asia and the Caucasus—including Tajikistan, Uzbekistan, Kazakhstan, and Azerbaijan—where frequent and unpredictable macroeconomic shocks destabilize financial data. To the best of our knowledge, this is among the first studies to examine drift mitigation methods on financial datasets from these regions. We investigate the use of synthetic outliers, a largely unexplored approach, to improve model stability against unforeseen shocks. To evaluate effectiveness, we introduce a two-level framework that measures both the extent of performance degradation and the severity of shocks. Our experiments on macroeconomic tabular datasets show that adding a small proportion of synthetic outliers generally improves stability compared to baseline models, though the optimal amount varies by dataset and model.111We release all code, metrics, and experiments, including the synthetic data used with the open dataset, at: https://github.com/zypl-ai/stabilization_uplift/.

1 Introduction

Machine learning models deployed in finance frequently experience performance degradation under distribution shift, known as model drift. Drift arises when statistical properties of new data diverge from the training distribution. More concretely, when the conditional relationship between features and outcomes changes, this is referred to as concept drift Hinder2024 ; Halstead2022 , and is particularly relevant in more unstable economies.

Traditional approaches to mitigating drift include monitoring model metrics and retraining with online or incremental learning, or expanding ensembles when drift is detected Gemaque2020 . Data-centric strategies such as resampling, sliding windows (keeping only the most recent chunk of data), domain adaptation to shifted distributions, and continuous feedback loops are also common Hinder2024 ; Gama2014 , as later discussed in Section 2. More recently, by simulating future distributions, synthetic data generation has been used to prepare models for drift conditions without waiting for real-world data Chiu2024 . However, the role of synthetic outliers in stabilizing models remains largely unexplored kraus2025machine particularly in the context of developing economies.

Building on this line of research, this paper makes the following contributions: (1) Stability metrics for model drift evaluation under shocks. We propose a two-level framework: the Stabilization Score (SS), which calculates the relative performance drop of a model under sudden shocks while normalizing by covariate drift, and the Stabilization Uplift (SU), a comparative evaluation of two models under shock, using their pre-/post-shock performance. (2) Synthetic outliers for model drift mitigation. We show that deliberately generated outliers, produced with zGAN azimi2024zgan , which we review in Appendix A, can improve model stability when combined with real and synthetic data (we calculate this using our metrics). (3) Focus on developing economies. While most work on model drift and stability relies on datasets from mature financial markets, we conduct experiments on macroeconomic tabular datasets from developing economies in Central Asia and the Caucasus, where shocks are often more present. This is both an underexplored empirical setting in the generative AI for finance literature and one where stabilization methods are especially critical.

2 Related Work

Drift detection and adaptation methods. Several forms of drift are especially present in financial applications: time-based drift, where dependencies evolve gradually over time (e.g., seasonal repayment behavior in credit scoring Zliobaite2012 ); conditional drift, where new data arrives from underrepresented regions of the feature space (e.g., new geographies Gama2014 ); and contextual or sudden drift, where input–output relations shift abruptly due to external shocks such as pandemics, conflicts, or policy changes Tsymbal2004 . A central challenge is identifying when model performance deteriorates due to distributional change. The ADWIN (ADaptive WINdowing) algorithm Bifet2007 remains a widely used baseline that resizes its window based on detected change. More recent work considers stability under adversarial conditions Korycki_2022 , causal approaches for interpretability YANG2025 , practical case studies (e.g., COVID-19) highlighting the vulnerability of financial models to sudden shocks SONNLEITNER2025 , and applications in business processes kraus2025machine . Classical approaches rely on incremental or online learning with sliding/expanding windows Agrahari2024 ; neural models under continuously evolving distributions often employ statistical tests such as Kolmogorov–Smirnov (KS) Prashanth2025 ; and unsupervised settings benchmark drift detection on complex real-world data streams lukats2025benchmark .

Synthetic data. While the targeted use of synthetic outliers to mitigate drift and improve stability remains largely unexplored, related work includes Puranik et al. Puranik2024 , who propose the TabOOD framework to generate out-of-distribution tabular samples that improve generalization, and Kraus et al. kraus2025machine , who demonstrate the use of synthetic data for drift detection in business processes.

3 Stabilization Metrics for Model Drift Evaluation under Shocks

Shocks

We define a shock as a sudden, isolated event in the data-generating process or external conditions that causes an immediate and significant change in feature distributions. Shocks are so abrupt that the detailed temporal evolution of the data is not considered; instead, we focus on two states: pre-shock (baseline) and post-shock (shocked). Formally, a shock is any event for which the calculated Distribution Shift (DS) between these two states exceeds a fixed, domain-informed threshold :

| (1) |

where and denote categorical and numerical features, and and represent the total variation distance and Kolmogorov-Smirnov (KS) statistic computed between the baseline and shocked distributions of each feature lecam1960locally ; Feng2024 ; Kolmogorov1933 .

Stabilization Score (SS)

To quantify stability under drift, we introduce the Stabilization Score (SS), which calculates a model’s ability to preserve predictive performance in the presence of shocks:

| (2) |

Here, and denote the model’s performance on baseline and shocked data, respectively, and ensures numerical stability. The numerator captures raw performance degradation, while the denominator contextualizes this degradation by the magnitude of the shift itself. By normalizing performance degradation with DS, the SS provides a fair assessment of stability: a model that maintains performance despite a large shift receives a high score, whereas the same degradation under minimal shift indicates fragility. SS ranges from 0.5 to 1, with higher values indicating greater stability. Its monotonic and concave relationship with DS ensures interpretability and consistent comparison across varying shock intensities.

Stabilization Uplift (SU)

While SS calculates a single model’s stability, comparing two models requires accounting for both performance preservation and relative superiority. We define the Stabilization Uplift (SU) to quantify the net advantage of model B over A under drift. Each model is first assigned a stability weight, favoring those that preserve accuracy across baseline and shocked states (acting as an internal reliability score): . To capture relative superiority on shocked data (reflecting relative performance under stress), we define . To avoid overestimating temporary gains, a combined superiority weight also accounts for the original performance differences (tempering the superiority signal with baseline performance): . Finally, the adjusted weights are and , yielding the overall uplift:

| (3) |

Note that here, emphasizes B’s stability weight when its superiority signal is strong, while simultaneously attenuating A’s. This complementary scaling ensures that uplift reflects a zero-sum tradeoff: gains attributed to B are balanced by losses attributed to A, preventing both models from being rewarded simultaneously. Also, multiplying the stability and superiority terms ensures that a model is rewarded only when it is both internally stable and credibly superior; if either factor is weak, the uplift is naturally down-weighted.

Contextualizing the proposed metrics

Unlike conventional performance-based calculations that track predictive drops without accounting for drift magnitude or normalization, SS combines performance preservation with quantified distribution shifts into a normalized, monotonic metric. SU further extends this by comparing models across baseline and post-shock performance, capturing relative superiority and stability. Overall, the framework jointly accounts for drift magnitude, stability, and comparative stability, which are often overlooked by existing metrics. Additional mathematical details can be found in Appendix D.

4 Experimental Results

Next, we present our experimental results. We begin by describing the private datasets used in our work. Although the dataset cannot be open-sourced, we provide context about the financial data, which was obtained from private entities in Tajikistan, Uzbekistan, Kazakhstan, Jordan, and Azerbaijan. We find that many of the models we explore for these tabular datasets: CatBoost Dorogush2018CatBoost , TabPFN Hollmann2025 , FT-Transformer Gorishniy2021 , HGBoosting Pedregosa2011 , NGBoost Duan2020NGBoost , XGBoost Chen2016XGBoost , LightGBM Ke2017LightGBM , and TabNet Arik2019TabNet benefit (see Appendix E) from augmenting their training pipeline with outliers using zGAN.

4.1 Overview of Financial Datasets in Developing Economies

We study private credit-risk datasets from Tajikistan (), Uzbekistan (), Kazakhstan (), Jordan (), and Azerbaijan (). All tasks are binary default prediction with class imbalance (), and most datasets also include macro-financial covariates. Pre-/post- segments use OOT when shocks are evident: trade conflict for , armed conflicts for and , and OOS otherwise (, ). Calculated distribution shifts range from very small to substantial (). This setting is salient for GenAI in finance: models face exogenous shocks and heavy tails yet must remain reliable for risk decisions. See Appendix G for split types/dates, feature inventories, and per-feature statistics (missingness, mean, std dev, skewness, kurtosis).

4.2 Experimental Setup

We evaluate whether classification models can be stabilized under drift by augmenting training with synthetic data and, when stated, synthetic outliers. Data is partitioned via Out-of-Time (OOT) or Out-of-Sample (OOS) splits into pre-shock (train/test) and post-shock (shocked test) segments; shocks correspond to real events or simulated shifts. Pre-shock data use an 80/20 train–test split.

The baseline model (A-model) trains only on real pre-shock data; the stabilized model (B-model) uses a 50/50 mix of real and synthetic. For synthesis, real training data may be oversampled to examples to fit a zGAN, which then generates realistic samples and optional outliers from Gaussian light tails (). We evaluate performance using AUC (pre-shock) and AUC (post-shock) over 51 Monte Carlo splits and report medians and ranges.

Throughout the paper, we use a single global set of logistic slopes for SU, , as shown in Table 8; they are not tuned per dataset. From these results, we compute SS for each model; SU then quantifies the stability gain from synthetic data/outliers, enabling consistent assessment across datasets and shock scenarios.

4.3 Main Results

We report medians over 51 Monte Carlo splits for AUC and AUC and derive Stabilization Uplift (SU). Three qualitative trends are consistent:

(i) Synthetic variability helps most flexible models. TabPFN and FT-Transformer often achieve the highest SU under shift; boosted trees benefit selectively. (ii) Outlier share is non-monotonic. Moderate injections (5–10%) frequently maximize SU; very small or very large shares can attenuate gains. (iii) Gains scale with shift magnitude. Improvements are largest where DS is moderate/high (, ) and attenuated when DS is minimal (, ).

A compact digest appears in Table 1; exhaustive per-model/per-outlier grids are provided in Appendix E.

| Dataset (country) | DS | Best (model, outliers%) | |

| (Tajikistan) | 0.2250 | TabNet, w/o | 0.8441 |

| (Uzbekistan) | 0.0050 | TabPFN, 50 | 0.7449 |

| (Azerbaijan) | 0.1802 | TabPFN, 5 | 0.9981 |

| Open (Lending Club) | 0.1193 | FT-Transformer, 100 | 0.8884 |

Table 1 reports only the best stabilization effect among all 64 experiments per dataset: for , the top result was achieved with TabNet trained on real and synthetic data without outliers, while the next-highest Stabilization Uplift of 0.8126 came from TabPFN trained on real and synthetic data consisting entirely of outliers (, see Table 3). Although a few per-model best configurations occur without outliers, across all best results outlier-augmented training improves stability in of cases (10 of 12; see Appendix E).

