AICO: Feature Significance Tests

for Supervised Learning

Abstract

The opacity of many supervised learning algorithms remains a key challenge, hindering scientific discovery and limiting broader deployment—particularly in high-stakes domains. This paper develops model- and distribution-agnostic significance tests to assess the influence of input features in any regression or classification algorithm. Our method evaluates a feature’s incremental contribution to model performance by masking its values across samples. Under the null hypothesis, the distribution of performance differences across a test set has a non-positive median. We construct a uniformly most powerful, randomized sign test for this median, yielding exact -values for assessing feature significance and confidence intervals with exact coverage for estimating population-level feature importance. The approach requires minimal assumptions, avoids model retraining or auxiliary models, and remains computationally efficient even for large-scale, high-dimensional settings. Experiments on synthetic tasks validate its statistical and computational advantages, and applications to real-world data illustrate its practical utility.

1 Introduction

Supervised learning algorithms have become foundational tools across scientific and industrial domains, enabling breakthroughs and transforming key sectors. However, their opacity poses a major challenge, hindering scientific discovery and limiting adoption in high-stakes domains like finance, public policy and health care, where transparency is crucial.

This paper proposes novel testing methods for addressing the opacity of learning algorithms, focusing on the role of an algorithms’s input variables (features). Specifically, we develop a family of hypothesis tests to assess the significance of features in any supervised learning model, whether for regression or classification. The tests are model- and distribution-agnostic: they only require the ability to query the trained model—no assumptions about the model class, data distribution or model target (e.g. conditional mean, quantile) are needed. The computational efficiency of our tests is unprecedented. The procedure does not require retraining or surrogate models, making it well-suited for analyzing complex, high-dimensional algorithms that are costly to train.

The tests are based on a new approach for evaluating the impact of a feature. We quantify a feature’s incremental contribution to a user-defined score function, which measures a model’s predictive or decision-making performance on a test sample. Specifically, we compute the feature effect as the change in score when the model is given the actual value of the feature versus when the feature is masked with a baseline value. This masking approach, which we call Add-In Covariates (AICO), avoids the variance inflation (excess randomness) introduced by permutation methods and the high cost of retraining-based and surrogate-model-based strategies. The score function and masking baseline can be user-specified to align with specific interpretability goals and downstream model use cases; we discuss a number of choices and the associated tradeoffs.

The feature effect measures the impact of a feature’s variability on model score; it represents the importance of a feature at the level of an individual sample. A null-feature’s effect has a distribution across a collection of test samples whose median is non-positive. We construct a uniformly most powerful, randomized sign test for this median. Randomization at the boundary of the critical region ensures the test’s exactness, i.e., its size (type I error probability) matching the user-specified nominal level (e.g. ). The test delivers exact, randomized feature -values that have, conditionally on the data, a uniform distribution on an interval which can be reported in practice. It is simple, robust and permits an efficient implementation. It requires minimal assumptions, ensuring its broad validity in practice. These properties allow users to make valid inferences regarding a model’s features without relying on large-sample approximations or parametric assumptions.

The median feature effect being tested is a natural measure of feature importance at the population level. We develop randomized, exact-coverage confidence intervals for the median that, together with the -values, enable principled inference regarding feature influence. The availability of confidence intervals distinguishes the median from widely-used algorithmic measures of feature importance (see Section 1.1 below). Moreover, depending on the selection of the masking baseline, the median can have several useful properties. These include robustness to correlation between features, which is common in practice. Furthermore, for linear regression, the median is proportional to the square of the feature’s regression coefficient, which is the canonical measure of importance in the linear context. Finally, we provide conditions guaranteeing that a feature’s median being 0 is equivalent to it being conditionally independent of the response given the remaining features.

Extensive experiments on synthetic “known truth” tasks demonstrate the statistical and computational performance of our approach in nonlinear regression and classification settings. We compare our tests with the recently developed, model-agnostic and non-asymptotic tests of \citeasnounberrett, \citeasnountansey2018holdout and \citeasnounLei2018predictive. We also compare with the model-X knockoff procedures of \citeasnouncandes2018panning and \citeasnoundeepknockoffs for variable selection with false discovery control. Our test is found to be as statistically powerful as the alternatives, with minimal false discovery, while reducing computational costs by several orders of magnitude. Moreover, we show that our feature importance measure is robust to noise in the data, delivering stable feature importance rankings. This contrasts sharply with widely-used algorithmic feature importance measures including SHAP [lundberg2017unified] which are found to be highly sensitive to noise in the data, leading to unstable feature rankings that make it difficult to draw reliable inferences regarding variable importance. Our findings complement the discussion of the theoretical caveats of algorithmic importance measures in \citeasnounverdinelli-wasserman, \citeasnounkumar and others.

Several comprehensive empirical analyses illustrate our testing and feature importance approach in real-world data settings. In the context of a credit scoring task using large ensembles of gradient boosting machines, our approach identifies and ranks several significant features describing past payment behavior and social factors. Interestingly, we find that gender, marital status, and age of card holders (all of which are protected characteristics under US lending laws) are significant predictors of credit card default, after controlling for past payment behavior. In the context of a mortgage state transition prediction task using a recently proposed set-sequence model based on long-convolution architectures [elliot] and trained on extensive panel data, our test identifies time-varying macro-economic variables such as mortgage rates, as well as features summarizing past state transitions as significant predictors of borrower behavior.

The rest of this introduction discusses the related literature. Section 2 introduces the notion of feature effects while Section 3 develops the testing procedure. Section 4 analyzes the median feature effect as an importance measure dual to the test. Section 5 studies the performance of the test and importance measure in synthetic regression and classification settings. Section 6 deploys the test on two real-world data sets. The proofs of technical results are given in an appendix. A Python package implementing our testing and importance procedures is available at https://github.com/ji-chartsiri/AICO.

1.1 Related literature

There is a large body of work developing algorithmic feature importance measures; see \citeasnounburkart-huber for an overview. Popular examples include measures based on Shapley values (e.g. SHAP, see \citeasnounlundberg2017unified and many others), measures based on local approximations (e.g. LIME, see \citeasnounribeiro2016should), and measures obtained by permutation methods (e.g. \citeasnounbreiman, \citeasnounfisher-rudin). These measures provide valuable insight into the role of features but unlike the feature importance measures delivered by our hypothesis testing approach, they typically do not offer statistical guarantees or -values. We demonstrate that algorithmic measures can be highly susceptible to noise in the data so the lack of confidence intervals is concerning. Moreover, algorithmic measures such as SHAP can be biased in the presence of feature correlation [verdinelli-wasserman]. Our approach can deliver importance measures that are robust to feature correlation. Finally, we demonstrate that our method achieves orders-of-magnitude improvements in computational efficiency over widely used algorithmic importance approaches, such as SHAP and permutation scores.

The statistical and econometric literature has developed significance tests for the variables in nonparametric regression models. \citeasnounfan-li, \citeasnounlavergne2000nonparametric, \citeasnounait-sahalia-bickel, \citeasnoundelgado-manteiga, \citeasnounlavergne2015 and others employ kernel methods to construct asymptotic-based testing procedures. \citeasnounwhite2001statistical, \citeasnounhorel-giesecke and \citeasnounfallahgoul and others construct gradient-based asymptotic tests using neural networks. Unlike these tests, ours are model-agnostic, non-asymptotic, deliver exact -values and confidence intervals, and can accommodate a wide range of data structures.

Pursuing a model-agnostic approach, \citeasnouncandes2018panning, \citeasnounberrett, \citeasnountansey2018holdout, \citeasnounjanson, \citeasnounbellot, \citeasnounwright and others develop non-asymptotic tests for a conditional independence hypothesis of feature significance in the model-X knockoff setting of \citeasnouncandes2018panning.222Conditional independence testing is challenging: \citeasnounshah-peters show that no test of conditional independence can be uniformly valid against arbitrary alternatives. We show that, for an appropriate choice of the masking baseline, our null is generally weaker than the conditional independence null studied in these papers; equivalence holds under additional conditions. \citeasnounLei2018predictive construct non-asymptotic tests based on the drop in model predictive accuracy due to removing features (LOCO: Leave-out-covariates). We, in contrast, test the improvement in model score due to masking a feature.

The computational requirements of the aforementioned model-agnostic testing procedures are a limiting factor. The LOCO test requires re-training the model for each feature to be tested, which can be prohibitive for feature-rich models that are costly to train. The model-X knockoff procedures require constructing an auxiliary model of the joint feature distribution, which can be as challenging and computationally costly as constructing the model to be tested. In fact, \citeasnounbates show that no algorithm can efficiently compute nontrivial knockoffs for arbitrary feature distributions. Our approach does not require any model re-training or the construction of auxiliary models, delivering an unprecedented degree of computational efficiency. Our numerical results demonstrate that the drastic gains in computational performance we achieve do not come at the expense of statistical performance.

2 Feature effect

We consider i.i.d. data with . Here, is a -dimensional feature vector taking values in a set and is a response taking values in a set . In a typical regression setting with tabular data, and . We make no assumptions on the population law from which is sampled.

We take as given a random split of into non-intersecting subsets and , which are used for training/validation and testing purposes, respectively. This partitioning is standard in supervised learning settings. In our testing framework, data splitting facilitates post-selection inference.

We also take as given a model (algorithm) trained on , which is to be tested. We do not make any assumptions on the form of the modeling target; could represent , a conditional quantile, or some other statistic of . We also do not impose assumptions on the training criterion (eg. error) or approach (eg. empirical risk minimization) being used for training.

We would like to test the statistical significance of a feature under the model . (Unless noted otherwise, is fixed.) In the special case that is linear, standard asymptotic procedures such as the -test are available. We develop a simple, non-asymptotic and model-agnostic testing procedure that does not require a special model structure, and is valid much more broadly for models of essentially any form.

We consider the impact on model performance of a feature’s variability across the test set . Performance is measured by a deterministic score function , which relates model output to response. Specifically, for a given feature value and response value , the score evaluates the quality of the model output in view of . Higher scores reflect better performance. A natural choice for is the negative of the loss function used for the training of . Examples include the negative loss in a regression context, the negative pinball loss in a quantile regression context, or the negative (binary or multi-class) cross-entropy loss in a classification context. With these specifications measures predictive accuracy. Other specifications of can measure model performance (e.g. revenue) in the context of a downstream screening or decisioning application of , for example the financial loss caused by a poor decision due to mis-classification. Finally, we can specify a function that does not depend on the second argument representing the response, to measure the behavior (e.g. sensitivity) of the model output on its own, without reference to the response.

We evaluate the effect on model score of a feature’s variability across the test set. For each we construct from a baseline feature value serving as a reference and a comparison feature value . In the baseline, the value of the feature to be tested is masked with a reference value whose choice is further discussed below. The comparison value is unmasked so that the predicted response can harness the actual sample value of the feature to be tested. We propose to measure the feature effect by the resulting score improvement.

Definition 2.1 (Feature Effect).

For a given score function , baseline feature value and comparison feature value , the feature effect on test sample is the score delta

Note that masking feature values for purposes of measuring a feature effect has significant advantages over alternative approaches such as randomly shuffling feature values (e.g. \citeasnounbreiman and \citeasnounfisher-rudin) or dropping a feature from the feature vector. Shuffling introduces excess variance into the measurement procedure and dropping features requires training sub-models, which (drastically) reduces the computational efficiency of the measurement procedure. Our masking approach avoids these issues.

2.1 Baseline and comparison features

Along with the selection of the score function , the selection of baseline and comparison feature values enables users to tailor the feature effect to the model and data structures at hand as well as the testing objectives. We provide a conceptional framework and several examples. Throughout, fix a feature that is to be tested; our notation usually suppresses the dependence on . We start by selecting a non-empty set of training samples that will be used to construct the baseline for the test sample . In a second step, we aggregate the samples in to obtain . Alternative aggregators include the mean, a quantile or a mode of .

