On the Robustness of Kernel Ridge Regression Using the Cauchy Loss Function

Abstract

Robust regression aims to develop methods for estimating an unknown regression function in the presence of outliers, heavy-tailed distributions, or contaminated data, which can severely impact performance. Most existing theoretical results in robust regression assume that the noise has a finite absolute mean, an assumption violated by certain distributions, such as Cauchy and some Pareto noise. In this paper, we introduce a generalized Cauchy noise framework that accommodates all noise distributions with finite moments of any order, even when the absolute mean is infinite. Within this framework, we study the kernel Cauchy ridge regressor (KCRR), which minimizes a regularized empirical Cauchy risk to achieve robustness. To derive the -risk bound for KCRR, we establish a connection between the excess Cauchy risk and -risk for sufficiently large scale parameters of the Cauchy loss, which reveals that these two risks are equivalent. Furthermore, under the assumption that the regression function satisfies Hölder smoothness, we derive excess Cauchy risk bounds for KCRR, showing improved performance as the scale parameter decreases. By considering the twofold effect of the scale parameter on the excess Cauchy risk and its equivalence with the -risk, we establish the almost minimax-optimal convergence rate for KCRR in terms of -risk, highlighting the robustness of the Cauchy loss in handling various types of noise. Finally, we validate the effectiveness of KCRR through experiments on both synthetic and real-world datasets under diverse noise corruption scenarios.

Keywords: Robust regression, generalized Cauchy noise,

robust loss function,

Cauchy loss function,

kernel ridge regression,

minimax-optimal convergence rates,

learning theory

1 Introduction

Robust regression seeks to accurately estimate the true regression function in scenarios where outliers, heavy-tailed distributions, or contaminated data points can significantly distort the results of standard regression methods. Mathematically, it aims to provide accurate estimates even when the noise or response distribution lacks a finite exponential expectation, meaning the distribution may have heavy tails but still possess a finite -th moment. Due to its resilience against such deviations from typical assumptions, robust regression has been extensively applied in fields such as finance (Pervez and Ali, 2022), economics (Khan et al., 2021), engineering (Agrusa et al., 2022), and environmental science (Pirtea et al., 2021).

Many studies on robust regression assume that the absolute mean of the noise is finite, typically represented as noise with a finite -th moment for . For instance, under the assumption of a finite -th moment with , Feng et al. (2015) investigate a correntropy-induced regression loss (Santamar´ıa et al., 2006) and derive error bounds for the -distance between the learned regressor and the true regression function. When the noise has finite variance, i.e., , Catoni (2012) proposes a log-truncated loss function for mean and variance estimation, demonstrating that the deviation of the estimator is comparable to that of the empirical mean estimator for Gaussian-tailed data, while Xu et al. (2020) establish excess risk bounds for the empirical log-truncated risk minimizer under the finite variance assumption. Further research has extended the use of Catoni’s log-truncated loss to cases where the noise has a finite -th moment with . For example, this loss function has been applied to least absolute deviation (LAD) regression (Chen et al., 2021), mean estimation (Lam and Cheng, 2021), and multi-armed bandits (Lee et al., 2020). Moreover, Xu et al. (2023) propose a generalized form of the log-truncated loss, which is used for solving quantile regression and generalized linear models (GLM). They establish excess risk bounds for the empirical log-truncated risk minimizer with respect to both the pinball loss and the GLM loss.

In many applications, the noise distribution does not have a finite absolute mean, i.e., the noise has only a finite -th moment for , as seen with Cauchy noise and certain Pareto noise distributions. Cauchy noise frequently arises in finance and markets (Ljajko et al., 2023), radar images (Karakuş et al., 2022), low-frequency atmospheric noise (Fu et al., 2010), and underwater acoustic signals (Idan and Speyer, 2010; Shi et al., 2020). It is also common in industrial wireless communication systems (Laus et al., 2018; Zhang et al., 2021), particularly in massive multiple-input multiple-output systems (Gülgün and Larsson, 2024). Meanwhile, Pareto noise is often used to model wealth distribution in societies. In such cases, the typical assumption of a finite -th moment with is violated, rendering existing theoretical guarantees inapplicable. Despite this, the Cauchy loss function (Black and Anandan, 1996) has empirically shown promising results in regression problems under extreme noise conditions (Mlotshwa et al., 2022). However, to the best of our knowledge, no existing work has established error bounds for the empirical Cauchy risk minimizer in non-parametric regression problems when the noise has only a finite -th moment with .

In this paper, we propose a generalized Cauchy noise assumption, which assumes that the logarithmic moment of the noise is finite. Since the logarithmic function grows more slowly than any polynomial function, this assumption can be satisfied by noise with a finite -th moment for any . Under this assumption, we find that, unlike the expected absolute loss or Huber loss (Huber, 1992), the expected Cauchy loss (Black and Anandan, 1996) remains finite, and its Bayes function coincides with the true regression function. This confirms that the regression function can be effectively learned by minimizing the Cauchy loss in the presence of various noise types. Based on this insight, we develop a kernel-based regression method called the kernel Cauchy ridge regressor (KCRR), which minimizes the regularized empirical Cauchy risk within a reproducing kernel Hilbert space (RKHS).

Since -risk is a widely used criterion in robust regression for measuring the -distance between the regressor and the true regression function, our goal is to establish the convergence rate of the KCRR with respect to -risk. To achieve this, we express the -risk of KCRR as the product of two terms: the supremum of the ratio between the -risk and the excess Cauchy risk across all regressors, and the excess Cauchy risk of KCRR itself. To bound the supremum of this risk ratio, we first show that the -risk can be bounded by the sum of the excess Cauchy risk and an -risk term, which decreases as grows. Upon further analysis, we demonstrate that for large values of , the -risk term can be bounded by an -risk term. This leads to a calibration inequality, indicating that the -risk becomes equivalent to the excess Cauchy risk when is sufficiently large. Next, to derive the upper bound of the excess Cauchy risk for KCRR, we decompose it into two components: the sample error and the approximation error. Benefiting from the refined calibration inequality, we show that the Cauchy loss satisfies the variance bound with an optimal exponent, which is crucial for deriving a promising oracle inequality for KCRR. Additionally, since the excess Cauchy risk is smaller than the -risk for any , the approximation error with respect to the Cauchy loss can be bounded by the approximation error in terms of -risk. By combining the upper bound of the risk ratio with the excess Cauchy risk of KCRR, we are able to establish an almost minimax-optimal convergence rate for KCRR in terms of -risk, given appropriate parameter choices.

The contributions of this paper can be summarized as follows:

(i) We introduce a generalized Cauchy noise assumption, which encompasses a broad range of noise distributions, including those without a finite absolute mean, such as Cauchy noise and certain Pareto noise. To tackle the robust regression problem under this challenging noise setting, we propose the KCRR and derive excess Cauchy risk bounds for KCRR. Under the assumption that the regression function is Hölder smooth, these bounds decrease as the scale parameter decreases.

(ii) Under the generalized Cauchy noise assumption, we establish a link between the excess Cauchy risk and the -risk. Specifically, for sufficiently large values of the Cauchy loss scale parameter , minimizing the two risks becomes equivalent. This shows that minimizing the Cauchy loss on noisy samples is equivalent to minimizing the -distance between the regressor and the true regression function, making the learning process robust to noise. This equivalence highlights why using the Cauchy loss leads to a resilient regressor in the presence of extreme noise.

(iii) Building on these results, we demonstrate that the scale parameter plays a crucial role in both the excess Cauchy risk bound from (i) and the equivalence between the Cauchy risk and -risk established in (ii). By selecting an appropriate , we achieve an almost minimax-optimal convergence rate for KCRR in terms of -risk, underscoring the robustness of the Cauchy loss in mitigating the effects of extreme noise.

(iv) We conduct experiments on synthetic and real-world regression datasets, demonstrating that KCRR outperforms existing methods under various types of noise corruption.

The remainder of this paper is organized as follows: In Section 2, we define the robust regression problem, introduce the generalized Cauchy noise assumption, explore the properties of the Cauchy loss function, and propose the KCRR method. In Section 3, we establish the connection between the excess Cauchy risk and -risk, and under mild assumptions, derive the almost minimax-optimal convergence rate of KCRR in terms of -risk, comparing it with existing rates. Section 4 provides a detailed error analysis for the -risk of KCRR. Experimental results and empirical comparisons with other loss functions are presented in Section 5. Finally, the proofs for Sections 2–4 are provided in Section 6, and the paper concludes with Section 7.

2 Robust Regression: Kernel Cauchy Ridge Regression

In this section, we first define the robust regression problem in Section 2.1, outlining the challenges posed by outliers and heavy-tailed noise. In Section 2.2, we introduce the generalized Cauchy noise assumption, which provides a framework for modeling such noise. We then delve into the characteristics of the Cauchy loss function in Section 2.3, highlighting its robustness against extreme noise and outliers. Finally, in Section 2.4, we propose the kernel Cauchy ridge regression (KCRR) method, which combines the Cauchy loss with kernel-based techniques to provide a powerful approach for robust regression.