5 Conclusion

In this work, we have shown that augmenting financial machine learning models with synthetic outliers can significantly improve their stability against sudden macroeconomic shocks. We addressed the critical challenge of poor model performance in volatile economies, particularly in Central Asia and the Caucasus. Our findings, based on an underexplored empirical setting, demonstrate that a deliberately data-centric approach can be effective. Across multiple models and financial datasets from Tajikistan, Uzbekistan, and other countries, we found that adding a small percentage of synthetic outliers generally leads to more stable performance. While the optimal amount of outliers is dataset- and model-dependent, the trend is clear: training on data that includes realistic extreme values makes models more resilient to real-world, unforeseen events. This proactive strategy contrasts with the common reactive approach of adjusting models only after drift occurs. Such resilience is particularly valuable in financial applications, where the cost of model failure can be substantial. A key limitation is the lack of a universal rule for selecting the best outlier percentage. Future work should therefore focus on developing heuristics that improve robustness on average without extensive manual tuning.

References

- [1] Fabian Hinder, Valerie Vaquet, and Barbara Hammer. One or two things we know about concept drift—a survey on monitoring in evolving environments. part b: locating and explaining concept drift. Frontiers in Artificial Intelligence, 7, 2024.

- [2] Ben Halstead, Yun Sing Koh, Patricia Riddle, Russel Pears, Mykola Pechenizkiy, Albert Bifet, Gustavo Olivares, and Guy Coulson. Analyzing and repairing concept drift adaptation in data stream classification. Machine Learning, 111(10):3489–3523, 2022.

- [3] Rosana Noronha Gemaque, Albert França Josuá Costa, Rafael Giusti, and Eulanda Miranda dos Santos. An overview of unsupervised drift detection methods. WIREs Data Mining and Knowledge Discovery, 10(6):e1381, 2020.

- [4] João Gama, Indrė Žliobaitė, Albert Bifet, Mykola Pechenizkiy, and Abdelhamid Bouchachia. A survey on concept drift adaptation. ACM Computing Surveys, 46(4), 2014.

- [5] Chun Wai Chiu and Leandro L. Minku. Smoclust: synthetic minority oversampling based on stream clustering for evolving data streams. Machine Learning, 113(7):4671–4721, 2024.

- [6] Alexander Kraus and Han van der Aa. Machine learning-based detection of concept drift in business processes. Process Science, 2(1):5, 2025.

- [7] Azizjon Azimi, Bonu Boboeva, Ilyas Varshavskiy, Shuhrat Khalilbekov, Akhlitdin Nizamitdinov, Najima Noyoftova, and Sergey Shulgin. zgan: An outlier-focused generative adversarial network for realistic synthetic data generation, 2024.

- [8] Indrė Žliobaitė. Learning under concept drift: an overview, 2010.

- [9] Alexey Tsymbal. The problem of concept drift: definitions and related work. In Computer Science Department, Trinity College Dublin, 2004.

- [10] Albert Bifet and Ricard Gavaldà. Learning from Time-Changing Data with Adaptive Windowing, pages 443–448. Proceedings of the 2007 SIAM International Conference on Data Mining (SDM), 2007.

- [11] Łukasz Korycki and Bartosz Krawczyk. Adversarial concept drift detection under poisoning attacks for robust data stream mining. Machine Learning, 112(10):4013–4048, June 2022.

- [12] Lingkai Yang, Jian Cheng, Yi Luo, Tianbai Zhou, and Xiaoyu Zhang. Detecting and rationalizing concept drift: A feature-level approach for understanding cause–effect relationships in dynamic environments. Expert Systems with Applications, 260:125365, 2025.

- [13] Benedikt Sonnleitner, Tom Madou, Matthias Deceuninck, Filotas Theodosiou, and Yves R. Sagaert. Evaluation of early student performance prediction given concept drift. Computers and Education: Artificial Intelligence, 8:100369, 2025.

- [14] Supriya Agrahari and Anil Kumar Singh. Comparison based analysis of window approach for concept drift detection and adaptation. Applied Intelligence, 55(1):39, 2025.

- [15] Prashanth B S, Manoj Kumar M V, Puneetha B H, and Ajay Kumara M A. A data-driven framework for detecting and mitigating concept drift in adaptive artificial neural networks. Procedia Computer Science, 258:1147–1158, 2025. International Conference on Machine Learning and Data Engineering.

- [16] Daniel Lukats, Oliver Zielinski, Axel Hahn, and Frederic Stahl. A benchmark and survey of fully unsupervised concept drift detectors on real-world data streams. International Journal of Data Science and Analytics, 19(1):1–31, 2025.

- [17] Bhagyashree Puranik, Bugra Can, and Yi Fan. Tabular out-of-distribution data synthesis for enhancing robustness. Amazon Science, 2024.

- [18] Lucien Le Cam. Locally asymptotically normal families of distributions. University of California Publications in Statistics, 3:37–98, 1960.

- [19] Weiming Feng, Liqiang Liu, and Tianren Liu. On deterministically approximating total variation distance. In Proceedings of the 2024 Annual ACM–SIAM Symposium on Discrete Algorithms (SODA), pages 1766–1791. SIAM, 2024.

- [20] A. Kolmogorov. Sulla determinazione empirica di una legge di distribuzione. Giornale dell’Istituto Italiano degli Attuari, 4(1):83–91, 1933.

- [21] Anna Veronika Dorogush, Vasily Ershov, and Andrey Gulin. Catboost: Unbiased boosting with categorical features, 2018.

- [22] Noah Hollmann, Samuel Müller, Lennart Purucker, Arjun Krishnakumar, Max Körfer, Shi Bin Hoo, Robin Tibor Schirrmeister, and Frank Hutter. Accurate predictions on small data with a tabular foundation model. Nature, 637(8045):319–326, 2025.

- [23] Yury Gorishniy, Ivan Rubachev, Valentin Khrulkov, and Artem Babenko. Revisiting deep learning models for tabular data. In NeurIPS 2021 Datasets and Benchmarks Track, 2021.

- [24] Fabian Pedregosa, Gaël Varoquaux, Alexandre Gramfort, Vincent Michel, Bertrand Thirion, Olivier Grisel, Mathieu Blondel, Peter Prettenhofer, Ron Weiss, Vincent Dubourg, Jake VanderPlas, Alexandre Passos, David Cournapeau, Matthieu Brucher, Matthieu Perrot, and Édouard Duchesnay. Scikit-learn: Machine learning in python. Journal of Machine Learning Research, 12:2825–2830, 2011.

- [25] Tony Duan, Anand Avati, Daisy Yi Ding, Daniel Nau, Saurabh Basu, Andrew Y. Ng, and Alec Schuler. Ngboost: Natural gradient boosting for probabilistic prediction. In Advances in Neural Information Processing Systems 33 (NeurIPS 2020), 2020.

- [26] Tianqi Chen and Carlos Guestrin. Xgboost: A scalable tree boosting system. In Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 785–794, 2016.

- [27] Guolin Ke, Qi Meng, Thomas Finley, Taifeng Wang, Wei Chen, Weidong Ma, Qiwei Ye, and Tie-Yan Liu. Lightgbm: A highly efficient gradient boosting decision tree. In Advances in Neural Information Processing Systems 30 (NeurIPS 2017), 2017.

- [28] Sercan Ö. Arik and Tomas Pfister. Tabnet: Attentive interpretable tabular learning. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 35, pages 6679–6687, 2021.

- [29] Ian Goodfellow et al. Generative adversarial nets. In NeurIPS, 2014.

- [30] Laurens de Haan and Ana Ferreira. Extreme Value Theory. Springer New York, 2006.

- [31] Diederik P Kingma and Max Welling. Auto-encoding variational bayes. ICLR, 2014.

- [32] Leland McInnes, John Healy, and James Melville. Umap: Uniform manifold approximation and projection for dimension reduction, 2020.

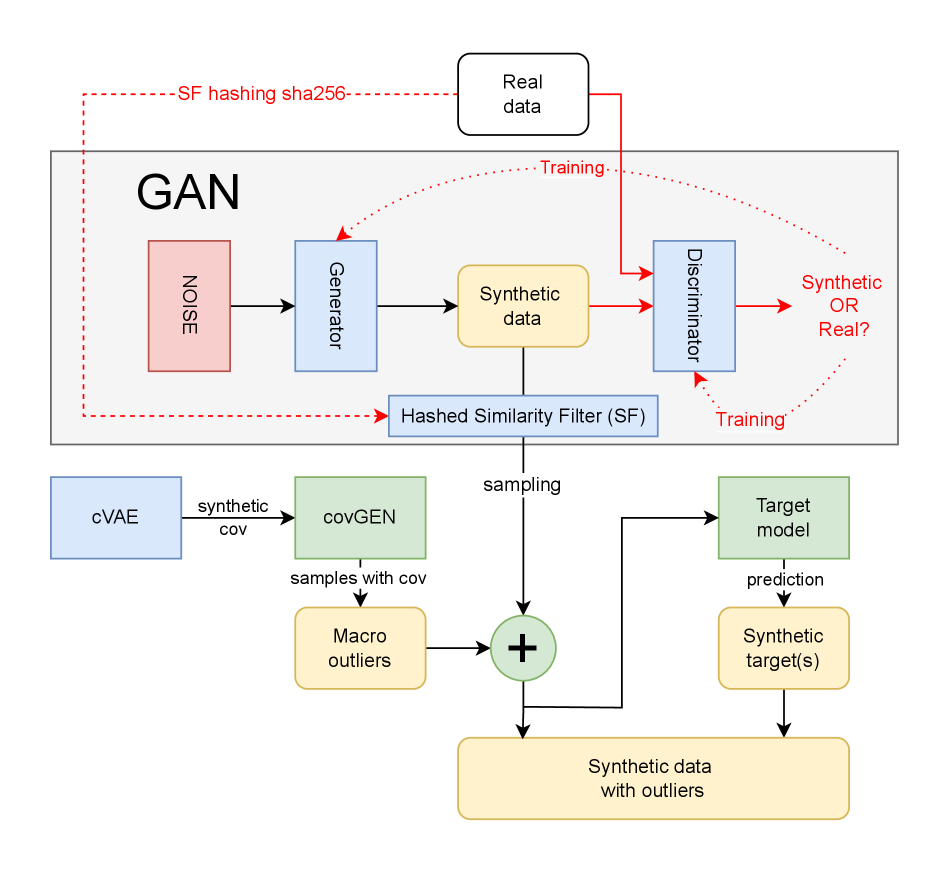

Appendix A Generative Model Description: zGAN

zGAN [7] is a generative adversarial network (GAN) [29] for realistic tabular synthesis with an explicit outlier mechanism. Beyond the standard generator-discriminator setup, zGAN adds components for controlled outlier generation and privacy protection.

Figure 1 illustrates the generalized structure of zGAN.

The key innovation is the Outliers Conditional Covariance Generator (covGEN) shown in Figure 1, which samples macro outliers from EVT 222Extreme Value Theory (EVT) [30] characterizes tail behavior and motivates sampling from heavy-tailed families (e.g., Gumbel, Weibull, Lévy) to emulate rare shocks; zGAN blends a controlled fraction of such samples (via covGEN) with typical synthetic data.-compatible multivariate families (normal, Laplace, Weibull, Gumbel, Lévy) using covariance matrices derived from real data or from a Conditional VAE (cVAE) [31].

The cVAE supplies covariances by minimizing reconstruction loss and KL divergence; generated outliers are then merged with base GAN samples. For privacy, zGAN applies a hash-based similarity filter [7] to avoid near-duplicates of real records, and for prediction tasks, a classification-style Target Model learns relationships across normal and extreme regions.