Example 2.1.

Take and let for all where is the mean of for each . The predicted response is constant across the test set. If feature is to be tested, select the comparison value . The predicted response harnesses feature 1’s actual sample value, . The feature effect represents the associated score improvement.

An alternative choice is and , again supposing feature is to be tested. The predicted baseline response is no longer constant across the test set, and accounts for the variation of features . Here measures a conditional feature effect.

Choices other than the mean may be appropriate for . For example, in the case of a one-hot feature which might encode a categorical variable, sensible choices for are a mode of or the value .333See \citeasnounhameed for extensions.

Consider choices of beyond the entire training set . We can pick specific samples from by first fixing a reference point in , , or and then selecting the samples from that lie in or outside a specified neighborhood of . The point can represent the (weighted) mean, mode or a -quantile of the responses , the predicted responses , or the values of the feature to be tested, . Potentially interesting special cases are quantiles for . Concretely, let be a reference response value and be a distance measure on . We can now take as the set of samples for which does not exceed or surpasses some threshold value. Other criteria can be envisioned, for example samples for which exceeds or falls short of . A similar approach applies to reference points in or .

Example 2.2.

Consider the reference point in , which is a quantile of the predicted responses at level . For example, in a binary soft classification setting such as fraud detection or credit scoring where represents the preferred (beneficial) outcome, this reference point represents the training samples with minimum predicted risk.444See \citeasnounboardman. We can take as the set of these samples and define and as in Example 2.1. The associated feature effect represents the score delta relative to the minimum risk baseline. It measures how much excess risk a feature explains.

A few basic principles guide the selection of reference points and the construction of the set . We wish to obtain values and that are sufficiently distinct, to avoid feature effects that are biased low which result in significance tests with low power.555\citeasnounsturmfels discuss these issues in the context of image classification. Similarly, we want to avoid saturation, where the predicted response is relatively flat in the neighborhood of . Finally, we might want to avoid the selection of values that are off the data manifold or in low-density areas of the training space. It is important to select an appropriate reference point and rule used to aggregate across (see Example 2.1). Alternatively, we might select an appropriate baseline value from the set , namely an element that is near the raw off-manifold value emerging from the baseline selection procedure.

For clarity, the discussion above has focused on selecting for testing a single feature . The approach naturally extends to testing multiple features, i.e. subsets of , which facilitates the exploration of higher-order effects including feature interactions. We also allow for the selection and aggregation of alternative baselines for a given sample. A general tool is sample-dependent or feature-dependent selection of .

2.2 Panel data

Panel data settings, where a collection of units are observed over some time period, are prevalent in many domains. While our approach assumes independent samples, a simple extension—grouping—allow us to treat some dependent settings like panel data. The idea is to aggregate feature effects within each unit of dependence, so that dependence is contained within groups with inter-group dependencies being mitigated.

Concretely, consider panel data , where indexes units and indexes time periods. We take as given a unit-level random split of the index set into disjoint training and testing subsets and , respectively, such that each unit, along with its entire time series, is assigned exclusively to either or . We treat the test set as a collection of samples and compute the per-unit-time feature effects for each . We then aggregate these effects within each unit: .

For purposes of computing baseline and comparison features in this group setting, we also treat the training data at a unit level. For each and feature , the per-unit-time samples are aggregated to obtain grouped feature samples , where is an aggregation function for the time series associated with unit (e.g. the mean, median, mode).

The grouping approach naturally extends to unbalanced panel data, where subjects may be observed at different time points or for different durations. In such cases, the average for each subject is computed only over the observed periods.

More broadly, the grouping approach can be adapted to other dependence structures beyond temporal ones. For instance, for spatially dependent data, one could group feature effects by region or neighborhood, under the assumption that neighborhoods are (approximately) independent. Similarly, in settings with repeated measurements, grouping by the underlying entity or context is effective.

3 Hypothesis testing

To construct a hypothesis test, we consider the empirical distribution of the feature effect across the test samples (the feature to be tested remains fixed). If that distribution has a non-positive center, then the feature is deemed insignificant. A large positive center is evidence of a feature being significant. There is a battery of alternative tests for the mean, median and other statistics, including , sign, Wicoxon, and permutation tests. We propose a simple sign test, which requires minimal assumptions on the data yet offers meaningful asymptotic relative efficiency vs. a -test.

Assumption 3.1.

The feature effects are independent draws from a conditional distribution given the training data with unique median . The associated distribution function is continuous.666A sufficient condition for the uniqueness of is strict monotonicity of in a neighborhood of .

Let be a Binomial- variable and let be its (lower) quantile at . Let be the test sample size. Moreover, let be the CDF of , where for .

Proposition 3.2.

Under Assumption 3.1, consider the hypotheses

| (1) |

for some . A Uniformly Most Powerful test of size rejects with probability where is the number of feature effect samples in the test set exceeding and

| (2) |

where and

| (3) |

-

•

Model trained on

-

•

Baseline feature values for

-

•

Comparison feature values for

-

•

Response values

-

•

Significance level

-

•

Score function

-

•

Test conclusion (True = Significant at level , False = Insignificant at level )

For brevity, we often suppress the dependence of the test statistic on . The test rejects with probability one if , the number of feature effects in the test set larger than , exceeds the -quantile of the Binomial- distribution. The test randomizes in case hits the boundary of the rejection region. Relative to a non-randomized test of with test function , randomization renders the test more aggressive; it ensures maximum power and guarantees exactness in the sense that

| (4) |

Algorithm 1 details the implementation of the test. Our applications of the test in Sections 5 and 6 below will use the value in (1).

In the context of our randomized test the notion of -value is ambiguous. A conventional -value could be defined as , the smallest level of significance at which is rejected with probability one, which is . (This is also a -value for a non-randomized test of with test function .) However, this formulation ignores the randomness of the UMP test’s decision rule. We follow \citeasnoungeyer-meeden and consider a randomized -value with conditional distribution function given by

From (2), this function represents a uniform distribution on an interval of length where

the right endpoint being the conventional -value. By iterated expectations and (4), we have

meaning that . In this sense, the randomized -value is exact, mirroring the exactness of the test’s decision rule (2). If is concentrated below a given level , or equivalently, if the conventional -value , we reject the null. If is concentrated above , or equivalently, if , we retain the null. Else the evidence is equivocal; we thus randomize by drawing a sample from and reject if . See Figure 1 for a visualization. In practice, it suffices to report the interval to fully characterize the -value; there is often no need to force a decision.

The power function of the test is given by

| (5) |

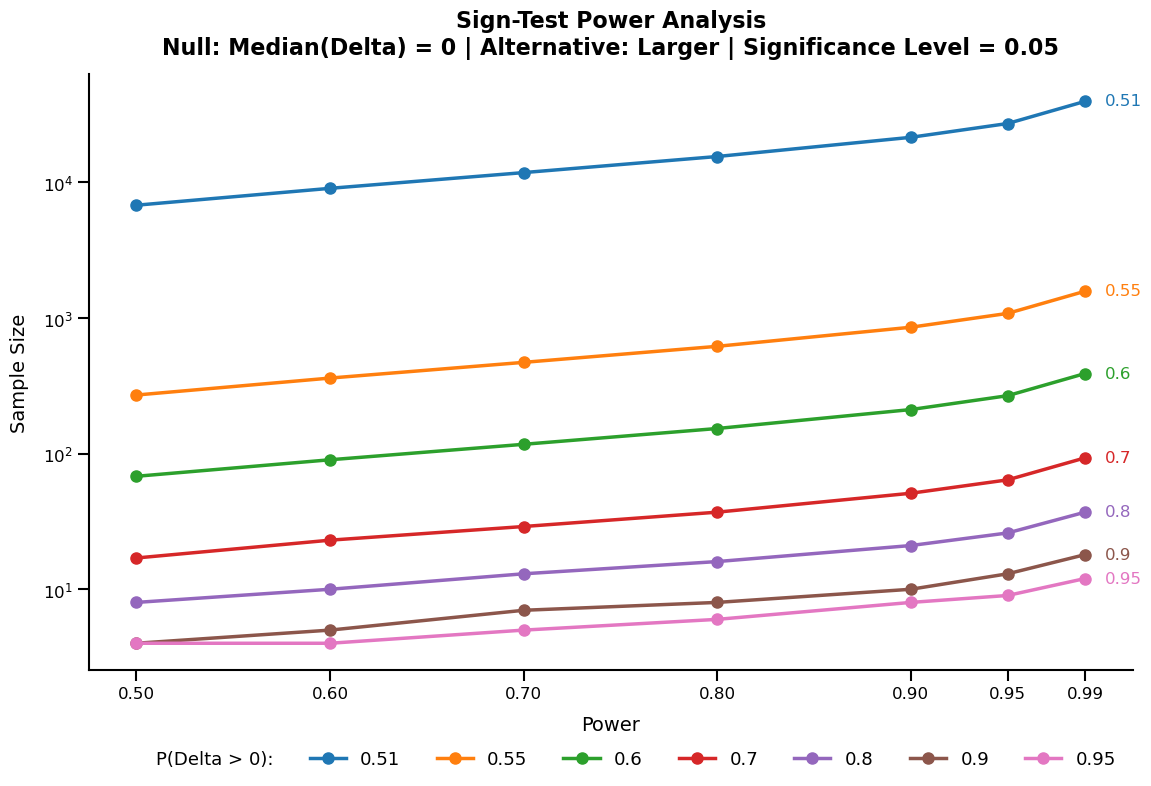

for values , where . The binomial probabilities in (3) are explicit. Since the test is uniformly most powerful, the function is increasing for fixed and . We can invert that function to determine the size of the test set required to achieve a desired level of power. The parameter can be estimated using a pilot sample or other approach, as discussed by \citeasnounnoether. Figure 2 plots the test sample size as a function of test power for several alternative values of .

The multiple testing problem can also be addressed in the randomized setting. A standard Bonferroni adjustment with test function and -value being conditionally uniform on the interval , where is the dimension of the feature vector, controls the family-wise error rate (FWER, the probability of having at least one false discovery), see \citeasnounkulinskaya2009fuzzy. For a less conservative approach, one can also control the False Discovery Rate [benjamini1995controlling]. \citeasnounkulinskaya2009fuzzy develop a formula and an algorithm for the adjusted rejection probability. \citeasnounhabiger2015multiple proposes an alternative Monte Carlo approach. \citeasnouncousido2022multiple provide a comparison of methods, finding that the Monte Carlo approach outperforms its alternatives in terms of test power.

4 Measuring feature importance

We require measures of feature importance that complement the feature -values delivered by our test. A local measure of feature importance is given by the feature effect , which represents the impact of a feature at the sample level. The median of the (conditional) feature effect distribution is a natural measure of feature importance at the population level. Under Assumption 3.1, a consistent estimator of is the empirical median

| (6) |

which satisfies for odd and approximate equality holding for even . Thus (6) is (approximately) as likely to overestimate as to underestimate it. Moreover, the distribution of is continuous. The estimator is unbiased if is symmetric about ; see Section 4.4 of \citeasnounlehmann.

We construct one-sided, randomized confidence intervals (CIs) for by inverting the test (2). Let denote the ordered sequence of ; we take and . Let denote the sampling distribution of the when is the true median.

Proposition 4.1.

In analogy to the randomized -value, the randomized CI (7) inherits the exactness of the test’s decision rule (2). If we reject the null for . If we retain the null. Else we reject with probability (that is, draw a sample from and reject if ).777For comparison, a non-randomized test of with test function has CI and rejects only if , implying a more conservative approach. In practice, it suffices to report the interval endpoints along with the rejection probability.