2.1 Robust Regression

In this paper, we consider a regression framework where is a compact, non-empty set and . The goal of the regression problem is to predict the value of an unobserved response variable based on the observed value of an explanatory variable . We formulate the regression model as follows:

| (1) |

where represents the true regression function with and denotes the noise variable, which is assumed to be independent of . In this context, outliers and heavy-tailed noise, represented by the noise variable , pose significant challenges for learning . Outliers can disproportionately influence traditional loss functions such as squared loss, absolute loss, and Huber loss, leading to biased estimates and diminished generalization performance. Moreover, heavy-tailed noise allows for large deviations in , exacerbating issues related to model stability and performance. Robust regression methods aim to address these challenges by utilizing loss functions designed to minimize the impact of extreme values. By reducing the influence of outliers and heavy-tailed noise, robust regression ensures more reliable predictions, even in the presence of such disruptions.

Let the joint probability distribution of in (1) on the space be denoted by . Consider a set of independent and identically distributed samples drawn from . The objective is to find a regressor that estimates the true regression function based on the observations generated by model (1). For any measurable function , the population risk and empirical risk are defined respectively as follows:

where represents the empirical measure based on the data , and is the Dirac measure at . The Bayes risk, which represents the minimal achievable risk with respect to and , is given by

Moreover, a measurable function that satisfies is called a Bayes function for the loss function and distribution .

Before proceeding, we introduce some notation that will be used throughout this paper. Let be a probability space. For , we denote by the space of measurable functions with a finite -norm. Specifically, for , the -norm is defined as , and for , we define . The space , equipped with the norm , forms a Banach space. For any Banach space , we denote its closed unit ball by . Additionally, we use the notation (or ) to indicate that there exists a constant such that (or ) for all . We write if there exists a constant such that for all . For a natural number , we denote . Lastly, for , we define , representing the larger of the two values.

2.2 Generalized Cauchy Noise

In the existing literature on robust regression, it is commonly assumed that a given -th moment of the noise variable in (1) is finite, meaning that , for some . For example, Feng et al. (2015); Brownlees et al. (2015) assume , while Xu et al. (2020); Zhang and Zhou (2018) consider the case where , and Xu et al. (2023); Shen et al. (2021a, b) extend the analysis to . These results apply to noise distributions with fast-decaying tails, such as Gaussian noise, and moderately heavy-tailed distributions like the Student- noise with degrees of freedom strictly greater than . However, as discussed in Section 1, many real-world scenarios involve data contaminated by extremely heavy-tailed noise, such as Cauchy noise or certain types of Pareto noise, which do not have finite variance or even a finite absolute mean. These cases, illustrated in the following examples, fall outside the scope of traditional assumptions.

Example 2.1 (Cauchy Noise).

The probability density function of the Cauchy distribution is given by

where is the scale parameter. Notably, for any , the absolute moment , meaning that neither the mean nor variance of Cauchy noise are finite. However, for , we have , indicating that the Cauchy noise satisfies the finite -th moment assumption only when .

Example 2.2 (Pareto Noise).

The probability density function of the (generalized) Pareto noise distribution is given by

where is the scale parameter and is the shape parameter. For Pareto noise with shape parameter , the -th moment exists only if . In particular, when , the variance becomes infinite, and when , the absolute mean is also infinite.

It is important to note that both Cauchy noise and Pareto noise with do not satisfy the finite -th moment assumption for ; they only meet this condition for some . To account for all noise distributions across the range , we propose the following assumption.

Assumption 2.3 (Generalized Cauchy Noise).

We assume that the noise variable in model (1) has a finite logarithmic moment, specifically, .

Clearly, because the logarithmic function grows more slowly than any polynomial function, Assumption 2.3 encompasses noise distributions with finite -th moments for all , as shown in the following lemma.

Lemma 2.4.

For any , if a noise distribution has a finite -th moment, i.e., , then it satisfies Assumption 2.3, i.e., .

For simplicity, we introduce the following assumptions: the noise is symmetrically distributed around zero and exhibits monotonically decreasing tails.

Assumption 2.5 (Symmetric Noise).

Assume that the noise variable is symmetrically distributed, meaning its probability density function satisfies for any .

Assumption 2.5 is clearly met by many commonly used noise distributions, such as Gaussian, Student-, Laplace, and Cauchy noise. This symmetry assumption is frequently employed in robust regression studies (see, e.g., D’Orsi et al. (2021); Tsakonas et al. (2014)).

Assumption 2.6 (Monotonically Decreasing Tails).

The noise variable is assumed to have monotonically decreasing tails. Specifically, for any such that , it holds that .

It is also evident that many commonly used and widely studied noise distributions satisfy Assumption 2.6. Examples include Gaussian noise, Student- noise, Cauchy noise, and Pareto noise.

2.3 The Cauchy Loss Function

As demonstrated in Lemma 2.4, certain noise distributions satisfy Assumption 2.3 but do not possess finite variance or a finite absolute mean, such as Examples 2.1 and 2.2. For such noise, commonly used robust regression loss functions, like the absolute loss and Huber loss, become ineffective since the associated risks are infinite.

In this paper, we explore the Cauchy loss function (Black and Anandan, 1996), which offers greater robustness against outliers compared to traditional loss functions. The Cauchy loss is defined as

| (2) |

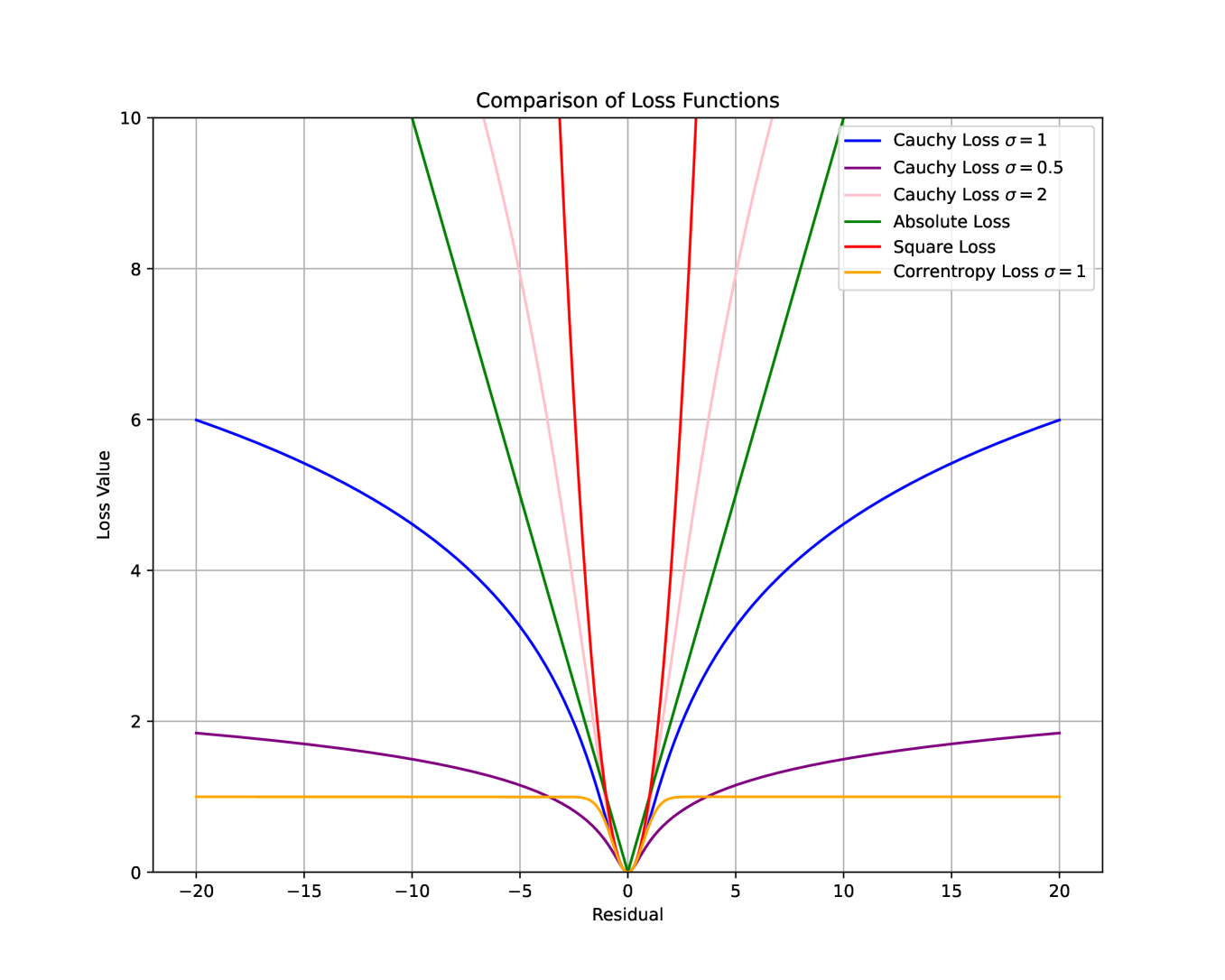

where is a parameter that controls the spread of the loss function. For small residuals, , the Cauchy loss behaves similarly to the square loss, but for large residuals, it grows logarithmically, reducing the influence of extreme noise. As shown in Figure 1, smaller values of yield smaller Cauchy losses for a given residual, while larger values cause the Cauchy loss to gradually approach the square loss.