In this work, synthetic data refers to zGAN-generated records from typical (non-extreme) regions of the training distribution, while synthetic (macro) outliers are deliberately sampled tail points that mimic shocks. Baselines use only real pre-shock data; stabilized models use a mix of real + synthetic, optionally with a set share of outliers. This distinction matters because stability gains under shocks primarily come from exposure to plausible tails.

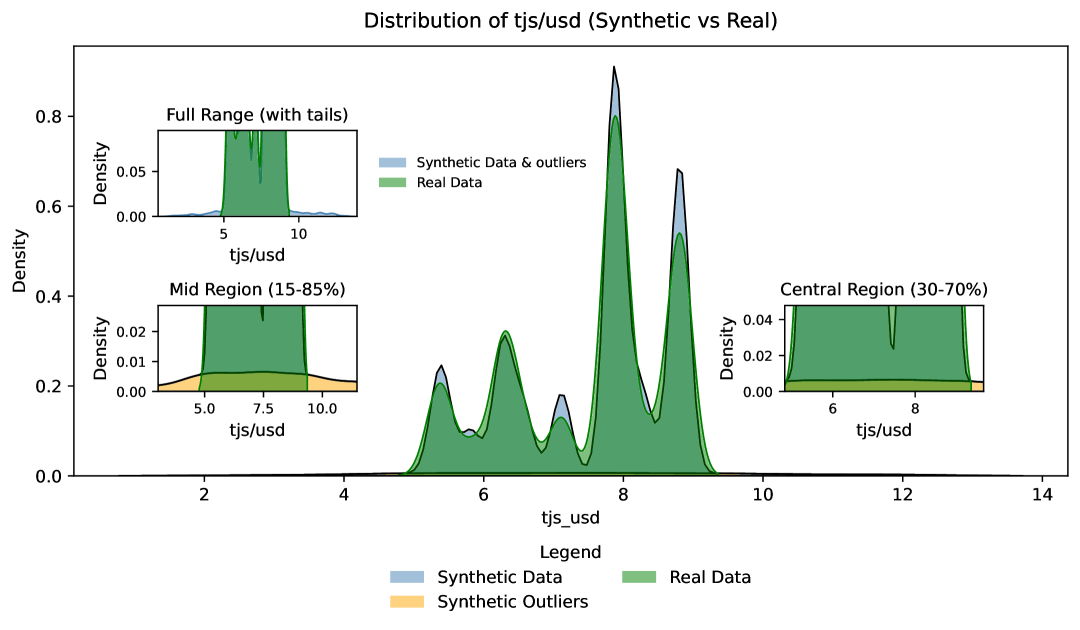

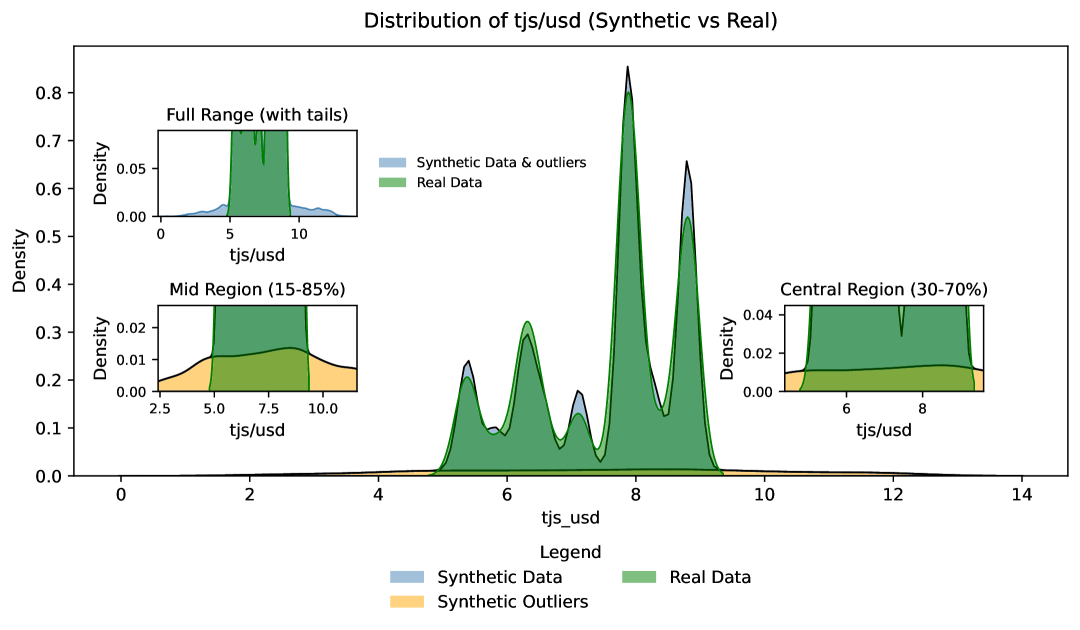

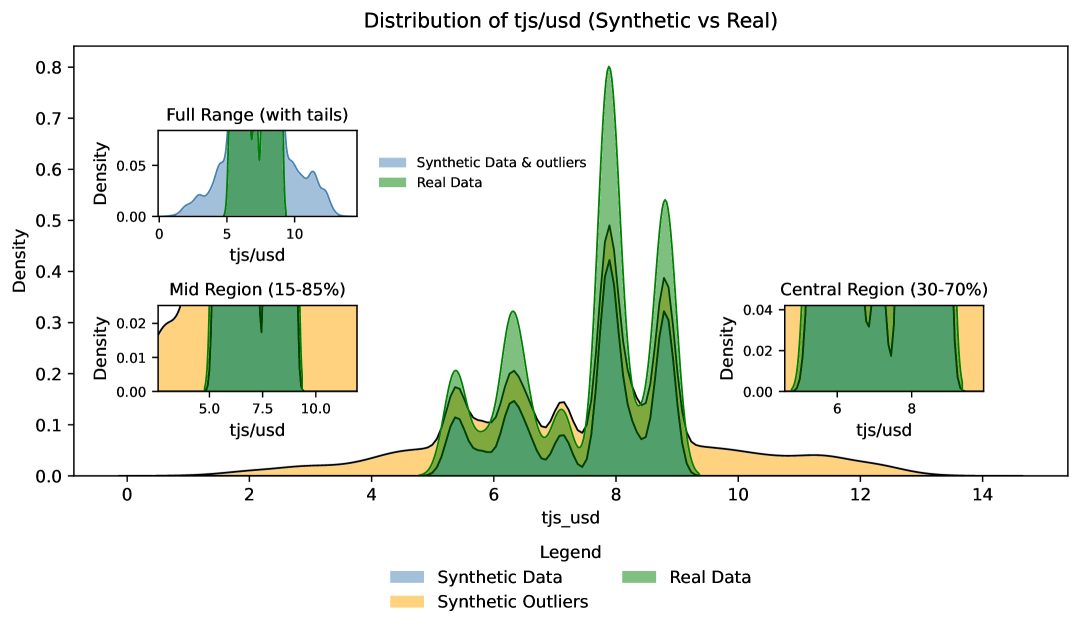

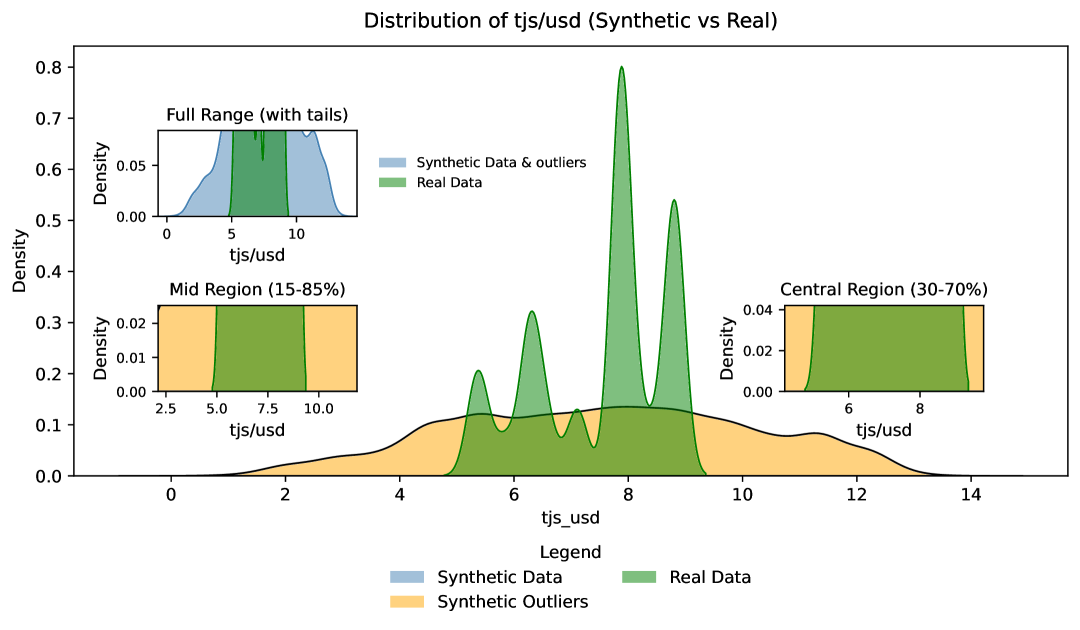

As an example of synthetic data and synthetic outliers, Figure 2 shows the distribution plots of the “tjs/usd” column (see Appendix G) from the Tajikistan dataset ().

(a) 5% outliers

(b) 10% outliers

(c) 50% outliers

(d) 100% outliers

Figure 2 shows the marginal distribution of the “tjs/usd” column from the Tajikistan dataset (). This column represents a macroeconomic indicator describing the exchange rate of the national currency of the Republic of Tajikistan (somoni) against the U.S. dollar. In each subfigure (a) – (d), the main plot includes zoomed-in insets: in the top-left inset, synthetic data with synthetic outliers are shown in blue, while the overlaid real data distribution is highlighted in green. The other two zoomed-in plots separately display the distribution of outliers, i.e., the tails, and the distribution of the main body of synthetic and real data.

