On Dequantization of Supervised Quantum Machine Learning via Random Fourier Features

Abstract

In the quest for quantum advantage, a central question is under what conditions can classical algorithms achieve a performance comparable to quantum algorithms–a concept known as dequantization. Random Fourier features (RFFs) have demonstrated potential for dequantizing certain quantum neural networks (QNNs) applied to regression tasks, but their applicability to other learning problems and architectures remained unexplored. In this work, we derive bounds on the generalization performance gap between classical RFF models and quantum models for regression and classification tasks with both QNN and quantum kernel architectures. We support our findings with numerical experiments that illustrate the practical dequantization of existing quantum kernel-based methods. Our findings not only broaden the applicability of RFF-dequantization but also enhance the understanding of potential quantum advantages in practical machine-learning tasks.

I Introduction

Supervised quantum machine learning (QML) models such as quantum kernel (QK) methods [1, 2] and quantum neural networks (QNNs) [3, 4] have recently gained significant attention with the fundamental objective of seeking advantages over classical machine learning methods. In parallel, one line of research known as dequantization aims to find efficient classical algorithms that can perform as well as QML models for certain tasks [5, 6, 7, 8]. These efforts both provide valuable insights into the potential advantages of QML and support the development of improved classical algorithms.

Random Fourier features (RFF) is a classical algorithm which has attracted attention as a potential dequantization method due to its simplicity and thorough study [9, 10, 11, 12].

It was first introduced by Ref. [13] to approximate shift-invariant kernels, a family of kernels depending only on the difference between the two inputs (e.g. the Gaussian kernel). The central idea is to construct a feature map by sampling from the Fourier transform of the target kernel. This feature map can be used to approximate the kernel or can be directly used in various classical machine learning tasks such as Ridge Regression (RR) and Support Vector Machines (SVMs).

RFF is particularly suited for the dequantization of a common class of supervised QML models that are known to have a finite Fourier series representation [14, 15]. However, among the two most typical supervised QML models, i.e., QNNs [3, 4] and QKs [1, 2], the use of RFF for dequantization has been limited to QNNs so far. For instance, Ref. [7] used RFF to dequantize QNN regression tasks and provided bounds on the difference between the optimal RFF and QNN decision functions. Subsequently, Ref. [8] derived a bound on the generalization performance of a QNN and the RFF algorithm for a regression problem. Nevertheless, the potential of RFF for the dequantization of QKs and for other learning tasks such as SVM classification remains unexplored. For more details about related works see App. A.

In this work, we extend the RFF-dequantization to a broader class of supervised QML including QK regression, SVMs with QKs (QSVM) and QNNs with SVM loss (QNN-SVM), as summarized in Table 1. Concretely, we adapt RFF to non-stationary kernels and propose sufficient conditions for RFF-dequantization, i.e., for when RFF can efficiently reach a true risk comparable to that of the QML models. Finally, we compare the performance of RFF with QSVM on a dataset of particle collisions. We further provide numerical experiments to show dequantization in practice with our RFF algorithm performing similarly to a QML model on a real-world dataset.

II Preliminaries

We denote vectors with boldface small letters () and matrices with capital letters (). Transpose and complex conjugate transpose of are represented as and . , and denote expected values, inner product and trace, respectively. For the matrix and vector norm, we use the notation , which corresponds to , (Frobenius), and infinity (Spectral) norm for , respectively. Note that the matrix norms here are not induced norms but Schatten norms. represents the norm of a Hilbert space . For the quantum systems, we use the Dirac notations. That is, represents a complex-valued vector while denotes its complex conjugate. Then, represents the inner product of two complex-valued vectors.

II.1 Classical Framework

Supervised Learning.

Let and be some unknown distribution and a set of functions mapping to , called hypothesis class, respectively. Given a set of independent identically distributed (i.i.d.) samples from and a (positive) loss function , supervised learning aims to minimize the true risk defined as over . However, since is unknown, learning algorithms work with the sample mean of the true risk over , known as empirical risk. Some learning algorithms map the input data to a Hilbert space called feature space using a feature map , so that the structure of data can be captured better.

Kernels.

A kernel function , or simply a kernel, is a symmetric and real-valued function used for measuring the similarity between a pair of data points and . Any kernel can be written as the inner product of a feature map in a Hilbert space i.e. . For any function that can be represented by the feature map of a kernel, i.e. , the RKHS norm of is defined as .

When a kernel’s output depends solely on the difference between the two inputs, it is called a shift-invariant (stationary) kernel.

Definition II.1 (Shift-invariant Kernel).

A shift-invariant kernel is a kernel on such that . Shift-invariant kernels are also called stationary kernels. On the other hand, the kernels that are not shift invariant are called non-stationary kernels.

A common example of a shift-invariant kernel is the Gaussian kernel . However, as we will see, most QKs are non-stationary.

Support Vector Machines.

SVMs are a widely used machine learning method for classification tasks. The main idea is to find a hyperplane in the feature space that maximizes the margin. That is, one seeks to minimize the regularized hinge loss,

| (1) |

where is a regularization hyperparameter that controls the separability of data (soft or hard margin). The dual problem can be solved by only dealing with the inner products of the input feature map pairs i.e. a corresponding kernel . This allows for the application of various kernel functions in SVMs without having access to or even knowing the underlying feature map. For more information on SVMs see App. B.4.

Linear Regression.

Linear Ridge Regression seeks to minimize the mean squared error loss between the data labels and the trainable labels . In other words, it seeks to solve the optimization problem

| (2) |

where again the real positive parameter serves as regularization. Similar to a kernel SVM, a kernel function can be used to solve the corresponding dual problem instead.

Random Fourier Features.

According to Bochner’s theorem (Thm. B.4), every bounded, normalized, continuous and shift-invariant kernel can be written as

| (3) |

where and is a probability distribution obtained by normalizing the Fourier transform of the kernel. RFF algorithm estimates this expectation using samples from the distribution. More precisely, given i.i.d. samples, , from the distribution , we can generate the random Fourier feature map,

| (4) |

The feature map can be used with high probability to construct the approximate kernel with a point-wise error no more than , if we choose where [13]. For more details on RFF, see App. B.5.

II.2 Quantum Framework

Quantum Kernels.

Quantum Neural Networks.

QNNs are parametrized quantum models where trainable parameters are optimized to minimize the loss for a learning problem. They typically consist of layers of data encoding followed by parametrized gates (unitary transformations) and then the measurement of an observable . More concretely, the output of a QNN can be written as

| (6) |

Here is an -layered circuit where is a parameterized unitary with a vector of trainable parameters and the are fixed unitaries that encode the input into the circuit. In the training phase of QNNs, the output function is evaluated on a quantum computer, as queried by an optimization performed on a classical computer. These models have been used for both regression [16, 3] and SVM classification [17, 18].

RFF Dequantization.

Throughout this work, we employ the following common encoding strategy, which we call a Hamiltonian encoding [14, 15].

Assumption II.2.

We assume that the QML model uses a Hamiltonian encoding, where a gate in the -th layer that encodes -th element of data is represented as for a Hermitian matrix .

It is known that QNNs using this type of encoding have the following Fourier representation [19]:

| (7) | ||||

where the frequency support of the encoding, , depends on the encoding Hamiltonians only and always contains . Also, it is symmetric around zero, i.e., . For ease of notation, we denote a subset containing only positive frequencies as without frequency zero. A detailed description of is presented in App. B.3.

Note that the output of a QNN in Eq. (7) can be written as the inner product between a vector of Fourier coefficients and the QNN feature map defined as

| (8) |

This means that the hypothesis class of a QNN can be represented by a cosine feature map. Consequently, RFF presents itself as a natural method for the dequantization of such models. This was originally highlighted in Ref. [7] which used the random Fourier feature map (Eq. (4)) to dequantize QNN for regression tasks, using the techniques in Ref. [10].

Subsequently, Ref. [8] employed the learning errors provided by Ref. [20] and bounded the gap between the true risk of the RFF empirical risk minimizer and the QNN true risk minimizer for ridge regression problems. These bounds depend on the properties of the sampling distribution and are then used to derive sufficient conditions under which RFF can match the performance of QNNs with efficient resources. We will discuss these conditions later in Sec. III.1, but before that, let us follow Ref. [8] and formalize RFF-dequantization as follows. For more details about related works see App. A.

Definition II.3 (RFF Dequantization).

Consider a supervised learning task with a training dataset . Given a quantum model (either a QNN or QK) with hypothesis class , denotes the true risk minimizer of the quantum model i.e. . We say the task is RFF-dequantized, if there exists a distribution such that for some , with , the following is true with high probability:

| (9) |

Here, is the decision function of the task trained with a dimensional RFF feature map (Eq. 4) sampled from and denotes the true risk.

Informally, we say the task is RFF-dequantized, if the performance of RFF with polynomial resources is not much worse than the best possible QML model.