The following lemma demonstrates that, under the generalized Cauchy noise Assumption 2.3, the Cauchy risk is always finite for any bounded regressor .

Lemma 2.7 (Finite Risk).

Unlike the infinite mean squared error (MSE) or mean absolute error (MAE) in the presence of extreme noise or outliers, the finiteness of the Cauchy risk highlights the robustness of the Cauchy loss function. This demonstrates that even under Cauchy noise and Pareto noise in Examples 2.1 and 2.2, the Cauchy loss admits a well-defined empirical risk minimization framework.

The key reason for finite Cauchy risk lies in how the Cauchy loss penalizes large prediction errors logarithmically, in contrast to the quadratic penalty of MSE or the linear penalty of MAE. As a result, extreme responses exert less influence on the Cauchy risk, making models trained under this loss function more resistant to the impact of outliers.

The following lemma establishes that the regression function is the exact minimizer of the Cauchy risk.

Lemma 2.8 (Optimality).

By combining Lemmas 2.7 and 2.8, we conclude that under the assumption of symmetric noise with a finite logarithm moment, the true regression function consistently yields a smaller Cauchy risk than any other regressor . Specifically, for any bounded . This provides a theoretical guarantee that minimizing the finite Cauchy risk leads to the recovery of the true regression function .

Comparison with the Correntropy Loss. The correntropy loss (Santamar´ıa et al., 2006) is defined as

| (3) |

where is the scale parameter. As illustrated in Figure 1, for small residuals , the correntropy loss behaves similarly to the square loss but asymptotically approaches as the residual increases. Its bounded nature ensures robustness against large errors, as it does not grow indefinitely with increasing residuals. However, its performance heavily depends on the choice of the bandwidth parameter . If is too small, the loss function becomes overly sensitive to minor noise, whereas a large may cause the model to ignore significant outliers. In contrast, the Cauchy loss in (2) strikes a more consistent balance between robustness to outliers and sensitivity to small errors.

Comparison with the Log-Truncated Loss. Log-truncated loss functions, introduced by Catoni (2012) for robust learning, take the form

where is a non-increasing function satisfying

| (4) |

In particular, Catoni (2012) considers with , while Xu et al. (2023) explore . When we take as the absolute loss, , set , and choose , which satisfies (4), the log-truncated loss becomes

| (5) |

which is the Cauchy loss given in (2) with . Compared to the Cauchy loss, the log-truncated loss introduces additional flexibility through the parameter , allowing fine-tuning for different noise distributions or robustness needs. However, this added flexibility comes at the cost of increased complexity in hyperparameter tuning and reduced interpretability.

2.4 Kernel Cauchy Ridge Regression

In this paper, we explore a kernel-based regressor that minimizes the Cauchy loss function to address the robust regression problem. Kernel-based regression is a non-parametric technique that leverages kernel functions to model the relationship between response and explanatory variables. Specifically, let represent the reproducing kernel Hilbert space (RKHS) induced by the Gaussian kernel function for , where is the bandwidth parameter. For any regressor and a clipping parameter , the clipped regressor is defined as

| (6) |

The parameter may vary depending on the sample size . By selecting larger than (the true regression function’s range), the clipped regressor is able to fully capture the behavior of , thereby avoiding underestimation and preserving the accuracy of the regression model. The clipping operation ensures the regressor does not produce extreme or nonsensical values, especially in the presence of unbounded noise or outlier data.

The following lemma demonstrates that the Cauchy loss is clippable, meaning that the Cauchy risk does not degrade after applying clipping, provided that the clipping parameter .

Lemma 2.9.

As demonstrated in Lemma 2.9, the Cauchy loss satisfies the clipping condition (Steinwart et al., 2006) under Assumptions 2.3, 2.5 and 2.6. Specifically, for any regressor , the risk of the clipped regressor is no greater than that of the original regressor , i.e., . This shows that applying the clipping operation to a regressor can result in a reduced or unchanged Cauchy risk.

Given a regularization parameter , the kernel Cauchy ridge regressor (KCRR), denoted by , is obtained by minimizing the empirical Cauchy risk, as follows:

| (7) |

Here, the first term controls the model complexity and the second term represents the clipped empirical Cauchy risk, ensuring robustness against outliers. Thus, KCRR belongs to the class of clipped regularized empirical risk minimization (CR-ERM) (Steinwart and Christmann, 2008, Definition 7.18), which enhances traditional regularized empirical risk minimization (RERM) by applying a clipping operation. This clipping reduces the influence of outliers or noise, resulting in improved generalization properties. In KCRR, the robustness is further strengthened by integrating the clipping mechanism with the robust Cauchy loss function.

3 Main Results and Statements

In this section, we aim to establish the convergence rates of KCRR in terms of -risk. The -risk measures the -norm distance between and the true regression function , denoted as , where is the marginal distribution of on . This metric directly quantifies the mean squared distance between the regressor and the regression function . One of the key advantages of the -risk metric is that it only depends on the distribution of and, therefore, that it is independent of the noise distribution, i.e. the distribution of . This property makes it particularly suitable for robust regression problems. Unlike other evaluation metrics that rely on residuals, such as the Huber loss or absolute loss, -risk does not require assumptions about the distribution of the noise or responses. Consequently, -risk offers a general approach to assess the accuracy of the regressor across various noise distributions. Moreover, the -risk enables consistent comparisons across different models and methods, which is why it is widely used in robust regression contexts, as noted in Feng et al. (2015).

In Section 3.1, we establish calibration inequalities specifically tailored for KCRR, laying the groundwork for understanding its performance. Section 3.2 delves into the excess risk bounds of KCRR in terms of the Cauchy loss, which is crucial for assessing the robustness of the method against outliers. Following this, Section 3.3 leverages the derived generalization bounds to calculate the convergence rates of KCRR concerning the -risk, providing insights into the effectiveness of the regression approach. Lastly, Section 3.4 offers a comparative analysis of these convergence rates against those of existing methods, highlighting the advantages of KCRR within the broader context of robust regression techniques.

3.1 Calibration Inequality for KCRR

To establish the error bound of KCRR with respect to the -risk, we first introduce a theorem that links the -risk to the excess Cauchy risk. This fundamental relationship provides the basis for a more comprehensive analysis of KCRR’s performance.

Theorem 3.1.

Let Assumptions 2.3, 2.5, and 2.6 hold. Additionally, let be the scale parameter of the Cauchy loss and let denote the true regression function. For any , let be the clipped version of defined as in (6) for a parameter . Under these conditions, there exists a constant , independent of , such that for any , the following relationship holds:

| (8) |

Theorem 3.1 demonstrates that when is sufficiently large, specifically for , the convergence rate of with respect to the -risk aligns with that of the excess Cauchy risk. This equivalence implies that minimizing the Cauchy risk is effectively the same as minimizing the -risk. Consequently, this relationship helps to explain why the Cauchy loss is effective for regression in accurately learning the true regression function in the presence of heavy-tailed noise.

3.2 Generalization Bound of KCRR with respect to the Cauchy Risk

Before presenting the generalization bound of KCRR with respect to the Cauchy risk, it is essential to introduce a smoothness assumption for the true regression function. This assumption is commonly applied in the analysis of non-parametric regression problems, as seen in works such as Härdle and Marron (1985).

Assumption 3.2 (Hölder Continuity).

Assume that the regression function in the model (1) is -Hölder continuous for some . This means that there exists a constant such that holds for all .

The following theorem establishes the generalization bound for KCRR when the scale parameter of the Cauchy loss is large, specifically in the context of robust regression.

Theorem 3.3.

Let Assumptions 2.3, 2.5, 2.6, and 3.2 hold, with as the scale parameter of the Cauchy loss , and let be the true regression function. Additionally, let denote the KCRR defined by (7), where the clipping parameter satisfies . Then, there exists a constant such that for any and any , with probability at least , the following holds

| (9) |

The condition in Theorem 3.3 stems from Theorem 3.1, which indicates that the generalization bound in (9) is valid only for sufficiently large . However, from (9), it is clear that the generalization bound with respect to the Cauchy loss decreases as becomes smaller, suggesting that a smaller is more desirable. Thus, plays a critical role in improving the generalization performance while ensuring the validity of the bound. Consequently, the optimal convergence rate is achieved when . Note that in (9), the exponent , defined as , originates from the upper bound on the entropy numbers of the Gaussian kernel in Lemma 6.3, where denotes the order of continuous differentiability of the Gaussian kernel . As can be arbitrarily large for the Gaussian kernel, can be chosen arbitrarily close to zero. Similar small exponents also appear in generalization bounds of kernel methods such as Theorem 7.1 of Eberts and Steinwart (2013).

By combining Theorems 3.1 and 3.3, we can derive an upper bound on the -risk of KCRR and observe that setting yields the fastest possible convergence rate in terms of -risk. On the one hand, the convergence rate of the KCRR regressor in terms of -risk is guaranteed to match the convergence rate with respect to the Cauchy loss only when exceeds the threshold . Since the -risk is always greater than or equal to the Cauchy risk, this equivalence represents the best possible outcome, implying that increasing beyond this threshold does not yield further improvement. On the other hand, as previously discussed, choosing ensures the optimal convergence rate with respect to the Cauchy loss. Thus, by balancing these two factors, it becomes clear that is the optimal choice for achieving the best -risk error bound.