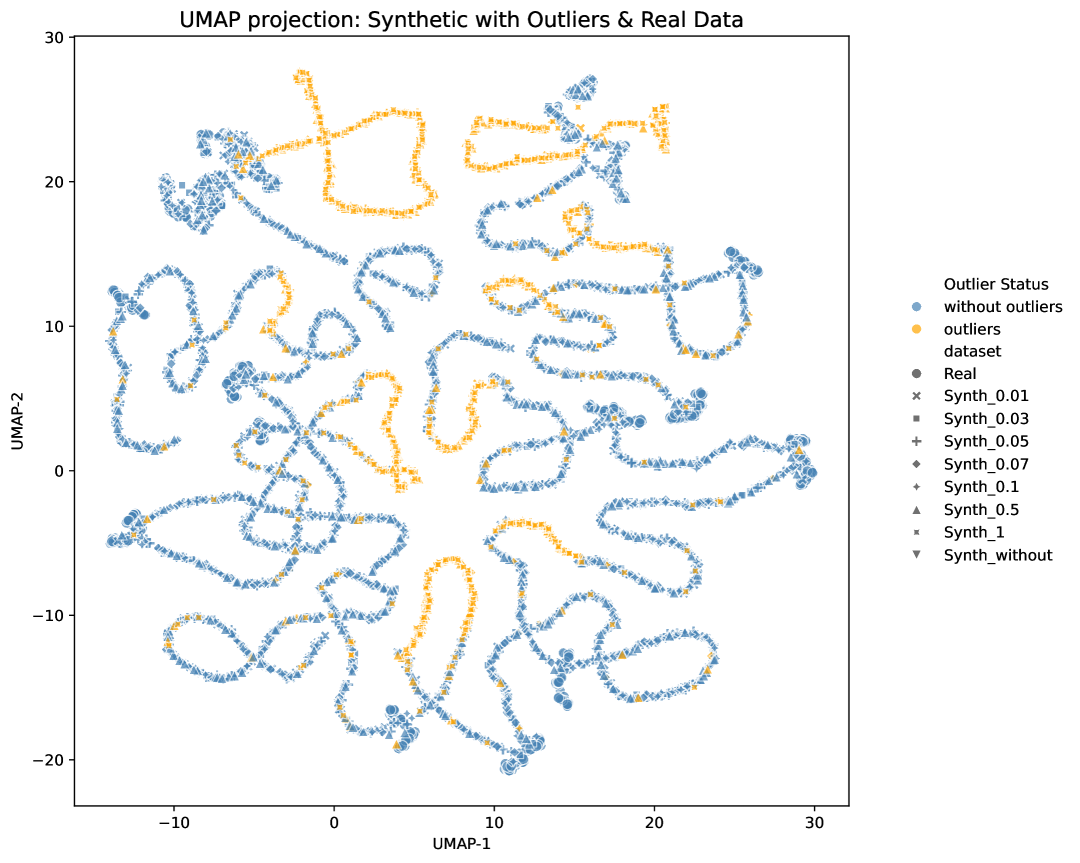

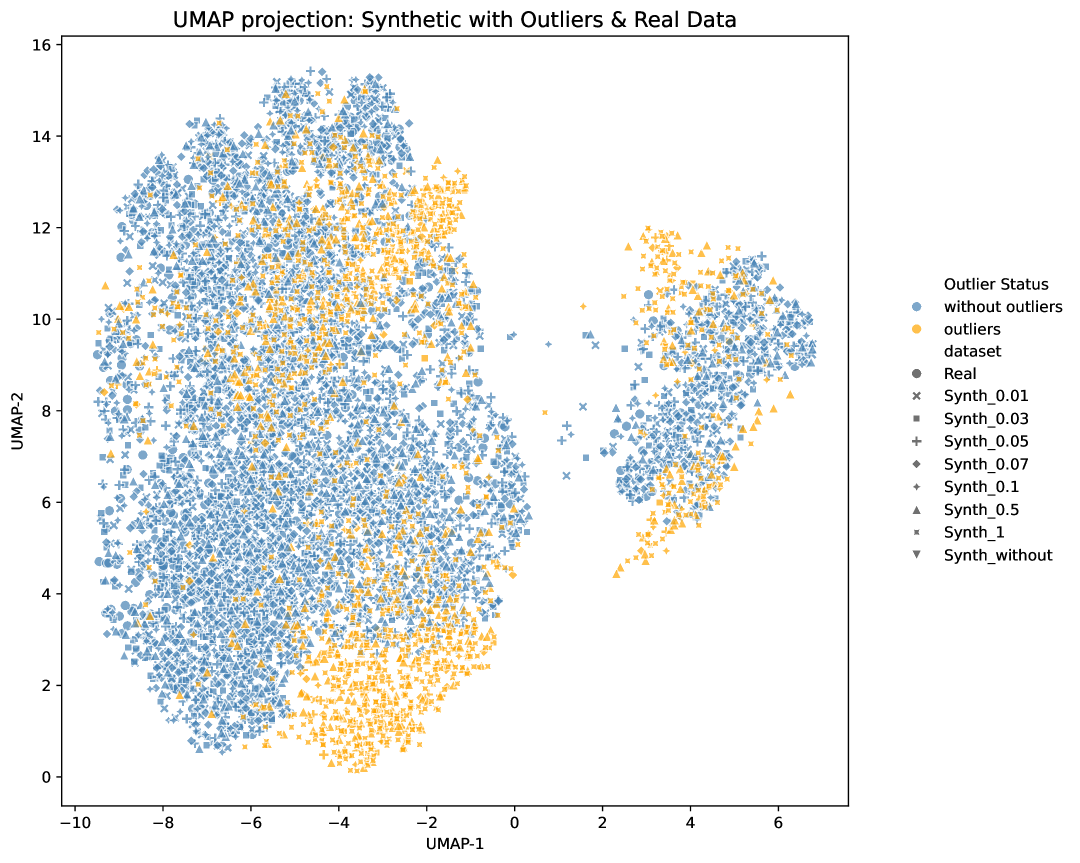

Figure 3 shows the Uniform Manifold Approximation and Projection (UMAP) [32] embeddings of the Tajikistan dataset ().

(a)

(b)

To construct the embeddings shown in Figure 3 (a) and (b), all generated synthetic datasets, with and without outliers, along with the real dataset, were combined into a single dataset. The merged Tajikistan dataset was then used to obtain the displayed embeddings.

The embedding variant shown in subfigure (a) differs from that in subfigure (b) solely in terms of preprocessing. The key distinction between the two preprocessing approaches lies in the feature composition and scaling: the first variant excludes categorical variables and does not apply normalization to numerical features, which may cause features with larger numeric ranges to dominate the UMAP space; the second variant retains all encoded categorical features and applies standardization to all variables, ensuring that each feature contributes equally to the dimensionality reduction results regardless of its original scale. Although subfigure (b) represents a more appropriate approach for algorithms sensitive to feature scaling, since the embedding is used purely for visual analysis, variant (a) is also applicable and appears more interpretable.

As shown in Figures 2 and 3, the outliers generated by zGAN are, in most cases, visually distinguishable from the synthetic data of the main distribution, while the synthetic data corresponding to the main distribution appear realistic, that is, they are barely distinguishable from the real data distribution. However, some outliers are still formed within the main distribution, which is particularly evident when a large number of outliers are present in the synthetic data, for instance, in the variant with outliers shown in Figure 2 (c).

The inclusion of some outliers within the main distribution is due to the post-processing of outliers performed by the covGEN module, see Figure 1. The post-processing step involves shifting negative outliers toward the center of the distribution, ensuring that the resulting outliers remain plausible within the logical constraints of the features. For example, the exchange rate of somoni to the U.S. dollar cannot take negative values.

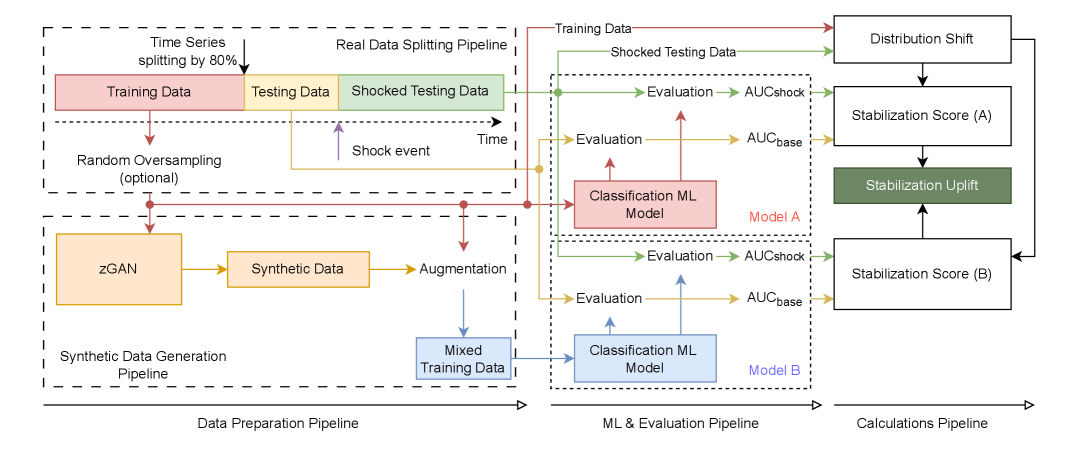

Appendix B Experimental Pipeline

The experimental pipeline consists of three main components: data preparation, ML modeling and evaluation, and the computation of the proposed quality metrics that characterize the stability of ML models under model drift conditions.

Figure 4 shows the experimental pipeline in the OOT setting with the identification of the shock portion.

The first stage of the experimental pipeline is data splitting, illustrated in the block “Real Data Splitting Schema” in Figure 4. The real data is partitioned according to the OOT principle into pre-shock data (Training and Testing) and post-shock data (Shocked Testing Data). The shock event is defined as the moment after which model drift is expected to occur, with concrete examples provided in Appendix C. The pre-shock data is further divided into training and testing sets in an 80/20 ratio using random sampling.

The resulting real data is used to train the A-model, which is evaluated using the metrics AUCbase, calculating performance in the pre-shock period, and AUCshock, calculating performance in the shock and post-shock periods.

To construct the B-model, which is assessed for stability against drift, the real training data is optionally upsampled to 10,000 samples through random resampling. These data are then used to train the zGAN model, which generates synthetic samples. The synthetic data is mixed with the original real data at a 50/50 ratio, and the combined dataset is used to train the B-model. The B-model is likewise evaluated using AUCbase and AUCshock.

To ensure the reliability of the final metrics, a Monte Carlo methodology is applied: each dataset is split into 51 subsets, on each of which a model is trained and evaluated. From the resulting 51 AUC values, the median and range are computed. The experimental methodology follows the approach described in [7].

Appendix C Shock Origins and Split Configuration

Table 2 summarizes, for each dataset, whether a concrete external shock was identified, the split type, the shock period, and the calculated Distribution Shift (DS).

| Dataset | Split | Shock Event | Shock Date |

Macro-financial

covariates |

DS |

| (Tajikistan) | OOT | Trade conflict | 2018-03-22 | 0.2250 | |

| (Uzbekistan) | OOS | 0.0050 | |||

| (Kazakhstan) | OOT | Armed conflict | 2021-12-30 | 0.1212 | |

| (Jordan) | OOS | 0.0026 | |||

| (Azerbaijan) | OOT | Armed conflict | 2021-12-30 | 0.1802 | |

| Open Data (LC) | OOT | Trade conflict | 2018-03-22 | 0.1193 |

It is important to note that the lowest Distribution Shift is observed when data is split using the OOS principle, as shown in Table 2. This indicates a low level of model drift, which is expected for data that is not affected by shock events.

Appendix D Algorithmic Description

To compute the Distribution Shift (1), we used tools from the SDV library designed for working with tabular data. The Metadata 333https://docs.sdv.dev/sdv/concepts/metadata method was used to automatically identify categorical and numerical column names, while the TVComplement 444https://docs.sdv.dev/sdmetrics/metrics/quality-metrics/tvcomplement and KSComplement 555https://docs.sdv.dev/sdmetrics/metrics/quality-metrics/kscomplement methods were used to calculate and , respectively. The pseudocode of the DS algorithm is shown in structure 1.