III RFF Dequantization of QML models

In the context of the dequantization of QML models via RFF, there are two main issues that can be explored. The first is whether RFF can approximate quantum kernels. This is motivated by the observation that, if a good approximation can be found, a similar performance is achievable using the approximate kernel [10]. Since QKs are non-stationary in general, the original RFF approximation algorithm does not apply to them directly. However, we can use similar ideas. Namely, we express a QK in the form of Eq. (3) for some and then replace the expectation with the sample mean.

Lemma III.1.

Although is diagonal if and only if the kernel is shift invariant, the diagonal elements of always form a valid probability mass function. That is, they are all non-negative (the positive semi-definite property of ) and sum to one (the unit-trace property of ). This motivates the following definition.

Definition III.2 (Kernel distribution).

Given a Hamiltonian-encoded QK in Eq. (10), we call its Fourier transform and its frequency support. We also define the diagonal distribution (probability mass function) of the kernel as the diagonal elements of its Fourier transform, i.e., .

With the property in Lem. III.1, we propose a RFF algorithm for approximating non-stationary kernels with a discrete Fourier spectrum (Alg. 3) in App. C. The main idea of this scheme is to sample frequencies from eigenvalues and eigenvectors of . We show that frequency samples are required to reach point-wise error with high probability, which is consistent with the bound for shift-invariant kernels introduced in Ref. [13]. However, the number of frequencies in scales exponentially with , the dimension of input data. This suggests prohibitive computational costs to obtain even for relatively small system sizes.

Nonetheless, the ability to efficiently approximate the kernel is only a sufficient but not necessary condition to outperform a given QML model using RFF. This leads us to the second, and arguably more important, issue - the possibility of dequantization (Def. II.3). That is, can a classical algorithm using random Fourier features have a generalization performance comparable to that of QML methods? We will thus proceed to discuss the dequantization of QML models with RFF methods for regression and SVM classification.

We begin with a brief review of the sufficient conditions for QNN regression established in Ref. [8] and introduce a new condition for QK regression (Sec. III.1.2). Then, we provide sufficient conditions for SVM classification tasks using QKs (Sec. III.2.1) and QNN-SVM (Sec. III.2.2). This is summarized in Table 1.

III.1 Dequantization for Regression

III.1.1 QNN Regression by Ref. [8]

Bounds on the difference between the true risk of RFF ridge regression and QNN regression were derived in Ref. [8]. These were then used to provide the following set of sufficient conditions for regression using QNNs to be RFF-dequantizable with a distribution .

-

•

Sampling Efficiency: The distribution is easy to sample from.

-

•

Concentration: The maximum of the distribution scales inversely polynomial the problem size i.e., .

-

•

Alignment: where are the Fourier coefficients of the best quantum model (Eq. (7)).

The sampling efficiency condition is clearly essential for the RFF algorithm to be viable. Given this, we do not explicitly mention it in our technical results shown hereafter.

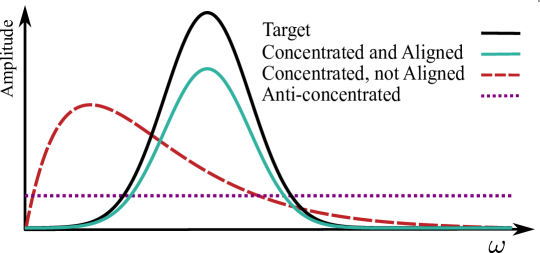

The concentration condition suggests that should not be very “flat” or close to uniform over . Namely, if the sampling distribution is very close to uniform, is exponential in .

The alignment condition indicates that a frequency that is more prominent in , should be proportionally more probable to be in the RFF feature map. We note that this condition appears differently in Ref. [8]. The original form of this condition is where is the kernel whose Fourier transform is distribution (defined in Eq. (3)). Yet, as the distribution can be regarded a hyperparameter of RFF, we can minimize over choices of . By doing so, we obtain the alignment condition as presented above; see App. D for more details. Fig. 1 provides a visual sketch of the interplay of the concentration and alignment conditions.

III.1.2 QK Regression

Here, we provide a set of sufficient conditions for RFF to dequantize (Def. II.3) QK regression. Our complete proof, which required extending RFF to non-stationary kernels, is provided in App. E.

Proposition III.3 (Sufficient conditions for RFF dequantization of QK regression).

Consider a regression task using a quantum kernel with Fourier transform . Then, the linear ridge regression with the RFF feature map (Eq. (4)) sampled according to distribution dequantizes the QK ridge regression if:

-

•

Concentration:

-

•

Alignment: where is a diagonal matrix with as its diagonal

-

•

Bounded RKHS norm: where is the true risk minimizer of kernel regression.

Indeed, the conditions we have found here for the dequantization of QK regression are relatively similar to those for QNN regression in Sec. III.1.1. In particular, the concentration conditions are identical in both cases. In contrast, the alignment condition has a different form and there is an additional condition on the RKHS norm that does not depend on the sampling distribution . Below, we discuss these conditions more in depth.

To gain an intuition for the alignment condition in this case, let us start considering the case where the QK is shift invariant. If is shift invariant then is diagonal and then, as shown in Lem. E.7 of the App. E, a sampling distribution completely aligned with the kernel () minimizes and the form of the condition reduces to the alignment condition for QNN regression. In this manner, the alignment condition here can be viewed as a generalization of the alignment condition in Ref. [8] to non-stationary kernels.

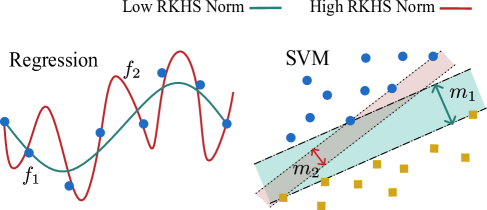

We stress that the RKHS norm condition applies to the norm of the optimal decision function of the QML model with respect to the QK . Intuitively, when this norm is large, the model is too complex, as sketched in Fig. 2, and the generalization may be poor [21]. In other words, QML models that do not satisfy the first condition are likely to have a bad performance in the first place and not be of interest for dequantization. Thus, this final condition can be seen as a condition to ensure a good performance for the QML model in the first place.

III.2 Dequantization for SVM Classification

We now proceed to extend the results of RFF dequantization to SVM classification. That is, we consider what changes when optimizing the hinge loss (Eq. (1)) instead of the mean square error loss (Eq. (2)). Similarly to regression models, we consider two types of QML models: QSVM and QNN-SVM. The former solves the dual SVM problem with a kernel matrix evaluated on a quantum computer, whereas the latter solves the primal SVM problem with the output of a QNN as a parametrized, trainable decision boundary. To dequantize the QML models, we introduce an RFF-based SVM algorithm inspired by Ref. [9] and then propose a set of sufficient conditions for dequantization.

III.2.1 Quantum SVM

First, we discuss our proposed RFF algorithm for SVM, Alg. 1, which is inspired by Ref. [9]. This algorithm takes a distribution over frequencies as input and samples from it to construct a random cosine feature map in Eq. (4). The SVM optimization problem is then solved with this feature map (See Alg. 1). The search radius , which appears as a constraint in optimization, plays a pivotal role in our theoretical analysis. However, in practice, it just needs to be chosen as a sufficiently large number. The generalization analysis of this algorithm is presented in App. F.

The following sufficient conditions for RFF-dequantization of QSVM are derived in App. G.

Proposition III.4 (Sufficient Conditions for RFF dequantization of QSVM).

Prop. III.4 implies that RFF can dequantize QSVM problems under a broadly similar set of conditions as regression. The biggest difference between the cases of SVM and regression is found in the square root appearing in the first two conditions; however, they do still intuitively capture concentration and alignment respectively.

To illustrate how the first condition captures concentration, let us consider two examples of distributions: delta function and uniform distribution. For the delta distribution on frequency zero, the measure is showing maximum concentration. For a uniform distribution, the concentration measure is which is exponential in showing anti-concentration. Moreover, this concentration measure is closely related to -Rényi entropy of the diagonal distribution defined as . In particular, this entropy is an upper bound for the tail of the distribution [22] further emphasizing its role as a concentration measure.

The second condition here implies that the optimal sampling distribution for the dequantization of QSVM should be proportional to the square root of the diagonal distribution. This arises from the fact that we use bounds provided by Ref. [9], which only works for Lipschitz loss functions such as SVMs. On the other hand, the bounds provided by Ref. [20] are used in Sec. III.1, because the regression task deals with the non-Lipschitz mean square loss. Nonetheless, the condition here can still be viewed as an alignment condition. We further suspect, but have not been able to prove, that the alignment condition in Prop. III.3 would also suffice in this case.

Finally, similarly to in Prop. III.3, we require the RKHS norm of the true risk minimizer to be polynomially bounded. In fact, this condition on the RKHS norm has a more immediate interpretation in the current SVM case as this norm is proportional to the inverse of the SVM margin. Thus this condition states that we need the data in the feature space to be separable with a margin that decreases at worst inverse polynomially in .