3.3 Convergence Rates of KCRR with respect to the -Risk

In this section, we derive the convergence rate of KCRR with respect to the -risk under two distinct scenarios: the practical case where the infinity norm is unknown, and the ideal case where is known to be bounded by a constant . By comparing these two settings, we provide insights into how the availability of information about impacts the convergence behavior of KCRR.

First, in practical applications, the infinity norm of the regression function is typically unknown. To ensure that the clipping parameter , we choose as a polynomial function of the sample size, i.e., , where . This guarantees that for sufficiently large , the condition is always satisfied.

The following theorem presents the convergence rates of KCRR with respect to the -risk in the realistic case where is unknown.

Theorem 3.4.

Theorem 3.4 establishes that for sufficiently large , KCRR can achieve a convergence rate of , up to an arbitrarily small order depending on and . This rate aligns with the minimax lower bound for robust regression under Cauchy noise, as demonstrated in (Zhao and Yang, 2023, Corollary 1). Hence, the convergence rate of KCRR in terms of the -risk is almost minimax-optimal, confirming its efficiency in this setting. Moreover, note that the minimax convergence rate under Gaussian noise in terms of the -risk is shown to be of the order in (Györfi et al., 2006, Theorem 3.2). Therefore, the convergence rates that KCRR achieves under the generalized Cauchy noise are almost the same as the possibly best rates under Gaussian noise, which illustrates the robustness of Cauchy loss against heavy-tailed noise.

In the following theorem, we establish the convergence rates of KCRR in terms of -risk under the ideal scenario where the infinity norm is known to be bounded by a constant . In this case, we set the clipping parameter to the constant .

Theorem 3.5.

Theorem 3.5 demonstrates that, in the ideal case, KCRR achieves the optimal convergence rate of in terms of the -norm for any , up to an arbitrarily small order related to . This result highlights the strong robustness of the Cauchy loss, as it allows KCRR to maintain near-optimal performance even under challenging noise distributions.

3.4 Comparison with Existing Convergence Rates

In this section, we compare the convergence rates proposed in our study with those established in the existing literature. In Section 3.4.1, we focus on the convergence rates derived from the application of correntropy loss (Feng et al., 2015). We evaluate these rates specifically in terms of the -norm, which is a crucial metric for measuring the mean squared distance between estimated regressors and the true regression function. In Section 3.4.2, we analyze the convergence rates associated with log-truncated absolute loss (Xu et al., 2023). This section will involve a detailed assessment of these rates in relation to traditional absolute loss metrics. Through these comparisons, we seek to provide a comprehensive overview of how our proposed convergence rates align with or differ from established methodologies, ultimately contributing to a more nuanced understanding of their applicability and performance in various regression scenarios.

3.4.1 Comparison with Rates Concerning the Correntropy Loss

In the context of robust regression, Feng et al. (2015) explore empirical risk minimization (ERM) concerning the correntropy loss defined in (3) within a general hypothesis space . Specifically, they formulate the problem as

| (11) |

Under the finite fourth-order moment assumption for the response distribution (Feng et al., 2015, Assumption 3), Theorem 4 in Feng et al. (2015) establishes the following error bounds:

| (12) |

with probability at least , where and the constant satisfies the Complexity Assumption I in Feng et al. (2015), i.e., the covering number of the function space is bounded by with the constant .

Let denote the unit ball of the RKHS . Assume that the true regression function satisfies the Hölder continuity in Assumption 3.2. According to Theorem 2, Theorem 3, and Inequality (1) in Eberts and Steinwart (2013), there exists a function with such that

| (13) |

Using the definition of from (Feng et al., 2015, Lemma 7) and Lemma 4.23 in Steinwart and Christmann (2008), we get

| (14) |

Moreover, by the inequality (6.19) in Steinwart and Christmann (2008) and since the Gaussian kernel is infinitely often differentiable, the Complexity Assumption I in Feng et al. (2015) holds for any arbitrarily small close to zero. By substituting (14) and (13) into (12), and choosing , and , we obtain

with probability at least , where is an arbitrarily small positive number related to . This result indicates that the convergence rate of is significantly slower than our convergence rate derived in (10). Introducing the clipping operation and our refined analysis of the calibration inequality in (8) may improve the convergence rates of and relax the moment assumption for the noise.

3.4.2 Comparison with Rates Concerning the Log-Truncated Loss

More recently, Xu et al. (2023) investigated regularized empirical risk minimization (RERM) with respect to the log-truncated absolute loss in (5) for with within a general hypothesis space . The optimization problem is formulated as

| (15) |

where is the regularization parameter. Under Assumption (Q.2) in Xu et al. (2023), which states that , it follows that . Utilizing the proof techniques from (Xu et al., 2023, Theorem 12), an upper bound on the excess absolute risk can be established as

| (16) |

with probability at least , where satisfies

By applying Theorem 2, Theorem 3, and Inequality (1) from Eberts and Steinwart (2013), we find that there exists a function such that

| (17) |

To encompass , we define the hypothesis space , where is a constant ensuring . Utilizing Theorem 6.27 and Lemma 6.21 from Steinwart and Christmann (2008), we can estimate the covering number as

| (18) |

Next, we substitute for the absolute loss, along with (17) and (18), into (3.4.2). By choosing

we obtain that for any ,

| (19) |

holds with probability at least .

To facilitate comparison, we will derive the convergence rate of our KCRR defined in (7) with respect to the absolute loss using Theorem 3.4. Given two random variables and , it follows that

From this, we can deduce that

Applying Theorem 3.4, we obtain that for any and ,

| (20) |

with probability at least . This rate in (20) is faster than the convergence rate presented in (19) for any , as and can be chosen to be arbitrarily small. Furthermore, our result in (20) holds under the assumption that exists for any , which requires only that . This condition is less stringent than the finite -th moment assumption of with .

More importantly, the theoretical results under (Xu et al., 2023, Assumption (Q.2)) do not hold for noise distributions that lack a finite absolute mean, such as Cauchy noise and Pareto noise. Furthermore, their error analysis cannot be applied or extended to these types of noise, as the assumption is crucial for their analysis. Specifically, to bound the difference between the risk associated with the log-truncated absolute loss and the absolute loss , the authors utilize Markov’s inequality along with (4). In (Xu et al., 2023, Lemmas 17 and 18), they demonstrate that the difference between the exponential transformations of these two losses can be bounded by terms that depend on . This expectation is finite for any only when (Xu et al., 2023, Assumption (Q.2)) is satisfied.

4 Error Analysis

In this section, we conduct an error analysis to establish the generalization error bound of KCRR, specifically in terms of -risk. One of the primary challenges in error analysis for robust regression lies in the fact that the regressor is fitted by minimizing a robust loss function. However, our goal is to derive the generalization error bound with respect to a different loss or risk criterion. In our study, we utilize the Cauchy loss to train our KCRR regressor. Nevertheless, it is essential to establish the convergence rate for KCRR based on the -risk, which serves as an important performance metric. This analysis will provide a comprehensive understanding of how well KCRR performs under this alternative criterion, contributing to our broader investigation of its effectiveness in various regression scenarios.

First, we note that the -risk of the KCRR regressor can be expressed as

| (21) |

In this expression, the first term is the ratio of the -risk to the excess Cauchy risk, which will be further explored in Section 4.1. The second term represents the excess Cauchy risk of KCRR. According to Inequality (7.39) in Steinwart and Christmann (2008), this can be decomposed into a sample error term and an approximation error term:

| (22) |

These two error terms will be analyzed in detail in Sections 4.2 and 4.3, respectively.

It is important to note that once the general relationship between -risk and the excess Cauchy risk is established, the expression in (4) effectively transforms the analysis of the -risk of KCRR into an analysis of the excess Cauchy risk of KCRR. Since KCRR is the clipped regularized empirical risk minimizer (CR-ERM) with respect to the Cauchy loss, we can directly derive an error bound for the excess Cauchy risk of KCRR within the CR-ERM framework. Moreover, by leveraging the supremum risk ratio, (4) allows us to bypass the differences between the two risks of KCRR, streamlining the analysis process.

4.1 Relationship between the Excess Cauchy Risk and -Risk

In this section, we outline the key concepts involved in studying the relationship between the excess Cauchy risk and the -risk. Specifically, we examine this relationship for a large scale parameter in Theorem 3.1.

Proof Sketch [of Theorem 3.1] Let . Then the -risk can be expressed as for . It is straightforward to establish that the -risk can be upper-bounded by

| (23) |

By elementary analysis, we can show that when , for any and ,

Then, for the Cauchy loss , we have

| (24) |

Applying the dominated convergence theorem, we can show that

Thus there exists a constant such that for any ,

| (25) |

Moreover, we have

| (26) |

Combining (4.1) with (25) and (26), we obtain that for any ,

Multiplying both sides by 2 and rearranging terms gives

| (27) |

Therefore, by (23), if , then we have

| (28) |

Combining (4.1) and (27), we find

From this inequality, we can rearrange terms to obtain

| (29) |

This completes the proof sketch of the assertion in Theorem 3.1.