It is worth noting that the pseudocode in Algorithm 1 uses 1-TVComplement and similarly for KSComplement, since the metric implementations in the library are designed such that higher scores indicate better quality.

The transformation in Algorithm 2 is necessary to invert the model, allowing models with, for example, flipped labels to be treated as informative. This approach ensures that the SS remains within an intuitively interpretable range of values, from 0.5 to 1. For example, in cases with label noise or label permutation, one of the AUC values may approach zero while the other remains close to one. Under such conditions, SS could otherwise be incorrectly spread across the full range from 0 to 1.

The final Stabilization Uplift score (3) is computed according to the algorithm presented in Algorithm 3.

As shown in Algorithm 3, the final Stabilization Uplift score reflects the stability and quality of model B compared to the baseline model A under a distributional shift. Smooth logistic weights are used to quantify the degradation of model performance between the base and shock scenarios. These weights capture not only the individual stability of each model but also the relative advantage of model B over model A. An additional supervisory weight further amplifies the contribution of the more stable model. The final score is computed as a weighted difference between the stabilization scores of the two models, accounting for both performance dynamics and distributional change structure.

The problem of selecting the coefficients and is discussed in Appendix F.

The resulting algorithmic framework is used to compute the metrics in a classification task; the description and results of the conducted experiments are presented in the following chapter.

Appendix E Experimental Results

Stabilization Uplift Across Baselines and Outlier Levels

Tables 3–6 report the experimental results for datasets that include macro-variables, for which synthetic outliers were generated accordingly. Table 7 summarizes the results for datasets without macro-variables, where stabilization experiments with synthetic outliers were not conducted, and only experiments with synthetic data without outliers were performed.

| Outliers, % | CatBoost | TabPFN | FT-Transformer | HGBoosting | NGBoost | XGBoost | LightGBM | TabNet |

| without | 0.2667 | 0.8093 | 0.0000 | 0.6363 | 0.0916 | 0.0000 | 0.0000 | 0.8441 |

| 1 | 0.0572 | 0.6319 | 0.0000 | 0.7106 | 0.1128 | 0.0000 | 0.0000 | 0.6258 |

| 3 | 0.0000 | 0.5281 | 0.0000 | 0.5442 | 0.1380 | 0.0000 | 0.0000 | 0.2737 |

| 5 | 0.0000 | 0.2542 | 0.0000 | 0.6764 | 0.0349 | 0.0000 | 0.0000 | 0.3266 |

| 7 | 0.0000 | 0.6951 | 0.0000 | 0.6079 | 0.1830 | 0.0000 | 0.0000 | 0.6171 |

| 10 | 0.0534 | 0.6703 | 0.0000 | 0.7266 | 0.5459 | 0.2362 | 0.1237 | 0.0000 |

| 50 | 0.0000 | 0.4705 | 0.0000 | 0.4760 | 0.0000 | 0.0000 | 0.0000 | 0.7257 |

| 100 | 0.0105 | 0.8126 | 0.0000 | 0.6905 | 0.4744 | 0.0000 | 0.0000 | 0.4562 |

| Outliers, % | CatBoost | TabPFN | FT-Transformer | HGBoosting | NGBoost | XGBoost | LightGBM | TabNet |

| without | 0.2667 | 0.4103 | 0.0109 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0002 |

| 1 | 0.0000 | 0.3061 | 0.0246 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| 3 | 0.0000 | 0.4888 | 0.0266 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| 5 | 0.0086 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| 7 | 0.0000 | 0.3259 | 0.0258 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| 10 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| 50 | 0.0000 | 0.7449 | 0.0220 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| 100 | 0.0000 | 0.4795 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0087 |

| Outliers, % | CatBoost | TabPFN | FT-Transformer | HGBoosting | NGBoost | XGBoost | LightGBM | TabNet |

| without | 0.1874 | 0.9827 | 0.9406 | 0.0000 | 0.0001 | 0.1859 | 0.6697 | 0.0000 |

| 1 | 0.6018 | 0.9863 | 0.9470 | 0.0000 | 0.0058 | 0.044 | 0.4001 | 0.0000 |

| 3 | 0.0150 | 0.9818 | 0.3784 | 0.5642 | 0.0207 | 0.0653 | 0.2549 | 0.0000 |

| 5 | 0.1272 | 0.9981 | 0.9163 | 0.0000 | 0.0015 | 0.1325 | 0.6295 | 0.0000 |

| 7 | 0.0786 | 0.9952 | 0.9460 | 0.0000 | 0.0032 | 0.3271 | 0.9196 | 0.0000 |

| 10 | 0.0037 | 0.9962 | 0.9555 | 0.7394 | 0.0164 | 0.1681 | 0.7486 | 0.0000 |

| 50 | 0.3238 | 0.9928 | 0.9447 | 0.0000 | 0.0000 | 0.0408 | 0.3750 | 0.9139 |

| 100 | 0.7496 | 0.9906 | 0.9540 | 0.1365 | 0.0143 | 0.1601 | 0.6879 | 0.0000 |

| Outliers, % | CatBoost | TabPFN | FT-Transformer | HGBoosting | NGBoost | XGBoost | LightGBM | TabNet |

| without | 0.0000 | 0.0000 | 0.6971 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0131 |

| 1 | 0.1680 | 0.0583 | 0.8861 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| 3 | 0.0578 | 0.0000 | 0.6198 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.2880 |

| 5 | 0.0000 | 0.0000 | 0.1671 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| 7 | 0.0000 | 0.0000 | 0.7289 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.4809 |

| 10 | 0.0000 | 0.0000 | 0.7896 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.1820 |

| 50 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0010 |

| 100 | 0.0000 | 0.0000 | 0.8884 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.6237 |

| Datasets | CatBoost | TabPFN | FT-Transformer | HGBoosting | NGBoost | XGBoost | LightGBM | TabNet |

| Kazakhstan () | 0.3526 | 0.8343 | 0.4758 | 0.0000 | 0.0000 | 0.0220 | 0.0164 | 0.0002 |

| Jordan () | 0.0251 | 0.0000 | 0.0544 | 0.5704 | 0.2881 | 0.0000 | 0.0000 | 0.3496 |

Across model–dataset pairs, adding a non-zero share of synthetic outliers improves stability in 135 out of 256 cases, corresponding to approximately , as shown in Tables 3–6.

For HGBoosting, NGBoost, XGBoost, and LightGBM, stabilization uplift is achieved in of cases, i.e., for 2 out of 4 datasets with macro-variables, when an additional share of synthetic outliers is introduced. For FT-Transformer, stabilization uplift is observed in of cases, and for CatBoost, TabPFN, and TabNet it is observed in of cases.

Across model–dataset pairs, adding a non-zero share of synthetic outliers improves stability in the vast majority of cases. Notable patterns are:

-

1.

flexible architectures (TabPFN, FT-Transformer) benefit most;

-

2.

the optimal outlier share is non-monotonic and typically small (5–10%);

-

3.

gains correlate with DS magnitude (largest for /, attenuated for low-DS /).

While a few best single configurations occur without outliers (e.g., TabNet on ), counting across all baselines shows more models improve with outliers than without, aligning with our conclusion that deliberate tail exposure enhances post-shock stability.

The Stabilization Uplift (3) metric takes a zero or near-zero value when stabilization methods fail to improve stability, i.e., when model B exhibits a larger difference between and compared to model A. If the applied stabilization method leads to a decrease in relative to ; that is, if the model’s performance after stabilization deteriorates compared to the non-stabilized model, then Stabilization Uplift decreases logistically according to the sigmoid steepness parameter , as shown in Algorithm 3. This approach to stability computation reflects the principle that the value of stability gains diminishes when model quality degrades as a result of applying stabilization methods.

This formulation also explains why the outcomes vary across the four datasets. On datasets with pronounced shocks and higher feature variability, models tend to stabilize when synthetic outliers are introduced, whereas on datasets with weaker shifts or more rigid feature structures, stabilization effects may be negligible or even detrimental. At the same time, architectural flexibility plays a critical role: highly expressive models (e.g., TabPFN, FT-Transformer) can adapt to tail augmentation and convert outliers into useful signal, while tree-based ensembles or boosting methods may fail to leverage the additional variability. Consequently, some models exhibit consistent stability gains, while others remain unaffected or even degrade, illustrating the joint influence of dataset characteristics and model architecture on stabilization outcomes.

Stabilization Uplift and AUC Components

For the open dataset available in the project’s GitHub repository, complete tables with all intermediate results and metrics are provided. The reported AUC values can be used to demonstrate how they relate to the final Stabilization Uplift metric, helping to better understand the behavior of this metric.

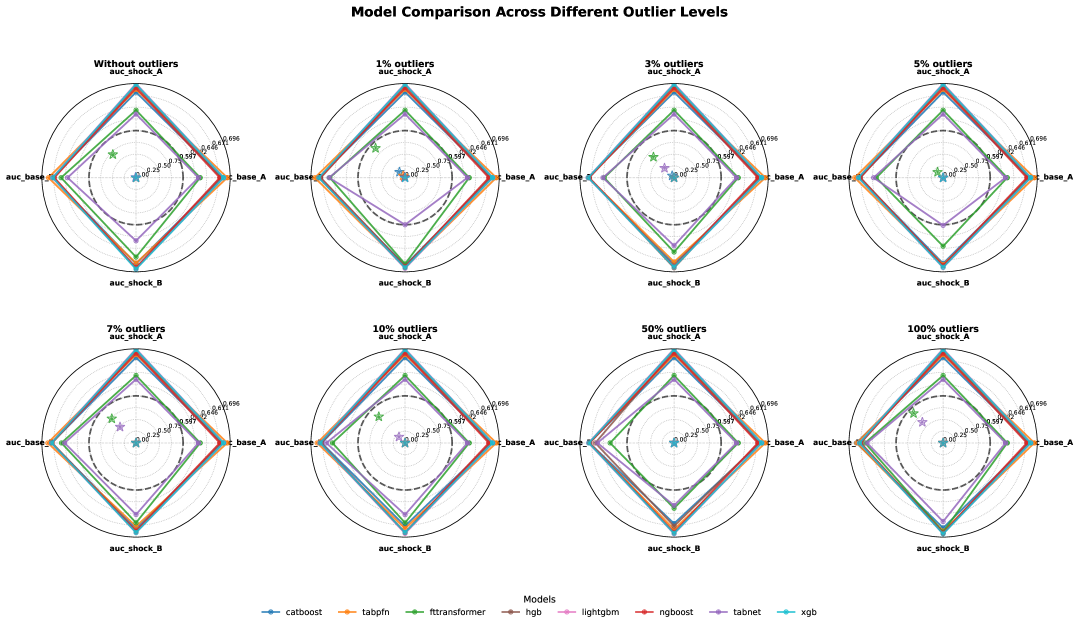

In Figure 5, radial plots illustrate the values of AUC and Stabilization Uplift for each baseline model and for different proportions of outliers in the synthetic data.

In Figure 5, each radial plot is constructed for the AUC and SU metric values corresponding to a specific proportion of outliers in the synthetic data, with different colors representing individual baselines. On the outer ring, points connected by lines indicate the AUC values, while on the inner ring, asterisks mark the SU metric values.

