Nonparametric Estimation from Correlated Copies of a Drifted 2nd-Order Process

Abstract.

This paper presents several situations leading to the observation of multiple - possibly correlated - copies of a drifted 2nd-order process, and then non-asymptotic risk bounds are established on nonparametric estimators of the drift function and its derivative. For drifted Gaussian processes with a regular enough covariance function, a sharper risk bound is established on the estimator of , and a model selection procedure is provided with theoretical guarantees.

†Université Paris Nanterre, CNRS, Modal’X, 92001 Nanterre, France.

Keywords: Correlated processes; Gaussian processes; Fractional Brownian motion; Functional Data; Nonparametric estimation; Drift estimation; Derivative estimation; Model selection.

1. Introduction

Let be the process defined by

| (1) |

where is a centered continuous 2nd-order process, and is an unknown piecewise continuous function. Consider also , and the processes defined by

| (2) |

where are copies of such that, for every ,

| (3) |

Several dynamics and observation schemes lead to Model (2) for well-chosen , and . First, correlated copies of a non-autonomous linear (fractional) diffusion process can be written as , where the corresponding , and are provided in Section 2.1.1. For instance, are appropriate to model the prices of interacting risky assets of same kind as in Duellmann et al. [10], or the elimination processes of a drug by patients involved in a clinical trial (see Donnet and Samson [9]). In the same spirit, Section 2.1.2 provides a basic interacting particle system leading to Model (2). Now, in statistical inference for stochastic differential equations, at least two kinds of estimators of the drift function are investigated in the literature: those computed from one long-time observation of the ergodic stationary solution (see Kutoyants [17] and Kubilius et al. [16]), and those computed from multiple copies of the solution observed on a short-time interval (see Comte and Genon-Catalot [5], Denis et al. [7], Marie [19], etc.). In our simple Model (1), when the fractional Brownian motion, Section 2.2 shows how to construct - with theoretical guarantees - correlated copies of from one long-time observation of .

Beyond the aforementioned possible applications of Model (2), the estimation of and (when ) - which is part of nonparametric functional data-analysis (see Ferraty and Vieu [11]) - need to be investigated. On nonparametric estimators of computed from one long-time observation of when is a Gaussian process, see Ibragimov and Rozakov [14], Chapter VII, or the more recent paper [21] written by Privault and Réveillac, and on those computed from multiple independent copies of observed on a short-time - possibly random - interval, the reader can refer to Bunea et al. [2], Kassi and Patilea [15] and references therein. On kernel-based nonparametric estimators of computed from multiple independent copies of , see Ghale-Joogh and Hosseini-Nasab [13] and references therein. On asymptotic results on projection estimators - in the B-spline basis - of all derivatives of in Model (2), the reader can refer to Cao [3]. Up to our knowledge, [3] is the only reference on a nonparametric estimator of in Model (2) driven by correlated signals.

In our paper, a simple estimator of (on ) is given by and reaches the parametric rate (see Section 3.1). However, having in mind the estimation of the drift function of a non-autonomous linear (fractional) diffusion process, a suitable estimator of (on ) is also required. So, now, assume that , and that the paths of are locally -Hölder continuous with . Moreover, consider , where , are continuously differentiable functions from into , and is an orthonormal family of . In the sequel, the orthogonal projection from onto is denoted by . Since is an estimator of reaching the parametric rate , so is for large enough, and since

a natural estimator of is given by

where the integral with respect to is taken in the sense of Young (see Friz and Victoir [12], Sections 6.1 and 6.2). In Section 3.2, a non-asymptotic risk bound is established on , and then improved when is a Gaussian process with a regular enough covariance function by using that for every , coincides with the Wiener integral on of with respect to . A model selection procedure is provided with theoretical guarantees on the corresponding adaptive estimator.

The outline of the paper is as follows. Section 2 deals with some dynamics and observation schemes leading to Model (2), the aforementioned theoretical results on and are established in Section 3, and Section 4 shows that both and are also satisfactory on the numerical side.

Notations. Throughout this paper, the -norm (resp. -norm) is denoted by (resp. ), and the uniform norm is denoted by .

2. Some dynamics and observation schemes leading to Model (2)

2.1. From (fractional) diffusions and interacting particle systems to Model (2)

This section shows how to construct from copies of a linear (fractional) diffusion, and from a basic interacting particle system. Moreover, possible applications in finance and in pharmacokinetics are mentioned.