III.2.2 QNN-SVM

Lastly, we move on to the dequantization of QNN-SVM. The following proposition is proved as Prop. G.7 of the App. E.

Proposition III.5 (Sufficient Conditions for RFF dequantization of QNN-SVM).

This proposition shows that for QNN-SVMs, despite the difference in loss function and the learning bounds used, we have the same alignment condition as Ref. [8]. The second condition is a bound on the 1-norm of the vector of Fourier coefficients of . Compared to the bound on the RKHS norm (equal to the 2-norm of ) which appears in Props. III.3 and III.4, it is related, but stricter:

Overall, Props. III.3, III.4 and III.5 suggest that the possible advantage of QML models with Hamiltonian encodings lies where the QML model performs well and has an anti-concentrated Fourier spectrum, or at least a spectrum complex enough such that it is hard to sample from its corresponding Fourier spectrum. In all other cases, it is theoretically possible to dequantize QNN and QK regression and classification tasks.

That said, it is important to stress that these theoretical guarantees are in several ways not of practical use. In particular, our definition of dequantization (Def. G.1), following that in Ref. [8], requires only the existence of a sampling strategy where RFF performs as well as the QML model, not that this distribution is known. Moreover, the sufficient conditions require this distribution to be aligned with the Fourier transform of the QK or the decision function of the QNN. Computing the Fourier transform of a QML model in general either requires an exponential (in the data dimensionality ) number of calls to a quantum computer or exponential (in the number of qubits ) classical memory. Even if the Fourier transform is known, there is no guarantee that the aligned distribution is easy to sample from. An interesting question is whether QML models can dequantized using RFF distributions that are independent or loosely dependent on the kernel and easy to sample from. To probe this question we provide some numerical results in the next section.

IV Numerical experiments

In this section, we investigate when QML models can be dequantized using RFF in practice. There are two key features of practical implementations of RFF and QNNs/QKs that are not captured by our theoretical analysis above. Firstly, as just discussed, we do not have access to the optimal RFF sampling distribution. Therefore, we look at the performance of RFF with simple, easy-to-sample-from, distributions that are loosely dependent on, or inspired by, the QK. Secondly, our analysis above compared the performance of RFF to the performance of QNNs/QKs assuming access to the exact loss/kernel values. However, in practice, as these will be measured on a quantum computer, we only ever have estimates of these values computed from a finite number of shots. Since the loss functions of QNNs and QC values often concentrate exponentially to some fixed data independent point [23, 24, 25], the unavoidability of shot noise can have a significantly detrimental effect on the quantum model performance.

For brevity, we focus here on QSVMs using QKs but the other cases are explored in App. H. For concreteness, we compare the performance of QSVMs with RFF-SVMs using data from high-energy physics. In particular, we use the dataset of Ref. [26] which consists of simulated proton-proton collisions. It includes a mix of Standard Model (SM) and Beyond Standard Model (BSM) processes, with numerous features simulated using Monte Carlo, whose dimension is reduced to 16, 32, and 64 with auto-encoders. Ref. [26] use this dataset for anomaly detection with QSVM. Here, we use the dataset for two-class classification with SVM, using a QK inspired by the same work that is detailed in Fig. 8 of the App. H. More details about the dataset and implementation are provided in App. H.

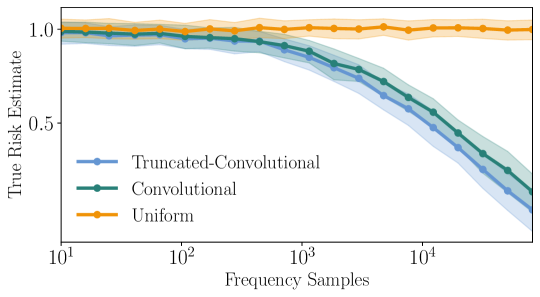

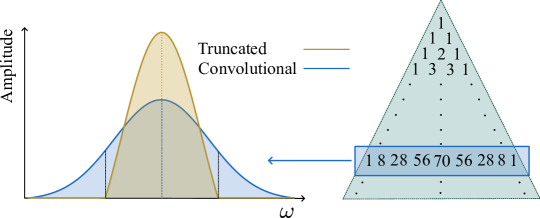

We consider three separable RFF sampling distributions. First, we use the “uniform” distribution over the set of all possible frequencies. Secondly, we use the fact that for QKs, lower frequencies are, on average, more likely to appear than higher ones. More precisely, the frequency profile has been shown to be the result of the convolution of the spectrum of the generators of the encoding [27]. For the kernel considered here, this yields the line from Pascal’s triangle with the same number of elements as the number of frequencies available for each dimension. We call this “convolutional” sampling (equivalent to Tree sampling in Ref. [7]). Thirdly, we cut the upper half of the frequency support from the convolutional distribution, and call it “truncated-convolutional” sampling. A sketch of these three sampling strategies is provided in Fig. 4 in the Appendices.

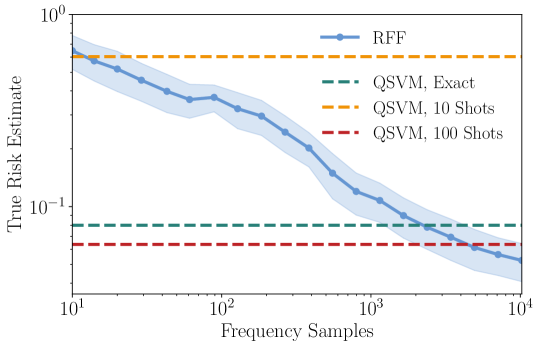

Fig. 3 shows a comparison between these three distributions. The uniform distribution fails, as predicted by Ref. [8]. Our proposed method of truncated-convolutional sampling method performs slightly better than the convolutional method on this data. The reason is that the number of frequencies in the frequency support increases exponentially with and so the support of the truncated distribution is exponentially smaller than the full support. Consequently, if the dataset consists of low frequencies, the truncated support has a much higher chance of sampling the relevant frequencies. This implies that a dataset that can not be represented only by low frequencies is a better candidate to establish the need for quantum computers in classification.

Fig. 5, compares the performance of truncated sampling with QSVM. RFF with truncated sampling can outperform the QSVM with different levels of shot noise. We see that with small shot counts, as expected, much fewer RFF samples are needed to achieve a better performance. Intriguingly, Fig. 5 shows a better performance for QSVM with 100 shots than the exact kernel evaluation. This can be attributed to low levels of shot noise acting like regularization in classical models preventing overfitting.

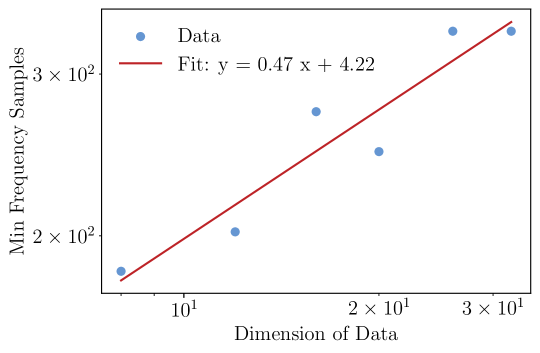

Any claim of dequantization as defined in Def. II.3 requires a scaling analysis over the dimension of the input data. Fig. 6 shows the minimum number of frequency samples for which RFF reaches the estimated risk of 0.15 with respect to the dimension of input data. The fitted line shows a polynomial growth of the resources required by the RFF algorithm, and hence indicates the efficiency of this algorithm on this dataset.

V Conclusion

In this work, we examine the question of whether RFF algorithms can dequantize supervised QML models. Existing work has focused solely on the dequantization of QNN regression, while we extend it to QK methods and SVM classification problems, as summarized in Table 1. Specifically, our Props. III.3, III.4, III.5 provide conditions under which classical algorithms (i.e., RFF) could be comparable to QML models in terms of true risks. Overall our results indicate two conditions for dequantizable quantum machine learning tasks namely alignment and concentration. These results help chisel out the types of problems for which we can hope to find potential quantum advantages for practical learning tasks. The Alignment condition implies that the Fourier spectrum of either the QK (for QK methods) or the QNN optimal decision function (for QNNs) determines the optimal RFF sampling distribution. Therefore, if this optimal distribution is efficient to find or sample from, dequantization can be possible. The concentration condition states that this optimal sampling distribution should be concentrated in some sense to ensure dequantization. For regression tasks this concentration condition manifests as a lower bound on the infinity norm of the distribution and, for QSVM, it puts an upper bound on 1/2-Renyi entropy of the distribution.

While we propose analytical bounds and conditions on dequantization of various quantum models using information from their Fourier transform, our ability to verify these conditions is limited by the computational cost of the Fourier transform. In other words, a full knowledge of the optimal RFF sampling distribution is not practically possible for large circuits. Whether this information can be obtained without the full Fourier transform remains an open question. Nevertheless, even if this optimal distribution can be obtained efficiently, its sampling complexity could still hinder dequantization.