The plots reveal a competition in SU values between the FT-Transformer and TabNet models, with the former generally outperforming the latter. Examining the AUC values, for instance at outliers, shows that the AUCs are largely comparable. However, the FT-Transformer exhibits a slight increase in relative to TabNet, along with a somewhat larger increase in , such that for both models . This AUC configuration represents a scenario where synthetic data stabilized the model, leading to a performance gain, while the pre-shock model shows a slightly smaller improvement compared to the post-shock AUC. In this case, each model receives an SU value roughly proportional to the AUC gain of model B relative to model A and the difference between post-shock and pre-shock AUC.

In the second case, at outliers, TabNet exhibits a larger pre-shock AUC gain relative to post-shock, meaning that the quality improvement from synthetic data with outliers primarily benefited the model less affected by the shock. Here, SU penalizes the model, resulting in a lower SU compared to FT-Transformer, since the synthetic outlier data substantially prepared the latter for the shock.

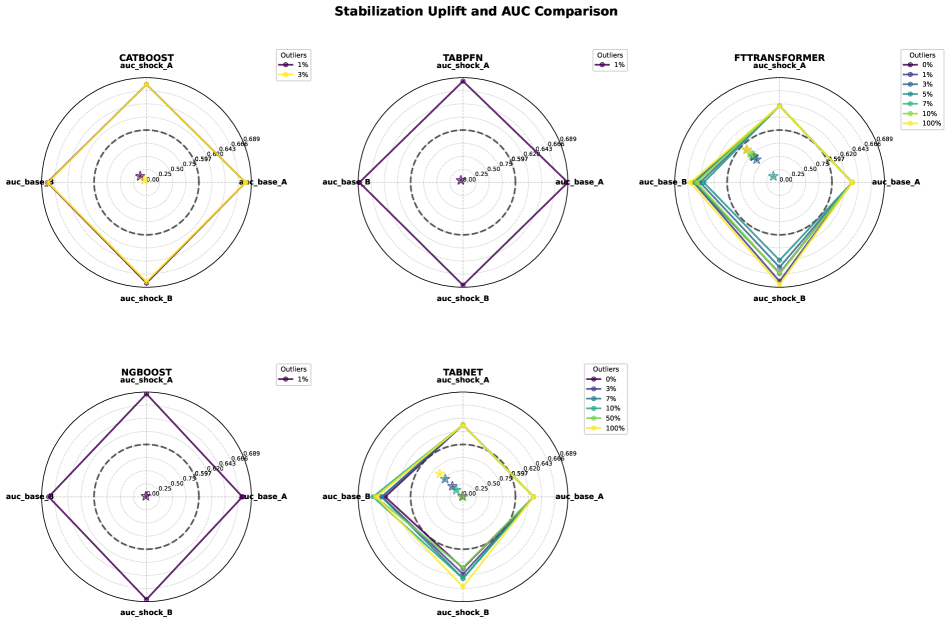

To observe the behavior of the SU metric in relation to AUC at different outlier percentages in the synthetic data, radial plots were constructed for each ML model, as shown in Figure 6. These plots exclude zero Stabilization Uplift values.

A visual analysis of Figure 6 reveals the underlying logic of the Stabilization Uplift metric. Specifically, higher SU values are assigned when an ML model achieves superior performance on the post-shock test depending on the outlier proportion, given an overall advantage of model B over model A. This takes into account the distance between the models’ Stabilization Scores (2), as illustrated, for example, by FT-Transformer and TabNet.

Appendix F On the Selection of Optimal and Quasi-Optimal Coefficients

The selection of optimal coefficients for formula (3) may involve several conditions important for the interpretability, fairness, and optimizability of the metric (in the case of its use as a loss function).

The interpretability of the metric can be verified using expert evaluations. For such a case, a table of expert assessments should be constructed, consisting of the shock and baseline AUC values for models A and B, as well as the DS (1) values, and the expert evaluations of SU themselves. In the general case, the problem can be described by the following expression:

| (4) |

where are the coefficients; — the number of data points (e.g., DS values or input–output pairs for SU); is the confidence weight reflecting the reliability or importance of the i-th expert assessment; is a loss function (e.g., or Huber), ; is a regularizer (e.g., ), and .

The expert-aligned, interpretable coefficients are then defined by:

| (5) |

with computed per (2)–(3) using the -th row of the expert table.

The fairness of the SU metric can be considered with respect to the DS metric. It is important that, for the chosen coefficients, the SU metric preserves its logarithmic growth with respect to changes in DS. The original objective function (4) is extended by incorporating expert annotations and introducing a reference logarithmic form as part of the regularization, resulting in the following problem formulation:

| (6) |

where is the vector of model parameters to be optimized, is the feasible set of parameters defined by hard constraints (monotonicity, concavity, slope bound, etc.); — the combined regularization term: — penalty for deviation from the reference logarithmic form ; — total variation smoothing to suppress abrupt jumps; — curvature penalty to reduce local bends in the curve.

Under the constraints of SU matching expert assessments and preserving the logarithmic form (6), stability of ML models can also be considered, which corresponds to the second fairness task, formulated as follows:

| (7) |

where is the vector of model parameters to optimize, is the feasible set defined by hard constraints (monotonicity, concavity, slope bound, etc.), are the parameters of the reference logarithmic form , and is the combined regularization term: — penalty for deviation from the reference log-form, — total variation smoothing to suppress abrupt jumps, — curvature penalty to reduce local bends, — stability penalty ensuring SU remains stable within an -range of variations of model AUC, i.e.,

If the Stabilization Uplift (SU) is used as a loss function, its theoretical optimizability can be established under standard assumptions. Let the parameter vector be restricted to the compact set

where are expert-chosen upper bounds ensuring positive and bounded coefficients, which in turn guarantee monotone and interpretable responses of the SU to variations in AUC. Let the total objective function be

where calculates the discrepancy between predicted and target SU values, and is a continuous regularization term including penalties for deviation from the reference logarithmic form, total variation, curvature, and stability with respect to -level variations in model AUC. Under the assumption that is continuous on the compact set , the Weierstrass extreme value theorem ensures the existence of at least one optimal parameter vector that minimizes . Therefore, by enforcing compactness of the parameter set and continuity of the objective and regularization terms, the SU is theoretically well-defined as a loss function and the corresponding optimization problem is guaranteed to be solvable in principle.

The search for optimal coefficients assumes the availability of a complete set of expert evaluations, AUC variants, and DS metric values. In practice, this is difficult to achieve; therefore, in real-world tasks, it is possible to search for quasi-optimal coefficients by having experts specify, for example, three SU points equal to 0, 0.5, and 1, followed by performing optimization computations. In this work 3, the selection of coefficient values was carried out using a quasi-optimal approach.

The coefficients obtained as a result of the quasi-optimal search are presented in Table 8.

| Scope | |||

| All datasets / all models (default) | 100 | 1000 | 1000 |

A single global set of was used for all datasets and models, without per-dataset tuning. The values were determined once using the quasi-optimal procedure described above under monotonicity and concavity constraints, and are presented in Table 8. A coarse sensitivity sweep with , , and confirmed that all qualitative conclusions remain unchanged. Reported scores correspond to the median values over 51 Monte Carlo splits.

Appendix G Specialized Datasets for Developing Economies

We provide additional details regarding our private datasets.

| Feature | Dtype | Description |

| age | int64 | Age of the client |

| gender | int64 | Gender of the client |

| amount_smn | float64 | Loan amount |

| duration | float64 | Duration of loan |

| int_rate | float64 | Interest rate |

| credit_history_count | int64 | Number of loans previously taken loans |

| dependants | float64 | Number of dependants in family |

| mon_remit | float64 | Monthly remittance (Macro variable) |

| mon_payment | float64 | Monthly payment |

| int_amount | float64 | Calculated interest amount |

| usd_rate | float64 | USD/Somoni rate (Macro variable) |

| alum_price | float64 | Aluminium price (Macro variable) |

| oil_price | float64 | Oil price (Macro variable) |

| cotton_price | float64 | Cotton price (Macro variable) |

| tjs_usd | float64 | Somoni/USD rate (Macro variable) |

| is_bad60 | int64 | Target variable (Bad/Good loan) |

| Feature | Dtype | Missing | Unique | Mean | Std | Skewness | Kurtosis | Min | 25% | Median | 75% | Max | IQR |

| age | int64 | 0 | 63 | 41.5845 | 11.8583 | 0.2574 | -0.8968 | 18 | 32 | 41 | 51 | 80 | 19 |

| gender | int64 | 0 | 2 | 0.6250 | 0.4841 | -0.5162 | -1.7335 | 0 | 0 | 1 | 1 | 1 | 1 |

| amount_smn | float64 | 0 | 1699 | 5249.441 | 3897.815 | 1.7069 | 4.2671 | 23.6 | 2500 | 4000 | 7000 | 30000 | 4500 |

| duration | float64 | 0 | 67 | 14.0019 | 4.4964 | 2.2536 | 19.0871 | 1 | 12 | 12 | 18 | 120 | 6 |

| int_rate | float64 | 0 | 39 | 0.3619 | 0.0410 | -1.1243 | 4.1508 | 0 | 0.34 | 0.36 | 0.40 | 0.47 | 0.06 |

| credit_history_count | int64 | 0 | 84 | 2.5480 | 2.7751 | 7.7530 | 127.332 | 1 | 1 | 2 | 3 | 84 | 2 |

| dependants | float64 | 0 | 18 | 5.2107 | 1.9663 | 1.1464 | 3.0468 | 0 | 4 | 5 | 6 | 17 | 2 |

| mon_remit | float64 | 0 | 26 | 1.94e+08 | 5.23e+07 | -0.0198 | -0.9197 | 9.50e+07 | 1.65e+08 | 1.81e+08 | 2.20e+08 | 2.77e+08 | 5.51e+07 |

| mon_payment | float64 | 0 | 12648 | 471.9793 | 375.2203 | 5.7272 | 120.661 | 4.6 | 249.91 | 379.09 | 577.58 | 15525 | 327.67 |

| int_amount | float64 | 0 | 12548 | 1359.216 | 1292.326 | 2.4415 | 10.2900 | 0 | 513.92 | 967.96 | 1729.66 | 29815.2 | 1215.74 |

| usd_rate | float64 | 0 | 71 | 7.7318 | 1.0970 | -0.5810 | -0.9108 | 5.5209 | 6.6207 | 7.8759 | 8.8050 | 11.405 | 2.1843 |

| alum_price | float64 | 0 | 77 | 1815.195 | 238.2081 | 0.3474 | -0.9940 | 1459.93 | 1592.36 | 1804.04 | 2030.01 | 2446.65 | 437.65 |

| oil_price | float64 | 0 | 77 | 51.4332 | 9.5819 | 0.0242 | -0.0631 | 21.04 | 45.69 | 50.90 | 57.54 | 76.73 | 11.85 |

| cotton_price | float64 | 0 | 75 | 78.2416 | 8.3149 | 0.2463 | -1.1698 | 63.53 | 70.28 | 78.92 | 85.16 | 97.71 | 14.88 |

| tjs_usd | float64 | 0 | 67 | 7.6490 | 1.1358 | -0.6587 | -0.7294 | 5.3074 | 6.6207 | 7.8719 | 8.8038 | 11.32 | 2.1831 |