Standard arguments lead to alternative two-sided CIs, which are not, however, dual to the test (2). Observe that for . Using these probabilities, we can combine intervals so as to attain a desired confidence coefficient. Choosing the intervals symmetrically, we obtain intervals

| (9) |

satisfying , where we select so that for given . Then, , implying a conservative approach. \citeasnounzielinski extend this argument using randomization, resulting in CIs with exact coverage and minimum expected length. Alternative asymptotic CIs can be obtained by bootstrapping (e.g. \citeasnounefron and \citeasnounfalk-kaufmann), empirical likelihood [chen-hall], sectioning [asmussen-glynn] and other methods.

We develop several useful properties of the population-level feature importance measure defined by the median . To this end, let where denotes the population law from which the observed data points are independently drawn. For concreteness, consider a model for estimating the conditional mean, and take and the score function as given. The (population) feature effect is given by where and are suitable baseline and comparison features, respectively.

As discussed in Section 2.1, the selection of and offers some degrees of freedom. Consider the basic choice from Example 2.1,

| (10) |

where for convenience we assume, without loss of generality, feature is to be tested. First note that for the choice (10) and given and , the feature effect is completely determined by the marginal laws of the features and the joint law of the response and . Thus the feature dependence structure does not matter; the importance measure generated by (10) is robust to feature correlation. This is a remarkable property given the sensitivity of popular importance measures including SHAP and LOCO to correlation among features (e.g. \citeasnounverdinelli-wasserman). The correlation sensitivity induces a bias in these measures, which can lead to dubious importance rankings.

Next we explore the relationship between and conditional independence. \citeasnouncandes2018panning, \citeasnounberrett, \citeasnountansey2018holdout, \citeasnounjanson, \citeasnounbellot and others develop tests for a conditional independence hypothesis of feature significance in the model-X knockoff setting of \citeasnouncandes2018panning. We show that the hypothesis we test () is generally weaker than an alternative conditional independence hypothesis. Below, we use the notation .

Proposition 4.2.

Under (10), if then almost surely.

Note that Proposition 4.2 extends to functions other than as long as implies that is independent of the first entry of . The converse to Proposition 4.2 is not generally true. A simple counterexample is , i.e., second-order significant variables. A special case where the converse does hold is a standard linear model

| (11) |

Before stating a converse of Proposition 4.2 under (11), we note the following “linear agreement” property: under (11) (and symmetry of the distribution of ), the median measuring feature importance is proportional to the square of the regression coefficient, which is the canonical measure of feature importance in a linear model. The proportionality factor is given by the variance of the feature.

Proposition 4.3.

5 Synthetic tasks

This section illustrates the robust performance of our test and feature importance measure on synthetic “known truth” regression and classification tasks using neural networks. It also benchmarks performance against existing model-agnostic tests and variable selection procedures, as well as alternative model-specific and -agnostic feature importance measures.

5.1 Regression

We consider a feature vector of dimension and a response of the form

| (12) |

where the error is independent of and the conditional mean function is given by

| (13) |

The features and are jointly normal with mean zero, unit variances and covariances equal to . The features are independent , is uniform on , where , is Poisson with mean 3 and and are independent variables with a -distribution and 5 degrees of freedom. The non-influential variables and are independent , are jointly normal with mean zero, unit variances and covariances equal to , and and are independent variables with a -distribution and 5 degrees of freedom.

We generate a training set of independent samples and a test set of independent samples. We train a single-layer neural network model of the conditional mean . Specifically,

| (14) |

where is the number of units, is the activation function, and and are parameters to be estimated. The training procedure uses a standard loss criterion, regularization (of the weights ), the Adam optimization method, a batch size of 32, and 500 epochs with early stopping. We iterate across five random initializations. A validation set ( of , not used for training) and a Bayesian approach are used to optimize the regularization weight, the learning rate and the number of units, . The optimal weight is , the optimal learning rate is and the optimal . The on the training (and test) data exceeds .

The testing procedure uses a score function consistent with the training criterion. We use the basic baseline and comparison feature specifications discussed in Example 2.1. That is, for testing feature we take

| (15) |

where is the mean of in case feature is continuous. For the one-hot feature , we use and for the Poisson feature , we use the “alternative mode” where is the probability mass function of . The latter choice avoids baseline and comparison features being identical for too many samples, which is an issue arising with the standard mode. Our specifications yield baseline values in the support of and .

| AICO | CPT | HRT | LOCO | Deep | Gaussian | |||||||

| Knockoff | Knockoff | |||||||||||

| 5% | 1% | 5% | 1% | 5% | 1% | 5% | 1% | 5% | 1% | 5% | 1% | |

| 1 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 2 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 3 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 4 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 8 | 8 | 10 | 10 |

| 5 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 8 | 8 | 10 | 10 |

| 6 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 7 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 8 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 9 | 9 | 10 | 10 |

| 9 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 11 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 12 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 13 | 0 | 0 | 3 | 2 | 0 | 0 | 0 | 0 | 3 | 3 | 4 | 4 |

| 14 | 0 | 0 | 1 | 1 | 1 | 1 | 1 | 1 | 2 | 2 | 3 | 3 |

| 15 | 0 | 0 | 2 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 4 | 4 |

| 16 | 0 | 0 | 4 | 4 | 1 | 1 | 0 | 0 | 1 | 1 | 3 | 3 |

| 17 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 | 2 | 2 | 3 | 3 |

| 18 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 | 2 | 2 |

| 19 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 2 |

We run 10 independent training/testing experiments to assess the behavior of the test. The second and third columns of Table 1 report the results for confidence levels and .888Limited numerical precision can lead to ties, i.e. samples whose true values are distinct are being rounded to the same value. If the value of a tie is strictly positive, we count each sample in the test statistic . Another numerical artifact is samples with true, non-zero value being rounded to 0. We treat these samples as if they indeed had non-positive values not contributing to , implying a conservative approach. Alternative, potentially less conservative treatments include dropping ties (adjusting ) or randomly breaking them. See also \citeasnounwittkowski for another approach. The test has perfect power and does not produce false discoveries. Feature correlation (e.g. ) and discrete feature distributions () do not affect performance. The test also correctly detects the significance of features which influence the response only through product terms. Additional experiments show robustness to alternative baseline specifications (e.g. taking as the training mean also for the discrete features , and using the median instead of the mean to construct ). We also verify robustness with respect to the score function including the alternative specification .

We contrast our test with recently developed model-agnostic alternatives, including the Leave-Out-Covariates Test (LOCO) of \citeasnounLei2018predictive, the Conditional Permutation Test (CPT) of \citeasnounberrett, and the Holdout Randomization Test (HRT) of \citeasnountansey2018holdout. LOCO tests the mean or median delta in model loss across the test set due to removing feature from . Specifically, represents the th sample feature value without the th component and represents a neural network model (14) trained on . Testing all features requires re-training the model (14) times, each time for a different feature set.999In our numerical experiments, each of the sub-models has the same architecture as the full model and is trained using the same approach as was used for . This approach entails a significant additional computational expense that our testing procedure avoids.

The CPT and HRT tests are based on the Conditional Randomization Test of \citeasnouncandes2018panning, which is computationally challenging. They test the conditional independence hypothesis where . The tests require sampling from the (unknown) conditional law of given . We follow \citeasnountansey2018holdout and construct mixture density neural networks for the conditional laws. For additional perspective, we also implement recent model-agnostic variable selection procedures, including the Gaussian Model-X Knockoff procedure of \citeasnouncandes2018panning and the Deep Model-X Knockoff procedure of \citeasnoundeepknockoffs. The former relies on a Gaussian model of the feature distribution while the latter constructs a deep neural network for sampling from the feature distribution. The construction of complex auxiliary models in the CPT, HRT and knockoff procedures entails a significant additional computational expense that our AICO approach avoids.

Table 1 reports the results of the aforementioned alternative procedures for 10 independent training/testing experiments. CPT, HRT and LOCO deliver the same power as AICO but come with an increased false discovery rate (some but not all of these false discoveries can be addressed by a standard Bonferroni correction). The Gaussian Knockoff procedure selects the significant features 1 through 12 in each independent experiment. However, it does generate some false discoveries (which is consistent with control of the expected false discovery rate). The Deep Knockoff procedure reduces false discoveries at the expense of lower power. This approach has slight difficulty identifying the features entering the model (5.1) through the product term .

We consider the performance of our AICO test as a function of the size of the test set. Table 2 reports the results for ; the case is reported in Table 1. The test offers maximum power even for as small as 500. The power deteriorates moderately for smaller ; false discoveries rise only very slowly. This validates the performance of the test even for small samples.

| AICO | ||||||||||||

| 5% | 1% | 5% | 1% | 5% | 1% | 5% | 1% | 5% | 1% | 5% | 1% | |

| 1 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 2 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 9 | 8 | 5 |

| 3 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 4 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 9 | 9 |

| 5 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 9 |

| 6 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 7 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 8 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 9 | 8 | 8 | 7 |

| 9 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 11 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 12 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 |

| 13 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 1 | 0 | 0 |

| 14 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 1 | 0 |

| 15 | 0 | 0 | 1 | 0 | 1 | 1 | 0 | 0 | 1 | 0 | 1 | 0 |

| 16 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 1 | 0 |

| 17 | 1 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 18 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 19 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 2 |

We turn to measuring feature importance. Table 3 provides a feature importance ranking according to the empirical median (6) for one of the 10 independent training/testing experiments that was randomly chosen. It also reports the endpoints of the randomized CI (7) for the population median at a level, and the standard (non-randomized) two-sided CI (9) along with coverage probabilities. Table 3 also provides the distribution of the randomized -value.101010Ties of samples due to limited numerical precision are retained in when computing CIs and coverage probabilities. This is consistent with their treatment in the testing procedure (footnote 8).

| AICO, Level | |||||||||||

| -value Distribution | Randomized One-Sided CI | Non-Randomized Two-Sided CI | |||||||||

| Rank | Feature | Median | P(Reject) | Lower | Upper | 98.8% | 1.2% | Coverage | Lower | Upper | Coverage |

| 1 | 24.993 | 1.000 | 0.000 | 0.000 | 24.951 | 24.951 | 0.99 | 24.947 | 25.040 | 0.99007 | |

| 2 | 15.788 | 1.000 | 0.000 | 0.000 | 15.661 | 15.661 | 0.99 | 15.647 | 15.938 | 0.99007 | |

| 3 | 14.572 | 1.000 | 0.000 | 0.000 | 14.511 | 14.511 | 0.99 | 14.506 | 14.640 | 0.99007 | |

| 4 | 12.898 | 1.000 | 0.000 | 0.000 | 12.789 | 12.789 | 0.99 | 12.775 | 13.022 | 0.99007 | |

| 5 | 8.137 | 1.000 | 0.000 | 0.000 | 8.063 | 8.063 | 0.99 | 8.054 | 8.218 | 0.99007 | |

| 6 | 6.210 | 1.000 | 0.000 | 0.000 | 6.155 | 6.155 | 0.99 | 6.148 | 6.273 | 0.99007 | |

| 7 | 1.697 | 1.000 | 0.000 | 0.000 | 1.669 | 1.669 | 0.99 | 1.666 | 1.730 | 0.99007 | |

| 8 | 0.953 | 1.000 | 0.000 | 0.000 | 0.941 | 0.941 | 0.99 | 0.940 | 0.964 | 0.99007 | |

| 9 | 0.416 | 1.000 | 0.000 | 0.000 | 0.409 | 0.409 | 0.99 | 0.409 | 0.424 | 0.99007 | |

| 10 | 0.416 | 1.000 | 0.000 | 0.000 | 0.409 | 0.409 | 0.99 | 0.408 | 0.424 | 0.99007 | |

| 11 | 0.143 | 1.000 | 0.000 | 0.000 | 0.140 | 0.140 | 0.99 | 0.139 | 0.146 | 0.99007 | |

| 12 | 0.084 | 1.000 | 0.000 | 0.000 | 0.082 | 0.082 | 0.99 | 0.082 | 0.086 | 0.99007 | |

| - | -1.154e-07 | 0.000 | 0.880 | 0.881 | -2.442e-06 | -2.437e-06 | 0.99 | -2.708e-06 | 1.478e-06 | 0.99007 | |

| - | -2.054e-07 | 0.000 | 0.928 | 0.928 | -2.176e-06 | -2.175e-06 | 0.99 | -2.389e-06 | 9.014e-07 | 0.99007 | |

| - | -3.060e-07 | 0.000 | 0.845 | 0.846 | -3.339e-06 | -3.338e-06 | 0.99 | -3.639e-06 | 2.127e-06 | 0.99007 | |

| - | -5.512e-07 | 0.000 | 0.937 | 0.937 | -2.966e-06 | -2.965e-06 | 0.99 | -3.275e-06 | 9.626e-07 | 0.99007 | |

| - | -1.340e-06 | 0.000 | 0.996 | 0.997 | -3.773e-06 | -3.773e-06 | 0.99 | -4.022e-06 | 0.000 | 0.99150 | |

| - | 0.000 | 0.000 | 0.860 | 0.861 | -1.426e-06 | -1.423e-06 | 0.99 | -1.634e-06 | 1.114e-06 | 0.99007 | |

| - | 0.000 | 0.000 | 0.815 | 0.816 | -1.517e-06 | -1.516e-06 | 0.99 | -1.716e-06 | 1.333e-06 | 0.99007 | |