To circumvent this practical issue, we use simple distributions that are easy to sample from. Using a task independent distribution bypasses the need for the Fourier analysis of the quantum circuit. Moreover, the efficiency of the RFF sampling subroutine is ensured by choosing these simple distributions to be separable and easy to sample from. Using practical compressed datasets from high-energy physics, we numerically show that these simplified distributions can outperform QSVM. While this theoretical work compares noiseless quantum models to RFF, numerical experiments show that a low level of shot noise may increase generalization performance. The interplay between shot noise and RFF dequantization remains unexplored.

An exciting direction for future work is extending our results to other types of data encoding. This study focuses on Hamiltonian encoding, a key ingredient to express QML models as finite Fourier series. However, alternative encodings, such as amplitude encoding, result in a continuous frequency space and thus fall outside the scope of our methods. Notably, a well-known QML model with a provable quantum advantage [28] relies on a QK using non-Hamiltonian encoding. Hence, exploring the dequantizability of QML models across various encoding strategies could offer deeper insight into power of RFF for dequantization and potential of quantum advantage.

Acknowledgments

Authors are grateful to Sofiene Jerbi, Daniel Stilck Franca and Elies Gil-Fuster for their valuable feedback on this work. MS, AB and MG are supported by CERN through the CERN Quantum Technology Initiative. AB is supported by the quantum computing for earth observation (QC4EO) initiative of ESA -lab, partially funded under contract 4000135723/21/I-DT-lr, in the FutureEO program. ZH acknowledges support from the Sandoz Family Foundation-Monique de Meuron program for Academic Promotion.

References

- Schuld and Killoran [2019] M. Schuld and N. Killoran, Physical Review Letters 122, 040504 (2019).

- Havl´ıček et al. [2019] V. Havlíček, A. D. Córcoles, K. Temme, A. W. Harrow, A. Kandala, J. M. Chow, and J. M. Gambetta, Nature 567, 209 (2019).

- Benedetti et al. [2019] M. Benedetti, E. Lloyd, S. Sack, and M. Fiorentini, Quantum Science and Technology 4, 043001 (2019).

- Abbas et al. [2021] A. Abbas, D. Sutter, C. Zoufal, A. Lucchi, A. Figalli, and S. Woerner, Nature Computational Science 1, 403 (2021).

- Schreiber et al. [2023] F. J. Schreiber, J. Eisert, and J. J. Meyer, Physical Review Letters 131, 100803 (2023).

- Shin et al. [2024] S. Shin, Y. S. Teo, and H. Jeong, Physical Review Research 6, 023218 (2024).

- Landman et al. [2022] J. Landman, S. Thabet, C. Dalyac, H. Mhiri, and E. Kashefi, arXiv preprint arXiv:2210.13200 (2022).

- Sweke et al. [2025a] R. Sweke, E. Recio-Armengol, S. Jerbi, E. Gil-Fuster, B. Fuller, J. Eisert, and J. J. Meyer, Quantum 9, 1640 (2025a).

- Rahimi and Recht [2008] A. Rahimi and B. Recht, Advances in Neural Information Processing Systems 21 (2008).

- Sutherland and Schneider [2015] D. J. Sutherland and J. Schneider, arXiv preprint arXiv:1506.02785 (2015).

- Avron et al. [2017] H. Avron, M. Kapralov, C. Musco, C. Musco, A. Velingker, and A. Zandieh, in International conference on machine learning (PMLR, 2017) pp. 253–262.

- Li et al. [2019] Z. Li, J.-F. Ton, D. Oglic, and D. Sejdinovic, in International conference on machine learning (PMLR, 2019) pp. 3905–3914.

- Rahimi and Recht [2007] A. Rahimi and B. Recht, Advances in neural information processing systems 20 (2007).

- Schuld [2021] M. Schuld, arXiv preprint arXiv:2101.11020 (2021).

- Shin et al. [2023] S. Shin, Y. Teo, and H. Jeong, Physical Review A 107, 012422 (2023).

- Mitarai et al. [2018] K. Mitarai, M. Negoro, M. Kitagawa, and K. Fujii, Physical Review A 98, 032309 (2018).

- Blance and Spannowsky [2021] A. Blance and M. Spannowsky, Journal of High Energy Physics 2021, 1 (2021).

- Innan et al. [2023] N. Innan, M. A.-Z. Khan, B. Panda, and M. Bennai, Quantum Information Processing 22, 374 (2023).

- Schuld et al. [2021] M. Schuld, R. Sweke, and J. J. Meyer, Physical Review A 103, 032430 (2021).

- Rudi and Rosasco [2017] A. Rudi and L. Rosasco, Advances in Neural Information Processing Systems 30, 1602.04474 (2017).

- Huang et al. [2021] H.-Y. Huang, M. Broughton, M. Mohseni, R. Babbush, S. Boixo, H. Neven, and J. R. McClean, Nature Communications 12, 1 (2021).

- Verstraete and Cirac [2006] F. Verstraete and J. I. Cirac, Physical Review B 73, 094423 (2006).

- McClean et al. [2018] J. R. McClean, S. Boixo, V. N. Smelyanskiy, R. Babbush, and H. Neven, Nature Communications 9, 1 (2018).

- Larocca et al. [2024] M. Larocca, S. Thanasilp, S. Wang, K. Sharma, J. Biamonte, P. J. Coles, L. Cincio, J. R. McClean, Z. Holmes, and M. Cerezo, arXiv preprint arXiv:2405.00781 (2024).

- Thanasilp et al. [2024] S. Thanasilp, S. Wang, M. Cerezo, and Z. Holmes, Nature Communications 15, 5200 (2024).

- Belis et al. [2024] V. Belis, K. A. Wozniak, E. Puljak, P. Barkoutsos, G. Dissertori, M. Grossi, M. Pierini, F. Reiter, I. Tavernelli, and S. Vallecorsa, Communications Physics 7, 10.1038/s42005-024-01811-6 (2024).

- Barthe and Pérez-Salinas [2024] A. Barthe and A. Pérez-Salinas, Quantum 8, 1523 (2024).

- Liu et al. [2021] Y. Liu, S. Arunachalam, and K. Temme, Nature Physics , 1 (2021).

- Nakaji et al. [2022] K. Nakaji, H. Tezuka, and N. Yamamoto, arXiv preprint arXiv:2209.01958 (2022).

- Jerbi et al. [2023] S. Jerbi, L. J. Fiderer, H. Poulsen Nautrup, J. M. Kübler, H. J. Briegel, and V. Dunjko, Nature Communications 14, 517 (2023).

- Gil-Fuster et al. [2024] E. Gil-Fuster, J. Eisert, and V. Dunjko, Machine Learning: Science and Technology 5, 025003 (2024).

- Sweke et al. [2025b] R. Sweke, S. Shin, and E. Gil-Fuster, arXiv preprint arXiv:2503.23931 (2025b).

- Steinwart and Christmann [2008] I. Steinwart and A. Christmann, Support vector machines (Springer Science & Business Media, 2008).

- Rudin [1990] W. Rudin, The basic theorems of fourier analysis, in Fourier Analysis on Groups (John Wiley & Sons, Ltd, 1990) Chap. 1, pp. 1–34.

- Yaglom [1987] A. M. Yaglom, Correlation Theory of Stationary and Related Random Functions, Volume I: Basic Results, Vol. 131 (Springer, 1987).

- Samo and Roberts [2015] Y.-L. K. Samo and S. Roberts, arXiv preprint arXiv:1506.02236 (2015).

- Remes et al. [2017] S. Remes, M. Heinonen, and S. Kaski, Advances in Neural Information Processing Systems 30 (2017).

- Cucker and Smale [2002] F. Cucker and S. Smale, Bulletin of the American mathematical society 39, 1 (2002).

- Kuhn and Tucker [1951] H. W. Kuhn and A. W. Tucker, in Proceedings of the Second Berkeley Symposium on Mathematical Statistics and Probability, 1950 (Univ. California Press, Berkeley-Los Angeles, Calif., 1951) pp. 481–492.

- Boyd and Vandenberghe [2004] S. Boyd and L. Vandenberghe, Convex Optimization (Cambridge University Press, 2004).

- Bergholm et al. [2018] V. Bergholm, J. Izaac, M. Schuld, C. Gogolin, M. S. Alam, S. Ahmed, J. M. Arrazola, C. Blank, A. Delgado, S. Jahangiri, et al., arXiv preprint arXiv:1811.04968 (2018).

- Pedregosa et al. [2011] F. Pedregosa, G. Varoquaux, A. Gramfort, V. Michel, B. Thirion, O. Grisel, M. Blondel, P. Prettenhofer, R. Weiss, V. Dubourg, J. Vanderplas, A. Passos, D. Cournapeau, M. Brucher, M. Perrot, and E. Duchesnay, Journal of Machine Learning Research 12, 2825 (2011).