2.1.1. Copies of a linear (fractional) diffusion

First, for any , consider the process defined by the (Itô) stochastic differential equation

| (4) |

where , , , are Brownian motions such that for every , and is a correlation matrix. For instance, (4) is appropriate to model the prices of interacting risky assets of same kind as in Duellmann et al. [10]. For every , thanks to the Itô formula,

| (5) |

Moreover, are centered continuous 2nd-order processes such that, by the stochastic integration by parts formula,

Thus, satisfy the condition (3) with

Now, for any , consider the process defined by the pathwise (Young) differential equation

| (6) |

where , , , are independent fractional Brownian motions of Hurst parameter , and are i.i.d. centered square-integrable random variables of common variance such that and are independent. Such a model with random effects is commonly used in population pharmacokinetics (see Donnet and Samson [9]), but usually and the stochastic integral in Equation (6) is taken in the sense of Itô. However, to take close to ensures that the paths of are moderately irregular, which is appropriate to model the elimination process of a drug by the -th patient of a clinical trial. For every , thanks to the change of variable formula for Young’s integral,

| (7) |

Moreover, are i.i.d. centered continuous 2nd-order processes such that

Thus, satisfy the condition (3) with

2.1.2. A basic interacting particle system

For any , consider the process defined by

| (8) |

where , , with , and are independent Brownian motions. Moreover, let be the process defined by

| (9) |

For every ,

leading to

with

The following proposition provides a matrix satisfying the condition (3) for .

Proposition 2.1.

For every ,

where

Proof.

Consider and . Since are independent Brownian motions,

Therefore,

∎

2.2. From long-time observation to correlated copies

In this section, is a fractional Brownian motion of Hurst parameter , and a single observation of on is available. For every , consider with , and

| (10) |

Assume that is a -periodic function such that . Then, for every ,

Since the fractional Brownian motion has stationary increments, are copies of , and then are copies of . First, the following proposition provides a matrix satisfying the condition (3) for these copies of .

Proposition 2.2.

Assume that . For every ,

where

with

Proof.

Consider and, without loss of generality, such that . First, since the fractional Brownian motion has stationary increments,

where

Now, assume that . By the Taylor-Lagrange formula, there exists

such that

Then,

Moreover, since ,

and

Thus,

In conclusion, for every and ,

∎

Now, as in Marie [18], let us consider a financial market model in which the prices process and the volatility process of the risky asset satisfy

| (11) |

where , (resp. ) is a Brownian motion (resp. a fractional Brownian motion of Hurst parameter ), and . Since , Model (11) takes into account the persistence-in-volatility phenomenon as in Comte et al. [4]. For every , thanks to the change of variable formula for Young’s integral,

Usually, only one long-time observation of , and then of , are available. So, in order to consider the estimators provided in Section 3 for Model (2), must be defined from by (10).

3. Nonparametric estimators of and

3.1. Nonparametric estimator of

First, the following proposition provides a risk bound on .

Proposition 3.1.

Assume that satisfy the condition (3). Then,

| (12) |

Proof.

Remark 3.2.

Assume that

and that are independent copies of . Then, one may take for every such that , and for every , leading to

Corollary 3.4.

Proof.

Corollary 3.5.

If are defined by (10) with , then

Proof.

Remark 3.6.

Assume that and . By Corollary 3.5,

3.2. Nonparametric estimator of

Throughout this section, is continuously differentiable from into , and the paths of are locally -Hölder continuous with . For instance, the paths of the fractional Brownian motion of Hurst parameter are locally -Hölder continuous for every (see Nualart [20], Section 5.1). In Models (5) and (7) presented in Section 2.1, depends on with . For this reason, needs to be estimated. As explained in the introduction section, a natural estimator of is given by

where is the Young integral operator.

Notation. In the sequel,

First, the following proposition provides a risk bound on in the general case.

Proposition 3.7.

Assume that for every ,

| (13) |

Then,

| (14) |

Proof.

First, since ,

Moreover,

Then,

| (15) |

Now, thanks to the integration by parts formula,

leading to

Therefore, by Equality (15),

∎

Remark 3.8.

Let us make a few comments about the risk bound (14).