The -value distributions show that our approach is able to clearly distinguish between the significant and irrelevant features. The distributions of the significant features are concentrated near 0, far below the level . This provides substantial evidence in favor of rejecting the null for these features (the rejection probability is equal to 1). The -value distributions of the irrelevant features are concentrated significantly above , implying clear retention of the null for these features. There are no equivocal cases, eliminating the need to actually randomize.

Feature is judged to be the most important feature, followed by features and . The remaining significant features are relatively less important compared with this group of variables. Features have (almost) identical medians and CIs and thus importance, consistent with their symmetric roles in the conditional mean function (5.1).

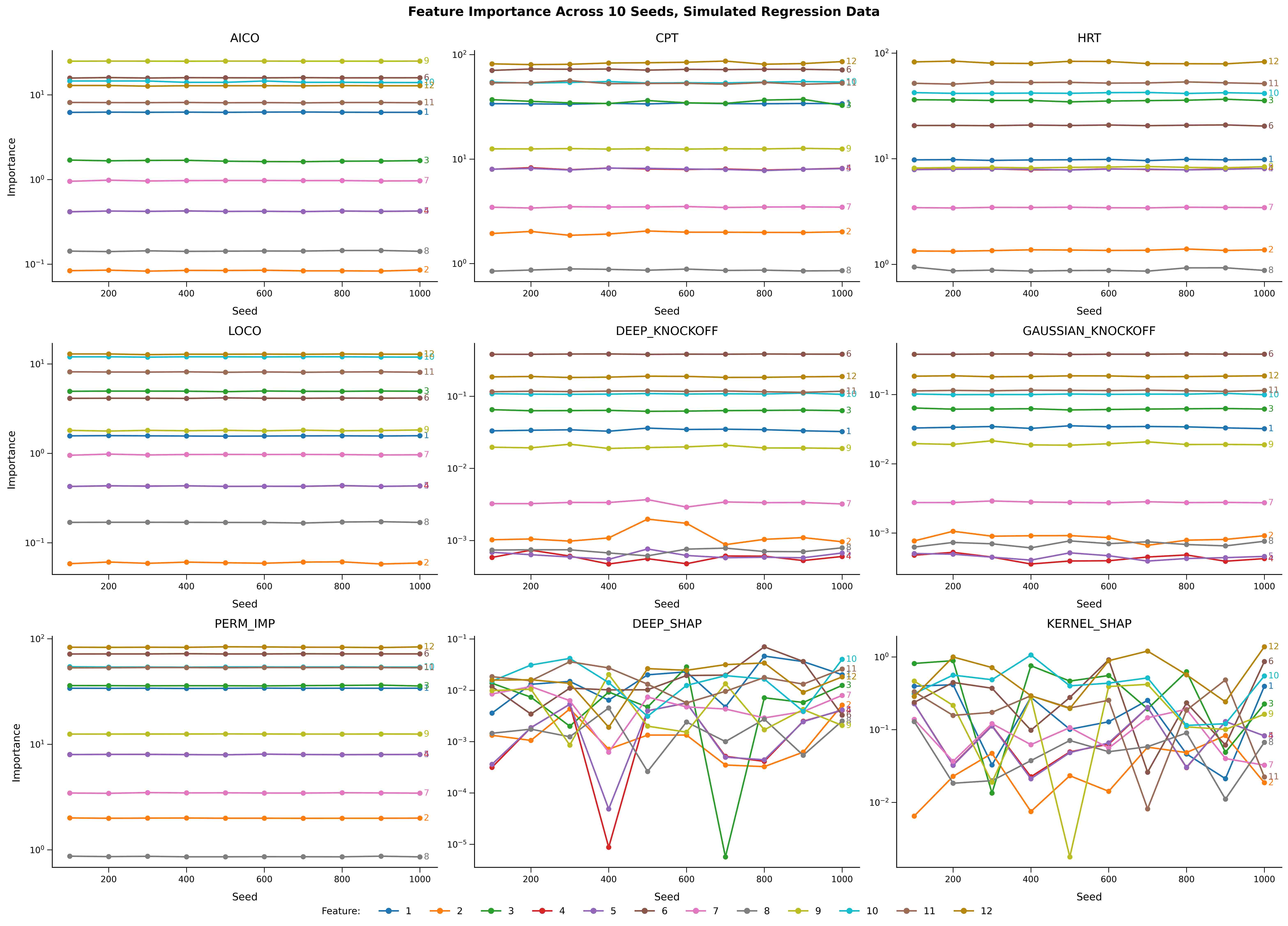

To demonstrate the stability of AICO feature importance scores, Figure 4 shows the empirical median (6) for each of the ten training/testing experiments. The AICO importance ranking is stable and robust to noise in the data. The ranking is also robust to alternative choices of the score function such as (results available upon request). For comparison, Figure 4 also provides test-implied feature importance scores for CPT, HRT, and LOCO [berrett, tansey2018holdout, verdinelli-wasserman], kernel and deep SHAP feature importance [lundberg2017unified], permutation feature importance scores [breiman, fisher-rudin], and Gaussian and deep knockoff feature importance scores [candes2018panning, deepknockoffs]. It is important to note that there is no ground truth for feature importance [hama-mase-owen]; hence we do not focus on the differences in importance rankings across alternative approaches. We do, however, highlight the robustness of the measures based on testing and variable selection procedures. The widely-used SHAP measures deliver inconsistent rankings across implementations (deep vs. kernel). The rankings are also highly unstable across experiments (data sets). That is, they appear to be highly susceptible to noise in the data. This questions the usefulness of SHAP for feature importance.