- Ishikawa [2018] T. Ishikawa, Rff_learn (2018), random-fourier-features package for python on github.

Appendix

Appendix A Related Work

RFF.

Ref. [13] first introduced RFF as a method for approximation of shift-invariant kernels and provided probabilistic bounds on the maximum point-wise approximation error of shift-invariant kernels. Later, the authors gave bounds on the true risk of random Fourier feature map for learning tasks with Lipschitz loss function [9]. Ref. [10] bounds the difference between decision functions achieved by the original and RFF-approximated kernels for tasks such as ridge regression and SVM using the proximity of kernel matrices. Ref. [20, 11] directly bounds the true risk of RFF for regression. Ref. [12] offer a framework that works for both regression and SVM.

Dequantization via RFF.

In the context of QML, RFF was the first method used to dequantize QNN regression by Ref. [7]. Their analytical results use the bounds of Ref. [10]. The authors also suggest practical sampling strategies for RFF. Ref. [8] extends the results to non-universal QNNs building up from Ref. [20]. The idea of random features has been used for quantum kernels but in a slightly different context. Ref. [29] uses random features to approximate a class of QKs called projected QKs [21, 30]. Ref. [31] uses RFF to approximate classical kernels with QKs.

Ref. [32] explores the possibility of efficient and exact evaluation of QNN kernels with matrix product state reweighting. It is shown that when the eigen spectrum of the kernel forms a matrix product state, it can be evaluated efficiently using tensors without the need for random feature sampling. A generalization comparison between this tensor network dequantization method and RFF-dequantization is left for future work.

Appendix B Background and Framework

B.1 Useful Notions from Kernel Theory

This section is largely based on Chapter 4 of Ref. [33].

Definition B.1 (Kernel Function).

Let be a non-empty set, then a function is called a kernel on if there exists a -Hilbert space and a map such that ,

| (11) |

We call and a feature map and a feature space, respectively. can be the set of real or complex numbers.

Definition B.2 (Reproducing Kernel Hilbert Space RKHS).

Let be a kernel on and be a Hilbert space for the feature map associated with the kernel. Then, the Hilbert space:

| (12) |

with norm:

| (13) |

is called the RKHS of and its norm is called the RKHS norm.

Definition B.3 (Kernel Integral Operator).

Given a kernel and a probability distribution over , we consider the space of square-integrable functions with respect to :

The kernel integral operator is then defined as

for all .

Bochner’s theorem provides some insights into the spectrum of shift-invariant kernels, which are targets of RFF.

Theorem B.4 (Bochner’s Theorem [34]).

A continuous function on is a shift-invariant kernel if and only if it is the Fourier transform of a non-negative measure. That is, every shift-invariant kernel can be expressed as

| (14) |

where is unique and non-negative. Moreover, by assuming without loss of generality, we have and thus is a probability density function.

Thm. B.4 shows a one-to-one correspondence between probability distributions and shift-invariant kernels. That is, the Fourier transform of every normalized shift-invariant kernel is a probability distribution. In this work, we consider quantum kernels (QKs), which are non-stationary in general. To do so, we focus on the following theorem.

Theorem B.5 (Yaglom 1987 [35, 36, 37]).

A complex-valued continuous bounded function on is the covariance function of a mean square continuous complex-valued random process on . Namely, a non-stationary continuous bounded kernel is positive semi-definite if and only if it can be represented as

| (15) |

where is a positive semi-definite function.

In analogy to Eq. (14), Eq. (15) shows that , is the Fourier transform of . Note that if is real, as is the case throughout this thesis, . Additionally, if is symmetric, i.e., , then is Hermitian and . If is diagonal, i.e. . all the elements are non-negative and is shift invariant according to (15), with which we can reproduce Bochner’s theorem (Thm. B.4). Note the technical detail that Thm. B.5 holds for a class of kernels called harmonizable kernels. However, except some highly contrived examples, most of complex-valued continuous bounded kernels are harmonizable. For more details refer to App. D of Ref. [36].

B.2 Some Useful Lemmas

Lemma B.6 (Cholesky Decomposition).

A positive definite (semi-definite) Hermitian matrix can be written as where is a lower triangular matrix with positive (non-negative) diagonal elements.

Corollary B.7 (Reverse Cholesky Decomposition ).

A positive definite (semi-definite) Hermitian matrix can be written as where is an upper triangular matrix with positive (non-negative) diagonal elements.

Proof.

Consider the permutation matrix with the same dimension as () such that and all of its other elements are . Together with Lem. B.6, we get . Moreover, by inserting into , we have . ∎

Corollary B.8.

A positive definite (semi-definite) Hermitian matrix can be written as where is an upper triangular matrix with normal columns and is diagonal with positive (non-negative) elements. Moreover, .

Proof.

We are given a positive semi-definite matrix . According to Cor. B.7, there exists an upper triangular matrix such that . Then we can write where ’s columns of . Take , then we have where . Define to be diagonal with ’s as its main diagonal and to be a matrix with normal vectors ’s as its columns. Then, we have . Moreover, . ∎

B.3 Quantum Kernels and Quantum Neural Networks

Definition B.9 (Fidelity Quantum Kernel).

Given an -qubit encoding unitary where , we define an encoded state as . Then the fidelity quantum kernel is a kernel on with:

| (16) |

In this work, we consider the Hamiltonian encoding (Assumption II.2), i.e., quantum circuits whose gate in the -th layer that encodes -th element of data has the form for a Hermitian matrix . Concretely, the encoding unitary operator is represented as

| (17) |

where and are fixed unitaries (i.e., non-variational unitary operators) and is the number of layers.

We also denote the ’th eigenvalues of by and define

| (18) |

for a vector index . For fidelity QKs using a Hamiltonian encoding the following Lemma holds.

Lemma B.10.

Proof.

The proof for one-dimensional input is provided in Ref. [14]. This result was extended to multi-dimensional inputs by taking the same steps for each dimension as done in Ref. [19]. Since can be written as a finite Fourier series, Thm. B.5 can be applied to prove the positive semi-definiteness of . The Hermitian property of is derived from the symmetry of the fidelity quantum kernels i.e. . To be more precise, we have

| (21) |

where we swapped the dummy variables in step (1) and in step (2) we used the fact that is real-valued and equal to its conjugate. By comparing the first and the last terms, we conclude that we have for all , which completes the proof. ∎

Note that the frequency support of encoding, , is symmetric around zero and always contains , meaning . Thus, we can define a set such that and . We define more formally.

Definition B.11 (Positive Frequency Support).

Corollary B.12.

Proof.

First, the fidelity quantum kernel is bounded; . Also, the Hamiltonian encoding is continuous (Assumption II.2), and has frequencies in from Lem B.10. Thus, using Thm. B.5, there exists a positive semi-definite matrix such that:

| (25) |

with . In the second equality, we use the vectorized form of the features to define in Eq. (22) and the fact that . Since is positive semi-definite according to Lem. B.6, there exists a lower triangular matrix with non-negative diagonal elements such that and the first part of the proposition is proved.

We remark that the map that brings to is isometric and reversible and thus a unitary. Therefore, we have . Because of the unitarity of , is still positive semi-definite, which completes the proof. ∎

Lemma B.13.

For any set , the associated map defined in Eq. (23) has the following property for where is the identity matrix.

Proof.

Lem. B.13 yields the following property of the Fourier transform of fidelity quantum kernels with Hamiltonian encoding, which we give below.

Corollary B.14.

B.4 Support Vector Machines

We here consider the framework of statistical learning theory. Suppose we have a set of i.i.d. samples drawn from some unknown distribution , and a set of functions , called hypothesis class, mapping to . Also, let be a positive function. The main goal in statistical learning theory is to find a function in the hypothesis class that minimizes the true risk defined as

| (28) |

However, since is unknown and thus the true risk is inaccessible, we usually optimize the empirical risk, which is the sample mean of the true risk using dataset , i.e.,

| (29) |

Some learning algorithms map the input data to a Hilbert space called feature space using a feature map , so that the structure of data can be captured better. In this case, we assume that is a subset of some RKHS associated with reproducing kernel i.e. for every function in there exists such that .

For a SVM classification problem, we minimize the hinge loss with the binary targets and . To avoid overfitting, a regularization term can be added to the empirical risk. More concretely, if we consider the RKHS of a kernel as the hypothesis class, the optimization problem is expressed as

with being the so-called regularization strength and denoting the RKHS norm.