-

(1)

The order of the bias term

For instance, assume that is the -supported trigonometric basis: and, for every such that ,

Assume also that belongs to the Fourier-Sobolev space

By DeVore and Lorentz [8], Corollary 2.4 p. 205, there exists a constant , not depending on , such that

Moreover,

So,

and then reaches the bias-variance tradeoff for

-

(2)

When are independent copies of , at least for the trigonometric basis, the risk bound (14) on is of same order as that on the estimator of the regression function derivative in Comte and Marie [6] (see Proposition 3.9 and Section 4.2). However, the second part of Section 3.2 deals with a sharper risk bound on when is a Gaussian process with a regular enough covariance function.

Now, assume that is a Gaussian process which covariance function is denoted by , is a Gaussian vector for every , and that there exists a correlation matrix such that, for every and ,

| (16) |

In particular, satisfy the condition (3) with

| (17) |

Moreover, is assumed to be a -Hölder continuous map from into with as, for instance, the covariance function of the fractional Brownian motion of Hurst parameter (see Friz and Victoir [12], p. 405-407). The reproducing kernel Hilbert space of is denoted by , and equipped with the usual inner product

where the 2D integral with respect to is taken in the sense of Young (see Friz and Victoir [12], Section 6.4). In the sequel, there exists a constant such that, for every ,

| (18) |

Example 3.9.

Let us provide a few examples of processes satisfying the condition (18).

-

(1)

Assume that is a Brownian motion. Then, for every ,

-

(2)

Assume that

(19) Then, for every ,

On the one hand, let be the covariance function of the fractional Brownian motion of Hurst parameter , and note that

If , then satisfies the condition (19) because . On the other hand, assume that

where , is a fractional Brownian motion of Hurst parameter , and is a centered Gaussian random variable of variance such that and are independent. So,

If , then satisfies the condition (19).

Let us establish a risk bound on - sharper than in Proposition 3.7 - by using that for every , coincides with the Wiener integral on of with respect to .

Proof.

Remark 3.11.

Let us make a few comments about the risk bound (3.10).

- (1)

-

(2)

Assume that there exists a constant such that, for every ,

(23) By following the same line as in the proof of Proposition 3.10, one can show that under the conditions (16) and (23) (instead of (18)),

(24) The condition (23) is less demanding than (18). Indeed, for instance, to assume that

(25) leads to (23), but not to (18) requiring that (see Example 3.9.(2)). So, satisfies the condition (23) with , while it satisfies (18) with only. However, the variance term in the risk bound (24) depends on instead of as in (3.10), possibly leading to a degraded rate in some bases. Moreover, the condition (18) allows to establish a risk bound on the adaptive estimator provided in the last part of Section 3.2 whereas (23) doesn’t.

Note that is the minimizer, in , of the objective function such that

This legitimates to consider the adaptive estimator with selected in in the following way:

| (26) |

where

and is a constant to calibrate in practice.

Under the conditions of Proposition 3.10, the following theorem provides a risk bound on when are nested models (i.e. for every such that ).

Proof.

The proof of Theorem 3.12 is dissected in three steps.

Step 1. First, for any and every ,

where

Then, by the definition of ,

where, for every ,

By using that for every , and since ,

| (27) |

Step 2. Consider , and note that

where

For any ,

Moreover, (17) and (18) - respectively - lead to

Then,

So, by using the same chaining technique as in the proof of Baraud et al. [1], Proposition 6.1, there exists a constant , not depending on , such that for every ,

| (28) |

Step 3 (conclusion). By Inequality (28), there exists a constant , not depending on , such that for every ,

So, by Inequality (27),

and then Proposition 3.10 allows to conclude. ∎

Finally, although Corollary 3.3 provides suitable risk bounds on - the estimator of - in Models (5) and (7), the function of interest is that denoted by . The conditions (16) and (18) (see Example 3.9) are satisfied in each of these models, and then one can deduce risk bounds on adaptive estimators of from Theorem 3.12. Since (resp. ) in Model (5) (resp. (7)), (resp. ) is an estimator of .