4.2 Bounding the Sample Error

In this section, we derive an upper bound for the sample error given by

which arises from both the randomness of the data and the complexity of the function space . One significant analytical challenge in bounding this sample error is related to the unbounded response, which may not even possess a finite absolute mean under Assumption 2.3.

The following lemma establishes the Lipschitz property of the Cauchy loss function, which is an important characteristic for assessing the stability and continuity of this loss with respect to changes in its inputs.

Lemma 4.1 (Lipschitz Property).

Let denote the Cauchy loss function with as the scale parameter. Then, for any two functions and and any response , we have

This property indicates that the difference in the Cauchy loss between the predictions and is bounded by the product of the scale parameter and the absolute difference between the outputs of the two functions. The Lipschitz property is particularly beneficial in the context of convergence analysis, as it guarantees that small changes in model predictions lead to proportionately small changes in the loss.

By applying Lemma 4.1 to the functions and , we can derive an upper bound for the excess Cauchy loss. According to the Lipschitz property established in Lemma 4.1, the excess Cauchy loss can be expressed as

Given that the supremum norm between the estimated function and the optimal function satisfies , we can substitute this supremum norm constraint into the inequality to obtain

This result demonstrates that the excess Cauchy loss can be effectively bounded by , even in scenarios where the response variable is unbounded.

Based on the variance bound definition presented in (Steinwart and Christmann, 2008, (7.36)), we derive the variance bound for the Cauchy loss by combining its Lipschitz property with the calibration inequality established in Theorem 3.1, as stated in the following lemma.

Lemma 4.2 (Variance Bound).

Let Assumptions 2.3, 2.5, and 2.6 hold. Let denote the Cauchy loss function with as the scale parameter and as the true regression function. Furthermore, let be a function and be the clipped version of , defined as in (6), with the clipping parameter satisfying . Then, there exists a constant such that for any , the following holds

This lemma establishes a quantitative relationship between the expected squared difference in Cauchy loss and the excess Cauchy risk. The significance of this variance bound lies in its ability to control the variance of excess Cauchy loss using its mean, even if has an infinite absolute mean. This result not only highlights the importance of clipping to mitigate the effects of unbounded responses but also plays a crucial role in establishing generalization guarantees for KCRR with respect to the Cauchy loss.

Lemma 4.2 shows that the Cauchy loss satisfies the variance bound defined by

where the excess loss , with and . The exponent lies in the range , and corresponds to Bernstein’s condition (Van Erven et al., 2015) and represents the optimal exponent for this variance bound. Consequently, Lemma 4.2 ensures low variance whenever the Cauchy risk is minimized. This implies that decreasing the risk directly controlls the variance of the excess loss.

The calibration result in (8) (Theorem 3.1) is pivotal in achieving the variance bound with the optimal exponent . This insight can guide a general analysis framework for establishing variance bounds for other robust loss functions.

Overall, this variance bound shows that small excess risks lead to well-controlled excess loss variance, strengthening the theoretical foundation of KCRR. Moreover, it also lays the groundwork for a robust oracle inequality, highlighting its predictive reliability in practical applications.

Proposition 4.3 (Oracle Inequality).

Let Assumptions 2.3, 2.5, and 2.6 hold. Let denote the Cauchy loss function with as the scale parameter and as the true regression function. Furthermore, let be the KCRR defined in (7) with the clipping parameter . Then there exists a constant such that for any , , , and , the following inequality holds with probability at least ,

| (30) | ||||

where is a constant only depending on and the data dimension .

This result establishes a key relationship between the regularized excess risk, the approximation error, and the sample error bound. It demonstrates how the choice of parameters affects the performance of KCRR, offering a theoretical guarantee for its generalization ability with respect to the Cauchy loss. In the next section, we will provide an upper bound for the approximation error term , where is to be chosen, as outlined in (30).

4.3 Bounding the Approximation Error

In this section, we derive an upper bound for the approximation error term

in the context of (30). This bound provides valuable insights into the KCRR model’s ability to approximate the true regression function, emphasizing the relationship between model complexity, the risk of a selected function , and the optimal risk .

Proposition 4.4.

This upper bound is critical as it underscores how well the function space can approximate the true regression function. It captures the balance between the regularization term and the excess risk of relative to the optimal risk . The bandwidth plays a key role in determining this bound, as a smaller of the approximation function can reduce excess risks but impose a higher penalty. This result clarifies the factors influencing the approximation errors of our method.

5 Experiments

To evaluate the effectiveness of KCRR, we conduct a series of experiments using an iterative algorithm to solve KCRR and compare its performance against three well-established methods: kernel least absolute deviation (KLAD) (Wang et al., 2014), kernel-based Huber regression (KBHR) (Wang et al., 2022), and the maximum correntropy criterion for regression (MCCR) (Feng et al., 2015). Each of these models can be formulated as

where represents the reproducing kernel Hilbert space (RKHS), and is the specific loss function used in each method: absolute loss for KLAD, Huber loss for KBHR, and correntropy loss for MCCR. This framework enables a consistent comparison of model performance across different loss functions.

5.1 Solving KCRR

In this section, we present an empirical approach to solving the KCRR problem defined in (7). According to the representer theorem, the solution to KCRR lies within the span of the kernel functions, which can be expressed as

where are the coefficients and is the intercept term.

To solve the KCRR problem, our objective is to determine the coefficients and intercept that minimize the following objective function:

| (31) |

where the first term is the loss function applied to the predictions, and the second term is a regularization term scaled by , which controls the complexity of the solution. This formulation provides a balance between fitting the data and maintaining model simplicity.

To solve (31), we use the iterated reweighted least squares (IRLS) method. This method iteratively minimizes a weighted least-squares problem, defined as

| (32) |

where are the weights from the previous iteration.

After each minimization step, the weights are updated as follows:

| (33) |

Here, represents the ratio of the Cauchy loss to the squared loss, adjusting the weighting of residuals based on the updated estimates. This iterative process allows the model to handle outliers more robustly by dynamically reweighting each data point.

We begin by initializing the weights as . In each iteration, we first derive the explicit solution of (32) for and . Following this, we update the weights based on the current solution using (33). This iterative process continues until convergence.

Given that the KCRR model is non-convex, applying the IRLS method to solve (31) guarantees convergence only to a stationary point Aftab and Hartley (2015). Nevertheless, the IRLS method is known for its efficiency and stability in reaching stationary points, making it a practical and effective approach in non-convex settings. Empirical evidence also suggests that IRLS performs well for similar non-convex optimization problems, indicating that a stationary point solution is likely to meet the accuracy requirements of the KCRR model. Therefore, in light of its practical effectiveness and empirical validation, a stationary point solution adequately serves our objectives.

5.2 Synthetic Experiments

In this section, we present simulation experiments on robust regression to demonstrate the effectiveness of KCRR in managing heavy-tailed noise.

To evaluate our approach, we use Friedman’s benchmark functions (Friedman, 1991) as the regression function . These functions are commonly applied in studies of robust regression, as seen in works like Feng et al. (2015). Below, we describe three of Friedman’s benchmark functions, which we use as the regression function :

-

, where ;

-

, where ;

-

, where .

For regression function , each coordinate , , is independently drawn from a uniform distribution on the interval . For regression functions and , each coordinate , , is independently drawn from distinct uniform distributions over the following intervals: , , , and .

We consider three different noise distributions, , as follows:

-

For Gaussian noise , the location parameter is set to zero. The scale parameter is adjusted so that the noise’s standard deviation is one-third of that of , in line with Tipping (2001). Specifically, this means .

-

For Cauchy noise , as in Example 2.1, the scale parameter is selected to achieve a signal-to-noise power ratio of . Thus, we choose so that .

-

For Pareto noise , as in Example 2.2, the shape parameter is set to . The scale parameter is determined based on a signal-to-noise ratio of , specifically by choosing such that .

To generate the response variable, noise was added to the regression function, resulting in . For each of Friedman’s functions, we produced noisy observations using the three different noise types described above, which were used for model training and cross-validation. Furthermore, an additional noise-free observations were generated for testing.

For KLAD, MCCR, and KCRR, the hyperparameter grids for the regularization parameter and the bandwidth are set to and , respectively. The grid for the squared scale parameter in the Cauchy and correntropy losses is selected as . These three models are fit on the standardized data. For KBHR, the hyperparameter grid for the scale parameter in the Huber loss, defined as , is set to . Prior to fitting KBHR, we standardize the feature variables.

To fit KLAD and KBHR, we employ stochastic gradient descent as implemented in the Sklearn package. For MCCR, we use IRLS as recommended by Feng et al. (2015).

The hyperparameters for all these algorithms are selected using 10-fold cross-validation, with the mean absolute error (MAE) as the selection criterion. The MAE is defined as

where represent the cross-validation samples.