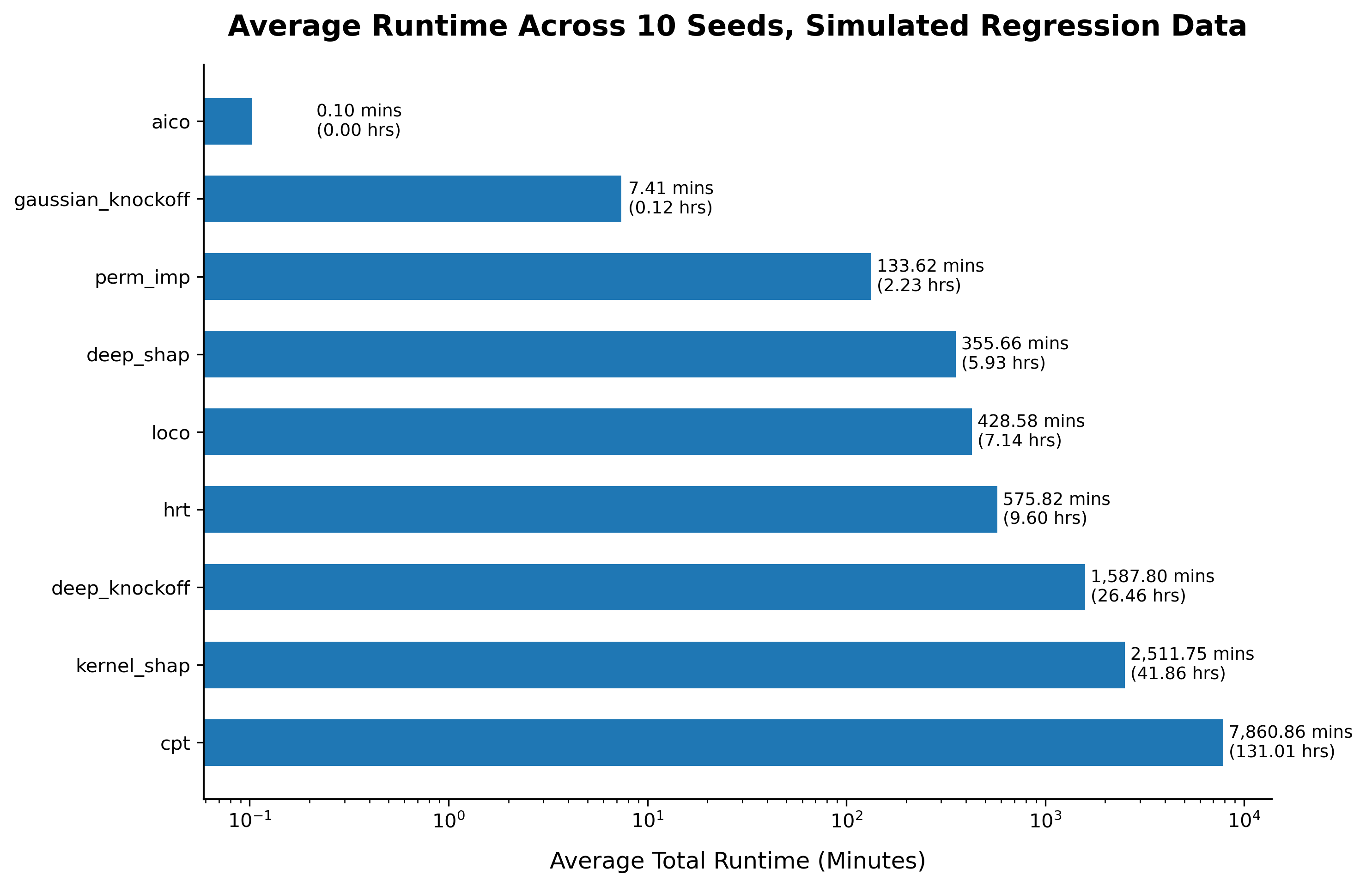

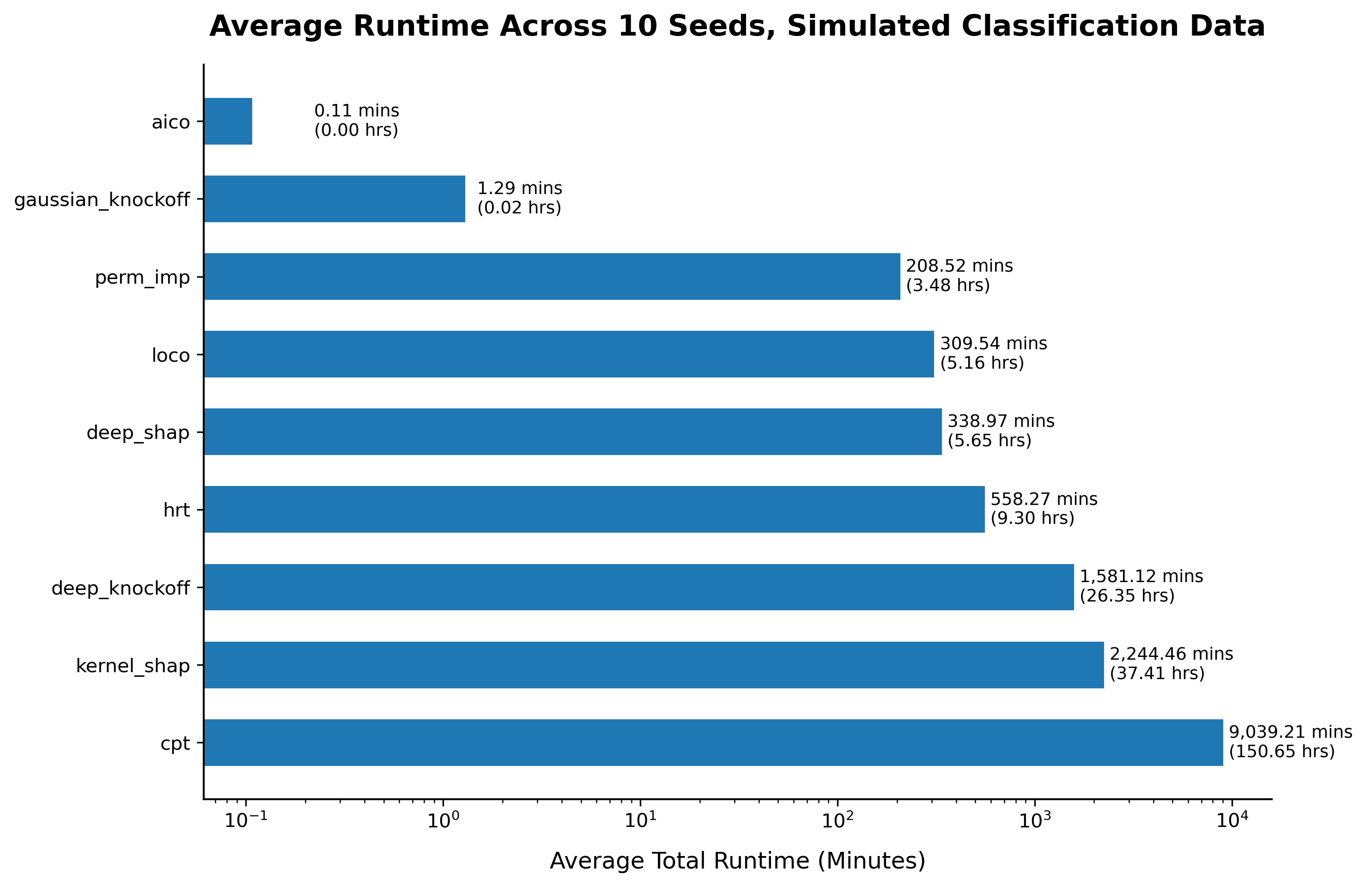

Finally we consider the computational efficiency of our test vs. the aforementioned alternatives. Figure 5 reports average computation times across 10 experiments.111111The compute environment consists of 8GB memory and 4 CPU cores (Intel Xeon CPU E5-2670, 2.60GHz and Silver 4110 CPU, 2.10GHz). In each of these experiments we test (AICO, CPT, HRT, LOCO) or screen (knockoffs) all 19 features or, in the case of SHAP and permutation feature importance, compute importance scores for all 19 features. The time reported includes the time to train any sub or auxiliary models. It does not include the time to train the original neural network (14).

AICO achieves an unprecedented degree of computational efficiency. In terms of full-fledged testing procedures, AICO is more than three orders of magnitude faster than LOCO, the next most efficient testing procedure. AICO is almost two orders of magnitudes more efficient than Gaussian knockoffs, the fastest screening procedure. It is more than three orders of magnitude faster than permutation importance, the fastest algorithmic feature importance measure. The testing results reported earlier in this section demonstrate that AICOs computational efficiency does not come at the expense of statistical performance.

5.2 Classification

We next consider a binary response governed by the model

| (16) |

where , the function is given by (5.1) and the features are as defined in Section 5.1. We generate a training set of independent samples and a test set of independent samples. The data are imbalanced, as is often the case in practice (e.g. credit scoring): about of the samples have . We train a single-layer neural network model of the conditional mean :

| (17) |

where , is the number of units, and and are parameters. The training procedure uses a standard cross-entropy criterion, regularization with weight (approximately the optimal weight in the regression model training), Adam, a batch size of 32, and 500 epochs with early stopping. A validation set ( of ) and a Bayesian approach are used to optimize the learning rate and the number of units, . The optimal learning rate is and the optimal . The Area Under the ROC Curve on the training (and test) data exceeds .

The testing procedure employs a score function consistent with the training criterion. We use the baseline and comparison feature specification (5.1). Table 4 reports the results for confidence levels . As in the regression case, the test has perfect power and avoids false discoveries. The test is generally robust to alternative specifications of the baseline (e.g. using the median instead of the mean to construct , setting to the training mean also for the 1-hot feature ).121212The local baseline has perfect power but some false discoveries. The test is also robust to using an alternative score function .

| AICO | CPT | HRT | LOCO | Deep | Gaussian | |||||||

| Knockoff | Knockoff | |||||||||||

| 5% | 1% | 5% | 1% | 5% | 1% | 5% | 1% | 5% | 1% | 5% | 1% | |

| 1 | 10 | 10 | 10 | 10 | 9 | 9 | 10 | 10 | 10 | 10 | 10 | 10 |

| 2 | 10 | 10 | 10 | 10 | 9 | 9 | 10 | 10 | 10 | 10 | 10 | 10 |

| 3 | 10 | 10 | 10 | 10 | 9 | 9 | 10 | 10 | 10 | 10 | 10 | 10 |

| 4 | 10 | 10 | 10 | 10 | 9 | 9 | 10 | 10 | 9 | 9 | 10 | 10 |

| 5 | 10 | 10 | 10 | 10 | 9 | 9 | 10 | 10 | 10 | 10 | 9 | 9 |

| 6 | 10 | 10 | 10 | 10 | 9 | 9 | 10 | 10 | 10 | 10 | 10 | 10 |

| 7 | 10 | 10 | 10 | 10 | 9 | 9 | 10 | 10 | 10 | 10 | 10 | 10 |

| 8 | 10 | 10 | 10 | 10 | 9 | 9 | 10 | 10 | 9 | 9 | 9 | 9 |

| 9 | 10 | 10 | 10 | 10 | 9 | 9 | 10 | 10 | 10 | 10 | 10 | 10 |

| 10 | 10 | 10 | 10 | 10 | 9 | 9 | 10 | 10 | 10 | 10 | 6 | 6 |

| 11 | 10 | 10 | 10 | 10 | 9 | 9 | 10 | 10 | 10 | 10 | 10 | 10 |

| 12 | 10 | 10 | 10 | 10 | 9 | 9 | 10 | 10 | 10 | 10 | 10 | 10 |

| 13 | 1 | 1 | 1 | 1 | 2 | 2 | 4 | 4 | 2 | 2 | 1 | 1 |

| 14 | 0 | 0 | 2 | 1 | 0 | 0 | 5 | 5 | 1 | 1 | 1 | 1 |

| 15 | 0 | 0 | 2 | 2 | 4 | 4 | 6 | 6 | 0 | 0 | 3 | 3 |

| 16 | 0 | 0 | 3 | 1 | 2 | 2 | 5 | 5 | 1 | 1 | 2 | 2 |

| 17 | 1 | 1 | 0 | 0 | 1 | 1 | 5 | 5 | 0 | 0 | 1 | 1 |

| 18 | 1 | 1 | 0 | 0 | 3 | 3 | 5 | 5 | 0 | 0 | 2 | 2 |

| 19 | 1 | 1 | 1 | 1 | 1 | 1 | 3 | 3 | 0 | 0 | 1 | 1 |

Table 4 also reports the results for LOCO, CPT, HRT and Gaussian and deep knockoff procedures. AICO, CPT and LOCO have full power. LOCO, however, suffers from significant number of false discoveries (which cannot be addressed with a standard Bonferroni adjustment). HRT and knockoff procedures have less power and some false discoveries. In this comparison, AICO outperforms the alternatives. It performs as well as in the regression setting.

| AICO | ||||||||||||

| 5% | 1% | 5% | 1% | 5% | 1% | 5% | 1% | 5% | 1% | 5% | 1% | |

| 1 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 9 | 7 | 3 | 0 |

| 2 | 10 | 10 | 10 | 10 | 6 | 5 | 3 | 2 | 6 | 5 | 3 | 1 |

| 3 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 8 | 8 |

| 4 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 9 | 6 | 2 | 4 | 0 |

| 5 | 10 | 10 | 10 | 10 | 10 | 10 | 8 | 8 | 8 | 6 | 6 | 1 |

| 6 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 8 | 6 | 2 | 1 |

| 7 | 10 | 10 | 8 | 7 | 3 | 3 | 2 | 0 | 1 | 0 | 0 | 0 |

| 8 | 10 | 10 | 5 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 9 | 10 | 10 | 10 | 10 | 6 | 3 | 3 | 1 | 5 | 3 | 3 | 1 |

| 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 9 | 9 | 8 | 5 |

| 11 | 10 | 10 | 10 | 10 | 6 | 2 | 9 | 5 | 0 | 0 | 3 | 1 |

| 12 | 10 | 10 | 10 | 10 | 10 | 9 | 6 | 5 | 5 | 2 | 2 | 0 |

| 13 | 0 | 0 | 1 | 0 | 1 | 0 | 3 | 0 | 0 | 0 | 0 | 0 |

| 14 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 2 | 1 |

| 15 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 1 | 0 |

| 16 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 2 | 0 |

| 17 | 1 | 1 | 1 | 0 | 1 | 0 | 2 | 0 | 0 | 0 | 0 | 0 |

| 18 | 1 | 1 | 1 | 0 | 1 | 0 | 2 | 0 | 0 | 0 | 0 | 0 |

| 19 | 0 | 0 | 1 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

Table 5 reports test results for varying test set sample sizes . Power decreases faster with than in the regression case, especially for features . False discoveries appear to be fairly insensitive to .