As is in the RKHS of by definition, it can also be written as for some (See Def. B.2). Thus, we can re-express the above optimization formulation as

| (30) |

The above formulation requires access to the feature map. This is not possible for every kernel e.g. some kernels have infinite dimensional feature maps. When the feature map is not efficiently accessible, the problem can be solved in its dual form which only requires evaluation of the kernel function . The dual problem solves the following optimization:

| (31) |

In other words, the dual problem has the advantage that we do not have to compute the feature maps explicitly, once the kernel for every pair of training data is computed (i.e., these values are stored in the Gram matrix with ). This is known as the “kernel trick” and enables the use of even infinite-dimensional feature maps.

The main idea of SVM classification as shown in Fig. 2, is to find a separating hyperplane that can maximize the distance between the samples of both classes, which is called margin. When misclassification is not allowed, i.e., in Eq. (30), it is called hard margin SVM. On the other hand, a classification scheme with large allows for some trade-off between misclassification error and the margin and is called soft-margin SVM. Moreover, by adding another optimization parameter as an offset to so that the decision function is written as , we can incorporate a single class SVM problem for anomaly detection into the same optimization problem as above. We note that the decision boundary of SVM is given by the sign of the function , as shown below.

Definition B.15 (Decision boundary of SVM).

The decision boundary of SVM for binary classification is a function such that the predicted label for a test sample is computed as .

Finally, we note that other loss functions can be used for different tasks. For example, the squared error is mostly used in regression tasks; in case the regularization is included with the loss, it is called a ridge regression problem. When kernel methods are used for ridge regression, the model is classed kernel ridge regression.

B.5 Random Fourier Features

Random Fourier features [13] is a method to approximate a shift-invariant kernel. The motivation comes from the fact that, although the kernel trick makes it possible to utilize infinite dimensional feature spaces, the computational complexity of solving the dual problem using Gram matrix is . Here, is the number of training data points. This indicates that the computation becomes infeasible with increase in data size. A circumventing approach to this problem is to approximate the kernel using a dimensional feature space and then solve the primal problem in the space; this is useful for as the complexity is .

According to Bochner’s theorem (Thm. B.4), for every bounded, normalized, continuous and shift-invariant kernel we have

| (32) |

where in step (1) we use the fact that is symmetric to write Eq. (14) with cosine functions. and is a probability distribution obtained by normalizing the Fourier transform of the kernel.

RFF algorithm estimates this expectation using samples from the distribution. More precisely, given i.i.d. samples, , from the distribution , we can generate the random Fourier feature map,

| (33) |

This method of approximating the kernel is called Random Fourier Features (RFF). RFF was first proposed in Ref. [13] together with a probabilistic bound on the approximation error that depends on the variance of distribution . Followed by the original work, tighter bounds are derived in Ref. [10]. Both of these sources prove that one can approximate a kernel with RFF with infinity norm error less than with high probability using frequency samples where is the variance of distribution .

We note that is not the unique way of approximating such kernels. Different feature maps such as

| (34) | ||||

| (35) |

can be used. Here, both feature maps are constructed by sampling ’s from distribution and ’s from uniform distribution between .

We remark that, if the kernel is periodic then we can obtain an exact Fourier series representation and thus have discrete frequencies rather than continuous ones. That is, instead of , the periodic kernel has the distribution satisfying .

In general, the approximation method can not be used for non-stationary kernels. As shown in Thm. B.5, non-stationary kernels can be written in a form similar to the shift-invariant kernel. However, in Eq. (15) is not guaranteed to be non-negative or even real and thus cannot be taken as a probability distribution in general.

Appendix C Approximation of Quantum Kernels with Random Features

In this section, we propose a method for approximating fidelity quantum kernels as defined in Def. B.9. Specifically, we introduce an RFF-based method tailored to approximate a family of non-stationary kernels, which we refer to as Discrete Spectrum kernels (Def. C.1). Our proposed methods take as input a real-valued discrete spectrum kernel and return the approximate kernel with the feature map for the original kernel .

The main idea of our proposal is to express the kernel as the expected value of the inner products of feature maps, as shown in Eq. (3), and estimate the output using its sample mean. In this regard, our methods are closely related to the RFF framework (see Sec. B.5). Similar to RFF, we have to obtain the probability distribution from which we sample the frequencies to construct the feature maps. To do so, we here consider two approaches: (1) Cholesky decomposition (Alg.2) and (2) eigenvalue decomposition (Alg. 3). The key distinction between these methods lies in their trade-offs. Namely, while Alg.2 has tighter more interpretable error bounds , the bounds for Alg. 3 converge to the original RFF framework [13] bounds when we consider shift-invariant kernels. Therefore the bounds for Alg. 3 can be seen as a generalization of the results of Ref. [13].

We again emphasize that our method applies to a family of non-stationary kernels (not necessarily quantum), but we in this work we focus on the fidelity quantum kernel.

C.1 Settings & Definitions

Before we introduce our proposal, we outline the settings and definitions that will be helpful in this section as well as the subsequent sections. Throughout this section, we assume is a compact set in .

Definition C.1 (Discrete Spectrum Kernel).

A kernel is called a Discrete Spectrum Kernel if its Fourier decomposition can be written as a finite sum:

| (36) |

where is a finite set of frequencies we call frequency support and

| (37) |

Without loss of generality, we assume that these kernels are normalized, i.e., . Note that the Fourier transform matrix , which we call Fourier transform of the kernel, is positive semi-definite and unit-trace. See Thm. B.5 for the details of these properties.

An example of a discrete spectrum kernel is a fidelity quantum kernel in Def. B.9.

Corollary C.2.

A fidelity quantum kernel defined in Def. B.9, with Hamiltonian encoding is a discrete spectrum kernel.

Proof.

For ease of understanding, we consider the following ordering of the frequencies in .

Definition C.3 (Ascending Ordering of ).

is in ascending ordering if the frequencies in are sorted based on the size of norm. More precisely, , if , then , where are frequencies related to th and th elements of .

Such ascending ordering is possible for every kernel without loss of generality. Thus, we assume this ordering is satisfied in any decomposition of the kernel involving from now on.

Moreover, the positive semi-definiteness and unit-trace property of motivates us to derive the following probability distributions from it.

Definition C.4 (Diagonal Distribution of Discrete Spectrum Kernels).

Any discrete spectrum kernel has the Fourier transform with the assumption on the ascending order of (Def. C.3). Diagonal elements of are positive and sum to one therefore they constitute a probability mass function. We denote this probability mass function with , and call it the diagonal probability distribution of the kernel.

Definition C.5 (Eigenvalue Distribution of Discrete Spectrum Kernels).

Any discrete spectrum kernel has the Fourier transform with the assumption on the ascending order of (Def. C.3). Eigenvalues of are positive and sum to one therefore they constitute a probability mass function. We denote this probability mass function with , and call it the eigenvalue probability distribution of the kernel.

Definition C.6 (Cholesky Distribution of Discrete Spectrum Kernels).

Any discrete spectrum kernel has the Fourier transform with the assumption on the ascending order of (Def. C.3). According to Corollary B.8, can be decomposed as where is upper triangular with (2-norm) unit columns and is a diagonal matrix with positive elements. The diagonal elements of constitute a probability mass function. We denote this probability mass function with , and call it the Cholesky probability distribution of the kernel.

In this section, we used eigenvalue distribution and Cholesky distribution to express non-stationary kernels as expectation values. We have previously defined the diagonal distribution in Def. C.4 in the main text (Def. III.2) where we call it the kernel distribution. This diagonal distribution plays an important role in the sufficient conditions (e.g. Prop III.4) we derive. We recall the definition here to emphasize its distinction from the other two distribution defined in Defs. C.5, C.6.

C.2 Kernel Approximation using Cholesky Decomposition

In what follows, we approximate a discrete spectrum kernel with its Cholesky decomposition.

Given a discrete spectrum kernel , we decompose its Fourier transform as as in Def. C.6. Here, we denote the ’th column of with and the diagonal elements of , with . Then, the kernel can be written as . By defining , we re-express the kernel as

| (38) |

Similar to the RFF approach for shift-invariant kernels, we can express the discrete spectrum kernel as an expected value of the inner product of two functions. With this expression, We can now approximate the kernel with the following dimensional feature map

| (39) |

using i.i.d. samples from distribution , , and the approximate kernel is given by

| (40) |

We provide our algorithm for the approximation of discrete spectrum kernels in Alg. 2.

Before we proceed to derive analytical bounds on the approximation method, we state the following Lemma about features .

Lemma C.7.

Consider the feature function defined as with of Eq. (37) in the ascending order and columns of an upper triangular matrix ’s that is normal for all . Then possesses the following properties:

-

•

-

•

Proof.

To prove the first property, we start with the upper bound of the feature function;

| (41) |

where we used Cauchy-Schwartz inequality and the normality of . Note that the first elements of are non-zero as they come from an upper triangular matrix. Next, we bound its gradient,

| (42) |

where we use the fact that in the first equality, and the triangle inequality is applied to get the second inequality. Recall that the absolute value of the ’th element of is one, i.e. . Lastly, we use the ascending ordering assumption on to bound all ’s with ∎

Now, we state the theorem showing the convergence of Alg. 2

Theorem C.8 (Performance Guarantee of Alg. 2).