To evaluate the performance of these algorithms on the test data, we use two metrics: the MAE defined as and the relative sum of squared error (RSSE) defined as

where are the test samples and is the mean of the values for . We conduct our experiments ten times and report the average values and standard errors for both metrics in Tables 1 and 2, respectively.

| Dataset | Noise | KLAD | KBHR | MCCR | KCRR |

|---|---|---|---|---|---|

| 1.4241 ± 0.0155 | 1.0441 ± 0.0096 | 0.7424 ± 0.0197 | 0.6122 ± 0.0182 | ||

| 1.4055 ± 0.0481 | 1.3600 ± 0.0340 | 0.9464 ± 0.0251 | 0.9026 ± 0.0188 | ||

| 1.2748 ± 0.0957 | 1.8464 ± 0.2287 | 0.5498 ± 0.0491 | 0.3821 ± 0.0312 | ||

| 54.0076 ± 1.1573 | 26.7090 ± 0.5068 | 24.1177 ± 0.7749 | 22.3529 ± 0.7565 | ||

| 39.8103 ± 2.2581 | 34.5415 ± 1.1040 | 18.6588 ± 0.6364 | 19.4297 ± 1.3433 | ||

| 37.1561 ± 2.4826 | 70.4954 ± 16.2335 | 9.1603 ± 1.0183 | 6.7785 ± 1.4664 | ||

| 0.0945 ± 0.0023 | 0.1181 ± 0.0028 | 0.0606 ± 0.0009 | 0.0463 ± 0.0007 | ||

| 0.1159 ± 0.0032 | 0.1336 ± 0.0050 | 0.1005 ± 0.0028 | 0.0902 ± 0.0031 | ||

| 0.1207 ± 0.0099 | 0.1725 ± 0.0059 | 0.0547 ± 0.0017 | 0.0425 ± 0.0012 |

-

*

For each dataset and each noise, we denote the best performance with bold.

| Dataset | Noise | KLAD | KBHR | MCCR | KCRR |

|---|---|---|---|---|---|

| 0.1619 ± 0.0041 | 0.0841 ± 0.0019 | 0.0406 ± 0.0021 | 0.0275 ± 0.0018 | ||

| 0.1464 ± 0.0101 | 0.1330 ± 0.0069 | 0.0659 ± 0.0035 | 0.0603 ± 0.0020 | ||

| 0.1308 ± 0.0208 | 0.2665 ± 0.0622 | 0.0235 ± 0.0048 | 0.0141 ± 0.0023 | ||

| 0.0465 ± 0.0017 | 0.0094 ± 0.0001 | 0.0068 ± 0.0005 | 0.0057 ± 0.0004 | ||

| 0.0227 ± 0.0028 | 0.0153 ± 0.0011 | 0.0041 ± 0.0002 | 0.0046 ± 0.0006 | ||

| 0.0199 ± 0.0045 | 0.0952 ± 0.0387 | 0.0012 ± 0.0003 | 0.0011 ± 0.0007 | ||

| 0.3334 ± 0.0078 | 0.3940 ± 0.0046 | 0.0994 ± 0.0060 | 0.0653 ± 0.0045 | ||

| 0.4060 ± 0.0130 | 0.4973 ± 0.0164 | 0.2263 ± 0.0148 | 0.1735 ± 0.0121 | ||

| 0.3236 ± 0.0399 | 0.7692 ± 0.0603 | 0.0929 ± 0.0072 | 0.0792 ± 0.0075 |

-

*

For each dataset and each noise, we denote the best performance with bold.

Tables 1 and 2 show that KCRR consistently outperforms KLAD, KBHR, and MCCR across Friedman’s functions, under various types of noise. Notably, KCRR demonstrates a significant advantage in scenarios with Pareto noise (case ), which lacks a finite -order moment. This result highlights that the Cauchy loss function offers greater robustness against extremely heavy-tailed noise compared to the other loss functions.

5.3 Real-world Data Experiments

| Dataset | ||

|---|---|---|

| Computer | ||

| Housing | ||

| Yacht |

We evaluate the performance of our models using four real-world regression datasets from the UCI Machine Learning Repository (Kelly et al., 2007): Computer Hardware, Facebook Metrics, Boston Housing, and Yacht Hydrodynamics. The details of these datasets, including the sample size and the number of features , are provided in Table 3.

For all the robust methods, the bandwidth parameter in the kernel function is chosen from the grid , and the squared scale parameter in the Cauchy loss and correntropy loss is selected from . The remaining parameter grids are kept the same as in the synthetic experiments. Each dataset is randomly split into for training and for testing. The experiments are repeated ten times, with parameters selected using -fold cross-validation based on the MAE criterion.

| Dataset | KLAD | KBHR | MCCR | KCRR |

|---|---|---|---|---|

| Computer | 44.4389 ± 4.5196 | 36.1817 ± 2.8616 | 30.3279 ± 2.7860 | 28.3316 ± 2.1660 |

| 79.2629 ± 6.7764 | 51.3577 ± 4.2343 | 13.5840 ± 2.0781 | 11.5963 ± 2.0316 | |

| Housing | 3.1702 ± 0.0796 | 2.5449 ± 0.0687 | 2.1804 ± 0.0411 | 2.0714 ± 0.0422 |

| Yacht | 6.3457 ± 0.4402 | 5.2080 ± 0.2433 | 1.0794 ± 0.0650 | 0.3984 ± 0.0315 |

-

*

For each dataset, we denote the best performance with bold.

| Dataset | KLAD | KBHR | MCCR | KCRR |

|---|---|---|---|---|

| Computer | 0.4924 ± 0.0545 | 0.2676 ± 0.0304 | 0.2635 ± 0.0898 | 0.1546 ± 0.0268 |

| 0.5594 ± 0.0370 | 0.1620 ± 0.0270 | 0.0643 ± 0.0225 | 0.0614 ± 0.0230 | |

| Housing | 0.3318 ± 0.0132 | 0.1948 ± 0.0144 | 0.1443 ± 0.0107 | 0.1201 ± 0.0058 |

| Yacht | 0.6305 ± 0.0329 | 0.2585 ± 0.0132 | 0.0119 ± 0.0018 | 0.0026 ± 0.0007 |

-

*

For each dataset, we denote the best performance with bold.

Tables 4 and 5 show that KCRR consistently outperforms other kernel-based robust regression methods on real-world datasets, as measured by both the MAE and RSSE metrics. These results underscore the effectiveness and adaptability of the Cauchy loss in managing various types of noise commonly found in real-world data.

6 Proofs

In this section, we present the proofs for the results in previous sections. Specifically, Section 6.1 demonstrates the finiteness of the Cauchy risk and establishes the corresponding Bayes function under the generalized Cauchy noise assumption. Section 6.2 provides detailed proofs for the main theoretical results outlined in Section 3. Lastly, Section 6.3 covers the proof related to the error analysis for the -risk of KCRR in Section 4.

6.1 Proofs Related to Section 2

of Lemma 2.4.

For any , we have . First, we prove that for any and . To this end, we construct the function for any . The derivative function of is given by , which is larger than zero for . Therefore, the function is increasing on . Now we show , which is equivalent to . Since for , we have and thus we get

where the last inequality follows from . Therefore, we get and thus is increasing on . In addition, we check that . Specifically, we have

Since and for any , we have

Therefore, we get and thus for any . Thus, we finish the proof of for any and .

In the following, we show that for any and . Under , we have and thus it suffices to show that for . To this end, we construct the function on . The derivative function of is given by , which is larger than zero for any . Therefore, is increasing on . Moreover, . Therefore for any .

By combining these two sides, we get for any and . Then we have

Therefore if , we get . ∎

of Lemma 2.7.

Using the definition of the Cauchy loss and the inequalities , we get

| (34) |

If , then we have

| (35) |

where the last inequality follows from Assumption 2.3.

of Lemma 2.8.

By the definition of , for any function , we have

Let the inner risk of the Cauchy loss be denoted as

| (36) |

Let us define a function of as

| (37) |

By taking the derivative of with respect to , we obtain

By Assumption 2.6, for any and any , we have

This implies that for any . Conversely, we can prove that for any . Moreover, it is clear that when by using Assumption 2.5. As a result, we can conclude that the inner risk behaves in the following manner:

| (38) |

Therefore, for any , there holds and is the unique minimal point of . Thus, for any and any , there holds . By the definition of , we have and . Therefore, and the equation holds if and only if . This leads to the result that the minimal inner risk is achieved when , i.e.,

By taking the expectation with respect to , we extend this result to the overall risk, yielding that

This demonstrates that the true regression function minimizes the Cauchy risk and completes the proof. ∎

of Lemma 2.9.

Since , we can analyze the relationship between and based on the value of .

- Case 1:

- Case 2:

Combining both cases, we conclude that holds for any . By taking the expectation with respect to , we extend this result to the overall risk, which establishes the desired assertion. ∎

6.2 Proofs Related to Section 3

6.2.1 Proofs Related to Section 3.1

Lemma 6.1.

of Lemma 6.1.

By Lemma 2.8, we have

| (39) |

For the Cauchy loss function, we have

Using the inequality for and substituting the regression model into the expression, we get

According to the symmetry assumption stated in Assumption 2.5, for any , we have . From this, we get

This together with (39) yields the assertion. ∎

of Theorem 3.1.