4. Numerical experiments

4.1. Estimation in Models (8) and (10) via

First, independent Brownian motions are simulated along the dissection of with and , and so are the processes defined by (8) thanks to the Euler scheme with , and

For any , the transformation (9) is applied to , leading to where, for every ,

Then, is estimated by , and by

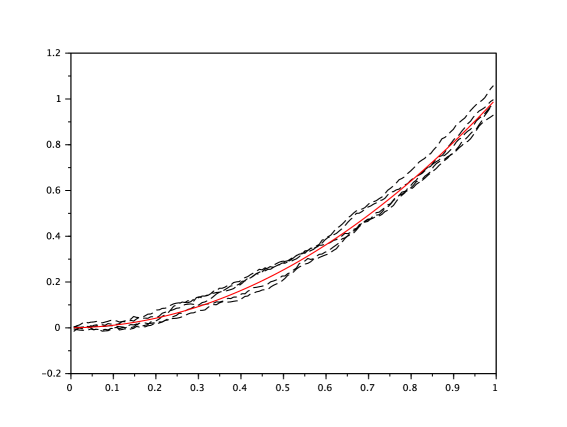

Figure 1 shows the true function (red line) and 5 estimations obtained thanks to (dashed black lines). The experiment is repeated times, and both the mean and standard deviation of the MISE of are very small: and respectively.

Now, consider , , , with , and the -periodic (and then -periodic) function such that

Note that, for every ,

For , the fractional Brownian motion , and then with , are simulated along the dissection

So, for every , the process defined by (10) is computed along :

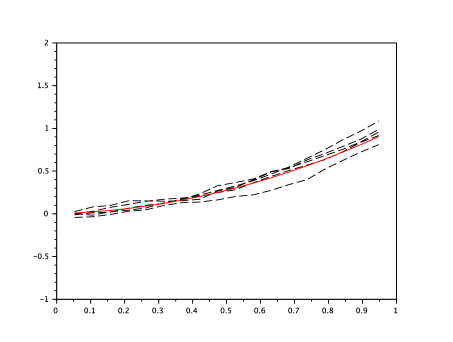

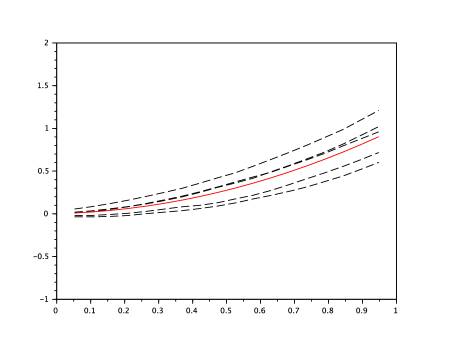

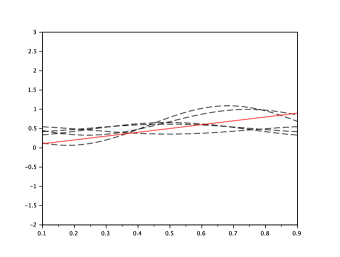

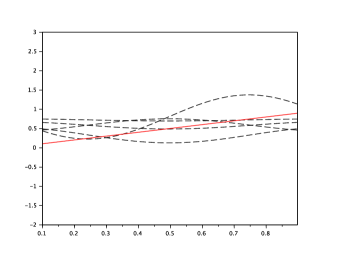

Again, is estimated by . Figure 2 shows the true function (red line) and 5 estimations obtained thanks to (dashed black lines) for two values of ( and ) and a double forgetting period ().

|

|

The experiment is repeated times for , but also for a single forgetting period (), and the means and standard deviations of are stored in Table 1.

| () | () | |

| () | () |

Both Figure 2 and the columns of Table 1 show that for a fixed value of , the mean and standard deviation of are small but degrade when increases. Moreover, the rows of Table 1 show that for a fixed value of , the mean and standard deviation of improve when increases. These numerical findings were expected from Corollary 3.5.

4.2. Estimation in Model (4) via

As in the first part of Section 4.1, independent Brownian motions are simulated along the dissection of with and . Consider the -dimensional process such that

where , , and with . Clearly, are correlated Brownian motions satisfying the condition (16), whose correlation increases with . For any , the solution of Equation (4) is simulated thanks to (5) with , where

Then, the drift function in Equation (4) is estimated by

where is the -supported trigonometric basis, and is selected in via (26).