Given a discrete spectrum kernel (Def. C.1) with a compact set of diameter , Alg. 2 is employed to obtain the feature vector . Then, the error of the approximated kernel is given by

| (43) |

where is the Cholesky distribution of the kernel in Def. C.6, is the frequency corresponding to -th row of , is the frequency support of and is an integer random variable sampled from distribution .

Moreover, with any fixed probability when

Proof.

We follow the steps in Ref. [13] to derive bounds on the error. First, let us define an error function as . For ease of understanding, we use the notation . We then write as a function on with respect to this new variable . Note that is a compact set in with diameter . According to Ref. [38], there exists an -net that covers with at most center points . This means that every is closer than to one of these center points; that is, there exists a from the set of center points such that .

We use the following Lemma to show the results.

Lemma C.9.

Given a compact set , an -net on with center points with , for any Lipschitz function with Lipschitz constant , and any , if

| (44) |

and

| (45) |

then we have

| (46) |

Proof.

We are given a compact set and a set of center points for an -net on this set. We denote the closest center point to a point with . Using the definition of an -net we have . Moreover, since is the Lipschitz constant of , we have . Therefore we have

| (47) | ||||

| (48) |

where in the second line we used the Lipschitz property of . ∎

We can apply Lemm. C.9 to the error function defined above. Note that in this case the domain of the error function is dimensional and . Moreover, since is a random function depending on samples of distribution , according to Lemm. C.9 if events () and () , both happen we can say that , . That is, the probability bounds of these two events provide the bound of the event . Therefore, in this proof we first bound the probability of each of these events and then bound the probability of both of them happening together.

We first work on () . Here, our strategy is to use Markov’s inequality. Namely, we have: . Next, we need to bound . Note that, because is differentiable (both are differentiable), where . Hence, we get

| (49) |

Here, we utilize the fact that is the concatenation of in the step (1). Now, due to the symmetry of the error function and linearity of the expectation, we only have to consider . Then, we obtain

| (50) |

where for step (1) we bounded the variance of a random variable with its second moment. For step (2) we used the fact that (triangle inequality and Cauchy-Schwartz inequality). For step (3) we use Lem. C.7.

By defining , we put the two equations above together and arrive at the following Markov’s bound:

| (51) |

Next, we move on to bound () . For ease of later discussion, we briefly recall sub-Gaussian random variables and some of their properties.

Definition C.10.

( Sub-Gaussian Random Variables) A random variable is called sub-Gaussian if, for every , the following satisfies;

| (52) |

Also, is called the variance proxy of this random variable.

Lemma C.11.

Sub-Gaussian random variables have the following properties.

-

1.

For every sub-Gaussian random variable with variance proxy we have

(53) for every .

-

2.

A random variable that is bounded in is sub-Gaussian.

-

3.

Given independent sub-Gaussian random variables with variance proxy respectively, the sum of these random variables is sub-Gaussian with variance proxy .

-

4.

From 1, 3. If ’s are independent sub-Gaussian random variables with variance proxies we have

(54)

Note that, according to Lem. C.7, we have , where ranges between and ; this indicates that is at least sub-Gaussian (Def. C.10 and point 3 of Lem. C.11). However, depending on the kernel, could be more concentrated and therefore sub-Gaussian for some . For the sake of generality and possible tighter bounds, we keep a general form and assume is sub-Gaussian. We then use Lem. C.11, to bound :

| (55) |

Now we can bound the probability of the maximum error of our approximation.

| (56) | ||||

| (57) | ||||

| (58) | ||||

| (59) | ||||

| (60) | ||||

| (61) |

where we use the complement of the event in the first, third and fourth lines. In the fifth line, we used union bound and Eq. (51), Eq. (55) are used for the last equality.

Now, this bound has the form . We choose and substitute it in the bound. By doing so the bound will have the form and the first part of the theorem is proven. To prove the second part, we can fix any probability for the left-hand side and solve for . Then, we get

| (62) |

∎

Fidelity quantum kernels, with integer frequencies i.e. are periodic with a period of on each dimension of their inputs. Consequently, they can be defined on with the diameter of . Therefore, we get

| (63) |

Note that, as mentioned before, an upper bound for is . Since the number of frequencies scales exponentially in this upper bound suggests the hardness of the approximation in the number of dimension. However, we conjecture that for most fidelity quantum kernels, is actually lower. Indeed, Ref. [27] suggests that most fidelity quantum kernels are low pass (the Fourier coefficient for high frequencies is relatively low), implying the potential for easier implementation.

C.3 Kernel Approximation using Eigendecomposition

Similar to the case for Cholesky decomposition, eigenvalue decomposition can also be used for the approximation. In this approach, instead of sampling the columns of the upper diagonal decomposition of from the Cholesky distribution (Def. C.6), we sample columns of the eigenvectors of the Fourier transform from eigenvalue distribution (Def. C.5). This method can reproduce the convergence bound derived for the shift-invariant kernels in Ref. [13].

Given a discrete spectrum kernel , we decompose its Fourier transform to eigenvalues and eigenvectors, such that . Then, the kernel can be written as , where is the ’th column of . By defining , the kernel can be expressed as

| (64) |

Thus, we can sample the features from to construct the kernel using its sample mean, which is provided in Alg. 3. Note that the matrix in this section consists of eigenvectors and is different from the Cholesky decomposition matrix we used in the previous section. Therefore the properties of the feature function are different from what we have in Lemm. C.7. We state some properties of function in the following lemma.

Lemma C.12.

Suppose the feature function defined as with in Def. C.3 and columns of a unitary ’s. Then g has the following properties:

-

•

-

•

Where is the norm of the largest frequency that exists in .

Proof.

For the first part, using Cauchy–Schwarz inequality, we have

| (65) |

where we use . Now, let us bound the gradient of the feature function as follows;

| (66) |

where we first use the fact that , and we then use the triangle inequality. We have denoted with Lastly, we apply the ordering assumption on to introduce . ∎

Previously, we have discussed that, if the Fourier transform of a discrete spectrum kernel is diagonal, that kernel is shift invariant and vice versa. This motivates us to define a measure of non-stationarity for these types of kernels.

Definition C.13 (Non-stationarity of a Discrete Spectrum Kernel).

Given a discrete spectrum kernel and its Fourier transform such that , we define its ’th non-stationarity measure as

| (67) |

where ’s are the orthonormal eigenvectors of and is a unitary with ’th column . Moreover is the frequency associated with the ’th element of and .

To see how this measure is related to non-stationarity, we consider two cases. The first example is a shift-invariant kernel with diagonal . In this case, and then . As a result which is its minimum. On the other hand, if the kernel is maximally non-diagonal such that , then , which is a large number because of and . This shows that captures “non-diagonalness" (i.e., how much the matrix is far from the diagonal one) of the kernel well.

Now, we state the convergence bounds for Alg. 3, which depends on this non-stationarity parameters.

Theorem C.14 (Performance Guarantee Alg. 3).

Given a discrete spectrum kernel (Def. C.1) with a compact set of diameter , we apply Alg. 3 with samples and obtain the feature vector . Then, the error of the approximated kernel is given by

| (68) |

where is the eigenvalue distribution of the kernel defined in Def. C.5 and is the ’th non-stationarity measure of the kernel defined in Def. C.13. Here, is the frequency corresponding to ’th row of and is the frequency support of .

Moreover, with any fixed probability when

Proof.

The proof is almost identical to the proof of Thm. C.8, except that the bound for the second moment of Lipschitz constant changes according to Lem. C.12;

| (69) | ||||

| (70) | ||||

| (71) | ||||

| (72) | ||||

| (73) | ||||

| (74) | ||||

| (75) |

Here, the second line utilizes the fact that the second moment of a random variable is always larger that the variance and Lem. C.12 is used in the last line. is defined as ’th non-stationarity measure of kernel (Def. C.13). The rest of the proof follows the same procedure as the one for Thm. C.8. ∎

Thm. C.14 shows that the number of frequency samples scales with . This bound suffers from the same problem as the bounds in Thm. C.8; that is, the exponential scaling of with . However, this bound is more interpretable because, if the kernel is shift-invariant, and we retrieve the bounds in Ref. [13].

Overall, this section provides a method to approximate discrete spectrum kernels using the Cholesky decomposition and eigenvalue decomposition of their Fourier transform. We also derived upper bounds on the probability of point-wise error. Comparing the two upper bounds, Alg. 2 shows a better scaling with if is sub-Gaussian with .