By the definition of the Cauchy loss and , we have

Let us define . Since , we have

Obviously, we have . Thus if , then

Since , we then have

Otherwise if , using the inequality , we get

Consequently, we obtain that when , for any and ,

Using the inequality for , and the symmetry assumption stated in Assumption 2.5, we get

| (40) |

Since and are bounded, by using the dominated convergence theorem, we have

Therefore, there exists a large number such that for any ,

| (41) |

Combining (41) with (6.2.1) and using , we obtain

This is equivalent to

| (42) |

Given that and , we can conclude that

Since , we have

| (43) |

Combining (6.2.1) with (42), we find

which is equivalent to

This together with Lemma 6.1 yields the assertion. ∎

6.2.2 Proofs Related to Section 3.2

6.2.3 Proofs Related to Section 3.3

of Theorem 3.4.

6.3 Proofs Related to Section 4

6.3.1 Proofs Related to Section 4.2

Before proceeding, we need to introduce the concept of entropy numbers (van der Vaart and Wellner, 1997), which serves as a measure of the capacity of a function set.

Definition 6.2 (Entropy Numbers).

Let be a metric space, and let with being an integer. The -th entropy number of is defined as

where denotes the closed ball of radius centered at .

The following lemma, derived from (Steinwart and Christmann, 2008, Theorem 6.26), provides an upper bound for the entropy number of Gaussian kernels.

Lemma 6.3.

Let the compact set and let be a distribution defined on , with representing the support of . Additionally, for , let denote the reproducing kernel Hilbert space (RKHS) associated with the Gaussian radial basis function (RBF) kernel over the set . Then, for every , there exists a constant such that

of Lemma 6.3.

Consider the following commutative diagram:

In this diagram, the extension operator , as defined in Corollary 4.43 of Steinwart and Christmann (2008), is an isometric isomorphism. This implies that

| (44) |

Let denote the space of all bounded functions on the set . For any , we have

This implies

| (45) |

Before proceeding, we need to introduce some notations. Specifically, we define the composition and introduce the function

| (46) |

Let denote the reproducing kernel Hilbert space (RKHS), and let . We define the function space

| (47) |

and

| (48) |

Additionally, we need to introduce a concept for measuring the capacity of a function set. This is defined as an expectation of the supremum with respect to the Rademacher sequence, see e.g., Definition 7.9 of Steinwart and Christmann (2008).

Definition 6.4 (Empirical Rademacher Average).

Let be a set of functions . Let be a Rademacher sequence associated with a distribution . This sequence consists of independent and identically distributed (i.i.d.) random variables, where . Then for a dataset , the -th empirical Rademacher average of the function set with respect to is defined as

To derive the bound of the empirical Rademacher average of , we first need to investigate the Lipschitz property of the Cauchy loss function. This involves establishing a supremum bound on the difference between the Cauchy loss values associated with two different regressors.

of Lemma 4.1.

Let us define the function

Taking the derivative of with respect to , we get

since it holds that . By applying the Mean Value Theorem, we can find some value between and such that

This leads to

yielding the desired assertion. ∎

of Lemma 4.2.

Lemma 6.5.

Let the function space be defined as in (48). For any and , there exists a constant that depends only on , , and such that for any , we have

where

and is a constant that depends on and .

of Lemma 6.5.

By applying Lemma 6.3 and setting , we obtain

| (49) |

To avoid confusion, we denote the constant that depends on and simply as for convenience. For any , we have

From this, we deduce that

which yields that

where the unit ball . By applying (A.36) from Steinwart and Christmann (2008) along with (49), we obtain

Let be an -net of with respect to . For any , there exists some index such that

By applying Lemma 4.1, we get

Consequently, we obtain

As a result, the set constitutes a -net of with respect to . This leads us to

Additionally, for any function , we have

Applying Lemma 4.1, we get

| (50) |

Furthermore, by Lemma 4.2, if , then for any , we have

Using Theorem 7.16 in Steinwart and Christmann (2008), we get

where . This finishes the proof. ∎

Before proving the oracle inequality in Proposition 4.3, we need to introduce two widely-used concentration inequalities. Specifically, Bernstein’s inequality is shown in (Steinwart and Christmann, 2008, Theorem 5.12) and Talagrand’s inequality is proven by Theorem 7.5 and Lemma 7.6 in Steinwart and Christmann (2008).

Lemma 6.6 (Bernstein’s Inequality).

Let be independent random variables on a probability space such that , , and for all . Then for any , we have

with probability at least .

Let us define

| (51) |

Lemma 6.7 (Talagrand’s Inequality).

For a given , let be as in (51) and define . For any such that , we assume and . For , we define the function by

Then, for any , we have

with probability at least .

of Proposition 4.3.

We begin by bounding the term . For , define random variables

It is clear that . By applying (50) and Lemma 4.2, we find that if , then . Additionally, we have . By applying Bernstein’s inequality from Lemma 6.6 to random variables , and utilizing the inequality , we obtain

| (54) |

with probability at least .

Then we bound the term . To this end, let us define

where . Symmetrization in Proposition 7.10 of Steinwart and Christmann (2008) and Lemma 6.5 yield

where is defined as in Lemma 6.5. Simple calculation shows that . Additionally, note that is a separable Caratheodory set according to Lemma 7.6 in Steinwart and Christmann (2008). Applying Peeling in Theorem 7.7 of Steinwart and Christmann (2008) to hence gives

By (50), we have

Using and Lemma 4.2, we get

By applying Talagrand’s inequality as stated in Lemma 6.7, we can conclude that for any ,

holds with probability at least . Based on the definition of , we have

| (55) |

with probability at least .

Combining (6.3.1) with (6.3.1) and (54), we obtain

| (56) |

with probability at least . To bound the terms in (6.3.1), we note that since , if , then it follows that . This implies that

Furthermore, if we set , we can derive the following inequalities:

These estimates allow us to conclude that we obtain

| (57) |

with probability at least . Elementary calculation yields that

holds with probability at least . Let us define

With this definition, we obtain

with probability at least . The last inequality holds under the condition that . This concludes the proof. ∎

6.3.2 Proofs Related to Section 4.3

of Proposition 4.4.

For a fixed parameter , we define the function by

| (58) |

For any , the convolution of and at is

Since the function has compact support and is bounded, it follows that . Combining this fact with Proposition 4.46 in Steinwart and Christmann (2008), we obtain

| (59) |

Moreover, since

we have

Then for any , we have

| (60) |

Using the rotation invariance of and the property for , we obtain

| (61) |

Let . By Proposition 4.46 in Steinwart and Christmann (2008), we have

| (62) |

where . Combining (6.3.2) and (6.3.2), we obtain

with . This together with Lemma 6.1 gives

where the constant . Furthermore, this conclusion, in conjunction with Lemma 2.9, yields the desired assertion. ∎

7 Conclusion

In this paper, we tackle the challenge of robust regression in situations where traditional noise assumptions, such as the existence of a finite absolute mean, are not applicable. We introduce a generalized Cauchy noise assumption that accommodates noise distributions with finite moments of any order, including heavy-tailed cases like Cauchy noise, which lacks a finite absolute mean. Through an analysis of the kernel Cauchy ridge regressor (KCRR), we establish a relationship between excess Cauchy risk and -risk, demonstrating that these risks become equivalent when the scale parameter of the Cauchy loss is large. Building on this foundation, we show that the excess Cauchy risk bound of KCRR improves as the scale parameter decreases, particularly under the assumption of Hölder smoothness. Moreover, we derive the almost minimax-optimal convergence rate for KCRR by effectively selecting a proper scale parameter of the Cauchy loss. This illustrates the robustness of the Cauchy loss in addressing various noise types. Our findings underscore the potential of KCRR as a reliable method for regression tasks in challenging noise environments.

Acknowledge

Annika Betken gratefully acknowledges financial support from the Dutch Research Council (NWO) through VENI grant 212.164.

References

- Aftab and Hartley (2015) Khurrum Aftab and Richard Hartley. Convergence of iteratively re-weighted least squares to robust m-estimators. In 2015 IEEE Winter Conference on Applications of Computer Vision, pages 480–487. IEEE, 2015.

- Agrusa et al. (2022) Anjulie S Agrusa, David C Kunkel, and Todd P Coleman. Robust regression and optimal transport methods to predict gastrointestinal disease etiology from high resolution egg and symptom severity. IEEE Transactions on Biomedical Engineering, 69(11):3313–3325, 2022.

- Black and Anandan (1996) Michael J Black and Paul Anandan. The robust estimation of multiple motions: Parametric and piecewise-smooth flow fields. Computer Vision and Image Understanding, 63(1):75–104, 1996.

- Brownlees et al. (2015) Christian Brownlees, Emilien Joly, and Gábor Lugosi. Empirical risk minimization for heavy-tailed losses. The Annals of Statistics, 43(6):2507–2536, 2015.

- Catoni (2012) Olivier Catoni. Challenging the empirical mean and empirical variance: a deviation study. In Annales de l’IHP Probabilités et statistiques, volume 48, pages 1148–1185, 2012.

- Chen et al. (2021) Peng Chen, Xinghu Jin, Xiang Li, and Lihu Xu. A generalized Catoni’s M-estimator under finite -th moment assumption with . Electronic Journal of Statistics, 15(2):5523–5544, 2021.