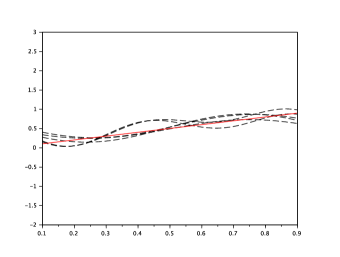

Figure 3 shows the true function (red line) and 5 adaptive estimations obtained thanks to (dashed black lines) for three values of (, and ).

|

|

|

The experiment is repeated times, and the means and standard deviations of and are stored in Table 2.

| Mean | |||

|---|---|---|---|

| StD. | |||

| Mean | |||

| StD. |

Both Figure 3 and Table 2 show that the mean and standard deviation of are small (of order ) when (i.e. are independent), but degrade when increases, which was expected from Theorem 3.12. Moreover, for all considered values of , the standard deviation of is lower than (see Table 2), meaning that our model selection procedure (26) is quite stable.

References

- [1] Baraud, Y., Comte, F. and Viennet, G. (2001). Model Selection for (Auto-)Regression with Dependent Data. ESAIM:PS 5, 33-49.

- [2] Bunea, F., Ivanescu, A.E. and Wegkamp, M.H. (2011). Adaptive Inference for The Mean of a Gaussian Process in Functional Data. Journal of the Royal Statistical Society B 73(4), 531-558.

- [3] Cao, G. (2014). Simultaneous Confidence Bands for Derivatives of Dependent Functional Data. Electronic Journal of Statistics 8, 2639-2663.

- [4] Comte, F., Coutin, C. and Renault, E. (2012). Affine Fractional Stochastic Volatility Models. The Annals of Finance 8, 337-378.

- [5] Comte, F. and Genon-Catalot, V. (2020). Nonparametric Drift Estimation for I.I.D. Paths of Stochastic Differential Equations. The Annals of Statistics 48(6), 3336-3365.

- [6] Comte, F. and Marie, N. (2023). On a Projection Estimator of the Regression Function Derivative. Journal of Nonparametric Statistics 35(4), 773-819.

- [7] Denis, C., Dion, C. and Martinez, M. (2021). A Ridge Estimator of the Drift from Discrete Repeated Observations of the Solution of a Stochastic Differential Equation. Bernoulli 27, 2675-2713.

- [8] DeVore, R.A. and Lorentz, G.G. (1993). Constructive Approximation. Springer.

- [9] Donnet, S. and Samson, A. (2013). A Review on Estimation of Stochastic Differential Equations for Pharmacokinetic/Pharmacodynamic Models. Advanced Drug Delivery Reviews 65, 929-939.

- [10] Duellmann, K, Küll, J. and Kunisch, M. (2010). Estimating Asset Correlations from Stock Prices or Default Rates - Which Method is Superior? Journal of Economic Dynamics & Control 34, 2341-2357.

- [11] Ferraty, F. and Vieu, P. (2006). Nonparametric Functional Data Analysis. Springer.

- [12] Friz, P. and Victoir, N. (2010). Multidimensional Stochastic Processes as Rough Paths: Theory and Applications. Cambridge University Press.

- [13] Ghale-Joogh, H.S. and Hosseini-Nasab, S.M.E. (2020). On Mean Derivative Estimation of Longitudinal and Functional Data: from Sparse to Dense. Statistical Papers 62, 2047-2066.

- [14] Ibragimov, I.A. and Rozakov, Y.A. (1978). Gaussian Random Processes. Springer.

- [15] Kassi, O. and Patilea, V. (2025). Optimal Inference for the Mean of Random Functions. arXiv:2504.11025.

- [16] Kubilius, K., Mishura, Y. and Ralchenko, K. (2017). Parameter Estimation in Fractional Diffusion Models. Springer.

- [17] Kutoyants, Y. (2004). Statistical Inference for Ergodic Diffusion Processes. Springer.

- [18] Marie, N. (2023). Nonparametric Estimation for I.I.D. Paths of a Martingale Driven Model with Application to Non-Autonomous Financial Models. Finance and Stochastics 27(1), 97-126.

- [19] Marie, N. (2025). From Nonparametric Regression to Statistical Inference for Non-Ergodic Diffusion Processes. Springer.

- [20] Nualart, D. (2006). The Malliavin Calculus and Related Topics. Springer.

- [21] Privault, N. and Réveillac, A. (2008). Stein Estimation for the Drift of Gaussian Processes Using the Malliavin Calculus. The Annals of Statistics 36(5), 2531-2550.