C.4 Numerical Experiment

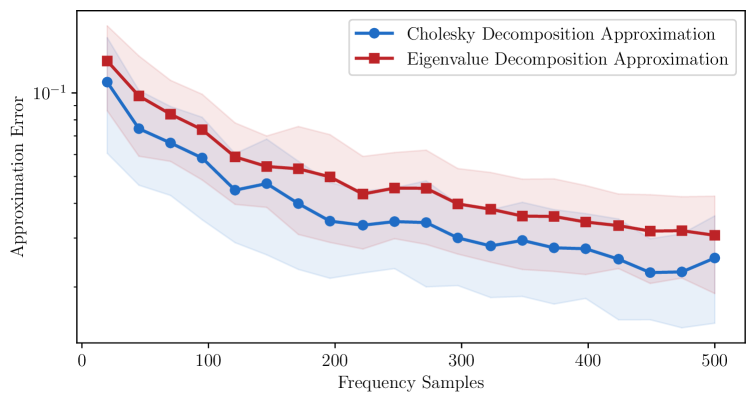

Finally, in this section, we support our theoretical results numerically. To show the convergence of Algs. 2, 3, we consider a simple kernel of 2 qubits and 2 layers with the feature map in Fig. 8. As shown in Fig. 7, the approximation error for both algorithms converges to zero. We see that Alg. 2, performs slightly better than Alg. 3. The advantage seems to be in the prefactor of the exponential decay over . This could indicate that our bounds for Alg. 3 are looser compared to Alg. 2 despite its interpretability.

Appendix D Alternative Alignment Condition of Ref. [8]

The main result of Ref. [8] (Thm. 1) states sufficient conditions under which RFF can reach the performance of QNN regression. A slightly different version of this theorem is stated as Thm. E.2 and we will later discuss this theorem in more details. In this appendix we show how these sufficient conditions imply an alignment between the sampling distribution of the RFF algorithm and the optimal decision function of QNN.

One of the sufficient conditions for dequantization provided in Ref. [8] is the alignment condition; expressed as,

where (Eq. (7)) is the output of the QNN model and is the shift-invariant kernel whose Fourier transform is distribution (defined in Eq. (3)).

This condition rises from the dependence of the number of required RFF frequency samples on the RKHS norm. To be more precise, the main result of Ref. [8] (Thm. 1) shows that RFF can reach the performance of QNN regression if where are the number of data and frequency samples, respectively.

Consequently, the value of this RKHS norm is important in determining the efficiency of RFF dequantization. Ideally we want to find a sampling distribution such that is relatively small. Ref. [8] suggests that a sampling distribution that is aligned with the Fourier transform of the optimal decision function is a good choice for RFF, using some examples to support their claim. Here, we show that a distribution that is proportional to the Fourier transform of is the minimizer of . In other words, we show the following:

Take any function in the RKHS. It can be described as a vector, as with as in Eq. 8. The distribution which minimizes is such that , i.e. the two vectors are aligned.

Before we proceed, let us recall the settings and the definitions in Ref. [8]. The kernel considered in Ref. [8] is a so-called re-weighted kernel for distribution , defined as with the feature map

| (76) |

Note that, throughout this section, is a vector of size with positive elements that sum to one, while and denote the sampling probability for frequency and frequency zero, respectively.

We recall from Def. B.2 that, for a kernel , such that , RKHS norm can be defined as:

| (77) |

We highlight two important facts. First, since the basis functions i.e., the elements of are linearly independent, the representation of any function with respect to the kernel is unique and the infimum of is simply the unique element that describes the function. Second, from Observation 1 in Ref. [8], we know that the RKHS is invariant under reversible re-weightings. This means that can be reconstructed by any of the re-weighting kernels with any distribution as long as .

Now, we prove that the weights for such a kernel should be aligned with the frequency spectrum of the target function to minimize the corresponding RKHS norm. To do so, we define the feature map associated with the uniform weighting as . Then, we can express , where consists of normalized Fourier coefficients of (Eq. (6)).

Given a re-weighted kernel , we can also write , and thus we have

| (78) |

where represents point-wise multiplication. Alternatively, we have with point-wise division . As a result, the minimization problem can be reduced to

| (79) |

This is a convex optimization problem over . We recall that an optimization problem of the form

with convex ’s and affine ’s is called a convex optimization problem. We define the Lagrangian of this problem as

| (80) |

The following conditions known as KKT conditions [39], [40, Ch. 5, p. 241-249] are necessary and sufficient for points to be optimal. In other words, if there exists such that:

then is the solution of the problem.

For our problem (Eq.(79)) the Lagrangian has the form

| (81) |

By applying KKT conditions [39], [40, Ch. 5, p. 241-249], we have

This concludes that the solution to this optimization problem is a distribution that is proportional to , i.e., the Fourier transform of . Hence, the distribution aligned with the spectrum of the target function gives us the lowest value for minimum number of data samples needed for dequantization. In the main text, we recast the alignment condition based on this derivation.

Appendix E Kernel Ridge Regression and RFF

In this section, we prove Prop. III.3 of the main text as Cor. E.6. First, we recall the definition of dequantization. Then, we recall the theorem from Ref. [8] and [20]. Next, we state Lem. E.3 about the relation between the RKHS norm of a function with respect to two different kernels. Using these as preliminaries, we prove Thm. E.4 about the generalization of QK regression. Finally, from Thm. E.4, we derive Cor. E.6, which corresponds to Prop. III.3 of the main text. Finally we propose Lem. E.7 on the interpretation of the alignment condition.

We defined dequantization in Def. II.3 of the main text. For convenience we state this definition again.

Definition E.1 (RFF Dequantization).

Consider a supervised learning task with a training dataset . Given a quantum model (either a QNN or QK) with hypothesis class , denotes the true risk minimizer of the quantum model i.e. . We say the task is RFF-dequantized, if there exists a distribution such that for some , with , the following is true with high probability:

| (82) |

Here, is the decision function of the task trained with a dimensional RFF feature map (Eq. 4) sampled from and denotes the true risk.

In short, we say a quantum learning task is dequantized when there exists a frequency sampling distribution for which RFF works almost as well as the quantum model in terms of true risk. Therefore, our objective in this section is to bound the difference between the true risk of RFF method and the minimum true risk in the RKHS of the quantum kernel.

Generalization of RFF is well studied in a classical setting and we can use the existing results to prove dequantization under certain conditions. In this work, similar to Ref. [8], we base our proofs on the results provided by Ref. [20]. Ref. [20] shows that under certain conditions, RFF regression performs almost as well as the exact kernel ridge regression. The following theorem summarizes these results.

Theorem E.2 (Thm. 3 From Ref. [8] ).

Consider a regression problem . Let be a kernel, and be the subset of the RKHS consisting of functions with an RKHS norm upper bounded by some constant .

We also denote the true risk minimizer over as .

Now, we assume the following:

1. The kernel has an integral representation

2. The function is continuous in both variables and satisfies almost surely, for some .

3. For some , almost surely when .

Additionally, define

and

Here, is the operator norm of the kernel integral operator (Def. B.3) and . Then, we assume by defining the number of data samples as . Also, let be the output of -regularized linear regression with respect to the feature map,

constructed from the integral representation of by sampling elements from . Then,

is enough to guarantee, with probability at least , that

This theorem bounds the difference between the true risk of RFF regression and the minimum possible true risk in which is the set of all functions in the RKHS of kernel with RKHS norm less than a constant . The theorem states that, if the number of frequency samples is larger than a threshold value of , then the true risk gap between RFF and the minimum true risk over decays with rate with the number of data samples .

This theorem can be applied to a QK method by finding such that the true risk minimizer of the QK method falls inside . To do so, we stablish a connection between the RKHS of a QK and the RKHS of the RFF kernel in the following lemma. Specifically, we provide a bound on the RKHS norm of with respect to two different kernels, which are associated with the same RKHS.

Lemma E.3.

Consider a real-valued shift-invariant kernel with a diagonal Fourier transform (such that no diagonal element is zero) and a frequency support . Consider another real-valued kernel with a non-diagonal Fourier transform on the same frequency support. That is, and , where is the trigonometric feature vector defined in Eq. (37). For any function that lies in the RKHS of both kernels, we have:

| (83) |

Proof.

For any set of frequencies , we are given a shift-invariant kernel with diagonal Fourier transform (such that no diagonal element is zero), and another kernel with non-diagonal Fourier transform . That is, and , where is the trigonometric feature vector defined in Eq. (37). These kernels’ corresponding feature maps are and , respectively.

We recall that the definition of the RKHS norm of a function with respect to a kernel is for . Now, we define the vector with the minimal RKHS norm for as . We then have

| (84) |

where we used the fact that is Hermitian because of the symmetry of the kernel. From the rightmost expression, we have that with . We remark that is invertible from the assumption that all diagonal elements are non-zero. As a result, we have

| (85) |

∎

Theorem E.4 (Quantum Kernel Ridge Regression vs. Random Fourier Features).

Consider a regression problem . Let be a fidelity quantum kernel with Fourier transform and frequency support (Def. III.2). We also denote as the true risk minimizer of quantum kernel ridge regression with kernel .