| is_bad60 | int64 | 0 | 2 | 0.0664 | 0.2490 | 3.4824 | 10.1273 | 0 | 0 | 0 | 0 | 1 | 0 |

| Feature | Dtype | Missing | Unique | Freq | Percent Top |

| sector | object | 0 | 6 | 142172 | 40.97% |

| education | object | 0 | 5 | 206582 | 59.53% |

| marital_status | object | 0 | 5 | 278051 | 80.12% |

| district | object | 0 | 36 | 46681 | 13.45% |

| Feature | Dtype | Description |

| gender | int64 | Client’s gender |

| monthly_payment | float64 | Loan monthly payment |

| contract_amount | float64 | Previous loan contract amount |

| item_amount | float64 | Amount of loan items |

| age | int64 | Client’s age |

| ltv | float64 | Loan to value ratio |

| contract_duration | int64 | Duration of loan |

| Interest Rate | int64 | Yearly interest rate |

| Balance of Trade | float64 | Balance of trade (macro variable) |

| Inflation Rate | float64 | Inflation rate (macro variable) |

| Current Account | float64 | Current client’s loans |

| Remittances | float64 | Remittances (macro variable) |

| usd_uzs | float64 | USD/UZS rate |

| rub_uzs | float64 | RUB/UZS rate |

| target | int64 | Target variable |

| Feature | Dtype | Missing | Unique | Mean | Std | Skewness | Kurtosis | Min | 25% | Median | 75% | Max | IQR |

| gender | int64 | 0 | 2 | 0.6001 | 0.4899 | -0.4087 | -1.8330 | 0 | 0 | 1 | 1 | 1 | 1 |

| monthly_payment | float64 | 0 | 12144 | 425133.4 | 263025.7 | 1.9526 | 5.4135 | 83333 | 255267 | 354000 | 522100 | 2577855 | 266833 |

| contract_amount | float64 | 0 | 12183 | 5032402 | 3098996 | 1.9644 | 5.5727 | 1000000 | 3036000 | 4195200 | 6182400 | 30934265 | 3146400 |

| item_amount | float64 | 0 | 5508 | 3747260 | 19730909 | 179.4820 | 32655.73 | 100000 | 2142000 | 3240000 | 4609000 | 3.59e+09 | 2467000 |

| age | int64 | 0 | 57 | 36.6165 | 9.4628 | 0.5756 | -0.3888 | 19 | 29 | 35 | 43 | 75 | 14 |

| ltv | float64 | 0 | 11665 | 2.3912 | 5.6335 | 9.8632 | 138.227 | 0.0015 | 1 | 1 | 1.5194 | 156.0924 | 0.5194 |

| contract_duration | int64 | 0 | 4 | 11.8973 | 0.7849 | -8.3539 | 73.5403 | 3 | 12 | 12 | 12 | 12 | 0 |

| Interest Rate | int64 | 0 | 4 | 14.9967 | 1.2978 | 0.7503 | -1.2519 | 14 | 14 | 14 | 17 | 17 | 3 |

| Balance of Trade | float64 | 0 | 17 | -873.39 | 648.5264 | 1.3614 | 1.3750 | -1826.6 | -1172.8 | -1072 | -798 | 763.2 | 374.8 |

| Inflation Rate | float64 | 0 | 12 | 10.9321 | 0.6566 | 1.0281 | 0.1271 | 10 | 10.5 | 10.8 | 11.1 | 12.3 | 0.6 |

| Current Account | float64 | 5989 | 5 | -1351.52 | 468.5964 | 1.4784 | 4.7791 | -1869.2 | -1869.2 | -1203.63 | -1203.63 | 453.07 | 665.57 |

| Remittances | float64 | 5989 | 5 | 2062.969 | 615.3457 | 2.7211 | 10.2272 | 1403.43 | 1884.28 | 1884.28 | 2390.8 | 4801.91 | 506.52 |

| usd_uzs | float64 | 0 | 413 | 10867.16 | 266.6989 | 0.9254 | -0.3744 | 10527.73 | 10666.01 | 10752.86 | 11030.51 | 11539.65 | 364.49 |

| rub_uzs | float64 | 0 | 412 | 149.4125 | 21.6284 | -0.6057 | 2.1259 | 76.3182 | 144.2943 | 146.5607 | 154.0946 | 206.7358 | 9.80 |

| target | int64 | 0 | 2 | 0.0777 | 0.2676 | 3.1561 | 7.9607 | 0 | 0 | 0 | 0 | 1 | 0 |

| Feature | Dtype | Missing | Unique | Freq | Percent Top |

| category | object | 0 | 20 | 12273 | 36.56% |

| region | object | 0 | 12 | 13266 | 39.52% |

| partner_id_top30 | object | 0 | 31 | 7981 | 23.77% |

| partner_filtered_15 | object | 0 | 16 | 20027 | 59.66% |

| Feature | Dtype | Missing | Description |

| flag_fin | int64 | 0 | |

| BAD | float64 | 0 | Target variable |

| credit_amount | float64 | 0 | Loan amount |

| LOAN_AMOUNT | float64 | 0 | Loan amount |

| DURATION | float64 | 0 | Loan duration |

| Gender | float64 | 0 | Client’s gender |

| AGE | int64 | 0 | Client’s age |

| credit_history_count | float64 | 16270 | Credit history count |

| OCCUPATION | float64 | 4769 | Client’s occupation |

| NUMBEROFCHILDREN | float64 | 254141 | Number of client’s children |

| BUDGETTOTALINCOME | float64 | 19 | Total income budget |

| GCVPSAL | float64 | 15635 | |

| hasCar | float64 | 4818 | Has client a car |

| has_house | float64 | 16392 | Has client a house |

| cumulative_dpd | float64 | 16511 | Cumulative due date |

| max_dpd | float64 | 16511 | Maximum due date |

| MOBILEPHONE | float64 | 3 | Has client a mobile phone |

| repeated_client | int64 | 0 | Is client a repeated client |

| Feature | Dtype | Missing | Unique | Mean | Std | Skewness | Kurtosis | Min | 25% | Median | 75% | Max | IQR |

| flag_fin | int64 | 0 | 1 | 1.0000 | 0.0000 | 1 | 1 | 1 | 1 | 1 | 0 | ||

| BAD | float64 | 0 | 2 | 0.0249 | 0.1558 | 6.1003 | 35.2139 | 0 | 0 | 0 | 0 | 1 | 0 |

| credit_amount | float64 | 0 | 87821 | 205889.9 | 170044.5 | 2.0781 | 6.4357 | 7495 | 89990 | 151980 | 262000 | 2000000 | 172010 |

| LOAN_AMOUNT | float64 | 0 | 115643 | 211923.9 | 172667.9 | 2.0275 | 6.0728 | 7495 | 94092 | 158125 | 270827 | 2000000 | 176735 |

| DURATION | float64 | 0 | 36 | 17.0035 | 13.1665 | 1.1281 | 0.3989 | 3 | 6 | 12 | 24 | 60 | 18 |

| Gender | float64 | 0 | 2 | 1.5861 | 0.4925 | -0.3496 | -1.8778 | 1 | 1 | 2 | 2 | 2 | 1 |

| AGE | int64 | 0 | 57 | 41.6174 | 12.7692 | 0.4234 | -0.7103 | 18 | 31 | 40 | 51 | 74 | 20 |

| credit_history_count | float64 | 16270 | 242 | 12.7823 | 38.1648 | 14.8352 | 442.1289 | 1 | 4 | 7 | 12 | 3000 | 8 |

| OCCUPATION | float64 | 4769 | 28 | 15.1335 | 6.8169 | 1.0544 | 0.0771 | 1 | 12 | 13 | 19 | 31 | 7 |

| NUMBEROFCHILDREN | float64 | 254141 | 12 | 0.4259 | 0.8538 | 2.5050 | 8.2227 | 0 | 0 | 0 | 1 | 15 | 1 |

| BUDGETTOTALINCOME | float64 | 19 | 74661 | 352058.8 | 529282.0 | 259.0210 | 100499.8 | 3960 | 195000 | 290000 | 429000 | 2.25e+08 | 234000 |

| GCVPSAL | float64 | 15635 | 86002 | 160984.1 | 188293.5 | 4.7613 | 75.8838 | -9990 | 55000 | 110548.5 | 201050 | 1.10e+07 | 146050 |

| hasCar | float64 | 4818 | 26 | 0.3202 | 0.6825 | 5.3495 | 137.7587 | 0 | 0 | 0 | 0 | 50 | 0 |

| has_house | float64 | 16392 | 2 | 0.1090 | 0.3116 | 2.5098 | 4.2993 | 0 | 0 | 0 | 0 | 1 | 0 |

| cumulative_dpd | float64 | 16511 | 35031 | 5005.386 | 21825.91 | 18.3173 | 1254.268 | -202 | 0 | 11 | 210 | 2.97e+06 | 210 |

| max_dpd | float64 | 16511 | 4125 | 204.598 | 808.5411 | 126.5898 | 34483.72 | -1 | 0 | 5 | 42 | 260000 | 42 |

| MOBILEPHONE | float64 | 3 | 331432 | 7.38e+09 | 3.42e+08 | 0.1235 | -1.8722 | 7.0e+09 | 7.05e+09 | 7.09e+09 | 7.76e+09 | 7.88e+09 | 7.08e+08 |

| repeated_client | int64 | 0 | 2 | 0.6110 | 0.4875 | -0.4553 | -1.7927 | 0 | 0 | 1 | 1 | 1 | 1 |

| Feature | Dtype | Missing | Unique | Freq (Top) | Percent Top |

| APPLCTNCREATIONDATE | object | 0 | 1174 | 1285 | 0.36% |

| SUBPRODUCT | object | 0 | 4 | 161777 | 45.43% |

| ON_OFF | object | 0 | 2 | 349039 | 98.03% |

| STATUSGROUP | object | 0 | 1 | 356069 | 100% |

| District | object | 0 | 18 | 44589 | 12.52% |

| Feature | Dtype | Missing | Description |

| total_income | int64 | 0 | Total income of client |

| interest_rate_monthly | float64 | 0 | Monthly interest rate |

| gender | int64 | 0 | Client’s gender |

| age | int64 | 0 | Client’s age |

| loan_amount | int64 | 0 | Loan amount |

| loan_duration | int64 | 0 | Loan duration |

| prior_loans | int64 | 0 | Prior loan of client |

| inflation_rate | float64 | 0 | Inflation rate (macro variable) |

| co_borrower | int64 | 0 | Loan co-borrower |

| bad_client_90 | int64 | 0 | Target variable |

| Feature | Dtype | Missing | Unique | Mean | Std | Skewness | Kurtosis | Min | 25% | Median | 75% | Max | IQR |

| total_income | int64 | 0 | 280 | 413.3466 | 510.547 | 33.80261 | 2346.652 | -3730 | 200 | 300 | 500 | 40979 | 300 |

| interest_rate_monthly | float64 | 0 | 16 | 0.320061 | 0.023323 | 0.712978 | 1.02767 | 0.22 | 0.30 | 0.31 | 0.33 | 0.42 | 0.03 |

| gender | int64 | 0 | 2 | 0.06994 | 0.255053 | 3.372414 | 9.373175 | 0 | 0 | 0 | 0 | 1 | 0 |