- D’Orsi et al. (2021) Tommaso D’Orsi, Gleb Novikov, and David Steurer. Consistent regression when oblivious outliers overwhelm. In Marina Meila and Tong Zhang, editors, Proceedings of the 38th International Conference on Machine Learning, volume 139 of Proceedings of Machine Learning Research, pages 2297–2306. PMLR, 18–24 Jul 2021.

- Eberts and Steinwart (2013) Mona Eberts and Ingo Steinwart. Optimal regression rates for SVMs using Gaussian kernels. Electronic Journal of Statistics, 7:1–42, 2013.

- Feng et al. (2015) Yunlong Feng, Xiaolin Huang, Lei Shi, Yuning Yang, and Johan AK Suykens. Learning with the maximum correntropy criterion induced losses for regression. The Journal of Machine Learning Research, 16(30):993–1034, 2015.

- Friedman (1991) Jerome H Friedman. Multivariate adaptive regression splines. The Annals of Statistics, 19(1):1–67, 1991.

- Fu et al. (2010) Tianhui Fu, Suihua Zhou, and Liqun Wang. Research on ELF atmospheric noise suppression method. In The Third International Conference on Computer Science and Information Technology, volume 5, pages 542–546. IEEE, 2010.

- Gülgün and Larsson (2024) Ziya Gülgün and Erik G. Larsson. Massive MIMO with Cauchy noise: Channel estimation, achievable rate and data decoding. IEEE Transactions on Wireless Communications, 23(3):1929–1942, 2024.

- Györfi et al. (2006) László Györfi, Michael Kohler, Adam Krzyzak, and Harro Walk. A Distribution-free Theory of Nonparametric Regression. Springer Science & Business Media, 2006.

- Härdle and Marron (1985) Wolfgang Härdle and James Stephen Marron. Optimal bandwidth selection in nonparametric regression function estimation. The Annals of Statistics, 13(4):1465–1481, 1985.

- Huber (1992) Peter J Huber. Robust estimation of a location parameter. In Breakthroughs in Statistics: Methodology and Distribution, pages 492–518. Springer, 1992.

- Idan and Speyer (2010) Moshe Idan and Jason L Speyer. Cauchy estimation for linear scalar systems. IEEE Transactions on Automatic Control, 55(6):1329–1342, 2010.

- Karakuş et al. (2022) Oktay Karakuş, Ercan E Kuruoğlu, Alin Achim, and Mustafa A Altınkaya. Cauchy-Rician model for backscattering in urban SAR images. IEEE Geoscience and Remote Sensing Letters, 19:1–5, 2022.

- Kelly et al. (2007) Markelle Kelly, Rachel Longjohn, and Kolby Nottingham. UCI machine learning repository, 2007. https://archive.ics.uci.edu.

- Khan et al. (2021) Dost Muhammad Khan, Anum Yaqoob, Seema Zubair, Muhammad Azam Khan, Zubair Ahmad, and Osama Abdulaziz Alamri. Applications of robust regression techniques: an econometric approach. Mathematical Problems in Engineering, 2021:1–9, 2021.

- Lam and Cheng (2021) Clifford Lam and Wenyu Cheng. Robust mean and eigenvalues regularized covariance matrix estimation. London School of Economics and Political Science, 2021.

- Laus et al. (2018) Friederike Laus, Fabien Pierre, and Gabriele Steidl. Nonlocal myriad filters for cauchy noise removal. Journal of Mathematical Imaging and Vision, 60:1324–1354, 2018.

- Lee et al. (2020) Kyungjae Lee, Hongjun Yang, Sungbin Lim, and Songhwai Oh. Optimal algorithms for stochastic multi-armed bandits with heavy tailed rewards. In H. Larochelle, M. Ranzato, R. Hadsell, M.F. Balcan, and H. Lin, editors, Advances in Neural Information Processing Systems, volume 33, pages 8452–8462. Curran Associates, Inc., 2020.

- Ljajko et al. (2023) Eugen Ljajko, Vladica Stojanović, Marina Tošić, and Ivan Božović. Cauchy split-break process: Asymptotic properties and application in securities market analysis. UPB Scientific Bulletin, Series A: Applied Mathematics and Physics, 85:139–154, 2023.

- Mlotshwa et al. (2022) Thamsanqa Mlotshwa, Heinrich van Deventer, and Anna Sergeevna Bosman. Cauchy loss function: Robustness under Gaussian and Cauchy noise. In Southern African Conference for Artificial Intelligence Research, pages 123–138. Springer, 2022.

- Pervez and Ali (2022) Asif Pervez and Irfan Ali. Robust regression analysis in analyzing financial performance of public sector banks: a case study of India. Annals of Data Science, pages 1–15, 2022.

- Pirtea et al. (2021) Marilen Gabriel Pirtea, Graţiela Georgiana Noja, Mirela Cristea, and Mirela Panait. Interplay between environmental, social and governance coordinates and the financial performance of agricultural companies. Agricultural Economics/Zemědělská Ekonomika, 67(12), 2021.

- Santamar´ıa et al. (2006) Ignacio Santamaría, Puskal P Pokharel, and José Carlos Principe. Generalized correlation function: definition, properties, and application to blind equalization. IEEE Transactions on Signal Processing, 54(6):2187–2197, 2006.

- Shen et al. (2021a) Guohao Shen, Yuling Jiao, Yuanyuan Lin, Joel L Horowitz, and Jian Huang. Deep quantile regression: Mitigating the curse of dimensionality through composition. arXiv preprint arXiv:2107.04907, 2021a.

- Shen et al. (2021b) Guohao Shen, Yuling Jiao, Yuanyuan Lin, and Jian Huang. Robust nonparametric regression with deep neural networks. arXiv preprint arXiv:2107.10343, 2021b.

- Shi et al. (2020) Kehan Shi, Gang Dong, and Zhichang Guo. Cauchy noise removal by nonlinear diffusion equations. Computers & Mathematics with Applications, 80(9):2090–2103, 2020.

- Steinwart and Christmann (2008) Ingo Steinwart and Andreas Christmann. Support Vector Machines. Springer Science & Business Media, 2008.

- Steinwart et al. (2006) Ingo Steinwart, Don Hush, and Clint Scovel. An oracle inequality for clipped regularized risk minimizers. In B. Schölkopf, J. Platt, and T. Hoffman, editors, Advances in Neural Information Processing Systems, volume 19, pages 1321–1328. MIT Press, 2006.

- Tipping (2001) Michael E Tipping. Sparse Bayesian learning and the relevance vector machine. The Journal of Machine Learning Research, 1(Jun):211–244, 2001.

- Tsakonas et al. (2014) Efthymios Tsakonas, Joakim Jaldén, Nicholas D. Sidiropoulos, and Björn Ottersten. Convergence of the Huber regression M-estimate in the presence of dense outliers. IEEE Signal Processing Letters, 21(10):1211–1214, 2014.

- van der Vaart and Wellner (1997) AW van der Vaart and Jon A Wellner. Weak convergence and empirical processes with applications to statistics. Journal of the Royal Statistical Society Series A (Statistics in Society), 160(3):596–608, 1997.

- Van Erven et al. (2015) Tim Van Erven, Peter D Grünwald, Nishant A Mehta, Mark D Reid, and Robert C Williamson. Fast rates in statistical and online learning. The Journal of Machine Learning Research, 16(1):1793–1861, 2015.

- Wang et al. (2014) Kuaini Wang, Jingjing Zhang, Yanyan Chen, and Ping Zhong. Least absolute deviation support vector regression. Mathematical Problems in Engineering, 2014(1):169575, 2014.

- Wang et al. (2022) Yue Wang, Baobin Wang, Chaoquan Peng, Xuefeng Li, and Hong Yin. Huber regression analysis with a semi-supervised method. Mathematics, 10(20):3734, 2022.

- Xu et al. (2023) Lihu Xu, Fang Yao, Qiuran Yao, and Huiming Zhang. Non-asymptotic guarantees for robust statistical learning under infinite variance assumption. The Journal of Machine Learning Research, 24(92):1–46, 2023.

- Xu et al. (2020) Yi Xu, Shenghuo Zhu, Sen Yang, Chi Zhang, Rong Jin, and Tianbao Yang. Learning with non-convex truncated losses by SGD. In Ryan P. Adams and Vibhav Gogate, editors, Proceedings of The 35th Uncertainty in Artificial Intelligence Conference, volume 115 of Proceedings of Machine Learning Research, pages 701–711. PMLR, 22–25 Jul 2020.

- Zhang et al. (2021) Jiachi Zhang, Liu Liu, Kai Wang, Yuanyuan Fan, and Jiahui Qiu. Measurements and statistical analyses of electromagnetic noise for industrial wireless communications. International Journal of Intelligent Systems, 36(3):1304–1330, 2021.

- Zhang and Zhou (2018) Lijun Zhang and Zhi-Hua Zhou. -regression with heavy-tailed distributions. In S. Bengio, H. Wallach, H. Larochelle, K. Grauman, N. Cesa-Bianchi, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 31, pages 1084–1094. Curran Associates, Inc., 2018.

- Zhao and Yang (2023) Bingxin Zhao and Yuhong Yang. Minimax rates of convergence for nonparametric location-scale models. arXiv preprint arXiv:2307.01399, 2023.