| AICO, Level | |||||||||||

| P-Value Distribution | Randomized One-Sided CI | Non-Randomized Two-Sided CI | |||||||||

| rank | variable | median | P(reject) | lower | upper | 98.8% | 1.2% | coverage | lower | upper | coverage |

| 1 | 3.577e-07 | 1.000 | 0.000 | 0.000 | 3.340e-07 | 3.340e-07 | 0.99 | 3.320e-07 | 3.829e-07 | 0.99007 | |

| 2 | 2.324e-08 | 1.000 | 0.000 | 0.000 | 2.077e-08 | 2.077e-08 | 0.99 | 2.053e-08 | 2.619e-08 | 0.99007 | |

| 3 | 6.722e-10 | 1.000 | 0.000 | 0.000 | 6.014e-10 | 6.016e-10 | 0.99 | 5.939e-10 | 7.656e-10 | 0.99007 | |

| 4 | 1.630e-10 | 1.000 | 0.000 | 0.000 | 1.442e-10 | 1.443e-10 | 0.99 | 1.426e-10 | 1.862e-10 | 0.99007 | |

| 5 | 6.989e-11 | 1.000 | 0.000 | 0.000 | 5.826e-11 | 5.828e-11 | 0.99 | 5.702e-11 | 8.597e-11 | 0.99007 | |

| 6 | 4.339e-11 | 1.000 | 0.000 | 0.000 | 3.697e-11 | 3.697e-11 | 0.99 | 3.643e-11 | 5.135e-11 | 0.99007 | |

| 7 | 3.169e-11 | 1.000 | 0.000 | 0.000 | 2.707e-11 | 2.707e-11 | 0.99 | 2.668e-11 | 3.733e-11 | 0.99007 | |

| 8 | 1.001e-11 | 1.000 | 0.000 | 0.000 | 8.027e-12 | 8.030e-12 | 0.99 | 7.821e-12 | 1.275e-11 | 0.99007 | |

| 9 | 6.787e-12 | 1.000 | 0.000 | 0.000 | 5.025e-12 | 5.025e-12 | 0.99 | 4.863e-12 | 9.439e-12 | 0.99007 | |

| 10 | 2.575e-14 | 1.000 | 0.000 | 0.000 | 1.823e-14 | 1.825e-14 | 0.99 | 1.755e-14 | 3.704e-14 | 0.99007 | |

| 11 | 1.100e-15 | 1.000 | 3.262e-71 | 3.431e-71 | 5.257e-16 | 5.261e-16 | 0.99 | 4.808e-16 | 2.326e-15 | 0.99007 | |

| 12 | 1.344e-17 | 1.000 | 1.706e-14 | 1.743e-14 | 2.386e-18 | 2.394e-18 | 0.99 | 1.972e-18 | 4.921e-17 | 0.99007 | |

| - | 0.000 | 0.000 | 1.000 | 1.000 | 0.000 | 0.000 | 0.99 | 0.000 | 0.000 | 1.00000 | |

| - | 0.000 | 0.000 | 1.000 | 1.000 | -1.396e-21 | -1.390e-21 | 0.99 | -2.680e-21 | 0.000 | 0.99485 | |

| - | -3.193e-21 | 0.000 | 1.000 | 1.000 | -5.676e-20 | -5.672e-20 | 0.99 | -7.258e-20 | 0.000 | 0.99503 | |

| - | 0.000 | 0.000 | 1.000 | 1.000 | -3.066e-22 | -3.052e-22 | 0.99 | -5.372e-22 | 0.000 | 0.99501 | |

| - | 0.000 | 0.000 | 1.000 | 1.000 | 0.000 | 0.000 | 0.99 | 0.000 | 0.000 | 0.99992 | |

| - | 0.000 | 0.000 | 0.940 | 0.940 | 0.000 | 0.000 | 0.99 | -1.849e-32 | 1.780e-22 | 0.99007 | |

| - | 0.000 | 0.000 | 1.000 | 1.000 | 0.000 | 0.000 | 0.99 | 0.000 | 0.000 | 0.99999 | |

Table 6 provides a feature importance ranking according to the empirical median (6) for one of the 10 independent training/testing experiments that was randomly chosen. It also reports the endpoints of the randomized CI (7) for the population median at a level, and the standard (non-randomized) two-sided CI (9) along with coverage probabilities. Table 3 also provides the distribution of the randomized -value.

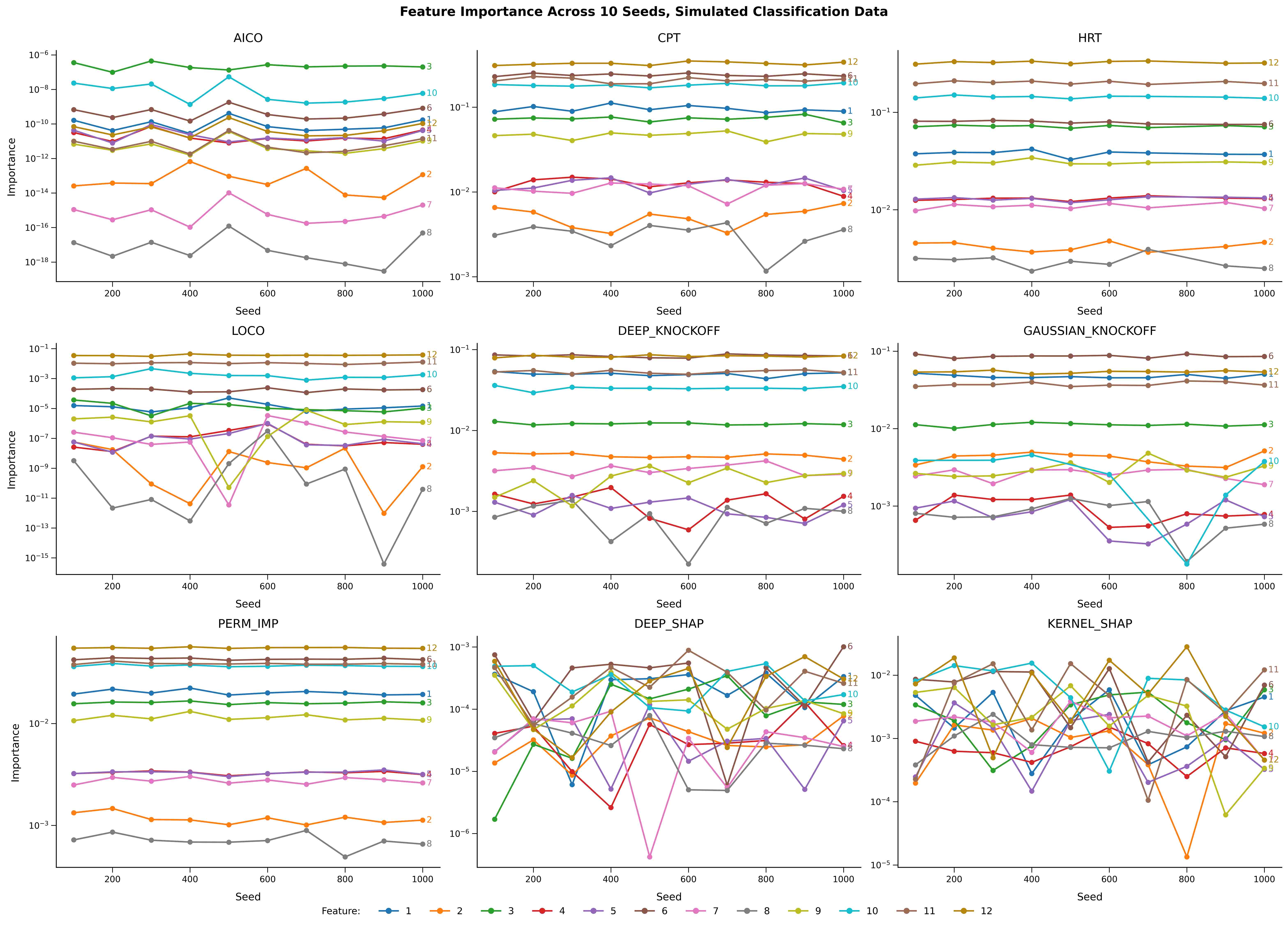

Figure 6 shows the empirical median (6) for each of the ten training/testing experiments, for each of several methods including AICO. Across methods, the scores of the less important variables tend to be (somewhat) more volatile than in the regression setting. SHAP delivers inconsistent and highly unstable rankings, as in the regression case.

Figure 7 reports average computation times across 10 experiments. As in the regression case, AICO achieves an unprecedented degree of computational efficiency. It is more than three orders of magnitude faster than LOCO, the next most efficient testing procedure. AICO is an order of magnitude more efficient than Gaussian knockoffs, the fastest screening procedure. It is more than three orders of magnitude faster than permutation importance, the fastest algorithmic feature importance measure.

6 Empirical applications

6.1 Credit card default

This section complements our theoretical and numerical results with an empirical application to credit card payment data from 30,000 credit card holders of a Taiwanese card issuer, collected in October 2005.131313The dataset is available at the UCI Machine Learning Repository: https://archive.ics.uci.edu/dataset/350/default+of+credit+card+clients The response variable is a binary indicator of payment default. There are 23 explanatory variables (see Table 7). The dataset was split into training (60%), validation (15%), and testing (25%) sets with class proportions maintained through stratified sampling. Categorical variables are one-hot encoded and continuous variables are standardized (mean 0 and unit variance) based on training set statistics.

| Feature | Data Type | Levels (for Categorical) | Description |

| LIMIT_BAL | Continuous | – | Amount of the given credit (NT dollars). |

| SEX | Categorical | Male, Female | Gender of the cardholder. |

| EDUCATION | Categorical | Graduate school, University, High school, Others | Education level of the cardholder. |

| MARRIAGE | Categorical | Married, Single, Others | Marital status of the cardholder. |

| AGE | Continuous | – | Age of the cardholder (in years). |

| PAY_0 | Categorical | Paid in full, 1 Month delinquent, 8 Months delinquent 9+ Months delinquent | Repayment status in September 2005. |

| PAY_2 | Categorical | Same as PAY_0 | Repayment status in August 2005. |

| PAY_3 | Categorical | Same as PAY_0 | Repayment status in July 2005. |

| PAY_4 | Categorical | Same as PAY_0 | Repayment status in June 2005. |

| PAY_5 | Categorical | Same as PAY_0 | Repayment status in May 2005. |

| PAY_6 | Categorical | Same as PAY_0 | Repayment status in April 2005. |

| BILL_AMT1 | Continuous | – | Amount of bill statement (NT dollars) in September 2005. |

| BILL_AMT2 | Continuous | – | Amount of bill statement (NT dollars) in August 2005. |

| BILL_AMT3 | Continuous | – | Amount of bill statement (NT dollars) in July 2005. |

| BILL_AMT4 | Continuous | – | Amount of bill statement (NT dollars) in June 2005. |

| BILL_AMT5 | Continuous | – | Amount of bill statement (NT dollars) in May 2005. |

| BILL_AMT6 | Continuous | – | Amount of bill statement (NT dollars) in April 2005. |

| PAY_AMT1 | Continuous | – | Amount paid (NT dollars) in September 2005. |

| PAY_AMT2 | Continuous | – | Amount paid (NT dollars) in August 2005. |

| PAY_AMT3 | Continuous | – | Amount paid (NT dollars) in July 2005. |

| PAY_AMT4 | Continuous | – | Amount paid (NT dollars) in June 2005. |

| PAY_AMT5 | Continuous | – | Amount paid (NT dollars) in May 2005. |

| PAY_AMT6 | Continuous | – | Amount paid (NT dollars) in April 2005. |

We implement an XGBoost [chen2016xgboost] classifier using a cross-entropy loss function. We use the area under the ROC curve (AUC) on the validation set as a metric for hyper-parameter optimization. We employ the Optuna package [akiba2019optuna], utilizing the Tree-Structured Parzen Estimator [bergstra2011algorithms], with 250 trials. The search space includes the boosting algorithm, tree-specific settings such as tree depth and minimum child weight, and regularization terms. Class imbalance was mitigated using a scaling weight parameter, and training was capped at 1,000 boosting rounds with early stopping if the validation AUC did not improve for 50 consecutive rounds. The optimal hyper-parameters include a gradient tree boosting algorithm [friedman2001greedy] with an approximation-based tree-building strategy; an L2 regularization parameter (lambda) of 0.2 and an L1 regularization parameter (alpha) of 0.001; a subsampling ratio of 100% (no subsampling); a column sampling ratio for each tree of 65%; a maximum tree depth of six levels; a minimum child weight of two; a learning rate (eta) of 0.05; a minimum loss reduction (gamma) of 0.00004; and a loss-guided tree growth policy.

We train an ensemble of 100 XGBoost models on 100 bootstrap samples of the training data, all using the same hyper-parameters obtained during the tuning phase. Each model was trained for up to 1,000 boosting rounds, with early stopping triggered after 50 rounds of no improvement in the validation AUC. Ensemble predictions are obtained by averaging the outputs of all 100 models. The resulting ensemble model has AUCs of on the training set, on the validation set, and on the test set. (The results are robust with respect to the model. An ensemble of neural networks, for example, yields very similar results.)