| age | int64 | 0 | 50 | 41.13744 | 10.87164 | 0.218156 | -0.84841 | 19 | 32 | 41 | 49 | 68 | 17 |

| loan_amount | int64 | 0 | 146 | 1119.353 | 591.8797 | 1.437098 | 6.50226 | 300 | 650 | 1000 | 1500 | 8000 | 850 |

| loan_duration | int64 | 0 | 51 | 25.37428 | 7.268534 | 0.422163 | 0.645454 | 6 | 20 | 24 | 31 | 113 | 11 |

| prior_loans | int64 | 0 | 15 | 2.271662 | 1.802722 | 2.143508 | 5.60351 | 1 | 1 | 2 | 3 | 15 | 2 |

| inflation_rate | float64 | 0 | 28 | 1.014938 | 1.030362 | -0.00989 | -0.76155 | -0.567 | 0.197 | 1.609 | 1.849 | 5.393 | 1.652 |

| co_borrower | int64 | 0 | 2 | 0.55431 | 0.497056 | -0.21853 | -1.95224 | 0 | 0 | 1 | 1 | 1 | 1 |

| bad_client_90 | int64 | 0 | 2 | 0.124306 | 0.32994 | 2.277411 | 3.186599 | 0 | 0 | 0 | 0 | 1 | 0 |

| Feature | Dtype | Missing | Unique | Freq | Percent Top |

| family_status | object | 0 | 5 | 13852 | 78.45 % |

| branch | object | 0 | 16 | 1969 | 11.15 % |

| Feature | Dtype | Missing | Description |

| CLAIM_AMOUNT | float64 | 0 | Loan amount |

| INTEREST_RATE | float64 | 0 | Interest rate |

| COLLATERAL | float64 | 0 | Does the loan has collateral |

| CREDIT_SUM | float64 | 0 | The sum of loan |

| target_60 | int64 | 0 | Target variable |

| DURATION | float64 | 0 | Duration of loan |

| AGE | float64 | 0 | Client’s age |

| Consumer Price Index CPI | float64 | 0 | Consumer price index (CPI) |

| Food Inflation | float64 | 0 | Food inflation (macro variable) |

| Inflation Rate | float64 | 0 | Inflation rate |

| Interest Rate2 | float64 | 0 | Inflation rate |

| Wages | float64 | 0 | Wages (macro variable) |

| Remittance | float64 | 0 | Remittance (macro variable) |

| Feature | Dtype | Missing | Unique | Mean | Std | Skewness | Kurtosis | Min | 25% | Median | 75% | Max | IQR |

| CLAIM_AMOUNT | float64 | 0 | 161 | 12193.39 | 13521.02 | 4.6163 | 45.7864 | 500 | 4100 | 7500 | 15000 | 200000 | 10900 |

| INTEREST_RATE | float64 | 0 | 26 | 22.15 | 2.73 | 1.1352 | 3.2927 | 16 | 21 | 22 | 24 | 34 | 3 |

| COLLATERAL | float64 | 0 | 219 | 17738.84 | 30898.06 | 4.4516 | 28.2051 | 283.5 | 4000 | 7000 | 15000 | 380000 | 11000 |

| CREDIT_SUM | float64 | 0 | 186 | 11329.17 | 11641.37 | 2.8103 | 15.7643 | 500 | 4000 | 7000 | 14999 | 150000 | 10999 |

| target_60 | int64 | 0 | 2 | 0.0537 | 0.2254 | 3.9615 | 13.6937 | 0 | 0 | 0 | 0 | 1 | 0 |

| DURATION | float64 | 0 | 27 | 26.30 | 7.76 | -0.0098 | -0.9507 | 8 | 24 | 24 | 36 | 48 | 12 |

| AGE | float64 | 0 | 50 | 46.66 | 10.53 | 0.0458 | -0.9695 | 22 | 38 | 46 | 56 | 71 | 18 |

| Consumer Price Index CPI | float64 | 0 | 24 | 180.08 | 12.26 | 0.6766 | -0.6089 | 164.8 | 169.5 | 176.9 | 189.5 | 208.6 | 20 |

| Food Inflation | float64 | 0 | 21 | 9.91 | 6.01 | 0.6594 | -1.4142 | 4.4 | 4.9 | 6.7 | 17.2 | 19.5 | 12.3 |

| Inflation Rate | float64 | 0 | 23 | 7.50 | 3.94 | 0.5851 | -1.4292 | 3.3 | 4.2 | 5.7 | 12.4 | 13.9 | 8.2 |

| Interest Rate2 | float64 | 0 | 8 | 6.95 | 0.68 | 0.2474 | -1.4979 | 6.25 | 6.25 | 7 | 7.75 | 8.25 | 1.5 |

| Wages | float64 | 0 | 24 | 750.50 | 49.60 | 0.7271 | -1.0307 | 690.9 | 722.9 | 725.6 | 809 | 839.4 | 86.1 |

| Remittance | float64 | 0 | 8 | 318.62 | 375.81 | 1.3966 | 0.2309 | 88.4 | 101.4 | 131 | 135 | 1215.2 | 33.6 |

| unclaimed | float64 | 0 | 98 | -864.22 | 4644.21 | -18.247 | 486.949 | -150000 | 0 | 0 | 0 | 23400 | 0 |

| overcolletoral | float64 | 0 | 147 | 6409.67 | 23338.97 | 5.5132 | 40.4910 | -20000 | 0 | 0 | 0 | 330000 | 0 |

| Feature | Dtype | Missing | Unique | Freq | Percent Top |

| PRODUCT_NAME | object | 0 | 2 | 2602 | 95.63 % |

| CREDIT_STATUS | object | 0 | 2 | 2269 | 83.39 % |

| SEGMENT | object | 0 | 7 | 1642 | 60.35 % |

| FIELD | object | 0 | 6 | 1622 | 59.61 % |

| BEGINDATE | object | 0 | 491 | 23 | 0.85 % |

| BRANCH | object | 0 | 20 | 289 | 10.62 % |

| CLIENT_STATUS | object | 0 | 2 | 2678 | 98.42 % |

| Feature | Dtype | Missing | Description |

| int_rate | float64 | 0 | The annual interest rate for the loan |

| annual_inc | float64 | 0 | The borrower’s self-declared annual income |

| acc_open_past_24mths | float64 | 50001 | Number of trades opened in past 24 months |

| dti | float64 | 412 | The debt-to-income ratio, representing monthly debt payments divided by monthly income |

| unemployment_rate | float64 | 169 | Unemployment rate |

| total_bc_limit | float64 | 50001 | Total bankcard high credit/credit limit |

| installment | float64 | 0 | The monthly payment owed by the borrower if the loan originates |

| fico_range_high | float64 | 0 | The upper boundary range the borrower’s FICO at loan origination belongs to |

| total_acc | float64 | 0 | The total number of credit lines in the applicant’s credit history |

| revol_bal | float64 | 0 | Total credit revolving balance |

| fico_range_low | float64 | 0 | The lower boundary range the borrower’s FICO at loan origination belongs to |

| avg_cur_bal | float64 | 70270 | Average current balance of all accounts |

| mo_sin_old_rev_tl_op | float64 | 70248 | Months since oldest revolving account opened |

| mths_since_recent_bc | float64 | 63383 | Months since most recent bankcard account opened |

| funded_amnt | float64 | 0 | The total amount committed to that loan at that point in time |

| federal_funds_rate | float64 | 103209 | Federal funds rate |

| loan_condition_int | int64 | 0 | Target variable |

| Feature | Dtype | Missing | Unique | Mean | Std | Skewness | Kurtosis | Min | 25% | Median | 75% | Max | IQR |

| int_rate | float64 | 0 | 672 | 13.30 | 4.79 | 0.72 | 0.52 | 5.31 | 9.75 | 12.79 | 16.02 | 30.99 | 6.27 |

| annual_inc | float64 | 0 | 65577 | 76290.19 | 70270.58 | 46.56 | 4849.01 | 0 | 45760 | 65000 | 90000 | 10999200 | 44240 |

| acc_open_past_24mths | float64 | 50001 | 55 | 4.70 | 3.19 | 1.37 | 4.36 | 0 | 2 | 4 | 6 | 64 | 4 |

| dti | float64 | 412 | 7347 | 18.32 | 11.35 | 27.11 | 2063.95 | -1 | 11.8 | 17.63 | 24.09 | 999 | 12.29 |

| unemployment_rate | float64 | 169 | 122 | 5.63 | 1.53 | 1.12 | 1.85 | 2 | 4.6 | 5.4 | 6.3 | 14.3 | 1.7 |

| total_bc_limit | float64 | 50001 | 17249 | 21606.22 | 21537.28 | 2.89 | 21.56 | 0 | 7800 | 15100 | 28080.25 | 1105500 | 20280.25 |

| installment | float64 | 0 | 84260 | 439.49 | 262.40 | 1.00 | 0.74 | 4.93 | 249.19 | 375.54 | 582.62 | 1719.83 | 333.43 |

| fico_range_high | float64 | 0 | 48 | 700.06 | 31.79 | 1.29 | 1.68 | 614 | 674 | 694 | 714 | 850 | 40 |

| total_acc | float64 | 0 | 144 | 24.93 | 12.01 | 0.96 | 1.68 | 1 | 16 | 23 | 32 | 176 | 16 |

| revol_bal | float64 | 0 | 84717 | 16251.73 | 22437.44 | 13.66 | 701.50 | 0 | 5925 | 11119 | 19741 | 2904836 | 13816 |

| fico_range_low | float64 | 0 | 48 | 696.06 | 31.79 | 1.29 | 1.68 | 610 | 670 | 690 | 710 | 845 | 40 |

| avg_cur_bal | float64 | 70270 | 77320 | 13466.77 | 16276.54 | 3.91 | 46.51 | 0 | 3095 | 7376 | 18683 | 958084 | 15588 |

| mo_sin_old_rev_tl_op | float64 | 70248 | 759 | 181.22 | 94.65 | 1.04 | 1.48 | 2 | 117 | 164 | 230 | 852 | 113 |

| mths_since_recent_bc | float64 | 63383 | 491 | 23.79 | 30.75 | 3.46 | 20.62 | 0 | 6 | 13 | 28 | 639 | 22 |

| funded_amnt | float64 | 0 | 1564 | 14469.33 | 8749.62 | 0.78 | -0.09 | 500 | 8000 | 12000 | 20000 | 40000 | 12000 |

| federal_funds_rate | float64 | 103209 | 53 | 0.26 | 0.38 | 3.69 | 18.11 | 0.04 | 0.07 | 0.09 | 0.29 | 5.31 | 0.22 |

| loan_condition_int | int64 | 0 | 2 | 0.22 | 0.41 | 1.35 | -0.17 | 0 | 0 | 0 | 0 | 1 | 0 |

| Feature | Dtype | Missing | Unique | Top | Freq | Percent_Top |

| grade | object | 0 | 7 | B | 400644 | 28.98 % |

| term | object | 0 | 2 | 36 months | 1043030 | 75.45 % |

| sub_grade | object | 0 | 35 | C1 | 87838 | 6.35 % |

| home_ownership | object | 0 | 6 | MORTGAGE | 682135 | 49.35 % |

| addr_state | object | 0 | 51 | CA | 201525 | 14.58 % |