As in the classification example of Section 5.2, we use a score function to run the test. We continue to use the baseline and comparison feature specification (5.1), where is the mean of in case feature is continuous. For a categorical variable we take the alternative mode where is the (marginal) support of and is the (empirical) probability mass function of . This specification yields values in the support of a categorical. Here, we treat a categorical variable as a single feature rather than treating the associated one-hot variables separately. Alternatively, if higher resolution is required, we can run the test for each individual level of a categorical.

Table 8 summarizes the test results for ( throughout). The significant features, ranked according to the empirical median (6), are PAY_0 through PAY_6, MARRIAGE, SEX, and AGE. Past delinquencies are significant predictors of future payment default. The more recent the payment record the stronger is the influence of timely payment. The actual monthly bill and payment amounts (e.g., PAY_AMT and BILL_AMT) are not significant. Marital status, gender and age, but not education level, are significant predictors of default, even after controlling for past payment behavior. However, the influence of these variables is relatively small, especially for age (the associated medians are at least an order of magnitude smaller than the medians of the payment records). These results indicate that personal circumstances have a statistically significant influence on borrower behavior, beyond patterns in prior payment.

| AICO, Level | |||||||||||

| P-Value Distribution | Randomized One-Sided CI | Non-Randomized Two-Sided CI | |||||||||

| rank | variable | median | P(reject) | lower | upper | 23.4% | 76.6% | coverage | lower | upper | coverage |

| 1 | PAY_0 | 0.150 | 1.000 | 0.000 | 0.000 | 0.143 | 0.143 | 0.99 | 0.142 | 0.155 | 0.99063 |

| 2 | PAY_2 | 0.121 | 1.000 | 0.000 | 0.000 | 0.117 | 0.117 | 0.99 | 0.116 | 0.125 | 0.99063 |

| 3 | PAY_3 | 0.095 | 1.000 | 0.000 | 0.000 | 0.091 | 0.091 | 0.99 | 0.091 | 0.099 | 0.99063 |

| 4 | PAY_4 | 0.059 | 1.000 | 0.000 | 0.000 | 0.055 | 0.055 | 0.99 | 0.054 | 0.064 | 0.99063 |

| 5 | PAY_5 | 0.037 | 1.000 | 2.520e-322 | 6.423e-322 | 0.035 | 0.035 | 0.99 | 0.035 | 0.039 | 0.99063 |

| 6 | PAY_6 | 0.030 | 1.000 | 1.020e-297 | 2.493e-297 | 0.029 | 0.029 | 0.99 | 0.029 | 0.032 | 0.99063 |

| 7 | MARRIAGE | 0.002 | 1.000 | 3.912e-11 | 4.561e-11 | 0.002 | 0.002 | 0.99 | 0.001 | 0.003 | 0.99063 |

| 8 | SEX | 0.002 | 1.000 | 1.026e-37 | 1.383e-37 | 0.001 | 0.002 | 0.99 | 0.001 | 0.002 | 0.99063 |

| 9 | AGE | 3.796e-04 | 1.000 | 1.788e-09 | 2.056e-09 | 2.200e-04 | 2.204e-04 | 0.99 | 2.036e-04 | 5.814e-04 | 0.99063 |

| - | LIMIT_BAL | 0.000 | 0.000 | 0.794 | 0.800 | 0.000 | 0.000 | 0.99 | 0.000 | 3.603e-04 | 0.99496 |

| - | BILL_AMT1 | -0.006 | 0.000 | 1.000 | 1.000 | -0.007 | -0.007 | 0.99 | -0.008 | -0.005 | 0.99063 |

| - | BILL_AMT2 | -0.001 | 0.000 | 1.000 | 1.000 | -0.002 | -0.002 | 0.99 | -0.002 | -9.540e-04 | 0.99063 |

| - | BILL_AMT3 | 0.000 | 0.000 | 0.975 | 0.976 | -1.599e-04 | -1.592e-04 | 0.99 | -1.751e-04 | 5.542e-05 | 0.99063 |

| - | BILL_AMT4 | -4.094e-04 | 0.000 | 1.000 | 1.000 | -5.298e-04 | -5.284e-04 | 0.99 | -5.504e-04 | -2.773e-04 | 0.99063 |

| - | BILL_AMT5 | -3.203e-04 | 0.000 | 1.000 | 1.000 | -5.070e-04 | -5.054e-04 | 0.99 | -5.220e-04 | -1.887e-04 | 0.99063 |

| - | BILL_AMT6 | -1.176e-04 | 0.000 | 1.000 | 1.000 | -2.041e-04 | -2.023e-04 | 0.99 | -2.160e-04 | -3.890e-05 | 0.99063 |

| - | PAY_AMT1 | -0.012 | 0.000 | 1.000 | 1.000 | -0.014 | -0.014 | 0.99 | -0.014 | -0.010 | 0.99063 |

| - | PAY_AMT2 | -0.008 | 0.000 | 1.000 | 1.000 | -0.009 | -0.009 | 0.99 | -0.010 | -0.007 | 0.99063 |

| - | PAY_AMT3 | -0.006 | 0.000 | 1.000 | 1.000 | -0.006 | -0.006 | 0.99 | -0.006 | -0.005 | 0.99063 |

| - | PAY_AMT4 | -3.764e-04 | 0.000 | 1.000 | 1.000 | -5.811e-04 | -5.779e-04 | 0.99 | -5.998e-04 | -1.935e-04 | 0.99063 |

| - | PAY_AMT5 | -0.002 | 0.000 | 1.000 | 1.000 | -0.002 | -0.002 | 0.99 | -0.002 | -0.002 | 0.99063 |

| - | PAY_AMT6 | -0.001 | 0.000 | 1.000 | 1.000 | -0.002 | -0.001 | 0.99 | -0.002 | -0.001 | 0.99063 |

| - | EDUCATION | -3.891e-04 | 0.000 | 0.848 | 0.853 | -0.001 | -0.001 | 0.99 | -0.001 | 4.611e-04 | 0.99063 |

We can further explore the role of a feature by running the test on subsets of the test set. For example, Table 9 reports the results for a test on the 4,029 (out of 7,500) samples for which . While EDUCATION is not significant at the level, it is significant at the level (the distribution of the -value is concentrated below ). Furthermore, EDUCATION is insignificant when running the test on the samples for which (results available on request). This means educational level is a significant predictor of default for an unmarried borrower but not a married one.

| AICO, Conditional on MARRIAGE = Single, Level | |||||||||||

| P-Value Distribution | Randomized One-Sided CI | Non-Randomized Two-Sided CI | |||||||||

| rank | variable | median | P(reject) | lower | upper | 83.0% | 17.0% | coverage | lower | upper | coverage |

| 1 | PAY_0 | 0.151 | 1.000 | 1.833e-248 | 5.763e-248 | 0.143 | 0.143 | 0.99 | 0.142 | 0.158 | 0.99023 |

| 2 | PAY_2 | 0.130 | 1.000 | 0.000 | 0.000 | 0.125 | 0.125 | 0.99 | 0.124 | 0.136 | 0.99023 |

| 3 | PAY_3 | 0.100 | 1.000 | 1.072e-295 | 3.822e-295 | 0.095 | 0.095 | 0.99 | 0.095 | 0.105 | 0.99023 |

| 4 | PAY_4 | 0.063 | 1.000 | 1.402e-260 | 4.555e-260 | 0.056 | 0.057 | 0.99 | 0.056 | 0.069 | 0.99023 |

| 5 | PAY_5 | 0.040 | 1.000 | 4.099e-183 | 1.071e-182 | 0.037 | 0.037 | 0.99 | 0.037 | 0.044 | 0.99023 |

| 6 | PAY_6 | 0.029 | 1.000 | 3.112e-171 | 7.848e-171 | 0.028 | 0.028 | 0.99 | 0.027 | 0.031 | 0.99023 |

| 7 | AGE | 0.002 | 1.000 | 2.601e-48 | 4.147e-48 | 0.002 | 0.002 | 0.99 | 0.002 | 0.002 | 0.99023 |

| 8 | SEX | 0.001 | 1.000 | 1.972e-16 | 2.560e-16 | 0.001 | 0.001 | 0.99 | 0.001 | 0.002 | 0.99023 |

| - | LIMIT_BAL | -4.292e-04 | 0.000 | 1.000 | 1.000 | -0.002 | -0.002 | 0.99 | -0.002 | 0.000 | 0.99511 |

| - | BILL_AMT1 | -0.005 | 0.000 | 1.000 | 1.000 | -0.007 | -0.007 | 0.99 | -0.007 | -0.003 | 0.99023 |

| - | BILL_AMT2 | -0.001 | 0.000 | 1.000 | 1.000 | -0.002 | -0.002 | 0.99 | -0.002 | -8.918e-04 | 0.99023 |

| - | BILL_AMT3 | 4.366e-05 | 0.000 | 0.376 | 0.388 | -1.597e-05 | -1.038e-05 | 0.99 | -3.777e-05 | 2.814e-04 | 0.99023 |

| - | BILL_AMT4 | -4.339e-04 | 0.000 | 1.000 | 1.000 | -6.109e-04 | -6.105e-04 | 0.99 | -6.237e-04 | -2.882e-04 | 0.99023 |

| - | BILL_AMT5 | -1.737e-04 | 0.000 | 1.000 | 1.000 | -3.338e-04 | -3.327e-04 | 0.99 | -3.612e-04 | -3.330e-05 | 0.99023 |

| - | BILL_AMT6 | -1.147e-04 | 0.000 | 1.000 | 1.000 | -2.326e-04 | -2.315e-04 | 0.99 | -2.509e-04 | 0.000 | 0.99474 |

| - | PAY_AMT1 | -0.014 | 0.000 | 1.000 | 1.000 | -0.015 | -0.015 | 0.99 | -0.016 | -0.011 | 0.99023 |

| - | PAY_AMT2 | -0.010 | 0.000 | 1.000 | 1.000 | -0.012 | -0.012 | 0.99 | -0.012 | -0.009 | 0.99023 |

| - | PAY_AMT3 | -0.006 | 0.000 | 1.000 | 1.000 | -0.008 | -0.008 | 0.99 | -0.008 | -0.005 | 0.99023 |

| - | PAY_AMT4 | -4.392e-04 | 0.000 | 1.000 | 1.000 | -7.181e-04 | -7.118e-04 | 0.99 | -7.488e-04 | -1.825e-04 | 0.99023 |

| - | PAY_AMT5 | -0.002 | 0.000 | 1.000 | 1.000 | -0.003 | -0.003 | 0.99 | -0.003 | -0.002 | 0.99023 |

| - | PAY_AMT6 | -0.002 | 0.000 | 1.000 | 1.000 | -0.002 | -0.002 | 0.99 | -0.002 | -0.001 | 0.99023 |

| - | EDUCATION | 0.001 | 0.000 | 0.012 | 0.013 | -7.817e-05 | -4.987e-05 | 0.99 | -2.034e-04 | 0.002 | 0.99023 |

In the US, marital status, gender and age are protected Characteristics under Fair Lending laws, so these variables are not used (they might not even be collected) to construct default probability estimates or credit scores for purposes of credit underwriting. Our results indicate, within the context of Taiwanese borrowers, that these attributes represent signals useful for risk prediction. All else equal, a score constructed without this set of variables might be less accurate.

6.2 Mortgage risk

We next consider AICO feature significance for a more complex classification model trained to predict the state of a mortgage loan in the next month given a history of a time-varying feature vector available at the beginning of the month. The 7 states are Current, 30 Days Delinquent, 60 Days Delinquent, 90+ Days Delinquent, Foreclosure, Paid Off, and Real Estate Owned. The analysis is based on an extensive panel dataset of mortgages from 4 ZIP codes in the greater Los Angeles area which are tracked monthly between 1/1994 and 12/2022 (this is a subset of the commercial CoreLogic Loan-Level Market Analytics dataset). The feature vector is of dimension , and includes variables such as the current state, FICO credit score, loan balance, current interest rate, market interest rate, unemployment rate, etc., many of which are time-varying.

We use the data filtering procedure of \citeasnoundlmr, resulting in roughly 5 million loan-month transitions from 117,523 active loans. The train/validation/test splits are as follows: 1/1994 - 6/2009, 7/2009 - 12/2009, and 1/2010 - 12/2022. We adopt the set-sequence model of \citeasnounelliot with LongConv [elliot-seq] for the sequence layer, which represents the current state of the art for mortgage transition data. We closely follow the training, validation and testing approach of \citeasnounelliot.

We use the feature effect grouping approach discussed in Section 2.2 for panel data, where a unit is a mortgage loan. The panel is unbalanced because loans enter the dataset at different times and are observed for different time periods. The negative multi-class cross-entropy loss is used as the score function , leading to a test of feature importance jointly for transitions between all states. Alternative formulations are possible; for example, we could target specific transitions (e.g. current to prepayment). Baseline and comparison features are chosen as in Section 6.1, at the level of a group.

Table 10 summarizes the test results for (). In line with expectations, the most important feature by far is the current state of the mortgage. The market mortgage rate is the second most important feature, highlighting the significance of time-varying macro-economic conditions for mortgage borrower behavior. Indeed, borrowers have an incentive to prepay and refinance their mortgage if the market mortgage rate falls below their own current loan interest rate (the latter is ranked eighth). We also recognize path-dependency: the number of times the borrower was current and the number of times the borrower was 30 days delinquent during the past 12 months are highly significant and economically important variables for borrower behavior.

| AICO, Level | |||||||||||

| P-Value Distribution | Randomized One-Sided CI | Non-Randomized Two-Sided CI | |||||||||

| rank | variable | median | P(reject) | lower | upper | 37.5% | 62.5% | coverage | lower | upper | coverage |

| 1 | current_state | 0.560 | 1.000 | 0.000 | 0.000 | 0.557 | 0.557 | 0.99 | 0.556 | 0.564 | 0.99016 |

| 2 | national_mortgage_rate | 0.006 | 1.000 | 5.372e-66 | 6.297e-66 | 0.005 | 0.005 | 0.99 | 0.005 | 0.006 | 0.99016 |

| 3 | pool_insurance_flag_value | 0.005 | 1.000 | 4.345e-314 | 6.182e-314 | 0.005 | 0.005 | 0.99 | 0.005 | 0.005 | 0.99016 |

| 4 | times_current | 0.002 | 1.000 | 5.920e-178 | 7.708e-178 | 0.002 | 0.002 | 0.99 | 0.002 | 0.003 | 0.99016 |

| 5 | times_30dd_value | 0.002 | 1.000 | 0.000 | 0.000 | 0.001 | 0.001 | 0.99 | 0.001 | 0.002 | 0.99029 |

| 6 | loan_age | 7.823e-04 | 1.000 | 3.830e-18 | 4.151e-18 | 5.401e-04 | 5.407e-04 | 0.99 | 5.230e-04 | 0.001 | 0.99016 |

| 7 | lagged_prepayment_rate | 7.518e-04 | 1.000 | 7.103e-127 | 8.870e-127 | 6.730e-04 | 6.732e-04 | 0.99 | 6.662e-04 | 8.298e-04 | 0.99029 |

| 8 | current_interest_rate_value | 6.497e-04 | 1.000 | 3.066e-83 | 3.667e-83 | 5.727e-04 | 5.730e-04 | 0.99 | 5.636e-04 | 7.351e-04 | 0.99016 |

| 9 | inferred_collateral_type_value | 5.229e-04 | 1.000 | 2.792e-43 | 3.173e-43 | 4.318e-04 | 4.318e-04 | 0.99 | 4.231e-04 | 6.206e-04 | 0.99016 |

| 10 | mba_days_delinquent_value | 3.738e-04 | 1.000 | 1.890e-131 | 2.370e-131 | 3.379e-04 | 3.380e-04 | 0.99 | 3.341e-04 | 4.136e-04 | 0.99016 |

| 11 | initial_interest_rate | 2.199e-04 | 1.000 | 1.219e-27 | 1.349e-27 | 1.775e-04 | 1.776e-04 | 0.99 | 1.751e-04 | 2.671e-04 | 0.99016 |

| 12 | times_foreclosure | 2.032e-04 | 1.000 | 2.492e-46 | 2.844e-46 | 1.680e-04 | 1.681e-04 | 0.99 | 1.631e-04 | 2.454e-04 | 0.99029 |

| 13 | original_balance | 1.815e-04 | 1.000 | 4.651e-43 | 5.283e-43 | 1.505e-04 | 1.505e-04 | 0.99 | 1.479e-04 | 2.178e-04 | 0.99016 |

| 14 | prepay_penalty_flag_value | 1.568e-04 | 1.000 | 6.926e-19 | 7.520e-19 | 1.152e-04 | 1.152e-04 | 0.99 | 1.115e-04 | 2.001e-04 | 0.99016 |

| 15 | buydown_flag_value | 1.294e-04 | 1.000 | 3.980e-35 | 4.462e-35 | 1.062e-04 | 1.064e-04 | 0.99 | 1.035e-04 | 1.536e-04 | 0.99016 |

| 16 | fico_score_at_origination | 1.233e-04 | 1.000 | 4.995e-36 | 5.609e-36 | 9.650e-05 | 9.669e-05 | 0.99 | 9.399e-05 | 1.515e-04 | 0.99016 |

| 17 | scheduled_monthly_pi_value | 3.479e-05 | 1.000 | 2.451e-30 | 2.726e-30 | 2.661e-05 | 2.663e-05 | 0.99 | 2.576e-05 | 4.341e-05 | 0.99016 |

| - | original_ltv | 1.874e-05 | 0.000 | 0.017 | 0.018 | -2.449e-06 | -2.418e-06 | 0.99 | -4.904e-06 | 4.245e-05 | 0.99016 |

| - | unemployment_rate | -3.907e-04 | 0.000 | 1.000 | 1.000 | -4.822e-04 | -4.813e-04 | 0.99 | -4.909e-04 | -2.838e-04 | 0.99016 |

| - | current_balance_value | -1.298e-06 | 0.000 | 0.520 | 0.524 | -3.206e-05 | -3.195e-05 | 0.99 | -3.507e-05 | 3.639e-05 | 0.99016 |

| - | scheduled_principal_value | -7.242e-06 | 0.000 | 1.000 | 1.000 | -1.134e-05 | -1.133e-05 | 0.99 | -1.176e-05 | -3.263e-06 | 0.99016 |

| - | convertible_flag_value | -1.886e-04 | 0.000 | 1.000 | 1.000 | -2.477e-04 | -2.476e-04 | 0.99 | -2.533e-04 | -1.270e-04 | 0.99016 |

| - | io_flag_value | -2.458e-04 | 0.000 | 1.000 | 1.000 | -2.948e-04 | -2.946e-04 | 0.99 | -2.989e-04 | -2.044e-04 | 0.99016 |

| - | negative_amortization_flag_value | 9.342e-05 | 0.000 | 0.015 | 0.015 | -7.297e-06 | -6.803e-06 | 0.99 | -1.626e-05 | 2.213e-04 | 0.99016 |

| - | original_term_value | -1.047e-04 | 0.000 | 0.999 | 0.999 | -1.854e-04 | -1.852e-04 | 0.99 | -1.936e-04 | -1.765e-05 | 0.99016 |

| - | times_60dd | -3.928e-04 | 0.000 | 1.000 | 1.000 | -5.032e-04 | -5.024e-04 | 0.99 | -5.118e-04 | -2.708e-04 | 0.99016 |

| - | times_90dd | -4.781e-04 | 0.000 | 1.000 | 1.000 | -5.630e-04 | -5.630e-04 | 0.99 | -5.723e-04 | -3.823e-04 | 0.99016 |

| - | lagged_foreclosure_rate | -1.049e-04 | 0.000 | 0.998 | 0.998 | -1.769e-04 | -1.765e-04 | 0.99 | -1.846e-04 | -9.468e-06 | 0.99016 |

Appendix A Proofs of technical results

Proof of Proposition 3.2.

Under Assumption 3.1, where . The Binomial distribution has a monotone likelihood ratio, so the Neyman-Pearson lemma [lehmann2006testing, Theorem 3.4.1] guarantees the existence of a UMP test for the hypotheses

for some . Due to the continuity of , we have so for and these hypotheses are equivalent to (1). The UMP test has test function for some and determined by the requirement that the test’s size be equal to . Formally, for any ,

It follows that and

We clearly have under so and furthermore, . This gives (3). ∎

Proof of Proposition 4.1.

Let and , where for , as in Proposition 3.2. From \citeasnoungeyer-meeden, a randomized CI for is given by the -cut of :

Then, by iterated expectations and the independence of , we get

by (4). (Recall that under .)

Since for , we have

Moreover, note that

Thus is equal to the union of and if and otherwise. ∎

Proof of Proposition 4.2.

Conditional independence implies that

for some function , so does not depend on the first entry of its argument vector. By construction, only differs from at the first entry. Therefore for any pair , and hence the feature effect is identically zero. ∎

Proof of Proposition 4.3.

Letting , under the stated hypotheses we get

With the score function,

Since is deterministic, and is the only source of randomness in ,

By iterated expectations, we conclude that

which completes the proof. ∎

References

- [1] \harvarditem[Ait-Sahalia et al.]Ait-Sahalia, Bickel \harvardand Stoker2001ait-sahalia-bickel Ait-Sahalia, Yacine, Peter Bickel \harvardand Thomas M. Stoker \harvardyearleft2001\harvardyearright, ‘Goodness-of-fit tests for kernel regression with an application to option implied volatilities’, Journal of Econometrics 105, 363–412.

- [2] \harvarditem[Akiba et al.]Akiba, Sano, Yanase, Ohta \harvardand Koyama2019akiba2019optuna Akiba, Takuya, Shotaro Sano, Toshihiko Yanase, Takeru Ohta \harvardand Masanori Koyama \harvardyearleft2019\harvardyearright, Optuna: A next-generation hyperparameter optimization framework, in ‘Proceedings of the 25th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining’, pp. 2623–2631.

- [3] \harvarditem[Alam et al.]Alam, Boardman, Huang \harvardand Turner2022boardman Alam, Md Shafiul, Jonathan Boardman, Xiao Huang \harvardand Matthew Turner \harvardyearleft2022\harvardyearright, Applications of integrated gradients in credit risk modeling, in ‘2022 IEEE International Conference on Big Data (Big Data)’, pp. 4997–5005.

- [4] \harvarditemAsmussen \harvardand Glynn2007asmussen-glynn Asmussen, Soren \harvardand Peter Glynn \harvardyearleft2007\harvardyearright, Stochastic Simulation: Algorithms and Analysis, Springer.

- [5] \harvarditem[Bates et al.]Bates, Candés, Janson \harvardand Wang2021bates Bates, Stephen, Emmanuel Candés, Lucas Janson \harvardand Wenshuo Wang \harvardyearleft2021\harvardyearright, ‘Metropolized knockoff sampling’, Journal of the American Statistical Association 116(535), 1413–1427.

- [6] \harvarditemBellot \harvardand Schaar2019bellot Bellot, Alexis \harvardand Mihaela van der Schaar \harvardyearleft2019\harvardyearright, Conditional independence testing using generative adversarial networks, in ‘Proceedings of the 33rd International Conference on Neural Information Processing Systems’, pp. 2202 – 2211.

- [7] \harvarditemBenjamini \harvardand Hochberg1995benjamini1995controlling Benjamini, Yoav \harvardand Yosef Hochberg \harvardyearleft1995\harvardyearright, ‘Controlling the false discovery rate: a practical and powerful approach to multiple testing’, Journal of the Royal Statistical Society: Series B (Methodological) 57(1), 289–300.